TRADE IDEA: ARRY COVERED CALLMetrics:

Buy 100 Shares at 3.23

Sell Oct 21st 4 call

2.83 db at the mid (i.e., 2.83 is your cost basis in the shares)

Max Profit: $117 (if called away at 4)

ROC: 41% ROC

Notes: A good spot to initiate this here, given a bit of horizontal support.

Optionsstrategy

SOLD TEVA SEPT 16TH 47.5 PUTSelling the 47.5 put naked here below support as a potential precursor to a covered call, which I got filled for a .73 ($73)/contract credit.

Basically, my thought process here is that I might want to covered call TEVA, but don't want to buy shares here at 53 (lower is better). I'll naturally watch price and roll the short put down and out for a credit should it appear that it's going to totally implode such that I could get the shares even cheaper. Otherwise, I'll just keep the credit collected for the short put here and/or cover in profit it if something better comes along.

BUYING POWER EFFICIENCY: "POOR MAN'S" VS. TRAD COVERED CALLSThere is more than one way to skin a cat. But some ways are more buying power efficient than others ... .

Here, I'm looking at a covered call in X. The implied volatility is >50%, so I can get a bit of premium on the call side to reduce my cost basis in any stock I buy here. For example, if I buy shares at 20.38, and sell the Sept 30th 20.5 call against (for a 1.50 ($150) credit at the mid), I can get into the whole package for a 19.03 debit ($1903), my cost basis in the shares will be $19.03 per share, and my max profit is $147 if called away at 23. However, for some, that $1903 stick price can be hefty, especially if they're working with a smaller account. The drawback is that I'm (a) stuck with stock I bought at 20.38 per share; and (b) the buying power effect may be larger than I'd like.

In comparison, I can also do a PWCC or poor man's covered call. Traditionally, this is set up using a long-dated, deep ITM long call option to stand in for the stock and -- like the covered call -- a call sold 30-45 DTE. Most of the time, I set these up using the 70 delta strike for the long option and the 30 delta strike for the short. As with the traditional covered call, I'm looking to reduce my cost basis in my "synthetic stock" (here, the long option) by selling calls against. Compared to the traditional covered call, the PWCC has a smaller price tag -- $361 (which is also my max loss for the setup, assuming I do nothing at all), and I look to exit the setup as a whole at 10-20% of what I paid for the setup which, in this case, isn't as attractive as the $147 max profit of the covered call. However, there is one other aspect of the setup worth noting -- my buying the Jan 20th 18 call gives me the right to exercise for shares at $18. With the covered call, I'm locked in with 20.38 shares; with the PWCC, I'm not.

COVERED CALL CANDIDATES: AMRN, ARRY, FOLDAMRN at 3.33/share; sell Sept 16th 3.5 call; 2.75 db; max profit $75 (21.4% ROC).

FOLD at 7.00/share; sell Sept 16th 7 call; 6.20 debit; max profit $80 (12.9% ROC).

ARRY at 4.54/share; sell Sept 16th 5 call; 4.19 db; max profit $81 (19.3% ROC).

Notes: Preliminary/off hours. I would also note I haven't looked at these guys' pipelines (they're all biotech) or done due diligence, which is why I'm just looking at them as "candidates" at the moment.

SOLD VRX SEPT 16TH 17.5 SHORT PUT... for a .91 ($91) credit ... .

Here are the metrics:

Probability of Profit: 76%

Max Profit: $91/contract

Max Loss/Buying Power Effect: Undefined/$175/contract

Break Even: 16.59

Notes: I'll look to take this off at 50% max profit. Not interested in being married to a position with this cluster of a company ... .

BOUGHT TO COVER GLD AUG 12TH 117/121 SHORT PUT VERTWith the short put wing of this Brexit wracked setup approaching worthless, I closed it today for a .04 ($4)/contract debit.

I then rolled the short call side out to the August 19th expiry to the 121/126 for a .50 ($50)/contract credit and (inadvertently) sold an overlapping short put spread against it for a .25 ($25)/contract credit. (This is what happens when you're busy and do stuff on the phone app ... ). Hopefully, price doesn't whip back into the put side, and I can fix the overlap with the next roll ... .

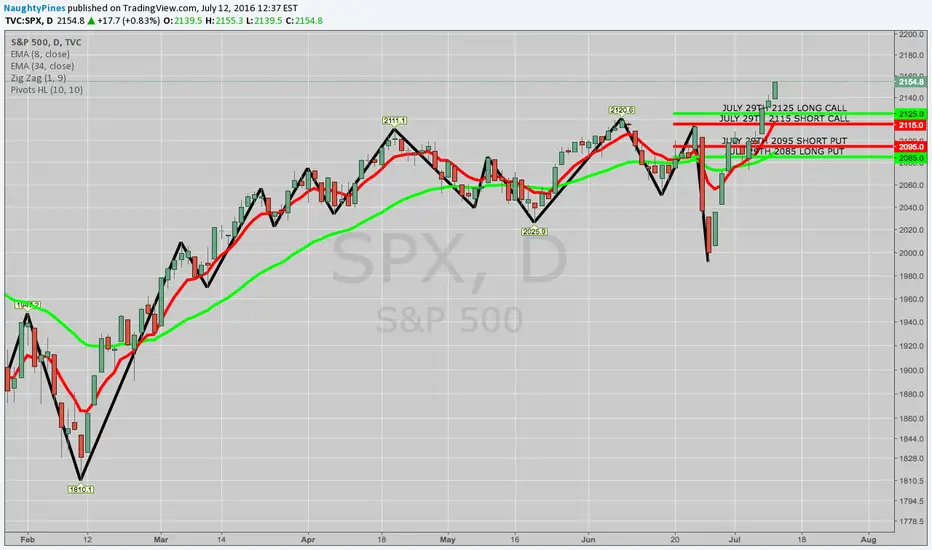

BOUGHT SPX JULY 22ND SPV TO CLOSE, ROLLED CALL SIDE FOR DURATION1. Closed the July 22nd 2020/2030 short put vertical for a .15 debit, as it's near worthless and done its job.

2. Rolled the July 22nd 2110/2120 call side out a week to the July 29th 2115/2125 and slight strike improvement for a .75 debit. The improvement isn't much, but I like to do these improvements small and over time until I get the required movement to exit the entire setup.

3. Sold the July 29th 2085/2095 short put vert to finance the call side roll for a 1.05 credit.

As with my NDX setup, what I need now is some movement back toward the call side to exit the entire setup at or above my "scratch point."

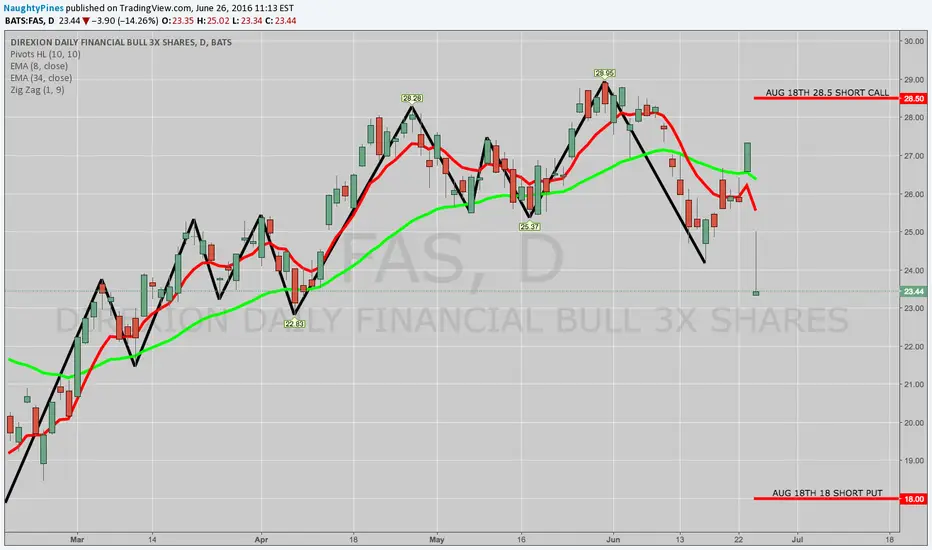

TRADE IDEA: FAS AUG 18TH 18/28.5 SHORT STRANGLETruth be told, I'm not a huge of fan of leveraged instruments, but when a $23 underlying has the potential to yield a $100 or more worth of credit, I'll briefly overlook the warts these instruments have as an "investment" tool ... .

Here are the metrics for the play:

Probability of Profit: 77%

P50: 81%

Max Profit: $127/contract at the mid (this is off hours pricing; we'll have to see whether that's possible at NY open)

Max Loss/Buying Power Effect: Undefined/$232/contract (estimated/off hours)

Break Evens: 16.73/29.77

Notes: I'll look to get a fill for anything north of $100/contract, given the price of the underlying. As usual, I'll look to take this off at 50% max profit.

KC shortUpdate on a upsloping trendline (blue) which acts as resistance

On the 5 hour chart, we should have generated a sell signal.

I still remain short via puyt spread 1x2s, as frost is no longer an issue. It appears the market is still digesting this from last week and should correct lower IMHO as physical supplies out of Brazil remain steady.

Warehouse stocks in EU and US plenty as well.

Dont get me wrong, as shown in the blue channel, even if we have a correction lower, the blue trend channel might indicate a change in trend, however the frost damage is simply not there and in order to rally, this market would need breaking news like that.... without anything of that sort coming out, I see a correction lower before making new highs.

Still, knowing coffee, I remain short with 1x2 calendar spreads, buying the downside 1 leg in one month and selling 2 lower puts in a month further back.

Binary Options Made Easy - GBPUSDWe look to place PUT or CALL Option at the confluence of Zones and Support & Resistance line for hourly expiry.

Binary Options Made Easy - EURUSD This is my method of trading Binary Options for the past 5 years trading only 30 minutes and hourly expiries. This method works 65 to 70% of the time and there are filters to further increase the winning %. We are not worried whether goes up or down. If it goes up, we SELL or place PUT options as it hits our SELL ZONES and buy areas where it drops and hits our BUY Zones.

As required with any form of trading, no strategy works all the time. Avoid over trading. Will observe how these zones marked plays out in the days ahead.

Money Management helps survive bad phases. Sticking to rules helps avoid emotional trading and maintain right psychology.

We are looking to place CALL or PUT options in the confluence area of Buy/Sell Zones in confluence with Support and Resistance on hourly candles with 30 minutes / 60 minutes expiries.

Will post results of the trades taken based on the areas marked.

Binary Options Made Easy - Trading Opportunities on USDJPYThis is my method of trading Binary Options for the past 5 years trading only 30 minutes and hourly expiries. This method works 65 to 70% of the time and there are filters to further increase the winning %. We are not worried whether goes up or down. If it goes up, we SELL or place PUT options as it hits our SELL ZONES and buy areas where it drops and hits our BUY Zones. As required with any form of trading, no strategy works all the time. Avoid over trading. Will observe how these zones marked plays out in the days ahead. Money Management helps survive bad phases. Sticking to rules helps avoid emotional trading and maintain right psychology.

We are looking to place CALL or PUT options in the confluence area of Buy/Sell Zones in confluence with Support and Resistance on hourly candles with 30 minutes / 60 minutes expiries.

Will post results of the trades taken based on the areas marked.

ROLLING SPY JUN 10TH 209/213 SCV TO JUNE 24TH 210/214 SCVRolling my SPY June 10th 209/213 short call vertical out a couple of weeks and up a strike for a little more time and a smidgeon of strike improvement (again ... ).

I got this filled for a $22/contract debit and then sold a 199/203 short put vertical in the same expiration for a $41/contract credit, so I'm net credit on the operation, so I've now got a SPY June 24th 199/203/210/214 iron condor in that expiry.

While I plan on continuing to roll the short call side up and out, if necessary, I'm naturally looking for price to stay between my 203 short put strike and my 210 short call strike toward expiry to exit the trade profitably.

SOLD JUNE 24TH SPX 2020/2030/2145/2155 IRON CONDORKeeping with the short term engagement trade theme here while I wait for some volatility to sell premium in something ... anything ... (currently, there is no fairly liquid underlying with an implied volatility rank of greater than 70 to work).

Metrics:

Probability of Profit: 58%

P50: 77%

Max Profit: $310/contract

Max Loss/Buying Power Effect: $690/contract

Theta: 8.99/contract

Delta: -3.62/contract

Notes: I'll look to take this off at 50% max profit or earlier if something pops to the forefront with decent volatility ... .

TRADE IDEA: IWM JULY 1ST 100/103/114/117 IRON CONDORLayering on a bit more bread on my butter while VIX>15 ... . This is about as full a boat as I like to have (not <25% in cash), so I may not be posting many new trade ideas here for a bit; most of them will be closing trades. I know ... boring ... .

Metrics:

Probability of Profit: 58%

P50: 65%

Max Profit: $102/contract

Max Loss/Buying Power Effect: $198/contract

Theta: 1.56/contract

Delta: -4.62/contract

Notes: You know the drill ... . Look to take this off at 50% max profit ... .

TRADE IDEA: GDX JUNE 17TH 20/27 SHORT STRANGLEGoing where the premium is at ... . I already have a setup in GDX in the same expiry, so I'm layering another on small here ... .

Metrics:

Probability of Profit: 69%

P50: 81%

Max Profit: $93/contract

Max Loss/Buying Power Effect: Undefined/~$236/contract

Delta: =8.29/contract

Theta: 2.98/contract

TRADE IDEA: VXX JUNE 17TH 17/27/37 LONG CALL BUTTERFLYWith low volatility having drained premium not only out of the broader market, but individual underlyings as well, I continue to look at VIX and VXX derivatives to go "long volatility" in lieu of opting for low vol strategies like debit spreads, calendars, and diagonals.

In this particular case, I'm opting to use a long call butterfly given its high risk/return ratio, its relative cheapness to put on, as well as the large profit zone the setup generates.

Here are the metrics for the setup:

Probability of Profit: 54%

Max Profit: $910/contract

Max Risk/Buying Power Effect: $90/contract

Notes: There are a couple of different ways to manage this intratrade, one of which merely involves taking the whole setup off in profit. The alternative way is to strip off the long call vertical portion of the setup (the 17/27 wing) first as price moves up, after which you would look to exit the short call vertical wing (27/37) as VXX mean reverts (as it is want to do).

COVERING VXX SEPT 16TH 13/MAY 6TH 17.5 SHORT CALL DIAGONALI put this on on April 1st, thinking it might be a while before I could take it off, but covered it today on this pop, freeing up the buying power for another go should be strike $17 again. I put it on for $373/contract, and took it off today for a $419 credit, yielding a $42.93/contract profit in six days.

Naturally, this isn't hugely earth shattering profit-wise, it's always best to take off a VXX setup of this type as soon as possible. The contango helps your short call in the long run, but also eats away at the value of your long over time ... .

SOLD APRIL 8TH GME SHORT STRANGLESorry I didn't get to post this before NY close ... .

Filled for a $94 credit. I usually like to see a $100/contract out of these setups, but I figured it was close enough ... . I'm looking for price to stay between my short strikes between now and expiration and for volatility to contract post-earnings announcement. Post-announcement, price is down about $2 to $28.38, so it looks good at this point .... .

I'll look to take it off at 50% max profit or for about $47 (a .47 debit).

SVXY -- Long via March 18th 31/35 Short Credit SpreadMarch 18th SVXY 31/35 ShortPut Credit Spread

1.64/$164 Max Profit Per Contract

WFT COVERED CALL IDEAWith covered calls, I look for cheap underlyings with high implied volatility rank/high implied volatility and setups that will produce at least a 10% return if called away at the short call strike.

WFT fits the bill, with a rank of 72, an implied of 84, and a 13.06% return if called away at the nearest out of the money strike.

Here's the setup:

Buy 100 shares WFT at 8.52

Sell 1 Feb 19 9 short call

Entire Package: 7.94 ($794)

Max Profit: (If Called Away at 9) $106

USO COVERED CALL IDEAHaving waited a long time for West Texas Intermediate to hit 2009 levels, I figured I'd put my money where my mouth was and go long USO when it did.

I filled this one earlier today:

Bought 100 Shares USO @ 10.05

Sold 1 Feb 19th 11 Call

Total Package: 9.69 debit

Max Profit: $131 (if called away at 11)

You could probably get a slightly better fill than I did, as USO ended the day at 9.90 ... .