Guardion Health Sciences (GHSI) BounceGHSI recently peaked at $3 and is trading below 50 cents currently. Potential upside is over 60% making this a great buy for anyone looking to ride the wave up. I would not hold beyond 50 cents. Day trade only

Pennystock

AMS - 209 Day Bullish Trend Representing Company GrowthAmerican Shared Hospital Services engages in leasing radiosurgery and radiation therapy equipment to healthcare providers. Its equipment includes Gamma Knife, PBRT, and IGRT. It operates through Medical Services segment. The company was founded by Ernest A. Bates in 1977 and is headquartered in San Francisco, CA.

SHORT INTEREST

6.66K 07/15/19

P/E Current

17.28

P/E Ratio (with extraordinary items)

19.69

P/E Ratio (without extraordinary items)

13.62

$SNAP Back to being the laughing stock of the SM, PT $4.00Chart shows massive downtrend approaching once support breaks, good time to take out a nice short IMO.

8p / 15p targets - buy entry triggers - gap to fill BULLISHAn amazing asset value company with newsflow

Copper & gold play.

potential financial partners in talks at moment

Several assets within Indonesia

An amazing track record BoD

8p 1st target with 15p mid-long term. 15p+ on big news.

At great value at moment & a bargain considering the assets.

60p / 75p target BULLISH - At support - RSI retrace #mfchartMassive amount of newsflow to come before drill summer campaign.

Cash in hand.

no warrants,

Lombard bought more,

JV / farm out partner to come,

appraisal well, production well & exploration well to come

60p to 75p target & make sure you slice along the way to protect profits.

156p - 200p targets - low mcap £14m with trading update soonA lot of last results have been priced in for some time now.

Progress has been done by company recently & they are ready to post a trading update very soon most likely this week.

recent bullish divergence

BoD have been buying as of late

Looking for at least 50-100% here, hopefully trading update will catch many by surprise.

Rejected Rejected Rejected - lost supportBe extremely careful here - this is an opp for a short I think.

Heavy down trend

Losing all time lows heads to further lows

3.52p / 6.78p price targets - 200ma approach - support heldas we get closer and closer to 200ma & support level is being held I think scaling in is a better decision as we don't know when it will start motoring

Zamsort is an amazing asset & worth much more then £18m mcap

Hopefully a sale of Casa will give us a nice amount to continue operations for Zamsort.

Pretty happy holding & waiting for delivery.

2.80p / 3.13p 1st target resistance - above t-lineLooking bullish at moment & could continue to head to target on low volume

Strong support - 1h chart higher low - $6.56 / $8.11 targetsGood earnings report here last week.

Cannabis momentum will soon come back.

Make sure u look at tigher timeframes to gather confirmation of trend reversal

I believe we are at the start of one but make sure u get tight stop losses

$6.56 / $8.11 targets

Keep a watch for entry - topup where support + 20maresistance becoming support & 20ma will also help to achieve the level

2.59p / 5.5p targets - Trend reversal - RSI strongBought at 1.86p & 1.74p today.

Company turning around with new CEO & new plans moving ahead.

Amazing tech with a huge amount of potential.

Cash in bank with last placing a month ago at 1.6p so plenty of time to grow.

Anything sub 0.09p is a good buy - support levelAs the drill is coming up in most likely November now this is a good play to keep a watch for then.

2 crosses - one bullish & one bearish short term

I think there will be a further touch of support before any bull run move to come ahead of drill

I hold at 0.087p and will add more sub 0.09p

If oil strikes at 14mbpd you are looking at a 24mil mcap vs present 5mil mcap & that is only 1 of the asset interest.

20ma rejected - high risk investment - wait for close overA stock that gets used as a pump vehicle on a downtrend with high risk

for proper confirmation as a good investment moving forward wait for 20ma official close above it.

12p - 15p conservative target / RSI breakout - 10x bus potentialDown trend reversal happening at moment

12p - 15p conservative 1st target & as business grows I think it will break 15p.

Revenue growth business going forward.

Demand is growing within the VR field, expansion to US & other regions continues

Shares in issue 250m

MCAP £19 m

Shares not in public hands circa 50%

BOD holding roughly 20%

CEO Martin single biggest shareholder near 10%

IPO 10p

Latest Raise 6p

Bargain at 30p levels - Undervalued - Revenue making - BULLExtremely bullish here & been waiting for months for this opportunity to buy down here.

Bought at 30.4p & will buy more if I get an opp at 29p-30p

Bullish divergence on RSI.

Resistance becomes support in most plays even if it takes a few weeks/months.

44.2p - 57p next resistance. Longer term will be more as this is a revenue growth making company.

Sorry for format copy paste wrong but here is the values for last years.

$53.7m revenue

$34.3m EBITDAX

$36.2m cash generated

Fully cashed up with $17m & $10m facility (undrawn)

South Disouq coming later this year.

Easy profit to be made from this levels.

Three months ended Twelve months

December 31 ended December

31 (audited)

US$ million, except per unit 2018 2017 2018 2017

amounts

---------- --------- -------- --------

Net revenues 13.8 11.0 53.7 39.2

---------- --------- -------- --------

Netback(2) 10.4 8.5 41.7 28.9

---------- --------- -------- --------

Net realized average oil price/service

fees - US$/barrel 59.07 54.39 62.43 46.70

---------- --------- -------- --------

Net realized average Morocco

gas price - US$/mcf 9.78 9.72 10.33 9.51

---------- --------- -------- --------

Netback - US$/boe 28.94 28.26 32.01 24.47

---------- --------- -------- --------

EBITDAX(2) (3) 7.1 8.0 34.3 21.4

---------- --------- -------- --------

Exploration & evaluation expense

("E&E") (0.2) - (5.7) (0.2)

---------- --------- -------- --------

Depletion, depreciation and

amortization ("DD&A") (6.3) (4.8) (17.3) (17.8)

---------- --------- -------- --------

Impairment expense (3.5) - (3.5) -

---------- --------- -------- --------

(Loss)/gain on acquisition - (4.7) (0.2) 29.6

---------- --------- -------- --------

Total comprehensive (loss)/income (4.0) (3.4) 0.1 28.3

---------- --------- -------- --------

Net cash generated from operating

activities 8.9 15.1 36.2 21.6

---------- --------- -------- --------

Cash and cash equivalents 17.4 25.8 17.4 25.8

Possibly a good buy at all time support - check fundamentalsSitting right at all time support & possibly a good buy but check fundamentals here.

Options almost 100% above price Volume/RSI growth - 0.14 targetStrong bullish signal from Tony Manini & Steve Hughes team with options at 0.08 (almost at 100%)

know them fairly well from ARS venture back on AIM which continues to perform

CUC quite iliquid stock but strong BoD which will deliver with patience.

If you are prepared to wait you will make 200%+ within 2 years if not more.

Weekly T-line re-test - possibly a bounce to come soonPossibly a bounce to come this week if fundamentals are in place with a potential catalyst.

No MA's above price which is a nice clear path of minimal resistance.

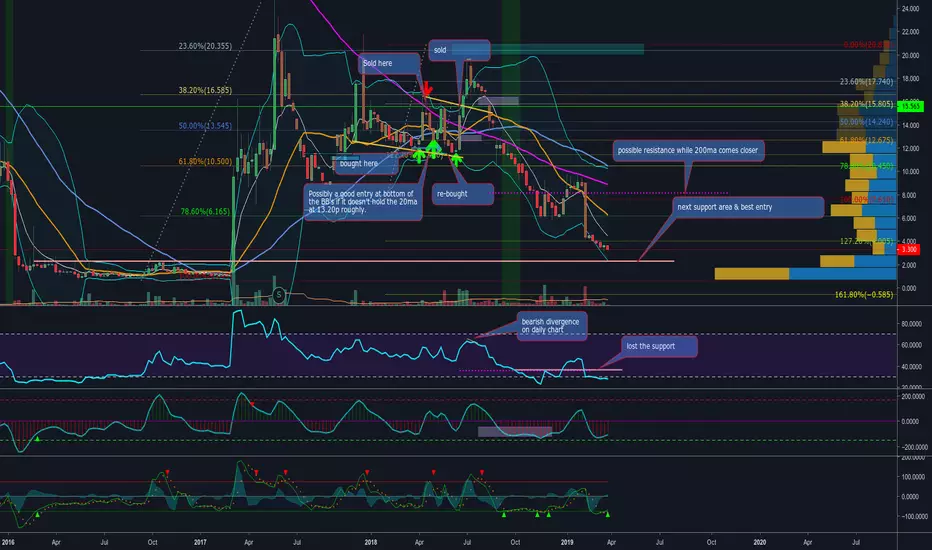

RSI Bearish divergence - 2.30-2.56p possible retrace #mfchartIt hit resistance at 3.34p and dropped last week but held t-line

due to bearish divergence I would think we could have a small retrace before next leg.

keep an eye on Moving averages as support as well.

Watch for entry at 2.29p No previous support - BearishBought & sold twice this stock but looking for a re-entry before operations resume later this year.

Keep a look out, price might bounce occasionally till then but best to look for a solid support area for entry.

Looking for entry around 2.2p-2.3p but possible best to scale in as there will be volume around there.