Bias more on upside supported by 40days moving average27/02/22

Doji candle form at 50% Fibo supported by 40days Moving Average in weekly chart.

If next few candle support around 50% fibo area, this will determine a strong support area.

Otherwise, we may see $44 as next support

PFE

PFE still lower to go. Pfizer looks to test $50, and possibly the gap around 46~ if things get really ugly. Omicron is looking really promising as granting significant immunity after infection, which should reduce demand for further vaccinations. These vaccines companies have YEARS of covid priced into their stocks... Short side is getting a bit long in the tooth for new entries, however I am still holding 2/3rds of my puts across the board for these plays.

We posted our short thesis in another thread www.tradingview.com

PFE | Shorting the Vaccine 💉My current position and play is marked on the chart. I am expecting more selling pressure to come in now that we closed below the nearest zone. Expectation is that PFE will head toward the next zone located at the bottom. I will be trailing my stop once PFE begins the bearish move.

Pfizer more to drop

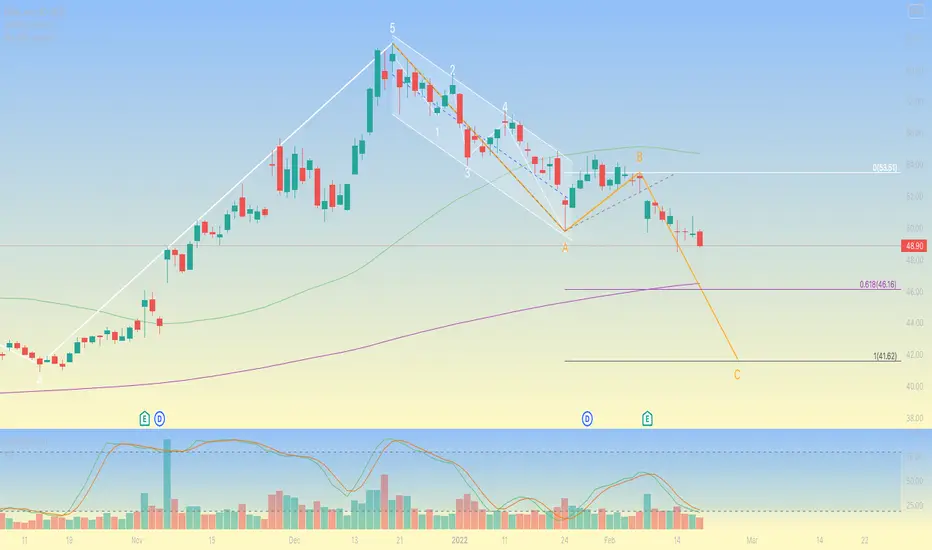

I see a 5 waves move up finished at $61 on 20th December, fallowed by an A-B-C standard correction.

Using the guideline of equality A=C and the Trend Based Fibonacci extension Pfizer will drop till about 1 level or $41.

This has support as well from $41 OCT 2021 level which is also the W4 level in the previous impulse movement.

Disclaimer:

This is my analysis and does not constitute financial advice

For more analysis like this ON DEMAND please leave me a message.

Pfizer: Ready to Shoot Lower? Pfizer - Short Term - We look to Sell at 49.33 (stop at 51.54)

The trend of lower highs is located at 53.50. Previous support located at 50.00. A move through bespoke support at 50.00 and we look for extended losses. Closed below the 20-day EMA. The medium term bias remains bearish.

Our profit targets will be 43.51 and 41.00

Resistance: 54.00 / 57.00 / 60.00

Support: 50.00 / 45.00 / 40.00

Disclaimer – Saxo Bank Group. Please be reminded – you alone are responsible for your trading – both gains and losses. There is a very high degree of risk involved in trading. The technical analysis, like any and all indicators, strategies, columns, articles and other features accessible on/though this site (including those from Signal Centre) are for informational purposes only and should not be construed as investment advice by you. Such technical analysis are believed to be obtained from sources believed to be reliable, but not warrant their respective completeness or accuracy, or warrant any results from the use of the information. Your use of the technical analysis, as would also your use of any and all mentioned indicators, strategies, columns, articles and all other features, is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness (including suitability) of the information. You should assess the risk of any trade with your financial adviser and make your own independent decision(s) regarding any tradable products which may be the subject matter of the technical analysis or any of the said indicators, strategies, columns, articles and all other features.

Please also be reminded that if despite the above, any of the said technical analysis (or any of the said indicators, strategies, columns, articles and other features accessible on/through this site) is found to be advisory or a recommendation; and not merely informational in nature, the same is in any event provided with the intention of being for general circulation and availability only. As such it is not intended to and does not form part of any offer or recommendation directed at you specifically, or have any regard to the investment objectives, financial situation or needs of yourself or any other specific person. Before committing to a trade or investment therefore, please seek advice from a financial or other professional adviser regarding the suitability of the product for you and (where available) read the relevant product offer/description documents, including the risk disclosures. If you do not wish to seek such financial advice, please still exercise your mind and consider carefully whether the product is suitable for you because you alone remain responsible for your trading – both gains and losses.

Pfizer Analysis 08.02.2022Hello Traders,

welcome to this free and educational analysis.

I am going to explain where I think this asset is going to go over the next few days and weeks and where I would look for trading opportunities.

If you have any questions or suggestions which asset I should analyse tomorrow, please leave a comment below.

I will personally reply to every single comment!

If you enjoyed this analysis, I would definitely appreciate it, if you smash that like button and maybe consider following my channel.

Thank you for watching and I will see you tomorrow!

Pfizer, and why you keep old notesI got an alert on Pfizer NYSE:PFE just now that on the 30m a Tradingview Spike Alert I had setup fired. This is following research I did over the weekend to the Support level that PFE reached in the recent down move. While doing that I found an old annotation from November 2020 earnings that informed a long term dividend investment play. It's nice to see how something has performed over the long term to remind an investor to buy and hold good companies.

The company has earnings tomorrow.

The Week Ahead: TWTR, UAA, GPN, PFE Earnings; ARKK, XBI, XRTEarnings Announcements in Options Liquid Underlyings with >70 rank and >50% 30-Day Implied:

TWTR (93 rank/90 30-day implied) (Thursday, before market open)

UAA (80/68) (Friday, before market open)

GPN (71/51) (Thursday, before market open)

PFE (76/42) (Tuesday, before market open)

Pictured here is a directionally neutral TWTR short strangle paying 1.34 on a buying power effect of 3.71 (on margin), 36.1% ROC at max; 18.1% at 50% max. It announces earnings on Thursday before market open, so look to put on a play in the waning hours of Wednesday's session if you want to take advantage of the ensuing volatility contraction post-announcement on Thursday.

For those more of a defined risk bent, consider the February 18th 25/30/44/49 iron condor, paying 1.14 at the mid price as of Friday's close on buying power effect of 3.86, 29.5% ROC at max, 14.8% at 50% max with 2 x expected move break evens.

UAA is probably small enough to short straddle/iron fly, with the February 18th 19.5 short straddle paying 2.42 on buying power of 3.93 (on margin), 61.6% ROC at max, 15.4% at 25% max. The risk one to make one iron fly would be a "stays within the expected move" sort of play with the February 18th 15.5/19.5/19.5/23.5, paying 2.03 on 1.97, 103% ROC at max; 25.8% ROC at 25% max.

The GPN February 18th 130/160 short strangle was paying 2.97 on buying power of 14.97 as of Friday's close, 19.8% ROC at max, 9.9% at 50% max. The bid/ask is showing wide in after hours, and I don't particularly like the five wides where I want to pitch my tent. This is probably why I haven't bothered to play it before.

Although PFE's 30-day is a bit <50%, I figured I'd price out a setup because of its high options liquidity. Unfortunately, it's not very compelling at the moment, with the 16 delta 48.5/58.5 in the February 18th contract paying a scant .89 on buying power of 6.12 as of Friday's close -- 14.5% ROC at max, 7.3% at 50% max.

Exchange-Traded Funds With Ranks >50 and 30-Day IV >35%:

ARKF (76/63)

XBI (71/45)

ARKK (70/67)

ARKG (70/65)

XRT (63/46)

KWEB (63/54)

SMH (60/41)

GDX (50/45)

Pick your Cathie Woods poison (ARKF, ARKK, ARKG), I guess. Otherwise, sell premium in XBI or (there's one I haven't seen in a while) ... XRT, although you're probably going to get more bang for your buck out of KWEB, with its higher 30-day.

Broad Market Exchange-Traded Funds, Ordered By Implied Volatility Rank:

QQQ (55/29)

IWM (54/30)

EFA (43/19)

SPY (41/22)

DIA (40/21)

$PFE - Downtrend Reversal - 4 Day Inside Bar - Upcoming CatalystNYSE:PFE

A hammer signaled reversal for $PFE. Shortly after price broke out of the downtrend resistance. Four inside bars have formed during period of consolidation.

$PFE looks primed for sharp movement. Catalyst would likely be FDA / CDC approval/rejection of its Covid vaccination for children, expected in 4th week of Feb. Application is for 2 doses, though 3 would be required. Application and study for 3rd shot are expected to be submitted during the initial application review phase.

This is one ticker to be aware of.

Biased long, but willing to play both sides.

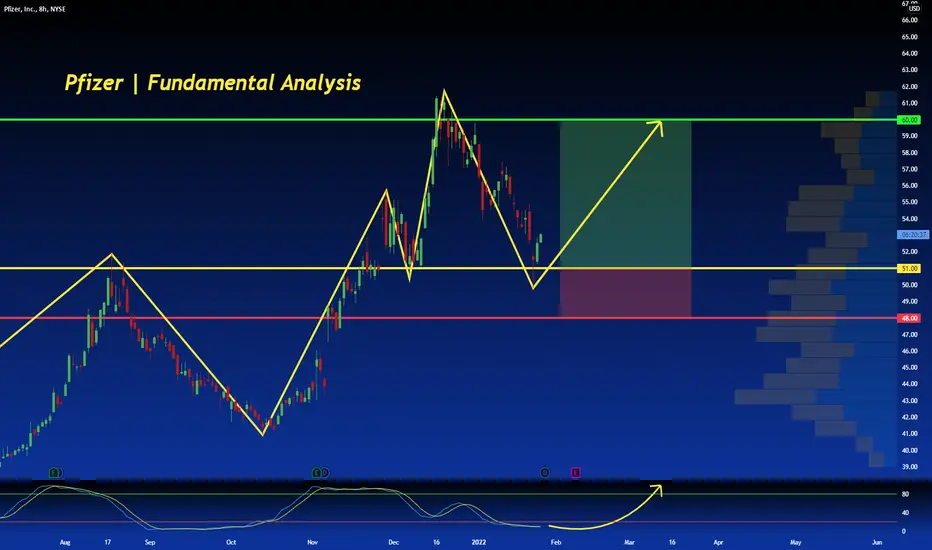

Pfizer | Fundamental Analysis | MUST READ | LONG 🔔Historically, Pfizer has not had much momentum when it comes to stock performance. Over the past ten years, the S&P 500 Index has outperformed this large pharmaceutical company. But now Pfizer is gaining momentum. Last year it outperformed the benchmark index - Pfizer was up 60%, while the S&P 500 was up 27%.

And today's Pfizer doesn't look much like Pfizer did a few years ago. In 2020, the company completed the separation of its Upjohn business, eliminating an element that was driving down revenues. Today, Pfizer has many "best sellers," a new coronavirus drug, and a full development cycle. So is it worth investing in this drug maker in 2022?

First, let's look at the company's Covid business. Pfizer is a leading supplier of vaccines in many parts of the world. In the U.S., the company has fully vaccinated more than 118 million people. But overseas, Pfizer's vaccine business is actually even bigger. The company claims that it generates 75% of its revenues from vaccine sales outside the United States.

The European Union recently exercised an option to supply more Pfizer vaccines, bringing the total number of doses of Pfizer vaccines to be delivered this year to over 650 million. The full agreement, signed last spring, calls for up to 1.8 billion doses to be delivered to the region by 2023.

In Pfizer's latest earnings report, the company projected vaccine revenue of $36 billion for all of 2021.

But this year could turn out to be even more successful for Pfizer than last year. Here's why. Vaccine orders remain high -- but with the addition of a new coronavirus product. Late last year, Pfizer received approval for the emergency use of Paxlovid, an oral coronavirus treatment. Paxlovid is a pill that should be given at the first sign of infection. The drug's main ingredient blocks the action of an enzyme necessary for the coronavirus replication process.

The U.S. has ordered 20 million courses of Paxlovid treatment, and the U.K. has ordered 2.75 million. SVB Leerink analyst Geoffrey Porges predicts that Paxlovid will generate more than $24 billion in revenue this year and $29.7 billion in vaccines, according to FiercePharma. That amounts to more than $50 billion in revenue from the coronavirus program alone.

Of course, investors are most concerned about what will happen to these revenues in a post-pandemic world. Right now, it's impossible to accurately predict the level of revenue from the coronavirus program in the future. And that represents uncertainty. Nevertheless, experts say the coronavirus will exist. And that means we will need remedies and treatments. So we can probably expect a satisfactory level of revenue from coronavirus-related products for quite some time.

But here's the best news: Pfizer is far from being a coronavirus-only company. The company's nine-month earnings report shows that at least six products are generating blockbuster revenue. And in the third quarter, the company says, revenue excluding the coronavirus vaccine rose 7 percent to more than $11 billion.

As if that weren't enough, Pfizer has something else to like. And that's the pipeline. The company is working on 94 programs -- 29 of which are in Phase 3 and nine of which are in the registration phase. That means we may see a new batch of drugs in the not-too-distant future. This is important because the patent on some of Pfizer's drugs expires at the end of this decade. The blood-thinning drug Eliquis, for example, will lose protection in 2028. This is a standard part of life for a pharmaceutical company - and that's why it's important to have a strong product portfolio to make up for future patent expirations.

Now let's look at the valuation. As mentioned earlier, Pfizer's stock price has risen slightly. But it is still trading at very reasonable levels. It trades at only 8.5 times projected earnings. In addition, Pfizer pays a solid dividend, with a yield of over 2.8%.

So should you invest in Pfizer in 2022? Well, now seems like a good time to do so. The company generates billions of dollars in revenue from its coronavirus vaccine program. It has a portfolio of non-coronavirus drugs and a full cycle of late-stage research. The stock looks inexpensive -- and an investment in this major pharmaceutical player will provide you with passive income in the form of dividends. All of this is a great formula for success this year and in the years to come.

PFIZER, INC Hello friends, Black Mountain Analysis Team:

PFIZER price after a good climb to the top is resting - Time resting or price resting -

You can see the positive divergence of the RSI indicator in the chart.

If supported, we can expect to climb again in the new year.

TP1=61-62$

TP2=65$

TP3=70-74$

____________________________

sl=54$

MRNA Inverse UpdateMRNA going according to plan from my earlier posts. I can't update with charts anymore, for some reason? So I am posting again. Re-iterating targets in the 170-180 range. $230 is the Line in the Sand for bearish continuation. took off a few of my puts today.

Pfeizer reversing. PFECOViD paranoia did great things for the pharma industry, including and especially Pfeizer. But, even then, nothing can grow forever. South Sea, East India and Pfeizer are no exceptions. The usual divergence with specific wave cycle finished. Highly, highly suspect for a reverse.

We are not in the business of getting every prediction right, no one ever does and that is not the aim of the game. The Fibonacci targets are highlighted in purple with invalidation in red. Fibonacci goals, it is prudent to suggest, are nothing more than mere fractally evident and therefore statistically likely levels that the market will go to. Having said that, the market will always do what it wants and always has a mind of its own. Therefore, none of this is financial advice, so do your own research and rely only on your own analysis. Trading is a true one man sport. Good luck out there and stay safe!

$PFE , another one chart for short thoughts pfe chart with thoughts for Potential short position

it is inside at down channel

disclaimer

Pfizer (PFE) to continue its BULL run in 2022!Fundamental Analysis

Pfizer, Inc. has consistently been one of the largest pharmaceutical companies in the world for the better part of the last two decades. The company has a remarkable history going back all the way to the year 1849, when Pfizer was founded in Brooklyn, New York. The large cap pharma giant has developed a well-balanced and deep portfolio of products in key areas like Inflammation and Immunology, Internal Medicine, Oncology, Rare Disease, Vaccines etc.

However, it seems that as a result of the success of Pfizer's vaccine COVID-19 treatments, many investors have forgotten about the rest of Pfizer's business and how successful it continues to be.

It is true that the sales of its COVID-19 vaccine ($36 billion in 2021 alone) have managed to nearly double Pfizer's annual revenue from $41.9 billion in 2020 to over $78 billion in 2021.

What's even more important is that the strong sales growth has also translated into higher profits for the company as its profit margins before interest and taxes, referred to as EBIT margin, have risen over the past year. This shows that Pfizer has managed its R&D and all other fixed and operating costs associated with development, production and distribution efficiently, thus improving the profitability ratios of the company. The large cap pharma giant has also managed to almost triple the size of its free cash flow to more than $29 billion over the past twelve months compared to only $11.6 billion in 2020. More free cash flow makes a business more robust, giving Pfizer more money to invest in research and development of new products, pay more in dividends, or strengthen its balance sheet.

The company currently has a total of 94 drugs in the pipeline spread across critical treatment areas like Inflammation and Immunology, Internal Medicine, Oncology, Rare Disease, Vaccines etc. all waiting regulatory approval.

- Phase 1(27); Phase 2 (29); Phase 3 (29); Registration (9)

Looking at the outstanding track record of Pfizer's drug development capabilities, we can easily state that the company will continue to be a leader in the sector that it operates in.

Macro view

The equity markets in the US are currently undergoing a process of meaningful repricing and re-valuation of what companies are actually worth, as everyone is getting ready for the Federal Reserve to start raising interest rates in the US and tighten its monetary policy. In a rising interest rate environment, investors tend to move away from expensive high-growth stocks trading at unreasonably high P/E and P/S valuations as the tighter monetary policy environment makes it much more difficult and more expensive for such companies to borrow and invest capital and produce the high earnings growth that investors expect from them. Well-established large cap Healthcare and Biotech stocks are considered to be least correlated with the monetary policy situation in the country as they tend to trade more on FDA drug approvals and drug-related announcements rather than actual earnings per share. Most of the leaders in this space also have a substantial pricing power, as people using their medicines are doing so because they need them and because the drugs are helping them get better. Thus, owning Healthcare and Biotech stocks in a rising inflation and interest rate environment is a defensive play that could end up paying off big time, as stocks in these sectors are rather volatile.

Technical Analysis

The stock has experienced a volatile retracement from its $61 all-time highs and is currently in a corrective phase. However, the uptrend is still intact as the price is well above both the strong horizontal support at $51 and the upward sloping diagonal support (blue line) at $44. Furthermore, the stock is trading above its 5, 20, 50, 200 EMAs, which is also a bullish continuation signal. We expect buyers to start coming in around the $52-53 level, thus establishing the next higher high. Once that is done, the stock will re-test its ATH at around $61 in Q1 of this year. The broad market framework, together with the many positive company related developments in the coming months are expected to bring enough momentum to the stock in order for it to break its previous ATH and set a new one sometime in Q2. Our target for the stock in H1 of 2022 is around the $68 level, which is roughly 30% higher from the current levels.

Follow and Copy us on eToro for more detailed market analyses, profitable trading ideas and a consistent portfolio performance.

[ b] Sincerely,

@DowExperts

INVERSE $MRNA breaking out!Massively bearish setup on MRNA. Whether we get one more deadcat, I do not know, but this thing is going to 170/180 area and could be as soon as next week. $125 is my final target. The amount of downside risk in MRNA is absolutely staggering. This is basically a $50-70 stock without the covid premium.

PFE / USD 1D Pfizer - Flying the Bull Flag?Bull flag in the trading sense of the word... I could see a retest of the ATH...Pretty sure the shareholders can too. Bull flag within the ascending broadening wedge pattern may visit around the $55.00 region first. Look at how fast this ones moved though. No surprises eh. Personally not trading this instrument.

Pfizer | Fundamental Analysis | LONG SETUP ⚡️Pharmaceutical giant Pfizer has been at the forefront of the industry, developing drugs to treat COVID since the pandemic began. Unfortunately, the world continues to struggle with different strains of the virus, most recently with the Omicron variant, but Pfizer's products are still in high demand, which will likely boost its results in 2022.

It's been about a year since the first COVID vaccine became available in the U.S., and a race has begun to ramp up production and dose distribution. Several companies have been working on vaccines, but the market has become a two-company market. The vast majority of the doses administered in the U.S. came from Pfizer and Moderna, two companies that developed vaccines using mRNA technology.

Pfizer and Moderna have developed mRNA vaccines that use the genetic code of the virus to trigger an antibody response in the human body.

Traditional vaccines use an attenuated form of the whole virus, which teaches the body to defend itself against it. This is essentially similar to how the body develops immunity after a person gets chickenpox, but the weakened virus does not make the person sick. Both types of vaccines achieve similar results, but pharmaceutical companies can reproduce the genetic code for production faster and easier than the virus itself.

Demand for the vaccine has increased primarily because of the ability of the virus to mutate into new variants. Initially, Pfizer's vaccine was supposed to treat with two doses, but as new variants emerged, many began to give a third shot (called a booster). Pfizer's original 2021 forecast called for 1.3 billion doses, but it ended up producing about 3 billion doses in 2021. Now, the company's management predicts that Pfizer will produce about 4 billion doses in 2022.

This is a tragic and challenging time for society as the pandemic continues, but Pfizer's leadership position has created tremendous benefits for the company. First, the actual sales of its vaccine have been enormous: The company's expected revenue in 2021 was $36 billion. By comparison, Pfizer's 2020 revenue was $41.9 billion; this means that the COVID vaccine nearly doubled Pfizer's business!

What's more, it was profitable for Pfizer. The company's earnings before interest and taxes, called EBIT margin, increased over the past year as the vaccine business grew. The company has also significantly increased free cash flow, which was more than $29 billion in the past twelve months, up from $11.6 billion in 2020. Increased free cash flow makes the business more sustainable, which gives Pfizer more money to invest in research and new product development, pay dividends, or strengthen its balance sheet.

As the Omicron option spreads, it is becoming more likely that COVID will not disappear entirely shortly. Pfizer recently developed an oral antiviral pill to treat early-stage COVID symptoms, and company executives estimate that 80 million courses of treatment could be produced in 2022. Although our focus today is on the next twelve months, Pfizer could potentially profit from the COVID treatment for several years.

Investors have reacted to Pfizer's COVID success; the company's stock is up 56% in the last year, a big gain for a company with a market value of $329 billion. Still, the market may not be valuing Pfizer highly enough.

If we want to value a stock by the amount of free cash flow that investors receive per share, we can look at the free cash flow yield; this percentage reflects how much of the stock price investors receive in free cash flow. We want to get as much free cash flow for our money as we can because it pays dividends, funds new products, and generally creates value for shareholders - it's like the "lifeblood" of a company. Accounting or non-cash items can affect earnings, so free cash flow can provide a fresh perspective on stock valuation.

Pfizer's increase in free cash flow this year resulted in higher returns because free cash flow grew faster than the stock price. Now that the stock has started to rise, yields are down, but we are still near multi-year highs, which means that the stock offers you more "value for your money" than it has for most of the last ten years. In other words, they are still cheap. With COVID firmly entrenched in our world, Pfizer retains its chances of success in 2022.

711 - Desperados: Momentum/Trend Cloud @ 7 - 12% correction to well over 23% on Trend... extremes.

Notice how Momentum has fallen below Trend.

A Picture of health or dysfunction.

IV

AAPL @ 61%

TSLA @ 63%

NVDA @ 77%

AMD @ 88%

and Beacon of Safety PFE @ 85%

Baba is now 90%

Pfizer is extreme as is Baba.

These are all later stage readings for Implied VX.

_____________________________________________________

All signs of a Shorter Term process of carving out a High prior

to the Ice Bucket challenge from the Federal Reserve.

$PFE Is testing the breakout zone, what's next?NYSE:PFE is currently testing the breakout zone, anticipating to retest recent highs again 61.70

Follow for more updates...

#AHMEDMESBAH

PFIZER, INC Black Mountain Analytical Team in the previous Pfizer Idea update:

We see that the resistance line of the rsi indicator is broken in the monthly time frame, if the failure is not fake and has happened validly, we can expect good things from this company.

There is also a pulse of positive news from the company. (Pfizer and BioNTech Provide on Omicron Variant)