The stock market is waiting for the release of PMI and NFP!The index is above the EMA200 and EMA50 in the 4H timeframe and is trading in its ascending channel

If the index rises towards the supply zone, which is also at the intersection with the weekly pivot and the midline of the channel, you can look for sell positions in the Nasdaq index

A valid breakout of the downward drawn Fibonacci retracement will provide a downward path for the indicator to the specified support area and then the bottom of the ascending channel

PMI

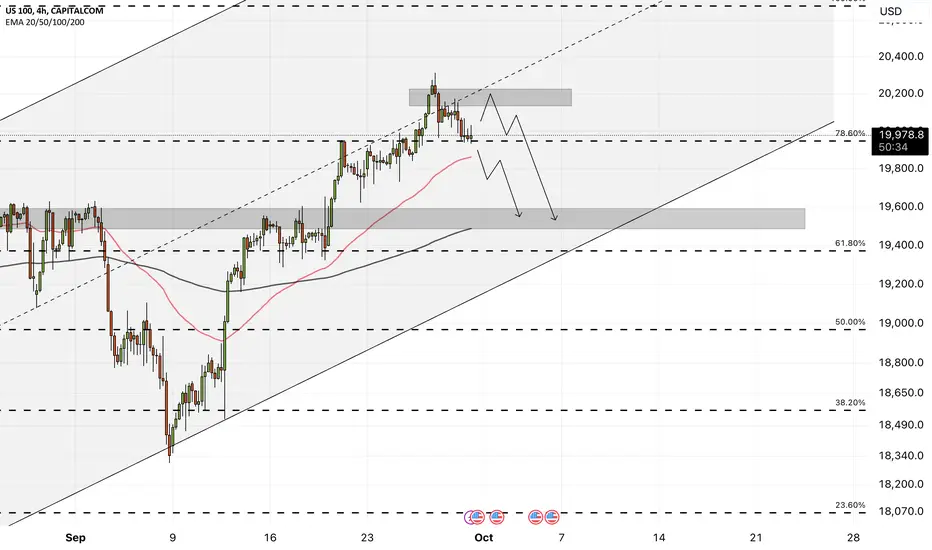

Nasdaq - Very weak start of the stock market in September!The US100 is below the EMA200 and EMA50 in the 4H time frame and is trading in its descending channel

The index has reached the target of the downward movement of its previous analysis, and you can save a part of your sales position and place your SL in profit

If the index continues to decline towards the specified demand zone, which also intersects with the midline of the descending channel, we can look for buying positions for the Nasdaq index

An upward price correction of the index will provide us with new sales position with a suitable risk reward

XAGUSD - Silver will go below 28 dollars?!Silver has been below the EMA200 and EMA50 in the 4H timeframe and has exited its ascending channel

If the downward movement continues and silver is placed in the specified demand zone, we can look for silver buying situations

Silver's upward correction will provide us with new sell positions with appropriate risk-reward

XAU/USD : More Bullish Move Ahead ? (READ THE CAPTION)By reviewing the #gold chart on the 2-hour timeframe, we can see that, as expected, the price sharply corrected to fill the FVG that had formed between $2506 and $2520. After entering the demand zone at $2506, gold experienced a strong upward movement, pushing back up to $2520! This analysis resulted in a gain of over 380 pips. Currently, gold is trading around $2505, and if it can stabilize above $2495, we can anticipate further growth. Otherwise, we may see a decline in gold prices to levels below $2490.

The Main Analysis :

Please support me with your likes and comments to motivate me to share more analysis with you and share your opinion about the possible trend of this chart with me !

Best Regards , Arman Shaban

((2+4+7+13+15+18+26+36+38+69+87+101+183+209+1000+1002+1000000000+1000000001+ 1000000853)^♾️*69) + 1 !

USDCAD: Three days short traders on the market, out of balanceHi everyone and welcome to my channel, please don’t forget to support all my work subscribing and liking my post, and for any question leave me a comment, I will be more than happy to help you!

“Trade setups, not movements”

1. DAY OF THE WEEK (Failed Breakout, False Break, Range Expansion)

Monday DAY 1 Opening Range

Tuesday DAY 2 Initial Balance

Wednesday DAY 3 (reset DAY 1) Mid Point Week

Thursday DAY 2 ✅

Friday DAY 3 Closing Range

2. SIGNAL DAY

First Red Day

First Green Day

3 Days Long Breakout

3 Days Short Breakout ✅

Inside Day

3. WEEKLY TEMPLATE

Pump&Dump

Dump&Pump ✅

Frontside

Backside ✅

4. THESIS:

Long: primary, considering the levels (low of the week, July low of the month, low of day), the signal three days breakout short traders in the market, and three session setup which it looks like setting for a long trade, I would be willing to expose risk in this trade after 9:45am PMI news release. Because of MRN, this market can potentially start a move back to the current HOW.

Short: secondary, this kind of signal not necessary lead to a reversal, I will leave the 3 session setup to drive this move.

Please note that the purpose of my analysis is to help me and you hunting the best trade setup for the day, none of my technical aspects are a way to forecast any directional market movement.

Gianni

GBP/USD Key Points

Tuesday’s UK Construction PMI came in above expectations at 55.3, the highest reading in more than two years

Time will tell whether traders are overly optimistic that the BOE will be able to cut rates relatively slower than its major rivals or whether more rate cuts still need to be discounted

GBP/USD’s bias remains to the downside and traders may look to sell this rally as long as rates remain below 1.2760 and the RSI holds below the 50 level.

In an eerily quiet week for UK economic data, GBP/USD has been taking its signal from developments elsewhere and general risk trends. The only notable data release this week was Tuesday’s Construction PMI, which came in above expectations at 55.3, the highest reading in more than two years.

Despite the strong reading (admittedly on a second- if not third-tier economic indicator), sterling has struggled to get into gear this week. Outside of the Swiss franc, the British pound is the weakest major currency since Sunday’s open.

This weakness has emerged despite the BOE being one of the least dovish major central banks looking forward. According to Bloomberg data, OIS traders are pricing in just 44bps of interest rate cuts from the Bank of England this year, or a bit below two 25bps rate cuts, compared to roughly 100bps (four 25bps rate cuts) and 68bps (almost three 25bps rate cuts) for the Fed and ECB respectively. Time will tell whether traders are overly optimistic that the BOE will be able to cut rates relatively slower than its major rivals or whether more rate cuts still need to be discounted, potentially keeping GBP/USD under pressure.

British Pound Technical Analysis – GBP/USD 4-Hour Chart

Turning our attention to the chart, GBP/USD remains in its 4-week bearish channel, despite the big rally during the first half of today’s US session.

One tool that traders can use to help handicap when a trend may break is the RSI indicator. In this case, the 14-period RSI on GBP/USD’s 4-hour chart has been stuck in a well-defined range between 30-50 since shortly after the bearish channel formed, signaling consistent, but not excessive, bearish momentum. Accordingly, bulls may want to watch to see if the RSI can break above the 50 level to either foreshadow or confirm a breakout in the exchange rate itself.

For now though, the bias remains to the downside and traders may look to sell this rally as long as rates remain below 1.2760 and the RSI holds below the 50 level.

-- Written by Matt Weller

#Bitcoin & The business cycle are intertwined!In the bottom pane is the US Purchasing managers index number

a number below 50 ( and nearly all the time below 47) means a recession/ economic slowdown is looming.

But as you can see on the rebound , as the PMI number moves above 50 and back into a expanding economy

we have seen it coincide with the great bitcoin bull markets.

Let's hope this trend continues.

USD/JPY – Surging yen improves to 15-week highThe Japanese yen continues to rally. USD/JPY is trading at 148.86 in the European session, down 0.31% on the day at the time of writing. On Thursday, the yen strengthened as much as 148.50, its best showing since May 11.

Only three weeks ago, the yen looked dead in the water. USD/JPY was trading just shy of 162, its highest level in almost four decades. Since then, the yen has been on an absolute tear, rising a staggering 7.9%, including 3.1% this week.

What is driving the yen’s spectacular turnaround? First, the Bank of Japan raised interest rates this week to 0.25%. Although rates remain at low levels, this rate increase, the second since March, indicates that the BoJ is slowly making the shift to normalization after decades of an ultra-loose accommodative policy.

The BoJ also announced it would taper its bond purchases, which is another tightening step.

Second, investors have become less enthusiastic about the US dollar now that a September cut is looking very likely and are looking to park their assets elsewhere.

The US economy is showing some signs of weakness, such as this week’s ISM manufacturing PMI for July, which posted the sharpest contraction since November 2023. This has driven funds away from the US dollar towards safe-haven assets such as the yen. Today’s nonfarm payrolls are expected to fall from 206 thousand to 175 thousand, which could further boost the yen at the expense of the US dollar.

This week’s BoJ rate hike showed that change is afoot in Japan and the government’s annual white paper on economic and fiscal policy, which was released today, supported that view. The white paper said that Japan was showing signs of breaking out of deflation, noting that businesses were now passing on costs to consumers due to increased costs from the yen’s sharp decline.

.

USD/JPY continues to break below support levels. Earlier, it pushed below support at 149.19 and is testing support at 148.72. Below, there is support at 149.59

150.03 and 150.44 are the next resistance lines

EURUSD: IntradayDear traders!

A mid-term channel is clear in the chart.

A short-term channel is also there! Any breaking below the bottom of short-term channel is hunting liquidity as long as we are perfectly over the zone!

Any breaks below the zone alter the bearish scenario! Remember that Final Manufacturing PMI release if USA could change the market direction.

DXY Flagging Down 103 Soon?!Here I have DXY on the 4Hr Chart!

Price has been in quite a Downtrend since the High @ 106.517 and now with the appearance of what seems to be a BEARISH BREAK of an ASCENDING CHANNEL which if we get a VALID BREAK and CLOSE out of this Channel .. This is signs of a Strong Continuation pattern, the BEAR FLAG!

The Big Push behind this weakness comes in with the disappointing ISM Manufacturing PMI's showing quite a bit of Contraction!

Final ISM Manufacturing PMI - 51.3 Actual v 50.9 Forecast

ISM Manufacturing PMI - 48.7 Actual v 49.8 Forecast

ISM Manufacturing Prices - 57 Actual v 60 Forecast

*To Validate this Pattern, we need to see a STRONG CLOSE outside with a SOFT RETEST of the Break!

Strifor || SILVER-23/05/2024Preferred direction: BUY

Comment: After yet another historical and local record for metals , this market began to correct faster than currency pairs. In silver , in particular, we have recorded a local maximum and are now confidently moving towards the support level of 29.77800 . Near this level, we consider long according to scenario №1 , taking into account the context. We also do not exclude scenario №2 , which involves buying at the 29.00 level. In both cases, we do not consider the target above the level of 31.80 , where this correction started.

Additional comments on this trade will be provided as situation changes. Follow us!

Thank you for like and share your views!

Strifor || AUDUSD-23/05/2024Preferred direction: SELL

Comment: We did not see another short-term growth in the Australian dollar , as a result of which we had to abandon this idea, and today it is most likely better to consider this instrument more from the seller’s point of view. The most likely maneuver in favor of the seller will most likely develop from the level of 0.66460 , which will most likely become resistance again (scenario №1) . However, a close above this level, especially on the daily chart, will immediately restore confidence in buying, and selling will have to wait.

Scenario №2 is more conservative, according to which you should look for a sale near the level of 0.67500 , after updating the local maximum.

Additional comments on this trade will be provided as situation changes. Follow us!

Thank you for like and share your views!

Macro Monday 45~The China Caixin PMI (Manu, Serv & Composite)Macro Monday 45

The China Caixin PMI

(Services and Composite released Today Monday)

Last week week we looked at the China Caixin Manufacturing PMI which will revise today with its updated readings that were released last Tuesday.

We will also look at the China Caixin Services PMI and the Caixin Composite PMI (a combination of the Services and Manufacturing PMI's) as these will both be released later today.

1.Manufacturing PMI – Already released

2. Services PMI – Released Today 6th May 2024

3. Composite PMI Released Today 6th May 2024 (both 1 + 2 combined)

What is the Caixin PMI?

▫️ The is an S&P Global report released monthly.

▫️ The Caixin PMI focuses on small & medium sized enterprises (SME’s) in China.

▫️ Surveys a small sample size of 650 private and state owned manufacturers and service providers.

Why Focus on China PMI's?

China, the 2nd largest economy in the world at approx. $18 trillion is often referred to as the world’s manufacturing superpower. In 2019, the Chinese manufacturing sector contributed nearly $4 trillion towards the country’s total economic output. Manufacturing accounted for almost 30% of China’s GDP during 2019 demonstrating the importance of manufacturing and the surveys completed by the manufacturers through the Purchaser Managers Index (PMI) surveys. Incredibly, in 2023 China’s manufacturing continued to increase and contributed 31.7% to China GDP, furthermore China’s exports reached record highs of $3.36 trillion. For a country that gets a lot of bad economic press, the economic data from manufacturing and exports suggests China is adaptable and is currently in expansionary territory. This will be further evident from the PMI charts we are about to review also.

Like most PMI’s the data will generally be derived from the following sub indicies; New Orders, Output, Employment, Supplier Deliveries and Inventories.

Reading both PMI’s:

>50 indicates expansion in the manufacturing sector compared to the previous month.

< 50 represents contraction

A reading of 50 indicates no change.

The Charts

China Caixin Manufacturing PMI - APR 2024

✅51.4 = Expansionary (>50 is expansionary)

▫️ Increased from 50.9 in Feb 2024 to 51.1 in Mar 2024

▫️ Increased from 51.1 in Mar 2024 to 51.4 in Apr 2024 – Figures for April were released on the 30th April 2024 (last week).

✅The Caixin Manufacturing PMI has remained expansionary for 6 consecutive (Nov 2023 – Apr 2024). It has been on a long term recovery since the Feb 2020 lows of 40.3, since then making a series of higher lows and recently sustaining 6 months of expansionary readings.

China Caixin Services PMI - Mar 2024

✅52.7 = Expansionary (>50 is expansionary)

⏳ April Figures released today (pending)

▫️ Increased from 50.2 in Sept 2023 to 52.7 in Mar 2024

▫️ Increase/decrease from 52.7 in Mar 2024 to ??? in Apr 2024 – Figures for April are released on today Monday 6th April 2024.

✅The Caixin Services PMI has remained expansionary for 15 consecutive months (Jan 2023 – Mar 2024). It has been on a long term recovery since the Feb 2020 lows of 26.5 when services took a huge hit during COVID-19 lockdowns, since then making a series of higher lows and recently sustaining 15 months of expansionary readings.

China Caixin COMPOSITE PMI - Mar 2024

✅52.7 = Expansionary (>50 is expansionary)

⏳ April Figures released today (pending)

THIS IS THE SUBJECT CHART AT OUTSET

▫️ Increased from 50 in Oct 2023 to 52.7 in Mar 2024

▫️ Increase/decrease from 52.7 in Mar 2024 to ??? in Apr 2024 – Figures for April are released on today Monday 6th April 2024.

✅The Caixin Composite PMI has remained expansionary for 5 consecutive months (Nov 2023 – Mar 2024). It has been on a long term recovery since the Feb 2020 similar to Manufacturing and Services PMI charts above. Looking at the composite chart, one can see that we moving sideways since Dec 2023 (Dec 52.6, Jan 52.5, Feb 52.5 & Mar 52.7). We are comfortably in the expansionary green zone on the composite.

In Summary

(subject to tomorrow’s readings for the Services and Composite PMI but we assume expansionary)

China Caixin Manufacturing PM I

↗️ Expansionary

The Caixin Manufacturing PMI for April 2024 rose to 51.4, marking the sixth straight month of expansion and the fastest growth since February 2023

China Caixin Services PMI

↗️ Expansionary

As of March 2024, the Caixin Services PMI increased slightly to 52.7, indicating growth in the services sector for the 15th consecutive month

(April 2024 Figures Release Today)

China Caixin COMPOSITE PMI

↗️ Expansionary

The Composite PMI reached 52.7 in March 2023, the highest since May 2023, showing the fifth consecutive month of growth in overall private sector activity.

(April 2024 Figures Release Today)

All the above readings suggest a continued expansion across China’s services and manufacturing sectors, reflecting improvements in demand and business activity across the SME cohort.

All these charts are available on my Tradingview Page and you can go to them at any stage over the next 5 - 10 years press play and you'll get the chart updated with the easy visual guide I provided. I hope its helpful

Lets get after it again this week 💪🏻

PUKA

Gold Long PositionI'm going to take this long position as it's closed higher than my key level and I see a nice bottom wick.

I expect Final Manufacturing PMI and ISM Manufacturing PMI to higher the Gold up to my TP point, then see a correction!

Let's see

GBPUSD Short Fundamental + Technical AnalyzeFundamentals : This weeks GBP PMI coupled with USD Unemployment claims and Core PCE has sent the Dollar rallying while GBP has been in some consolidation until today.

Technical : From a Technical point GBP broke the Bearish Trendline at the same time the Dollar was rallying from news, GBP later retraced some of the sell off and retested the Bearish Trendline it broke earlier which is where the short opportunity become available. Target around a 1% move or check to see when the Dollar takes out its high around 106.5

Macro Monday 44~China NBS PMI & Manufacturing Caixin PMIMacro Monday 44

The China NBS PMI and Manufacturing Caixin PMI

(both released Tuesday 30th April 2024)

China NBS General PMI – Surveys by 3,200 large corporations

▫️ Provided by the National Bureau of Labor Statistics

▫️ Based on a large sample size surveying 3,200 companies across China.

▫️ The NBS PMI has a stronger focus on larger state-owned firms.

▫️ Recently increased from 50.9 in Feb 2024 to 52.7 in Mar 2024 (>50 = Expansionary)

China Manufacturing Caixin PMI – Surveys by 650 SME’s

▫️ The is an S&P Global report released monthly.

▫️ The Caixin PMI focuses on small & medium sized enterprises (SME’s) in China.

▫️ Surveys a smaller sample size of 650 private and state owned manufacturers.

▫️ Recently increased from 50.9 in Feb 2024 to 51.1 in Mar 2024 (>50 = Expansionary)

N.B: The China Services Caixin PMI will be released Monday 6th May which when combined with the China Manufacturing Caixin PMI will form the all encompassing China Caixin Composite PMI. We will cover the China Services and Composite PMI next week on Monday 6th May 2024.

Both the Manufacturing Caixin PMI and the China NBS General PMI are of companies that are mostly export-orientated & located along China’s Costal Regions. These are the manufacturing and export hubs of China, the likes of major coastal regions such as Guangdong, Zhejiang, and Shanghai which have strategic access to ports and shipping routes.

China, the 2nd largest economy in the world at approx. $18 trillion is often referred to as the world’s manufacturing superpower. In 2019, the Chinese manufacturing sector contributed nearly $4 trillion towards the country’s total economic output.

Manufacturing accounted for almost 30% of China’s GDP during 2019 demonstrating the importance of manufacturing and the surveys completed by the manufacturers through the Purchaser Managers Index (PMI) surveys. Incredibly, in 2023 China’s manufacturing continued to increase and contributed 31.7% to China GDP, furthermore China’s exports reached record highs of $3.36 trillion in 2023.

For a country that gets a lot of bad economic press, the economic data from manufacturing and exports suggests China is adaptable and is currently in expansionary territory. This will be further evident from both the PMI charts we are about to review below.

Like most PMI’s the data will generally be derived from the following sub indices; New Orders, Output, Employment, Supplier Deliveries and Inventories.

Reading both PMI’s:

>50 indicates expansion in the manufacturing sector compared to the previous month.

< 50 represents contraction

A reading of 50 indicates no change.

The Charts

China NBS General PMI – Surveys from 3,200 large corporations (subject chart above)

▫️ After hitting an all time low of 28.9 in Feb 2020 from the COVID-19 pandemic, China’s NBS General PMI has experienced significant fluctuations.

▫️ The NBS PMI made two subsequent significant lows in Apr and Dec 2022 at approx. 42.6.

▫️ By March 2023, the PMI reached an all-time high of 57.0, indicating strong expansion in both manufacturing and non-manufacturing sectors.

▫️ This fell to a low of 50.3 in Dec 2023, and since then we have risen to 52.7 in Mar 2023.

🚨 Next release for April is released this Tuesday 30thApril 2024.

China Manufacturing Caixin PMI – Surverys from 650 SME’s

▫️ The China Manufacturing Caixin PMI for smaller SME’s has demonstrated a series of higher lows since February 2020 demonstrating a strong recovery out of the COVID-19 pandemic.

▫️ Momentarily reaching all time highs of 54.9 Nov 2020, thereafter falling significantly to 46 in April 2022, since then the Manufacturing Caixin has pressed into expansionary territory of 51.1 (March 2024).

▫️ This was the fifth straight month of growth in factory activity and the fastest pace since February 2023, boosted by higher new orders from domestic and abroad, with foreign sales rising the most in a year while output climbed the most since last May.

🚨 Next release for April is released this Tuesday 30thApril 2024.

Both PMI's are in expansionary territory which is positive news for China production and exports. SME's appear to have made a more gradual and measured recovery in the Caixin PMI versus the volatile nature of the large corporations in the NBS PMI. Regardless both are swinging higher towards 52 or 53 placing them in the expansionary mode.

Potential Trade Set Up

On a separate note, adding to China's expansionary potential from above economic data and the PMI charts, one of the worlds greatest traders Peter Brandt

@PeterLBrandt

recently posted a potential buy signal one of Chinas main indexes, the Heng Seng Index which looks to have formed a Head and Shoulders bottom with a recent break out (see most recent post under this one).

The Heng Seng Index (HSI) serves as a great proxy for Asian markets, its the main indicator of the overall market performance in Hong Kong and includes 82 constituent companies, representing about 60% of the total capitalization of the Hong Kong Stock Exchange. The companies in the HSI are considered blue chips and thus the index operates a good basal gauge of market sentiment in China. Definitely a chart to add to your arsenal for Asian markets.

All these charts are available on my Tradingview Page and you can go to them at any stage over the next 5 - 10 years press play and you'll get the chart updated with the easy visual guide I provided. I hope its helpful

Lets get after this week 💪🏻

PUKA

Macro Monday 43 - Japan Composite PMI Macro Monday 43

Japan Composite PMI – Japan’s Business Activity

(Flash PMI is released Tuesday 23rd April 2024)

Unfortunately, I had great difficulty in locating the Japan Composite Flash PMI in chart form on TradingView (it appears to not be available).

Instead we will briefly cover the Japan Composite PMI chart which is the final PMI released later on Tuesday 7th May 2024 (for April). We can review the Flash PMI figures that are released tomorrow regardless for an indication. The flash consists of about 90% of the final PMI input thus is a good forward view on how the final PMI will come in on the 7th May 2024.

Over the past three weeks we have covered the following three indicators for Japan:

1.Macro Monday 41 - Japan Consumer Confidence Index (CCI)

🚨 Pessimistic but with an improving long term trend. A positive ranging move from 28.6 in Nov 2022 to 39.5 in April 2024. This is the highest reading in c. 5 years, a significant milestone and trend higher. A move above 40.86 would signify a move above the historical average level of consumer sentiment (less pessimistic, as only above 50 it optimistic).

2. Macro Monday 42 - Japan Reuters Tankan Index (RTI)

✅ Business Optimism is high with the Japan Reuters Tankan Index standing at +9, down from the previous month's 10 however firmly in the positive (above zero).

3. Macro Monday 43 - Japan Composite PMI

✅ THIS WEEK we take a quick look at the Japan Composite PMI which is firmly in the positive at 51.7 (above 50 is expansionary and below 50 is contractionary).

As you can see from the chart below we have been in an uptrend since Nov 2023

The Japan Composite PMI for March 2024 was 51.7, indicating continued expansion in private sector activity (businesses). This matches the optimistic business sentiment in the Japan Reuters Tankan Index. This marked the third consecutive month of growth and the strongest pace since late September in PMI. The service sector saw solid expansion, while the decline in manufacturing production softened slightly. New orders accelerated to a seven-month peak, primarily led by the service economy. Employment growth was the steepest since May 2023, and there was a marginal rise in outstanding business. Input prices expanded robustly, leading businesses to increase their selling prices at the most pronounced rate for seven months. Overall, the PMI provides insight into the health of Japan’s private sector economy

The overview of the past three weeks we covered and what they broadly tell us? 👇🏻

Japan Businesses are in expansion and optimistic whilst the Japanese Consumer remains reserved

In contrast to the positive Business Sentiment and Business Activity in Japan, the Japanese consumer is not as optimistic and appears to be trailing business behind sentiment(RTI) and activity (PMI). The Japan Consumer Confidence Index (CCI) came in at 39.5 for March. Whilst this was the highest reading in 5 years for the Japan CCI and demonstrated a trending recovery from lows of 28.6 in Nov 2022, the Japan CCI remains below its historical average level of 40.86. Despite a sizable recovery since Nov 2022, the current 39.5 suggests the Japanese Consumer is still more pessimistic than the historical average.

Whats the Japan PMI made up of?

The Japan Composite PMI is a weighted average of several key components that provide insight into the health of the private sector economy.

Here are the main components :

New Orders (30%): Measures the volume of new orders received by businesses. An increase in new orders suggests growing demand and potential future production.

Output (25%): Reflects the level of production or business activity. Higher output indicates expansion, while lower output signals contraction.

Employment (20%): Tracks changes in employment levels. A rising employment index indicates job creation and economic growth.

Suppliers’ Delivery Times (15%): Monitors the time it takes for suppliers to deliver goods or services. Longer delivery times may indicate supply chain disruptions.

Stocks of Purchases (10%): Measures inventory levels. An increase in stocks suggests businesses are building up inventories, while a decrease may indicate reduced demand.

The above components collectively provide a comprehensive view of economic conditions in Japan’s private sector

How to read the PMI chart

The Composite PMI varies between 0 and 100, with a reading above 50 indicating overall growth compared to the previous month, and below 50 indicating contraction.

PUKA

DXY update before PMI price is near the resistance 0f 104.750 >> 104.800 >> 105

now the question whether the price sweep or run through this liquidity ???

as price has made higher high and higher lows with recent bos we are looking to buy instead of going short

during the impulsive momentum candle price has left behind some bullish fvg which are pending below at the level of 103.700 level before this we have higher low (this higher low could be the liquidity

before 103,700 i dont see any major fvg or ob as of 4h time frame

price currently going all time high which need to take a pullback to fuel the upside move again

the candle formed since 27th march are mostly sideways following a trending which is another area of liquidity laying below it

Macro Monday 40 - Euro Area Composite PMI Macro Monday 40

Euro Area Composite PMI

(Released this Thurs 4thApril 2024)

The Euro Area Composite PMI (Purchasing Managers’ Index) is a significant coincident economic indicator that provides insights into the current overall health of the eurozone economy.

The Euro Area Composite PMI data is collected from a representative panel of around 5,000 manufacturing and services firms around the EU and then a weighted average of the two is provided to create the composite reading.

This index tracks variables such as sales, new orders, employment, inventories, and prices. Very similar to the US PMI that we previously covered.

The Chart

The chart illustrates the following metrics;

🟢Manufacturing PMI (green line)

🔴Services PMI (red line)

🔵Overall composite PMI (Thick Blue Line)

The green zone (>50) illustrates the economic expansion zone and the red area illustrates the economic contraction zone (<50). The 50 level itself is neutral.

Now, let’s very briefly cover the last three weeks of Macro Mondays No. 38, 39 & todays 40. These all featured the Eurozone economic health and can be valuable metrics to remain informed on. With a click of my charts in trading view you can remain updates with a visual easy on the eye.

EU Current Sentiment Outlook

(negative but improving)

1.The Euro Area Economic Sentiment Index is based on current sentiment surveys from EU Businesses and consumers for all 27 EU Member States.

-The current economic outlook as distinguished by businesses and consumers in the EU is currently below average at 96.3 (<100 is below average and >100 is above average).

- We have seen an improvement since Sept 2023 with an increase from 93.4 to 96.3 at present but remain in the negative.

EU Forward Looking Sentiment

(Firmly Positive)

2.The Euro Area ZEW Economic Index is a 6 month forward looking economists outlook for 20 of the 27 Euro Member states.

-The ZEW Index is anticipating optimistic economic conditions for the coming 6 months with a current reading of 33.5 which is well above the historical average of 21.39 on the chart. Economists in then EU see things improving over the coming two quarters.

EU Manufacturing and Services current performance composite

(Neutral - leaning negative)

3.Featured today, the Euro Area Composite PMI is a coincident indicator offering real-time health of the Eurozone economy through data collected from manufacturing and services firms.

-The Euro Area Composite PMI is currently close to neutral at 49.9 (just under the neutral 50 line) demonstrating that over the recent month we have been in marginal contraction in the EU according to the manufacturing/services composite.

- However, if we look at the individual Manufacturing PMI we can clearly see we are in negative/contractionary territory at 45.7 (green line) whilst the services PMI is rising into expansionary territory at 51.1 (red line). This is common theme in the US PMI at present also with services performing better than manufacturing sector.

The beauty of these charts is that you can go onto my TradingView Page and press update, and the chart will update you with all these metrics, informing you at a glance with how these metrics are performing collectively with a nice visual guide.

Thanks again for coming along and I hope this additional Eurozone chart helps you in your current and future understandings of EU Economic Sentiment, Forward looking economists sentiment and how manufacturing and services firms are feeling overall.

Bottom line is, economic sentiment appears to be leaning optimistic for the immediate future, however we await more readings for a conclusive trend direction from the coincident indicators, the ZEW Index and the Euro Area PMI index.

PUKA

Macro Monday 39 - Euro Area Economic Sentiment Indicator (ESI)Macro Monday 39

Euro Area Economic Sentiment Indicator

(Next Release is this Wednesday 27th March 2024)

Last week we covered the the Euro Area ZEW Economic Sentiment Index (the "ZEW Index") and learned that the sentiment data for the ZEW Index comes from 350 economists spanning the Euro Area (20 of the 27 EU member states that use the Euro currency). The ZEW Index attempts to provide a sentiment lead with economists factoring in their 6 month forward projections into the sentiment data.

This week we look at a different more current sentiment indicator, the Euro Area Economic Sentiment Indicator (ESI). The data for the ESI is derived from the businesses and consumers of all 27 EU Member States. The ESI therefore has a larger data set to the 20 countries covered in the ZEW Index. The ESI is closer to the truth of what businesses and consumers are currently experiencing on the ground across Europe. The ESI is not forward looking like the ZEW index, the ESI should be considered a coincident indicator presenting the current state of economic sentiment among businesses and consumers across the EU. In any event we can still use the ESI data and the chart to identify trends and to know where sentiment stands when it is released each month.

Interestingly, at present the ESI figure is more negative than the ZEW Index. The ZEW is in positive sentiment territory (forward looking) whilst the ESI is firmly in negative sentiment territory (current outlook). Based on each data sets objective, you would think that the ESI would move into positive territory over the coming 6 months based on the forward looking positive ZEW Index. No guarantees of course. We can watch this as it plays out in real time and see if the ESI follows the ZEW Index.

Lets have a closer look at the ESI

The Euro Area Economic Sentiment Indicator (ESI) is a measure created by the European Commission to gauge economic confidence across the Euro Area.

The survey data for the Economic Sentiment Indicator (ESI) is initially collected at the national level for each country within the Euro Area. These individual country results are then aggregated to create the overall ESI, which reflects the economic sentiment for the entire EU (all 27 countries). The data is also seasonally adjusted to account for regular seasonal variations and provide a clearer picture of the underlying economic trends.

The data is derived from survey responses from the following economic sectors in each country (with weightings);

1. Industry (40%)

2. Services (30%)

3. Consumers (20%)

4. Retail (5%)

5. Construction (5%)

Balances are constructed as the difference between the percentages of respondents giving positive and negative replies.

The ESI data is scaled to a long-term average of 100 with a standard deviation of 10. This means that the average sentiment over time is set at 100.

As the ESI’s scale centers around a mean of 100 values above this suggest higher-than-average confidence, while those below indicate lower confidence. It’s seasonally adjusted to reflect consistent economic trends.

The Chart (above subject chart)

The chart follows the structure discussed above and we have split the chart by color as follows:

>100 = Above Average Economic Sentiment🟢Green

<100 = Above Average Economic Sentiment🔴 Red

▫️ As you can see on the chart we made a record low in pessimism in May 2020 at 58.7 which was closely followed by a record high in optimism in Oct 2021 at 119.5.

▫️ The chart has arrows that are 17pts in length. You will see the arrows across the chart whereby if there was a greater than 17pt drop from the green zone into red the red zone, this historically has coincided with recession

▫️ The most recent drop from🟢119.5 in Oct 2021 to 🔴93.9 in Oct 2023 is a drop of 25.6pts, greater than the 17pt typical recession drop. "This time might be different" may actually apply because we had all time highs in sentiment in Oct 2021, however that does not detract from the fact we are currently firmly in negative economic sentiment sub 100 at 95.4.

▫️ You can see that any time we have fallen below the 85 level (red dotted line) we have confirmed a recession. This does not mean that you need a sub 84 reading for a recession, only that when this has occurred in the past, it only occurred during some of the deeper recessions.

A quick note on the Euro Area terminology as this was bugging me as the ESI covers all 27 EU member states

Euro Area Terminology?

The term “Euro Area Economic Sentiment Indicator” can be somewhat misleading because the ESI indeed covers all 27 EU Member States, not just those in the 20 in the Euro Area or Eurozone. The name likely persists because the ESI is particularly significant for the Euro Area, where economic policies are closely aligned and the shared currency means that economic sentiment has direct implications for monetary policy. However, the ESI’s broader EU-wide scope allows for a comprehensive view of economic sentiment across the entire European Union, which is valuable for comparative analysis and policy-making at the EU level.

Thank for coming along again, if you like the content and find it informative please let me know

PUKA

Macro Monday 34 ~ S&P PMI Composite FlashMacro Monday 34

S&P PMI Composite Flash

This S&P PMI “Flash” Composite is a very useful and relatively new data set made available since Nov 2013 that is particularly useful at providing an advance indication of the ISM Purchasing Managers Index (ISM PMI Index) which is released a week later.

We are aware from prior Macro Mondays that the ISM PMI index is based on data collected through surveys of over 800 companies in the U.S. and covers variables such as sales, new orders, employment, inventories and prices, all of which give us an indication of trends in the economy.

S&P Flash Composite Main Benefits

1. The term "Flash" in the name refers to the fact that it is a preliminary or early quick estimate of the ISM Purchasing Managers' Index (PMI) which is released later in the month. For example this month the S&P Flash Composite is released this week on Thursday 22nd Feb whilst the final ISM PMI reading is released Friday 1st March (both readings are for the month of Feb).

2. The S&P PMI Composite Flash is a “composite” insofar as it combines both the manufacturing and services sectors PMI’s into a single index. This provides a more comprehensive overview of economic activity compared to looking at either sector in isolation (however you can also view the flash PMI for Services and Manufacturing separately, these are released on the same day).

So the S&P PMI Composite Flash consists of two main components:

1. Manufacturing PMI: Measures economic activity in manufacturing.

2. Services PMI: Measures economic activity in the services sector.

Both components are based on surveys of purchasing managers and provide insights into factors like new orders, production, and employment. The Composite PMI combines these components to offer an overall picture of economic health, with readings above 50 indicating expansion and below 50 indicating contraction.

How do we get an advance “FLASH” PMI reading and how reliable is it?

The main difference between the data used in the S&P PMI Composite Flash and the final PMI figures lies in the sample size(smaller) and timing (earlier release with most recent data exclusion).

According to Investopedia and a report from S&P Global Flash (Jan 2023), the Flash Composite PMI release is based on about 85% of total PMI survey responses each month. Clearly, a significant portion of survey responses are included in the Flash PMI which would lead you to believe that its reliable early indicator but how reliable has it been historically?

In the aforementioned S&P Global Report it also provided the historical average difference between the flash and final PMI index values (final minus flash) since comparisons were first available, which are;

Composite Difference = 0.1

Manufacturing Difference = 0.0

Services Difference = 0.2

We can see that the Manufacturing Flash PMI release readings are the most reliable and that the Services Flash PMI is less reliable. Whilst both are not far off the mark, it’s a notable difference for services considering that services represents over 80% of Gross Domestic Product (GDP), thus small differences in services hold more weight. Regardless, we can be relatively satisfied that the S&P PMI Composite Flash Index is a very good and reliable early indicator of the Final ISM PMI. I will certainly be looking at this metric going forward so that I can have a great early indication of the ISM PMI.

When you review the chart of the Flash PMI with the Final PMI, you'll see that the difference appears greater than the marginal difference discussed above. This highlights, how on a chart, the difference a week or a weeks worth of data can make to how a chart appears (with the absent or included 15% of data). You will also notice that the Flash PMI is more volatile with higher and lower swings. It reminds me a little of the CPI headline vs CPI core chart in this respect, as both ultimately move in the same direction but one oscillates less than the other.

I hope the next Flash PMI released this Thursday 22nd Feb will help arm you with what is very reliable early indication of the ISM PMI (released a week later on the 1st March).

Thanks for coming along

PUKA

📊 Upcoming PMI Report Analysis 📈PMI Report Update

The PMI Services report is due out in approximately 2 hours. Last month, the index rose from 50.6% to 53.4%. This month, the forecast is slightly lower at 53%.

There is not a significant difference between the actual figure from last month and the forecast. However, the key point is that the figure is above 50.

In general, a higher than expected reading is likely to lead to a rise in the dollar index, while a lower than expected reading is likely to lead to a fall in the dollar index.

If the actual figure is in line with the forecast or there is no significant difference from last month, we do not expect any major market reaction.

Additional Information:

The PMI (Purchasing Managers' Index) is a survey-based measure of economic activity.

A reading above 50 indicates expansion, while a reading below 50 indicates contraction.

The PMI Services report focuses on the services sector of the economy.

The services sector is the largest sector of the economy in most developed countries.

__________

This information is provided for general knowledge purposes only and should not be considered as investment advice. Please consult with a qualified financial advisor before making any investment decisions.

Macro Monday 13~Purchase Managers IndexMacro Monday 13

ISM Purchasing Managers Index

The ISM Purchasers Managers Index (PMI) measures month over month change in economic activity within the manufacturing sector.

The PMI is a survey-based indicator that is compiled and released each month by the Institute for Supply Management (ISM). The survey is sent to senior executives at more than 400 companies in 19 primary industries, which are weighted by their contribution to U.S. Gross Domestic Product (GDP).

A PMI above 50 represents an expansion in manufacturing when compared with the previous month. A PMI reading under 50 represents a contraction while a reading at 50 indicates no change. The further away from 50, the greater the level of change.

According to Investopedia "ISM data is considered to be a leading indicator of economic trends. Not only does the ISM Manufacturing Index report information on the prior two months, it outlines long-term trends that have been building over time based on prevailing economic conditions".

The ISM reports are released on the first business day of each month for the month that has previously closed. Thus, they are some of the earliest indicators of current economic activity that investors and business leaders get regularly. Something to look out for next Monday 2nd October 2023.

The PMI focuses mainly on the five major survey areas;

1. Employment (20%)

2. New orders (30%) Covered in Macro Monday 6

3. Production/Output (25%)

4. Inventory levels (10%)

5. Supplier deliveries (15%)

We covered the ISM New Orders Index in Macro Monday 6 as it is the largest component of the Purchaser Managers Index making up 30% of the overall index. I will leave a link to the chart.

The Chart

The chart outlines the last 12 recessions (shaded red zones) with the PMI readings over the same period. As we are already aware above 50 on the PMI reading is expansionary and below 50 is contractionary (red thick line).

Three Main Findings

1. In 11 out of 12 recessions a PMI reading at or below 42 was established. This means if the PMI falls to 42 there is a 92% probability of a recession. At present we have not reached that level, we are currently at 47.6.

2. The PMI has bottomed 10 out of 12 times in Quarter 1 (between Jan – March) with the remaining two bottoms happening in Quarter 2 (both in May). This means that 83% of the time the PMI cycle appears to bottom in Quarter 1 with the most bottoms in January (6) with Feb(2) and May(2) in close second place.

- It’s worth noting that the bottom of the PMI cycle

may not be the bottom of a stock market cycle. If

we are forward looking then a rising PMI is positive

for the economy and markets but ideally a move

above 50 is the true signal of economic expansion

from a manufacturing standpoint.

3. The average PMI bottom to bottom cycle timeframe over the past 6 cycles is 58 months with the shortest being 37 months and the longest being 86 months. We are currently at month 38 and the average month of 58 is Jan 2025 with the max of 86 months being May 2027.

- How interesting is it that both these potential PMI

bottom dates line up with our two most frequent

PMI bottom months indicated in point 2 (January

and May).

- Interestingly according to U.S. government

research, since WWII the business cycle in America

takes, on average, around 5.5 years which closely

aligns with our 58 month (or roughly 5 year)

indication for the PMI chart. The business cycle

incorporates an aggregate of economic data such

as the ISM data, GDP and income/employment

metrics. We might cover the business cycle in more

detail on a future Macro Monday.

The ISM New Orders Index (30% of the PMI)

Similar to the ISM New Orders Index Chart (covered in Macro Monday 6) which makes up 30% of the PMI, we have not reached below the 42 level on this chart either which has provided a 100% confirmation of recession when we have had a definitive move below the 42 level historically.

For ISM New Orders if we stay below a sub 50 level on the ISM New Orders Chart for greater than 7 months it has resulted in a recession every time except for 1966 and 1995 (8 out of 10 times). We are currently 14 months below the 50 level which is unprecedented, with the new orders index nudging a little lower on the August reading from 47.3 down to 46.8.

ISM Data Release 2nd October 2023

When we receive our next ISM Data release next Monday 2nd October 2023 we can refer back to the PMI chart and the New Orders Index Chart and see how things have progressed and if we have reached and critical levels.

These charts and the others I have completed on Macro Mondays are all designed so that you can revisit them at any point and press play on TradingView and see if we are breaking new into higher or lower risk territory.

I hope they all help towards your investing and trading decisions.

Have a great Monday guys, Lets get after it!

PUKA