ISM vs SPX yoy divergence signals more downside comingBig ISM decline with SPX divergence is signaling more SPX downside is likely in coming months

PMI

China problems, Central Banks & euro riseThis week begins to give a first idea of the economic consequences of the epidemic (so far in the context of China). We are talking about the manufacturing PMI index for China, which fell to 35.7 in February (compared to 50 in January). The non-manufacturing index came out even worse, showing a value of 29.6 (the lowest in history). Recall that any value below 50 indicates a decrease in economic activity. And this is only the first swallow. Then there will be new indicators, and each of them will plunge financial markets into an ever greater depression, at least for some time.

Meanwhile, in China itself, the epidemic continues to decline rapidly. In Wuhan (the epicenter of the epidemic), they even began to close the first temporary hospitals due to the lack of patients. But the relay race in China is confidently intercepted by the world as a whole. South Korea, Italy, Iran - current epicenters, which are also not localized, but, on the contrary, spread the virus to other countries. If we draw an analogy with China, then at best for the next month we will find exclusively disappointing news. So you should not count on something good from March.

Accordingly, the outcome from risky assets is likely to continue, respectively, gold and other safe-haven assets will find fundamental support. This week we will continue to use the bundle of buying gold - buying USDJPY as a promising medium-term position. In our opinion, the strengthening of the yen, if it continues, will be limited, but the opportunities for gold growth look much more extensive in this regard. Our disbelief in the significant strengthening of the yen is due to the fact that Japan is experiencing serious economic difficulties and traditionally one of the components of the equation to solve them was the devaluation of the yen, so the Bank of Japan is either around 107 or about 105, but most likely it will intervene and prevent the yen from strengthening.

In general, central banks are again in the spotlight. Everyone expects salvation from them. As it was during the crisis of 2007-2009. So far, they live up to expectations, since all key central banks have noted rather aggressive statements about their readiness to act.

Markets traditionally focus on the Fed. This is mainly due to the current difficulties of the dollar and the frank success of the EURUSD pair. With each new hundred growth points of EURUSD, our desire to sell a pair grows stronger, as does our desire to increase transaction volumes for sale.

Part of the dollar’s problems lies in the plane of the presidential election. We try to minimize the analysis of the political plane, focusing on the economy. But today is the so-called Super Tuesday. The day when 1344 of the 1991 Democratic Party delegates cast their ballots for a particular candidate. So far, Sanders is the undisputed leader (probability of victory = 57%), but Biden still has chances (probability of victory = 31%). So the day for the US political sphere is very significant.

The pound was under pressure yesterday due to the negotiation process between the UK and the EU on a trade agreement. There is already a familiar game of tug of war and trade for the best conditions, tied to mutual threats. As in the case of Brexit, we prefer to see not the current noise, but the perspective. And it is such that the parties are likely to agree in one form or another.

Accordingly, the pound will receive its positive sooner or later. So in the medium term, we do not see any problems for medium-term purchases of the British pound. Rather, on the contrary, we see good shopping opportunities. In current conditions, sales of the EURGBP pair seem ideal to us.

Time for a China bear play after PMI printThe YANG China Bear fund should gain this week after an extremely bad print on China's manufacturing PMI, which came in 22% worse than expected over the weekend. China has been claiming economic recovery-- they say 90% of their state-run firms are back in business-- but the numbers belie those claims. Also go check out a BBC article titled "Coronavirus: Nasa images show China pollution clear amid slowdown" to see breathtaking photographic evidence of how the Chinese economy has ground to a halt. Markets are only just beginning to appreciate the scale of the economic impact of this thing. It's going to be bad.

China is slowing down, the US homes sales are growingYesterday was notable for the fact that for the first time in an epidemic, the number of new cases in China was lower than in the rest of the world. On the one hand, this indicates a reduction in the epidemic in China, and on the other, the continuation of the deterioration of the situation in the world. Since the situation with the epidemic in China is improving quite rapidly, we can begin to summarize its preliminary results. And although it’s too early to talk about specifics, some estimates can be obtained already here and now.

These are the so-called early response indicators. For example, Bloomberg calculates 8 early response indicators for China. So 5 out of 8 in February decreased. But this is not the worst. The February indicators of business confidence fell to the lowest values in the history of observations. Business can be understood: the sales of new cars and real estate in China fell by more than 90%.

Bloomberg data is also confirmed by a monthly study of the health of small and medium enterprises in China. The results are record low in the history of such studies.

As for the more classical metrics, it is expected that China's GDP growth will decline to the lowest levels since 1990. Goldman Sachs, for example, expects China's GDP growth in the first quarter by only 2.5%.

A sharp slowdown in the economy is frightening not only by the fact of the slowdown but also by the problems that it carries: rising unemployment, increasing bad debts, increasing bankruptcies, falling financial results of companies, decreasing domestic demand, etc.

Speaking of official statistics, the first signals will appear on February 29, when the February PMI for China will be published. As expected, it will fall to the lowest levels since the global financial crisis (while some experts predict even lower values).

Yesterday's data on sales of new homes in the USA looked rather provocative against this background: in January they grew by +7.9% to 764,000 with a forecast of +3.5% to 718,000. However, we will see what will happen there in February, especially in light of the Center’s warning the United States Disease Control and Prevention Regarding the threat of a possible spread of the virus throughout the United States.

In general, the situation continues to be tense and for any positive, whether it is a decrease in the number of patients or the development of a vaccine, there is a negative right there (problems in the economy of China and the world, the spread of the epidemic, sales on stock markets, etc.). Accordingly, we do not see any reason to radically change anything in the trading plan.

So today we are looking for points for buying gold (but we are careful - we buy on the slopes with mandatory stops), we sell oil, we sell EURUSD, we buy GBPUSD, we sell USDJPY with small stops.

Does SPX vs PMI divergence signal upcoming recession? No, not really. Only 3 of 7 divergences signaled recessions in the last 50 years. Besides, some recessions did not have any divergence.

So data doesn't support the recession is coming thesis.

Red flag -> Divergence with recession following

Green flag -> Divergence w/o recession

? -> No divergence signal before recession

(This post is in response to some comments I received)

SPX performance vs PMI diverging significantly SPX yoy performance vs PMI Manufacturing index

Tried to replicate TeddyVallee's chart w/o z-scores he published on Twitter

Big divergences I could find are marked with flags. I may be missing a few so make your own decisions

Looks like when PMI and SPX diverged, most of the time SPX was correct!

Could it be that stocks are the first to feel the liquidity flood which then lifts the PMI?

My bet is even if there is a pull back, uptrend should continue and PMI should bounce next

SPX v PMI Pmi remains in contraction , the chart highlights simply , the discord between a leading economic indicator and Indices Price.

Europe is “disappointing”, we trade with oscillatorsMonday turned out to be a relatively calm day for the foreign exchange market. The euro and the pound could not reach Friday's peaks, due to the weak macroeconomic statistics.

For example, in Germany, the PMI in the manufacturing sector fell to its lowest level in the last couple of months and amounted to 43.4. This confirms that the largest eurozone economy is experiencing serious problems. Recall, any index value below 50 means that activity in the manufacturing sector is declining.

Germany is not an exception. Weak data came from both France and the UK. According to PMI, manufacturing activity in Britain is at its lowest level over the last 7 years. The PMI in the manufacturing sector in the UK came out at 47.4 pips (analysts expected 49.2).

In general, the lack of growth of the euro and the pound against the background of such data is quite logical.

On the other hand, this is not a reason to refuse to buy EURUSD and GBPUSD. All we need is statistics on industrial production in the United States come out weak. Well, for the pound it would be nice if the data on the labour market did not disappoint.

In general, today we are not expecting any revelations and strong directional movements. In our opinion, the best trading tactics for today is oscillatory trading. So we trade with RSI or Stochastic or you can choose another one.

Once again, we draw attention on extremely attractive positions for sales of the Russian ruble.

EURUSD potential H&S patternAfter Brexit vote and a spike in EUR, we retraced the move the next day. Now seems like a H&S is forming with divergence. Proper support in terms of the trend line 200SMA and 1.11 area. Elliott waves suggest the final leg of retracement in wave (c).

PMI data coming in this morning from Europe this morning. Negative numbers would give more probability to this trade. 1st confirmation is the close of the nice bearish candle on 1 hour. 2nd at the test of support and break.

Good Luck and have a great trading week!

Could EUR break the current range today?From technical perspective, the pair is stuck in the 1.1100 - 1.1050 range. And we'll need to see a sharp breakouth in any direction to give us more clarity in the medium-term. For now, while the Dollar index is bullish in the medium-term, we can expect the euro to fall below 1.1050.

Additionally, ECB President Lagarde will make her first major speech later today. If Lagarde uses today's speech as an opportunity to clarify her position on easing, we will see a strong reaction in EUR. A dovish prospects can push EUR/USD lower to 1.10, especially if that will be supported by weaker PMIs. More optimistic bias, on the other hand, could raise the euro to a 2-week high above $ 1.11. Outside of this, a positive surprise on PMIs will indicate that the European manufacturing malaise is bottoming and this will helps EUR/USD and German 10-years yields push higher. Further key resistance is 200-day SMA around 1.1175 (Nov. high).

Either way, there appears scope for an uptick in EURUSD volatility. Our strategy is for trading in the range - Buy on the top limit and Sell on the bottom border with tight Stop-Losses above 1.1100 for the Sell position and bellow 1.1025 for the Buy.

What do you think?

Why buying EURUSD is a great chanceLooking at the EURUSD daily chart, it clearly shows that it has come to a very important support level. That is a great reason for its purchasing. The stops are relatively small - about 30-40 points, and the profits, in this case, are about 100 points (the nearest strong resistance is located in the region of 1.1160). That is, purely technically, taking into account adequate money management (the profit margin is 2.5 times higher than the stop value), so that is a nice opportunity for earning.

The fundamental background is the only thing that can negatively influence. In our opinion, the situation with the euro does not look hopeless and the chances of supporting 1.1060 are quite large.

The Eurozone economy is experiencing tough times. However, yesterday's data on retail sales and business activity in the Eurozone came out better than expected, which is more important that the indicators showed a positive trend: retail sales grew by + 0.1% with a forecast 0%, and the composite PMI index was 50.6 with a forecast 50.2 ( the value of the indicator above 50 indicates an increase in economic and business activity). Against the background of rather weak data, these signals have been extremely positive.

Leaving the EU without a deal option is eliminated from the agenda. which is great news for the euro. Against this background, the pound rose by 1000 points. And the euro added only 100-200 points, it means that the euro did not worked out yet. Why should the euro grow because of the information that the “hard” Brexit will not take place? The fact is that Britain’s exit from the EU without a deal is not only about losses for the UK but also multibillion-dollar losses for the Eurozone economy, therefore potentially serious problems for the euro. So the removal of this issue from the agenda is a positive signal in favour of purchases of the euro. Its descent below 1.10 was an attempt to discount under exit without a deal. And since it does not take place, then the euro should return to its original position, to grow.

Trade war escalation between the US and the EU is delayed while approaching the end of trade wars between the US and China. For the euro, this is a positive signal. Let us explain: the locomotive of the Eurozone economy is Germany.

The German economy is export-dependent, that is, its success/failure is determined by the state of global markets, primarily China. The end of the trade wars between the United States and China will give a powerful impetus to the return of the world economy to the normal statement and one of the first to benefit from this will be Germany. In turn, improving the state of the German economy is improving the state of the Eurozone as a whole. And this is will reflect positively on the euro.

So, we do not see serious threats to the euro at the moment. Rather, on the contrary, there are good opportunities for buying exceptionally cheap euros.

S&P500 gains despite economic data worsening S&P500 reaches a new ATH. However ISM/PMI Data out of the US speak a different language. After we have already witnessed a global slowing and contracting of the economy with many countries having PMIs under the 50 level for quite some time now, the US has now followed this trend that has been going on for over a year. PMIs again came in lower today and under the important 50 mark, which means in the contracting area. We have now 3 readings in the PMIs under 50 over the last 3 months, signaling that the situation is not just a statistical outsider but a trend. I am expecting the US market (S&P500) despite worsening data still to reach potentially the 3200 level. However these gains are driven mainly be the expectations that the FED can turn things around like always. Should we reach the 3200 level and economic data has not been improving until then, I am expecting a bigger 3 Wave correction to start from there, potentially even a correction that could be correcting the bull market which has startet in the year of 2009, this could happen if despite FED interventions the Economic Data doesn't improve. Hence expect a correction from the 3200 level, the size of the correction then will be unfold on weather the FEDs interventions are successful or not. Either way I am expecting that it will get very interesting soon keep the markets under close observation. Good luck!

LONG TWITTER WITH INVESTMENT HORIZON FOR 3 QUARTERLY REPORTI expect a drawdown of Twitter in general with a drawdown of the market after the release of bad PMI in the USA,

and the purchase of twitter with the investment horizon on the report, all details are reflected in the graph,

please zoom in to see the text on the graph

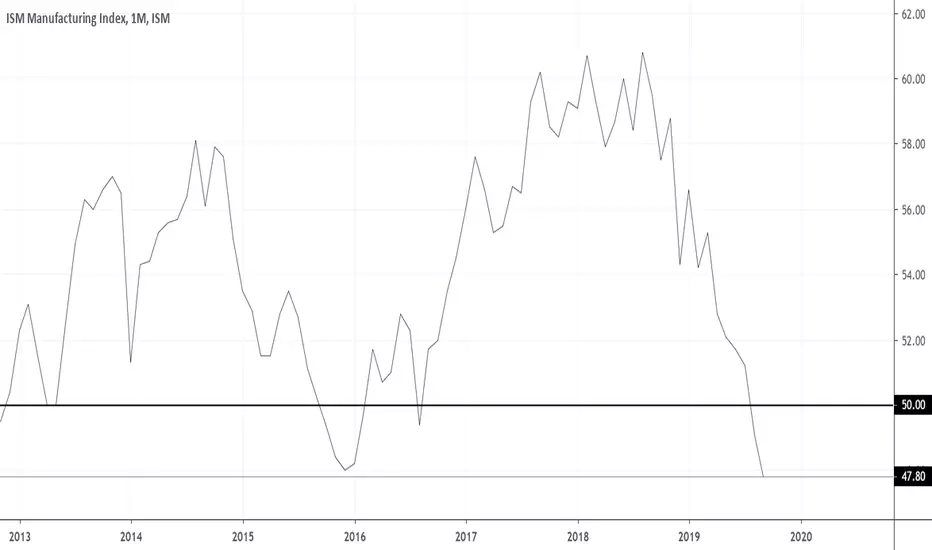

SP shortsetup still active as Economic Data in the US WorsensIf you have watched my analysis before I still expect the US Market to correct to the downside min. a 50% retracement from the last significant low. Fundamental Data is worsen as we stay in the contracting area under 50 and get a new lower reading with 47.8.

The weakness of Eurozone, the mercy of Iran and demarche of SinoSome cases are still unresolved also news that the Chinese delegation has cancelled a planned visit to American farms only exacerbates. So yesterday's gold growth was more than logical against the backdrop of fears of the failure of negotiations on trade wars. Our position on gold is unchanged - we continue to look for points for asset purchases.

This is happening against the background of a decrease in oil quotes. Moreover, there was an additional reason for bears. The decision of the Iranian authorities to release the British tanker Stena Impero. Formally, this is a signal of the tension decrease in the region. However, you should not rely on peace in the Middle East. The situation continues to be unstable, especially after the United States decided to send the military to help Saudi Arabia.

However, our recommendation to sell oil remains relevant. In our opinion, the factors in favour of asset sales outweigh the arguments in favour of purchases. Among the main arguments the restoration of oil production by Saudi Arabia, fears of a decrease in demand on the oil market amid a deterioration in the global economy and the offshore revolution in the United States.

Euro update. PMI indices in the whole Eurozone, as well as its key economies - Germany and France - came out distressing. Production indices everywhere dropped below 50, falling below the most pessimistic forecasts. For example, the PMI in the manufacturing sector in Germany in September reached 41.4 with a forecast 44.0 (by the way, the rate of decline in Germany's economic indicators is the highest over the past 10 years). That is, economic activity is deteriorating rapidly. Although the PMI in the Eurozone as a whole is still above 50, judging by the current dynamics, it will soon go below this mark. Yes, and the current value of 50.4 is the lowest mark for the last 4 years.

Recall that we recommend selling the euro primarily against the Japanese yen, as well as the British pound. Even against the dollar, for all our disbelief in it, we are more likely to sell euros than buy. Moreover, the data on PMI indices in the USA yesterday came out not only above 50, but also better than forecasts.

Once again, we point on excellent opportunities for Russian ruble sales.

ORBEX: EURUSD, USDJPY, GBPUSD On The Move!In today's #marketinsights video recording I analyse EURUSD, USDJPY and GBPUSD

#Euro down on:

- Disappointing German Manufacturing PMI (actual 41.4 vs expected 44.1 vs previous 43.5)

- ECB could have made a mistake talking somewhat 'neutral'

- Draghi's speech hinted to high uncertainty, decision-making harder and harder

#Yen down on:

- Disappointing Japanese Manufacturing PMI (actual 48.9 vs expected 49.8 vs previous 49.3)

- Potential stimulus measures

- Potential US-Iran deal

#Dollar up on:

- Trade talk optimism

- Markit Manufacturing PMI (actual 51 vs expected 50.4 vs previous 50.3)

#Pound down on:

- Thomas cook sentiment

- Parliament prorogation sentiment

- Barnier's pessimistic comments

Stavros Tousios

Head of Investment Research

Orbex

This analysis is provided as general market commentary and does not constitute investment advice

Euro and pound week, pressure on the dollar and weak NFPsBoris Johnson managed to turn into the worst premiere minister ever. His attempts to neutralize Parliament so he could complete Brexit by October 31 failed. As a result, Johnson lost a majority in Parliament. Why even Johnson’s brother disowned him left the Cabinet and the party.

As we warned in our reviews, Johnson's defeats are pound’s strength. As a result, the pound after gaining lows since 2016, added about 400 points by the end of the week. So those of our readers who listen to our recommendations should have earned good money.

As for the pound and Brexit. The legislation, which requires Johnson to ask for a three-month extension to Britain’s EU membership if parliament has not approved either a deal or consented to leave without agreement by Oct. 19, is expected to be signed into law by Queen Elizabeth on Monday.

Readers could earn a couple of hundred points on our recommendation to buy AUDJPY.

NFP data was the main statistical event of the past week. As we predicted, they turned out to be rather weak and below forecasts (+ 130K at the forecast + 160K). So, the dollar was under pressure. On September 18, the Fed is likely to lower the rate, and the dollar could be sold out.

As for the Canadian dollar. On Wednesday, the Bank of Canada did not reduce the rate, and then on Friday the Canadian labour market showed excellent results, as the Ivey PMI Business Activity Index did. So sales of the USDCAD, despite its decline by more than 200 points, look like a good trading opportunity.

The euro and the pound can gain a lot this week. As for the pound, the confrontation between Parliament and Johnson will continue. Therefore pound volatility explosions are quite likely.

As for the euro, the announcement of the results of the ECB meeting will be the main event. There are a lot of are waiting for a new round of monetary easing from the Central Bank. If a new program of quantitative easing and rate cuts would enter into force then the euro will be under pressure.

This week we will continue to look for points for gold purchases as last week, this tactic showed great results.

Do not forget to sell the Russian ruble (the Central Bank of the Russian Federation again reduced the rate), as well as oil (supply on the market is growing amid the threat of lower demand).

This week we will continue to look for points for gold purchases as last week, this tactic showed great results.

Do not forget to sell the Russian ruble (the Central Bank of the Russian Federation again reduced the rate), as well as oil (supply on the market is growing amid the threat of lower demand).

Johnson loses and Pound Victory, Bank of Canada and GoldWe continue to watch the confrontation between the British Parliament and Prime Minister Boris Johnson. Boris Johnson is losing another battle. On Tuesday, Boris Johnson not only lost his working majority, but he also could not initiate early elections.

As we predicted, the pound strengthened. Even the weak data on business activity in the UK could not prevent its strengthening: the PMI index of business activity in the services sector came out below forecasts (50.6 with a forecast of 51.0).

The dollar continued to suffer losses in the foreign exchange market. Even the euro strengthened against it. And this even though retail sales in the Eurozone came in the negative zone (-0.6%). However, despite yesterday's growth of the EURUSD, we are rather sceptical about buying euros.

Gold purchases look much more attractive and prospective under the current conditions. Another Fed rate cut in a couple of weeks (100% of traders believe in) could give an upward impulse to gold for its growth in the region of 1600. Recall that one of the key arguments against buying gold is its inability to generate guaranteed profit. But the Fed's rate-cutting cycles could lead to the dollar losing its ability to generate profit and becoming not interesting to investors.

The Bank of Canada announced that it left the policy rate steady. As a result, the Canadian dollar strengthened by a hundred points against the US dollar. Central Bank is not planning to cut rates in Canada saying that there are no reasons for that yat.

Today, as for macroeconomic statistics, it is interesting primarily for US employment data from ADP. Weak data could trigger dollar sales - traders will not wait for official statistics on Friday and will rush to discount under weak NFPs in advance.

Bears Continue To Drive The Dollar Lower so we recommend selling it since we expect a stronger wave of sales due to statistics on the US labour market.

Besides, today we will buy gold and the Japanese yen. Sales of the Russian ruble and oil are also what we are interested in.

The threat, problems, and preferencesTurkish President Recep Tayyip Erdogan removed Murat Cetinkaya as the central bank governor. In fact, this is an attempt to threaten the Central Bank of Turkey of independence, so the country's monetary policy is fully synchronized with the Government’s actions and objectives. Therefore crumbled.

This is a wake-up call to the world. Recall, Trump continues to weigh heavily against the Federal Reserve System, he wants a cheaper US dollar and Tight Monetary Policy. As a result, the Fed is facing another dilemma. The fact is that RATE-CUTTING could be perceived as a “response” to Trump's pressure. So there is a risk that the Fed may postpone the rate reduction in order to show that their actions are completely independent. However, we consider this option unlikely. So our recommendation to sell the dollar on the intraday basis as well as mid-term position.

The head of Russia’s State Statistics Service (Rosstat), who had been responsible for Russian statistics since 2009, was removed from his position however the Russian economy is still weak. PMI indices in Russia in June went below 50 (it means a decline in business activity). It is not about crossing the mark below 50, but at the rate at which the indicators are deteriorating. For example, back in May, the PMI index for the service sector was 52 (in June 49.7), and for the industrial sector - 51.5 (in June 49.2). So the rate at the end of June dropped sharply, updating the 2016 minimums. So, our recommendation to sell the ruble at any convenient opportunity.

Our trading plans and ideas are as follows. We will continue to look for points for dollar sales. We work on gold without special preferences - buy is at overbought and sell at oversold price levels. USDJPY we will sell. Medium-term purchases of pound and euro are still attractive. We will sell the Russian ruble, as well as oil.

ADP, ECB’s new head & July 4thThe publication of data on employment in the US private sector from ADP was the main even. Considering that official statistics from the US Department of Labor will be published tomorrow, traders and other financial market participants are expressing interest in. Analysts had expected growth in May (140K) however, the number is + 102K, only. On the one hand, the data is lower than forecast, on the other hand, it is significantly higher than the previous frankly disastrous numbers (recall that last month the increase was 27K, only). Well, this is a rather alarming signal. Also yesterday, data on the US trade balance was published (- $ 55.5 billion with a forecast $ 54.0).

Our recommendation is “sell the dollar”. Especially, if you remember Trump's attack on the dollar. Traditionally, in Twitter, the President of the United States called for the devaluation of the dollar.

And about the weak UK business activity data (Composite PMI index went below 50, that is 49.7), which increased the downward pressure on the pound. It’s too late to sell the pound and too early to buy. A similar index was published in Eurozone. The situation there is better (52.2 with the forecast 52.1). So, euro purchasing is not a bad idea ( on the intraday basis).

Ms Lagarde was honored to have been nominated for the ECB presidency. According to experts, Lagarde will adhere to a stimulating monetary policy aimed at ensuring economic growth in Europe. So, the euro might be under pressure.

We expect low liquidity in financial markets due to a holiday in the USA (Fourth of July – Independence Day). The “weak” market may well surprise in the form of volatility explosions, so today it is worth trading with caution.

Our trading recommendations for today: we will continue to look for points for dollar sales as well as the Russian ruble. Since AUDUSD has finished the day with a 0.7020 mark, we do not sell it, duo to further growth. Sell oil. As for gold, today we are working without obvious preferences on the oscillator signals.

US record, OPEC decision, Australian dollar under threatOn Monday, the markets continued to try to incorporate with the prices the G20 summit results. What Trump declared to be the victory in a trade war but is actually not. So, yesterday we observed the appearance of inefficiencies in financial markets that could be used to make money. In particular, we are talking about the gold falls into the bottoms of 1380-s, which can and should be used for asset purchases and earnings, as well as the growth of the Australian dollar above 0.70, which should be used to sell AUDUSD.

About the Australian dollar. Today, the Reserve Bank of Australia cut the rate for the second time in a row (this time from 1.25% to 1%). We believe that this is quite a serious signal to sell AUDUSD. Ideal prices for opening short sales are in the area of 0.7000-0.7020. In this case, stops can be placed above 0.7040, and profits - in the area of 0.6870.

Yesterday could be decisive for the dynamics of oil over the next few months. But the outcome of the OPEC meeting was too obvious. The cartel decided to extend the OPEC + No. 2 contract for 9 months until March 2020. Current progress in a trade war is a positive sign for oil. Well, all points are in favor of asset purchases. However, there might be a trap. Given the current consensus, oil growth will need something more than just an extension. For example, an increase in the volume of reductions or some additional conditions that narrow the supply on the oil market. But these conditions remained unchanged. In addition, a potential uncertainty factor is a participation in deal countries outside the cartel. Today, Russia and other countries must agree on their decision and position. At best, they will agree with the OPEC deal, which is already taken into account in the price, at worst they can announce their particular position, which can be an unpleasant surprise for buyers.

Total, while oil is below $ 60 (WTI brand), we recommend selling it. We put small stops in this case (above $ 60.40), but profits can be set fairly solid, up to the bottom $ 50.

Meanwhile, the United States recorded a new record: 121 months of continuous economic growth. This is a record in the entire history since 1854. Given the potential easing of monetary policy by the Fed, the United States has good chances to extend this series, as evidenced by yesterday's data on US business activity. The ISM index in the non-production sector in June was 51.7 points (forecast: 51.0), which testifies in favor of the growth of economic activity in the country.

What cannot be said about the Eurozone, where the PMI index in the manufacturing sector in June was significantly lower than 50 (47.6, with the forecast of 47.8) and was the lowest since 2013. Unpleasantly surprised China, whose PMI in the manufacturing sector was also below 50 (49.4).

Our trading preferences for today are as follows: we will continue to look for convenient sales opportunities for the dollar and the Russian ruble. In addition, we will continue to sell AUDUSD. We are selling oil today, but we are closely following the outcome of the OPEC meeting. As for gold, we will continue to work without obvious preferences, selling from overbought and buying from oversold.