Opening (IRA): SMH 2 x July 19th 210/215 Short Put Vertical... for a 1.00 in credit.

Comments: Part two of delta adjustment trade ... .

Instead of rolling up the 205/215 short put vertical, I closed it out (See Post Below), and then re-erected a 2 x 5 to delta balance against my call side, whose short leg is at the -32 delta strike.

This doesn't increase buying power effect, since the 2 x 5 is equivalent to the 1 x 10 on the call side.

The end result is a 2 x 210/2 x 215/255/265 iron condor, -5.79/3.42 delta/theta on which I've netted 3.36 in credits.

Premiumselling

Closing (IRA): SMH 205/215 Short Put Vertical... for a .87 debit.

Comments: First part of an adjustment trade. Instead of rolling the short put vertical aspect of my 205/215/255/265 up to delta balance, I'm closing it out.

Then, I'll re-erect a 2 x 5 (the equivalent of a 10-wide) to delta balance against the call side, whose short leg is at the 32 delta.

Opening (IRA): SMH July 19th 205/215/275/285 IC... for a 2.17 credit.

Comments: An additive delta adjustment to the current SMH IC I have on. (See Post Below).

With the original setup's short call aspect converging on -25 delta and the short put converging on +10, selling a skewed IC with the oppositionally delta'd short call/short put (i.e., at the +25 short put and the -10 delta short call) to bring back the position back to net delta flat with 63 days until expiry.

4.40 total credits collected with a current delta/theta of 1.02/5.81.

Opening (IRA): BITO June 21st 24 Short Put... for a 1.82 credit.

Comments: Adding a short put on weakness here to my covered call, which I'm sticking in with to grab the monthly divvy.

I'm okay with being assigned additional shares, since the break even of the June 24 is below the cost basis of what I currently have on. Otherwise, I'm perfectly fine with doing my usual take profit at 50% of max.

Metrics:

Buying Power Effect/Break Even: 22.18

Max Profit: 1.82 ($182)

ROC as a Function of Buying Power Effect: 8.21%

ROC at 50% Max: 4.10%

Opening (IRA): TLT August 16th 85 Short Put... for a .98 credit.

Comments: Targeting the strike paying around 1% of the strike price in credit, adding to my position at intervals, assuming I can get in at strikes better than what I currently have on.

Opening (IRA): TLT July 19th 83/August 16th 83 Short PutsComments: Getting in at strikes better than what I currently have on in July and August.

July 19th 83: Filled for an .85 credit

August 16th 83: Filled for a 1.11 credit

I'm fine with potentially getting assigned with shares at 83, since they're way below the cost basis of the covered calls I currently have on. I knew this might end up being a very, very long duration trade that would potentially take time to work out, but ... yeesh, the weakness.

Will look to roll out the most at risk strikes I've got in July (at the 86) and August (at the 85) at some point ... .

Opening (IRA): SMH July 19th 189/199/255/265 Iron Condor... for a 2.23 credit.

Comments: A small engagement trade in the semiconductor ETF (31.5% 30-Day IV).

Going somewhat wide here with the deltas, with the short option legs camped out at 16 delta on both sides. I generally like to collect one-third the width of the wings in credit for these, but am going a little more long-dated than usual, so want to give it a smidge more room to be wrong.

The assumption here is neutral, with the bet being that it slops around between my short option strikes. I'll generally look to take profit at 50% max and/or adjust sides on approaching worthless or on side test.

Metrics:

Buying Power Effect: 7.77

Max Profit: 2.23

ROC at Max: 28.70%

ROC at 50% Max: 14.35%

Delta/Theta: .37/3.01

Opening (IRA): QQQ October 18th 325 Short Put... for a 3.52 credit.

Comments: Adding a rung out in Q4 here with QQQ IVR at 81.0, targeting the <16 delta strike paying around 1% of the strike price in credit.

Will generally look to manage shorter duration rungs as I come to them ... .

Opening (IRA): TQQQ June 21st 52 Short Put... for a 2.49 credit.

Comments: Adding to my TQQQ position on weakness ... . This is a bit longer-dated than I like to go with shorter duration premium selling, which I like to keep in that 45 DTE wheelhouse, but May has now only 35 days in it, and I like to stick to monthlies in all but the most options liquid underlyings.

Will generally look to take profit at 50% max. I'm fine with being assigned, then proceeding to sell call against if that occurs.

Metrics:

BPE/Break Even: 49.51

Max Profit: 2.49 ($249)

ROC at Max Profit: 5.03%

ROC at 50% Max: 2.51%

Delta/Theta: 24.36/3.37

Opening (IRA): SPY September 20th 445 Short Put... for a 4.64 credit.

Comments: Targeting the <16 delta strike paying around 1% of the strike price in credit to emulate dollar cost averaging into the broad market.

Was starting to get somewhat worried that we would never have decent IV again. This ain't great, but I'll take it ... . Will generally look to take profit at 50% max.

Opening (IRA): SPY August 16th 460 Short Put... for a 4.95 credit.

Comments: A Q3 starter position ... . Targeting the shortest duration <16 delta strike paying around 1% of the strike price in credit to emulate dollar cost averaging into the broad market. July isn't paying, so going out to August.

Will look to add rungs in shorter duration, assuming I can get in at strikes better than what I've got on currently.

Opening (IRA): QQQ August 16th 380 Short Put... for a 4.00 credit.

Comments: Starting to round out my Q3 rungs here on weakness and higher IV, targeting the <16 delta strike paying around 1% of the strike price in credit to emulate dollar cost averaging into the broad market.

Opening (IRA): IWM July 19th 190 Short Put... for a 2.33 credit.

Comments: Targeting the shortest duration <16 delta strike paying around 1% of the strike price in credit to emulate dollar cost averaging into the broad market. (This is actually at the 18 delta, but it was either the 190 or the 185 where I wanted to pitch my tent from a delta standpoint).

Starting to slowly deploy third quarter rungs here in broad market (IWM, QQQ, SPY) while I piddle around with shorter duration higher IV sector ETF stuff.

Opening (IRA): IWM Sept/Oct 160/150 Short PutsComments: Going ahead and rounding out Q3 rungs here with IVR at 82.7.

September 20th 160: filled for a 1.99 credit

October 18th 150: filled for a 1.61 credit

Will look to manage shorter duration rungs as I come to them ... .

Opening (IRA): TLT July 19th 86 Short Put... for a .98 credit.

Comments: Adding to my TLT position on weakness here, targeting the strike paying around 1% of the strike price in credit.

I already have rungs on in April/May/June, so am adding a smidge out in July.

With QQQ and SPY knocking on ATH's, holding off on my usual broad market plays to await weakness and/or higher IV.

Opening (IRA): QQQ September 20th 430 Short Put... for a 4.34 credit.

Comments: Adding a rung out in Sept at the <16 delta strike paying around 1% of the strike price in credit to emulate dollar cost averaging Into the Q's. I already have rungs on in June, July, and August ... .

Will naturally back-track into shorter duration if I can get in at strikes better than what I currently have on.

Opening (IRA): QQQ August 16th 370 Short Put... for a 4.30 credit.

Comments: Targeting the <16 delta strike paying around 1% of the strike price in credit to emulate dollar cost averaging into the Q's.

Adding at a strike better than what I currently have on in August ... .

Opening (IRA): IWM August 16th 170 Short Put... for a 1.78 credit.

Comments: Starting to round out my Q3 rungs here on weakness and higher IV, targeting the <16 delta strike paying around 1% of the strike price in credit to emulate dollar cost averaging into the broad market. Already have June and July rungs on, so going out to August here.

Opened (IRA): IWM June/July 182/180 Short PutsComments: Added at strikes better than what I currently have on in weakness, targeting the <16 delta strikes in the respective expiries paying around 1% of the strike price in credit to emulate dollar cost averaging into the small cap ETF.

June 21st 182: Filled for 1.89

July 19th 180: Filled for 2.22

I also briefly looked at QQQ and SPY, but couldn't get in at strikes better than what I currently have on, so am leaving those positions alone for now.

Opening (IRA): IWM June 21st 175/July 19th 170 Short PutsComments: Targeting the <16 delta strikes paying around 1% of the strike price in credit to emulate dollar cost averaging into the small caps ETF.

Adding here on weakness, better strikes than what I currently have on in those expires.

Filled the June 21st for a 1.75 credit; the July 21st 170 for 1.76.

Opening (IRA): IWM June 21st 185 Short Put... for a 1.87 credit.

Comments: Targeting the <16 delta strike in the shortest duration that pays around 1% of the strike price in credit to emulate dollar cost averaging into the broad market.

The ROC %-age isn't tremendously sexy here, so primarily doing this to keep theta on and burning while I work shorter duration, higher IV underlyings (e.g., SMH, XBI, GDX/GDXJ, etc.).

Opening (IRA): XBI June 21st 82 Short Put... for a 1.90 credit.

Comments: Selling a put here, since the resulting cost basis if assigned shares would be lower than the cost basis of the position I've currently got on now. The full position is now a June 21st 82/88 covered strangle (i.e., short put, stock, short call).

Will look to take profit at 50% max.

Metrics:

Buying Power Effect/Break Even/Cost Basis in Shares if Assigned: 80.10

ROC at Max as a Function of Buying Power Effect: 2.37%

ROC at 50% Max as a Function of Buying Power Effect: 1.19%

Delta/Theta: 23.36/2.42

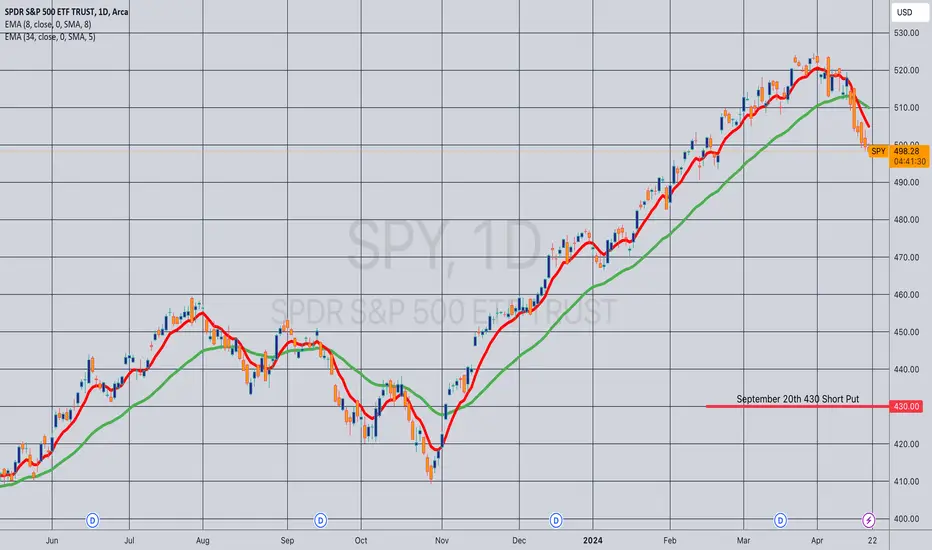

Opening (IRA): SPY September 20th 430 Short Put... for a 4.34 credit.

Comments: Targeting the <16 delta strike paying around 1% of the strike price in credit to emulate dollar cost averaging into S&P 500 ETF, adding at a strike better than what I currently have on.

As with my other broad market, will look to generally take profit at 50% max or -- if assigned -- sell call against at the strike price my short put was at.