EURAUD - Will RBA weaken the Aussie this week?The Aussie has been rallying strongly since the last RBA Rate Statement, and coupled with the weakness on the US Dollar, the AUDUSD has gained more than 6% in the last 30 days. As often stated in the RBA Rate Statement, rising Aussie will complicate the economic transition. Given the RBA is meeting this week, will they send out a dovish tone to push the Aussie lower?

Should that happen, we will be focusing on EURAUD for a potential long opportunity.

Price has recently bounced strongly after hitting the target at 1.4478, giving us the expectation that we can now expect one more wave (5-wave) up towards 1.5032 - 1.5409 region.

Combining with the potential of a year end tapering from ECB, we are currently holding on to a bullish bias on the EUR.

What would be a better opportunity combining the fundamental forces of EUR and AUD, if RBA were to adopt a dovish tone this week.

*Disclaimer - these are all just my personal observation and perspective of the market. Make sure you do your own due diligence before taking any trades.

RBA

AUDUSD: Gaining strength during a bull market in steelI think AUDUSD is ready to move, I booked a short term long, so my long here is risk free if stopped. We can enter at market, and add on dips, just don't buy your full position in one go. Target on chart, stop at 0.7582.

Best of luck,

Ivan Labrie.

AUDUSD - What's Next Post-RBA?A slightly more dovish statement from the RBA this morning sent the Aussie falling towards 0.7600 level.

We didn't catch the AUDUSD trade this morning but we traded the EURAUD and AUDJPY. In fact we shared the EURAUD trade idea () yesterday before RBA today.

Our traders know how we leverage on the risk events and trade the fundamental catalyst in the financial market. Understanding the concept of waves movement in the market - impulse or corrective - is crucial in knowing with high probability where price is likely to go.

As shared with our traders over and over again, DO NOT jump into a trade after an impulse move.

So what's next for AUDUSD post RBA?

Here're some current views and analysis -

1) Previous price move hit the 161.8% fibonacci level, giving us an expectation of a 5-wave structure developing.

2) Price came into the 23.6 - 38.2% fibonacci level potentially completing the minimum expectation for a wave 4 correction.

Depending on how price react from here -

1) If price develop as a correction, we are likely to see another push lower;

2) If price bounce off from this level, we are likely to see price reaching for 0.7740 area.

**This Friday NFP might be the key in providing us more information.

Short AUDGBP to 0.585 based on stagnant RBAExpect Reserve Bank of Australia (RBA) rates to stay stagnant. There has been a drop in auction clearance rates and property values across previously hot markets of Melbourne and Sydney due to APRA's interest only lending changes, but this is nothing to cause concern for the RBA.

We can see the beginning of a downtrend on AUDGBP as confirmed by a lack of buying volume and the crossover of the moving average at 20, 50 and 100 on the 4hr Charts.

Retail Sales in Australia are also expected to show a slower growth.

From these factors I am predicting a short to around 0.5850 which we have previously seen as strong resistance prior to the last major bull run and now expect this to turn to a support.

As always,

Stay focused and trade to trade well.

AUDUSD Weekly ForecastI expect the RBA to be neutral/slightly dovish in their rate statement this week. With AUDUSD at the trendline it's now held for over one year, I expect another push down from here. If this breaks, who knows where this pair will end up.

AUD USD SHORT!Aud/usd is a short for me. Beautiful rejection wicks right at the resistance. A perfect elliot wave is going to look for an ABC correction, most likely towards 61.8 which is also where the support will be. Stoch looks like its about to crossover and the RSI is overbought and already curved down.

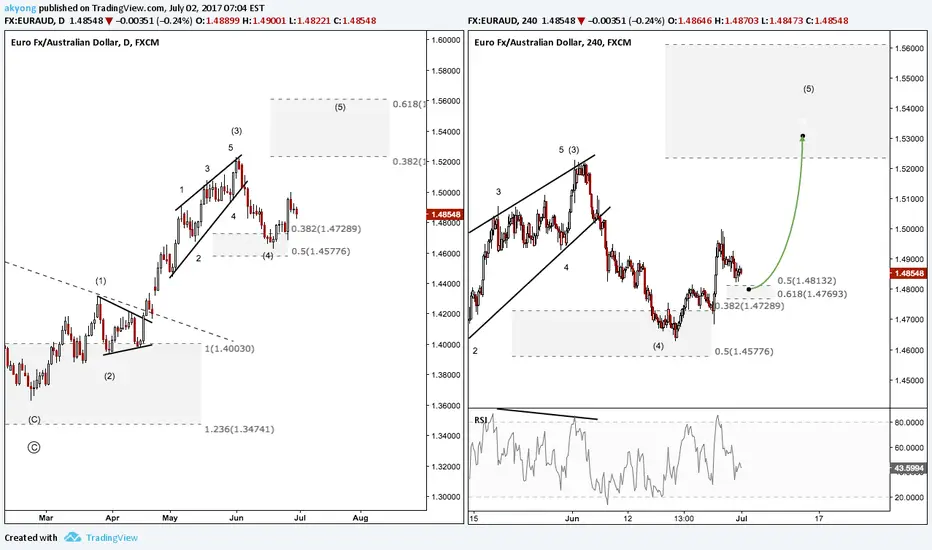

EURAUD - Time to head higher?Early June we shared an idea on EURAUD short term downside towards 1.4732 area ().

After hitting that area and completing the short term correction, we are now expecting price to move higher towards 1.5230 area to complete the overall 5-wave structure.

Here are some reasons for me to have a bullish bias on EURAUD -

1) Price development on daily timeframe is showing a potential 5-wave structure development;

2) Price is currently showing bullish impulses on 4-hour timeframe after hitting the 0.382 - 0.50 fibonacci area, completing the minimum retracement for a wave 4 correction; and

3) The most recent price move is corrective, thus indicating that there is a high probability of seeing a bullish impulse to the upside.

*Next week RBA Rate Statement and Cash Rate might be the catalyst to move the Aussie.

P.S. My personal bias is to the upside, but doesn't mean it's time now to take a buy trade. Make sure you have a proper strategy to engage the trade according to your personal plan :)

AUDUSD Short OpportunityI agree with Kathy Lien's analysis in this article. There is a strong opportunity for an AUDUSD short here, especially with the potential for a slight USD recovery this week and next due to rate hike expectations.

www.investing.com

However, this will ultimately set us up for a swing buy, hopefully around 0.73000.

AUD WEAKNESSPLACED SELL LIMIT ORDER @0.75337 PREDICTING TRENDLINE RETEST AND FELL DUE TO THE WEAKNESS IN AUD AFTER RBA INTEREST RATES REMAINING THE SAME WHICH LED TO BEARS TAKING OVER. LOOKING TO TAKE PROFIT @WEEKLY SUPPORT .

AUDUSD: Likely going up after retesting supportI think we can see a rally against the dollar here, and in other pairs naturally. This one happens to have a nice setup overall and has positive carry. You could risk a drop under yesterday's low, or 1-3 atr below 0.7475. There's upside to retest the next resistance level initially, eventually, one day it could break out in the monthly, but it's hard to put your finger on it and say, ok here it goes.

Good luck,

Ivan Labrie.

AUDNZD Elliott Forecast & Flag Breakout TradeAt the moment, in the big picture we are forming an ABC zigzag correction pattern which will take us into the 1.07408 area in which price will continue upwards. For now we can short down to this level by taking flag breakouts in favor of the downside. We have just closed below an ascending triangle on the lower timeframes and this has lead me to go short taking conservative targets @1.08240.

I may, however, trail stops with structure if the AUD interest rate decision causes more bears to step in.

AUDUSD Loosens Grip on 0.7608 Ahead of RBAIt’s no surprise that the AUDUSD challenged the confluence of support at 0.7608 yesterday. The pair looked weak during the last 48 hours of trade last week which is something I mentioned over the weekend.

The 0.7608 area is the intersection of trend line support from the December 2016 low and a horizontal level that’s been a factor since the January 24th high from earlier this year.

At the time of this writing, the pair is sitting just below these two levels ahead of an RBA rate decision. The event kicks off at 12:30 am EST, and unlike past decisions, the consensus as to what the bank will likely do is largely unsettled.

But given the last few weeks of price action, I’m only interested in a downside break. And unless the actual level is a bit lower than 0.7608, sellers appear to have done just that with yesterday’s close at 0.7604.

With that said, entering ahead of such a momentous event like a central bank rate decision is never a good idea. So unless you’re already short the AUDUSD from higher levels and therefore have a buffer to work with, it may be best to stay idle a while longer.

But structurally, the pair is one of the better looking right now which is why it remains at the top of my list.

The next key support comes in at the mid-March low of 0.7500. A close below that would expose the 0.7330 area. This is the 50% retracement of the 2016 range and is very near the wedge support that I mentioned last week.

Alternatively, a move higher from current levels would likely encounter sellers near 0.7670. A close above that would pave the way for a retest of wedge resistance near 0.7730.

AUDUSD: A traders' marketThe key levels on chart give an excellent idea of what's going on in $AUDUSD. My bias is the long side, so I'm buying each chance I get, on dips against support with tight stops. It's fairly easy to close in profit in a day or two most of the time. Longer term, we could be building a rally of monthly scale, but we need time to break above the resistance zone here.

While buyers defend the lows, we're safe and can join them after any adverse excursion, but book partial profits each time until we really move.

I'd reccomend using no stops, but sizing trades based on average true range values.

Good luck!

Ivan Labrie.

AUD/USD M/T shortHi guys,

In effect, this is an extension of my aussie trade posted pre-Trump (26th October 2016) in which we bagged 500 pips.

AUDUSD has seen rapid recovery off the back of both dollar weakness (mainly due to lack of details of the US administration's economic plans) and rapidly rising commodity prices, in particular iron ore (/it has rallied 10% recently, mainly based on speculation).

At present, the commodity currencies are more overvalued than any of their G10 counterparts at 15% in TWI terms, almost as much as they were a couple of years ago before they corrected substantially lower due to weaker commodity prices and rate cuts from the central banks (RBA in this case). Long term FX valuations point to AUD/USD fair value at 0.70.

RBA have sounded more optimistic on growth recently but $MS and others expect a slowdown in the housing sector, which could trigger an RBA cut. It is likely that the RBA wants to limit AUD upside in the n/t and is ready to soft its tone in case the FX rate appreciates excessively. Moreover, as the market could well price in more aggressive action by the Fed, relative mon pols support USD against AUD in coming months.

Iron ore futures need a reality check, which is my main reason for taking this trade (as well as favourable price action, esp on the weekly charts). RBA expects additional iron ore output from Brazil, as well as potential return of some output in China, to weigh on iron ore prices in the near term and doesn't see iron ore sticking around $90/metric ton. One could argue for days about whether iron ore prices should have rallied etc but one thing is for sure (as sure as you can be in this game!): iron ore prices need a correction. I see propensity for a correction down to as low as $80.

Looking at price action, upward momentum seems to be waning (bearish RSI div + 2 weekly dojis). A correction towards the 50% retracement of the Nov-Dec 2016 move seems likely, in my view.

GL all!

AUDUSD: Update - Consolidating here will give us continuationIf AUDUSD is to hold here, and eventually break out, and cross the overhead resistance, we can see a massive rally take off, which you definitely don't want to miss. If you missed my previous entries, you may go long here, risking a drop under 0.7811. Keep risk to 0.5-1%. This is a swing trade setup.

If you want, additionally, or perhaps if more conservative, you may use our monthly setup stop loss: 0.75248. Upside is significant, so don't miss this opportunity!

Good luck,

Ivan Labrie.

RBA rate decision preview, key levels highlightedThe RBA rate decision tomorrow at 0330GMT has unanimous expectations for rates to remain unchanged at record low 1.50% (ASX 30-Day Interbank Cash Rate Futures pricing in a 95% chance of a hold). Data has been weak since the last meeting with Unemployment Rate rising for both December and January and is now at the highest since June 2016, while we also saw a miss on expectations for all GDP and CPI figures. Despite this, the RBA is expected to use alternative methods to drive the economy, as soaring Building Approvals and rising house prices narrow the scope a near-term rate cut (low rates push up house prices), while surprisingly Goldman Sachs see the next RBA rate move to be a hike amid global economic recovery and increasing incomes. Pressure on the central bank is building as GDP on a Q/Q basis posted a contraction for the first time since Q1 of 2011 and retail sales hit a 4-month low in December. Additional easing is still a possibility according to JPMorgan who stated RBA could ease further this year if there is turbulence in the strength of the economy, while Credit Suisse stated RBA could have to cut rates as many as 3 more times. Since markets are expecting no rate move, focus will be on the statement as neutral or hawkish comments could dampen hopes of future easing and boost AUD

Dark Cloud Cover at TL resistanceThe Aussie finished Friday lower, printing Dark Cloud Cover on back of stronger than expected annual wage growth in the US. Reversal candle occurred at falling wedge resistance / former support confluence and pair looks set to resume lower.

Initial support is the .7296 - .7283 hourly zone, with a break below there confirming the top and targeting the lows above .7150. A break above .7365 would invalidate the set up and shift focus to the Dec 14 high at .7525.

AUDNZD Elliott wave trade signal: Can Santa rally pull AUDNZD?Talking Points:

Technical Strategy: Bullish can be confirmed soon

Elliottwave Count:

Wave 2 can mark completed

Analysis

As per previous analysis, AUDNZD (Australian dollar / NewZealand dollar) was expecting to complete it's wave 2 correction @ 1.0350 after having an high over 1.0726. We were seen corrective move towards 1.0350 in expanded flat correction. We also had a nice bounce from channel support and horizontal support from 1.0350 levels. We are considering it's reversal trend and able to count five wave upwards move in lower time frame. Considering that analysis, we are targeting wave (iii) in coming months which can at-least target above 1.0726. However, we under estimated correction target and correction is still in progress. We are now seeing complex w-x-y correction in placed. We are marking that correction over as we see inner bearish trend line breakout. We will gain more confidence once we have trend line breakout which was drawn from wave 1 towards wave (x) and B. Breakout level can be on 1.0500. However, we are optimistic here and putting correction complete and look for impulse movements in wave 3.

We are looking for break of 1.0488 to confirm our analysis

Action

We re-initiated our long position with definite stoploss.(No Action now)

-- By Hoagtrading.com (Twitter: @Hoagtrading)

AUDUSD: Longer term charts might indicate a downtrendThere's a discrepancy between timeframes in $AUDUSD, with the daily recently turning into a downtrend, after suggesting buying dips was viable all year; the weekly in an uptrend, and close to fail to confirm bearish momentum within 2 weeks; and the monthly indicating a full flung downtrend is en route, and it should eventually achieve the 0.63111 mark by or before the end of December 2017.

In the short term, the daily chart despite indicating bears are in control, might indicate a retracement or sideways consolidation is about to start, specially viable after we hit the second target, and/or when time for the daily downtrend runs out by January 3rd.

RgMov warns you in the daily, if you wish to go long to catch a retracement, because price might just go sideways, chopping buyers and sellers out for a while, so it will be easier to take the sell side only, either after an overbought rally in the daily, or after a sideways consolidation ends.

(I prefer to do nothing for now, but, if you're interested in going long, you can try to buy a new daily high, risking a drop under last week's low)

Good luck,

Ivan Labrie

AUDCAD: Trend will resumeTalking Point:

Technical Strategy: Confirming it's bearish outlook

Elliottwave View: Reversal confirmed and counting impulsive waves

Analysis

AUDCAD was trading sideway from Aug-2013. We were seen May-2015 a declined again but unable to takeout Aug-2013 low in impulse manner. We were experienced a bounce from 9170 area in May-2015. However, upside was corrective and can be counted as flat correction in Elliott-wave and possibly correction is over on 1.04 zone. With that in mind, we are expecting trend reversal should be taking place and can be seen impulsive declined from 1.04 and possibly we had it's first leg down from 1.04 to 0.9864 and now reversal confirmed from 1.0100 level. Currently we are counting impulsive bearish wave. We were expecting it's minor first leg and was expected small correction towards 1.00. This will provide anyone to join who missed this train. On 7th Dec (Today), we are confirming correction should be over. We are marking this is a complex flat correction where price was traded in range bound.

Action

We are running two short position from 1.01 and 1.004, and for both position we lowered down our stoploss. We also added plan for third position here.

- By Hoagtrading.com (@hoagtrading)

AUDUSD: Monthly range expansions show sellers get trapped higherLooking at monthly ranges, we see that months with sharp selloffs, that surpass the previous true range, as measured from the open to the low, have been causing sellers to get trapped at increasingly higher prices. This is bullish and shows accumulation, and shakeouts taking place. The monthly chart shows a mode near the highs, and now we're testing support at the bottom of the monthly range, so we have a great opportunity on the long side, after the market got extremely one sided.

Sellers might get trapped here again, this time higher than the previous range expansion months, which is bullish overall. Daily and weekly RgMov readings are bullish, and we have massive lag relative to copper and iron ore, which eventually will play out, so I remain bullish.

The entry to add to longs is described in my 4h chart, see related ideas for more information.

Keep these levels in mind, once above, they act as support on a retest.

Good luck,

Ivan Labrie.

AUDUSD enters former support zoneThe Aussie broke through long term channel support in mid-November; falling nearly 300 pips in 3 days, before finding support above 73. Pair has since retraced approximately 61.8% of the decline from 7580 and is testing the .7440 - 75 former support zone. We are looking for a turn lower from here and an eventual break below the 5 month low at 7285. Alternatively; a break above 75 would target the next former support zone at 7555 - 7610, butwe expect any gains to remain capped below there.

AUDCAD: Trend Reversal?Talking Point:

Technical Strategy: Confirming it's bearish outlook

Elliottwave View : Confirming completion of wave (C) of c

Analysis

AUDCAD was trading sideway from Aug-2013. We were seen May-2015 a declined again but unable to takeout Aug-2013 low in impulse manner. We were experienced a bounce from 9170 area in May-2015. However, upside was corrective and can be counted as flat correction in elliott-wave and possibly correction is over on 1.04 zone. With that in mind, we are expecting trend reversal should be taking place and can be seen impulsive declined from 1.04 and possibly we had it's first leg down from 1.04 to 0.9864. Ongoing upward momentum can be wave 2 / wave B.

Action

We are having level planned to short this pair with limited risk and having maximum rewards.

-- By @Hoagtrding (Hoagtrading.com)