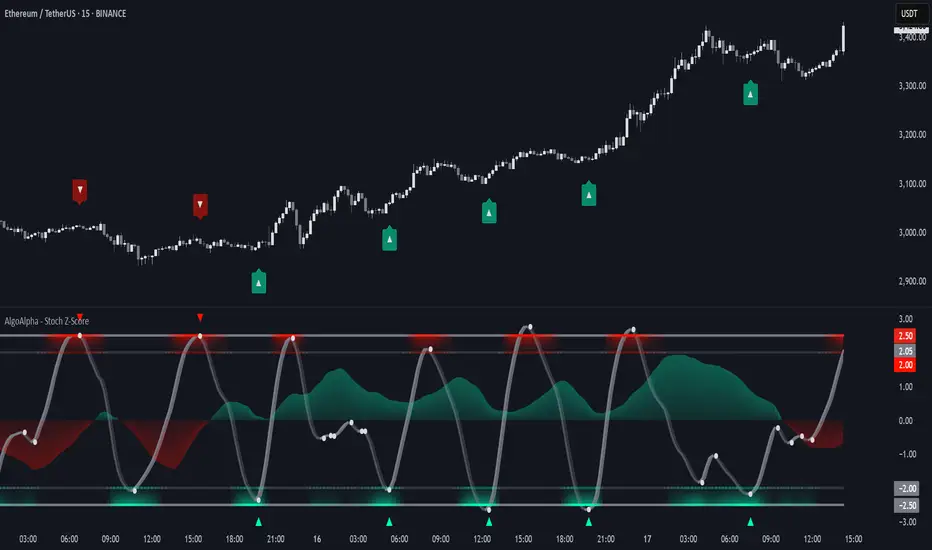

Stochastic Z-Score [AlgoAlpha]🟠 OVERVIEW

This indicator is a custom-built oscillator called the Stochastic Z-Score , which blends a volatility-normalized Z-Score with stochastic principles and smooths it using a Hull Moving Average (HMA). It transforms raw price deviations into a normalized momentum structure, then processes that through a stochastic function to better identify extreme moves. A secondary long-term momentum component is also included using an ALMA smoother. The result is a responsive oscillator that reacts to sharp imbalances while remaining stable in sideways conditions. Colored histograms, dynamic oscillator bands, and reversal labels help users visually assess shifts in momentum and identify potential turning points.

🟠 CONCEPTS

The Z-Score is calculated by comparing price to its mean and dividing by its standard deviation—this normalizes movement and highlights how far current price has stretched from typical values. This Z-Score is then passed through a stochastic function, which further refines the signal into a bounded range for easier interpretation. To reduce noise, a Hull Moving Average is applied. A separate long-term trend filter based on the ALMA of the Z-Score helps determine broader context, filtering out short-term traps. Zones are mapped with thresholds at ±2 and ±2.5 to distinguish regular momentum from extreme exhaustion. The tool is built to adapt across timeframes and assets.

🟠 FEATURES

Z-Score histogram with gradient color to visualize deviation intensity (optional toggle).

Primary oscillator line (smoothed stochastic Z-Score) with adaptive coloring based on momentum direction.

Dynamic bands at ±2 and ±2.5 to represent regular vs extreme momentum zones.

Long-term momentum line (ALMA) with contextual coloring to separate trend phases.

Automatic reversal markers when short-term crosses occur at extremes with supporting long-term momentum.

Built-in alerts for oscillator direction changes, zero-line crosses, overbought/oversold entries, and trend confirmation.

🟠 USAGE

Use this script to track momentum shifts and identify potential reversal areas. When the oscillator is rising and crosses above the previous value—especially from deeply negative zones (below -2)—and the ALMA is also above zero, this suggests bullish reversal conditions. The opposite holds for bearish setups. Reversal labels ("▲" and "▼") appear only when both short- and long-term conditions align. The ±2 and ±2.5 thresholds act as momentum warning zones; values inside are typical trends, while those beyond suggest exhaustion or extremes. Adjust the length input to match the asset’s volatility. Enable the histogram to explore underlying raw Z-Score movements. Alerts can be configured to notify key changes in momentum or zone entries.

Indicators and strategies

Choch Pattern Levels [BigBeluga]🔵 OVERVIEW

The Choch Pattern Levels indicator automatically detects Change of Character (CHoCH) shifts in market structure — crucial moments that often signal early trend reversals or major directional transitions. It plots the structural break level, visualizes the pattern zone with triangle overlays, and tracks delta volume to help traders assess the strength behind each move.

🔵 CONCEPTS

CHoCH Pattern: A bullish CHoCH forms when price breaks a previous swing high after a swing low, while a bearish CHoCH appears when price breaks a swing low after a prior swing high.

Break Level Mapping: The indicator identifies the highest or lowest point between the pivot and the breakout, marking it with a clean horizontal level where price often reacts.

Delta Volume Tracking: Net bullish or bearish volume is accumulated between the pivot and the breakout, revealing the momentum and conviction behind each CHoCH.

Chart Clean-Up: If price later closes through the CHoCH level, the zone is automatically removed to maintain clarity and focus on active setups only.

🔵 FEATURES

Automatic CHoCH pattern detection using pivot-based logic.

Triangle shapes show structure break: pivot → breakout → internal high/low.

Horizontal level marks the structural zone with a ◯ symbol.

Optional delta volume label with directional sign (+/−).

Green visuals for bullish CHoCHs, red for bearish.

Fully auto-cleaning invalidated levels to reduce clutter.

Clean organization of all lines, labels, and overlays.

User-defined Length input to adjust pivot sensitivity.

🔵 HOW TO USE

Use CHoCH levels as early trend reversal zones or confirmation signals.

Treat bullish CHoCHs as support zones, bearish CHoCHs as resistance.

Look for high delta volume to validate the strength behind each CHoCH.

Combine with other BigBeluga tools like supply/demand, FVGs, or liquidity maps for confluence.

Adjust pivot Length based on your strategy — shorter for intraday, longer for swing trading.

🔵 CONCLUSION

Choch Pattern Levels highlights key structural breaks that can mark the start of new trends. By combining precise break detection with volume analytics and automatic cleanup, it provides actionable insights into the true intent behind price moves — giving traders a clean edge in spotting early reversals and key reaction zones.

Lorentzian Theory Classifier🧮 Lorentzian Theory Classifier: An Observatory for Market Spacetime

Transcend the flat plane of traditional charting. Enter the curved, dynamic reality of market spacetime. The Lorentzian Theory Classifier (LTC) is not an indicator; it is a computational observatory. It is an instrument engineered to decode the geometry of market behavior, revealing the hidden curvatures and resonant frequencies that precede significant turning points.

We discard the outdated tools of Euclidean simplicity and embrace a more profound truth: financial markets, much like the cosmos described by general relativity, are governed by a fabric that is warped by the mass of participation and the energy of volatility. The LTC is your lens to perceive this fabric, to move beyond predicting lines on a chart and begin reading the very architecture of probability.

The Resonance Manifold: Standard Euclidean models search for historical analogues within a rigid sphere, missing the crucial outliers that define market extremes. The LTC's Lorentzian Resonance engine operates in a curved, non-Euclidean space, allowing it to connect with these "fat-tail" events—the true genesis points of major reversals.

🌌 THE THEORETICAL FRAMEWORK: A new Grand Unified Theory of Market Analysis

The LTC is built upon a revolutionary synthesis of concepts from special relativity, quantum mechanics, and information theory. It reframes market analysis not as a problem of forecasting, but as a problem of state recognition in a non-Euclidean manifold.

1. The Lorentzian Kernel: The Mathematics of Reality

Financial markets are not Gaussian. Their reality is one of "fat tails"—sudden, high-impact events that standard models dismiss as anomalies. The LTC acknowledges this reality by using the mathematically pure and robust Lorentzian kernel as its core engine:

Similarity(x, y) = 1 / (1 + (||x − y||² / γ²))

||x − y||²: The squared distance between the current market state (x) and a historical state (y) in our 8-dimensional feature space.

γ (Gamma): A dynamic bandwidth parameter, our "Lorentz factor," which adapts to market entropy (chaos). In calm markets, gamma is small, demanding precise resonance. In chaotic markets, gamma expands, intelligently seeking broader patterns.

This heavy-tailed function is revolutionary. It correctly assigns profound significance to the rare, extreme events that truly define market structure, while gracefully tuning out the noise of mundane price action. It doesn't just calculate; it understands context.

2. The 8-Dimensional State Vector: The Market's Quantum Fingerprint

To achieve a holistic view, the LTC projects the market onto an 8-dimensional Hilbert space, where each dimension represents a critical "observable":

Momentum & Acceleration (f_rsi, f_roc): The market's velocity and its rate of change.

Cyclical Position (f_stoch, f_cci): The market's location within its recent oscillation cycles.

Energy & Participation (f_vol, f_cor): The force of capital flow and its harmony with price.

Chaos & Uncertainty (f_ent, f_mom): The degree of randomness and the standardized force of price changes.

These are not eight separate indicators. They are entangled properties of a single "market wavefunction." The LTC's genius lies in measuring the geometric distance between these complete quantum states.

3. The k-NN Oracle: A Council of Past Universes

The LTC employs a k-Nearest Neighbors algorithm, but in our curved Lorentzian spacetime. It poses a constant, profound question: " Which moments in history are most geometrically congruent to the present moment across all eight dimensions? "

It then summons a "council" of these historical neighbors. Each neighbor's future outcome (did price ascend or descend?) casts a vote, weighted by its resonant similarity. The result is a probabilistic forecast of stunning clarity:

Prognosis: The final weighted consensus on future direction.

Assurance: The degree of unanimity within the council—a direct measure of the prediction's confidence.

The Funnel of Conviction: The LTC's process is a rigorous distillation of information. Raw, chaotic market data is resolved into a clean 8-dimensional state vector. The Lorentzian Kernel filters these states for resonance, which are then passed to the k-NN Oracle for a vote. Noise is eliminated at each stage, resulting in a single, validated, high-conviction signal.

⚙️ THE COMMAND CONSOLE: A Guide to Calibrating Your Observatory

Mastering the LTC's inputs is to become an architect of your own analytical universe. Each parameter is a dial that tunes the observatory's focus, from galactic structures to subatomic fluctuations. The tooltips in-script—over 6,000 words of documentation—provide immediate reference; this guide provides the philosophy.

A summarized guide to the Core, Signal, Supreme, and Visual controls is included directly in the indicator's code and tooltips. We encourage all users to explore these settings to tune the LTC to their unique analytical style.

🏆 THE SUPREME DASHBOARD: Your Mission Control

The dashboard is not a data table; it is your command interface with market reality. It translates the intricate dance of probabilities and vectors into clear, actionable intelligence.

⚡ ORACLE STATUS

Prognosis: The primary directional vector. Its color, magnitude, and emoji (⚡) reveal the strength and conviction of the Oracle's forward guidance.

Assurance: A real-time gauge of prediction quality, from "LOW" (high uncertainty) to "ELITE" (overwhelming statistical consensus). Interpret this as your core risk metric: trade with conviction when Assurance is ELITE; trade with caution when it is LOW.

🔮 RESONANCE ANALYSIS

Chaos: A direct measurement of market entropy. "LOW CHAOS" signifies a predictable, orderly regime. "HIGH CHAOS" is a warning of randomness and unpredictability, where trend-following logic may fail.

Turbulence: A measure of raw volatility. When the market is "TURBULENT," expect wider price swings and increased risk. Use this metric to adjust stop-loss distances and profit targets dynamically.

🏆 PERFORMANCE & ⚔️ GUARD METRICS

These sections provide illustrative statistics on the script's recent historical behavior. Metrics like Yield Ratio and Guard Index offer a quick heuristic on the prevailing risk-reward environment. Crucially, these are for observational context only and are not a substitute for your own rigorous testing and analysis.

🎨 THE VISUAL MANIFESTATION: Charting the Unseen

The LTC's visuals are designed to transform your chart from a 2D price graph into a 4D informational battlespace.

The Dynamic Aura (Background Color): This is the ambient energy field of the market. A luminous green (Ascend) signifies a bullish resonance field; a deep red (Descend) indicates bearish pressure.

The Assurance Shroud (Blue Bands): A visualization of confidence. When the shroud is wide and expansive , the Oracle's vision is clear and its predictions are robust.

The Prognosis Arc (Curved Line): A geodesic projection of the market's most likely path, based on the current Prognosis.

The Turbulence Cloud (Orange Mist): A visual warning system for market chaos. When this entropic mist expands , it is a clear sign that you are navigating a nebula of high unpredictability.

Oracle Markers (▲▼): The final, validated signals. These are not merely pivot points. They are moments in spacetime where a structural pivot has been confirmed and then ratified by a high-conviction vote from the Lorentzian Oracle. They are the pinnacles of confluence.

The Analyst's Observatory: The LTC transforms your chart into a command center for market analysis, providing a complete, at-a-glance view of market state, risk, and probabilistic trajectory.

🔧 THE ARCHITECT'S VISION: From a Blank Slate to a New Cosmos

The LTC was not assembled; it was derived. It began not with code, but with first principles, asking: "If we were to build an instrument to measure the market today, unbound by the technical dogmas of the 20th century, what would it look like?" The answer was clear: it must be multi-dimensional, it must be adaptive, and it must be built on a mathematical framework that respects the "fat-tailed" nature of reality.

The decision to use a pure Lorentzian kernel was non-negotiable. It represented a commitment to intellectual honesty over computational ease. The development of the Supreme Dashboard was driven by the philosophy of the "glass cockpit"—a belief that a trader's greatest asset is not a black box signal, but a transparent and intuitive flow of high-quality information. This script is the result of that unwavering vision: to create not just another indicator, but a new lens through which to perceive the market.

⚠️ RISK DISCLOSURE & PHILOSOPHY OF USE

The Lorentzian Theory Classifier is an instrument of profound analytical power, intended for the serious, discerning trader. It does not generate infallible signals. It generates high-probability, data-driven hypotheses based on a rigorous and transparent methodology. All trading involves substantial risk, and the future is fundamentally unknowable. Past performance, whether real or simulated, is no guarantee of future results. Use this tool to augment your own skill, to confirm your own analysis, and to manage your own risk within a well-defined trading plan.

"The effort to understand the universe is one of the very few things that lifts human life a little above the level of farce, and gives it some of the grace of tragedy."

— Steven Weinberg, Nobel Laureate in Physics

Trade with rigor. Trade with perspective. Trade with enlightenment. Trade with insight. Trade with anticipation.

— Dskyz, for DAFE Trading Systems

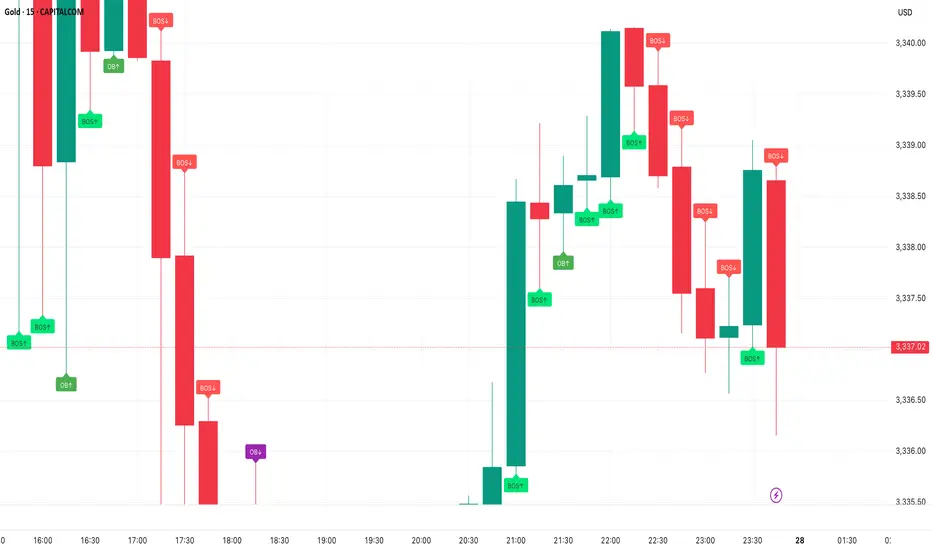

Smart Money Concepts - By TradingNexus – Pro Visual Edition📊 Smart Money Concepts by TradingNexus

This script is designed for clean and visual Smart Money analysis.

This script identifies Smart Money Concepts with a clean and powerful visual layout, focusing on high-probability zones.

It displays:

Order Blocks (OB↑ / OB↓) when there's strong bullish or bearish candle reversal.

Fair Value Gaps (FVG↑ / FVG↓) only after impulsive candles (e.g., breaking previous highs/lows).

Break of Structure (BOS↑ / BOS↓) when a real structural shift happens.

🔥 Strong Zones only when OB + FVG + BOS align — these are ideal institutional entry areas.

Smart Elliott Wave [The_lurker]🔷 Smart Elliott Wave – موجات إليوت الذكية

A professional indicator for automatically detecting and analyzing Elliott Wave patterns on the chart. Built on classical Elliott Wave theory, it enhances accuracy with dynamic Fibonacci validation and geometric logic—solving the most common issues traders face when applying Elliott Wave manually: complexity, subjectivity, and misinterpretation of corrections.

🎯 Key Features

Smart Elliott Wave offers a layered intelligent system that:

- Automatically detects impulsive and corrective wave structures

- Validates wave formations using Fibonacci rules

- Highlights potential reversal zones (PRZ)

- Sends instant alerts for newly detected patterns

- Supports both bullish and bearish trends

- Includes fully customizable user settings

🧠 Core Concept

The indicator analyzes price movement over time using pivot points (discovered via `ta.pivothigh` and `ta.pivotlow`) to detect wave structures that conform to Elliott Wave sequencing:

- Impulse Wave: 0-1-2-3-4-5

- Simple Correction: ABC

- Complex Correction: WXY

Each structure is validated through a strict set of logical rules combined with Fibonacci ratio checks to ensure pattern integrity and reduce false signals.

🧩 Wave Structure Components

1️⃣ Impulse Waves

- Wave 3 is not the shortest

- Wave 4 does not overlap Wave 1

- Waves 1, 3, and 5 are impulsive; Waves 2 and 4 are corrective

- Fibonacci validation can be applied to Waves 2 and 4 if enabled

2️⃣ Simple Corrections (ABC)

- Wave B partially retraces Wave A

- Wave C completes the structure without invalid overlap

- Fibonacci ratios validate the symmetry of A, B, and C (if enabled)

3️⃣ Complex Corrections (WXY)

- Only used if ABC structure is insufficient

- Requires 6 sequential pivot points: W, X, Y

- W and Y are corrective; X is a linking wave

- Follows both structural and ratio-based validations

📏 Dynamic Fibonacci Validation

When Enable Fibonacci Rules is active:

- Validates against common ratios:

`38.2%`, `50%`, `61.8%`, `78.6%`, `127.2%`, `161.8%`

- Adjustable **Fibonacci Tolerance** allows for controlled deviation

- Patterns are ignored if ratios fall outside the accepted range

🔮 Potential Reversal Zones (PRZ)

- Calculated from the most recent completed impulse wave

- Uses Fibonacci extensions to project PRZ ahead of price

- Customizable visibility and color for each ratio

- Used as dynamic take-profit or stop-loss zones

🖍️ Dual Trend Detection & Wave Coloring

- Supports both bullish and bearish patterns

- Automatic wave coloring for quick visual recognition:

- 🟦 Blue: Bullish waves

- 🟥 Red: Bearish waves

- Optional fill color for correction zones

🔔 Smart Alert System

Instant alerts are triggered when a valid wave pattern is confirmed:

- New impulse wave detected

- ABC correction appears

- Complex WXY correction formed

> Alerts are triggered only after the bar closes to prevent repainting.

⚙️ Indicator Settings

📌 Wave Detection Settings

- Pivot Left Strength: Bars to the left used for pivot detection

- Pivot Right Strength: Bars to the right for confirmation (0 = real-time)

- Enable Fibonacci Rules: Toggle Fibonacci ratio validation

- Fibonacci Tolerance: Allowed deviation in percentage

🎨 Display Settings

- Show Previous Patterns: Toggle between all patterns or only the latest

- Fill correction zones with color

- Customize wave and PRZ color schemes

📉 PRZ Settings

- Show/hide specific Fibonacci ratios

- Customize each PRZ color

- Set maximum bar extension for PRZ display

🔕 Alert Settings

- Enable or disable alerts for each type of pattern

📚 Practical Use Cases

- Daily or intraday price structure analysis

- Combine with RSI, MACD, or momentum indicators

- Filter weak signals using Fibonacci-based pattern validation

- Use PRZ zones as dynamic entry/exit targets

- Learn and reinforce Elliott Wave theory through real-time examples

📝 Important Notes

- Setting `Pivot Right = 0` allows for real-time pattern previews (may repaint)

- Disabling Fibonacci validation increases pattern count but reduces accuracy

- TradingView limits to 500 visual objects (labels, boxes, lines); older patterns may be removed

- PRZ extends up to 100 bars or 0.618 of the previous impulse duration by default

⚠️ Disclaimer:

This indicator is for educational and analytical purposes only. It does not constitute financial, investment, or trading advice. Use it in conjunction with your own strategy and risk management. Neither TradingView nor the developer is liable for any financial decisions or losses.

🔷 Smart Elliott Wave – موجات إليوت الذكية

مؤشر احترافي لرصد وتحليل أنماط موجات إليوت تلقائيًا على الرسم البياني، يعتمد على المبادئ الكلاسيكية للنظرية مع تعزيزها بالتحقق الرياضي والهندسي، ويهدف إلى تجاوز العقبات التي يواجهها معظم المتداولين عند تطبيق موجات إليوت يدويًا، مثل صعوبة التحديد، التقديرات الذاتية، وتشويش التصحيحات.

🎯 ما الذي يميز هذا المؤشر؟

يُقدّم Smart Elliott Wave نظامًا تراكبيًا ذكيًا يقوم بـ:

رصد تلقائي للموجات (الدافعة والتصحيحية)

التحقق من صحة النموذج باستخدام قواعد فيبوناتشي

عرض مناطق الانعكاس المحتملة (PRZ)

توليد تنبيهات لحظية عند تشكّل أنماط جديدة

دعم الاتجاهين (الصاعد والهابط)

واجهة إعدادات مرنة قابلة للتخصيص الكامل

🧠 الفكرة الأساسية

يعتمد المؤشر على تحليل حركة السعر عبر تسلسل زمني من النقاط المحورية (Pivots)، والتي تُكتشف باستخدام دوال مدمجة مثل ta.pivothigh وta.pivotlow. ثم يُبني فوق هذه النقاط نماذج هندسية متوافقة مع تسلسل موجات إليوت:

الموجة الدافعة (Impulse): تسلسل 0-1-2-3-4-5

التصحيح البسيط (ABC)

التصحيح المعقد (WXY)

ويتم التحقق من كل نموذج اعتمادًا على قواعد إليوت + نسب فيبوناتشي، ما يضمن موضوعية التصنيف، ودقة التحديد.

🧩 مكوّنات التحليل:

1️⃣ الموجات الدافعة (Impulse Waves):

يُشترط أن تكون الموجة الثالثة غير الأقصر.

لا تتداخل الموجة الرابعة مع نطاق الموجة الأولى.

تأكيد أن الموجات 1 و3 و5 دافعة، و2 و4 تصحيحية.

يتم التحقق من نسب تصحيح الموجتين 2 و4 حسب قواعد فيبوناتشي عند تفعيلها.

2️⃣ التصحيح البسيط (ABC):

B تصحيح جزئي للموجة A.

C تُكمل الهيكل بدون تداخل مع A.

يتم التحقق من أطوال الموجات وفق نسب فيبوناتشي لضمان التناسق.

3️⃣ التصحيح المعقد (WXY):

لا يتم تفعيله إلا عند فشل ABC في تفسير النمط.

يتطلب 6 نقاط محورية متسلسلة: W, X, Y.

W وY تصحيحيتان، وX رابط مركزي.

يخضع أيضًا لقواعد النسب والتماثل البنائي.

📏 التحقق باستخدام نسب فيبوناتشي:

عند تفعيل خاصية Enable Fibonacci Rules، يتم التحقق الصارم من نسب تصحيح الموجات:

النسب المعتمدة:

38.2%, 50%, 61.8%, 78.6%, 127.2%, 161.8%

إذا لم تكن الموجة ضمن نطاق النسبة + نسبة التسامح (Tolerance)، يتم تجاهل النموذج.

يُستخدم هذا التحقق أيضًا لرسم مناطق الانعكاس المحتملة (PRZ).

🔮 مناطق الانعكاس المحتملة (PRZ)

تُحسب PRZ باستخدام نسب فيبوناتشي انطلاقًا من نهاية آخر موجة دافعة.

تُعرض بشكل مستطيلات شفافة أو ملونة.

يمكن تخصيص كل نسبة لونًا وشكلًا خاصًا.

تُستخدم PRZ كأداة توقع للموجة التالية أو لتحديد أهداف وقف الخسارة وجني الأرباح ديناميكيًا.

🖍️ دعم الاتجاهين وتلوين الموجات:

يدعم المؤشر النماذج الصاعدة والهابطة بشكل تلقائي.

يتم استخدام تلوين بصري لتسهيل التمييز:

الأزرق: للموجات الصاعدة

الأحمر: للموجات الهابطة

لون تعبئة مخصص لمناطق التصحيح

🔔 نظام التنبيهات الذكية

يحتوي المؤشر على تنبيهات تلقائية يتم تفعيلها عند اكتمال أي نمط جديد.

يدعم التنبيهات التالية:

موجة دافعة جديدة

تصحيح بسيط ABC

تصحيح معقد WXY

التنبيهات تُطلق بعد إغلاق الشمعة التي تحقق فيها النموذج (غير فوري Repainting-safe)

⚙️ إعدادات المؤشر

📌 إعدادات تحليل الموجة:

Pivot Left Strength: عدد الأعمدة (bars) إلى اليسار لتحديد الانعكاس

Pivot Right Strength: الأعمدة إلى اليمين لتأكيد الانعكاس (0 يعني تنبؤ لحظي)

Enable Fibonacci Rules: تفعيل/تعطيل التحقق من فيبوناتشي

Fibonacci Tolerance: نسبة التفاوت المقبولة بالنسب المئوية

🎨 إعدادات العرض:

Show Previous Patterns: إظهار كل الأنماط المكتشفة أو آخر نمط فقط

PRZ Settings:

إظهار أو إخفاء نسب معينة

تخصيص الألوان

تحديد امتداد مربع PRZ زمنيًا (Max Bars)

🔕 إعدادات التنبيهات:

تفعيل/تعطيل تنبيه عند كل نمط جديد

📚 حالات الاستخدام العملية:

تحليل الحركة السعرية في بداية كل جلسة

دمج المؤشر مع أدوات مثل RSI أو MACD للحصول على إشارات مركّبة

مراقبة الموجات التوسعية والتصحيحية على فواصل 4H / Daily

استخدام PRZ كأداة لتحديد الأهداف أو وقف الخسارة

التعلم العملي لنظرية إليوت من خلال أمثلة حية

📝 ملاحظات مهمة:

تعيين Pivot Right = 0 يعني نقاط فورية (قد يعاد رسمها لاحقًا)

تعطيل فيبوناتشي يزيد عدد النماذج، لكن قد يُضعف دقتها

TradingView يحد عدد الكائنات المرسومة (Labels, Boxes, Lines) إلى 500، مما قد يؤدي إلى حذف الأنماط الأقدم تلقائيًا

PRZ يمتد افتراضيًا حتى 100 شمعة، أو 0.618 من مدة الموجة الدافعة السابقة

⚠️ إخلاء مسؤولية:

هذا المؤشر لأغراض تعليمية وتحليلية فقط. لا يُمثل نصيحة مالية أو استثمارية أو تداولية. استخدمه بالتزامن مع استراتيجيتك الخاصة وإدارة المخاطر. لا يتحمل TradingView ولا المطور مسؤولية أي قرارات مالية أو خسائر.

Scalper - Pattern Recognition & Price Action🔍 Introducing the Ultimate Scalping Toolkit for TradingView

📊 “Scalper – Pattern Recognition & Price Action”

💥 Unlock precision trading with one of the most advanced Pine Script indicators ever built!

✅ Key Features:

📌 Multiple Moving Averages (SMA, EMA, HMA, VWMA & more) – fully customizable per timeframe

🔍 Candlestick Pattern Detection – from Engulfing & Doji to Morning/Evening Stars and Three Soldiers/Crows

⚡ Smart Price Action Tools – Fair Value Gaps, Order Blocks, Breakout Zones

🧠 Confluence Engine – Aggregates multi-signal zones for high-probability entries

📉 Dynamic Support & Resistance Lines – auto-detected from historical swing points

📈 RSI & CCI Reversal Zones – spot hidden turning points before the crowd

🎯 Perfect for Scalpers, Day Traders & Pattern Hunters

💡 This is not just another indicator — it's a complete trading assistant that identifies structure, signals strength, and simplifies decision-making.

🚀 Plug it into your TradingView chart today and start seeing the market in a whole new way.

👉 DM us for access : t.me

Custom Opening TimesThis indicator displays custom opening levels on your chart. Define multiple opening times, each with its own customizable style. Display these levels as horizontal lines at the opening price, or as vertical lines to mark the opening time.

Custom Opening Times

4 Independent Groups with 4 custom opening levels each

Set any custom opening time (displayed in New York Local Time)

Choose between Opening Price lines, Vertical time markers, or Both

Cutoff Times: Stop extending lines after specified times

Higher Timeframe Levels

5 Configurable HTF levels supporting any timeframe

Display opening prices from Daily, Weekly, Monthly, Quarterly, and custom timeframes

Show Previous High/Low levels from higher timeframes

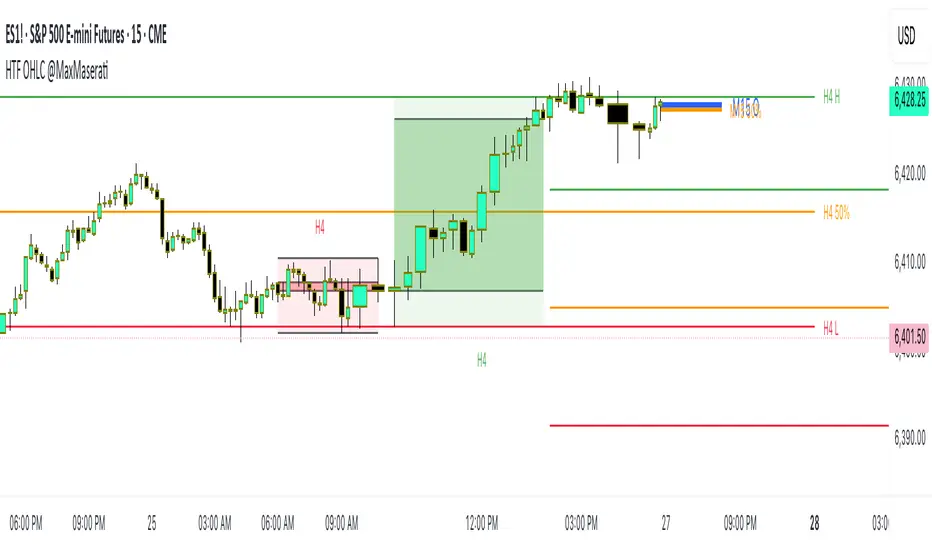

HTF OHLC Candle + 50% @MaxMaseratiHTF OHLC Candle + 50% @MaxMaserati

This advanced multi-timeframe indicator displays higher timeframe OHLC data as visual candle boxes and extended key levels on lower timeframe charts, providing essential context for institutional trading decisions.

Core Functionality:

Multi-Timeframe Box Display:

Main Timeframe Box (Default H4): Shows complete higher timeframe candles as colored boxes with separate body and wick visualization, including bullish (green) and bearish (red) candle representation with customizable transparency levels.

Independent Box 2 (Default M15): Secondary timeframe display with lime/fuchsia color scheme, allowing traders to monitor intermediate timeframes simultaneously with different visual styling.

Independent Box 3 (Default H1): Third independent timeframe with blue/orange color scheme, providing additional context for multi-timeframe analysis and confluence identification.

OHLC Level Analysis:

Each timeframe box includes individual Open, High, Low, and Close level lines with customizable colors and visibility settings. These levels act as key support and resistance zones that institutional traders often respect.

50% Retracement Levels:

Automatic calculation and display of 50% levels between each timeframe's high and low, representing critical equilibrium zones where price often finds support or resistance during retracements.

Extended Line System:

Current Live Timeframe Extended Lines: Real-time extension of the forming candle's Open, High, Low, and 50% levels with customizable line weights and label positioning.

TF2 Extended Lines (Default H4): Previous completed candle's key levels extended forward, showing immediate higher timeframe reference points for current price action.

TF3 Extended Lines (Default Daily): Longer-term reference levels from daily or weekly timeframes, providing macro trend context and major institutional levels.

Key Features:

Smart Timeframe Detection: Only displays boxes for timeframes higher than the current chart timeframe, preventing redundant information and maintaining chart clarity.

Global Box Limit Control: Intelligent cleanup system that maintains optimal performance by limiting total displayed elements while preserving the most recent and relevant timeframe periods.

Comprehensive Customization: Full control over colors, transparency, line weights, label sizes, and visibility for each timeframe component, allowing personalized setups for different trading styles.

Label System: Automatic timeframe identification labels (H4, M15, D1, etc.) positioned on each box for instant timeframe recognition and clear multi-timeframe organization.

Current Candle Options: Optional display of forming/current candles for each timeframe, enabling real-time monitoring of developing price action and potential setup completion.

This indicator is essential for traders utilizing multi-timeframe analysis, institutional trading concepts, and higher timeframe confluence strategies, providing clear visual representation of key levels and candle structures that drive major market movements.

Gann Single Square Swing Trading System with Gann AnglesGann Single Square Swing Trading System

This script automatically detects "squares" - geometric patterns where price movement equals time movement. When price moves the same distance as the number of bars (time), it creates powerful support/resistance levels based on Gann theory.

Key Visual Elements

• Box: The detected square pattern

• Dark Blue Line (50%): Most important trading level

• Green Lines: Profit target levels (125%, 150%)

• Red Lines: Stop loss levels (-25%, -50%)

• Colored Angle Lines: Gann angles for trend direction

• Quality Score: Blue label showing setup strength (aim for 70%+)

Simple Trading Rules

LONG Trades (Green 🟢 Square)

1. Entry: Buy when price touches the dark blue 50% line from above

2. Stop Loss: Place below the red -25% line

3. Take Profit: Exit at green 125% line (first target) or 150% line (second target)

SHORT Trades (Red 🔴 Square)

1. Entry: Sell when price touches the dark blue 50% line from below

2. Stop Loss: Place above the red -25% line

3. Take Profit: Exit at green 125% line (first target) or 150% line (second target)

Entry Checklist

✅ Square quality score > 70%

✅ Price touches 50% level (dark blue line)

✅ Volume above average (if volume filter enabled)

✅ Clear square formation visible

Alerts

The script generates automatic alerts when price reaches the 50% trading level. Enable alerts in TradingView to get notified of setups.

Bottom Line: Wait for the alert → Check quality score → Enter at 50% level → Set stop at red line → Take profit at green line.

Zone of Interest (ZOI) - FractalsZone of Interest (ZOI) with Breakout Start/Exit Alerts

Overview

The Zone of Interest (ZOI) indicator identifies demand and supply zones based on fractal pivots and provides breakout alerts with Start/Exit signals for precise entry and exit interpretation.

Unlike basic breakout indicators that send alerts on every bar, this script ensures clean alerts only at breakout start and breakout end, making it ideal for traders who want clarity without alert spam.

Key Features

✔ Demand & Supply Zones:

Zones created from fractal pivots (swing highs/lows).

Auto-extend zones until expiry.

✔ Breakout Detection:

Detects bullish (price breaks above demand) and bearish (price breaks below supply) breakouts.

✔ Start & Exit Labels:

START LONG when bullish breakout begins.

EXIT LONG when bullish trend ends.

START SHORT when bearish breakout begins.

EXIT SHORT when bearish trend ends.

✔ Clean Alerts:

Alerts fire only on START and EXIT (not every bar).

✔ Visual Cues:

Triangles for every breakout bar (optional visual reference).

Green/Red background shading during active breakout phase.

Inputs

Input - Description

Fractal Length - Number of bars to confirm a fractal pivot.

Zone Expiry (Bars) - Maximum bars before a zone is removed.

Min Distance Between Zones (%) - Prevents overlapping zones by comparing midpoints.

How It Works

Uses fractal pivots to identify swing highs and lows.

Creates Supply Zones (red) from pivot highs and Demand Zones (green) from pivot lows.

Extends zones to the right until expiry or price action invalidates them.

Breakouts occur when price closes beyond the most recent zone boundary.

Tracks breakout phases and fires alerts only at Start and Exit.

✅ Example: How to Use

Suppose you're analyzing XAU/USD on a 15-minute chart:

Step 1: A green demand zone forms at 3344 – 3360.

Step 2: Price pulls back into the zone and starts moving higher.

Step 3: When price closes above 3360, the indicator triggers START LONG and shades the background green.

Step 4: You ride the trend while price remains above the zone.

Step 5: If price later falls back below 3360, an EXIT LONG label appears, and an alert fires.

✅ This helps you avoid spam alerts and focus on key breakout events.

Best Practices

Works well on 15m and higher timeframes.

Combine with trend confirmation (EMA, Supertrend) for better accuracy.

Designed for manual trading and alert-based setups, not automation.

S&R Zones MTF (TechnoBlooms)S&R Zones MTF – Multi-Timeframe Support & Resistance Boxes

🔍 Overview

S&R Zones MTF is a professional-grade yet beginner-friendly indicator that dynamically plots Support & Resistance zones across multiple timeframes, helping traders recognize high-probability reversal areas, entry confirmations, and price reaction points.

This tool visualizes structured zones as colored boxes, allowing both new and experienced traders to analyze multi-timeframe confluence with ease and clarity.

🧠 What Is This Indicator?

S&R Zones MTF automatically detects the most significant support and resistance levels from up to four custom timeframes, using a configurable lookback period. These zones are displayed as colored horizontal boxes directly on the chart, making it easy to:

Spot where price has historically reacted

Identify potential reversal or breakout zones

Confirm entries with institutional-style precision

🛠️ Key Features

✅ Multi-Timeframe Zone Detection (up to 4 timeframes)

📦 Auto Plotted Boxes for Support (Blue) & Resistance (Pink)

🧱 Dynamic Height based on average price range or fixed input

🏷️ Timeframe Labels to instantly identify zone origin

🎛️ Customizable inputs: Lookback length, box color, height style

🔁 Real-time updates as price structure changes

🎓 Educational & Easy to Use

Whether you’re a new trader learning about price structure, or a professional applying institutional concepts, this tool offers an educational layout to understand:

How price respects historic zones

Why multi-timeframe zones offer stronger confluence

How to use zones for entry, exit, or risk placement

📈 How to Use (Multi-Timeframe Strategy)

Select Your Timeframes – Customize up to 4 higher timeframes (e.g., 1m, 5m, 15m, 1h).

Observe Overlapping Zones – When multiple timeframes agree, those zones are more significant.

Entry Confirmation – Wait for price to reach a zone, then look for reversal patterns (engulfing candle, pin bar, etc.)

Combine with Other Tools – Use alongside indicators like RSI, MACD, or Order Blocks for added confidence.

💡 Pro Tips

Zones from higher timeframes (1H, 4H) are often more powerful and reliable.

Confluence matters: If a 15m support zone aligns with a 1H support zone — that's a high-probability reaction area.

Use break-and-retest strategies with zone rejections for sniper entries.

Enable "Auto Height" for a more adaptive, volatility-based zone display.

🌟 Summary

S&R Zones MTF blends precision, clarity, and professional analysis into a visual structure that’s easy to understand. Whether you're learning support & resistance or optimizing your MTF edge — this tool will bring clarity to your charts and confidence to your trades.

SulLaLuna PO3 Acceleration Tracker### 🚀 **Power of 3 Acceleration Script | Enter the Cave of Wonder 🧙♂️**

> *“When we find the God Candle, we don’t just ride it—we ritualize it.”*

> — The Calzolaio Way

🌕 The **SulLaLuna PO3 Acceleration Tracker** is a tool born from Smart Money theory, built with surgical logic, and forged to ride the **acceleration phase** with confluence and confidence.

Inspired by the teachings of (youtu.be), this indicator captures the moment of explosive expansion—the candle after the manipulation wick, the price action spark that ignites the trend.

---

### ⚔️ The PO3 Framework (ICT)

* **Accumulation** – Compression, trap laid

* **Manipulation** – Liquidity taken, fakeouts triggered

* **Expansion** – God Candle. This is where we enter.

This script automatically detects that exact **post-manipulation acceleration** candle and plots:

* ✅ TP/SL based on risk-reward

* ✅ Dynamic trend dashboard (15m to 1D)

* ✅ Long/Short trade markers

* ✅ Custom alerts and dashboard positioning

---

### 🔁 **Use Confluence**

> ⚠️ *No entry should ever be made on one signal alone.*

For optimal precision, pair this script with a **trend-strength and momentum filter**.

I personally use (), a brilliant tool that dynamically adapts to volatility and momentum changes using a responsive EMA and wave strength logic. It's CC BY-NC-SA 4.0 licensed and adds serious edge in distinguishing true trends from false breaks.

💡 Look for PO3 entries that align with:

* ✅ Bullish dominance in trend speed

* ✅ Dynamic EMA slope support

* ✅ MTF Trend agreement on the SulLaLuna dashboard

---

### ✨ The Cave of Wonder

This is more than just a script—this is your **map**.

The Cave of Wonder isn’t a place, it’s a **process**. Each PO3 entry is a torch lighting the path deeper into the vaults of financial freedom.

When you use this with **discipline**, **data**, and **divine timing**, you don't just take trades.

You take **territory**.

---

### 🔗 Try It. Trade It. Ritualize It.

🛠️ Built by @Calzolaio

🎓 Based on PO3 by @TheMovingAverage

📊 Powered by trend confluence from @Zeiierman

> “Capture the Acceleration. Honor the Trend. Trade with the Moon.” 🌕

Market Adjusted EMAGabriel’s Market Adjusted EMA (MAD) is a dynamically weighted exponential moving average that adapts to three core market forces:

🔹 Price Strength (75%) – Choose between traditional RS-based EMA or slope-sensitive Linear Regression EMA for trend responsiveness.

🔹 Volume Pressure (23%) – Uses volume or ATR-based logic to reflect demand/supply shifts.

🔹 Volatility Risk (2%) – Adapts based on the real VIX or fallback Williams VIX Fix for non-equities.

MAD uses Hurst-inspired weighting and π-based multipliers to normalize responsiveness across assets. It’s ideal for identifying dynamic trend shifts and acts as a context-aware anchor for price action strategies.

✅ Built-in alert when price crosses MAD.

⚙️ Customizable inputs for VIX, volume type, and slope adjustment.

🎯 Suitable for equities, crypto, and futures alike.

CBC Flip with Volume [Pt]█ CBC Flip with Volume

A price-action based indicator that detects real-time control flips between bulls and bears, enhanced with volume filtering and Pine Screener compatibility.

This tool tracks when the market shifts from bear control to bull control or vice versa, using candle structure and volume behavior. It highlights key reversal points, filters low-conviction moves, and provides two screener-ready outputs for directional monitoring.

█ What It Detects

This script identifies when control flips between buyers and sellers on a candle-by-candle basis. A flip is confirmed only when both price structure and volume meet strict criteria. The indicator uses an internal state to track who is in control and updates when a flip occurs.

█ Flip Conditions

Bull Flip

• Previous bar was under bear control

• Current candle closes above the previous high

• Candle is bullish (close is above open)

• Volume is greater than the previous bar

Bear Flip

• Previous bar was under bull control

• Current candle closes below the previous low

• Candle is bearish (close is below open)

• Volume is greater than the previous bar

When a flip occurs, the indicator updates the control state and records the open price of the flip candle.

█ Strong Flip Detection

A flip is considered strong when volume is also greater than the average volume over a set number of candles (default is 50). Strong flips are visually emphasized using larger markers and darker background shading. This helps filter out moves that lack follow-through volume.

█ Visual Elements on Chart

• Bull Flip (Normal): Small teal triangle below the candle

• Bull Flip (Strong): Larger green triangle below the candle

• Bear Flip (Normal): Small salmon triangle above the candle

• Bear Flip (Strong): Larger red triangle above the candle

• Background Color:

– Green shades for bull flips

– Red shades for bear flips

– Darker color when flip is strong

These visual elements appear only on the candle where a flip is detected. No markers are shown on continuation candles.

█ Inputs

• Volume MA Lookback : Sets the moving average length used for determining whether volume is high enough for a strong flip (default: 50)

█ Alerts

• Bull Flip – Notifies when bulls take control

• Bear Flip – Notifies when bears take control

Alerts are triggered at candle close.

█ Pine Screener Support

This script includes two output columns for TradingView’s Pine Screener:

• Bull in Control (% gain) : Shows the percentage gain from the bull flip’s open to the current close. Resets to 0 when bulls lose control.

• Bear in Control (% gain) : Shows the percentage drop from the bear flip’s open to the current close (as a positive number). Resets to 0 when bears lose control.

These outputs allow you to filter for active moves. For example:

• Bull in Control (% gain) > 2.0 to find strong uptrends

• Bear in Control (% gain) > 1.5 to find sharp breakdowns

█ Use Cases

• Confirm breakouts using volume-backed flips

• Spot short-term reversals at key zones

• Filter out low-volume chop

• Combine screener results with trend or volatility filters

• Build entries around control flips and follow-through strength

Inspired by MapleStax’s original CBC method.

Date Marker GPTDate Marker GPT

By Jimmy Dimos (corrected by ChatGPT-o3)

Description

This overlay indicator automatically plots vertical lines at each weekly option-expiration timestamp (Friday at 3 PM CST) for both historical and upcoming periods, helping you visualize key expiration dates alongside your price action and regression tools. Shown is my Date Maker GPT vertical blue Lines, Linear Regression Channel(not part of my script) and zigzag++ also not part of my script.

⸻

Key Features

• Past Expirations: Draws 12 past Friday markers at 3 PM CST

• Future Expirations: Projects 12 upcoming Friday markers at 3 PM CST

• Timezone Handling: Uses UTC internally (21:00 UTC = 3 PM CST)

• Customizable: num_fridays_past and num_fridays_future inputs let you adjust how many weeks to display

⸻

How It Works

1. Timestamp Calculation

• Uses Pine Script’s dayofweek() and timestamp() functions to find each Friday at the target hour.

• Two helper functions, get_previous_friday() and get_next_friday(), compute offsets in days/weeks based on the current bar’s date.

2. Drawing Lines

• Loops through the specified number of weeks in the past and future.

• Calls line.new() for each expiration timestamp, extending lines across the entire chart.

⸻

Usage Tips

• Overlay this script on any OHLC chart to see how price tends to cluster around option expirations.

• Combine with a linear regression or trend-channel indicator to anticipate likely trading ranges leading into expiration.

• Tweak the num_fridays_past and num_fridays_future parameters to focus on shorter or longer horizons.

⸻

Disclaimer: This tool is provided for educational and analytical purposes only. It is not financial advice. Always conduct your own research and risk management.

Breath Trade OB AlertThis is a indicator that is written specifically for BTCUSD 5 minutes trade

when this indicator occur .Just enter the position with the write director.

and exit when 50 EMA reached.

Triple Momentum Core v1🧠 Technical Structure:

Triple Momentum Core analyzes the underlying wave of price movement through a three-stage system:

1. 🔵 Follow Line – The First Spark of Momentum:

Constructed using Bollinger Bands and ATR, this line detects the very first signs of directional price expansion. It gently whispers when the market begins stretching with force in one direction.

2. 🟢 SuperTrend – Confirmation and Directional Validation:

After the initial move, SuperTrend acts as the second checkpoint — validating whether the price action is evolving into a genuine trend or fading out. It confirms whether the impulse has the strength to sustain.

3. 🔴 PMax – Core Trend & Structural Anchor:

Based on Moving Average and ATR logic, PMax tracks the heartbeat of the trend. It serves as a dynamic structural boundary — critical for identifying trend continuation and managing risk.

4. 🟡 PMax MA Line – Smooth Trend Pulse & Adaptive Guide:

This yellow moving average line within the PMax system softly follows the overall trend flow, without reacting to sharp price noise. It acts as a balanced, stable guide to gauge the solidity of the trend’s body structure.

(If you prefer a cleaner view without any moving average lines, you can disable it from the settings.)

🧠 Technical Structure:

Triple Momentum Core analyzes the underlying wave of price movement through a three-stage system:

1. 🔵 Follow Line – The First Spark of Momentum:

Constructed using Bollinger Bands and ATR, this line detects the very first signs of directional price expansion. It gently whispers when the market begins stretching with force in one direction.

2. 🟢 SuperTrend – Confirmation and Directional Validation:

After the initial move, SuperTrend acts as the second checkpoint — validating whether the price action is evolving into a genuine trend or fading out. It confirms whether the impulse has the strength to sustain.

3. 🔴 PMax – Core Trend & Structural Anchor:

Based on Moving Average and ATR logic, PMax tracks the heartbeat of the trend. It serves as a dynamic structural boundary — critical for identifying trend continuation and managing risk.

4. 🟡 PMax MA Line – Smooth Trend Pulse & Adaptive Guide:

This yellow moving average line within the PMax system softly follows the overall trend flow, without reacting to sharp price noise. It acts as a balanced, stable guide to gauge the solidity of the trend’s body structure.

(If you prefer a cleaner view without any moving average lines, you can disable it from the settings.)

💡 Why “Triple Momentum Core”?

Because this indicator doesn’t just detect movement — it breaks it down into its essential phases:

Ignition, validation, and confirmation.

Each layer captures a unique and essential part of price behavior:

The first reaction (Follow Line) ignites the initial spark.

The second reaction (SuperTrend) confirms whether that spark will become a real trend.

The third and final layer (PMax) structurally anchors and follows that trend.

That’s why we call it Triple Momentum Core:

A synchronized 3-engine momentum system working in harmony to capture the lifecycle of a trend — from spark to structure.

Key Indicators Dashboard (KID)📌 Overview

Key Indicators Dashboard (KID) is a comprehensive all-in-one technical analysis tool designed for discretionary, systematic, and quantitative traders. It brings together multiple essential trading metrics into a highly customizable, interactive dashboard that overlays directly on your TradingView chart.

🎯 What Does KID Do?

KID consolidates all vital market metrics into a single, glanceable dashboard—saving screen space and analysis time. Whether you are screening equities or monitoring open positions, the KID panel updates dynamically, highlighting actionable signals and market conditions based on your own thresholds and trading style.

🛠 Key Features

⦿ Volatility and Range Metrics

ADR (Average Daily Range, % and Value): Quantifies average price movement over a defined period, with threshold-based color highlights.

ATR (Average True Range, % and Value): Measures volatility as both value and percentage of price.

⦿ Relative Strength and Trend Metrics

Relative Strength (RS) vs. Benchmark: Dynamically calculated using a customizable comparative symbol (default: NSE:NIFTYMIDSML400).

IBD-style RS Rating: Weighted average of price changes over several periods (3, 6, 9, and 12 months).

Trend Detection: Uses Supertrend indicator to visually identify up/down market trends.

⦿ Liquidity and Volume Analysis

Relative Volume (RVol): Comparison of current volume to moving average volume.

Turnover (in Cr): Average turnover calculation to assess liquidity.

Market Cap & Free Float: Real-time computation using price and outstanding/floating shares.

⦿ Trend Strength and Structure

MA Extensions: Compares price extension from a selected moving average, depicted as ATR multiples and percentages.

Moving Averages (MAs): Choice of EMA/SMA with customizable lengths, including up to four plotted MAs and detection of MA crossovers.

⦿ Breakout and Tightness Detectors

52-Week High/Low: Calculates and optionally marks the highest and lowest prices over 252 trading days, including percentage distance from current price.

Minervini Trend Template: The Trend Template is a set of technical criteria designed to identify stocks in strong uptrends.

• Price > 50-DMA > 150-DMA > 200-DMA

• 200-DMA is trending up for at least 1 month

• Price ≥ 52-week high proximity

• Price is at least 30% above its 52-week low.

• Price is within at least 25 percent of its 52-week high

• Table highlights when a stock meets all above criteria.

Tightness Indicator: Highlights periods with compressed price action relative to historical ranges.

⦿ Candlestick Patterns and Power Bars

Inside Bar Detection: Color- and shape-based highlighting of "inside bars" for pattern traders.

PowerBar (Purple Dot): Flags bars with strong price movement paired with high volume, using ROC and volume thresholds.

⦿ Sector/Industry

Automatically reflects symbol sector and industry if available from trading platform data.

⚙️ Customizable Visualization

Switchable between vertical or horizontal layout.

Works in dark/light mode

User-configurable to toggle any indicator ON or OFF.

User-configurable Moving (EMA/SMA), Period/Lengths and thresholds.

🔔 Built-in Alerts

Supports automatic alert creation for:

ADR%, ATR/ATR %, RS, RS Rating, Turnover

Moving Average Crossover (Bullish/Bearish)

52-Week High/Low

Inside Bars (Bullish/Bearish)

Tightness

Minervini Trend Template

⏳PineScreener Capabilities

The indicator’s alert conditions act as filters for PineScreener.

Available Screener Filters & Alerts:

Price Filters: Minimum and maximum price cutoffs.

Daily Change Filters: Minimum and maximum daily percent move.

Volatility Filters: ADR% and ATR% thresholds met or exceeded.

Liquidity Filters: Minimum average turnover and relative volume cutoffs.

Momentum/Trend Filters:

• Strong RS/RS Rating

• Uptrend/Downtrend state (Supertrend-based)

• Price extensions (detect overbought/oversold situations quickly)

• Breakout proximity via 52-week high/low alerts

Pattern and Setup Detection:

• Minervini Trend Template

• Inside Bar

• Tightness (compressed/volatility contraction setups)

• PowerBar (High ROC + high volume bars)

• MA crossover or above/below specific MAs

⦿ (Optional) : For horizontal table orientation increase Top Margin to 16% in Chart (Canvas) settings to avoid chart overlapping with table.

⚡ Add this script to your chart and start making smarter trade decisions today! 🚀

Prev Candle Quarters (MTF) – % + PriceThis TradingView indicator visualizes quarter levels (25%, 50%, 75%, 100%) of the previous candle body from a user-selected higher timeframe, helping traders identify key reaction zones within a candle’s structure.

ulti-Timeframe Input: Choose between 15m, 1H, or 2H candles for your measurement basis.

Body-Based Calculation: Measures from open to close of the previous candle (not wick-to-wick), reflecting where price actually closed.

Precise Quarter Levels: Automatically draws horizontal lines at 25%, 50%, 75%, and 100% of the candle body.

Custom Toggles: Enable or disable each individual level via checkboxes.

Price + % Labels: Each level includes a clean label showing the exact price and corresponding percentage.

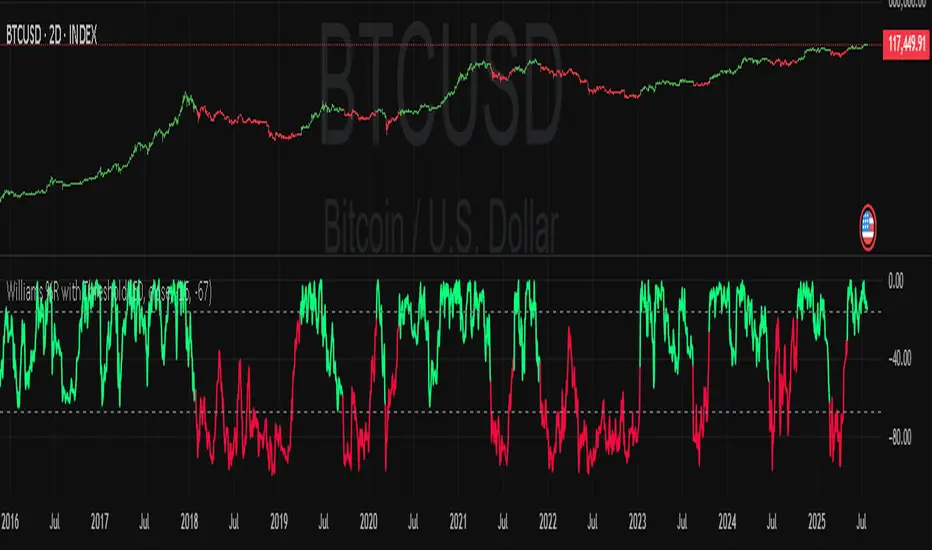

Williams Percent Range with ThresholdEnhance your trading analysis with the "Williams Percent Range with Threshold" indicator, a powerful modification of the classic Williams %R oscillator. This custom version introduces customizable uptrend and downtrend thresholds, combined with dynamic candlestick coloring to visually highlight market trends. Originally designed to identify overbought and oversold conditions, this script takes it a step further by allowing traders to define specific threshold levels for trend detection, making it a versatile tool for momentum and trend-following strategies.

Key Features:

Customizable Thresholds: Set your own uptrend (default: -16) and downtrend (default: -67) thresholds to adapt the indicator to your trading style.

Dynamic Candlestick Coloring: Candles turn green during uptrends, red during downtrends, and gray in neutral conditions, providing an intuitive visual cue directly on the price chart.

Flexible Length: Adjust the lookback period (default: 50) to fine-tune sensitivity.

Overlay Design: Integrates seamlessly with your price chart, enhancing readability without clutter.

How It Works:

The Williams %R calculates the current closing price's position relative to the highest and lowest prices over a specified period, expressed as a percentage between -100 and 0. This version adds trend detection based on user-defined thresholds, with candlestick colors reflecting the trend state. The indicator plots the %R line with color changes (green for uptrend, red for downtrend) and includes dashed lines for the custom thresholds.

Usage Tips:

Use the uptrend threshold (-16 by default) to identify potential buying opportunities when %R exceeds this level.

Apply the downtrend threshold (-67 by default) to spot selling opportunities when %R falls below.

Combine with other indicators (e.g., moving averages or support/resistance levels) for confirmation signals.

Adjust the length and thresholds based on the asset's volatility and your trading timeframe.

Market to NAV Premium Arbitrage Alpha IndicatorBitcoin treasury companies such as Microstrategy are known for trading at significant premiums. but how big exactly is the premium? And how can we measure it in real time?

I developed this quantitative tool to identify statistical mispricings between market capitalization and net asset value (NAV), specifically designed for arbitrage strategies and alpha generation in Bitcoin-holding companies, such as MicroStrategy or Sharplink Gaming, or SPACs used primarily to hold cryptocurrencies, Bitcoin ETFs, and other NAV-based instruments. It can probably also be used in certain spin-offs.

KEY FEATURES:

✅ Real-time Premium/Discount Calculation

• Automatically retrieves market cap data from TradingView

• Calculates precise NAV based on underlying asset holdings (for example Bitcoin)

• Formula: (Market Cap - NAV) / NAV × 100

✅ Statistical Analysis

• Historical percentile rankings (customizable lookback period)

• Standard deviation bands (2σ) for extreme value detection (close to these values might be seen as interesting points to short or go long)

• Smoothing period to reduce noise

✅ Multi-Source Market Cap Detection

• You can add the ticker of the NAV asset, but if necessary, you can also put it manually. Priority system: TradingView data → Calculated → Manual override

✅ Advanced NAV Modeling

• Basic NAV: Asset holdings + cash.

• Adjusted NAV: Includes software business value, debt, preferred shares. If the company has a lot of this kind of intrinsic value, put it in the "cash" field

• Support for any underlying asset (BTC, ETH, etc.)

TRADING APPLICATIONS:

🎯 Pairs Trading Signals

• Long/Short opportunities when premium reaches statistical extremes

• Mean reversion strategies based on historical ranges

• Risk-adjusted position sizing using percentile ranks

🎯 Arbitrage Detection

• Identifies when market pricing significantly deviates from fair value

• Quantifies the magnitude of mispricing for profit potential

• Historical context for timing entry/exit points

CONFIGURATION OPTIONS:

• Underlying Asset: Any symbol (default: COINBASE:BTCUSD) NEEDS MANUAL INPUT

• Asset Quantity: Precise holdings amount (for example, how much BTC does the company currently hold). NEEDS MANUAL INPUT

• Cash Holdings: Additional liquid assets. NEEDS MANUAL INPUT

• Market Cap Mode: Auto-detect, calculated, or manual

• Advanced Adjustments: Business value, debt, preferred shares

• Display Settings: Lookback period, smoothing, custom colors

IT CAN BE USED BY:

• Quantitative traders focused on statistical arbitrage

• Institutional investors monitoring NAV-based instruments

• Bitcoin ETF and MSTR traders seeking alpha generation

• Risk managers tracking premium/discount exposures

• Academic researchers studying market efficiency (as you can see, markets are not efficient 😉)

VIX‑Based σ‑BandsThis Pine Script v5 indicator builds a volatility‑based envelope around yesterday’s close using CBOE’s volatility indices. It dynamically pulls VIX, VXN, VXD or RVX—depending on whether you’re charting ES, NQ, YM or RTY—and converts annualized volatility into dollar‑move bands at ±¼ σ, ±½ σ, ±1 σ, and ±2 σ. Optional “mid‑lines” fill in the gaps between each band for even finer precision.

Supertrend with ADX & MTF MA Filter# **Supertrend with ADX & MTF MA Filter - Comprehensive Explanation**

---

## **1. Purpose of This Indicator**

This indicator combines three powerful technical analysis tools to create a robust trading system:

✅ **Supertrend** (Trend-following)

✅ **ADX Filter** (Trend strength confirmation)

✅ **MTF MA Filter** (Multi-timeframe trend direction confirmation)

**Primary Goals:**

✔ **Identify high-probability trend reversals** with confirmation from multiple indicators

✔ **Filter out weak trends** using ADX (Average Directional Index)

✔ **Add higher timeframe context** with MTF (Multi-TimeFrame) Moving Average

✔ **Reduce false signals** by requiring confluence between all three components

---

## **2. Core Logic & Components**

### **A. Supertrend (Base Indicator)**

- **Calculation:**

```pine

up = hl2 - (Multiplier * ATR(Periods))

dn = hl2 + (Multiplier * ATR(Periods))

```

- **Bullish trend** when price > `up` (green line)

- **Bearish trend** when price < `dn` (red line)

- **Why Supertrend?**

- Simple yet effective trend-following system

- Adapts to volatility via ATR (Average True Range)

---

### **B. ADX Filter (Trend Strength Confirmation)**

- **ADX Calculation:**

```pine

= calcADX(adxLength, adxSmoothing)

strongTrend = adxVal >= adxThreshold

```

- **ADX > Threshold (Default: 20)** = Strong trend

- **DI+ > DI-** = Bullish momentum

- **DI- > DI+** = Bearish momentum

- **Why ADX?**

- Avoids trading in choppy markets (low ADX = weak trend)

- Confirms if Supertrend signals occur in a strong trend

---

### **C. MTF MA Filter (Higher Timeframe Trend Alignment)**

- **Moving Average Calculation:**

```pine

= getMA(maSource, maLength, maType, maTF)

```

- **MA Type:** SMA, EMA, WMA, or DEMA

- **Timeframe:** Any (1m, 5m, 1H, 4H, D, W, M)

- **Trend Direction:**

- **Buy Signal:** MA must be **rising**

- **Sell Signal:** MA must be **falling**

- **Why MTF MA?**

- Aligns trades with the **higher timeframe trend**

- Reduces counter-trend entries

---

## **3. How to Use This Indicator**

### **A. Buy Conditions (All Must Be True)**

1. **Supertrend turns bullish** (price crosses above `up` line)

2. **ADX ≥ Threshold** (trend is strong)

3. **Higher timeframe MA is rising** (confirms bullish bias)

### **B. Sell Conditions (All Must Be True)**

1. **Supertrend turns bearish** (price crosses below `dn` line)

2. **ADX ≥ Threshold** (trend is strong)

3. **Higher timeframe MA is falling** (confirms bearish bias)

### **C. Recommended Settings**

| Parameter | Recommended Value | Description |

|-----------|------------------|-------------|

| **ATR Period** | 14 | Sensitivity of Supertrend |

| **Multiplier** | 1.5-3.0 | Adjust for volatility |

| **ADX Threshold** | 20-25 | Higher = stricter trend filter |

| **MA Length** | 20-50 | Smoothness of trend filter |

| **MA Timeframe** | 1H/D | Align with trading style |

---

## **4. Trading Strategies**

### **A. Trend-Following Strategy**

- **Enter:** When all 3 conditions align (Supertrend + ADX + MA)

- **Exit:** When Supertrend flips or ADX drops below threshold

### **B. Pullback Strategy**

- **Wait for:**

- Supertrend in trend direction

- ADX remains strong

- MA still aligned

- **Enter:** On pullback to Supertrend line

### **C. Multi-Timeframe Confirmation**

- **Intraday traders:** Use 4H/D MA for trend bias

- **Swing traders:** Use D/W MA for trend bias

---

## **5. Advantages Over Standard Supertrend**

✔ **Fewer false signals** (ADX filters weak trends)

✔ **Higher timeframe alignment** (avoids trading against larger trends)

✔ **Customizable MA types** (SMA, EMA, WMA, DEMA)

✔ **Works on all markets** (stocks, forex, crypto)

---

### **Final Thoughts**

This indicator is designed for traders who want **high-confidence trend signals** by combining:

🔹 **Supertrend** (entry trigger)

🔹 **ADX** (trend strength filter)

🔹 **MTF MA** (higher timeframe trend alignment)

By requiring all three components to align, it significantly improves signal quality compared to standalone Supertrend systems.

**→ Best for:** Swing trading, trend-following, and avoiding choppy markets.