Broadcom Middle of Range RisksI like Broadcom if it gets down to $178. Right now it's still floating from the AAPL news. I wouldn't be inclined to sell here, but if looking to buy (like myself) I'd wait in hopes for $178.

Target (Potential Next Support) $302.

Good luck!

SEMI

Nvidia Just Under Major SupportNvidia seems to have been pulled down by the Dow just like Apple as both are just under major support. I'm sorry for my previous Nvidia chart that drew support near 140, I recognize where I screwed up, but this chart should be good. Fortunately actual 117 support wasn't that far below and my NVDA isn't too in the red.

NVDA has the lowest revenue multiple in years right now. I know it's well off it's long term trend line, but it's growth rate is unlike anything it's ever been so expecting a steeper trend line to appear makes a lot of sense. Eventually I would imagine we'll get back to that trend line, but not anytime soon.

The Dow hitting major support should finally lift NVDA and the others that have been dragged down like AAPL and AMZN.

Good luck!

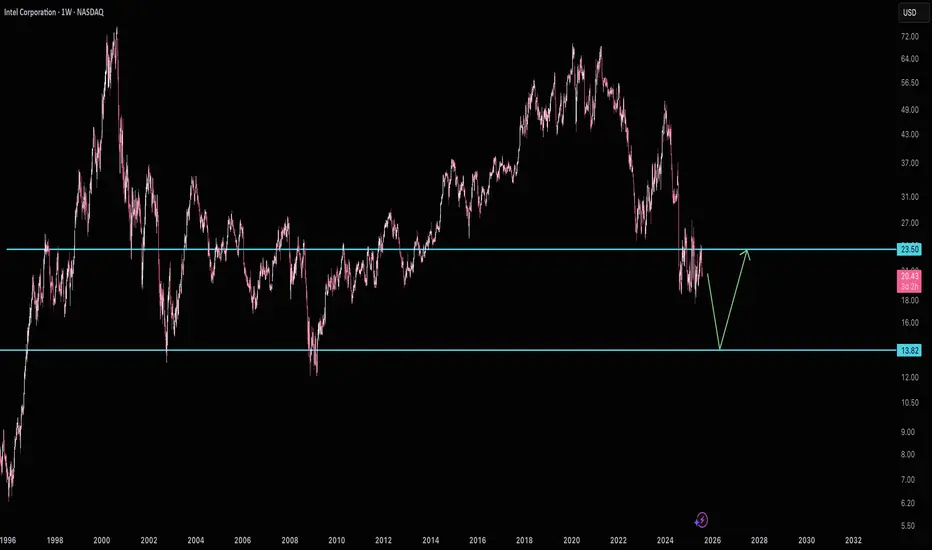

Intel looks to want $13Intel looks to be waiting below $24 resistance for $13 support. I wouldn't short it at it's current price, but I would be patient and wait for $13 if you're looking to buy. Good luck!

Monolithic Power | MPWR | Long at $580.00Monolithic Power $NASDAQ:MPWR. If the semiconductor market continues to get attention in connection with AI, there may be a bounce here near $580.00 as NASDAQ:MPWR enters my historical simple moving average area. However, a further dip into the high $400s wouldn't surprise me (tax harvesting season is in session) and doesn't change the thesis as long as the overall trend continues to stay positive. While NASDAQ:MPWR is a strong company with growth predictions on the horizon, it has a 65x P/E, 46x price-to-cash flow, lots of insider selling, and some near-term concern if the economy shows weakness. From a technical analysis perspective, though, it's in an area of opportunity as long as semis stay a "hot" investment. Thus, at $580.00, NASDAQ:MPWR is in a personal buy zone.

Target #1 = $690.00

Target #2 = $745.00

Target #3 = $825.00

Target #4 = $908.00

Semiconductors Finishing Consolidation for Next Move UpSemi's are ready to move after a long consolidation. This is a big signal for Nvidia that is likely to lead and significantly outperform.

Good luck!

TSM 246 BY 2025 High Demand for Advanced Chips: TSMC is at the forefront of producing chips for AI, 5G, and IoT applications. The increasing demand for these technologies, especially AI chips which power both consumer and enterprise solutions, could drive revenue growth. Posts on X and web results show TSMC's Q3 2024 earnings were significantly up year-over-year due to AI demand, suggesting a strong trajectory for chip sales.

Technological Leadership: TSMC's ability to manufacture chips at smaller process nodes (like 3nm and the upcoming 2nm) gives it a competitive edge over rivals. The company's advancements in semiconductor technology are critical for producing high-performance, energy-efficient chips. Web results discuss the introduction of 2nm chips in 2025, which could further solidify TSMC's market position and justify a higher stock valuation.

Customer Base and Market Share: TSMC services major tech companies like Apple, Nvidia, and AMD, giving it a stable and growing customer base. Its dominance in the foundry market (over 50% market share) means it's integral to the success of many tech products. The company's partnerships, particularly with Nvidia for AI chips, as noted in posts on X, could significantly boost its revenue.

Geopolitical Strategy: While there are risks associated with Taiwan's geopolitical situation, TSMC's strategy of diversifying its manufacturing base (e.g., expanding in the U.S., Japan, and Europe) mitigates some of these risks. This expansion could tap into new markets and reduce dependency on its facilities in Taiwan, potentially stabilizing or even increasing investor confidence.

Financial Performance: TSMC has demonstrated strong financial health with consistent revenue growth, impressive profit margins, and substantial free cash flow. According to web results, TSMC's revenue growth rate could reach 20%-25% in 2025, with a gross margin potentially peaking at 50%, which could positively impact its stock price.

Investment in R&D and Capacity Expansion: TSMC's commitment to R&D ensures it remains at the cutting edge of semiconductor technology. The company's plans for capacity expansion, particularly in advanced processes, are designed to meet the growing demand. The increased capacity for CoWoS packaging, as mentioned in posts on X, is expected to address the robust demand driven by AI.

Analyst Forecasts and Market Sentiment: Analysts have been bullish on TSMC, with some predicting that the stock could hit high targets due to its pivotal role in tech supply chains. Web results from financial analysts and stock forecast sites suggest positive sentiment, with some projecting the stock to reach or exceed $246 by 2025 based on current trends and forecasts.

Long-term Growth Prospects: The semiconductor industry is expected to grow due to the proliferation of connected devices, data centers, and the automotive sector moving towards more electrification and automation. TSMC's position in this landscape suggests long-term growth, which could drive its stock price higher.

NVIDIA 200 BEFORE 2026 !!! CAFE CITY STUDIO

NVIDIA (NVDA) has been at the forefront of technological innovation, particularly in the realms of AI and graphics processing, positioning it well for significant stock price growth. Here are several reasons why NVIDIA's stock might hit $200 by 2025:

Dominance in AI and Data Center Markets:

NVIDIA's GPUs are the backbone for many AI and machine learning applications. Their leadership in this space, especially with the advent of AI-driven technologies across industries, is expected to keep revenue growth robust. The company's data center segment has seen exponential growth, with analysts predicting a continued upward trend due to the increasing demand for computing power in AI applications.📷📷📷

Strategic Product Roadmap:

NVIDIA's product pipeline, including the Blackwell architecture, is anticipated to propel the company forward. The Blackwell chips, expected to launch in 2025, are designed to push performance boundaries for AI applications, potentially capturing more market share and driving revenue. The expectation around these new architectures creates a bullish outlook for

NVIDIA's stock.📷📷

Strong Financial Performance:

NVIDIA's financial results have consistently outperformed expectations. For instance, Q2 FY 2025 saw a revenue increase of 122% year over year, demonstrating the company's ability to maintain high growth rates. Despite a natural slowdown expected due to tougher year-over-year comparisons, the company's growth is still projected to be impressive at around 43% for FY 2026, supporting a narrative of sustained stock price appreciation.📷📷

High Barriers to Entry and Market Moats:

The complexity and performance of NVIDIA's offerings create high barriers for competitors, ensuring NVIDIA's market leadership. Analysts highlight NVIDIA's 24-month technological lead in AI GPUs, with high switching costs for customers locked into NVIDIA's ecosystem. This moat is expected to support premium pricing and market share retention, which could translate into stock value growth.📷📷

Analyst Optimism:

Numerous Wall Street analysts have set price targets for NVIDIA well above its current levels, with some predicting it could hit $200 or more by 2025. These forecasts are based on NVIDIA's strong fundamentals, technological edge, and market position in AI and computing solutions.📷📷

Market Sentiment and Valuation:

Even though NVIDIA's stock trades at a premium valuation (62 times trailing earnings as of recent data), analysts believe that its growth trajectory justifies this price. If NVIDIA continues to meet or exceed growth expectations, its valuation could expand further, driving the stock price towards $200. However, achieving this target would require either a significant earnings surge or a market sentiment favoring even higher multiples for tech growth stocks.📷

Global AI Adoption:

Posts on X highlight the ongoing global shift towards AI, with NVIDIA at the forefront. The demand for NVIDIA's computing solutions is expected to grow as AI becomes more integral to various sectors, from automotive to cloud computing, thereby supporting stock price growth.

ASML Holding | ASML | Long at $680.00NASDAQ:ASML Holding, a developer and servicer of advanced semiconductor equipment systems for chipmakers, dipped backed into my overall, long-term selected simple moving average (SMA). From here, stocks typically bounce or drop, but given the AI boom is far from "over", I anticipate another bounce to eventually close the gap near $1,060. It may show some minor weakness to close the gap in the low $600s and get the bears excited. But, unless the economy further shows major weakness in the semiconductor space, NASDAQ:ASML is in my personal "buy zone" at $680.

Target #1 = $730.00

Target #2 = $915.00

Target #3 = $1,060.00

AVGO Getting tightPrice is consolidating inside this ascending triangle and getting tight

I have been noticing some good call flow on the 185 Strike.

I am adding this to my watchlist for a break of the resistance and a move higher towards 200

SMCI is going...Price broke above descending triangle, I like it above $28

With NVDA strength, this is probably a great setup to retest $31 today

Watching this closely

$NVDA $650 by 6/1Welp.... say it ain't so... do what you want of course... I have this target by June 1st of this year. Refer to 22' Top.

$AMD Recognize where and whyThis is a chart I created several weeks ago. I find these points of inflection fantastic for support or resistance depending on the PA of course. I've drawn these on several tickers and the outcome is almost always the same. This is just information. Do what you want with it.

Upward trending channel - ASX:SEMI (Long)SEMI currently sitting on upward trend line within established bullish channel.

Previous support line at $16.30 where demand triggered another uptrend to above $17.00.

RSI currently within average buying levels around ~56-60% showing higher highs, indicating another potential run back towards previous ATH SP level of $17.54.

Aiming to take a long position between $17.00 - $17.10 if buying pressure increases in the coming days.

Disclaimer: NOT financial advice, I am not a qualified finance profession. These ideas are my own based on my research. Please consult a licensed financial advisor before making any investment decisions.

ASML Holding Options Ahead of EarningsAnalyzing the options chain of ASML Holding prior to the earnings report this week,

I would consider purchasing the 760usd strike price Puts with

an expiration date of 2023-7-21,

for a premium of approximately $20.55.

If these options prove to be profitable prior to the earnings release, I would sell at least half of them.

Looking forward to read your opinion about it.

SMH - TECH Welfare @ $282 Billion / $25B Tax Credit PerNancy and the Gang anxiously await the Senates Taxpayer handout to the Industry.

Po Nancy, $107 Million simply is not enough for her and Pablo the Shark Tank Drunk.

Nancy had to gobble $341K in losses on NVDA after exiting her 25K Shares in a loss due

to slime lights a shinning.

Bravo, add 3 zeros and it's all good.

Everyone should lose a hand.

Preferably, a head.

__________________________________________________________________________

They'll need to expedite this Grift Gift as China's warned off the Carrier Group as well

as Fancy - show up and it's going to be "A Dangerous Moment"... Nancy risks our young

men and women in the Navy with harm's way...

Don't give it a second thought.

Saddle up and please take the rest of the House and Senate with you.

Create a Threat to National Security... Risk Lives, Profit from it as a matter of course.

Shut up Hoi Polloi, we didn't ask you, we decide - you obey.

___________________________________________________________________________

The insiders in and outside the Beltway can't wait to get this Theft to the House and wrap

it up for August recess.

Qui Bono, you ask?

Intel, TSMC, and Texas Instruments - direct Jing.

Fabless chipmakers like Nvidia and AMD will not be left out in the cold. They will receive

"Scientific Grants out of the $230 Billion in free money for "Innovation."

It is quite likely the following Companies will join the Grift eventually:

Micron Technology Inc. (MU)

Amkor Technology Inc. (AMKR)

Camtek Ltd. (CAMT)

Analog Devices Inc. (ADI)

Although these ladies doth protest too much, it's an irresistible deal... free money.

We'll see $175B in Tax Credits gifted when everyone joins the Semi-Orgy.

You and me - we get the Bill @ $457 Billion.

Enjoy or do something.

ps. - IMF: Russian economy doing better than expected

NVDA south?Getting rejected at prior support area, now resistance.

Good R:R having SL just above the trendline

No entry until confirmation on smaller time-frame

SOXL close to a strong supportSOXL tracks the performance of the thirty largest U.S. listed semiconductor companies.

The semiconductor space is still hot, but the companies in the leveraged Direxion Daily Semiconductor Bull 3X Shares (SOXL) didn`t performed well against the inflation and raising interest rates recently.

I think SOXL is now close to the strong support of $21, pre-pandemic level, from which it can bounce to the $36 resistance.

Looking forward to read your opinion about it.

$UCTT go long, potential outperformer in semi equipment spaceUCTT has begun to outperform the overall semiconductor industry represented by the etf SMH. The trend has clearly been broken on the weekly chart.

There has been a good amount of volume in this week so far, creating that very bullish weekly candle. Hoping we finish strong this week. Looking to create a position if it shows continuation.

EV/EBITDA ratios for the leaders in the semiconductor manufacturing equipment; as you can see UCTT has the best one since any EV/EBITDA below 10 is considered healthy.

8.2577 UCTT

16.5404 AMAT

19.0102 LRCX

18.1225 KLAC

Micron cerca de romper record del 2000. Lo lograra? Micron sigue subiendo después de su reporte trimestral, y al los analistas arrancar el 2022 subiendo sus estimados con respecto a la accion. Les contamos como la salud técnica y fundamental están en la accion de cara hasta 2022

$AMD | 1/3 - 1/7 AMD 143 - 144 BOUNCE

Rationale: Bounce off trendline on the daily chart

News catalyst: AMD hosts its 2022 Product Premiere event at CES to highlight innovations and solutions featuring upcoming AMD Ryzen processors and AMD Radeon graphics.

$mu analysis Sometimes there is no need to get creative. Semiconductors have been hot, and $MU is one of the few that hasn't made a new high yet (although it came close, wicking into supply levels near the all time high of $96.69). The bigger picture here is that price is extended from the 21 day and closed below the 5 day last week. It seems a slight pullback is in order

FB - INTC V.2 FB options degenerates are back, surprise.

Put Volumes dominating the Volume although O/I is split.

297.50 @ 1,357

300.00 @ 5,886

305.00 @ 1,854

310.00 @ 2,873

312.50 @ 556

315.00 @ 1,273

317.50 @ 819

320.00 @ 3,540

322.50 @ 1,210

325.00 @ 1,672

Semiconductors, Comm, Telco, Software - are being used to push to the NA

to Price Objectives @ 15513 - 15517 as the VXN broke its Lows and is making

New Lows for the Day.

Range break leads to higher Price Objectives.

We are SOH until FB reports.

INTC - Provides Intel on the State of Affairs in MANUAfter a run ahead of EPS, the 46.07 ended up another Ghost in the ALGO Machine.

EPS for Intel, another Disasater after FAB MANU ASML's ugliness, Lucky for ASML

the Dippers were all too anxious to Bid it back up erasing 1/2 its losses from

805.

Earnings Season has added more complexity to the Mix.

NQ made a run for the top of the Range @ 15513/17 - only to unload to its

Prior close by ZERO.

It gave back all the gains on INTC... all of them.

These are the challenges to EPS, volatile and setting up for the unseemly news

from Chips. Today's Intel Dip buyers were dunked to the 52.50 Level on the DOM,

the scene of prior High Crimes and Felonies.

As Semi's continue to report, they will continue to reveal Q3 was indeed a disaster,

lots of Fudge, no Walnuts.

Today's EPS was TECH heavy, tomorrow is Freaky Friday - the most overused Day

of the Week to Crush the VX Complex.

With the 400 Ticks of CF ahead, it will, no doubt be challenging.

Trade Safe, it is very dangerous at present.

Timeframes are in Conflict, complete conflict. Weeks end will begin to resolve this

when we see where the Weekly Candle closes. Last Week's close = 15134.50.