TRADE IDEA: GILD AUG 19TH 79/94 SHORT STRANGLEGILD announces earnings on Monday after market close, so look to put this on sometime before the final bell.

Metrics:

Probability of Profit: 74%

Max Profit: $123/contract

Max Loss/Buying Power Effect: Undefined

Break Evens: 77.77/95.23

Notes: This is being done in the off hours, so I'm not getting accurate buying power effect metrics for this setup, and it's likely that the strikes will have to be tweaked slightly and/or the fill price adjusted during open market hours ... . Unsure if I'm going to do this trade myself, as I have some "housekeeping" to do on existing setups, and want to see first what buying power i've got left after I do that ... .

Shortstrangle

EARNINGS PLAY: NFLX JULY 29TH 85.5/111 SHORT STRANGLEUnfortunately, the only underlying announcing earnings next week that has sufficient implied volatility to consider selling premium in is NFLX, with an implied volatility of 52%.

It announces earnings on Monday after market close, so look to put on a play some time on Monday, preferably right before the NY close.

Preliminarily (I'm checking this crap in off hours, so it's rarely spot on), here are the metrics for the two setups I would consider doing:

NFLX July 29th 85.5/111 short strangle

Probability of Profit: 74%

Max Profit: $215/contract

Max Loss: Undefined

Break Evens: 83.35/113.15

NFLX July 29th 81.5/85.5/111/115 iron condor

Probability of Profit: 70%

Max Profit: $99/contract

Max Loss: $301/contract

Break Evens: 84.51/111.99

Naturally, strikes may need to be tweaked slighly depending on price movement on Monday.

NOTABLE HIGH IV STOCKS WITH IV > 50%1. P, 79%

2. FCX, 76%

3. X, 75%

4. TWTR, 67%

5. STX, 57%

6. ABX, 56%

7. NFLX, 56%

8 GG, 53%

9. SLW, 52%

Naturally, we are coming into earnings season here, so there's a reason that some of these have high IV here (e.g., NFLX announces in a week and a half). Ordinarily, I like IV to be >50% and IVR (current IV's level relative to where it's been for the past 52 weeks to be high, too), but I may not find a great deal of 70%+ IVR plays here with broad market volatility so low (VIX finished the week below 15).

Neverthless, it may be worthwhile to churn through this small list for premium selling plays (iron condors, short strangles, short straddes), assuming there's sufficient time before earnings to sneak a play in. Otherwise, it's probably best just to wait to do the standard volatility contraction play surrounding earnings ... .

WBA EARNINGS PLAYSWBA announces earnings tomorrow before market open, so look to put on a play before today's NY close.

Here are the metrics for defined/undefined risk setups:

WBA July 15th 76.5/90 short strangle

POP%: 76%

Max Profit: $106/contract

Max Loss/Buying Power Effect: Undefined/$1031/contract

WBA July 15th 74/78/89/93 iron condor

POP%: 67%

Max Profit: $104/contract

Max Loss/Buying Power Effect: $296/contract

Notes: Shoot to take these off at 50% max profit and move on. For the short strangle, the buying power effect metric is quite "ugly." For the iron condor, I had to bring the wings in to squeeze $100+ out of the setup, which lowers the probability of profit (POP) of the setup heftily. There are always trade offs between max profit potential, buying power effect (defined vs. undefined), and probability of profit ... . To gain with one metric, you inevitably give up ground on another ... .

PREMIUM SELLING CANDIDATES FOR TUESDAY -- CY, HOG, POTWith broader market volatility bleeding out of the markets, I'm on the hunt for non-index premium-selling plays, and there are a few that have popped up on my radar. That being said, earnings season is nigh, so it might be best to be particularly selective as to individual underlying plays, keeping powder dry for the actual earnings, rather than pulling the trigger here such that you have to guide the setup around the actual earnings announcement. In any event, here are a few to look at:

Individual Underlyings

CY: implied volatility rank 100, implied volatility 78. The unfortunate thing about Cypress Semiconductor from a premium selling standpoint is its price, which limits the profitability of iron condor/short strangle setups. Where this is the case, the go-to is a short straddle. Preliminarily (looking at off hours quotes here), an August 19th 10 short straddle will bring in $228 in credit with break evens at 7.72 and 12.28, which would fit in nicely with CY price action. However, if you're looking to take the straddle off at 25% max profit (the usual goal for straddles), you're not looking at a tremendously great play here, even though these little "grounders" add up over time ... .

HOG: implied volatility rank 100, implied volatility 63. Preliminarily, an August 19th 42.5/65 short strangle would bring in $168/contract, the drawback being that the underlying only offers monthly expirations ... .

POT: implied volatility rank 70, implied volatility 51. Like CY, you won't be able to get much out of a play if you go short strangle or iron condor, leaving you with a short straddle as the go-to setup. The August 19th 17 short strangle will bring in $227/contract credit with break evens of 14.73 on the lowside, 19.27 on the topside which is not a bad fit for what POT is doing on its chart (essentially, sideways chop between 15 and 20).

Exchange-Traded Funds

The ETF space is not looking particularly attractive here, with the vast majority of them sub-50 in implied volatility rank. The one standout is SLV (coming in at 70), but you won't be able to get much premium out of an SLV play due to fairly low implied volatility (currently 34, which is fairly high for SLV), although it looks enticing for some kind of directional play (bearish assumption).

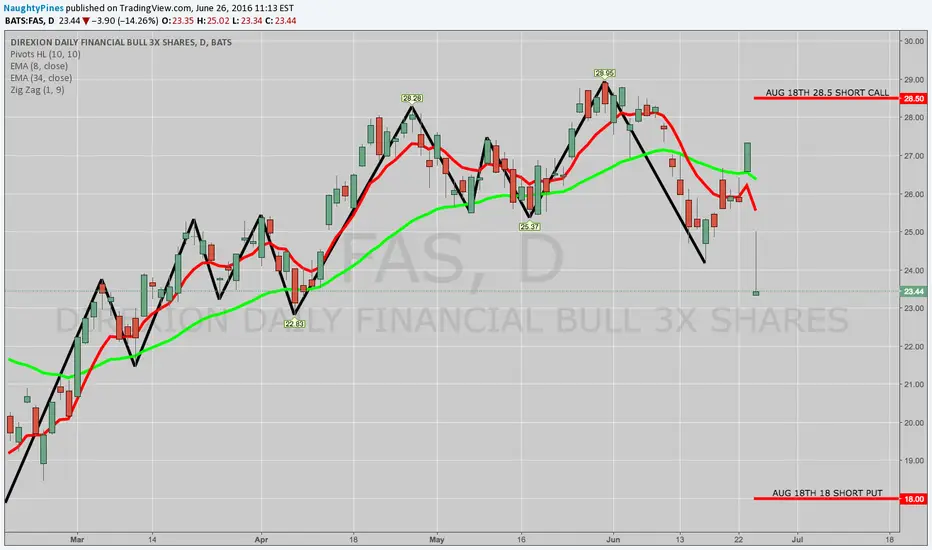

TRADE IDEA: FAS AUG 18TH 18/28.5 SHORT STRANGLETruth be told, I'm not a huge of fan of leveraged instruments, but when a $23 underlying has the potential to yield a $100 or more worth of credit, I'll briefly overlook the warts these instruments have as an "investment" tool ... .

Here are the metrics for the play:

Probability of Profit: 77%

P50: 81%

Max Profit: $127/contract at the mid (this is off hours pricing; we'll have to see whether that's possible at NY open)

Max Loss/Buying Power Effect: Undefined/$232/contract (estimated/off hours)

Break Evens: 16.73/29.77

Notes: I'll look to get a fill for anything north of $100/contract, given the price of the underlying. As usual, I'll look to take this off at 50% max profit.

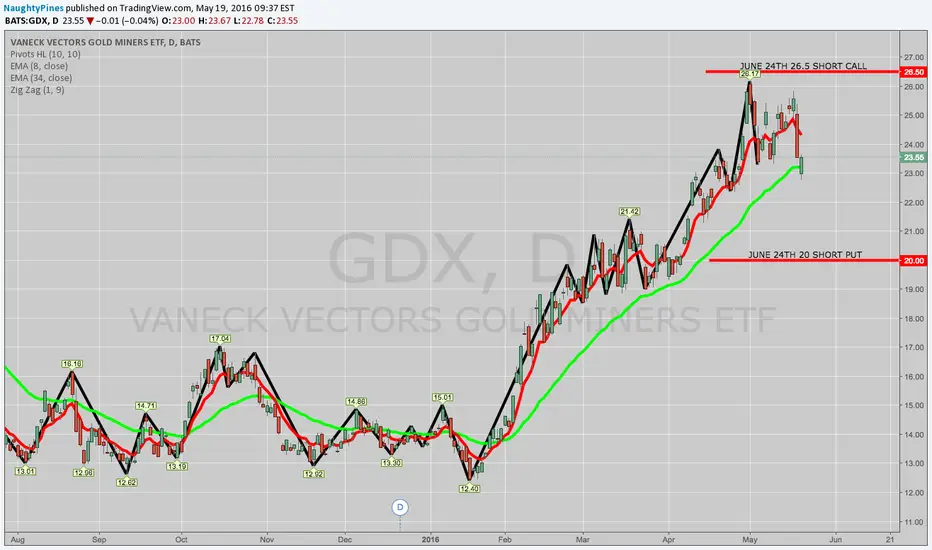

TRADE IDEA: GDX JUNE 24TH 20/26.5 SHORT STRANGLEContinuing to follow the volatility ... . And it's currently in gold ... .

Metrics:

Probability of Profit: 72%

P50: 78%

Max Profit: $95/contract

Max Loss/Buying Power Effect: Undefined/~$250/contract

Theta: 3.11/contract

Delta: -9.7/contract

Notes: I'll shoot for taking this off at 50% max profit ... .

TRADE IDEA: BBY JUNE 3RD 29.5/35 SHORT STRANGLEBBY announces earnings on 5/24 (Tuesday) before market open, so look to put on a play shortly before Monday's NY close to take advantage of the implied volatility crush that commonly occurs post-earnings announcement. Here's the preliminary setup, since price may move during the NY session, requiring slight adjustment of the strikes:

BBY June 3rd 29.5/35 short strangle

Probability of Profit: 71%

Max Profit: $104/contract

Max Loss/Buying Power Effect: Undefined/~$371/contract

Note: Look to take this off at 50% max profit.

TRADE IDEA: WFT JULY 15TH 4/6 SHORT STRANGLEThis is part of a small WFT covered call I'm working ... . The strategy here is to continue to reduce cost basis in the underlying shares. Here I'm doing it with a July 15th 4/6 short strangle in an attempt to sell premium while the implied volatility is still high ... .

Metrics:

Probability of Profit: 63%

Max Profit: $61/contract

Max Loss/Buying Power Effect: Undefined/~$50 (in this particular case, the max loss is actually governed by the fact that the stock price cannot go below $0, so the max loss is actually $400 (the short put strike x 100 shares ($400) minus the credit received for the short call $61 or $339).

TRADE IDEA: XME JUNE 24TH 19/23.5 SHORT STRANGLEFollowing the premium. With a nearly 70% implied volatility rank and an implied volatility slightly north of 50%, I'm going nondirectional here (what's new) with this short strangle.

Metrics:

Probability of Profit: 65%

P50: 78%

Max Profit: $107/contract

Max Loss/Buying Power Effect: Undefined/~$250/contract

Theta: 2.55/contract

Delta: -7.55/contract

Notes: I'll shoot for taking this off at 50% max profit ... . Premium selling opportunities in underlyings with >70 implied volatility rank and >50 implied volatility are still thin in this market. My choices were XME, GDX, and GDXJ. I already have a couple of short strangles I layered on in GDX, so XME it is.

TRADE IDEA: GDX JUNE 17TH 20/27 SHORT STRANGLEGoing where the premium is at ... . I already have a setup in GDX in the same expiry, so I'm layering another on small here ... .

Metrics:

Probability of Profit: 69%

P50: 81%

Max Profit: $93/contract

Max Loss/Buying Power Effect: Undefined/~$236/contract

Delta: =8.29/contract

Theta: 2.98/contract

TRADE IDEA: GDX JUNE 17TH 21.5/29 SHORT STRANGLEThere is simply not much high quality premium to sell out there; this is one of them (>70 implied volatility rank; >50 implied volatility).

Metrics:

Probability of Profit: 69%

P50: 79%

Max Profit: $109/contract

Max Loss/Buying Power Effect: Undefined/~$255/contract

Breakevens: 20.41/30.09

Theta: 3.13/contract

Delta: -8.87/contract

Notes: I'm looking to take this off at 50% max if I get filled.

SOLD WFM MAY 13TH 25.5/31 SHORT STRANGLESold this earlier today, but can't get onto Dough currently for the metrics ... .

In any event, filled for $85/contract. I'll look to take it off for 50% max profit in the volatility contraction post-earnings.

SOLD TWTR MAY 6TH 15/19.5 SHORT STRANGLEWhile I wait for my "gaggle" of long VIX/VIX derivative setups to play out, I'm going to play a few of these smaller earnings announcements, so that I can keep powder dry for the juicier underlyings (should their implied volatility ever ramp up to my standards).

Metrics:

Probability of Profit: 77%

Max Profit: $79/contract

Buying Power Effect/Underfined: ~$187/contract; Undefined Risk

Look to take it off for 50% max profit ... .

BOUGHT EWZ MAY 27TH 22.5/31.5 SHORT STRANGLE TO CLOSEOriginally opened for a $104 credit, I closed this out today for a $60 debit, yielding a $40.92/contract profit after fees/commissions ... .

TRADE IDEA: EWZ MAY 27TH 22.5/31.5 SHORT STRANGLEI already have a couple EWZ premium selling setups on, but with an implied volatility rank of 95 and implied volatility of 59, I'm going to put some more on here. I'm going small and using multiple expirations for setups to disperse my risk, while taking advantage of this fairly low priced underlying to haul in some pretty good credit.

Here's the metrics:

Probability of Profit: 73%

Max Profit: $105/contract

Buying Power Effect/Max Loss: ~$271/contract; undefined

Notes: I'm going short strangle here due to the limited buying power effect, as well as better metrics over an iron condor, where the long options "drag" on max proft. As with all my short strangles, I'll look to take this off at 50% max profit.

TRADE IDEA: MON APRIL 15TH 76.5/81/93.5/98 IRON CONDORMON announces earnings on Wednesday before market open, so look to put on your play on Tuesday in the waning hours and minutes of the NY session. As with all earnings plays, you may have to tweak your strikes somewhat, depending on how MON moves running into the end of the session.

Here are the metrics for this defined risk setup:

Probability of Profit: 69%

Max Profit: $63/contract

Buying Power Effect/Max Loss: $387/contract

Alternatively, you can go short strangle:

MON April 15th 81/93.5 short strangle

Probability of Profit: 72%

Max Profit/Buying Power Effect: $99/~$1140/contract

Notes: Because we're just at the beginning of earnings season, I'm looking to manage my capital a bit more efficiently here and will probably use the iron condor because it's defined risk and the per contract buying power effect is easier to swallow than that of the short strangle ... . Additionally, the broad market is in a low volatility environment here, and I don't want to have a bunch of buying power tied up with earnings plays in the event we get a volatility pop such that I can wade back into 45 DTE index ETF setups.

BOUGHT TO CLOSE LULU APRIL 15TH 63.5/68.5 SHORT STRANGLEWith this little dip here we got today, I bought back my LULU short strangle to close it out for a small profit.

Here's the whole chain:

Sold to open LULU April 8th 54/68 short strangle for $130 credit

Bought to close LULU April 8th 54 short put for a $2 debit

Rolled LULU April 8th 68 short call to April 15th 68.5 short call for a $17 credit

Sold to open LULU April 15th 63.5 short put for a $32 credit

Bought to close LULU April 15 63.5/68.5 short strangle for a $143 debit

Total Credits Collected: $179

Total Debits Paid: $145

Profit: $34/contract; $26/contract after fees/commissions

Naturally, it would have been nice if the setup had worked out from the get-go, I'd been able to take 50% of the original credit received as profit and moved on, but things don't always work out that way. The important thing is that it isn't a loser, and that I got out of it fairly quickly for scratch or better and can now redeploy the buying power on a higher probability setup ... .

ROLLING LULU APRIL 8TH 68 TO APRIL 15TH 68.5 SHORT CALLI didn't like how price was dancing around my short call strike post earnings, particularly with an analyst upgrade that's probably keeping it there, so I rolled the April 8th 68 short call to the April 15th 68.5 to give it a touch more space and time to work out (filled for a .12 ($12) credit).

Since I closed out my original setup's short put at near worthless, I also sold a 63.5 short put in the same expiry for an additional .32 ($32) credit), resulting in an April 15th 63.5/68.5 short strangle.

TRADING IDEA: LULU APRIL 8TH 54/68.5 SHORT STRANGLEI'm going to go with a nondirectional bias here (pretty much always do).

Here are the metrics for both a run of the mill one standard deviation short strangle, as well as an iron condor:

April 8th 54/68.5 short strangle

Probability of Profit: 70%

Max Profit: 1.30/contract ($130)

Buying Power Effect/Max Risk: ~$616/undefined

Break Evens: 55.30/67.20

April 15 50/54/68.5/72.5 iron condor

Probability of Profit: 68%

Max Profit: 1.00/contract ($100)

Buying Power Effect/Max Risk: $301/contract

Break Evens: 53.01/69.49

Notes: I had to go a touch farther out in time for the iron condor to get the long options strikes I wanted, but it'll still yield about $100/contract ... . Look to take either setup off at 50% max profit on the volatility contraction that is likely to occur post earnings.

BOUGHT GME APRIL 8TH 27/32.5 SHORT STRANGLE TO CLOSEI originally filled this for a .94 credit, and I'm out today for a .47 debit (50% max profit/$47 contract).

NEXT UP: LULU EARNINGS -- WEDNESDAY BEFORE MARKETLULU announces earnings on Wednesday before market open, so look to put on your setup before close on Tuesday.

This is what I'm looking at tentatively right now:

April 8th 53.5/68.5 short strangle

Probability of Profit: 73%

Max Profit: $124/contract

Buying Power Effect/Max Risk: $616/undefined

Notes: This is a tentative setup. Naturally, a lot depends on how much LULU's volatility rises here, as well as how much its price moves before the announcement. Also, I don't think I'm going to see $1.24 come Tuesday, although you never know (.92's the low; 1.24 the mid; 1.55 the high for this setup).

I'll also try to post a defined risk iron condor if I can work out a setup that'll yield something close to a $1.00 credit ($100/contract) ... .

SOLD APRIL 8TH GME SHORT STRANGLESorry I didn't get to post this before NY close ... .

Filled for a $94 credit. I usually like to see a $100/contract out of these setups, but I figured it was close enough ... . I'm looking for price to stay between my short strikes between now and expiration and for volatility to contract post-earnings announcement. Post-announcement, price is down about $2 to $28.38, so it looks good at this point .... .

I'll look to take it off at 50% max profit or for about $47 (a .47 debit).