GBPUSD Price ForecastSell trade for GBPUSD

Share thoughts in the comments

Like and follow for more content

Good Luck

Sterling

GBP/NZD NICE SET UPThis looks like a beautiful set up with rvi and price action blending perfectly price rising to a neckline and ema 89, looks very good to short on weakness. price has been consolidating under the neckline and looks ready to drop,

LOVELY SET UP!This looks like a beautiful set up with rvi and price action blending perfectly price rising to a neckline and ema 89, looks very good to short on weakness. price has been consolidating under the neckline and looks ready to drop,

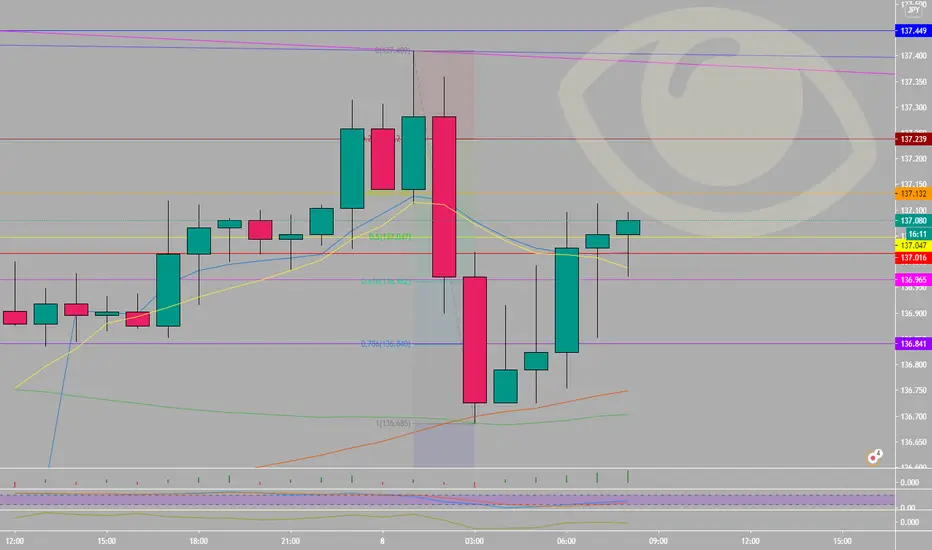

EUR/JPY BULLISHIm long the euro/yen on daily timeframe and now price on 15m chart has presented a good entry signal bouncing of uk pivot point. long to a higher high. the dollar is falling and eur/usd is highly correlated to dragon, so euro/usd climbing signals bullish interest in euro/yen all be it a bit weaker.

GBP/AUD looks set to continue downPound struggling with fundamentals. price looks ready to collapse from these levels.

GBPUSD US ELECTIONS SELL LIMIT!!!!!!!!!the Pair traded in a range the last couple weeks, however the pattern shows that the upside momentum is still corrective for a

downtrend continuation. 7-9-11 swings are related to A,B,C corrective phases in Elliott Wave Theory.

tomorrow is the US ELECTIONS results so we will definitely expect high volatility trading, thats why i prefer to put pending orders ( sell limit ) orders near 1.3270 level

to short the pair and probably target 1.2390 the monthly engulfing pattern target.

Good luck

GBP/AUD 30M SHORTI have the daily chart ready to sell off, so right now on the 30m we have had this little rally, i am looking to short from this extension.

xauusd GOLD buysI am risking around 50 pips to buy gold for a nice retracement and pullback back into 1900 and 1920 and 1930 with potential targets!

GBP/AUD bears are strongRVI Bearish cross and sterling looking weak into next week, could be time to short after last weeks rally of sorts as price enters supply area and good defensive bearish battleground before show the start of bearish breakdown on daily.

GBP/AUD bears are strongRVI Bearish cross and sterling looking weak into next week, could be time to short after last weeks rally of sorts as price enters supply area and good defensive bearish battleground before show the start of bearish breakdown on daily.

EUR/GBPWE look to have broken bullish out of a descending wedge, on top of this we have the rvi bullish cross on daily chart, as this classes as consolidation look for bullish breakout.

SIMPLE FTSE 1Ha very simple trade to short ftse 100 down on hourly timeframe, overall trend is slightly down on daily. 1h is now facing resistance. so im gunna short it downwards towards target. if ftse continues down expect a stronger GBP.

gbp/usd buywith the 4h swing low being in, I have been looking for 1h weakness to start accumulating a long position, the hourly chart is now in this zone for me and as such i will take a long position with stop below the 1h low and hold it on 4h chart till we have the start of a distribution. as you can see we have an indicator relative vigor index buy signal. i remain bullish on the pair until proven otherwise.

Pound fell sharp as BoE Gov Bailey not seeing V shaped recoveryThe Bank of England asked banks on 12th October on how ready they are for zero or negative interest rates, following up its announcement last month that it was considering how to take rates below zero if necessary. The BOE set a deadline of Nov. 12 a week after its next monetary policy announcement for banks to respond. Money Markets are expecting BOE's next move to be an increase in the 745 billion Pound bond buying program in November.

Technically, GBPUSD came out fom upward rising channel in 4hr with a break of channel support at 1.2960 or 50ma heading towards 1.2845-50 Oct 10th low. A break upside 50ma again can rise towards 1.2980 or 200ma and 1.3082 Oct 12th high. As we see a small retrace to the todays pivot point at 1.2955-60 would be a selling zone freshly for downside said targets. Overall sell on rise is advised for the day.

Suggestion: SELL GBPUSD FROM 1.2950-60 SL ABV 1.3030 TGT 1.2880/2830

ELSE

BUY GBPUSD FROM 1.3030 FOR 1.3120 WITH SL BELOW 1.2950

GBPUSD Buy SetUpGBPUSD H&S set up

Share thoughts in the comments

Like and follow for more content

Good Luck

GBP/AUD bears are strongAUSSIE is strong currency right now, sterling looks like it wants to sell of in this pair. 1h and 4h look for good short signals and ride the next wave down. lots of pips on the table up for grabs

Is GJ a 1200 Pip Short ?$GJ $GBPJPY

price now, 137.07

1200 pip short down to 124.69 ?

fill the March 2020 dumpy wick ?

FiboGroup & Saxxo Traders Short ?

broke below the daily 100ma, came up retested bearish trendline, back down below the 100ma and it's off to the races ?

recent touch of bearish trendlines ?

oscilators overbought ?

Brexit Bearish ?

send it ?

POUND STERLING COT. GJ EXCHANGE COT. All LONG but Fibogroup.

POUND STERLING COT. GJ EXCHANGE COT. All LONG but Fibogroup.

GBP Futures COT CME Big Long / Retail Short. COT GJ Overall Sentiment Long. Most Retail Exchanges Long but Fibogroup in Austria 56% Short.

i don't think i'm aloud to leave links but google FXSSI current ratio. :)

luv u buddys

OANDA:GBPUSD

BRITISH POUND STERLING - CHICAGO MERCANTILE EXCHANGE

FUTURES ONLY POSITIONS AS OF 09/29/20 |

--------------------------------------------------------------| NONREPORTABLE

NON-COMMERCIAL | COMMERCIAL | TOTAL | POSITIONS

--------------------------|-----------------|-----------------|-----------------

LONG | SHORT |SPREADS | LONG | SHORT | LONG | SHORT | LONG | SHORT

--------------------------------------------------------------------------------

(CONTRACTS OF GBP 62,500) OPEN INTEREST: 159,049

COMMITMENTS

39,216 51,961 5,384 88,988 78,464 133,588 135,809 25,461 23,240

Retail Exchanges in the COT

FiboGroup Austria . 56% Short

IGG Chicago

Dukas Swiss,

Saxo Denmark.

Oanda New York

Insta Cyprus . only 50.7% long :slot_machine:

:slot_machine: :slot_machine: :slot_machine:

I’m not short. I'm looking to short. I'm looking to get in and get out. I'm looking to Long Dollar. I'm looking to stack pips into cash. I'm looking for 10 pip 10 lot cup o coffee afternoons. We'll see, someday, til then: self brew'd teaspoons, middle of the night.

Simple but very effectiveprice has rejected neckline with a wick bar look for buy signals on lower tf or use stop under the wicks as seen. FINAL POST i promise haha enjoy and have a nice weekend everyone. Peace

short : GBP/USDwe can see a small correction on the uk session , then we make a new fall to 1.28 support zone

What are the banks saying about EUR, USD, JPY and GBP?I receive bank research each day...

I'll drop some of their comments here/

Euro

Citi: EUR trades marginally below overnight highs around 1.1730 at the time of writing (-0.1% in Asia). As a reminder, CitiFX Strategy still believes the EURUSD correction has room to go and it is not yet time to fade it. Several factors, including a slightly less dovish Fed, derisking into US elections, and USD positioning all support this thesis. Strategy is still structurally bullish EURUSD but prefers to add longs on a deeper correction towards 1.14.

JPMorgan: No real reason for the move higher yesterday and it was a little strange when you consider that stocks and commodities were lower on the day. But the head scratching wasn’t confined to EURO, where EM which ignored the positive risk rally on Monday, chose to rebound into midday, before retracing somewhat. The random price action could be a result of Month/Quarter end flow and while I have no insight into whether this is indeed the reason or not, this afternoon is likely to be volatile as the story plays out. O/N the Biden/Trump presidential debate was at times farcical, as both candidates thought the way to make an impact was to name call and see who could shout the loudest. While there was no clear winner, Biden’s betting odds widened by 7% points and the Election remains his to lose. While Biden extended his lead, it was clear that Trump is unlikely to go quietly, meaning a contested election is still very much a concern for markets. But with polls suggesting that 87% of Americans have already made up their minds on how they will vote, these debates may be nothing more than a 3 part Comedy drama. Watch the wires for headlines as Lagarde and Lane are due to speak at today’s ECB watchers Conference and Brexit discussions continue. Mnuchin and Pelosi also continue to talk although an agreement still feels unlikely. All of this may be insignificant, if the much anticipated Month/Quarter end flow dominates proceedings as expected this afternoon. We had been tactically short EUR/USD but are now playing things very close to home, as we try to navigate the potential volatile moves this afternoon.

ING: EUR: All eyes on Lagarde USD weakness helped EUR/USD yesterday absorb the new of a possible delay in the EU Recovery Fund as some countries look determined to use the veto if the rule-of-law conditions are not dropped. Today, the pair appears more vulnerable, also due to some potential Brexit spill-over. President Lagarde’s comments will be closely watched amid rising speculation over a rate cut.

Danske: Although EUR/USD is again on the rise, sentiment across inflation expectations, equities and credit continue to appear weak, and it is, in our view, too early to call off further downside in the pair. Indeed, to the extent that the Danish experience with new COVID-19 lockdowns is anything to go by in a broader context, it is worth noting that consumer spending (card and mobile payments data) are starting to show signs of weakness. We still view EUR/USD as rangebound with risks tilted to the downside towards 1.16 near term. What could make us change this view? Progress on Brexit (watch for whether 'tunnel' negotiations are reached this week), a 'clear' US election outcome and thus a US fiscal boost, and/or central banks renewing their reflation vows. Today watch for ECB speakers at the Watchers conference and for Fed minutes for any hints on the latter, although we think it is too early for a major shift on either side of the Atlantic.

GBP

Citi: GBP mirrors AUD movement, trading down -0.2% to 1.2840 at the time of writing. After the London close, headlines on Bloomberg emerged that the EU has rebuffed a new round of UK proposals on state-aid rules.

“The British offer still doesn’t go far enough, according to two officials in Brussels, who said insufficient progress has so far been made for the talks to head into the intense final phase, known as the tunnel, at the end of this week.”

Talks will continue before a meeting on Friday between chief negotiators Barnier and Frost, where yet another round of talks could be proposed to iron out remaining differences, should no breakthrough be found this week. CitiFX Strategy’s Adam Pickett outlines expectations here: Nothing new from Brexit and BoE headlines.

Also note that the EU’s deadline for changes to the UKIM Bill is today – infringement proceedings against the UK are expected to start on October 1.

JPMorgan: Choppy day for sterling yesterday in which we saw much of Monday’s strength reverse as talks continue in Brussels, the highlight of the day were reports that the UK had sent 5 draft legal texts including one on state aid i n an effort to advance the talks however subsequent reports had European sources saying that the proposals did not go far enough and that insufficient progress has been made to enter the tunnel phase. Flows were pretty light although the HF sector did turn to small net sellers tempering the exuberant run (4 sessions) of net buying into the talks. The IMB meanwhile trundles on clearing the HoC hurdle and now moving to the House of Lords in which it should fail –what follows is then an iterative process between the two houses after a few rounds of which Johnson will be able to force it through anyway –developments here are unlikely to impact negotiations this week. The situation will remain opaque and will be punctuated by brief noises in either direction –our overarching suspicion is that political leaders will need to get involved to agree on the thornier issues and thus the tone could take a turn for the worse into the end of the week. As such we remain in tactical mode here as we end the teeth of month and quarter end rebalancing today. 1.2780/90 remains supportive ahead of 1.2740/50 (0.9115/20, 0.9065/70 EURGBP) while 1.2880/85 remains resistance with 1.2930 above (0.9165/70, 0.9220/25 EURGBP).

Lloyds: The rally from 1.2675 has backed away from 1.2935/45 resistance. A move through there opening an extension towards 1.3010/50 with a break there suggesting 1.2675 was a meaningful low. A slide back through 1.2805/1.2780 support would suggest the rebound from 1.2675 is merely another correction risking another test lower to the 1.26-1.25 region. Longer term, we are biased that the bear cycle from the 2007 and 2014 highs completed with a major ‘double bottom’ in the 1.15-1.14 region. However, we are monitoring the current pullback closely and watching 1.25 and 1.20 key supports.

USD

Citi: Month-end: CitiFX Quant’s preliminary estimates have also suggested that USD pressure should prevail. The sharp losses in equities in September leads the asset rebalancing model to suggest a rotation into equities from bonds with a moderately strong signal at +0.8/-0.7 historic standard deviations respectively. The FX impact of the signals is likely to be USD buying, with the signal significant by historic standards (over 2 standard deviations).

JPY

JPMorgan: Biden seemed to hold his own as Trump turned the debate into chaotic theatre and while Biden’s advantage in betting odds has grown ~7% overnight it is also becoming clearer that Trump will not go quietly, the risk of a contested election is very real and probably rising –as such risk is trading on a softer footing for now. However price action today will be increasingly hard to put into context as we have month/quarter end to deal with –USDJPY was pretty bid in Tokyo into Japanese half-FY and go to be touching resistance at 105.75/80 yet again before risk turned, this will be a focal point today should the implied rebalancing (from MTD stock divergences) come to pass. We are looking to sell USDJPY further onto a 106 handle today if we get the chance, through105.75/80, 106.50/60 is the next level above, meanwhile 105.20/25 remains solid with 104.85/90 below.

Sterling shows bullish tone on tuesday,is it fading again?Sterling held onto a moderately bullish tone Tuesday, recording a fourth consecutive daily gain. From a technical standpoint, H4 recently knocked on the door of 1.29, a level that’s withstood two upside attempts this week. In spite of this, sellers offer a non-committal tone at the moment.

As having said, 1.29 is proving a problematic hurdle to overpower on the H4 right now, despite the higher timeframe supports in sight. Yet, given the lacklustre show from sellers here, a 1.29 breach is still potentially in store. Above 1.29, the river north on the higher timeframes appears ripple free until daily resistance at 1.3017, which happens to merge with the key figure 1.30 and H4 resistance at 1.3009.Dip-buying at any retest seen at 1.28 remains a possible scenario (should intraday sellers strengthen their grip).Another setup worth keeping a tab on is a H4 close above 1.29, signalling bullish scenarios in favour of reaching the 1.30 range. Irrespective of the support used, conservative traders are likely to seek at least additional H4 candlestick confirmation before committing.