Weak dollar pushing pound to above 1.29 handleTechnically, GBPUSD holding abv 1.28 handle strongl and heading for 1.29 and sustain abv can test 1.32. Intraday perspective h4 chart holding above 50ma at 1.2822 and h1 200ma at 1.2822 saying 1.2820 a strong support for the day. One can build a buy positions for the upside target 1.2920 yesterday high also a 136ma too in h4, followed by 200ma at 1.3045 h4 timeframe. Overall buy on dips is advised for the day.

Suggestion: BUY GBPUSD FROM CMP 1.2855 SL BELOW 1.2800 TGT 1.2920/2950

ELSE SELL BELOW 1.2800 FOR 1.2755/2730 SL ABV 1.2830

Sterling

GBPUSD SHORT & LONGpossible price pattern for short term trades.

downside target ~1.27

upside main bullish target is still waiting at 1.36+

FX Update: European mood brightens and sterling surgesSummary: The mood across markets has brightened further in Europe on smooth Brexit hopes driven by the news that major London clearinghouses will retain access to the EU after December 31. This has EURGBP eyeing downside pivot levels. Elsewhere, things are looking a bit less bright as the strong US dollar weighs on sentiment for EM currencies and even among the small G10 currencies.

Sterling was already showing signs of resilience late last week, in part on lowered expectations that the BoE is looking into an imminent move to a negative rate policy (BoE’s Ramsden using those words almost exactly in the minutes after I am writing this, as he sees the effective lower bound at 0.1%), but also on a suddenly more positive tone from informal Brexit talks that were somewhat drowned out over the furor over negative policy rate considerations recently. The Brexit talks are set to get more formal this week and starting tomorrow, with this round seen as a last dash effort if any agreement is to be made on Boris Johnson’s timeline aiming for mid-October agreement. Particular focus from the EU side will apparently be on how any trade deal will be enforced after the recently passed Brexit bill could walk back key portions of the Withdrawal Agreement, which effectively stipulated a customs border across the Irish Sea (separating Northern Ireland from the rest of the UK.)

A specific headline supporting sterling this morning was the news from ESMA (Paris-based European Securities and Markets Authority) that the UK’s clearinghouses for derivatives, energy and metals trades will be able to continuing doing business with EU financial institutions after the December 31 end of the Brexit transition period. This is hugely important as the derivatives portion of the above includes things like the global settling of USD, GBP and EUR swaps.

Chart: EURGBP

EURGBP is pressing back lower toward what is arguably the downside pivot area around 0.9000, which would begin to fully reverse the early September spike inspired by Boris Johnson’s new move to get the Brexit Bill in place. Still, the action will remain highly headline dependent over the next week and more into mid-October on whether we are moving toward a deal. Positioning for a directional move in options is a way to trade outcomes for those fearing the large swings in the spot exchange rate until we either get a deal or a hard Brexit. For the former a long put spread expiring 8 Jan 21 with strikes of 0.88 and 0.86 cost about 56 pips offering almost 3 to 1 reward-to-risk. Strikes farther out of the money offer better multiples if the underlying trades down to the lower strike.

Elsewhere, the strong mood in Europe this morning is not providing notable positive contagion into emerging markets, where the USD strength is beginning to hurt. An FT article (paywall) this morning points out the scale of EM borrowing (some $100 billion since the outbreak of Covid-19) and rightly wonders at the ability for emerging markets to repay this debt. With USD liquidity growth slowing from the initial huge splash, the risk to EM is enormous if the resurgence of Covid-19 or any other threat keeps the global recovery weak or worse. US political dysfunction is another risk across markets as well, keeping new US stimulus possibly bottled up until after a new US Congress sits in January.

One EM currency that may be eyeing specific outcomes is the Russian ruble, as USDRUB accelerated higher to close last week in a move that doesn’t seem particularly driven by oil fundamentals. Ruble traders and owners of Russian assets may be eyeing the strength of Joe Biden in the US election polls, as Biden and the Democrats are seen as likely to be far less friendly to Russia than Trump on accusations of prior interference in US elections and the poisoning of Russian opposition leader Navalny. The ruble is close to its Covid-19 panic lows than most other major EM currencies, save for the Turkish lira, where even last week’s 200 basis point hike failed to stem the selling, with the lira tumbling to new cycle lows this morning.

The G-10 rundown

USD – the USD strength beginning to ease somewhat by lunchtime in Europe on very strong risk sentiment all morning long in Europe. Considerable work to be done by the USD bears to reverse the recent rally impulse.

EUR – as noted in today’s Saxo Market Call podcast, European banks are in the dumps, with the broad banking index of equities touching its lowest level since the 1980’s. Is there any EU recovery without a proper cleanup of the banking system? The mood is very positive today, but let’s see if that lasts.

JPY – the Japanese yen is hanging in better than one would expect on a day in which European equities are ripping some 2-3% higher. Part of the resilience likely down to sympathy with USD moves in the crosses and a local weakness here in the reflationary narrative (commodity prices

GBP – sterling firmer on the developments noted above and plenty more where that came from if we get clear signals that the two sides are moving toward a deal later this week as the latest Brexit talks get under way tomorrow.

CHF – the positive mood in Europe rubbing off ever so slightly on CHF, with EURCHF have a poke at 1.0800 again this morning - the bigger level there is 1.0900. The latest weekly sight deposit data showed negligible change (no real intervention ongoing last week).

AUD – the Aussie is disappointing here, suggesting that the story for the Aussie is more linked to commodity prices and the reflationary story more than risk sentiment per se, as liquid, risky assets are putting in a stellar performance today, while iron ore remains stuck near a two-month low. Still, structural weakness for AUDUSD only really arrives with a forceful move below 0.7000.

CAD – the USDCAD bounce has been gentler than the USD bounce elsewhere, with CAD showing its tendency to track USD direction in crosses like AUDCAD (big mover that one recently)

NZD – the kiwi generally following the Aussie’s lead, though in the AUDNZD cross, the kiwi extended aggressively stronger last week – the latest distraction is the 1.0750 area, the last major Fibo (61.8%) of the rally wave from July and August, though bulls there need a negative NZD catalyst and move above 1.0800-50 to rekindle their hopes.

SEK – the positive mood in Europe rubbing off more easily on SEK aftter EURSEK shot above its 200-day moving average last week, likely on doom-and-Covid-19-gloom. Lets’ see if that moving average, now near 10.56 provides any support.

NOK – the krone suffered a brutal decline last week and risk-on in Europe is finally seeing the currency put in a show of support. A lot of work to do to reverse the damage.

John Hardy

Head of FX Strategy

Disclaimer

The Saxo Bank Group entities each provide execution-only service and access to Analysis permitting a person to view and/or use content available on or via the website. This content is not intended to and does not change or expand on the execution-only service. Such access and use are at all times subject to (i) The Terms of Use; (ii) Full Disclaimer; (iii) The Risk Warning; (iv) the Rules of Engagement and (v) Notices applying to Saxo News & Research and/or its content in addition (where relevant) to the terms governing the use of hyperlinks on the website of a member of the Saxo Bank Group by which access to Saxo News & Research is gained. Such content is therefore provided as no more than information. In particular no advice is intended to be provided or to be relied on as provided nor endorsed by any Saxo Bank Group entity; nor is it to be construed as solicitation or an incentive provided to subscribe for or sell or purchase any financial instrument. All trading or investments you make must be pursuant to your own unprompted and informed self-directed decision. As such no Saxo Bank Group entity will have or be liable for any losses that you may sustain as a result of any investment decision made in reliance on information which is available on Saxo News & Research or as a result of the use of the Saxo News & Research. Orders given and trades effected are deemed intended to be given or effected for the account of the customer with the Saxo Bank Group entity operating in the jurisdiction in which the customer resides and/or with whom the customer opened and maintains his/her trading account. Saxo News & Research does not contain (and should not be construed as containing) financial, investment, tax or trading advice or advice of any sort offered, recommended or endorsed by Saxo Bank Group and should not be construed as a record of our trading prices, or as an offer, incentive or solicitation for the subscription, sale or purchase in any financial instrument. To the extent that any content is construed as investment research, you must note and accept that the content was not intended to and has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such, would be considered as a marketing communication under relevant laws.

GBPJPY Long term viewGBPJPY long term view.

Impuslive wave, followed by abcde corretive structure and continuation.

Share thoughts in the comments below

Like and comment for more content

Sterling gold at 1.24447 ? short this is my new girlfriend. she is on top Daily 200 and 100 ma. She is below the 9. She is at a .618 support level 1.26914. Her golden roads are 1.24447 or 1.28943. and then 1.43455. Golden bricks for miles. Brexit? Lockdown? Brits behave. Will Cable?

I will chase when pound makes run to the gold / 124447 first? then moonski to 1435skis?

heart london emoji

OANDA:GBPUSD

ridethepig | Oven Ready GBP Chart PackThe economic landscape and political development

📌 What the less advanced participants must know about the Brexit saga and economic development

First a few reminders.

We call the resistance area drawn across the first chart our ' Loading Zone ', and here the word 'loading' is used in a trading sense and not its progressive sense.

The 1.23xx and 1.15xx are considered the 'absolute lows' in the current range (once again in a strictly trading sense). It is easy to find the centre, positioned where the scaffolding supports our price structure.

By defining our centre, we have created technical borders around the price, in other words the map of our flows (1.35xx, 1.23xx and 1.15xx).

1️⃣ By political development, I mean the reckless retreat of UK market access in the short-term

The procedure to return to WTO rules is the same as the advance towards the house of economic bondage; whether you want to argue about sovereignty or debate migration, the loss of market access in the immediate term will damage the UK real economy. No-deal Brexit is coming in October despite the political fairy dust and attempts from the Supreme Court to 'take back control'. A ruthless Downing Street hijacked the entire country and are at the wheel aiming to cause maximum pain to the economy in the near term with their edenistic view of rebuilding into 2030 and beyond. So "development" of UK exposure is not really in play for the next 1-2 or even 3 years, but the idea is much rather that UK assets should be redeveloped from lower levels. It is good - if I may say so - from a markets perspective with the spirit of volatility in mind. However, from a humanist and democratic perspective there is a major threat. For example, think how undemocratic it would be to break international laws, destabilise the union and undermine previous commitments (we are not talking about a Banana republic, rather the country of the Magna Carta!!). It's very difficult to find any Brexiteers on the ground that truly wanted no-deal - let alone support for Johnson.

2️⃣ The global economic landscape must not be considered in itself to be healthy, but rather simply an environment which helps politicians pass the blame.

This is an important notion for all those following the covid dominos . The advance of Covid has given cover, where possible for politicians globally to develop counter arguments for nationalism without the criticism from the public. Because, as we have discussed together before, the end of the economic cycle is an unavoidable chapter in the sense that the economy, as with all things in life cycles naturally. For that reason, we should first position for a breakdown in the UK currency.

The following chart demonstrates the unavoidable cycle down:

Since the economic cycle down will last into 2021/2022, we may characterise the advances in equities as noise for our purposes as the equity market is not a reflection of the real economy via artificial CB intervention. Now the UK CFO, Rishi Sunak, can be seen like a deer in the headlights. The effect of years and years of policy mistakes? Tax hikes are coming, and the consumer will pick up the bill.

On the cable front, sellers position is comfortable from the point of view that the macro direction and confidence in the public sector are blocked via NDB. A breakdown of the wedge would trigger flows towards the centre at 1.23xx and in addition, unlock 1.14xx and 1.05xx the 1985 lows. Invalidation for the bear case would only come from a breach of 1.35xx. So, we can rightfully continue to look for selling opportunities across UK assets, including the currency.

Thanks as usual for keeping the feedback coming 👍 or 👎

Another ascending triangle?PERSONAL PREFERENCE ONLY

DO NOT FOLLOW OR COPY

IF YOU DID FOLLOW PLEASE DO IT UNDER PROPER RISK MANAGEMENT

I DO NOT AND WILL NOT TAKE ANY RESPONSIBILITIES

A perfect ascending triangle has happened last week which lead to a 80 pips profit and is this going to happen once again this week?

Although last bullish trendline is broken but currently there might be another ascending triangle forming and if 1.3007 does break, the next 2 significant levels are 1.306 and 1.3115 but 1.3115 are above H4 200MA so suggested TP level is 1.306

but there are also chances that the bear will continue if the 1.30070 level are tough enough and lead another sell off of pound

Uncertainty of Sterling is only building up as there seems to be another Coronavirus wave coming and also Brexit are making sterling pairs become difficult to analysis as no one really know what will actually happen after Brexit.

And if the bullish trendline does break again, there are 3 significant levels which can be used as support :

1.279

1.265

1.2475

PERSONAL PREFERENCE ONLY

DO NOT FOLLOW OR COPY

IF YOU DID FOLLOW PLEASE DO IT UNDER PROPER RISK MANAGEMENT

I DO NOT AND WILL NOT TAKE ANY RESPONSIBILITIES

GBPJPY . Bears Bulls both want Ace OANDA:GBPJPY

Bears and Bulls both want Ace. 1K or more pips. The hunger, the greed, the odds, the charts, the uncertainty, the sharks in the water. They'll risk it. Little known fact, bears and bulls are good swimmers and sharks can't walk. Pound Yen. Guppy? Is this guppy? Pound Yen. Looks bullish to me cause life sounds like hell in Britain right now but hey gotta do what ya gotta do for the flu thing, don't hate me, that's why they're doing it. Right? Check the new. Brexit hell, but they're making deals right? Bojo just doesn't care. I trust that. Don't trust me. Why am I bullish on the Yen?!! Is it cause banks like LYG are at all time lows? How low can British banks go? Is that the only stinker? I should do some research. I'm bullish but I'll short. Sure i'll i do it. Why not? Either way, whoever is right on this, is gonna make an ace of pips. I hope it's you! And me. We'll see....

tbc...

GBPCHF Sell the breakoutGBP to get even weaker this week. Make sure you selling on the breakout.

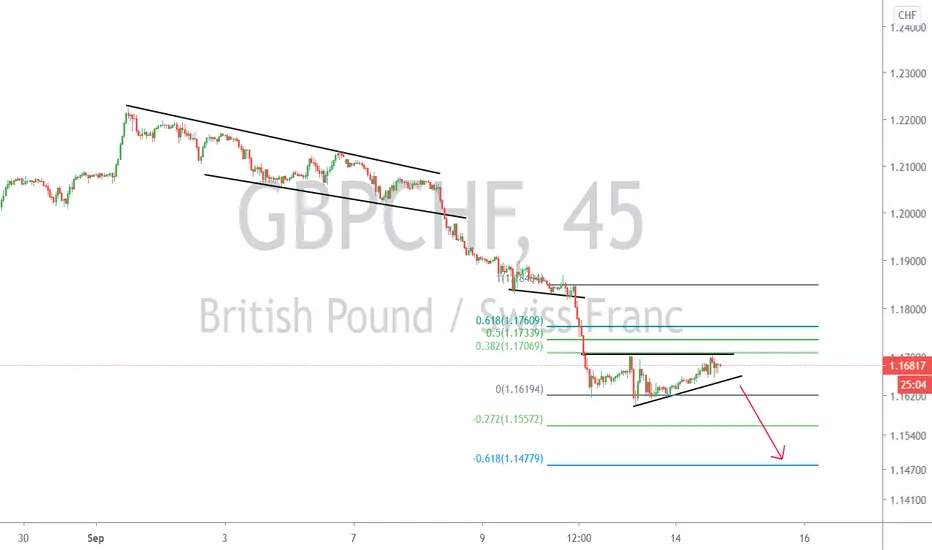

Comment with your thoughts in the comment section below.

Like and Follow for more content

gbpjpyidea for this week

target 135.000 first of all!

Weekly , strong bearish engulfing

Rejection on the daily.

GBPNZD SHORTShort idea for this week.

GBP major falls last week, and I think it will continue, all TF point to the downside, including weekly, daily, 4h.

Price is heading for a major weekly support level in place since 2017. I think it could reach the first target of 1.90600 easily.

Onwards to 1.89200 then.

ridethepig | GBPA timely update to the cable chart after an annihilation last week...

📍 Taking back control (of support)

If we take a closer look at the breakdown we can see that above all it is directed at a lack of confidence in building UK exposure against a no-deal backdrop. What is perhaps even more crucial is the conception of 'track and trace' which is of course difficult to argue against, however if liberty is lost then confidence will follow!

If we take into account that the short-term damage from Brexit will relatively speaking demand action from BOE with front loaded cuts and another QE bazooka then sharp speculators can come together and understand the hyper devaluation of Sterling; classical monetary plays to offset the reduction in market access.

Euro seemed to lead the way on the leg higher and sterling seems to be leading the legs lower in G10 FX because of its high beta. The 1.35xx highs were rejected in fantastic style; and since the entire scaffolding for the leg higher since July has been reversed. Here eyeballing a move back towards 1.225x and 1.207x, possible extensions towards March lows and $1.10 with no-deal this year.

As usual thanks for keeping the feedback coming 👍 or 👎

GBPJPY - Short Idea (again)I have laid...it...out.

1.6:1

I would be quick to scale out of this, could just be a pullback to further upside?

be a Baller.

#GBPUSD F**CK GBP WILL GO TO THE MOON LOOK AT THIS ANALYSIS, FOR ME GBP WILL GO TO THE MOON, BUY AT EVERY CORRECTION

#GBPUSD LONG VERY VERY LONG GBPUSD BREAK THE TRIANGLE I EXPECT MORE UPTREND I WILL POST ANOTHER ANALISYS TO SHOW YOU WHY