Brief overview of the stocks of the 2 major GPU manufacturersRecently I decided to take a delve into the sector of the stock market that truly represents my personal interests, the performance PC hardware sector. I've been performing investigation into various companies such as NASDAQ:INTC (Intel Corporation), NASDAQ:NVDA (Nvidia) & NASDAQ:AMD (Advanced Micro Devices). In many peculiar ways, these companies are very similar but also have some startling differences. What caused me to publish this idea, despite the fact that I am trying to build up some reputation, is I was doing some comparisons between Nvidia and AMD as they are the 2 major competitors in the graphics card market which is currently in some state of paralysis. During my brief investigation, I was trying to identify which option would be a viable option for 3+ year investment. Through some comparison I've come to notice some surprising facts about each company.

First of all, AMD was not a competitive company for more than 10 years after their "birth". Around 5 years ago they were on the brink of bankruptcy, due to various factors including more debt than what could have been considered manageable or sustainable. Since then, Lisa Su was appointed CEO of AMD and pulled the company straight out of that sticky situation. Since then AMD has risen in price more than 1300 percentage points. The company has attained a fairly stable financial position and moderate PE ratio in comparison to its competitors. Considering its growth, the PE ratio and earnings per share are actually impressive.

Nvidia has been established for a significantly longer period of time and have diversified within the hardware market to try maintain their monopoly as best they can despite companies such as AMD coming along and "rocking the boat". Between these 2 companies, they are sitting at very similar positions in the present bull market (At least from the perspective of an investor seeking a diversified portfolio). Due to Nvidia being listed for a considerably longer period of time, they have had time to grow and their overall market cap is sitting at just over $800B whilst AMD is sitting at a quarter of this. Both companies on the other hand have very similar EPS of $3.28 (AMD) and $3.30 (Nvidia). Based solely on statistical indication, AMD will prevail as the best investment choice as they have maintained a considerably lower PE ratio versus Nvidia (47.93 AMD; 97.17 Nvidia) and the PE hints towards their future performance as it has done in the past.

Obviously a multiplier of 47 is by no means 'attractive' but in comparison nearly 100, I would far rather put my money in AMD especially considering how good management at AMD has become, the overall stability is reassuring from a speculative stand point.

TL;DR: AMD is looking to be the far more appealing investment versus Nvidia (lower PE, similar EPS considering stocks available and company capacity)

Technology

11/29 | QQQ | Watchlist #1 QQQ -387

(Below 387 for puts)

Price targets: $383, $375

Technical Analysis: QQQs has been in a linear regression channel for the past year so under 387 will begin retesting the bottom of the channel

Rationale: With increased news of a new covid variant, if QQQs continue to sell off, the plan is to buy and hold a $380 put for a month's expiration 12/24

#PLTR - Reversal H&S under formation. Get ready to go...Palantir is showing a right shoulder under formation, with the characteristic that the volumes on the head are low, as it should be for this kind of reversal pattern.

In my opinion the price is now targeting the 21.30$ level, where it will probably and ultimately breaking the H&S neckline. This might be happening today or on Mon-Tue next week and not necessarely in today session

Not a financial advice, just personal opinion. Do your own due diligence and good luck!

#PLTR reacts well on 20$ support and closed above yesterday highAs I shared this morning, I hoped for a daily close abve the high of the yesterday doji candle. The price managed to close higher than that and this is to me a great sign of possible reversal and confirmation of the rebounce from the 20$ level.

I just would like to mention that the last two times the RSI touched the oversold territory (May and July 2021) the price reacted reaching an average of 45% increase and I want to think that this might be happening again this time.

Not a financial advice, just personal opinion. Do your own due diligence and good luck!

#PLTR - Price possibly rebouncing from key support at 20$?Hi All, my main 3 take-outs from this analysis are the following:

1- Price possibly rebouncing from a key support of 20$ (price has been moving between 27$ and 20$ since a lot f time)

2- 4H chart shws engulfing bullish pattern as also an RSI in oversld territory, which might be a god sign of possible reversal from these levels

3- There are still two gaps at 24$ and 27$ (as also at 31$) that will be needed to be filled sooner or later

Not a financial advice, just personal opinion. Do your own due diligence and good luck!

NDX analysis 11-22-21 Sell off immanent ?NDX analysis market sell off immanent or massive reversal to new highs?

VMW showing some super bullish signsVMW recently split off from DELL and went out on it's own, which is great news as anything AI and cloud right now is super bullish and besides it's the only one i feel that can actually compete with AMZN Cloud AWS, tbh i'm planning on doing a break down video for this play maybe try to get it out before it reports earnings so i can help show people it has some great fundamentals and coming from one of the TECH giants DELL shows nothing but upside potential in my book as you can see it is on this down trend and has had some false breaks through but being that alot of tech plays are starting to pick up steam it will be one that i will be watching for to get a nice break out to the top side.

$MIRM november update*This is not financial advice, so trade at your own risks*

*My team digs deep and finds stocks that are expected to perform well based off multiple confluences*

*Experienced traders understand the uphill battle in timing the market, so instead my team focuses mainly on risk management*

Recap: My team entered $MIRM on 10/29/21 at $15.70 per share. Our first take profit is at $26.

Mirum Pharmaceuticals $MIRM released their 3rd quarter earnings today after market close. In this report they announced a loss of -$1.55 per share on revenue of $5.0 million. This earnings beat is staggering, especially when acknowledging the fact that the revenue consensus was only $0.8 million. $MIRM is still an under the radar company currently, but a revenue beat of 502.4% will definitely turn some heads. In addition, post-earnings five insiders accumulated a vast amount of shares. These insiders know what's coming, and lucky for us we do too. Our first take profit is honestly a huge underestimate of this companies potential, and in the future we may have to make some major adjustments.

This is a buy and throw away the key type of investment. My teams holding! Will you?

OUR ENTRY: $15.70

FIRST TAKE PROFIT: $26

If you want to see more, please like and follow us @SimplyShowMeTheMoney

$RMO we hit and quit for a 18% gain*This is not financial advice, so trade at your own risks*

*My team digs deep and finds stocks that are expected to perform well based off multiple confluences*

*Experienced traders understand the uphill battle in timing the market, so instead my team focuses mainly on risk management*

Recap: On November 2, 2021 my team entered lithium-ion battery company Romeo Power $RMO at $4.45 per share. Our first take profit was set at $5.25.

$RMO released their 3rd quarter earnings report today after market close. In this report they reported a loss of $0.20 per share on revenue of $5.8 million. After this announcement $RMO experienced a very brief price jump to $5.70, but since then it has trickled back down to $4.78 per share.

My teams first take profit was hit post-market at $5.25 per share today. We sold all of our shares at $5.25 as we anticipate $RMO to stay within the $4-$6 range until they get around to announcing their 4th quarter earnings. We believe that this price range is a fair estimate, however this could change on the drop of really good or bad news.

We still believe in $RMO long-term, however we did not have enough sentiment to continue holding once our first take profit was hit today.

My team has made a gain of 18% from this trade.

Congrats to those of you who took this trade with us.

ENTRY: $4.45

TAKE PROFIT 1 (HIT): $5.25

TAKE PROFIT 2: $7.00

If you want to see more, please like and follow us @SimplyShowMeTheMoney

$KBR: Potential Space Cadet? KBR is positioned well in a variety of markets from aerospace to sustainable technology. As humanity begins to look beyond Earth, I believe KBR will be there to supply..

Hertz Ponzied - Gap Down Sell Off - Avoid the FOMOMeme stonks are about to collapse with crypto. Valuation matters. Rising rates US5Y new multi year highs. Finally. That's great for small cap gems.

Crypto & Meme Stonks to #cannabisreform

States Reform Act - Today 2pm ET

$KERN has the Compliance Data SOFTWARE. #thegem

how to #valueinvesting #investingnfts

$ESTC: Netherlands Data ManagementStrong momentum setup here with ESTC, going to be watching potential break outs next week

PalantirPalantir engages in the development of data integration and software solutions. It operates through the Commercial and Government segments. The Commercial segment offers services to clients in the private sector. The Government segment provides solutions to the United States (US) federal government and non-US governments. It offers automotive, financial compliance, legal intelligence, mergers and acquisitions solutions. Its products include Palantir Gotham and Palantir Foundry. (Via Robinhood). I'm big on the defense sector and knowing how much the government trusts this company I need to take a deeper look. The main thing that impressed me with Palantir outside of their general scope of business was the attractiveness of the Hedge Funds that has this in their portfolio. I normally don't bank on things like this. However, Vanguard (5%), Blackrock (4%), and State Street (1%) has this in portfolio. I do need to do more research on this company I will admit, but I'm confident that we are at a good price now for a good profit down the line (1 year or more out). Looking at the chart, looks like we on a retracement to the upside with a recent bear flag breakout. On the 15 min TF (This is the daily) there is a gap that needs to be filled around $23.66 It also seems as if price wants to break past the 20/50 ema if it does reach that gap which would be a good thing for shareholders. As I do more research, I will up my consideration!

What do you think?

Like, Follow, Agree, Disagree!

LG Display is Looking UndervaluedFundementals:

P/E ratio at 3.5

OLED Sales gonna be higher since the holiday season

LCD Prices remain high

LG beat Q3 expectations

OLED growth going to be lucrative as LG position itself as the leader.

Technicals:

14day MA cross 50 Day MA

Bullish Reversal Pattern Formation

Twitter bull & bust Casetwitter has recently made a sharp downside move towards 100EMA on the weekly chart which looks like will hold for a couple of upside sessions as of now as the market is over all in strong upside momentum with daily record close across the board. That being said, the over all picture for the company and stock looks a bit shaky with sharp sell off from the past week. if the stock does manage to climb back towards the 70/72ish area i believe it can still dive down towards the 2019 Area all over again. which will be an Ideal place to go long on this stock. but for Day traders this stock can be a real treat as the daily volume is high so the volatility is there to make money both ways. Personally i would go long with $48 as the stop loss area and $70 as Take profit and would be a seller at $70 with stop loss at $76 and all the way towards $30/35$ take profit.

Massive Ranges. Massive Risk. Massive Upside?NASDAQ:TSLA playing in some massive ranges. Given the high degree of global economic uncertainty and frothy market conditions we could see TSLA make one final herculean push, but reality seems like it will need to set in sooner than later (remember, this is a monthly chart.)

Would love to see this final rally top out with similarity to the previous rally that's charted. If this plays out, I suspect we consolidate in the massive blue box territory range. I personally would be thrilled to (finally) open a NASDAQ:TSLA long position in the bottom third of this blue box territory. If we do top out sooner than later, the question will become whether or not NASDAQ:TSLA ever re-enters the bottom portion of this range. Without question, things have changed since this previous rally, and it could easily be argued that these two rallies have absolutely nothing in common. For this reason, I will only be using this for rough entry targets. The kind of entries that you don't exit. The kind of position that you pass down in your will.

Thoughts?

Ramblings of a technology slave.Fintwit has been buzzing about gamestop,inflation, crashes, levels, archegos, gamma, short squeezes, amc, margin, PFOF, SI, CPI, Transition, Trump, Jay Powell, Gary 's bananas and more.

I don't think there has been a dull week in the markets since $GME woke the world.

I'm a HUGE fan of Roaring Kitty as he inspired me to start taking control of my financial future along with TheStockGuy .

That is until I lost money trying to understand markets, trading, hft, wsb, archegos all taught me valuable lessons in todays markets.

You see, I have undiagnosed ADHD.

I'm also a slave to technology and have been since before 87.

So much so I didn't even notice the .com burst working for a .com company.

I didn't notice the housing crisis while helping a business partner paint his 5k sqft house he bought for under 200k (a forclosure).

I wrote compression and data collection software for embedded systems (what you now know as IOS/Android) as my entry level job 20 years ago.

I believe covid life style was inevitable because I lived it since I was 25, over 20 years ago.

I have an unscratchable itch for practical learning.

I've read 1 book my entire life.

i've been consumed by video games ever since I was 10 (pong,tandy).

I think your family is everything.

I've built over 1000 websites.

I worked in the same NORTEL building shortly after, an incident.

time is the only real valuable asset.

I think Cannabis will be a replacement for alcohol in a few years ( NASDAQ:HEXO ).

My favorite movies are Bill and Ted's excellent adventure and the matrix.

I need a spell correction in TradingView Ideas before I loose my shit.

The first thing I wrote was a pac-man/ snake game for a high school teacher that inspired me to learn programming.

I lost a kidney to teenage drinking while studying advanced C++

I have studied and had first hand knowledge of everything crypto (dial in bulletin boards,gzip,rar,warez,pgp,p2p,napster) without ever being invested in it.

The last 6+ months I've been dissecting markets/trends in my limited spare time as copium for covid.

my 5yr son has ADHD and learned to be a doge coin tycoon in roblox in a few days, without any help/schooling, and only because he saw my interest in it.

I came across this, I guess you can call "idea", today and it was almost like a Eurika moment for me. It scratched that itch.

you see, I remember things, but not in vivid detail. experiences mostly.I heard decades ago about Moore's law.

The speculation was that by 2040 humans would be integrated into circuits. Guess who is on schedule of making that a reality.

What I'm trying to say is people should stop arguing and fighting around the word.

In the end, we're all going to be slaves of technology. Resistance is futile (but it's not the end).

With the help of technology I believe the human race will overcome our evolutionary bad cards and primitive egos.

I owe my entire life to advancing of technology.

Just think about it for a moment.

Imagine you could store your ideas, thought processes and experiences and memories in a computer for your loved ones to ask you a question in 40 years.

Using human -> technology advancements is the way of the future.

Always has been.

Happy Labor Day!

Talk to someone you care about. It helps me every time.

TECHNOLOGY TECHNICAL ANALYSISTechnical analysis for TECHNOLOGY Index based on Trend Analysis, Chart Pattern and Fibonacci Retracement

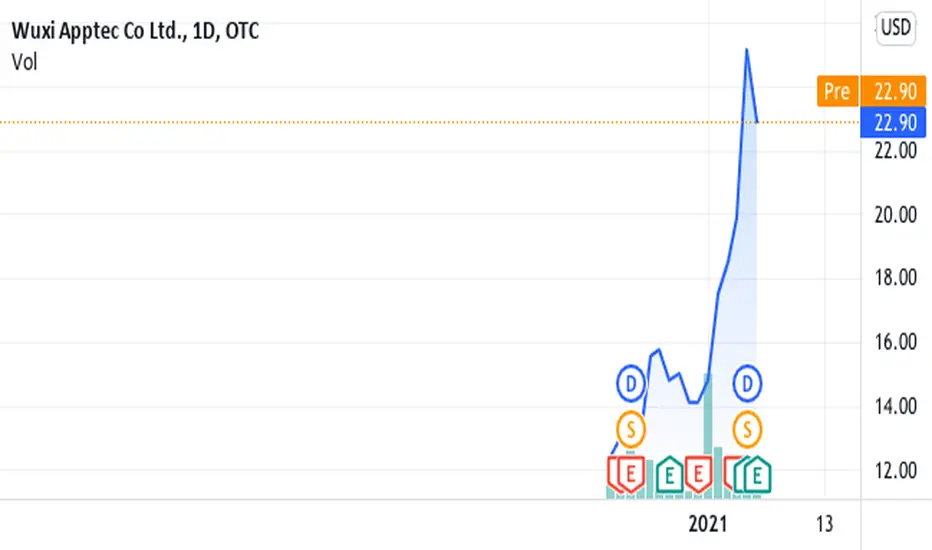

Wuxi Apptec Embraces a More Health-Conscious ChinaAfter a booming year in 2018, Wuxi has yet to slow down. The following article analyzes the success of Wuxi and its shortcomings.

China has released a number of new policies to help make the biopharma industry more transparent and efficient.

By 2020, China had full coverage of medical service systems in rural and urban areas; 90% of residents in China can access the nearest medical point within 15 minutes.

Wuxi Apptec has achieved consecutive quarter-over-quarter revenue growth for 13 quarters since the first beginning of 2018 (other than the first quarter of 2020 due to Covid-19).

Wuxi PharmaTech, a contract research and manufacturing organization, was founded by Dr. Ge Li in 2000. The company changed its name to Wuxi Apptec after Wuxi acquired Apptec Laboratory Services Inc., a US-based medical device and biologics testing company. Wuxi was delisted from the NYSE after going private, with a valuation of USD 3.3 billion. The company has thrived under the leadership of Ge Li as Wuxi went from just 4 people in 2000 to over 28,000 employees in 2021. Ge Li claims that the company's main mission is to provide high-quality research services at a low cost.

Wuxi has been growing rapidly since its inception, but we expect more imminent growth as China rolls out new healthcare-related policies and people become more health-conscious. Although the thriving healthcare market will inevitably attract new entrants that may evolve into strong competitors, Wuxi Apptec is highly likely to withstand the competition.

Rising health awareness

While brands like GNC and The Vitamin Shoppe helped raise healthcare awareness in the west, China was lackluster in this department and put little emphasis on personal well-being. Over the past decade, however, China's healthcare industry grew exponentially as society's attitude towards healthcare took a massive turn. The rising disposable income has led to the paradigm shift from being reactive consumers to proactive consumers. 84% of 3,000 respondents in China, in a survey conducted by Ipsos, reported that they are consciously making health-oriented decisions now.

According to a report by McKinsey, the global wellness economy, accelerated by COVID-19, has an estimated market size of USD 1.5 trillion as of 2021 with 5% to 10% annual growth each year. China reported the highest share of wellness spending online out of the six countries, including Japan. Monosodium glutamate (MSG) is a controversial flavor-enhancing ingredient for its possible adverse effects after consuming more than 3 grams. Major MSG producer Henan Lotus is experiencing a steady decrease in sales as the Chinese population, once the largest consumer of MSG, is becoming more health-aware. Bain and Kantar Worldpanel also reported that sales of chewing gums have also decreased by 14% in the last two years, chocolate sales decreased by 6%, and confectionaries decreased by 4%.

Favorable policies

President Xi announced the initiation of the Health China 2030 (HC 2030) plan in October 2016. The main goals are to prioritize healthcare on a national level, spur innovations in the healthcare industry, promote scientific development, and bring equal access to public health services to all parts of China, especially the country's rural areas. HC 2030 also aims to establish and enhance social policies and institutional systems regarding health, cultivate a healthy environment and intensively promote the advancement of the healthcare industry. Companies in the healthcare industry have seen something of a boost in their revenue as the healthcare trend continues. By 2020, China had extended medical service coverage so thoroughly that 90% of residents could access the nearest medical point within 15 minutes. The medical cost growth was also curbed as 2020 marked the lowest proportion of residents' medical expenditure in 20 years, with 27.7%.

Government policies have favored the development of the healthcare industry in China, especially that of Contract Research Organizations (CROs) and Contract Development and Manufacturing Organizations (CDMOs). In 2015, China had a backlog of over 20,000 drug registrations pending review and approval. The National People's Congress (NPC) held a meeting to discuss the reformation of the drug registration system. As a result, China Food and Drug Administration (CFDA) regulators received more resources than in the past, and the government launched the Market Authorization Holder Program (MAH) to make it easier to bring new drugs to the market. Furthermore, the Review and Approve Process (RAP) was simplified and made more efficient. For example, high-quality generics for orphan conditions with robust bioequivalence data will be eligible for expedited review during the CFDA's regulatory process. As of July 2021, a rare disease database (Orphanet) has recognized over 6,000 diseases, propelling pharma companies to roll out more medicine that will undergo a newly implemented process. CROs and CDMOs benefit from these new policies as pharma companies look to increase their research output to develop and produce new drugs. The expedited RAP incentivizes companies to roll out new drugs to cope with the increasing number of orphan diseases recorded.

The unique advantage

Wuxi Apptec is a "fully integrated contract research development and manufacturing organization with the ability to provide one-stop services that offer its clients assistance in discovery, development and manufacturing service demands." The wide variety of services that Wuxi covers allows the company to embrace the soaring healthcare market in China. Wuxi Apptec expects to extend its impact further as the global new drug R&D outsourcing market snowballs. However, Wuxi must persist in its R&D investment to fare well against companies with more flexible cash flow and new entrants with newer technology.

With a boom in customer demand, China's pharmaceutical R&D and manufacturing service market is expected to maintain its current high-speed growth. Wuxi's unique competitive advantage comes from its cost-efficient services. As of 2021, Wuxi has over 28,000 employees, most of whom are chemists, making Wuxi possibly the biggest employer of chemists in the world. Since the company has cheaper labor costs than the industry average, Wuxi can produce almost the same amount of research output for a fraction of the price (around 25% to 40% less than western companies' services).

Additionally, policies such as the MAH, expedited reviews, and HC 2030 have encouraged pharmaceutical innovations in China. Wuxi can capture the rising demand from Chinese pharma companies with its rather high R&D efficiency. Although Wuxi may not have the financial strength of some significant pharma companies with in-house R&D departments, the company will retain its leading position as one of the most profitable R&D and manufacturing businesses in China.

Financial metrics

According to Wuxi's interim report this year, the company realized CNY 10.54 billion total revenue, a year-over-year growth of 45.70%. CNY 2.50 billion came from China, which represents year-over-year growth of 48%. This data showcases the company's ability to capture the rising healthcare tides and demands for research and innovations. 48% growth also marks the largest increase compared to the company's revenue growth in the US and Europe. Wuxi also has a 100% retention rate of its top 10 customers from 2015 to the interim of 2021. As of June 30, 2021, the company's new clients have contributed CNY 849 million in revenue. Frost & Sullivan published a market research report in June 2021, which ranked Wuxi Apptec first by market share in the China-based drug discovery CRO market, pre-clinical and clinical CRO market, and small molecule CDMO market.

Bottom line

The combined forces of new policies and rising healthcare awareness have put Wuxi Apptec in a prime position to consolidate its leadership in China. The company should remain profitable as long as it maintains below industry average labor cost, heavy investment in its R&D department and reasonable M&A strategies to help expand and improve Wuxi's services and operations. Given the recent regulatory crackdown on Chinese tech companies, Wuxi should tread carefully in its effort to capture a more significant share in the Chinese market.

China's rapid growth in the healthcare industry bodes well for the nation, but what does it mean for its people? While the government poured resources into promoting innovations and development in the medical field, the affordability issue gained little attention. Although China has over 90% of residents with basic health insurance plans, it still poses a hefty paycheck for the average worker. Despite the rising wave of healthy living, China has to do more to provide sustainable healthcare.

For the full article with the charts, please visit the original link.

Technology Services has been on fire for the month of OCT.The Technology Service sector has been extremely bullish for this month.

One of the sector leaders on the heatmap across the board. This run may or may not stall out for a min.

Hate that I didn't spot these trades.

They are all now on my radar. I will only be eyeing smaller timeframes entries and exits due to the lateness of me now wanting to trade them.

I'm a swing trader at heart, but I scale in often.

Watch the TS sector over the next few weeks as a whole.

DARKTRACE Technical Levels Long Opportunity Without question DARK is a stock to be following in the world of AI and Cyberattacks

which seem to be all we read about just lately See WEF for enlightenment .

Technically we are sitting in the middle of a ascending channel

which we have been trading inside of since June .

I have drawn some levels using FIB to provide some areas of support and Entry if

any one wishes to start scaling in .

The IPO was 2.50 back in April and since then DARK has already printed 10.00GBP as a ATH

on Sept 24 followed by a 30% retrace and now retesting those previous highs again although

I am expecting the levels I have given to be claimed in the coming months.

Appreciate Likes Follows and constructive feedback .

See below for other Trade Setups

ATER BIGGEST BREAKOUT IN HISTORY?I potentially see one of the biggest breakouts in the history of all stocks????? Look at what I am seeing.

$DKNG GETTING READY FOR A +40% MOVE!What Is the Accumulation Area?

The accumulation area on a price and volume chart is characterized by mostly sideways stock price movement, which is seen by investors or technical analysts as indicative of large institutional investors buying, or accumulating, a large number of shares over time.

Source: www.investopedia.com

1HR

- Price trading sideways since late September.

Analyst Price Target on $DKNG (TipRanks)

High: 105

Average: 70.06 (44.01% Upside)

Low: 41