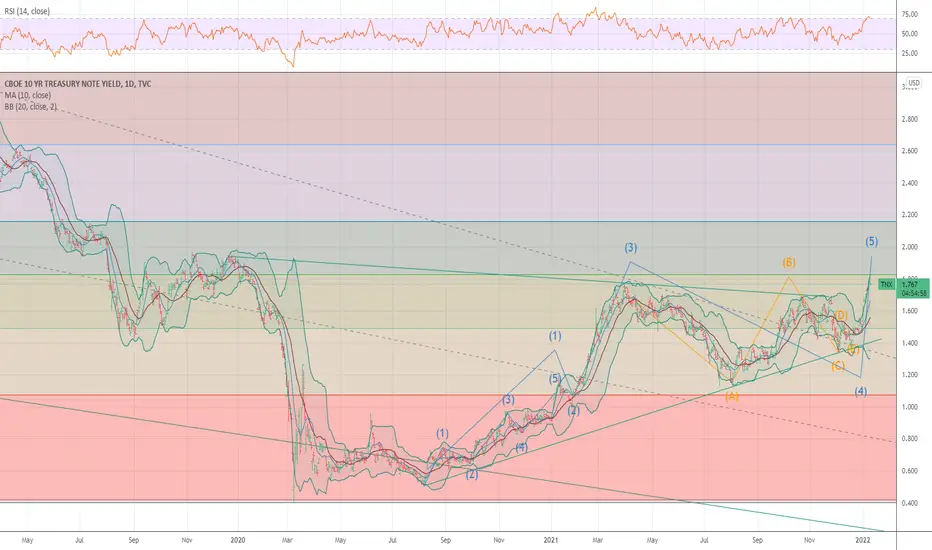

TNX - 10Yr Yields Sell Offers and Bond VX / Trouble

Bond Bagholders just never learn - this Secular Cult is doomed to extinction.

The two-year Treasury yield posted its biggest single-day jump since the

market volatility of March 2020.

Of course, this was after Federal Reserve Chair Jerome Powell promoted

the Policy Flip Flop that the Fed will raise rates in March, and left the screen

porch door open for a quicker than-anticipated pace of rate increases.

The Dot Plot is wiggling in excitement.

IN reality, the FED will begin to Temper expectations.

It is what they do - Lie Cheat Steal / Delay.

10 Yr Yields have seen another fantastic ROC-driven Spike which advanced

well ahead of the Pre-Spring Meltup in 2021.

__________________________________________________________________

TNX will provide a very large indication as to how the preset Wedge on the ES/NQ

resolve, likely this week...

Keep it in purview at all times, sudden violent reactions are to be expected.

TNX

𝟭𝟬-𝘆𝗲𝗮𝗿 𝗗𝗮𝗶𝗹𝘆: $TNX Daily. Resistance HoldingPossible the market has gotten ahead of itself on the rate rise? 4 hikes fully priced in already. Ascending channel at key resistance area

$TLT $ZN_F $ZB_F $TYX $DXY $SPY $VIX $QQQ #Tech #Rates #Trading

TNX ProjectionsBased off this *very* well respected weekly channel on the 10 year, I do believe 2.0-2.5% is quite possible, if not likely.

Real interests at historical low - S&P500/M2SL at big resistanceHi folks!

I just tried to take a broader perspective on things again, and wanted to take a look at the

pricing of the S&P500 relative to the M2 Money Supply, as well as the effect of real interest rates on markets.

Note that the orange line here is the negative of the real interest rates - that is, .

My takes are these:

(1) The S&P500 relative to the M2 (broad -i.e. including credit) money supply is at a critical level given historical data - only once have this level of resistance broken (during the dotcom bubble).

(2) The real interest rate have NEVER been this negative - with current rates even beating those of the 70´s and 80´s.

(3) (Not shown in chart) The treasury have been falling constantly since the 80´s, and have nowhere to go to the downside ATM.

(4) The critical support of the S&P500/M2SL lies approximately at the break-even for real interest rates if we compare their development from the 60.

I strongly believe that the real interest will move towards zero eventually - either the Fed and the governments manage to curb inflation rather quickly through credit regulations, taxes and interest rate hikes,

or the markets will just ignore it in the end and dump their bonds (no one will hold bonds at a certain loss of 5.6% or more in annual terms - that is madness!).

When this occurs, the stock market will take a huge dump - even compared to the M2 money supply (which will most likely decrease in the time to come!).

DYOR.

NFA.

I wish you all well!

TNX - Clear indication of a Pullback10 Year Yeidls should begin to pull back, this will provide a

welcome wind for TECH into EPS Season.

Bond VX is retreating as well.

RSI/STO Summation indicates an overbought condition.

____________________________________________________

Seemingly - this implies our thesis for the Recac has come into

the Trade and was supported by the Short Squeeze and Gamma

Call Squeeze after the Put Close.

Jumbos want to make $, it is axiomatic the ranges will expand and

Profits can be made on ALL sides of the Ranges.

It is that simple.

ZN - 10 Year Note Futures / An important ChartThe importance of ZN as an Instrument cannot be overstated.

It has been extremely technical and Reliable in assisting us in

forecasting Rate Mid Curve and provided the ROC's for TNX.

Today's MAcro Data begins with the CPI @ 8:30 AM EST using

the new Base Effect from the BLS.

______________________________________________________

CPI is projected to be 4%.

Food prices have already increased substantially into 2022

as we indicated Mid-Q4 2021 - Pordiucer were going to begin

passing along increases at an average rate of 20-23%.

Energy continues to Rise as do Commodities, on balance, across

the Board.

M2 continues to move higher, as does the Fed's Balance Sheet.

_______________________________________________________

The reaction to the CPI this morning will provide direction for the

Indexes the balance of the week.

Pricing Power is being passed along to end-users (consumers) at

a time when the Federal Reserve is indicating they are about to begin

an aggressive reduction in Liquidity and an accelerated pace of

increases to the Fed Funds Rate.

We have seen back to back ALGO driven increases in the ES / NQ / YM

and indicated 10 Yr Yields would pullback ~ 1.81% (1.808 was close

enough).

2021/2022 measured move is now .998 to 1.808 - a near doubling of

the Mid Curve.

________________________________________________________

The Bond "safety" Trade wasn't entirely wrong until the Curve

began to work its magic. We indicated in July Rates would begin

rising again into the end of 2021.

Where the Bond Buters lost sight of the Safety Trade was quite

simple - Convention holds only when the Yield Curve is steepening.

As YCC gave way to a FED backstop where the recycling ballooned

the Fed's Balance Sheet and Auction after failed Auctions began to

appear beginning at the long end of the Curve.

My Thesis proved 100% correct, then as now.

We anticipate a reaction to Mid Curve on today's ReCalc.

Safe Trading.

10 yr yield to see 1.75 to 1.86 at 50% TOPPED The chart posted is that of the 10 yr yield A few months back my forecast was for a move backup to 1.75/ 1.86 into the 50% area . I stand by this being the TOP of the range and we are now set up for deflation to show up . the 10 year will not be moving up for sometime

TNX - Monthly Historical Chart 40 Year ChannelThe Event which will provide relief to the Bond Complex is the Federal Reserve

walking back its most recent Policy Statement.

The Short End of the Curve witnessed an aggressive move of 6-9 Bips. This doesn't

appear to be much on the surface of it.

Unfortunately, it is.

______________________________________________________________________

The Yield Curve is not effectively communicating at either end and throughout the

Curve.

Far too much is made of prior Paradigms, with a real lack of understanding of the Glacial

movements in the Bond Complex.

40 years is a long time - an unparalleled Bull Market in Binds coming off the Volcker Era

after the Whip Inflation Now Era.

Price in trend - it remains in Trebbt as the sheer largess of the Bond Market is 11X that

of Equities.

_______________________________________________________________________

The Risks remain to Rates rising.

Hopefully - there is not a disorderly eruption as it would wreak havoc in ways we have

not seen in a very long time.

Blackrock at key supportAs you can see, the price has respected the 200sma (blue) since the break from Covid lows.

Risk-reward-ratio presented is interesting as you will figure out if you are right or wrong pretty quickly; especially since the Bollinger bands have been contracting as we have consolidated.

Trade setup:

Target around $1000 for profit-exit.

Loss-protection exit 1-2% under the 200sma.

Fundamental Analysis '

- The $TNX (interest rates) has broken out which is positive for financial institutions.

- There is a cyclical tilt to the market as high valuation companies in the technology sector are hit hard.

* Note: Earnings are starting at the end of next week for the financial sector.

TNX - Deep CrabThese harmonic patterns have been a real hit or miss for me. However I couldn't help, but notice that the fibs alligned so nicely.

The "potential reversal zone" is the 1.618 XA project @ 2.519.

The BC projections of 2.24 and 2.618 (both in grey) were used to define the range of that zone.

The AB=CD projection was also include of the 1.272 and 1.618.

1.272 is an alternate target

1.618 because I like the symmetry with the 2.618 BC projection at 2.254.

Despite labeled with a "potential reversal zone", keep in mind the momentum on this sucker. The 30,40, and 50 week MA look like they are ready to flip bullish in the coming weeks if this thing gains some ground.

Not financial advice by any means. I just thought it'd be fun to share. Best of luck!

harmonictrader.com

I HAVE MOVED BACK TO 100 CASH TODAY 11.55 AM T10 yr is near my 1.75 target . and really no move in the put/call the vxn hit a target but no puts buying so i thing vxn could see a 41 handle . minor gain in calls ndva a 2 point gain and broke even on msft . I HAVE covid and this is so hard even to type this back to bed .

TNX - The Tech WreckerAs yields began another disorderly move, The NQ finally took notice.

The range posted for the NQ this Morning - Traded in Full.

It was nice to see Reality begin to sink in finally.

Industrial caught the spillage while the 711s were hammered with9ut

relenting.

____________________________________________________________

FOMC @ 2 PM EST tomorrow should set the Trend for some time to come.

Bonds have been providing clear indications of a mishap, in particular ZN.

TNX - ROC @ 2.43%10 Year Yields getting itchy once again.

2Yr - 10Yr worthy of observation.

Dot Plot - 2022 @ 1.125%

Page 4 - www.federalreserve.gov

10 Year Note Yield - Short / Intermediate Duration

Inflation has been mispriced in excess of 16 months. The Federal Reserve should have

begin to reduce Liquidity by Mid 2020 as Fiscal Stimulus had taken effect into July into

September when Fiscal Stimulus began Peak.

The Fed's Balance Sheet continued to expand with the Purchase of RMBC/MBS/UST/Corp.

Debt, while Shadow operations under FASB 56 continued to increase nearly matching the

Fed's accumulated Holdings. $8 Trillion in combined Net exposures, provided outsized

gains for Equities.

Bonds began a revolt in early 2021, only to see the Fed step up and employ YCC in early

April, attempting to stem the fastest rising rates in US History.

The Fed and US Treasury can control all Points on the Yield Curve as the Buyer of last resort.

Clearly, the Short End used to require far less effort when re-fundings were under 30 Months.

This is no longer the case, as they expand funds from 5-7s out to the '30s where we have seen

multiple "Auction Failures". Buyers simply refused to participate.

A Creep effect begins to enter the equation with respect to expectations.

The Long End of the Curve begins to flatten, traditionally indicating a recession ahead according

to conventional Bond Wisdom. And therein is the issue, this is not the 1970s and StagFlation

is not the Environment.

We are within an Inflationary Depression and have been for some time by any real and

credible Metric.

Economic Activity began to lag in Q1 2021, by Q2 the results were Peak consumption for

the US Consumers. It will be downhill for into Q3 and worsening into Q4 as we indicated

in July, all metrics were showing clear signs of another Global Slowdown as occurred in

Q2/Q3 2019.

Excess Capacity was quietly, but quickly becoming underutilized, as well as under-reporting

of Global Economic prospects.

____________________________________________________________________________

For 2022, I see a rapid and substantive decline gaining Momentum.

Economic Activity was pulled forward into 2021.

Inflation Numbers need to be brought to heel with BLS Recalc for Inflation, taking effect

in January 2022. This extraordinary measure will fail. The headline Numbers adjusted by

this tampering will not change Prices Paid.

Malcontent - the result as What is purported and Reality will diverge to create further distrust

and increasing Loss of Confidence - Quickly compounding.

Quietly, absolutely not... as Monetary Policy will not be alone as the "Build Back Better" Fiscal

Policy has been delayed. Further Stimulus down the road... only serves to compound the problem

and stave off the Pitchforks and Lanterns.

_____________________________________________________________________________

Covid Variants continue to expand - 19/ Epsilon / Delta / Omicron / New Variant TBA

The Fed indicated in their most recent FOMC Meeting Minutes and Press Conference, Omicron

is an "Uncertainty" and why the FED called it out within their Policy Statement.

Indicating the US Economy could handle the "Omicron" Variant at present while acknowledging

the FED is a "Long Way from knowing what it will turn out to be..."

"It is unclear on how the New Variant would suppress Demand and Supply."

"Wave upon wave, people are learning to live with this..."

Vaccinations, according to the Raven reduce the "Economic Effect."

Timeline for Variant assessment - 3 to 6 Weeks... Omicron doesn't really have an impact on the

Taper as the Chair wants participants to believe.

_______________________________________________________________________________

The Stock Market is and is not the Economy - it depends on which way the wind is blowing. A

Northern Gale changes arrangements, this is what the Raven is laying the groundwork for into

Q1.

An overextended Credit based Financial Economy has a great number of hurdles ahead in addition

to a Central Bank which may or may not embark on further meddling.

That is immaterial to a larger extent as Global Markets for DEBT are Tightening at a time when

the compound effect of all Economic activity is waning... instructs us all as to how "intent" will

reprice DEBT / Inflation / Expectations and Sentiment.

__________________________________________________________________________________

Factors that lead to growth in 2021... the plug is being pulled.

Q4 rebound is a seasonal pattern, and yet Holiday sales will prove to have been DISMAL.

The Dollar remains at risk to the upside, clearly holding its own, the Dollar will move higher

at least to 100.

___________________________________________________________________________________

The Fed can do plod along - Markets will adjust as they permit the Net Drag to do their work for them.

___________________________________________________________________________________

Regional BAnks are showing two consecutive quarters of Savings Drawdown from Q3 thru Q4.

___________________________________________________________________________________

The Inflation/deflation debates have always amused me as an Economist. This is best framed within the

context of Credit Malfeasance again the expansion of Moore's Law to an Exponential Function.

Technology is deflationary, it reduces a great many Economic functions while increasing efficiencies

in ways, most fail to understand.

Monetary Policy is the Inflation component with an added twist, the Supply Shocks and shortages due

to the Shut Down of the Global Economy. An extraordinary time in Humanity's History.

This will be discussed at length in follow-on commentary.

_____________________________________________________________________________________

Moral hazards abound and are plentiful at precisely the wrong time.

A Nation of Gamblers - www.tradingview.com

PS. - the House always wins

10 Year Note Yield - 2%+ Ahead Into June - AugustThe Price Objective remains 2.28%.

Beyond sewing the usual seeds of discontent, observe the Larger Monthly Indications.

The above Chart is of extreme importance, it demonstrates how Capital Stocks begin to

turn, Glacial at first, as Momentum builds, they begin to accelerate.

This will end up a 4 or 5 part series discussing the potential impacts.

_____________________________________________________________________________

Price has broken above 2 Key Downtrends. It is attempting to reach the 3rd, which has acted

as resistance for years.

This is a material change in the underlying Bond Market Note Structure. It is no longer the

conventional depository for Principal and Coupon as a great many believe.

______________________________________________________________________________

Capital Stocks are in need of review:

Real Estate - the Hybrid / Principal and Coupon (Rents) A Negative correlation to Higher Rates

with cascading effects to Higher Rates. A 70% increase in Conventional and Jumbo Mortgage

Rates would see a 18 to 24% drop in the Price of Residential Real Estate.

Equities - the Buyback / Prop where Corporate Debt is used for Buybacks

Increased borrowing Costs temper Buybacks, Inflows do not. This is a double

edged sword we will discuss in detail.

Bitcoin - The repository (Not Depository) for excess Liquidity. BTC has a Positive

correlation to rising Rates. BTC has a Price Objective near $137K at the extreme

extensions for Rates of the 10 Year Note Yield.

Bills / Notes / Bonds / - Debt instruments with attendant Hybrid function of Principal / Coupon.

______________________________________________________________________________

Bonds (prior to 2006) were traditionally a function of the Business Cycle which has been supplanted

by the Credit Cycle (no longer a Cycle by appearances).

Prior to 2008 Congress would pass a Bill in the Legislature, after speaking with the US Treasury to

determine how to "Finance" its Fiscal requirements. Once the Bill was passed and signed into Law,

the US Treasury would conduct operations with the Federal Reserve Central Bank in New York to

issue the increased Credit/Debt (The FED taking their statutory 6% issuance) to the US Government.

Bills, Note and Bonds would be placed with Primary Broker Dealers (Fed Member Banks) and offered

at "Auction" to the Public, Institutions, exogenous Central Banks, Funds, Swaps and overnight Swaps

for shorter duration T-Bills sweeps.

This funding mechanism for DEBT no longer exists.

FASB 56 - took the Governments Budgets and Funding "Dark" as a "Matter of National Security". The

General Purpose Federal Financial Reports are Classified Documents.

The material Facts of FASB 56 - files.fasab.gov

13 Short Pages well worth educating one's self as to how the Government conducts itself.

TARP/TALF were undisclosed Operations which maintained their Shadow Financing for years.

94% of Americans were against Commercial Bank Bailouts. Privatizing Gains while publicly

subsidizing losses was viewed with extreme displeasure.

___________________________________________________________________________________

Over the past 14 Year, we see the outcome(s) - Interventions in Auctions by the Federal Reserve,

Yield Curve Control, the Outright Purchase of RMBS/MBS again (this began in 2004 in size as the

Federal Reserve's concerns over Real Estate began to mount).

The FED has become the buyer of Last Resort - currently @ $8.758 Trillion in Assets of which

$8.296 are "Securities" - this excludes "Shadow Operations" of FASB 56.

In less than 2 years, the Federal Reserves Balance Sheet rose from $4.212 Trillion to more than

Double that amount (NET of Shadow Operations)

I estimate Shadow Operation under FASB 56 to be in excess of $3.8 Trillion - this excludes the

Trillions missing from the Federal Coffers @ DOD, HUD and a great many other Agencies.

_________________________________________________________________________________

Follow - On commentary will begin breaking down the Trends and discuss the potent outcomes

and timeframes for each Capital Stock.

There is a large amount of information to be discussed, requiring a methodical analysis of

all points on the outcome curve.

More to follow - HK

THE BIGGER PICTUREI don't think people have any idea what is about to happen..

Retail is going to get crushed

Long DXY

Short 10-year treasury

Short BTC

BTCUSD vs TNXBitcoin could be headed lower vs TNX. Bitcoin has been in this trend for over 3 years and it looks like it popped out the bottom. BTCUSD/TNX ratio tells us that rates are headed higher if bitcoin were to stay flat.

10-YEAR YIELD ANALOGUEPossible analogue from the lead up to the last financial crisis. Potential catalysts still taking shape. Continued central bank NIRP would support this scenario.

TNX - Zimbabwe / YCC / Capital Stock / Melt Up / FX - ECB BOJ EUBonds are at a Critical Juncture.

Unable to serve their function due to YCC we are now

staring down the Crack the Boom Phase V.5

Not much is functioning correctly... not remotely.

_______________________________________________

We are quickly becoming Zimbabwe.

Of the 3 Capital Stocks, Equities may well end up the

catch-all bucket and Melt Up in Violent Fashion.

By appearances, the Equity Complex itself is the remaining

capital Stock for the Inflation Trade.

Real Estate is immobile, illiquid and the Bond Market

remains on the Path of Destruction. Both DOA in Real Terms.

If you did not believe this earlier, perhaps now...

The Raven has made it clear you will lose 2x as quickly.

Welcome to Zimmy World akin to Waterworld but we are

afloat in a Sea of Sharks feeding on the remaining viable,

liquid - Equity Complex.

McC OSC's are deeply in negative for all Indices - DEEP.

They declined yesterday as the ES NQ YM RTY all reversed.

Frankly, horrifying as What is, is not what should be as the

Flamingo's Sports Book has gone into DeFib Mode.

___________________________________________________

They are using the Recalc to extend and pretend, a concern

we expressed would be a game-changer, it now is realized.

Yes, the Indices are grossly overbought and could face a reversal...

Maybe...

A great deal will depend on how committed Everyone is to the

Zimbabwe Trade.

___________________________________________________

Sad, pathetic, destructive - yes.

It is what it is, be prepared for complete Insanity.

It's beginning.

Powell made it quite clear, repeatedly clear - the Focus and cover

is labor. Rates... the slide in 2 for 2022, lied, of course, then added

potentially 3, then mentioned 2024...

The FEDs #1 Mandate is Price Stability... # 2 Full Employment.

Raven went all in by not mentioning Mandate #1, they abandoned

it. It isn't Transitory - it is the way, Instability.

Both are now a joke so depressing, it warrants consideration

as to what they are truly after.

It is quite simple - protect their own.

It disgusts me to write this, but I'd be remiss in not doing so.

_____________________________________________________

The Only thing that can upend this insidious trend is Yields.

Flattering to Inversion on the Short End will take time.

Equity Complex Extensions to follow in Commentary.

Bonds Vs BTC and Equities What does everyone think about this?

This is the conclusion forecast of all the previous ideas I've been working up to

I don't see many people talking about the bigger picture of what is actually happening with Smart Money VS Retail

TNX and BTC show the correlation

TLT and the NDX show a similar but opposite correlation

Bonds lead then Risk assets follow accordingly

Wouldnt this make sense fundamentally?

BTC Is a hedge against inflation so it copies the 10-year bond outpacing inflation

Equities especially growth stocks are not a hedge to inflation so they have an opposite correlation to what interest rates are doing

I think something big is going to happen and a lot of people will get shaken out.

You can see the big fear narratives all stacking up before the new year!

The whales have been trick or treating this holiday season and I think this X mas rally was a big trick for all the retail shrimp to get caught in the feasting season.

The Roadmap to Bitcoin and the NASDAQ 100 My observations:

The 10-year Treasury bond is a leading indicator to show where smart money hedges its bets. The 10-year treasury bond is also perfectly correlated to Bitcoin. When this moves up, Bitcoin goes up. When this moves down, Bitcoin goes down. The NASDAQ 100 on the other hand has a lagging inverse correlation to the 10-year Treasury bond. The 10-year Treasury bond is currently taking the shape of an inverse head and shoulders and also is in an uptrend. We also have the Federal Reserve possibly tapering and hiking interest rates in the near term. The likely situation is that interest rates move higher from here.

The prediction:

What I am seeing in this scenario is that the 10-year bond moves up to the multi-year resistance zone which ultimately means that Bitcoin has 1 last leg up before a leveraged blow-off top scenario. This will also coincide with these events while they unravel, the stock market is currently in its A-B-C correction wave. After this point, it is likely that the 10-year Treasury bond will be rejected off the multi-year resistance and nose-dive south. This is when Bitcoin will start its massive correction and the Bitcoin dominance will fall off a cliff resulting in a massive Alt Season. During this time while interest rates go down, the stock market will then move to higher highs and there will be potentially some catalyst to bring it down to one synchronised dance.

My points to support this theory:

* Bitcoin is still in an uptrend.

* The Fed is anticipating interest rates to rise and taper, which is a real possibility.

* The 10-year bond is taking the shape of an inverse head and shoulders and is currently in an uptrend.

In summary:

There is currently a lot of fear in the markets and what I think is happening is that the big players are tax-loss harvesting risk-on assets, hence why the DXY has been gaining superior strength. This ultimately drives the risk on asset prices lower changing the sentiment of the market to bearish. In the New Year of 2022, smart money can re-buy back risk on assets at a cheaper price to give them a headstart to 2022.

BTC ROAD MAP Current Observations with the 10-year treasury bond and BTC

There is an identical correlation between the 2 and we can see BTC is used as an inflation hedge moving with the interest rates.