USDJPY to 150.500USDJPY is going to test 150.500 level, Dollar is going to be stronger in next few days.

After testing this level we will waiting price moves.

Follow to see next signals

Yen

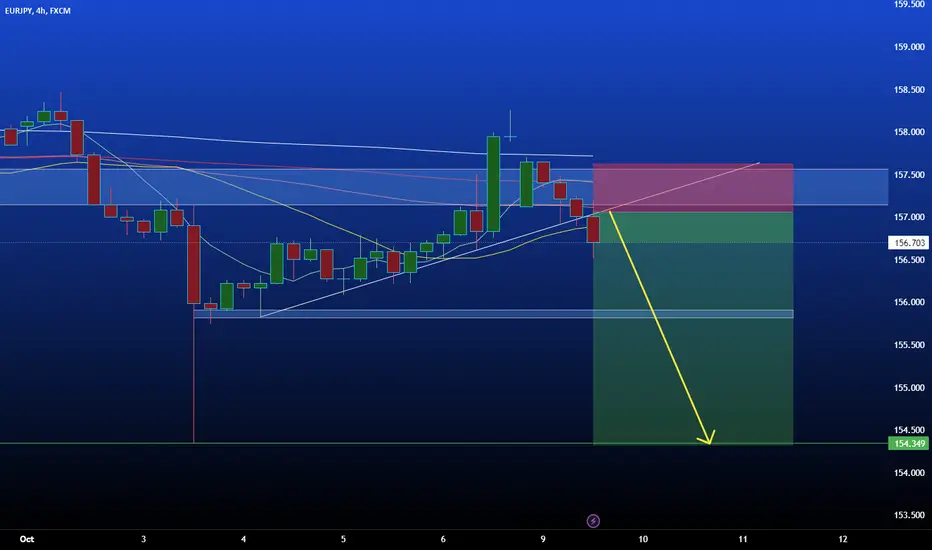

EURJPY: Price gone higher than expected for a better entry.Price moved a lot higher to fill the overnight gap down.

My idea yesterday became invalid but this gives me a better entry:

Gap down suggests general direction and now the gap has been filled, supported by a pinbar on the 1hr I'm getting in short with a first TP at 156 (ultimately I think 154), but I think this could be the start of the reversal.

EURJPY H4 | Heading into resistanceEUR/JPY is rising towards a pullback resistance and could potentially reverse off this level to drop lower.

Sell entry is at 183.020 which is a pullback resistance level.

Stop loss is at 184.550 which is a level that lies above a pullback resistance.

Take profit is at 181.128 which is a pullback support that aligns with the 38.2% Fibonacci retracement level.

High Risk Investment Warning

Trading Forex/CFDs on margin carries a high level of risk and may not be suitable for all investors. Leverage can work against you.

Forex Capital Markets Limited (www.fxcm.com):

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 70% of retail investor accounts lose money when trading CFDs with this provider. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money..

Stratos Europe Ltd, previously FXCM EU Ltd (www.fxcm.com):

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 74% of retail investor accounts lose money when trading CFDs with this provider. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

FXCM Australia Pty. Limited (www.fxcm.com):

Trading FX/CFDs carries significant risks. FXCM AU (AFSL 309763), please read the Financial Services Guide, Product Disclosure Statement, Target Market Determination and Terms of Business at www.fxcm.com

Stratos Global LLC (www.fxcm.com):

Losses can exceed deposits.

Please be advised that the information presented on TradingView is provided to FXCM (‘Company’, ‘we’) by a third-party provider (‘TFA Global Pte Ltd’). Please be reminded that you are solely responsible for the trading decisions on your account. There is a very high degree of risk involved in trading. Any information and/or content is intended entirely for research, educational and informational purposes only and does not constitute investment or consultation advice or investment strategy. The information is not tailored to the investment needs of any specific person and therefore does not involve a consideration of any of the investment objectives, financial situation or needs of any viewer that may receive it. Kindly also note that past performance is not a reliable indicator of future results. Actual results may differ materially from those anticipated in forward-looking or past performance statements. We assume no liability as to the accuracy or completeness of any of the information and/or content provided herein and the Company cannot be held responsible for any omission, mistake nor for any loss or damage including without limitation to any loss of profit which may arise from reliance on any information supplied by TFA Global Pte Ltd.

The speaker(s) is neither an employee, agent nor representative of FXCM and is therefore acting independently. The opinions given are their own, constitute general market commentary, and do not constitute the opinion or advice of FXCM or any form of personal or investment advice. FXCM neither endorses nor guarantees offerings of third party speakers, nor is FXCM responsible for the content, veracity or opinions of third-party speakers, presenters or participants.

USDJPY H4 | Rising into resistanceUSD/JPY is rising towards a pullback resistance and could potentially reverse off this level to drop lower.

Sell entry is at 149.414 which is a pullback resistance level.

Stop loss is at 150.160 which is a swing-high resistance.

Take profit is at 148.406 which is an overlap support that aligns close to the 38.2% Fibonacci retracement level.

High Risk Investment Warning

Trading Forex/CFDs on margin carries a high level of risk and may not be suitable for all investors. Leverage can work against you.

Forex Capital Markets Limited (www.fxcm.com):

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 70% of retail investor accounts lose money when trading CFDs with this provider. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money..

Stratos Europe Ltd, previously FXCM EU Ltd (www.fxcm.com):

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 74% of retail investor accounts lose money when trading CFDs with this provider. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

FXCM Australia Pty. Limited (www.fxcm.com):

Trading FX/CFDs carries significant risks. FXCM AU (AFSL 309763), please read the Financial Services Guide, Product Disclosure Statement, Target Market Determination and Terms of Business at www.fxcm.com

Stratos Global LLC (www.fxcm.com):

Losses can exceed deposits.

Please be advised that the information presented on TradingView is provided to FXCM (‘Company’, ‘we’) by a third-party provider (‘TFA Global Pte Ltd’). Please be reminded that you are solely responsible for the trading decisions on your account. There is a very high degree of risk involved in trading. Any information and/or content is intended entirely for research, educational and informational purposes only and does not constitute investment or consultation advice or investment strategy. The information is not tailored to the investment needs of any specific person and therefore does not involve a consideration of any of the investment objectives, financial situation or needs of any viewer that may receive it. Kindly also note that past performance is not a reliable indicator of future results. Actual results may differ materially from those anticipated in forward-looking or past performance statements. We assume no liability as to the accuracy or completeness of any of the information and/or content provided herein and the Company cannot be held responsible for any omission, mistake nor for any loss or damage including without limitation to any loss of profit which may arise from reliance on any information supplied by TFA Global Pte Ltd.

The speaker(s) is neither an employee, agent nor representative of FXCM and is therefore acting independently. The opinions given are their own, constitute general market commentary, and do not constitute the opinion or advice of FXCM or any form of personal or investment advice. FXCM neither endorses nor guarantees offerings of third party speakers, nor is FXCM responsible for the content, veracity or opinions of third-party speakers, presenters or participants.

AUDJPY: Is this the start of the reversal?We saw some JPY strength last week and I think we could be starting to see reversal, however my confirmation of this will be below 93 support.

Even though BoJ hasn't intervened yet, there was a lot of buying in the week which we saw against the USD, I still expect BoJ intervention soon.

Nice pinbar rejection on the 4HR from my resistance block.

Looking for a short here on LTF's, but with tight SL and will keep it following any move down.

GBPJPY H8 - Pending Short SignalsGBPJPY H8

Probably the cleanest setup out of it's peers that were analysed on Sunday, GBPJPY resistance/support price of 183 looks very clean. We are coming up for a test of that 183.00 handle, it could certainly be an opportunity to grab shorts.

As markets opened on Sunday we saw the bearish gap, I wonder if this is something that will pin and dump towards the liquidity lows of 178 from last week.

AUDJPY H4 | Rising into 50% Fibo resistanceAUD/JPY is rising towards a pullback resistance and could potentially reverse off this level to drop lower.

Sell entry is at 95.039 which is a pullback resistance that aligns with the 50.0% Fibonacci retracement level.

Stop loss is at 95.580 which is a level that sits above the 61.8% Fibonacci retracement level.

Take profit is at 93.887 which is a swing-low support level.

High Risk Investment Warning

Trading Forex/CFDs on margin carries a high level of risk and may not be suitable for all investors. Leverage can work against you.

Forex Capital Markets Limited (www.fxcm.com):

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 70% of retail investor accounts lose money when trading CFDs with this provider. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Stratos Europe Ltd, previously FXCM EU Ltd (www.fxcm.com):

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 74% of retail investor accounts lose money when trading CFDs with this provider. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

FXCM Australia Pty. Limited (www.fxcm.com):

Trading FX/CFDs carries significant risks. FXCM AU (AFSL 309763), please read the Financial Services Guide, Product Disclosure Statement, Target Market Determination and Terms of Business at www.fxcm.com

Stratos Global LLC (www.fxcm.com):

Losses can exceed deposits.

Please be advised that the information presented on TradingView is provided to FXCM (‘Company’, ‘we’) by a third-party provider (‘TFA Global Pte Ltd’). Please be reminded that you are solely responsible for the trading decisions on your account. There is a very high degree of risk involved in trading. Any information and/or content is intended entirely for research, educational and informational purposes only and does not constitute investment or consultation advice or investment strategy. The information is not tailored to the investment needs of any specific person and therefore does not involve a consideration of any of the investment objectives, financial situation or needs of any viewer that may receive it. Kindly also note that past performance is not a reliable indicator of future results. Actual results may differ materially from those anticipated in forward-looking or past performance statements. We assume no liability as to the accuracy or completeness of any of the information and/or content provided herein and the Company cannot be held responsible for any omission, mistake nor for any loss or damage including without limitation to any loss of profit which may arise from reliance on any information supplied by TFA Global Pte Ltd.

The speaker(s) is neither an employee, agent nor representative of FXCM and is therefore acting independently. The opinions given are their own, constitute general market commentary, and do not constitute the opinion or advice of FXCM or any form of personal or investment advice. FXCM neither endorses nor guarantees offerings of third party speakers, nor is FXCM responsible for the content, veracity or opinions of third-party speakers, presenters or participants.

CADJPY H4 | Heading into 38.2% FiboCAD/JPY is rising towards a pullback resistance and could potentially reverse off this level to drop lower.

Sell entry is at 108.896 which is a pullback resistance that aligns with the 38.2% Fibonacci retracement level.

Stop loss is at 109.680 which is a level that sits above an overlap resistance and the 50.0% Fibonacci retracement level.

Take profit is at 107.490 which is a swing-low support.

High Risk Investment Warning

Trading Forex/CFDs on margin carries a high level of risk and may not be suitable for all investors. Leverage can work against you.

Forex Capital Markets Limited (www.fxcm.com):

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 70% of retail investor accounts lose money when trading CFDs with this provider. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money..

Stratos Europe Ltd, previously FXCM EU Ltd (www.fxcm.com):

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 74% of retail investor accounts lose money when trading CFDs with this provider. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

FXCM Australia Pty. Limited (www.fxcm.com):

Trading FX/CFDs carries significant risks. FXCM AU (AFSL 309763), please read the Financial Services Guide, Product Disclosure Statement, Target Market Determination and Terms of Business at www.fxcm.com

Stratos Global LLC (www.fxcm.com):

Losses can exceed deposits.

Please be advised that the information presented on TradingView is provided to FXCM (‘Company’, ‘we’) by a third-party provider (‘TFA Global Pte Ltd’). Please be reminded that you are solely responsible for the trading decisions on your account. There is a very high degree of risk involved in trading. Any information and/or content is intended entirely for research, educational and informational purposes only and does not constitute investment or consultation advice or investment strategy. The information is not tailored to the investment needs of any specific person and therefore does not involve a consideration of any of the investment objectives, financial situation or needs of any viewer that may receive it. Kindly also note that past performance is not a reliable indicator of future results. Actual results may differ materially from those anticipated in forward-looking or past performance statements. We assume no liability as to the accuracy or completeness of any of the information and/or content provided herein and the Company cannot be held responsible for any omission, mistake nor for any loss or damage including without limitation to any loss of profit which may arise from reliance on any information supplied by TFA Global Pte Ltd.

The speaker(s) is neither an employee, agent nor representative of FXCM and is therefore acting independently. The opinions given are their own, constitute general market commentary, and do not constitute the opinion or advice of FXCM or any form of personal or investment advice. FXCM neither endorses nor guarantees offerings of third party speakers, nor is FXCM responsible for the content, veracity or opinions of third-party speakers, presenters or participants.

USDJPY H4 | Reversal off pullback resistanceUSD/JPY could rise towards a pullback resistance and potentially reverse off this level to drop lower.

Sell entry is at 149.414 which is a pullback resistance level.

Stop loss is at 150.160 which is a swing-high resistance.

Take profit is at 148.406 which is an overlap support that aligns close to the 38.2% Fibonacci retracement level.

High Risk Investment Warning

Trading Forex/CFDs on margin carries a high level of risk and may not be suitable for all investors. Leverage can work against you.

Forex Capital Markets Limited (www.fxcm.com):

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 70% of retail investor accounts lose money when trading CFDs with this provider. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Stratos Europe Ltd, previously FXCM EU Ltd (www.fxcm.com):

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 74% of retail investor accounts lose money when trading CFDs with this provider. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

FXCM Australia Pty. Limited (www.fxcm.com):

Trading FX/CFDs carries significant risks. FXCM AU (AFSL 309763), please read the Financial Services Guide, Product Disclosure Statement, Target Market Determination and Terms of Business at www.fxcm.com

Stratos Global LLC (www.fxcm.com):

Losses can exceed deposits.

Please be advised that the information presented on TradingView is provided to FXCM (‘Company’, ‘we’) by a third-party provider (‘TFA Global Pte Ltd’). Please be reminded that you are solely responsible for the trading decisions on your account. There is a very high degree of risk involved in trading. Any information and/or content is intended entirely for research, educational and informational purposes only and does not constitute investment or consultation advice or investment strategy. The information is not tailored to the investment needs of any specific person and therefore does not involve a consideration of any of the investment objectives, financial situation or needs of any viewer that may receive it. Kindly also note that past performance is not a reliable indicator of future results. Actual results may differ materially from those anticipated in forward-looking or past performance statements. We assume no liability as to the accuracy or completeness of any of the information and/or content provided herein and the Company cannot be held responsible for any omission, mistake nor for any loss or damage including without limitation to any loss of profit which may arise from reliance on any information supplied by TFA Global Pte Ltd.

The speaker(s) is neither an employee, agent nor representative of FXCM and is therefore acting independently. The opinions given are their own, constitute general market commentary, and do not constitute the opinion or advice of FXCM or any form of personal or investment advice. FXCM neither endorses nor guarantees offerings of third party speakers, nor is FXCM responsible for the content, veracity or opinions of third-party speakers, presenters or participants.

EURJPY: Finally ready to reverse?EURJPY has been hanging around 157 - 157.5 range for some time, we saw a break below last week which quickly recovered, but we've broken back below now so I expect a stronger push back down to the low of last week (caused by JPY buying).

With price action there was also a failure to make a new high, we saw a short pinbar on the 4HR before we broke back below my resistance block.

I see this happening again as the BoJ look to defend their currency, I'm expecting JPY to start to perform well across the board - they may not provide any interest but their inflation is low and their economic performance is looking ok to me to, and also money flows and so a reversal should be coming soon.

I also think the EURO is in trouble, with stagflation, this will lead to recession imo and will hit the EURO so this is one of the JPY crosses I'm expecting big declining moves from.

CHFJPY I Potential Short from Resistance Welcome back! Let me know your thoughts in the comments!

** CHFJPY Analysis - Listen to video!

We recommend that you keep this pair on your watchlist and enter when the entry criteria of your strategy is met.

Please support this idea with a LIKE and COMMENT if you find it useful and Click "Follow" on our profile if you'd like these trade ideas delivered straight to your email in the future.

Thanks for your continued support!

HapHazrd Pairs #2 UsdJpy💹First Ever Silent Commentary! Welcome to the first ever Silent Commentary Analysis for the Pair UsdJpy.

0:0 Intro!

:20 Monthly Analysis

3:45 Weekly analysis

5:09 Daily Analysis

7:11 4hr analysis

We can observe a strong trend and obvious momentum on UJ since the Year began. The Septmeber monthly candle closed bove the Candles to the lefthandside suggesting a breakout and more upside for UJ up to the structural highs at 152.

NZDJPY H4 | Potential bearish reversalNZDJPY is rising towards a pullback resistance and could potentially reverse from here to drop lower towards our take profit target.

Entry: 88.898

Why we like it:

There is a pullback resistance that aligns close to the 61.8% Fibonacci retracement level

Stop Loss: 89.699

Why we like it:

There is a pullback resistance that aligns above the 78.6% Fibonacci retracement level

Take Profit: 87.746

Why we like it:

There is a swing-low support level

Please be advised that the information presented on TradingView is provided to Vantage (‘Vantage Global Limited’, ‘we’) by a third-party provider (‘Everest Fortune Group’). Please be reminded that you are solely responsible for the trading decisions on your account. There is a very high degree of risk involved in trading. Any information and/or content is intended entirely for research, educational and informational purposes only and does not constitute investment or consultation advice or investment strategy. The information is not tailored to the investment needs of any specific person and therefore does not involve a consideration of any of the investment objectives, financial situation or needs of any viewer that may receive it. Kindly also note that past performance is not a reliable indicator of future results. Actual results may differ materially from those anticipated in forward-looking or past performance statements. We assume no liability as to the accuracy or completeness of any of the information and/or content provided herein and the Company cannot be held responsible for any omission, mistake nor for any loss or damage including without limitation to any loss of profit which may arise from reliance on any information supplied by Everest Fortune Group.

CADJPY H4 | Rising into 38.2% Fibo resistanceCADJPY is rising towards a pullback resistance and could potentially reverse off this level to drop lower.

Sell entry is at 108.904 which is a pullback resistance that aligns with the 38.2% Fibonacci retracement level.

Stop loss is at 109.580 which is a level that lies above an overlap resistance and the 50.0% Fibonacci retracement level.

Take profit is at 104.790 which is a swing-low support level.

High Risk Investment Warning

Trading Forex/CFDs on margin carries a high level of risk and may not be suitable for all investors. Leverage can work against you.

Forex Capital Markets Limited (www.fxcm.com):

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 70% of retail investor accounts lose money when trading CFDs with this provider. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Stratos Europe Ltd, previously FXCM EU Ltd (www.fxcm.com):

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 74% of retail investor accounts lose money when trading CFDs with this provider. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

FXCM Australia Pty. Limited (www.fxcm.com):

Trading FX/CFDs carries significant risks. FXCM AU (AFSL 309763), please read the Financial Services Guide, Product Disclosure Statement, Target Market Determination and Terms of Business at www.fxcm.com

Stratos Global LLC (www.fxcm.com):

Losses can exceed deposits.

Please be advised that the information presented on TradingView is provided to FXCM (‘Company’, ‘we’) by a third-party provider (‘TFA Global Pte Ltd’). Please be reminded that you are solely responsible for the trading decisions on your account. There is a very high degree of risk involved in trading. Any information and/or content is intended entirely for research, educational and informational purposes only and does not constitute investment or consultation advice or investment strategy. The information is not tailored to the investment needs of any specific person and therefore does not involve a consideration of any of the investment objectives, financial situation or needs of any viewer that may receive it. Kindly also note that past performance is not a reliable indicator of future results. Actual results may differ materially from those anticipated in forward-looking or past performance statements. We assume no liability as to the accuracy or completeness of any of the information and/or content provided herein and the Company cannot be held responsible for any omission, mistake nor for any loss or damage including without limitation to any loss of profit which may arise from reliance on any information supplied by TFA Global Pte Ltd.

The speaker(s) is neither an employee, agent nor representative of FXCM and is therefore acting independently. The opinions given are their own, constitute general market commentary, and do not constitute the opinion or advice of FXCM or any form of personal or investment advice. FXCM neither endorses nor guarantees offerings of third party speakers, nor is FXCM responsible for the content, veracity or opinions of third-party speakers, presenters or participants.

Is it safe to set sell orders at 150.000 for USD/JPY now? Did the BoJ secretly intervene in USD/JPY on Tuesday? And is there more to come? For now, Bank of Japan officials have avoided explicitly stating whether they had stepped into the market to strengthen the yen. After the USD/JPY crossed 150.000 (its weakest levels in a year), a huge candle appeared on Tuesday touching as low as 147.300 before closing at 149.100.

The Bank of Japan's data apparently showed that it did not intervene (its current account balance was within the estimated range). So, if it wasn’t a BoJ intervention, what was it? A self-fulfilling prophecy? Maybe both? It’s all a bit murky. Even former BOJ official Hideo Kumano said that Tuesday's move showed all the hallmarks of intervention.

Of course, if it was the BoJ, they would be willing to do it again if needed as they have stated many times (although the officials like to phrase it as combating excess volatility rather than combatting a weakening yen). Tuesday intervention could have just been a warning shot to those looking to bet against the yen, with more drastic action from the BoJ locked and loaded.

The BoJ last officially intervened in the currency markets in September and October last year, when the USD/JPY hit a 32-year low of 151.940. At that time, intervention was able to push the pair down to 146.000. Which begs the question; what could be some possible targets this year? Well, the aforementioned wick’s low of 147.300 is an obvious target, with 147.000 just below it. But, like the wider context, targets become a little murkier after these levels. Last year's pivot points at 145.700 and 145.500 might come into play.

Yen Drops Below 150 Per Dollar - Exercise Caution in TradingThe Japanese yen has recently dropped below the critical threshold of 150 per dollar, primarily due to mounting concerns regarding intervention measures. In light of this situation, I strongly urge you to exercise caution and consider pausing yen trading until further clarification is obtained.

The sudden decline in the yen's value has raised concerns among market participants, as it suggests the possibility of intervention by the Japanese government or central bank. Intervention refers to deliberate actions taken by authorities to influence their currency's exchange rate, typically through buying or selling large amounts of their own currency in the foreign exchange market. Such interventions can have a profound impact on the currency's value and create significant volatility in the market.

Given the uncertainty surrounding the current situation, it is prudent to reassess our trading strategies and ensure that we are not unnecessarily exposed to potential risks. Therefore, I strongly recommend that you temporarily halt yen trading until we receive further guidance or clarification from reliable sources regarding any potential intervention measures.

In the meantime, I encourage you to closely monitor the latest news and market developments related to the yen. Stay informed about any official statements or actions from the Japanese government or central bank, as these can provide valuable insights into the future direction of the currency. Additionally, consider diversifying your portfolio to reduce reliance on yen-based assets until the situation stabilizes.

Please remember that our primary objective is to protect our investments and mitigate risk. By exercising caution and temporarily pausing yen trading, we can better position ourselves to navigate the current market uncertainties and make informed decisions when clarity emerges.

If you have any questions or require further guidance, please do not hesitate to reach out to me or our dedicated support team. We are here to assist you and ensure that you have the necessary information to make well-informed trading decisions.

So this happened on the USDJPY overnightThe USDJPY crept over the 150 price level before crashing down almost 300 pips to retest the 22nd September swing low and 61.8% Fibonacci retracement level at the 147.40 price level.

Eventually, the price settled along the 149 price level and back within the bullish channel.

The 150 price level is significant as it was likely the BoJ's price level for an intervention. This move could be viewed as the first stealth intervention as the Ministry of Finance did not confirm the intervention.

Is this going to be a repeat of the series of BoJ interventions we saw in October 2022?

GJ LTF RANGEGJ has been in this intraday range and we have now seen a breakout and retest we can aim for some sell trade

Any correction is a selling opportunityHello traders,

If you are shorting keep it open to the rectangle!

If not! Any correction is a selling opportunity.

Levels calculated order_block, regarding support and resistances, channel and pivot points.

EURJPYEJ has been ranging for a while. Anticipating it to take out buyside then take out sellside liquidity or to the 157.066 before continuation upwards.

USDJPY: My next 2 moves as I expect BoJ to defend their currencyI'm expecting USDJPY to carry on meandering towards the 150 mark, and it's at this level that we've previously seen BoJ step in to defend their currency,

We saw the same in June / July 2022, and I think we'll see it again.

BoJ has started hinting at a change to monetary policy for the first time in a long time, we saw a very small reaction in the past week to this, but right now the dollar is too strong for this to have made a difference.

I'm expecting DXY to retrace from current levels and this cross could be a big beneficiary if BoJ do what I think, it's always good to trade strength against weakness.

There could well be some little long scalp opportunities for me (with very very tight SL's moving to BE asap) on the way up to 150 (within the rising wedge) as that's still some good pips away, but for me the bigger moves now will be to the downside.

I'm not planning on getting caught with any longs up here...

This is a big news week for this pair with FOMC on Wednesday and BoJ interest rate decision and conference Friday, will be interesting to see how this all pans out ahead of these fundamentals, but beyond them I'm expecting things to play out as per this idea.

I've plotted two moves, first from the 150 ish mark down to support, and then another sell down to the rising long term trendline.

Potential Intervention by Bank of Japan - Pause Yen Trading? As you are aware, the USD/JPY currency pair has been experiencing considerable volatility lately, with the exchange rate approaching the critical level of 155. While we strive to maintain a balanced and unbiased approach, it is essential to acknowledge the potential consequences if the USD/JPY falls beyond this threshold.

In such a scenario, it is highly likely that the Bank of Japan (BoJ) may intervene to stabilize the yen's value against the US dollar. Historically, the BoJ has demonstrated a proactive approach to prevent excessive currency fluctuations, especially when they may adversely affect Japan's economy.

Considering this possibility, we strongly recommend that traders take a moment to reassess their current yen trading positions. Pausing yen trading during this uncertain period may prove to be a prudent decision, allowing us to gauge the BoJ's response and the subsequent market sentiment.

We understand that as traders, you possess the expertise to make informed decisions based on your individual strategies and risk appetite. However, we believe it is our responsibility to highlight potential market events that could have a significant impact on your trading activities.

To stay updated on the latest developments regarding the USD/JPY exchange rate and the Bank of Japan's potential intervention, we encourage you to regularly monitor reliable news sources and leverage comprehensive research tools.

In conclusion, we urge you to exercise caution and consider pausing yen trading until further clarity emerges regarding the Bank of Japan's intervention. By adopting a prudent approach, we can safeguard our positions and navigate the market with greater confidence.