Breaking out!The price breaks through the purple resistance and is preparing to start an upward movement.

A compression triangle formation is taking shape, with the lows resting on the underlying purple trendline.

At $203.3, the weekly 100-period simple moving average (SMA100, green line) is located. A close above this level would be an important confirmation of the bullish reversal.

$ZM Long Setup (Probabilistic Bias: Bullish)Chart: 1H | Framework: Smart Money Concepts + Fibonacci + ORB | Date: July 8, 2025

🧠 Technical Insight:

Zoom ( NASDAQ:ZM ) has reclaimed its Equilibrium Zone (around $78) after sweeping liquidity into the Discount Area and tapping a bullish Order Block near $76. A clear CHoCH (Change of Character) signals a potential structural reversal.

🔍 Key Levels:

Support Zone (Discount Area): $75.80–76.50

Equilibrium/POI Zone: $78.00

Target 1 (Fibonacci 0.786): $80.65

Target 2 (Fair Value Gap / 0.886): $82.71

Target 3 (Strong High / Supply): $84.00–85.00

Invalidation: Below $75.30

📊 Volume Spike on July 5-8 confirms active participation near lows—suggesting possible accumulation.

🌐 Macro Context:

Recent Fed comments hint at rate pause or mild easing, boosting tech sentiment.

AI adoption remains a long-term catalyst for enterprise SaaS solutions—beneficial to Zoom’s growth narrative.

Nasdaq leadership rotation may favor ZM’s mean reversion after underperformance.

🔥 Catalyst Watch:

Earnings expected late July—option flow may front-run results.

Monitor implied volatility and ORB breakout ranges (15-min 0930–0945) for intraday confirmation.

📌 Summary (VolanX Signal Score):

Trend Reversal Probability: 67%

Risk-to-Reward: 2.8R

Bias: LONG

Conviction: Moderate to High

📉 Not Financial Advice — For Research Purposes Only

#ZM #SmartMoneyConcepts #WaverVanir #VolanX #OrderBlocks #Equilibrium #TechStocks #Fibonacci #Liquidity #OptionsFlow #MacroUpdate #TradingView #EarningsPlay #ORBStrategy #CHoCH

PLTR temporary top?Bearish case

Monthly RSI at 91

Weekly candles encountering resistance

Daily candles under the 20 day SMA

Bullish case

Monthly candle not a clear bearish candle, no monthly volume spike or no monthly RSI double top like SMCI and no bearish divergence detected yet.

Weekly no continuation down after first 2 red weekly candles

Daily volume spike suggest temp bottom

Conclusion

Let's see the next weekly candle from July 7 to 11.

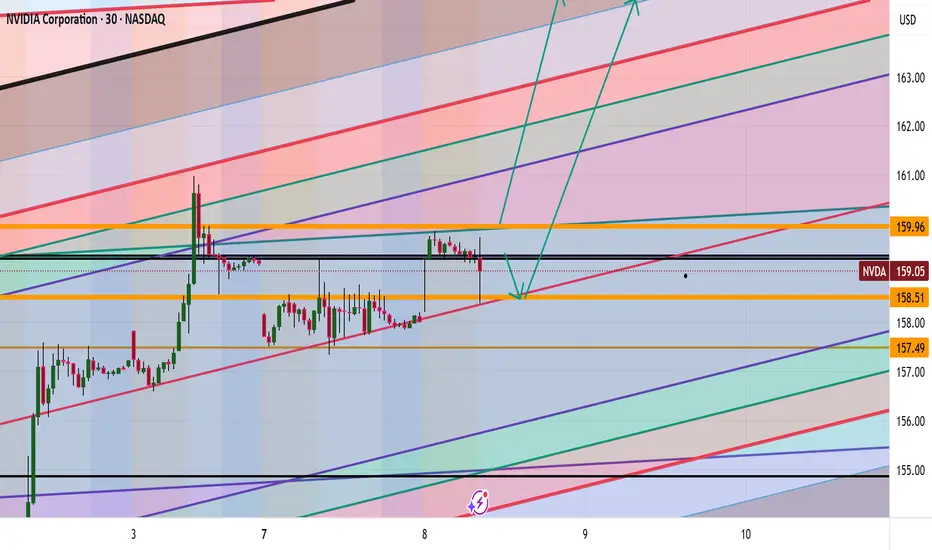

NVDA Analysis To 164?Quick breakdown of NVDA

Appears we hit our corrected level, we could go deeper possibly or hold at this level and drive up to 164

This is looking like a nice little setup long indeed

Trade Smarter Live Better

Kris/Mindbloome Exchange

CSCO Long CallsCisco's uptrend exceeded previous highs and heading toward 127% extension from the 4/9 Tariff lows.

Prices are currently consolidating between $68 and $70 with a volume level.

I am buying in the lower 1/2 - 1/4 of the range with an expectation of a move back to the $70 level and beyond.

August 15 67.5 Calls

E - $68.50

T1 - 69.80

S.L. 30% of option Price

DDOG - Recent entry to S&P500, looking for entry point on $150+I've started looking into #DDOG with its recent addition into the S&P500. The current chart setup looks like a cup and handle. It will be re-testing the 150 and 160 level. If it can break out beyond $155, it has momentum to climb higher with more institutional investors coming in. Note it has been above this level before in 2021 and it was close before in Q4 2024. It has got steady growth in their financials each quarter.

AAPL can we hit 260?

Appears we are making a correction down to the levels of 208 then if that does not hold 205 with a possible drive up to the 260.

Question is are we going drive deeper with the correction ?

Be Careful folks this is a wild one

Trade Smarter Live Better

Kris/Mindbloome Exchange

One to watchI'm waiting for a higher low to form and entry will be on the following bullish candle.

I'll post more about entry and target when the set up forms, which could be 2-3 weeks

Inverse Head and Shoulders Already Completed Toward a New ATHThe price has completed the formation of an inverse head and shoulders pattern, with the final breakout occurring last week.

Volume confirms the validity of the pattern.

The distance from the head to the neckline projects a target toward a new all-time high (ATH).

As often happens after a breakout, a retest of the neckline may occur, which could present a good entry or accumulation opportunity

AEHR watch $15.99-16.27: Major Resistance may give a Dip BuyAEHR has been flying high with the general market.

Approaching a significant resistance into $16 round.

$15.99-16.27 is the exact zone of concern up here.

.

Previous analysis that caught the BreakOut:

===============================================

.

MSFT Correction then to 504?Morning everyone

Currently we are seeing a possible correction to the 495 zone with a possible break to the upside to 504 is what we are currently seeing.

Trade Smarter Live Better

Kris/Mindbloome Exchange

7/7/25 - $eose - Spec punt long ~$5/shr7/7/25 :: VROCKSTAR :: NASDAQ:EOSE

Spec punt long ~$5/shr

- at $5/shr (-ish) you get a company that will be ramping the living daylights out of revenue into 2h

- any battery tech that VST mgmt r referring to "domestic mfg" will benefit the entire sector, esp names like NASDAQ:EOSE w/ ample mfg and revenue already scaling

- obv. if it *is* Eos, well, see u at like *make up a number*

- batteries are the sector i am admittely not as smart on as i'd like to be, esp given my love for NASDAQ:NXT and to a slightly lesser degree NASDAQ:FSLR (and solar as a dominant generation tech in the coming decade)

- so here's to putting some skin in the game to force me to get smart faster than i'd otherwise do from the sidelines

- if you like quantum memes... how about a market cap w/ revenue, real world use case and exploding (actually, not made up) growth already in 2H with a chart that doesn't already look toppy/ or meme-esque

- what resources/ ppl should i follow to get smarter here?

V

PLTR just started the first phase of the Wyckoff distributionBased on the weekly and daily charts provided for Palantir (PLTR), here is a Wyckoff analysis and a corresponding diagonal option spread strategy.

### **Wyckoff Phase Analysis of PLTR**

From the price and volume action on the charts, **PLTR appears to be in the initial stages of a Wyckoff distribution phase (Phase A)**. This phase marks the stopping of the prior uptrend.

* **Weekly Chart:** The long and powerful uptrend is characteristic of a **Markup** phase. However, the recent price action shows a significant change. The peak near $148.22, followed by a sharp decline, can be interpreted as a **Buying Climax (BC)** and an **Automatic Reaction (AR)**. This is a classic sign that large institutions ("smart money") may be starting to sell or distribute their shares.

* **Daily Chart:** The daily chart shows a failure to make new highs, followed by a very sharp sell-off on a spike in volume. This represents a significant **Sign of Weakness (SOW)** and confirms that the character of the market has changed from bullish to potentially bearish or neutral. The uptrend has been broken.

In summary, the strong upward momentum in PLTR has halted, and the stock is showing clear signs of entering a distribution or consolidation phase at these higher prices.

### **Trading PLTR with a Bearish Diagonal Put Spread**

Given the analysis that PLTR is entering a distribution phase, a neutral to bearish outlook is appropriate. A **bearish diagonal put spread** is a suitable strategy to profit from a potential decline in price or even from the stock trading sideways, as it benefits from time decay.

This strategy involves buying a longer-dated, in-the-money (ITM) put option and selling a shorter-dated, out-of-the-money (OTM) put option.

**How to Structure the PLTR Trade (Current Price ~ $130.74):**

1. **Buy a Long-Term Put:**

* **Action:** Buy to open a put option.

* **Expiration:** Choose a later expiration, for example, **4-6 months out**, to give the distribution and potential markdown phase time to develop.

* **Strike Price:** Select an in-the-money (ITM) strike to create a bearish position. A strike price around **$140 or $145** would be appropriate.

2. **Sell a Short-Term Put:**

* **Action:** Sell to open a put option.

* **Expiration:** Select a near-term expiration, typically **30-45 days away**.

* **Strike Price:** Choose an out-of-the-money (OTM) strike below the current price. For instance, selling the **$120 strike** would provide income and define your risk.

**Example Trade (Illustrative Purposes Only):**

* **Buy 1 PLTR put with an expiration 5 months away at a $140 strike.**

* **Sell 1 PLTR put with an expiration in 35 days at a $120 strike.**

The objective is for the short put to lose value from time decay and expire worthless, allowing you to keep the premium. This premium reduces the cost of your long-term bearish put. You can then sell another short-term put for the following month to continue generating income against your long-term bearish position.

> ***Disclaimer:*** *This content is for informational purposes only and should not be construed as financial advice. Options trading involves substantial risk and is not appropriate for all investors. Please conduct your own research and consult with a qualified financial professional before making any investment decisions.*

WMT is ready for another phase of the price discoveryThis Week (July 8 - 12):

Support: The 20-day moving average around $96.70 is the first floor. Below that, the key range support is at $95.00.

Resistance: The top of the range and the all-time high around $101.50 is the ceiling that needs to break.

Next Month (July):

Support: The main support for the entire structure is the $95.00 level. A break below that would be a major warning sign.

Resistance: If we break above $101.50, there is no overhead resistance. We would be in "blue sky territory," with a projected target near $108.

Dakota Gold Corp. (DC) Benefits From Gold RallyDakota Gold Corp. (DC) is a gold exploration and development company focused on revitalizing historic mining districts in South Dakota, particularly the Homestake District. With a strong land position and modern exploration techniques, Dakota Gold aims to unlock high-potential resources in a proven gold-rich region. The company’s growth is driven by rising gold prices, increasing investor interest in U.S.-based mining, and the potential for significant new discoveries.

On the chart, a confirmation bar with increasing volume signals growing momentum. The price has entered the momentum zone after breaking above the .236 Fibonacci level. A trailing stop can be placed just below this level using the Fibonacci snap tool to protect gains while keeping exposure to further upside.

Breakout Triangle // Gann 45° angleRigetti just broke out of the correction triangle. Also the two purple 45! gann angles hint toward an upshift. Pricetarget 1: ~16 USD // Pricetarget 2: ~24 usd // Stoploss just below 12 USD

SNAP is in the Wyckoff Accumulation phaseThis Week (July 8 - 12):

Support: The 20-week moving average around $9.00 is now the immediate floor. Below that, the recent support shelf is at $8.00.

Resistance: The first hurdle is the recent high around $10.40. Above that, the path opens up towards $12.00.

Next Month (July/August):

Support: The absolute low of the Selling Climax at $7.10 is the line in the sand that must hold.

Resistance: A major zone of contention will be around $14.00, which was a significant support/resistance area in the past.

PEP is in the Wyckoff Accumulation phaseThis Week (July 8 - 12):

Support: The recent consolidation shelf around $130.00 is the first line of defense. The absolute low and our line in the sand is the Selling Climax low at $127.60.

Resistance: The 20-week moving average at $138.30 is the immediate ceiling it needs to break through.

Next Month (July/August):

Support: The $127.60 low remains the critical long-term support.

Resistance: If it can clear the $140 level, the next major area of resistance to watch is around $150.00, a previous support zone that will likely attract sellers.

(NFLX) Brake out I would like to see (NFLX) brake this consolidation pattern. Once it does we should see a hard push past the resistance. It both of these happen I will be getting in on the pull back.

Tesla's Self-Inflicted Crisis of ConfidenceInvestors wanted Elon Musk to double down on EVs. Instead, they got a new political party and another reason to sell the stock.

Musk vs Trump: A Fight Investors Didn’t Ask For

Tesla’s latest sell-off has little to do with earnings or electric vehicles. Shares dropped 6.8% on Monday after Elon Musk announced plans to launch a new US political party, escalating his feud with Donald Trump and reigniting investor concerns about distraction at the top.

The fallout from Musk’s political re-entry has been swift. Tesla’s valuation has lost over $200 billion since late May, when Musk’s role in Trump’s short-lived government efficiency task force came to an end. His renewed focus on political activism contradicts April’s pledge to spend “far more” time on Tesla, and comes at a moment when the business is already under pressure from slowing EV sales and collapsing regulatory tailwinds.

Politics, Profits and a Shrinking Mandate

Trump’s so-called “big, beautiful bill” is slashing support for electric vehicles across the board. Gone is the $7,500 federal tax credit, set to expire in September. Gone too are the emissions penalties that allowed Tesla to bank billions in regulatory credits from legacy automakers. William Blair analysts estimate that over $2 billion in high-margin profit is now at risk.

The political clash is getting personal. Trump has mocked Musk’s behaviour as a “train wreck”, suggested deportation, and floated nationalising SpaceX. Investors, meanwhile, are left questioning whether Musk’s growing list of battles is starting to erode Tesla’s long-term advantage. The distraction risk is real, and the market is responding.

Technical Breakdown: Key Levels in Play

Tesla’s share price has woefully underperformed this year. The stock is down 22% year-to-date, while the S&P 500 is up 6%. Recent price action highlights just how vulnerable Tesla has become to the political whims of its CEO. The public fallout with Trump helped define a new swing high in May, which now acts as clear resistance. A new swing low was formed in early June, and that is now the short-term level bulls need to defend.

Adding Keltner Channels to the chart puts the recent volatility into perspective. The sideways bands and price bouncing between them show a market stuck in broad equilibrium. There’s little directional conviction, but that may be changing. Monday’s sell-off pushed Tesla below the volume-weighted average price anchored to the April lows. If the shares remain below this VWAP and break under the June swing lows, it would confirm the attempted recovery has failed and signal that the bears are back in control.

For now, Tesla isn’t trading like a high-growth innovator. It’s trading like a politically charged meme stock with no clear trend and no adult supervision.

Tesla (TSLA) Daily Candle Chart

Past performance is not a reliable indicator of future results

Disclaimer: This is for information and learning purposes only. The information provided does not constitute investment advice nor take into account the individual financial circumstances or objectives of any investor. Any information that may be provided relating to past performance is not a reliable indicator of future results or performance. Social media channels are not relevant for UK residents.

Spread bets and CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 85.24% of retail investor accounts lose money when trading spread bets and CFDs with this provider. You should consider whether you understand how spread bets and CFDs work and whether you can afford to take the high risk of losing your money.

DOW is in the Wyckoff accumulation phaseThis Week (July 8 - 11):

Support: The recent low at $27.10 is the immediate floor. The ultimate support is the Selling Climax low at $25.10.

Resistance: The 20-day moving average (green line) around $28.50 is the first hurdle. Above that, look for a test of $30.00.

Next Month (July):

Support: The $25.10 low absolutely must hold.

Resistance: The primary target is the top of the trading range, established by the Automatic Rally, at $33.00.

Costco is in the Wyckoff distribution phaseThis Week (July 8 - 11):

Support: The immediate floor is at $965. Below that, the low from the initial sell-off around $955 is critical.

Resistance: The 20-day moving average (that green line) at ~$992 is the first ceiling. If it gets frisky, look for sellers to appear at $1,030.

Next Month (July):

Support: If $955 breaks, this whole structure fails. The next major stop would be the April lows around $872. That's the edge of the cliff.

Resistance: The all-time high of $1,067 is the ultimate party zone that the bouncers (sellers) are not letting anyone back into right now.

Apple May Dip to $203 FVG Before Resuming UptrendFenzoFx—AAPL (Apple) is bullish, testing the $210.0 resistance while Stochastic warns of an overbought market.

A dip to the bullish FVG at $203.0 is likely before the uptrend resumes.