Adaptive Market Profile – Auto Detect & Dynamic Activity ZonesAdaptive Market Profile is an advanced indicator that automatically detects and displays the most relevant trend channel and market profile for any asset and timeframe. Unlike standard regression channel tools, this script uses a fully adaptive approach to identify the optimal period, providing you with the channel that best fits the current market dynamics. The calculation is based on maximizing the statistical significance of the trend using Pearson’s R coefficient, ensuring that the most relevant trend is always selected.

Within the selected channel, the indicator generates a dynamic market profile, breaking the price range into configurable zones and displaying the most active areas based on volume or the number of touches. This allows you to instantly identify high-activity price levels and potential support/resistance zones. The “most active lines” are plotted in real-time and always stay parallel to the channel, dynamically adapting to market structure.

Key features:

- Automatic detection of the optimal regression period: The script scans a wide range of lengths and selects the channel that statistically represents the strongest trend.

- Dynamic market profile: Visualizes the distribution of volume or price touches inside the trend channel, with customizable section count.

- Most active zones: Highlights the most traded or touched price levels as dynamic, parallel lines for precise support/resistance reading.

- Manual override: Optionally, users can select their own channel period for full control.

- Supports both linear and logarithmic charts: Simple toggle to match your chart scaling.

Use cases:

- Trend following and channel trading strategies.

- Quick identification of dynamic support/resistance and liquidity zones.

- Objective selection of the most statistically significant trend channel, without manual guesswork.

- Suitable for all assets and timeframes (crypto, stocks, forex, futures).

Originality:

This script goes beyond basic regression channels by integrating dynamic profile analysis and fully adaptive period detection, offering a comprehensive tool for modern technical analysts. The combination of trend detection, market profile, and activity zone mapping is unique and not available in TradingView built-ins.

Instructions:

Add Adaptive Market Profile to your chart. By default, the script automatically detects the optimal channel period and displays the corresponding regression channel with dynamic profile and activity zones. If you prefer manual control, disable “Auto trend channel period” and set your preferred period. Adjust profile settings as needed for your asset and timeframe.

For questions, suggestions, or further customization, contact Julien Eche (@Julien_Eche) directly on TradingView.

Adaptive

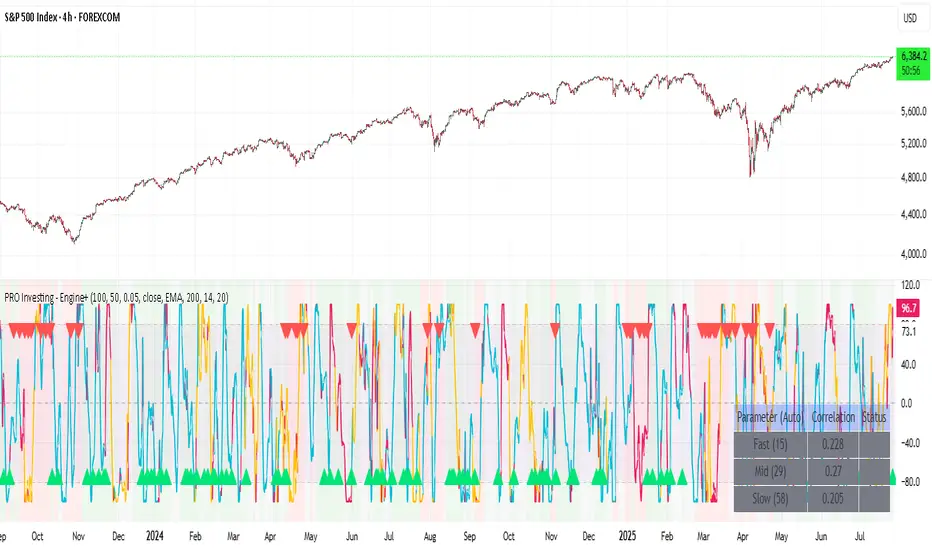

PRO Investing - Apex EnginePRO Investing - Apex Engine

1. Core Concept: Why Does This Indicator Exist?

Traditional momentum oscillators like RSI or Stochastic use a fixed "lookback period" (e.g., 14). This creates a fundamental problem: a 14-period setting that works well in a fast, trending market will generate constant false signals in a slow, choppy market, and vice-versa. The market's character is dynamic, but most tools are static.

The Apex Engine was built to solve this problem. Its primary innovation is a self-optimizing core that continuously adapts to changing market conditions. Instead of relying on one fixed setting, it actively tests three different momentum profiles (Fast, Mid, and Slow) in real-time and selects the one that is most synchronized with the current price action.

This is not just a random combination of indicators; it's a deliberate synthesis designed to create a more robust momentum tool. It combines:

Volatility analysis (ATR) to generate adaptive lookback periods.

Momentum measurement (ROC) to gauge the speed of price changes.

Statistical analysis (Correlation) to validate which momentum measurement is most effective right now.

Classic trend filters (Moving Average, ADX) to ensure signals are only taken in favorable market conditions.

The result is an oscillator that aims to be more responsive in volatile trends and more stable in quiet periods, providing a more intelligent and adaptive signal.

2. How It Works: The Engine's Three-Stage Process

To be transparent, it's important to understand the step-by-step logic the indicator follows on every bar. It's a process of Adapt -> Validate -> Signal.

Stage 1: Adapt (Dynamic Length Calculation)

The engine first measures market volatility using the Average True Range (ATR) relative to its own long-term average. This creates a volatility_factor. In high-volatility environments, this factor causes the base calculation lengths to shorten. In low-volatility, they lengthen. This produces three potential Rate of Change (ROC) lengths: dynamic_fast_len, dynamic_mid_len, and dynamic_slow_len.

Stage 2: Validate (Self-Optimizing Mode Selection)

This is the core of the engine. It calculates the ROC for all three dynamic lengths. To determine which is best, it uses the ta.correlation() function to measure how well each ROC's movement has correlated with the actual bar-to-bar price changes over the "Optimization Lookback" period. The ROC length with the highest correlation score is chosen as the most effective profile for the current moment. This "active" mode is reflected in the oscillator's color and the dashboard.

Stage 3: Signal (Normalized Velocity Oscillator)

The winning ROC series is then normalized into a consistent oscillator (the Velocity line) that ranges from -100 (extreme oversold) to +100 (extreme overbought). This ensures signals are comparable across any asset or timeframe. Signals are only generated when this Velocity line crosses its signal line and the trend filters (explained below) give a green light.

3. How to Use the Indicator: A Practical Guide

Reading the Visuals:

Velocity Line (Blue/Yellow/Pink): The main oscillator line. Its color indicates which mode is active (Fast, Mid, or Slow).

Signal Line (White): A moving average of the Velocity line. Crossovers generate potential signals.

Buy/Sell Triangles (▲ / ▼): These are your primary entry signals. They are intentionally strict and only appear when momentum, trend, and price action align.

Background Color (Green/Red/Gray): This is your trend context.

Green: Bullish trend confirmed (e.g., price above a rising 200 EMA and ADX > 20). Only Buy signals (▲) can appear.

Red: Bearish trend confirmed. Only Sell signals (▼) can appear.

Gray: No clear trend. The market is likely choppy or consolidating. No signals will appear; it is best to stay out.

Trading Strategy Example:

Wait for a colored background. A green or red background indicates the market is in a tradable trend.

Look for a signal. For a green background, wait for a lime Buy triangle (▲) to appear.

Confirm the trade. Before entering, confirm the signal aligns with your own analysis (e.g., support/resistance levels, chart patterns).

Manage the trade. Set a stop-loss according to your risk management rules. An exit can be considered on a fixed target, a trailing stop, or when an opposing signal appears.

4. Settings and Customization

This script is open-source, and its settings are transparent. You are encouraged to understand them.

Synaptic Engine Group:

Volatility Period: The master control for the adaptive engine. Higher values are slower and more stable.

Optimization Lookback: How many bars to use for the correlation check.

Switch Sensitivity: A buffer to prevent frantic switching between modes.

Advanced Configuration & Filters Group:

Price Source: The data source for momentum calculation (default close).

Trend Filter MA Type & Length: Define your long-term trend.

Filter by MA Slope: A key feature. If ON, allows for "buy the dip" entries below a rising MA. If OFF, it's stricter, requiring price to be above the MA.

ADX Length & Threshold: Filters out non-trending, choppy markets. Signals will not fire if the ADX is below this threshold.

5. Important Disclaimer

This indicator is a decision-support tool for discretionary traders, not an automated trading system or financial advice. Past performance is not indicative of future results. All trading involves substantial risk. You should always use proper risk management, including setting stop-losses, and never risk more than you are prepared to lose. The signals generated by this script should be used as one component of a broader trading plan.

RSI Mansfield +RSI Mansfield+ – Adaptive Relative Strength Indicator with Divergences

Overview

RSI Mansfield+ is an advanced relative strength indicator that compares your instrument’s performance against a configurable benchmark index or asset (e.g., Bitcoin Dominance, S&P 500). It combines Mansfield normalization, adaptive smoothing techniques, and automatic detection of bullish and bearish divergences (regular and hidden), delivering a comprehensive tool for assessing relative strength across any market and timeframe.

Originality and Motivation

Unlike traditional relative strength scripts, this indicator introduces several distinctive improvements:

Mansfield Normalization: Scales the ratio between the asset and the benchmark relative to its moving average, transforming it into a normalized oscillator that fluctuates around zero, making it easier to spot outperformance or underperformance.

Adaptive Smoothing: Automatically selects whether to use EMA or SMA based on the market type (crypto or stocks) and timeframe (intraday, daily, weekly, monthly), avoiding manual configuration and providing more robust results under varying volatility conditions.

Divergence Detection: Identifies four types of divergences in the Mansfield oscillator to help anticipate potential reversal points or trend confirmations.

Multi-Market Support: Offers benchmark selection among major crypto and global stock indices from a single input.

These enhancements make RSI Mansfield+ more practical and powerful than conventional relative strength scripts with static benchmarks or without divergence capabilities.

Core Concepts

Relative Strength (RS): Compares price evolution between your asset and the selected benchmark.

Mansfield Normalization: Measures how much the RS deviates from its historical moving average, expressed as a scaled oscillator.

Divergences: Detects regular and hidden bullish or bearish divergences within the Mansfield oscillator.

Timeframe Adaptation: Dynamically adjusts moving average lengths based on timeframe and market type.

How It Works

Benchmark Selection

Choose among over 10 indices or market domains (BTC Dominance, ETH Dominance, S&P 500, European indices, etc.).

Ratio Calculation

Computes the price-to-benchmark ratio and smooths it with the adaptive moving average.

Normalization and Scaling

Transforms deviations into a Mansfield oscillator centered around zero.

Dynamic Coloring

Green indicates relative outperformance, red signals underperformance.

Divergence Detection

Automatically identifies bullish and bearish (regular and hidden) divergences by comparing oscillator pivots against price pivots.

Baseline Reference

A clear zero line helps interpret relative strength trends.

Usage Guidelines

Benchmark Comparison

Ideal for traders analyzing whether an asset is outperforming or lagging its sector or market.

Divergence Analysis

Helps detect potential reversal or continuation signals in relative strength.

Multi-Timeframe Compatibility

Can be applied to intraday, daily, weekly, or monthly charts.

Interpretation

Oscillator >0 and green: outperforming the benchmark.

Oscillator <0 and red: underperforming.

Bullish divergences: potential relative strength reversal to the upside.

Bearish divergences: possible loss of momentum or reversal to the downside.

Credits

The concept of Mansfield Relative Strength is based on Stan Weinstein’s original work on relative performance analysis. This script was built entirely from scratch in TradingView Pine Script v6, incorporating original logic for adaptive smoothing, normalized scaling, and divergence detection, without reusing any external open-source code.

Adaptive Squeeze Momentum +Adaptive Squeeze Momentum+ (Auto-Timeframe Version)

Overview

Adaptive Squeeze Momentum+ is an enhanced volatility and momentum indicator designed to identify compression and expansion phases in price action. It is inspired by the classic Squeeze Momentum Indicator by LazyBear but introduces automatic parameter adaptation to any timeframe, making it simpler to use across different markets without manual configuration.

Concepts and Methodology

The script combines Bollinger Bands (BB) and Keltner Channels (KC) to detect periods when volatility contracts (squeeze) or expands (release).

A squeeze occurs when BB are inside KC, suggesting low volatility and potential breakout scenarios.

A squeeze release is detected when BB expand outside KC.

Momentum is derived using a linear regression applied to the difference between price and a midrange reference level.

Original Improvements

Compared to the original Squeeze Momentum Indicator, this version offers several enhancements:

Automatic Adaptation: BB and KC lengths and multipliers are dynamically adjusted based on the chart’s timeframe (from 1 minute up to 1 month), removing the need for manual tuning.

Simplified Visualization: A clean, minimalist histogram and clear squeeze state cross markers allow for faster interpretation.

Flexible Application: Designed to work consistently on intraday, daily, and higher timeframes across crypto, forex, stocks, and indices.

Features

Dynamic Squeeze Detection:

Gray Cross: Neutral (no squeeze detected)

Blue Cross: Active squeeze

Yellow Cross: Squeeze released

Momentum Histogram:

Positive/negative momentum shown with slope-based coloring.

Timeframe-Aware Parameters:

Automatically sets optimal BB/KC configurations.

Usage

Watch for blue crosses indicating an active squeeze phase that may precede a directional move.

Use the histogram color and slope to gauge momentum strength and direction.

Combine squeeze release signals with momentum confirmation for potential entries or exits.

Credits and Licensing

This script was inspired by LazyBear’s OLD “Squeeze Momentum Indicator” (). The implementation here significantly expands upon the original by introducing auto-adaptive parameters, restructured logic, and a new visualization approach. Published under the Mozilla Public License 2.0.

Disclaimer

This indicator is for educational purposes only and does not constitute financial advice. Use at your own risk.

Active PMI Support/Resistance Levels [EdgeTerminal]The PMI Support & Resistance indicator revolutionizes traditional technical analysis by using Pointwise Mutual Information (PMI) - a statistical measure from information theory - to objectively identify support and resistance levels. Unlike conventional methods that rely on visual pattern recognition, this indicator provides mathematically rigorous, quantifiable evidence of price levels where significant market activity occurs.

- The Mathematical Foundation: Pointwise Mutual Information

Pointwise Mutual Information measures how much more likely two events are to occur together compared to if they were statistically independent. In our context:

Event A: Volume spikes occurring (high trading activity)

Event B: Price being at specific levels

The PMI formula calculates: PMI = log(P(A,B) / (P(A) × P(B)))

Where:

P(A,B) = Probability of volume spikes occurring at specific price levels

P(A) = Probability of volume spikes occurring anywhere

P(B) = Probability of price being at specific levels

High PMI scores indicate that volume spikes and certain price levels co-occur much more frequently than random chance would predict, revealing genuine support and resistance zones.

- Why PMI Outperforms Traditional Methods

Subjective interpretation: What one trader sees as significant, another might ignore

Confirmation bias: Tendency to see patterns that confirm existing beliefs

Inconsistent criteria: No standardized definition of "significant" volume or price action

Static analysis: Doesn't adapt to changing market conditions

No strength measurement: Can't quantify how "strong" a level truly is

PMI Advantages:

✅ Objective & Quantifiable: Mathematical proof of significance, not visual guesswork

✅ Statistical Rigor: Levels backed by information theory and probability

✅ Strength Scoring: PMI scores rank levels by statistical significance

✅ Adaptive: Automatically adjusts to different market volatility regimes

✅ Eliminates Bias: Computer-calculated, removing human interpretation errors

✅ Market Structure Aware: Reveals the underlying order flow concentrations

- How It Works

Data Processing Pipeline:

Volume Analysis: Identifies volume spikes using configurable thresholds

Price Binning: Divides price range into discrete levels for analysis

Co-occurrence Calculation: Measures how often volume spikes happen at each price level

PMI Computation: Calculates statistical significance for each price level

Level Filtering: Shows only levels exceeding minimum PMI thresholds

Dynamic Updates: Refreshes levels periodically while maintaining historical traces

Visual System:

Current Levels: Bright, thick lines with PMI scores - your actionable levels

Historical Traces: Faded previous levels showing market structure evolution

Strength Tiers: Line styles indicate PMI strength (solid/dashed/dotted)

Color Coding: Green for support, red for resistance

Info Table: Real-time display of strongest levels with scores

- Indicator Settings:

Core Parameters

Lookback Period (Default: 200)

Lower (50-100): More responsive to recent price action, catches short-term levels

Higher (300-500): Focuses on major historical levels, more stable but less responsive

Best for: Day trading (100-150), Swing trading (200-300), Position trading (400-500)

Volume Spike Threshold (Default: 1.5)

Lower (1.2-1.4): More sensitive, catches smaller volume increases, more levels detected

Higher (2.0-3.0): Only major volume surges count, fewer but stronger signals

Market dependent: High-volume stocks may need higher thresholds (2.0+), low-volume stocks lower (1.2-1.3)

Price Bins (Default: 50)

Lower (20-30): Broader price zones, less precise but captures wider areas

Higher (70-100): More granular levels, precise but may be overly specific

Volatility dependent: High volatility assets benefit from more bins (70+)

Minimum PMI Score (Default: 0.5)

Lower (0.2-0.4): Shows more levels including weaker ones, comprehensive view

Higher (1.0-2.0): Only statistically strong levels, cleaner chart

Progressive filtering: Start with 0.5, increase if too cluttered

Max Levels to Show (Default: 8)

Fewer (3-5): Clean chart focusing on strongest levels only

More (10-15): Comprehensive view but may clutter chart

Strategy dependent: Scalpers prefer fewer (3-5), swing traders more (8-12)

Historical Tracking Settings

Update Frequency (Default: 20 bars)

Lower (5-10): More frequent updates, captures rapid market changes

Higher (50-100): Less frequent updates, focuses on major structural shifts

Timeframe scaling: 1-minute charts need lower frequency (5-10), daily charts higher (50+)

Show Historical Levels (Default: True)

Enables the "breadcrumb trail" effect showing evolution of support/resistance

Disable for cleaner charts focusing only on current levels

Max Historical Marks (Default: 50)

Lower (20-30): Less memory usage, shorter history

Higher (100-200): Longer historical context but more resource intensive

Fade Strength (Default: 0.8)

Lower (0.5-0.6): Historical levels more visible

Higher (0.9-0.95): Historical levels very subtle

Visual Settings

Support/Resistance Colors: Choose colors that contrast well with your chart theme Line Width: Thicker lines (3-4) for better visibility on busy charts Show PMI Scores: Toggle labels showing statistical strength Label Size: Adjust based on screen resolution and chart zoom level

- Most Effective Usage Strategies

For Day Trading:

Setup: Lookback 100-150, Volume Threshold 1.8-2.2, Update Frequency 10-15

Use PMI levels as bounce/rejection points for scalp entries

Higher PMI scores (>1.5) offer better probability setups

Watch for volume spike confirmations at levels

For Swing Trading:

Setup: Lookback 200-300, Volume Threshold 1.5-2.0, Update Frequency 20-30

Enter on pullbacks to high PMI support levels

Target next resistance level with PMI score >1.0

Hold through minor levels, exit at major PMI levels

For Position Trading:

Setup: Lookback 400-500, Volume Threshold 2.0+, Update Frequency 50+

Focus on PMI scores >2.0 for major structural levels

Use for portfolio entry/exit decisions

Combine with fundamental analysis for timing

- Trading Applications:

Entry Strategies:

PMI Bounce Trades

Price approaches high PMI support level (>1.0)

Wait for volume spike confirmation (orange triangles)

Enter long on bullish price action at the level

Stop loss just below the PMI level

Target: Next PMI resistance level

PMI Breakout Trades

Price consolidates near high PMI level

Volume increases (watch for orange triangles)

Enter on decisive break with volume

Previous resistance becomes new support

Target: Next major PMI level

PMI Rejection Trades

Price approaches PMI resistance with momentum

Watch for rejection signals and volume spikes

Enter short on failure to break through

Stop above the PMI level

Target: Next PMI support level

Risk Management:

Stop Loss Placement

Place stops 0.1-0.5% beyond PMI levels (adjust for volatility)

Higher PMI scores warrant tighter stops

Use ATR-based stops for volatile assets

Position Sizing

Larger positions at PMI levels >2.0 (highest conviction)

Smaller positions at PMI levels 0.5-1.0 (lower conviction)

Scale out at multiple PMI targets

- Key Warning Signs & What to Watch For

Red Flags:

🚨 Very Low PMI Scores (<0.3): Weak statistical significance, avoid trading

🚨 No Volume Confirmation: PMI level without recent volume spikes may be stale

🚨 Overcrowded Levels: Too many levels close together suggests poor parameter tuning

🚨 Outdated Levels: Historical traces are reference only, not tradeable

Optimization Tips:

✅ Regular Recalibration: Adjust parameters monthly based on market regime changes

✅ Volume Context: Always check for recent volume activity at PMI levels

✅ Multiple Timeframes: Confirm PMI levels across different timeframes

✅ Market Conditions: Higher thresholds during high volatility periods

Interpreting PMI Scores

PMI Score Ranges:

0.5-1.0: Moderate statistical significance, proceed with caution

1.0-1.5: Good significance, reliable for most trading strategies

1.5-2.0: Strong significance, high-confidence trade setups

2.0+: Very strong significance, institutional-grade levels

Historical Context: The historical trace system shows how support and resistance evolve over time. When current levels align with multiple historical traces, it indicates persistent market memory at those prices, significantly increasing the level's reliability.

Adaptive Causal Wavelet Trend FilterThe Adaptive Causal Wavelet Trend Filter is a technical indicator implementing causal approximations of wavelet transform properties for better trend detection with adaptive volatility response.

The Adaptive Causal Wavelet Trend Filter (ACWTF) applies mathematical principles derived from wavelet analysis to financial time series, providing robust trend identification with minimal lag. Unlike conventional moving averages, it preserves significant price movements while filtering market noise through signal processing that i describe below.

I was inspired to build this indicator after reading " Wavelet-Based Trend Identification in Financial Time Series " by In, F., & Kim, S. 2013 and reading about Mexican Hat wavelet filters.

The ACWTF maintains optimal performance across varying market regimes without requiring parameter adjustments by adapting filter characteristics to current volatility conditions.

Mathematical Foundation

Inspired by the Mexican Hat wavelet (Ricker wavelet), this indicator implements causal approximations of wavelet filters optimized for real-time financial analysis. The multi-resolution approach identifies features at different scales and the adaptive component dynamically adjusts filtering characteristics based on local volatility measurements.

Key mathematical properties include:

Non-linear frequency response adaptation

Edge-preserving signal extraction

Scale-space analysis through dual filter implementation

Volatility-dependent coefficient adjustment, which I love

Filter Methods

Adaptive: Implements a volatility-weighted combination of multiple filter types to optimize the time-frequency resolution trade-off

Hull: Provides a causal approximation of wavelet edge detection properties with forward-projection characteristics

VWMA: Incorporates volume information into the filtering process for enhanced signal detection

EMA Cascade: Creates a multi-pole filter structure that approximates certain wavelet scaling properties

Suggestion: try all as they will provide slightly different signals. Try also different time-frames.

Practical Applications

Trend Direction Identification: Clear visual trend direction with reduced noise and lag

Regime Change Detection: Early identification of significant trend reversals

Market Condition Analysis: Integrated volatility metrics provide context for current market behavior

Multi-timeframe Confirmation: Alignment between primary and secondary filters offers additional confirmation

Entry/Exit Timing: Filter crossovers and trend changes provide potential trading signals

The comprehensive information panel provides:

Current filter method and trend state

Trend alignment between timeframes

Real-time volatility assessment

Price position relative to filter

Overall trading bias based on multiple factors

Implementation Notes

Log returns option provides improved statistical properties for financial time series

Primary and secondary filter lengths can be adjusted to optimize for specific instruments and timeframes

The indicator performs particularly well during trend transitions and regime changes

The indicator reduces the need for using additional indicators to check trend reversion

Adaptive Quadratic Kernel EnvelopeThis study draws a fair-value curve from a quadratic-weighted (Nadaraya-Watson) regression. Alpha sets how sharply weights decay inside the look-back window, so you trade lag against smoothness with one slider. Band half-width is ATRslow times a bounded fast/slow ATR ratio, giving an instant response to regime shifts without overshooting on spikes. Work in log space when an instrument grows exponentially, equal percentage moves then map to equal vertical steps. NearBase and FarBase define a progression of adaptive thresholds, useful for sizing exits or calibrating mean-reversion logic. Non-repaint mode keeps one-bar delay for clean back-tests, predictive mode shows the zero-lag curve for live decisions.

Key points

- Quadratic weights cut phase error versus Gaussian or SMA-based envelopes.

- Dual-ATR scaling updates width on the next bar, no residual lag.

- Log option preserves envelope symmetry across multi-decade data.

- Alpha provides direct control of curvature versus noise.

- Built-in alerts trigger on the first adaptive threshold, ready for automation.

Typical uses

Trend bias from the slope of the curve.

Entry timing when price pierces an inner threshold and momentum stalls.

Breakout confirmation when closes hold beyond outer thresholds while volatility expands.

Stops and targets anchored to chosen thresholds, automatically matching current noise.

Adaptive MACD Deluxe [AlgoAlpha]OVERVIEW

This script is an advanced rework of the classic MACD indicator, designed to be more adaptive, visually informative, and customizable. It enhances the original MACD formula using a dynamic feedback loop and a correlation-based weighting system that adjusts in real-time based on how deterministic recent price action is. The signal line is flexible, offering several smoothing types including Heiken Ashi, while the histogram is color-coded with gradients to help users visually identify momentum shifts. It also includes optional normalization by volatility, allowing MACD values to be interpreted as relative percentage moves, making the indicator more consistent across different assets and timeframes.

CONCEPTS

This version of MACD introduces a deterministic weight based on R-squared correlation with time, which modulates how fast or slow the MACD adapts to price changes. Higher correlation means smoother, slower MACD responses, and low correlation leads to quicker reaction. The momentum calculation blends traditional EMA math with feedback and damping components to create a smoother, less noisy series. Heiken Ashi is optionally used for signal smoothing to better visualize short-term trend bias. When normalization is enabled, the MACD is scaled by an EMA of the high-low range, converting it into a bounded, volatility-relative indicator. This makes extreme readings more meaningful across markets.

FEATURES

The script offers six distinct options for signal line smoothing: EMA, SMA, SMMA (RMA), WMA, VWMA, and a custom Heiken Ashi mode based on the MACD series. Each option provides a different response speed and smoothing behavior, allowing traders to match the indicator’s behavior to their strategy—whether it's faster reaction or reduced noise.

Normalization is another key feature. When enabled, MACD values are scaled by a volatility proxy, converting the indicator into a relative percentage. This helps standardize the MACD across different assets and timeframes, making overbought and oversold readings more consistent and easier to interpret.

Threshold zones can be customized using upper and lower boundaries, with inner zones for early warnings. These zones are highlighted on the chart with subtle background fills and directional arrows when MACD enters or exits key levels. This makes it easier to spot strong or weak reversals at a glance.

Lastly, the script includes multiple built-in alerts. Users can set alerts for MACD crossovers, histogram flips above or below zero, and MACD entries into strong or weak reversal zones. This allows for hands-free monitoring and quick decision-making without staring at the chart.

USAGE

To use this script, choose your preferred signal smoothing type, enable normalization if you want MACD values relative to volatility, and adjust the threshold zones to fit your asset or timeframe. Use the colored histogram to detect changes in momentum strength—brighter colors indicate rising strength, while faded colors imply weakening. Heiken Ashi mode smooths out noise and provides clearer signals, especially useful in choppy conditions. Use alert conditions for crossover and reversal detection, or monitor the arrow markers for entries into potential exhaustion zones. This setup works well for trend following, momentum trading, and reversal spotting across all market types.

CNN Statistical Trading System [PhenLabs]📌 DESCRIPTION

An advanced pattern recognition system utilizing Convolutional Neural Network (CNN) principles to identify statistically significant market patterns and generate high-probability trading signals.

CNN Statistical Trading System transforms traditional technical analysis by applying machine learning concepts directly to price action. Through six specialized convolution kernels, it detects momentum shifts, reversal patterns, consolidation phases, and breakout setups simultaneously. The system combines these pattern detections using adaptive weighting based on market volatility and trend strength, creating a sophisticated composite score that provides both directional bias and signal confidence on a normalized -1 to +1 scale.

🚀 CONCEPTS

• Built on Convolutional Neural Network pattern recognition methodology adapted for financial markets

• Six specialized kernels detect distinct price patterns: upward/downward momentum, peak/trough formations, consolidation, and breakout setups

• Activation functions create non-linear responses with tanh-like behavior, mimicking neural network layers

• Adaptive weighting system adjusts pattern importance based on current market regime (volatility < 2% and trend strength)

• Multi-confirmation signals require CNN threshold breach (±0.65), RSI boundaries, and volume confirmation above 120% of 20-period average

🔧 FEATURES

Six-Kernel Pattern Detection:

Simultaneous analysis of upward momentum, downward momentum, peak/resistance, trough/support, consolidation, and breakout patterns using mathematically optimized convolution kernels.

Adaptive Neural Architecture:

Dynamic weight adjustment based on market volatility (ATR/Price) and trend strength (EMA differential), ensuring optimal performance across different market conditions.

Professional Visual Themes:

Four sophisticated color palettes (Professional, Ocean, Sunset, Monochrome) with cohesive design language. Default Monochrome theme provides clean, distraction-free analysis.

Confidence Band System:

Upper and lower confidence zones at 150% of threshold values (±0.975) help identify high-probability signal areas and potential exhaustion zones.

Real-Time Information Panel:

Live display of CNN score, market state with emoji indicators, net momentum, confidence percentage, and RSI confirmation with dynamic color coding based on signal strength.

Individual Feature Analysis:

Optional display of all six kernel outputs with distinct visual styles (step lines, circles, crosses, area fills) for advanced pattern component analysis.

User Guide

• Monitor CNN Score crossing above +0.65 for long signals or below -0.65 for short signals with volume confirmation

• Use confidence bands to identify optimal entry zones - signals within confidence bands carry higher probability

• Background intensity reflects signal strength - darker backgrounds indicate stronger conviction

• Enter long positions when blue circles appear above oscillator with RSI < 75 and volume > 120% average

• Enter short positions when dark circles appear below oscillator with RSI > 25 and volume confirmation

• Information panel provides real-time confidence percentage and momentum direction for position sizing decisions

• Individual feature plots allow granular analysis of specific pattern components for strategy refinement

💡Conclusion

CNN Statistical Trading System represents the evolution of technical analysis, combining institutional-grade pattern recognition with retail accessibility. The six-kernel architecture provides comprehensive market pattern coverage while adaptive weighting ensures relevance across all market conditions. Whether you’re seeking systematic entry signals or advanced pattern confirmation, this indicator delivers mathematically rigorous analysis with intuitive visual presentation.

SuperTrend: Silent Shadow 🕶️ SuperTrend: Silent Shadow — Operate in trend. Vanish in noise.

Overview

SuperTrend: Silent Shadow is an enhanced trend-following system designed for traders who demand clarity in volatile markets and silence during indecision.

It combines classic Supertrend logic with a proprietary ShadowTrail engine and an adaptive Silence Protocol to filter noise and highlight only the cleanest signals.

Key Features

✅ Core Supertrend Logic

Built on Average True Range (ATR), this trend engine identifies directional bias with visual clarity. Lines adjust dynamically with price action and flip when meaningful reversals occur.

✅ ShadowTrail: Stepped Counter-Barrier

ShadowTrail doesn’t predict reversals — it reinforces structure.

When price is trending, ShadowTrail forms a stepped ceiling in downtrends and a stepped floor in uptrends. This visual containment zone helps define the edges of price behavior and offers a clear visual anchor for stop-loss placement and trade containment.

✅ Silence Protocol: Adaptive Noise Filtering

During low-volatility zones, the system enters “stealth mode”:

• Trend lines turn white to indicate reduced signal quality

• Fill disappears to reduce distraction

This helps avoid choppy entries and keeps your focus sharp when the market isn’t.

✅ Visual Support & Stop-Loss Utility

When trendlines flatten or pause, they naturally highlight price memory zones. These flat sections often align with:

• Logical stop-loss levels

• Prior support/resistance areas

• Zones of reduced volatility where price recharges or rejects

✅ Custom Styling

Full control over line colors, width, transparency, fill visibility, and silence behavior. Tailor it to your strategy and visual preferences.

How to Use

• Use Supertrend color to determine bias — flips mark momentum shifts

• ShadowTrail mirrors the primary trend as a structural ceiling/floor

• Use flat segments of both lines to identify consolidation zones or place stops

• White lines = low-quality signal → stand by

• Combine with RSI, volume, divergence, or your favorite tools for confirmation

Recommended For:

• Traders seeking clearer trend signals

• Avoiding false entries in sideways or silent markets

• Identifying key support/resistance visually

• Structuring stops around real market containment levels

• Scalping, swing, or position trading with adaptive clarity

Built by Sherlock Macgyver

Forged for precision. Designed for silence.

When the market speaks, you listen.

When it doesn’t — you wait in the shadows.

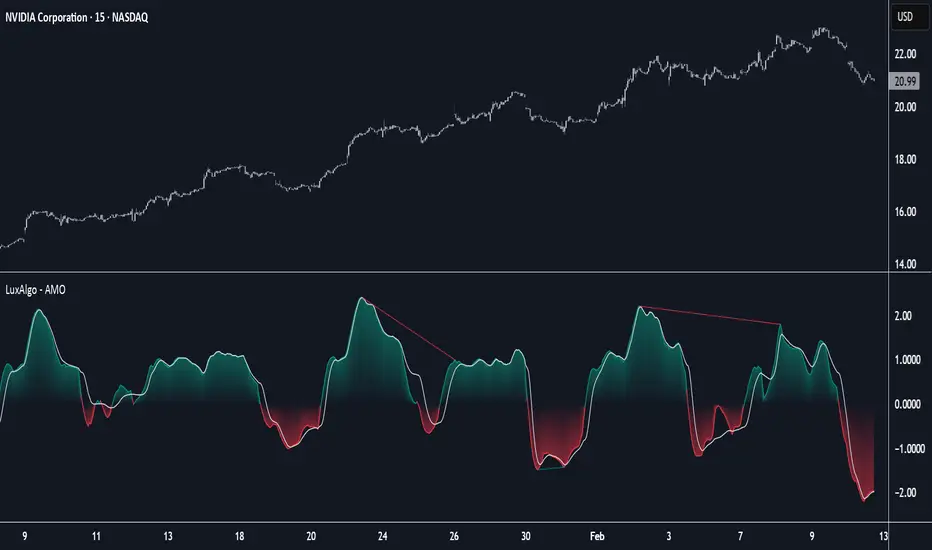

Adaptive Momentum Oscillator [LuxAlgo]The Adaptive Momentum Oscillator tool allows traders to measure the current relative momentum over a given period using the maximum delta in price.

It features a histogram with gradient color, divergences, and an adaptive moving average that allows traders to clearly see the smoothed trend direction.

🔶 USAGE

This unbounded oscillator has positive momentum when values are above 0 and negative momentum when values are below 0. The adaptive moving average is used as a minimum lag smoothing tool over the momentum histogram.

🔹 Signal Line

There are two main uses for the signal line drawn on the chart above.

Momentum crosses above or below the signal line: acceleration in momentum.

Signal line crosses the 0 value: positive or negative momentum.

🔹 Data Length

On the chart above, we can compare different length sizes and how the tool values change, allowing traders to get a shorter or longer-term view of current market strength.

🔹 Smoothing Length

In the previous figure, we can compare how different Smoothing Length values affect the oscillator output.

🔹 Divergences

The divergence detector is disabled by default. Traders can enable it and adjust the divergence length from the settings panel.

As we can see in the chart above, by changing the length of the divergences, traders can fine-tune their detection, a small number will detect smaller divergences, and use a larger number for larger divergences.

🔶 SETTINGS

Data: Select data source, close price by default

Data Length: Select the length for data gathering

Smoothing Length: Select the length for data smoothing

Divergences: Enable/Disable divergences detection and length

Machine Learning | Adaptive Trend Signals [Bitwardex]⚙️🧠Machine Learning | Adaptive Trend Signals

🔷Overview

Machine Learning | Adaptive Trend Signals is a Pine Script™ v6 indicator designed to visualize market trends and generate signals through a combination of volatility clustering, Gaussian smoothing, and adaptive trend calculations. Built as an overlay indicator, it integrates advanced techniques inspired by machine learning concepts, such as K-Means clustering, to adapt to changing market conditions. The script is highly customizable, includes a backtesting module, and supports alert conditions, making it suitable for traders exploring trend-based strategies and developers studying volatility-driven indicator design.

🔷Functionality

The indicator performs the following core functions:

• Volatility Clustering: Uses K-Means clustering to categorize market volatility into high, medium, and low states, adjusting trend sensitivity accordingly.

• Trend Calculation: Computes adaptive trend lines (SmartTrend) based on volatility-adjusted standard deviation, smoothed RSI, and ADX filters.

• Signal Generation: Identifies potential buy and sell points through trend line crossovers and directional confirmation.

• Backtesting Module: Tracks trade outcomes based on the SmartTrend3 value, displaying win rate and total trades.

• Visualization: Plots trend lines with gradient colors and optional signal markers (bullish 🐮 and bearish 🐻).

• Alerts: Provides configurable alerts for trend shifts and volatility state changes.

🔷Technical Methodology

Volatility Clustering with K-Means

The indicator employs a K-Means clustering algorithm to classify market volatility, measured via the Average True Range (ATR), into three distinct clusters:

• Data Collection: Gathers ATR values over a user-defined training period (default: 100 bars).

• Centroid Initialization: Sets initial centroids at the highest, lowest, and midpoint ATR values within the training period.

• Iterative Clustering: Assigns ATR data points to the nearest centroid, recalculates centroid means, and repeats until convergence.

• Dynamic Adjustment: Assigns a volatility state (high, medium, or low) based on the closest centroid, adjusting the trend factor (e.g., tighter for high volatility, wider for low volatility).

This approach allows the indicator to adapt its sensitivity to varying market conditions, providing a data-driven foundation for trend calculations.

🔷Gaussian Smoothing

To enhance signal clarity and reduce noise, the indicator applies Gaussian kernel smoothing to:

• RSI: Smooths the Relative Strength Index (calculated from OHLC4) to filter short-term fluctuations.

• SmartTrend: Smooths the primary trend line for a more stable output.

The Gaussian kernel uses a sigma value derived from the user-defined smoothing length, ensuring mathematically consistent noise reduction.

🔷SmartTrend Calculation

The pineSmartTrend function is the core of the indicator, producing three trend lines:

• SmartTrend: The primary trend line, calculated using a volatility-adjusted standard deviation, smoothed RSI, and ADX conditions.

• SmartTrend2: A secondary trend line with a wider factor (base factor * 1.382) for signal confirmation.

SmartTrend3: The average of SmartTrend and SmartTrend2, used for plotting and backtesting.

Key components of the calculation include:

• Dynamic Standard Deviation: Scales based on ATR relative to its 50-period smoothed average, with multipliers (1.0 to 1.4) applied according to volatility thresholds.

• RSI and ADX Filters: Requires RSI > 50 for bullish trends or < 50 for bearish trends, alongside ADX > 15 and rising to confirm trend strength.

Volatility-Adjusted Bands: Constructs upper and lower bands around price action, adjusted by the volatility cluster’s dynamic factor.

🔷Signal Generation

The generate_signals function generates signals as follows:

• Buy Signal: Triggered when SmartTrend crosses above SmartTrend2 and the price is above SmartTrend, with directional confirmation.

• Sell Signal: Triggered when SmartTrend crosses below SmartTrend2 and the price is below SmartTrend, with directional confirmation.

Directional Logic: Tracks trend direction to filter out conflicting signals, ensuring alignment with the broader market context.

Signals are visualized as small circles with bullish (🐮) or bearish (🐻) emojis, with an option to toggle visibility.

🔷Backtesting

The get_backtest function evaluates signal outcomes using the SmartTrend3 value (rather than closing prices) to align with the trend-based methodology.

It tracks:

• Total Trades: Counts completed long and short trades.

• Win Rate: Calculates the percentage of trades where SmartTrend3 moves favorably (higher for longs, lower for shorts).

Position Management: Closes opposite positions before opening new ones, simulating a single-position trading system.

Results are displayed in a table at the top-right of the chart, showing win rate and total trades. Note that backtest results reflect the indicator’s internal logic and should not be interpreted as predictive of real-world performance.

🔷Visualization and Alerts

• Trend Lines: SmartTrend3 is plotted with gradient colors reflecting trend direction and volatility cluster, accompanied by a secondary line for visual clarity.

• Signal Markers: Optional buy/sell signals are plotted as small circles with customizable colors.

• Alerts: Supports alerts for:

• Bullish and bearish trend shifts (confirmed on bar close).

Transitions to high, medium, or low volatility states.

🔷Input Parameters

• ATR Length (default: 14): Period for ATR calculation, used in volatility clustering.

• Period (default: 21): Common period for RSI, ADX, and standard deviation calculations.

• Base SmartTrend Factor (default: 2.0): Base multiplier for volatility-adjusted bands.

• SmartTrend Smoothing Length (default: 10): Length for Gaussian smoothing of the trend line.

• Show Buy/Sell Signals? (default: true): Enables/disables signal markers.

• Bullish/Bearish Color: Customizable colors for trend lines and signals.

🔷Usage Instructions

• Apply to Chart: Add the indicator to any TradingView chart.

• Configure Inputs: Adjust parameters to align with your trading style or market conditions (e.g., shorter ATR length for faster markets).

• Interpret Output:

• Trend Lines: Use SmartTrend3’s direction and color to gauge market bias.

• Signals: Monitor bullish (🐮) and bearish (🐻) markers for potential entry/exit points.

• Backtest Table: Review win rate and total trades to understand the indicator’s behavior in historical data.

• Set Alerts: Configure alerts for trend shifts or volatility changes to support manual or automated trading workflows.

• Combine with Analysis: Use the indicator alongside other tools or market context, as it is designed to complement, not replace, comprehensive analysis.

🔷Technical Notes

• Data Requirements: Requires at least 100 bars for accurate volatility clustering. Ensure sufficient historical data is loaded.

• Market Suitability: The indicator is designed for trend detection and may perform differently in ranging or volatile markets due to its reliance on RSI and ADX filters.

• Backtesting Scope: The backtest module uses SmartTrend3 values, which may differ from price-based outcomes. Results are for informational purposes only.

• Computational Intensity: The K-Means clustering and Gaussian smoothing may increase processing time on lower timeframes or with large datasets.

🔷For Developers

The script is modular, well-commented, encouraging reuse and modification with proper attribution.

Key functions include:

• gaussianSmooth: Applies Gaussian kernel smoothing to any data series.

• pineSmartTrend: Computes adaptive trend lines with volatility and momentum filters.

• getDynamicFactor: Adjusts trend sensitivity based on volatility clusters.

• get_backtest: Evaluates signal performance using SmartTrend3.

Developers can extend these functions for custom indicators or strategies, leveraging the volatility clustering and smoothing methodologies. The K-Means implementation is particularly useful for adaptive volatility analysis.

🔷Limitations

• The indicator is not predictive and should be used as part of a broader trading strategy.

• Performance varies by market, timeframe, and parameter settings, requiring user experimentation.

• Backtest results are based on historical data and internal logic, not real-world trading conditions.

• Volatility clustering assumes sufficient historical data; incomplete data may affect accuracy.

🔷Acknowledgments

Developed by Bitwardex, inspired by machine learning concepts and adaptive trading methodologies. Community feedback is welcome via TradingView’s platform.

🔷 Risk Disclaimer

Trading involves significant risks, and most traders may incur losses. Bitwardex AI Algo is provided for informational and educational purposes only and does not constitute financial advice or a recommendation to buy or sell any financial instrument . The signals, metrics, and features are tools for analysis and do not guarantee profits or specific outcomes. Past performance is not indicative of future results. Always conduct your own due diligence and consult a financial advisor before making trading decisions.

Adaptable Relative Momentum Index [ParadoxAlgo]The Adaptable Relative Momentum Index (RMI) by ParadoxAlgo is an advanced momentum-based indicator that builds upon the well-known RSI (Relative Strength Index) concept by introducing a customizable momentum length. This indicator measures price momentum over a specified number of periods and applies a Rolling Moving Average (RMA) to both the positive and negative price changes. The result is a versatile tool that can help traders gauge the strength of a trend, pinpoint overbought/oversold levels, and potentially identify breakout opportunities.

⸻

Smart Configuration Feature

What sets this version of the RMI apart is ParadoxAlgo’s exclusive “Smart Configuration” functionality. Instead of manually adjusting parameters, traders can simply select their Asset Class (e.g., Stocks, Forex, Futures/Indices, Crypto, Commodities) and Trading Style (e.g., Scalping, Day Trading, Swing Trading, Short-Term Investing, Long-Term Investing). Based on these selections, the indicator automatically optimizes its core parameters:

• Length – The period over which the price changes are smoothed.

• Momentum Length – The number of bars used to calculate the price change.

By automating this process, users save time on tedious trial-and-error adjustments, ensuring that the RMI’s settings are tailored to the characteristics of specific markets and personal trading horizons.

⸻

Key Features & Benefits

1. Momentum-Based Insights

• Uses RMA to smooth price movements, helping identify shifts in market momentum more clearly than a basic RSI.

• Enhanced adaptability for a wide range of asset classes and time horizons.

2. Simple Yet Powerful Configuration

• Smart Configuration automatically sets optimal parameter values for each combination of asset class and trading style.

• Eliminates guesswork and manual recalibration when switching between markets or timeframes.

3. Overbought & Oversold Visualization

• Integrated highlight zones mark potential overbought and oversold extremes (default at 80 and 20).

• Optional breakout highlighting draws attention to times when the indicator crosses these key thresholds, helping spot possible entry or exit signals.

4. Intuitive Design & Ease of Use

• Clean plotting and color-coded signal lines make it easy to interpret bullish or bearish shifts in momentum.

• Straightforward dropdown menus keep the interface user-friendly, even for novice traders.

⸻

Practical Applications

• Early Trend Detection: Spot emerging trends when the RMI transitions from oversold to higher levels or vice versa.

• Breakout Confirmation: Confirm potential breakout trades by tracking overbought/oversold breakouts alongside other technical signals.

• Support/Resistance Confluence: Combine RMI signals with horizontal support/resistance levels to reinforce trade decisions.

• Trade Timing: Quickly gauge when momentum could be shifting, helping you time entries and exits more effectively.

⸻

Disclaimer

As with any technical indicator, the Adaptable Relative Momentum Index should be used as part of a broader trading strategy that includes risk management, fundamental analysis, and other forms of technical confirmation. Past performance does not guarantee future results.

⸻

Enjoy using the Adaptable RMI and experience a more streamlined, flexible approach to momentum analysis. Feel free to explore different asset classes and trading styles to discover which configurations resonate best with your unique trading preferences.

Ehlers Adaptive Trend Indicator [Alpha Extract]Ehlers Adaptive Trend Indicator

The Ehlers Adaptive Trend Indicator combines Ehlers' advanced digital signal processing techniques with dynamic volatility bands to identify robust trend conditions and potential reversals. This powerful tool helps traders visualize trend strength, adaptive support/resistance levels, and momentum shifts across various market conditions.

🔶 CALCULATION

The indicator employs a sophisticated adaptive algorithm that responds to changing market conditions:

• Ehlers Filter : Calculates a weighted average based on momentum differences to create an adaptive trend baseline.

• Dynamic Bands : Volatility-adjusted bands that expand and contract based on recent price action.

• Trend Level : A dynamic support/resistance level that adapts to the current trend direction.

• Smoothed Volatility : Market volatility measured and smoothed to provide reliable band width.

Formula:

• Ehlers Basis = Weighted average of price, with weights determined by momentum differences

• Volatility = Standard deviation of price over Ehlers Length period

• Smoothed Volatility = EMA of volatility over Smoothing Length

• Upper Band = Ehlers Basis + Smoothed Volatility × Sensitivity

• Lower Band = Ehlers Basis - Smoothed Volatility × Sensitivity

• Trend Level = Adaptive support in uptrends, resistance in downtrends

🔶 DETAILS

Visual Features :

• Ehlers Basis Line (Yellow): The core adaptive trend reference that serves as the primary trend indicator.

• Trend Level Line (Dynamic Color): Changes between green (bullish) and red (bearish) based on the current trend state.

• Fill Areas : Transparent green fill during bullish trends and transparent red fill during bearish trends for clear visual identification.

• Bar Coloring : Optional price bar coloring that reflects the current trend direction for enhanced visualization.

Interpretation :

• **Bullish Signal**: Price crosses above the upper band, triggering a trend change with the Trend Level becoming dynamic support.

• **Bearish Signal**: Price drops below the lower band, confirming a trend change with the Trend Level becoming dynamic resistance.

• **Trend Continuation**: Trend Level rises in bullish markets and falls in bearish markets, providing adaptive trailing support/resistance.

🔶 EXAMPLES

The chart demonstrates:

• Bullish Trend Identification : When price breaks above the upper band, the indicator shifts to bullish mode with green trend level and fill.

• Bearish Trend Identification : When price falls below the lower band, the indicator shifts to bearish mode with red trend level and fill.

• Trend Persistence : Trend Level adapts to market movement, rising during uptrends to provide dynamic support and falling during downtrends to act as resistance.

Example Snapshots :

• During a strong uptrend, the Trend Level continuously adjusts upward, keeping traders in the trend while filtering out minor retracements.

• During trend reversals, clear color changes and Trend Level shifts provide early warning of potential direction changes.

🔶 SETTINGS

Customization Options :

• Ehlers Length (p1) (Default: 30): Controls the primary adaptive calculation period, balancing responsiveness with stability.

• Momentum Length (p2) (Default: 25): Determines the lag for momentum calculations used in the adaptive weighting.

• Smoothing Length (Default: 10): Adjusts the volatility smoothing period—higher values provide more stable bands.

• Sensitivity (Default: 1.0): Multiplier for band width—higher values increase distance between bands, lower values tighten them.

• Visual Settings : Customizable colors for bullish and bearish trends, basis line, and optional bar coloring.

The Ehlers Adaptive Trend Indicator combines John Ehlers' digital signal processing expertise with modern volatility analysis to create a robust trend-following system that adapts to changing market conditions, helping traders stay on the right side of the market.

Ehlers Adaptive RSIThe Ehlers Adaptive RSI improves on the traditional RSI by dynamically adjusting its period based on market conditions.

Problem with the Classic RSI:

The traditional Relative Strength Index (RSI) uses a fixed period (e.g., 14), making it slow to react in volatile markets and too sensitive in stable conditions.

How the Adaptive RSI Solves This:

Instead of a fixed period, this version automatically adapts based on market volatility using a combination of ATR (Average True Range) and EMA (Exponential Moving Average).

Key Benefits:

More Responsive – Quickly adapts to market shifts, reducing lag.

Less Noise – Filters out unnecessary fluctuations in stable trends.

Self-Adjusting – No need to manually change RSI settings for different market conditions.

Better Signal Accuracy – Helps detect real trend reversals without false alarms.

This script is for informational and educational purposes only. It does not constitute financial advice, and past performance does not guarantee future results. Use it at your own risk.

Hull Moving Average Adaptive RSI (Ehlers)Hull Moving Average Adaptive RSI (Ehlers)

The Hull Moving Average Adaptive RSI (Ehlers) is an enhanced trend-following indicator designed to provide a smooth and responsive view of price movement while incorporating an additional momentum-based analysis using the Adaptive RSI.

Principle and Advantages of the Hull Moving Average:

- The Hull Moving Average (HMA) is known for its ability to track price action with minimal lag while maintaining a smooth curve.

- Unlike traditional moving averages, the HMA significantly reduces noise and responds faster to market trends, making it highly effective for detecting trend direction and changes.

- It achieves this by applying a weighted moving average calculation that emphasizes recent price movements while smoothing out fluctuations.

Why the Adaptive RSI Was Added:

- The core HMA line remains the foundation of the indicator, but an additional analysis using the Adaptive RSI has been integrated to provide more meaningful insights into momentum shifts.

- The Adaptive RSI is a modified version of the traditional Relative Strength Index that dynamically adjusts its sensitivity based on market volatility.

- By incorporating the Adaptive RSI, the HMA visually represents whether momentum is strengthening or weakening, offering a complementary layer of analysis.

How the Adaptive RSI Influences the Indicator:

- High Adaptive RSI (above 65): The market may be overbought, or bullish momentum could be fading. The HMA turns shades of red, signaling a possible exhaustion phase or potential reversals.

- Neutral Adaptive RSI (around 50): The market is in a balanced state, meaning neither buyers nor sellers are in clear control. The HMA takes on grayish tones to indicate this consolidation.

- Low Adaptive RSI (below 35): The market may be oversold, or bearish momentum could be weakening. The HMA shifts to shades of blue, highlighting potential recovery zones or trend slowdowns.

Why This Combination is Powerful:

- While the HMA excels in tracking trends and reducing lag, it does not provide information about momentum strength on its own.

- The Adaptive RSI bridges this gap by adding a clear visual layer that helps traders assess whether a trend is likely to continue, consolidate, or reverse.

- This makes the indicator particularly useful for spotting trend exhaustion and confirming momentum shifts in real-time.

Best Use Cases:

- Works effectively on timeframes from 1 hour (1H) to 1 day (1D), making it suitable for swing trading and position trading.

- Particularly useful for trading indices (SPY), stocks, forex, and cryptocurrencies, where momentum shifts are frequent.

- Helps identify not just trend direction but also whether that trend is gaining or losing strength.

Recommended Complementary Indicators:

- Adaptive Trend Finder: Helps identify the dominant long-term trend.

- Williams Fractals Ultimate: Provides key reversal points to validate trend shifts.

- RVOL (Relative Volume): Confirms significant moves based on volume strength.

This enhanced HMA with Adaptive RSI provides a powerful, intuitive visual tool that makes trend analysis and momentum interpretation more effective and efficient.

This indicator is for educational and informational purposes only. It should not be considered financial advice or a guarantee of performance. Always conduct your own research and use proper risk management when trading. Past performance does not guarantee future results.

Adaptive Trend FinderAdaptive Trend Finder - The Ultimate Trend Detection Tool

Introducing Adaptive Trend Finder, the next evolution of trend analysis on TradingView. This powerful indicator is an enhanced and refined version of Adaptive Trend Finder (Log), designed to offer even greater flexibility, accuracy, and ease of use.

What’s New?

Unlike the previous version, Adaptive Trend Finder allows users to fully configure and adjust settings directly within the indicator menu, eliminating the need to modify chart settings manually. A major improvement is that users no longer need to adjust the chart's logarithmic scale manually in the chart settings; this can now be done directly within the indicator options, ensuring a smoother and more efficient experience. This makes it easier to switch between linear and logarithmic scaling without disrupting the analysis. This provides a seamless user experience where traders can instantly adapt the indicator to their needs without extra steps.

One of the most significant improvements is the complete code overhaul, which now enables simultaneous visualization of both long-term and short-term trend channels without needing to add the indicator twice. This not only improves workflow efficiency but also enhances chart readability by allowing traders to monitor multiple trend perspectives at once.

The interface has been entirely redesigned for a more intuitive user experience. Menus are now clearer, better structured, and offer more customization options, making it easier than ever to fine-tune the indicator to fit any trading strategy.

Key Features & Benefits

Automatic Trend Period Selection: The indicator dynamically identifies and applies the strongest trend period, ensuring optimal trend detection with no manual adjustments required. By analyzing historical price correlations, it selects the most statistically relevant trend duration automatically.

Dual Channel Display: Traders can view both long-term and short-term trend channels simultaneously, offering a broader perspective of market movements. This feature eliminates the need to apply the indicator twice, reducing screen clutter and improving efficiency.

Fully Adjustable Settings: Users can customize trend detection parameters directly within the indicator settings. No more switching chart settings – everything is accessible in one place.

Trend Strength & Confidence Metrics: The indicator calculates and displays a confidence score for each detected trend using Pearson correlation values. This helps traders gauge the reliability of a given trend before making decisions.

Midline & Channel Transparency Options: Users can fine-tune the visibility of trend channels, adjusting transparency levels to fit their personal charting style without overwhelming the price chart.

Annualized Return Calculation: For daily and weekly timeframes, the indicator provides an estimate of the trend’s performance over a year, helping traders evaluate potential long-term profitability.

Logarithmic Adjustment Support: Adaptive Trend Finder is compatible with both logarithmic and linear charts. Traders who analyze assets like cryptocurrencies, where log scaling is common, can enable this feature to refine trend calculations.

Intuitive & User-Friendly Interface: The updated menu structure is designed for ease of use, allowing quick and efficient modifications to settings, reducing the learning curve for new users.

Why is this the Best Trend Indicator?

Adaptive Trend Finder stands out as one of the most advanced trend analysis tools available on TradingView. Unlike conventional trend indicators, which rely on fixed parameters or lagging signals, Adaptive Trend Finder dynamically adjusts its settings based on real-time market conditions. By combining automatic trend detection, dual-channel visualization, real-time performance metrics, and an intuitive user interface, this indicator offers an unparalleled edge in trend identification and trading decision-making.

Traders no longer have to rely on guesswork or manually tweak settings to identify trends. Adaptive Trend Finder does the heavy lifting, ensuring that users are always working with the strongest and most reliable trends. The ability to simultaneously display both short-term and long-term trends allows for a more comprehensive market overview, making it ideal for scalpers, swing traders, and long-term investors alike.

With its state-of-the-art algorithms, fully customizable interface, and professional-grade accuracy, Adaptive Trend Finder is undoubtedly one of the most powerful trend indicators available.

Try it today and experience the future of trend analysis.

This indicator is a technical analysis tool designed to assist traders in identifying trends. It does not guarantee future performance or profitability. Users should conduct their own research and apply proper risk management before making trading decisions.

// Created by Julien Eche - @Julien_Eche

Supertrend with RSI FilterThis indicator is an enhanced version of the classic Supertrend, incorporating an RSI (Relative Strength Index) filter to refine trend signals. Here is a detailed explanation of its functionality and key advantages over the traditional Supertrend.

1. Indicator Functionality

The indicator uses ATR (Average True Range) to calculate the Supertrend line, just like the classic version. However, it introduces an additional condition based on RSI to strengthen or weaken the Supertrend color based on market momentum.

2. Interpretation of Colors

The indicator displays the Supertrend line with dynamic colors based on trend direction and RSI strength:

- Uptrend (Supertrend in buy mode):

- Dark green (Teal): RSI above the defined threshold (default 50) → Strong bullish confirmation.

- Light gray: RSI below the threshold → Indicates a weaker uptrend or lack of confirmation.

- Downtrend (Supertrend in sell mode):

- Dark red: RSI below the threshold → Strong bearish confirmation.

- Light gray: RSI above the threshold → Indicates a weaker downtrend or lack of confirmation.

The opacity of the color dynamically adjusts based on how far RSI is from its threshold. The greater the difference, the more vivid the color, signaling a stronger trend.

3. Key Advantages Over the Classic Supertrend

- Filters out false signals: The RSI integration helps reduce false signals by only validating trends when RSI aligns with the Supertrend direction.

- Weakens uncertain signals: When RSI is close to its threshold, the color becomes more transparent, alerting traders to a less reliable trend.

- Classic mode available: The 'Use Classic Supertrend' option allows switching to a standard Supertrend display (fixed red/green) without the RSI effect.

4. Customizable Parameters

- ATR Length & ATR Factor: Define the sensitivity of the Supertrend.

- RSI Period & RSI Threshold: Allow refining the RSI filter based on market volatility.

- Classic mode: Enables/disables the RSI filtering to revert to the original Supertrend.

This indicator is especially valuable for traders looking to refine their trend signals based on market momentum measured by RSI.

This indicator is for informational purposes only and should not be considered financial advice. Trading involves risks, and past performance does not guarantee future results. Always conduct your own analysis before making any trading decisions.

AI Adaptive Oscillator [PhenLabs]📊 Algorithmic Adaptive Oscillator

Version: PineScript™ v6

📌 Description

The AI Adaptive Oscillator is a sophisticated technical indicator that employs ensemble learning and adaptive weighting techniques to analyze market conditions. This innovative oscillator combines multiple traditional technical indicators through an AI-driven approach that continuously evaluates and adjusts component weights based on historical performance. By integrating statistical modeling with machine learning principles, the indicator adapts to changing market dynamics, providing traders with a responsive and reliable tool for market analysis.

🚀 Points of Innovation:

Ensemble learning framework with adaptive component weighting

Performance-based scoring system using directional accuracy

Dynamic volatility-adjusted smoothing mechanism

Intelligent signal filtering with cooldown and magnitude requirements

Signal confidence levels based on multi-factor analysis

🔧 Core Components

Ensemble Framework : Combines up to five technical indicators with performance-weighted integration

Adaptive Weighting : Continuous performance evaluation with automated weight adjustment

Volatility-Based Smoothing : Adapts sensitivity based on current market volatility

Pattern Recognition : Identifies potential reversal patterns with signal qualification criteria

Dynamic Visualization : Professional color schemes with gradient intensity representation

Signal Confidence : Three-tiered confidence assessment for trading signals

🔥 Key Features

The indicator provides comprehensive market analysis through:

Multi-Component Ensemble : Integrates RSI, CCI, Stochastic, MACD, and Volume-weighted momentum

Performance Scoring : Evaluates each component based on directional prediction accuracy

Adaptive Smoothing : Automatically adjusts based on market volatility

Pattern Detection : Identifies potential reversal patterns in overbought/oversold conditions

Signal Filtering : Prevents excessive signals through cooldown periods and minimum change requirements

Confidence Assessment : Displays signal strength through intuitive confidence indicators (average, above average, excellent)

🎨 Visualization

Gradient-Filled Oscillator : Color intensity reflects strength of market movement

Clear Signal Markers : Distinct bullish and bearish pattern signals with confidence indicators

Range Visualization : Clean representation of oscillator values from -6 to 6

Zero Line : Clear demarcation between bullish and bearish territory

Customizable Colors : Color schemes that can be adjusted to match your chart style

Confidence Symbols : Intuitive display of signal confidence (no symbol, +, or ++) alongside direction markers

📖 Usage Guidelines

⚙️ Settings Guide

Color Settings

Bullish Color

Default: #2b62fa (Blue)

This setting controls the color representation for bullish movements in the oscillator. The color appears when the oscillator value is positive (above zero), with intensity indicating the strength of the bullish momentum. A brighter shade indicates stronger bullish pressure.

Bearish Color

Default: #ce9851 (Amber)

This setting determines the color representation for bearish movements in the oscillator. The color appears when the oscillator value is negative (below zero), with intensity reflecting the strength of the bearish momentum. A more saturated shade indicates stronger bearish pressure.

Signal Settings

Signal Cooldown (bars)

Default: 10

Range: 1-50

This parameter sets the minimum number of bars that must pass before a new signal of the same type can be generated. Higher values reduce signal frequency and help prevent overtrading during choppy market conditions. Lower values increase signal sensitivity but may generate more false positives.

Min Change For New Signal

Default: 1.5

Range: 0.5-3.0

This setting defines the minimum required change in oscillator value between consecutive signals of the same type. It ensures that new signals represent meaningful changes in market conditions rather than minor fluctuations. Higher values produce fewer but potentially higher-quality signals, while lower values increase signal frequency.

AI Core Settings

Base Length

Default: 14

Minimum: 2

This fundamental setting determines the primary calculation period for all technical components in the ensemble (RSI, CCI, Stochastic, etc.). It represents the lookback window for each component’s base calculation. Shorter periods create a more responsive but potentially noisier oscillator, while longer periods produce smoother signals with potential lag.

Adaptive Speed

Default: 0.1

Range: 0.01-0.3

Controls how quickly the oscillator adapts to new market conditions through its volatility-adjusted smoothing mechanism. Higher values make the oscillator more responsive to recent price action but potentially more erratic. Lower values create smoother transitions but may lag during rapid market changes. This parameter directly influences the indicator’s adaptiveness to market volatility.

Learning Lookback Period

Default: 150

Minimum: 10

Determines the historical data range used to evaluate each ensemble component’s performance and calculate adaptive weights. This setting controls how far back the AI “learns” from past performance to optimize current signals. Longer periods provide more stable weight distribution but may be slower to adapt to regime changes. Shorter periods adapt more quickly but may overreact to recent anomalies.

Ensemble Size

Default: 5

Range: 2-5

Specifies how many technical components to include in the ensemble calculation.

Understanding The Interaction Between Settings

Base Length and Learning Lookback : The base length determines the reactivity of individual components, while the lookback period determines how their weights are adjusted. These should be balanced according to your timeframe - shorter timeframes benefit from shorter base lengths, while the lookback should generally be 10-15 times the base length for optimal learning.

Adaptive Speed and Signal Cooldown : These settings control sensitivity from different angles. Increasing adaptive speed makes the oscillator more responsive, while reducing signal cooldown increases signal frequency. For conservative trading, keep adaptive speed low and cooldown high; for aggressive trading, do the opposite.

Ensemble Size and Min Change : Larger ensembles provide more stable signals, allowing for a lower minimum change threshold. Smaller ensembles might benefit from a higher threshold to filter out noise.

Understanding Signal Confidence Levels

The indicator provides three distinct confidence levels for both bullish and bearish signals:

Average Confidence (▲ or ▼) : Basic signal that meets the minimum pattern and filtering criteria. These signals indicate potential reversals but with moderate confidence in the prediction. Consider using these as initial alerts that may require additional confirmation.

Above Average Confidence (▲+ or ▼+) : Higher reliability signal with stronger underlying metrics. These signals demonstrate greater consensus among the ensemble components and/or stronger historical performance. They offer increased probability of successful reversals and can be traded with less additional confirmation.

Excellent Confidence (▲++ or ▼++) : Highest quality signals with exceptional underlying metrics. These signals show strong agreement across oscillator components, excellent historical performance, and optimal signal strength. These represent the indicator’s highest conviction trade opportunities and can be prioritized in your trading decisions.

Confidence assessment is calculated through a multi-factor analysis including:

Historical performance of ensemble components

Degree of agreement between different oscillator components

Relative strength of the signal compared to historical thresholds

✅ Best Use Cases:

Identify potential market reversals through oscillator extremes