Vinicius Setup ATR

Description:

This script is a strategy based on the Supertrend indicator combined with volume analysis, candle strength, and RSI. Its goal is to identify potential entry points for buy and sell trades based on technical criteria, without promising profitability or guaranteed results.

Script Components:

Supertrend: Used as the main trend compass. When the trend is positive (direction = 1), buy signals are considered; when negative (direction = -1), sell signals are considered.

Volume: Entries are only validated if the volume is above the average of the last 20 candles, adjusted with a 1.2 multiplier.

Candle Body: The candle body must be larger than a certain percentage of the ATR, ensuring sufficient strength and volatility.

RSI: Used as a filter to avoid trades in extreme overbought or oversold zones.

Support and Resistance: Identified based on simple pivots (5 periods before and after).

Customizable Parameters:

ATR Length and Multiplier: Controls the sensitivity of the Supertrend.

RSI Period: Adjusts the relative strength filter.

Minimum Volume and Candle Body: Settings to validate entry signals.

Entry Conditions:

Buy: Positive trend + strong candle + high volume + RSI below 70.

Sell: Negative trend + strong candle + high volume + RSI above 30.

Exit Conditions:

The trade is closed upon the appearance of an opposite signal.

Notes:

This is a technical system with no profit guarantees.

It is recommended to test with realistic capital values and parameters suited to your risk management.

The script is not optimized for specific profitability, but rather to support study and the construction of setups with objective criteria.

ATR

DEMA Trend Oscillator Strategy📌 Overview

The DEMA Trend Oscillator Strategy is a dynamic trend-following approach based on the Normalized DEMA Oscillator SD.

It adapts in real-time to market volatility with the goal of improving entry accuracy and optimizing risk management.

⚠️ This strategy is provided for educational and research purposes only.

Past performance does not guarantee future results.

🎯 Strategy Objectives

The main goal of this strategy is to respond quickly to sudden price movements and trend reversals,

by combining momentum-based signals with volatility filters.

It is designed to be user-friendly for traders of all experience levels.

✨ Key Features

Normalized DEMA Oscillator: A momentum indicator that normalizes DEMA values on a 0–100 scale, allowing intuitive identification of trend strength

Two-Bar Confirmation Filter: Requires two consecutive bullish or bearish candles to reduce noise and enhance entry reliability

ATR x2 Trailing Stop: In addition to fixed stop-loss levels, a trailing stop based on 2× ATR is used to maximize profits during strong trends

📊 Trading Rules

Long Entry:

Normalized DEMA > 55 (strong upward momentum)

Candle low is above the upper SD band

Two consecutive bullish candles appear

Short Entry:

Normalized DEMA < 45 (downward momentum)

Candle high is below the lower SD band

Two consecutive bearish candles appear

Exit Conditions:

Take-profit at a risk-reward ratio of 1.5

Stop-loss triggered if price breaks below (long) or above (short) the SD band

Trailing stop activated based on 2× ATR to secure and extend profits

💰 Risk Management Parameters

Symbol & Timeframe: Any (AUDUSD 5M example)

Account size (virtual): $3000

Commission: 0.4PIPS(0.0004)

Slippage: 2 pips

Risk per trade: 5%

Number of trades (backtest):534

All parameters can be adjusted based on broker specifications and individual trading profiles.

⚙️ Trading Parameters & Considerations

Indicator: Normalized DEMA Oscillator SD

Parameter settings:

DEMA Period (len_dema): 40

Base Length: 20

Long Threshold: 55

Short Threshold: 45

Risk-Reward Ratio: 1.5

ATR Multiplier for Trailing Stop: 2.0

🖼 Visual Support

The chart displays the following visual elements:

Upper and lower SD bands (±2 standard deviations)

Entry signals shown as directional arrows

🔧 Strategy Improvements & Uniqueness

This strategy is inspired by “Normalized DEMA Oscillator SD” by QuantEdgeB,

but introduces enhancements such as a two-bar confirmation filter and an ATR-based trailing stop.

Compared to conventional trend-following strategies, it offers superior noise filtering and profit optimization.

✅ Summary

The DEMA Trend Oscillator Strategy is a responsive and practical trend-following method

that combines momentum detection with adaptive risk management.

Its visual clarity and logical structure make it a powerful and repeatable tool

for traders seeking consistent performance in trending markets.

⚠️ Always apply appropriate risk management. This strategy is based on historical data and does not guarantee future results.

Intraday Uncertainty [PhenLabs]📊 Intraday Uncertainty

Version: PineScript™ v6

📌 Description

The Intraday Uncertainty indicator offers traders a visual representation of market certainty/uncertainty during trading sessions. By comparing each price bar’s range to the Average True Range (ATR), it provides an intuitive way to gauge market conviction through a color gradient system.

This tool helps traders identify periods of high certainty (potentially trending markets) versus high uncertainty (potentially choppy or volatile markets) without complex calculations or multiple indicators. The color-coded bars create an immediate visual cue to support decision-making in varying market conditions.

🚀 Points of Innovation

Automated range-to-ATR ratio calculation that adapts to changing market volatility

Dynamic color gradient system that visually distinguishes between certain and uncertain price action

Customizable gradient clamping to fine-tune sensitivity to market conditions

Integrated dashboard that provides clear interpretation guidance

Position-flexible legend that accommodates different chart layouts

Highly optimized for performance with minimal calculation overhead

🔧 Core Components

ATR Calculation: Measures market volatility using a configurable lookback period

Range-to-ATR Ratio: Compares current bar’s high-low range against average volatility

Gradient Mapping System: Converts numerical uncertainty values into an intuitive color scale

Dashboard Legend: Provides clear interpretation guidance with customizable positioning

🔥 Key Features

Bar Coloring: Instantly identifies market certainty levels through intuitive color gradients

Customizable ATR Period: Adjust sensitivity to historical volatility based on trading style

Gradient Clamping: Fine-tune the color sensitivity using the Range/ATR multiplier

Color Customization: Personalize the color scheme to match your chart aesthetics

Informative Dashboard: Quickly interpret color meanings with the optional on-chart legend

Flexible Display Options: Customize dashboard position and text size for your chart layout

🎨 Visualization

Color Gradient: Bars colored on a spectrum from green (high certainty) to red (high uncertainty)

Dashboard Legend: Optional on-chart guide explaining the color interpretation

Color Intensity: Stronger colors indicate more extreme certainty/uncertainty levels

At-a-glance Interpretation: Quickly identify market conviction without analyzing numbers

📖 Usage Guidelines

Calculation Settings

ATR Period

Default: 14

Range: 1+

Description: Controls the lookback period for ATR calculation. Lower values increase sensitivity to recent volatility, while higher values provide more stability.

Gradient Clamp (Range/ATR Multiplier)

Default: 2.0

Range: 0.1+

Description: Sets the maximum Range/ATR ratio for gradient scaling. Ranges above this value display the end color (high uncertainty).

Color Settings

Gradient Start Color (High Certainty)

Default: Green

Description: Color representing high market certainty (low Range/ATR ratio)

Gradient End Color (Low Certainty)

Default: Red

Description: Color representing low market certainty (high Range/ATR ratio)

Dashboard Settings

Show Dashboard Legend

Default: True

Description: Toggles the visibility of the on-chart interpretation guide

Dashboard Position

Options: top_right, top_left, bottom_right, bottom_left, middle_right, middle_left

Default: bottom_right

Description: Controls the placement of the dashboard on your chart

Dashboard Text Size

Options: tiny, small, normal, large, huge

Default: normal

Description: Adjusts the text size of the dashboard for readability

✅ Best Use Cases

Identifying potential trend shifts when certainty levels change dramatically

Confirming trend strength through consistent certainty levels

Detecting choppy/sideways markets with persistent high uncertainty

Filtering trading signals from other indicators based on certainty levels

Gauging market conviction behind price breakouts or pullbacks

Optimizing entry/exit timing based on certainty/uncertainty transitions

⚠️ Limitations

Does not predict future price direction, only measures current bar certainty

May provide false signals during news events or unexpected volatility spikes

Requires context within the broader market environment for optimal interpretation

Color interpretation is relative rather than absolute across different securities

ATR-based calculation means sensitivity varies across different timeframes

💡 What Makes This Unique

Simplicity: Single visual indicator that doesn’t require multiple technical tools

Adaptability: Automatically adjusts to changing market volatility conditions

Contextual Analysis: Provides market conviction context beyond just price movement

Intuitive Design: Color-based system that requires minimal learning curve

Efficiency: Lightweight calculation that doesn’t impact chart performance

🔬 How It Works

1. ATR Calculation:

Calculates the Average True Range using the specified period

Establishes a baseline for normal market volatility

2. Range Analysis:

Measures each bar’s high-low range

Compares this range to the current ATR value to create a ratio

3. Gradient Mapping:

Converts the Range/ATR ratio to a normalized value between 0 and 1

Maps this value onto a color gradient between the start and end colors

Applies the resulting color to the price bar

4. Dashboard Creation:

Constructs an information panel on the last visible bar

Populates it with color samples and interpretation guidance

💡 Note:

This indicator works best when used in conjunction with other technical analysis tools rather than in isolation. The certainty/uncertainty measure provides context for your trading decisions but should not be the sole basis for entries and exits. Consider using higher certainty periods for trend-following strategies and exercise caution during periods of high uncertainty.

Rogue ORB PRORogue ORB Pro is a precision-engineered Opening Range Breakout (ORB) indicator built for active intraday traders who need real signals, not noise.

This tool identifies high-probability breakout entries from the opening range, enhanced with optional ATR-based stop loss levels, deviation targets, cooldown filters, and a relative volume gate to filter weak setups.

🔍 Key Features:

Opening Range High/Low: Drawn from a user-defined time window and locked for the day

Deviations: Automatically plots target zones above and below the OR range (e.g. 1, 2 deviations)

Pre-Market Levels: Automatically draws pre market high and low lines at the end of pre market session

Buy/Sell Signals: Triggered on breakout of the OR High/Low with configurable breakout logic (touch or close)

ATR Stop Loss Line: Dynamically drawn at a fixed ATR distance from breakout candle, with optional SL label

Cooldown Period: Prevents back-to-back signals by enforcing a user-defined bar delay between entries, can help with overtrading

Volume Filter: Optional relative volume filter that requires breakout candles to exceed a custom volume threshold

VWAP Overlay: Visual VWAP for directional bias and confluence

FSH ATR MTF MonitorThe FSH ATR MTF Monitor tracks the Average True Range (ATR) and current range across six customizable timeframes, displaying the results in a table. When a timeframe’s range exceeds its ATR, the range value turns yellow, signaling heightened volatility. This multi-timeframe tool helps traders assess market conditions and plan entries or exits.

Key Features:

- Monitors ATR and range for up to six timeframes simultaneously.

- Customizable ATR length and timeframe inputs.

- Highlights ranges exceeding ATR in yellow for quick identification.

- Table display with toggle option for flexibility.

How to Use:

1. Add the indicator to your chart.

2. Adjust the ATR length and timeframes in the inputs as needed.

3. Watch for yellow range values to spot volatility spikes across timeframes.

4. Toggle the table off if not needed.

Ideal for scalpers, swing traders, or anyone analyzing volatility across multiple timeframes.

ATR Stop BufferThe ATR Stop Buffer indicator calculates the Daily Average True Range (ATR) and converts it into ticks based on the symbol's minimum price movement. It then displays the full ATR, 2% of ATR, and 10% of ATR in a clean table format, rounded up for simplicity. This tool is ideal for traders who want to set volatility-based stop-loss levels or buffers for their trades.

Key Features:

- Uses a 14-period Daily ATR for robust volatility measurement.

- Converts ATR into ticks for precise application across different instruments.

- Table display with toggle option for flexibility.

- Perfect for risk management and trade planning.

How to Use:

1. Add the indicator to your chart.

2. Use the table values to adjust your stop-loss distances (e.g., 2% ATR for tight stops, 10% ATR for wider buffers).

3. Toggle the table off if you only need the values occasionally.

Note: Works best on instruments with defined tick sizes (e.g., futures, forex, stocks).

Adaptive Fibonacci Pullback System -FibonacciFluxAdaptive Fibonacci Pullback System (AFPS) - FibonacciFlux

This work is licensed under a Attribution-NonCommercial-ShareAlike 4.0 International (CC BY-NC-SA 4.0). Original concepts by FibonacciFlux.

Abstract

The Adaptive Fibonacci Pullback System (AFPS) presents a sophisticated, institutional-grade algorithmic strategy engineered for high-probability trend pullback entries. Developed by FibonacciFlux, AFPS uniquely integrates a proprietary Multi-Fibonacci Supertrend engine (0.618, 1.618, 2.618 ratios) for harmonic volatility assessment, an Adaptive Moving Average (AMA) Channel providing dynamic market context, and a synergistic Multi-Timeframe (MTF) filter suite (RSI, MACD, Volume). This strategy transcends simple indicator combinations through its strict, multi-stage confluence validation logic. Historical simulations suggest that specific MTF filter configurations can yield exceptional performance metrics, potentially achieving Profit Factors exceeding 2.6 , indicative of institutional-level potential, while maintaining controlled risk under realistic trading parameters (managed equity risk, commission, slippage).

4 hourly MTF filtering

1. Introduction: Elevating Pullback Trading with Adaptive Confluence

Traditional pullback strategies often struggle with noise, false signals, and adapting to changing market dynamics. AFPS addresses these challenges by introducing a novel framework grounded in Fibonacci principles and adaptive logic. Instead of relying on static levels or single confirmations, AFPS seeks high-probability pullback entries within established trends by validating signals through a rigorous confluence of:

Harmonic Volatility Context: Understanding the trend's stability and potential turning points using the unique Multi-Fibonacci Supertrend.

Adaptive Market Structure: Assessing the prevailing trend regime via the AMA Channel.

Multi-Dimensional Confirmation: Filtering signals with lower-timeframe Momentum (RSI), Trend Alignment (MACD), and Market Conviction (Volume) using the MTF suite.

The objective is to achieve superior signal quality and adaptability, moving beyond conventional pullback methodologies.

2. Core Methodology: Synergistic Integration

AFPS's effectiveness stems from the engineered synergy between its core components:

2.1. Multi-Fibonacci Supertrend Engine: Utilizes specific Fibonacci ratios (0.618, 1.618, 2.618) applied to ATR, creating a multi-layered volatility envelope potentially resonant with market harmonics. The averaged and EMA-smoothed result (`smoothed_supertrend`) provides a robust, dynamic trend baseline and context filter.

// Key Components: Multi-Fibonacci Supertrend & Smoothing

average_supertrend = (supertrend1 + supertrend2 + supertrend3) / 3

smoothed_supertrend = ta.ema(average_supertrend, st_smooth_length)

2.2. Adaptive Moving Average (AMA) Channel: Provides dynamic market context. The `ama_midline` serves as a key filter in the entry logic, confirming the broader trend bias relative to adaptive price action. Extended Fibonacci levels derived from the channel width offer potential dynamic S/R zones.

// Key Component: AMA Midline

ama_midline = (ama_high_band + ama_low_band) / 2

2.3. Multi-Timeframe (MTF) Filter Suite: An optional but powerful validation layer (RSI, MACD, Volume) assessed on a lower timeframe. Acts as a **validation cascade** – signals must pass all enabled filters simultaneously.

2.4. High-Confluence Entry Logic: The core innovation. A pullback entry requires a specific sequence and validation:

Price interaction with `average_supertrend` and recovery above/below `smoothed_supertrend`.

Price confirmation relative to the `ama_midline`.

Simultaneous validation by all enabled MTF filters.

// Simplified Long Entry Logic Example (incorporates key elements)

long_entry_condition = enable_long_positions and

(low < average_supertrend and close > smoothed_supertrend) and // Pullback & Recovery

(close > ama_midline and close > ama_midline) and // AMA Confirmation

(rsi_filter_long_ok and macd_filter_long_ok and volume_filter_ok) // MTF Validation

This strict, multi-stage confluence significantly elevates signal quality compared to simpler pullback approaches.

1hourly filtering

3. Realistic Implementation and Performance Potential

AFPS is designed for practical application, incorporating realistic defaults and highlighting performance potential with crucial context:

3.1. Realistic Default Strategy Settings:

The script includes responsible default parameters:

strategy('Adaptive Fibonacci Pullback System - FibonacciFlux', shorttitle = "AFPS", ...,

initial_capital = 10000, // Accessible capital

default_qty_type = strategy.percent_of_equity, // Equity-based risk

default_qty_value = 4, // Default 4% equity risk per initial trade

commission_type = strategy.commission.percent,

commission_value = 0.03, // Realistic commission

slippage = 2, // Realistic slippage

pyramiding = 2 // Limited pyramiding allowed

)

Note: The default 4% risk (`default_qty_value = 4`) requires careful user assessment and adjustment based on individual risk tolerance.

3.2. Historical Performance Insights & Institutional Potential:

Backtesting provides insights into historical behavior under specific conditions (always specify Asset/Timeframe/Dates when sharing results):

Default Performance Example: With defaults, historical tests might show characteristics like Overall PF ~1.38, Max DD ~1.16%, with potential Long/Short performance variance (e.g., Long PF 1.6+, Short PF < 1).

Optimized MTF Filter Performance: Crucially, historical simulations demonstrate that meticulous configuration of the MTF filters (particularly RSI and potentially others depending on market) can significantly enhance performance. Under specific, optimized MTF filter settings combined with appropriate risk management (e.g., 7.5% risk), historical tests have indicated the potential to achieve **Profit Factors exceeding 2.6**, alongside controlled drawdowns (e.g., ~1.32%). This level of performance, if consistently achievable (which requires ongoing adaptation), aligns with metrics often sought in institutional trading environments.

Disclaimer Reminder: These results are strictly historical simulations. Past performance does not guarantee future results. Achieving high performance requires careful parameter tuning, adaptation to changing markets, and robust risk management.

3.3. Emphasizing Risk Management:

Effective use of AFPS mandates active risk management. Utilize the built-in Stop Loss, Take Profit, and Trailing Stop features. The `pyramiding = 2` setting requires particularly diligent oversight. Do not rely solely on default settings.

4. Conclusion: Advancing Trend Pullback Strategies

The Adaptive Fibonacci Pullback System (AFPS) offers a sophisticated, theoretically grounded, and highly adaptable framework for identifying and executing high-probability trend pullback trades. Its unique blend of Fibonacci resonance, adaptive context, and multi-dimensional MTF filtering represents a significant advancement over conventional methods. While requiring thoughtful implementation and risk management, AFPS provides discerning traders with a powerful tool potentially capable of achieving institutional-level performance characteristics under optimized conditions.

Acknowledgments

Developed by FibonacciFlux. Inspired by principles of Fibonacci analysis, adaptive averaging, and multi-timeframe confirmation techniques explored within the trading community.

Disclaimer

Trading involves substantial risk. AFPS is an analytical tool, not a guarantee of profit. Past performance is not indicative of future results. Market conditions change. Users are solely responsible for their decisions and risk management. Thorough testing is essential. Deploy at your own considered risk.

VIDYA Auto-Trading(Reversal Logic)Overview

This script is a dynamic trend-following strategy based on the Variable Index Dynamic Average (VIDYA). It adapts in real time to market volatility, aiming to enhance entry precision and optimize risk management.

⚠️ This strategy is intended for educational and research purposes. Past performance does not guarantee future results. All results are based on historical simulations using fixed parameters.

Strategy Objectives

The objective of this strategy is to respond swiftly to sudden price movements and trend reversals, providing consistent and reliable trade signals under historical testing conditions. It is designed to be intuitive and efficient for traders of all levels.

Key Features

Momentum Sensitivity via VIDYA: Reacts quickly to momentum shifts, allowing for accurate trend-following entries.

Volatility-Based ATR Bands: Automatically adjusts stop levels and entry conditions based on current market volatility.

Intuitive Trend Visualization: Uptrends are marked with green zones, and downtrends with red zones, giving traders clear visual guidance.

Trading Rules

Long Entry: Triggered when price crosses above the upper band. Any existing short position is closed.

Short Entry: Triggered when price crosses below the lower band. Any existing long position is closed.

Exit Conditions: Positions are reversed based on signal changes, using a position reversal strategy.

Risk Management Parameters

Market: ETHUSD(5M)

Account Size: $3,000 (reasonable approximation for individual traders)

Commission: 0.02%

Slippage: 2 pip

Risk per Trade: 5% of account equity (adjusted to comply with TradingView guidelines for realistic risk levels)

Number of Trades: 251 (based on backtest over the selected dataset)

⚠️ The risk per trade and other values can be customized. Users are encouraged to adapt these to their individual needs and broker conditions.

Trading Parameters & Considerations

VIDYA Length: 10

VIDYA Momentum: 20

Distance factor for upper/lower bands: 2

Source: close

Visual Support

Trend zones, entry points, and directional shifts are clearly plotted on the chart. These visual cues enhance the analytical experience and support faster decision-making.

Visual elements are designed to improve interpretability and are not intended as financial advice or trade signals.

Strategy Improvements & Uniqueness

Inspired by the public work of BigBeluga, this script evolves the original concept with meaningful enhancements. By combining VIDYA and ATR bands, it offers greater adaptability and practical value compared to conventional trend-following strategies.

This adaptation is original work and not a direct copy. Improvements are designed to enhance usability, risk control, and market responsiveness.

Summary

This strategy offers a responsive and adaptive approach to trend trading, built on momentum detection and volatility-adjusted risk management. It balances clarity, precision, and practicality—making it a powerful tool for traders seeking reliable trend signals.

⚠️ All results are based on historical data and are subject to change under different market conditions. This script does not guarantee profit and should be used with caution and proper risk management.

Highest High Line with Multi-Timeframe Supertrend and RSIOverview:

This powerful indicator combines three essential elements for traders:

Highest High Line – Tracks the highest price over a customizable lookback period across different timeframes.

Multi-Timeframe Supertrend – Displays Supertrend values and trend directions for multiple timeframes simultaneously.

Relative Strength Index (RSI) – Shows RSI values across different timeframes for momentum analysis.

Features:

✅ Customizable Highest High Line:

Selectable timeframes: Daily, Weekly, Monthly, Quarterly, Yearly

Adjustable lookback period

✅ Multi-Timeframe Supertrend:

Supports 1min, 5min, 10min, 15min, 30min, 1H, Daily, Weekly, Monthly, Quarterly, Yearly

ATR-based calculation with configurable ATR period and multiplier

Identifies bullish (green) & bearish (red) trends

✅ Multi-Timeframe RSI:

Calculates RSI for the same timeframes as Supertrend

Overbought (≥70) and Oversold (≤30) signals with color coding

✅ Comprehensive Table Display:

A clean, structured table in the bottom-right corner

Displays Supertrend direction, value, and RSI for all timeframes

Helps traders quickly assess trend and momentum alignment

How to Use:

Use the Highest High Line to identify key resistance zones.

Confirm trend direction with Multi-Timeframe Supertrend.

Check RSI values to avoid overbought/oversold conditions before entering trades.

Align multiple timeframes for stronger confirmation of trend shifts.

Ideal For:

✅ Scalpers (lower timeframes: 1m–30m)

✅ Swing Traders (higher timeframes: 1H–D)

✅ Position Traders (Weekly, Monthly, Quarterly)

💡 Tip: Look for Supertrend & RSI confluence across multiple timeframes for higher probability setups.

Scalping Entry/Exit Indicator by DiGetImagine having a tool that not only spots high-probability entry signals but also visually marks them on your chart with color-coded cues and automated alerts. The Scalping Entry/Exit Indicator by DiGet does exactly that—by fusing a range of classic candlestick patterns (such as Bullish Hammers, Engulfing patterns, and Morning/Evening Stars) with dynamic risk management levels, this script empowers you to make swift and informed trading decisions. Whether you're an active trader or an algorithm enthusiast, this indicator offers both precision and clarity in identifying scalp opportunities, making your chart analysis more efficient and visually engaging.

Indicator Breakdown

Input Parameters:

The indicator accepts a customizable risk-reward ratio, an ATR period for volatility measurement, and a lookback period to scan for valid candlestick patterns.

ATR & Candle Calculations:

It computes the Average True Range (ATR) to dynamically set stop-loss and take-profit levels. Additionally, it determines the body and wick sizes of each candlestick to help identify key reversal patterns.

Pattern Detection:

Multiple bullish patterns (Hammer, Engulfing, Morning Star) and bearish patterns (Shooting Star, Engulfing, Evening Star) are detected. There’s also a simplified version of the Head & Shoulders pattern, offering further validation for reversal signals.

Signal Generation & Trade Levels:

The script consolidates the pattern signals into combined “buy” and “sell” triggers. It then calculates the respective stop-loss (SL) and take-profit (TP) levels based on the current price and ATR, providing a robust risk management framework.

Visual Aids & Alerts:

To enhance usability, the indicator changes the chart’s background color to green for buy signals and red for sell signals. It also draws labels, lines (representing SL and TP), and markers directly on the chart, along with alert conditions to notify traders of actionable signals.

This indicator is an excellent addition to your TradingView toolkit—ideal for scalpers and short-term traders seeking clarity, precision, and automated signal generation on their charts.

Enjoy trading with confidence and precision!

Adaptive Fibonacci Volatility Bands (AFVB)

**Adaptive Fibonacci Volatility Bands (AFVB)**

### **Overview**

The **Adaptive Fibonacci Volatility Bands (AFVB)** indicator enhances standard **Fibonacci retracement levels** by dynamically adjusting them based on market **volatility**. By incorporating **ATR (Average True Range) adjustments**, this indicator refines key **support and resistance zones**, helping traders identify **more reliable entry and exit points**.

**Key Features:**

- **ATR-based adaptive Fibonacci levels** that adjust to changing market volatility.

- **Buy and Sell signals** based on price interactions with dynamic support/resistance.

- **Toggleable confirmation filter** for refining trade signals.

- **Customizable color schemes** and alerts.

---

## **How This Indicator Works**

The **AFVB** operates in three main steps:

### **1️⃣ Detecting Key Fibonacci Levels**

The script calculates **swing highs and swing lows** using a user-defined lookback period. From this, it derives **Fibonacci retracement levels**:

- **0% (High)**

- **23.6%**

- **38.2%**

- **50% (Mid-Level)**

- **61.8%**

- **78.6%**

- **100% (Low)**

### **2️⃣ Adjusting for Market Volatility**

Instead of using **fixed retracement levels**, this indicator incorporates an **ATR-based adjustment**:

- **Resistance levels** shift **upward** based on ATR.

- **Support levels** shift **downward** based on ATR.

- This makes levels more **responsive** to price action.

### **3️⃣ Generating Buy & Sell Signals**

AFVB provides **two types of signals** based on price interactions with key levels:

✔ **Buy Signal**:

Occurs when price **dips below** a support level (78.6% or 100%) and **then closes back above it**.

- **Optionally**, a confirmation buffer can be enabled to require price to close **above an additional threshold** (based on ATR).

✔ **Sell Signal**:

Triggered when price **breaks above a resistance level** (0% or 23.6%) and **then closes below it**.

📌 **Important:**

- The **buy threshold setting** allows traders to **fine-tune** entry conditions.

- Turning this setting **off** generates **more frequent** buy signals.

- Keeping it **on** reduces false signals but may result in **fewer trade opportunities**.

---

## **How to Use This Indicator in Trading**

### 🔹 **Entry Strategy (Buying)**

1️⃣ Look for **buy signals** at the **78.6% or 100% Fibonacci levels**.

2️⃣ Ensure price **closes above** the support level before entering a long trade.

3️⃣ **Enable or disable** the buy threshold filter depending on desired trade strictness.

### 🔹 **Exit Strategy (Selling)**

1️⃣ Watch for **sell signals** at the **0% or 23.6% Fibonacci levels**.

2️⃣ If price **breaks above resistance and then closes below**, consider exiting long positions.

3️⃣ Can be used **alone** or **combined with trend confirmation tools** (e.g., moving averages, RSI).

### 🔹 **Using the Toggleable Buy Threshold**

- **ON**: Buy signal requires **extra confirmation** (reduces false signals but fewer trades).

- **OFF**: Buy triggers as soon as price **closes back above support** (more signals, but may include weaker setups).

---

## **User Inputs**

### **🔧 Customization Options**

- **ATR Length**: Defines the period for **ATR calculation**.

- **Swing Lookback**: Determines how far back to find **swing highs and lows**.

- **ATR Multiplier**: Adjusts the size of **volatility-based modifications**.

- **Buy/Sell Threshold Factor**: Fine-tunes the **entry signal strictness**.

- **Show Level Labels**: Enables/disables **Fibonacci level annotations**.

- **Color Settings**: Customize **support/resistance colors**.

### **📢 Alerts**

AFVB includes built-in **alert conditions** for:

- **Buy Signals** ("AFVB BUY SIGNAL - Possible reversal at support")

- **Sell Signals** ("AFVB SELL SIGNAL - Possible reversal at resistance")

- **Any Signal Triggered** (Useful for automated alerts)

---

## **Who Is This Indicator For?**

✅ **Scalpers & Day Traders** – Helps identify **short-term reversals**.

✅ **Swing Traders** – Useful for **buying dips** and **selling rallies**.

✅ **Trend Traders** – Can be combined with **momentum indicators** for confirmation.

**Best Timeframes:**

⏳ **15-minute, 1-hour, 4-hour, Daily charts** (works across multiple assets).

---

## **Limitations & Considerations**

🚨 **Important Notes**:

- **No indicator guarantees profits**. Always **combine** it with **risk management strategies**.

- Works best **in trending & mean-reverting markets**—may generate false signals in **choppy conditions**.

- Performance may vary across **different assets & timeframes**.

📢 **Backtesting is recommended** before using it for live trading.

Supertrend with RSI FilterThis indicator is an enhanced version of the classic Supertrend, incorporating an RSI (Relative Strength Index) filter to refine trend signals. Here is a detailed explanation of its functionality and key advantages over the traditional Supertrend.

1. Indicator Functionality

The indicator uses ATR (Average True Range) to calculate the Supertrend line, just like the classic version. However, it introduces an additional condition based on RSI to strengthen or weaken the Supertrend color based on market momentum.

2. Interpretation of Colors

The indicator displays the Supertrend line with dynamic colors based on trend direction and RSI strength:

- Uptrend (Supertrend in buy mode):

- Dark green (Teal): RSI above the defined threshold (default 50) → Strong bullish confirmation.

- Light gray: RSI below the threshold → Indicates a weaker uptrend or lack of confirmation.

- Downtrend (Supertrend in sell mode):

- Dark red: RSI below the threshold → Strong bearish confirmation.

- Light gray: RSI above the threshold → Indicates a weaker downtrend or lack of confirmation.

The opacity of the color dynamically adjusts based on how far RSI is from its threshold. The greater the difference, the more vivid the color, signaling a stronger trend.

3. Key Advantages Over the Classic Supertrend

- Filters out false signals: The RSI integration helps reduce false signals by only validating trends when RSI aligns with the Supertrend direction.

- Weakens uncertain signals: When RSI is close to its threshold, the color becomes more transparent, alerting traders to a less reliable trend.

- Classic mode available: The 'Use Classic Supertrend' option allows switching to a standard Supertrend display (fixed red/green) without the RSI effect.

4. Customizable Parameters

- ATR Length & ATR Factor: Define the sensitivity of the Supertrend.

- RSI Period & RSI Threshold: Allow refining the RSI filter based on market volatility.

- Classic mode: Enables/disables the RSI filtering to revert to the original Supertrend.

This indicator is especially valuable for traders looking to refine their trend signals based on market momentum measured by RSI.

This indicator is for informational purposes only and should not be considered financial advice. Trading involves risks, and past performance does not guarantee future results. Always conduct your own analysis before making any trading decisions.

Engulfing Candles (ATR-Based)This indicator detects Engulfing Patterns with an ATR-based filtering mechanism and trend confirmation. Unlike a basic engulfing pattern indicator that only checks if a current candle engulfs the previous one, this script incorporates trend detection using either the 50-period SMA alone or a combination of 50 and 200-period SMAs to ensure that signals align with the broader trend. The indicator identifies Bullish Engulfing patterns when a strong bullish candle engulfs a smaller bearish candle in a downtrend and Bearish Engulfing patterns when a strong bearish candle engulfs a smaller bullish candle in an uptrend. It also generates alerts and visually marks these patterns with labels ("BU" for bullish and "BE" for bearish) while highlighting the background accordingly.

What sets this indicator apart from a normal engulfing indicator is its ATR-based filtering system, which ensures that only significant engulfing candles are considered. Instead of accepting any engulfing pattern, the script measures candle body size relative to 1.5x ATR (configurable) to filter out weak signals. It also differentiates between long-bodied and small-bodied candles to confirm that the engulfing pattern represents real momentum shifts. This approach reduces false signals caused by small, insignificant candles and ensures that traders focus on high-probability reversal patterns. By integrating trend-based filtering and ATR-based confirmation, this indicator provides more reliable and context-aware engulfing signals than a standard engulfing pattern detector.

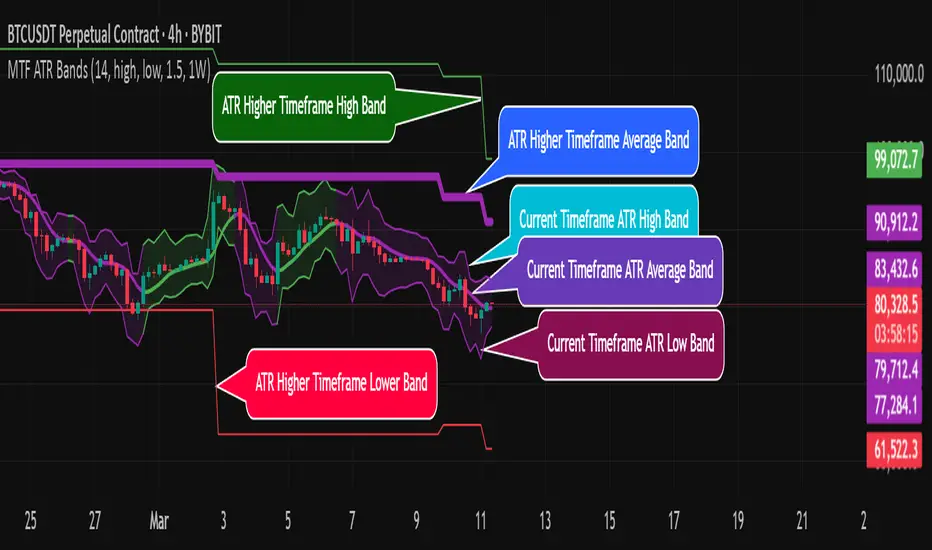

MTF ATR BandsA simple but effective MTF ATR bands indicator.

The script calculate and display ATR bands low and high of the current timeframe using high, low inputs and an RMA moving average, adding to it ATR of the period multiplied with the user multiplier, default is set to 1.5.

Than is calculated a smoothed average of the range and the color of it based on its slope, same color is used to fill the atr bands.

Than the higher timeframe bands are calculated and displayed on the chart.

How can be used ?

The higher timeframe average and bands can give you long term direction of the trend and the current timeframes moving average and filling short term trend, for example using the 15 min chart with a 4h HTF bands, or an 1h with a daily, or a daily with an weekly or weekly with bi-monthly atr bands.

Also can be used as a stop loss indicator.

Hope you will like it, any question send me a PM.

TEMA OBOS Strategy PakunTEMA OBOS Strategy

Overview

This strategy combines a trend-following approach using the Triple Exponential Moving Average (TEMA) with Overbought/Oversold (OBOS) indicator filtering.

By utilizing TEMA crossovers to determine trend direction and OBOS as a filter, it aims to improve entry precision.

This strategy can be applied to markets such as Forex, Stocks, and Crypto, and is particularly designed for mid-term timeframes (5-minute to 1-hour charts).

Strategy Objectives

Identify trend direction using TEMA

Use OBOS to filter out overbought/oversold conditions

Implement ATR-based dynamic risk management

Key Features

1. Trend Analysis Using TEMA

Uses crossover of short-term EMA (ema3) and long-term EMA (ema4) to determine entries.

ema4 acts as the primary trend filter.

2. Overbought/Oversold (OBOS) Filtering

Long Entry Condition: up > down (bullish trend confirmed)

Short Entry Condition: up < down (bearish trend confirmed)

Reduces unnecessary trades by filtering extreme market conditions.

3. ATR-Based Take Profit (TP) & Stop Loss (SL)

Adjustable ATR multiplier for TP/SL

Default settings:

TP = ATR × 5

SL = ATR × 2

Fully customizable risk parameters.

4. Customizable Parameters

TEMA Length (for trend calculation)

OBOS Length (for overbought/oversold detection)

Take Profit Multiplier

Stop Loss Multiplier

EMA Display (Enable/Disable TEMA lines)

Bar Color Change (Enable/Disable candle coloring)

Trading Rules

Long Entry (Buy Entry)

ema3 crosses above ema4 (Golden Cross)

OBOS indicator confirms up > down (bullish trend)

Execute a buy position

Short Entry (Sell Entry)

ema3 crosses below ema4 (Death Cross)

OBOS indicator confirms up < down (bearish trend)

Execute a sell position

Take Profit (TP)

Entry Price + (ATR × TP Multiplier) (Default: 5)

Stop Loss (SL)

Entry Price - (ATR × SL Multiplier) (Default: 2)

TP/SL settings are fully customizable to fine-tune risk management.

Risk Management Parameters

This strategy emphasizes proper position sizing and risk control to balance risk and return.

Trading Parameters & Considerations

Initial Account Balance: $7,000 (adjustable)

Base Currency: USD

Order Size: 10,000 USD

Pyramiding: 1

Trading Fees: $0.94 per trade

Long Position Margin: 50%

Short Position Margin: 50%

Total Trades (M5 Timeframe): 128

Deep Test Results (2024/11/01 - 2025/02/24)BTCUSD-5M

Total P&L:+1638.20USD

Max equity drawdown:694.78USD

Total trades:128

Profitable trades:44.53

Profit factor:1.45

These settings aim to protect capital while maintaining a balanced risk-reward approach.

Visual Support

TEMA Lines (Three EMAs)

Trend direction is indicated by color changes (Blue/Orange)

ema3 (short-term) and ema4 (long-term) crossover signals potential entries

OBOS Histogram

Green → Strong buying pressure

Red → Strong selling pressure

Blue → Possible trend reversal

Entry & Exit Markers

Blue Arrow → Long Entry Signal

Red Arrow → Short Entry Signal

Take Profit / Stop Loss levels displayed

Strategy Improvements & Uniqueness

This strategy is based on indicators developed by "l_lonthoff" and "jdmonto0", but has been significantly optimized for better entry accuracy, visual clarity, and risk management.

Enhanced Trend Identification with TEMA

Detects early trend reversals using ema3 & ema4 crossover

Reduces market noise for a smoother trend-following approach

Improved OBOS Filtering

Prevents excessive trading

Reduces unnecessary risk exposure

Dynamic Risk Management with ATR-Based TP/SL

Not a fixed value → TP/SL adjusts to market volatility

Fully customizable ATR multiplier settings

(Default: TP = ATR × 5, SL = ATR × 2)

Summary

The TEMA + OBOS Strategy is a simple yet powerful trading method that integrates trend analysis and oscillators.

TEMA for trend identification

OBOS for noise reduction & overbought/oversold filtering

ATR-based TP/SL settings for dynamic risk management

Before using this strategy, ensure thorough backtesting and demo trading to fine-tune parameters according to your trading style.

FVG | iSolani

Unveiling Market Inefficiencies with Precision

In fast-moving markets, spotting hidden opportunities often hinges on identifying imbalances between price and value. The FVG | iSolani indicator revolutionises this process by detecting Fair Value Gaps (FVGs) —zones where price action skips over "fair" valuation levels, creating potential retracement targets. Combining advanced filtering, dynamic visualisation, and automated management, this tool empowers traders to pinpoint high-probability setups with unprecedented clarity.

Core Methodology

The indicator employs a multi-layered approach to identify FVGs:

Three-Bar Gap Analysis: Bullish FVGs form when the current low exceeds the high of two bars prior, while bearish FVGs occur when the current high stays below the low of two bars back.

Volatility-Adjusted Filtering: Gaps are measured against a 100-bar standard deviation to exclude insignificant price jumps.

Volume Confirmation: Only gaps accompanied by above-average volume (relative to a 1-bar SMA) are validated, filtering out low-conviction moves.

Auto-Invalidation System: Continuously monitors price action to remove FVG zones once price closes within their range, maintaining chart cleanliness.

Breaking New Ground

This tool introduces three paradigm-shifting innovations:

Volume-Weighted Significance: Unlike traditional FVG detectors, it ties gap validity to volume spikes, emphasising institutional activity.

Adaptive Zone Management: Boxes automatically extend rightward (when enabled) and self-destruct when invalidated, eliminating manual cleanup.

Smart Color Encoding: Offers both monochrome (for multi-timeframe analysis) and standard bull/bear color schemes, with customisable transparency.

Engine Under the Hood

The script operates through four key processes:

Gap Detection: Scans every new bar for three-candle patterns meeting FVG criteria.

Statistical Filtering: Applies user-defined threshold (default: 1σ) to separate meaningful gaps from market noise.

Box Rendering: Draws semi-transparent zones between gap boundaries using TradingView's box objects, styled according to user preferences.

Array-Based Memory: Stores all active FVGs in arrays, enabling real-time validation checks against current price action.

Standard Configuration

Optimised default settings balance visibility and functionality:

Filter: 1.0 (1 standard deviation threshold)

Colors: "Mono" mode (gray boxes) with 90% transparency

Text Labels: Enabled in medium gray

Extension: Gaps extend indefinitely rightward

Borders: Dotted lines with visible outlines

Through its fusion of quantitative rigor and visual adaptability, the FVG | iSolani transforms raw price data into actionable intelligence. By focusing on volume-confirmed gaps and automating zone management, it cuts through market chaos to reveal structurally significant levels—a must-have for traders navigating breakouts, reversals, or order-flow analysis.

Trendchange Zones Indicator | iSolani

Spotting Reversals Before They Happen: The iSolani Trendshift System

Where RSI Meets Smart Volume Analysis - Your Visual Guide to Market Turns

Core Methodology

RSI-Powered Zones

Identifies critical levels using:

14-period RSI (default) with 70/30 thresholds

Semi-transparent boxes marking overbought (red) and oversold (green) territories

Zone persistence until RSI returns to neutral range

Dynamic Level Tracking

Plots evolving support/resistance using:

Pivot highs/lows with 15-bar lookback (default)

Auto-extending lines that adapt to new price extremes

Volume-Confirmed Breakouts

Flags significant moves with:

5/10 EMA volume oscillator

20% volume threshold (default) for confirmation

Technical Innovation

Three-Layer Confirmation

Unique combination of:

Classic RSI extremes

Price structure through pivot points

Volume-fueled momentum shifts

Adaptive Visualization

Zones maintain historical context at 33% transparency

Dynamic lines extend indefinitely until invalidated

Discreet labels for breakout events

System Workflow

Calculates RSI values in real-time

Draws colored zones when RSI crosses 70/30

Marks pivot points every 15 bars (default)

Updates support/resistance lines on new pivots

Triggers alerts when price breaks levels with volume confirmation

Standard Configuration

RSI Settings : 14-period length

Pivot Detection : 15-bar left/right lookback

Visuals : 33% transparency zones with thin borders

Volume Threshold : 20% oscillator difference

Alerts : Breakout signals with "B" labels

This system transforms the classic RSI into a spatial analysis tool - not just showing when markets are overextended, but where they're likely to reverse. The dynamic lines act as moving barriers that adapt to market structure, while the volume filter ensures only high-conviction breaks get flagged. By layering momentum, price action, and volume dynamics, it creates a multi-spectrum view of potential trend changes.

Daily True Range (DTR) vs Average True Range (ATR)Overview

The "DTR vs ATR with Color-Coded Percentage" indicator is a powerful volatility analysis tool designed for traders who want to understand daily price movements in the context of historical volatility. It calculates the Daily True Range (DTR)—the raw measure of a single day’s volatility—and compares it to the Average True Range (ATR), which smooths volatility over a user-defined period (default 14 days). The indicator presents this data in an intuitive table, featuring a color-coded percentage that visually represents how the current day’s move (DTR) stacks up against the average volatility (ATR). This helps traders quickly assess whether the current day’s price action is unusually volatile, average, or subdued relative to recent history.

Purpose

Volatility Comparison: Visualize how the current day’s price range (DTR) relates to the average range (ATR) over a specified period.

Decision Support: Identify days with exceptional movement (e.g., breakouts or reversals) versus normal or quiet days, aiding in trade entry/exit decisions.

Risk Management: Gauge daily volatility to adjust position sizing or stop-loss levels based on whether the market is exceeding or falling short of typical movement.

Features

Daily True Range (DTR) Calculation:

Computes the True Range for the current day as the greatest of:

Current day’s High - Low

High - Previous Close

Low - Previous Close

Aggregates data on any timeframe to ensure accurate daily values.

Average True Range (ATR):

Calculates the smoothed average of DTR over a customizable period (default 14 days) using Wilder’s smoothing method.

Updates in real-time as the day progresses.

Timeframe Flexibility: Works on any chart timeframe (e.g., 1-minute, 1-hour) while always calculating DTR and ATR based on daily data.

Color-Coded Display in either compact or table mode

The percentage value is color-coded in the table based on configurable thresholds:

Safe (default 75): Normal range, within typical volatility

Warning: (default 75-125): Above-average volatility.

Danger (default 125): Exceptionally high volatility

Multi-Timeframe ATR Levels by Hitesh2603Description:

"Multi-Timeframe ATR Levels by Hitesh2603" is a versatile and adaptive indicator designed to help traders identify key price levels based on the Average True Range (ATR) from a higher timeframe. The script automatically adapts to the current chart’s timeframe and allows you to customize the higher timeframe for ATR calculations, making it ideal for intraday and swing trading strategies.

The indicator plots upper and lower price levels based on the ATR multiplier, providing clear visual cues for potential profit-taking or exit points. It also includes features like editable timeframe presets , historical level plotting , labels , and alerts , making it a powerful tool for traders of all experience levels.

---

Key Features:

1. Automatic Timeframe Adaptation : - The script automatically detects the current chart’s timeframe and selects the appropriate higher timeframe for ATR calculations.

2. Editable Preset Timeframe Pairs : - Customize the higher timeframe for each chart timeframe directly in the indicator settings.

3. Dynamic ATR-Based Levels :- Plots upper and lower price levels using the formula:

- Upper Level = Current Candle Open + (Previous Candle ATR * Multiplier)

- Lower Level = Current Candle Open - (Previous Candle ATR * Multiplier)

4. Customizable Inputs :

- Adjust ATR length, multiplier, line length, colors, and more.

5. Labels :

- Displays the exact values of the upper and lower levels for easy reference.

6. Historical Levels :

- Optionally plots historical levels for all candles.

7. Alerts :

- Get notified when the price crosses the upper or lower levels.

---

Use Cases:

1. Intraday Trading :

- Use the script on a 5-minute or 15-minute chart with a 1-hour higher timeframe to identify intraday profit-taking or exit points.

2. Swing Trading :

- Use the script on a 1-hour or 4-hour chart with a daily higher timeframe to identify swing trading opportunities.

3. Position Trading :

- Use the script on a daily chart with a weekly higher timeframe to identify key levels for position trading.

4. Breakout Confirmation :

- Use the upper and lower levels as confirmation points for breakouts or reversals.

5. Risk Management :

- Use the levels to set stop-loss or take-profit targets based on market volatility.

---

How to Use:

1. Add the Script to Your Chart :

- Search for "Multi-Timeframe ATR Levels by Hitesh2603" in the TradingView indicator library and add it to your chart.

2. Customize the Settings :

- Adjust the inputs (e.g., ATR length, multiplier, line length, colors, etc.) to suit your trading strategy.

3. Set the Higher Timeframe :

- The script will automatically display an input for the higher timeframe based on the current chart’s timeframe. Customize it as needed.

4. Interpret the Levels :

- The script will plot two horizontal lines (upper and lower levels) on the chart. Use these levels for profit-taking, exits, or breakout confirmation.

5. Enable Alerts :

- Set up alerts to get notified when the price crosses the upper or lower levels.

---

Input Parameters:

1. ATR Length :

- The period used to calculate the ATR (default: 14).

2. ATR Multiplier :

- The multiplier applied to the ATR to calculate the levels (default: 0.65).

3. Line Length :

- The number of candles to extend the lines (default: 10).

4. Show Labels :

- Toggle to display the exact values of the levels (default: true).

5. Show Historical Levels :

- Toggle to plot historical levels for all candles (default: false).

6. Line Colors :

- Customize the colors of the upper and lower levels.

7. Line Width :

- Adjust the thickness of the lines (default: 2).

---

Example:

- Current Chart : 5-minute

- Higher Timeframe : 1-hour

- Previous Hour’s ATR : 4.6

- Current Hour’s Open : 102

- Multiplier : 0.65

Levels :

- Upper Level = 102 + (4.6 * 0.65) = 105.0

- Lower Level = 102 - (4.6 * 0.65) = 99.0

The script will plot horizontal lines at 105.0 and 99.0 on the 5-minute chart.

---

Alerts:

- Price Crosses Upper Level :

- Triggered when the price crosses above the upper level.

- Price Crosses Lower Level :

- Triggered when the price crosses below the lower level.

---

Notes:

- The script is designed to be flexible and adaptable to various trading styles and timeframes.

- Always backtest and validate the indicator with your trading strategy before using it in live trading.

---

Credits:

- Developed by Hitesh2603 .

- Special thanks to the TradingView community for inspiration and support.

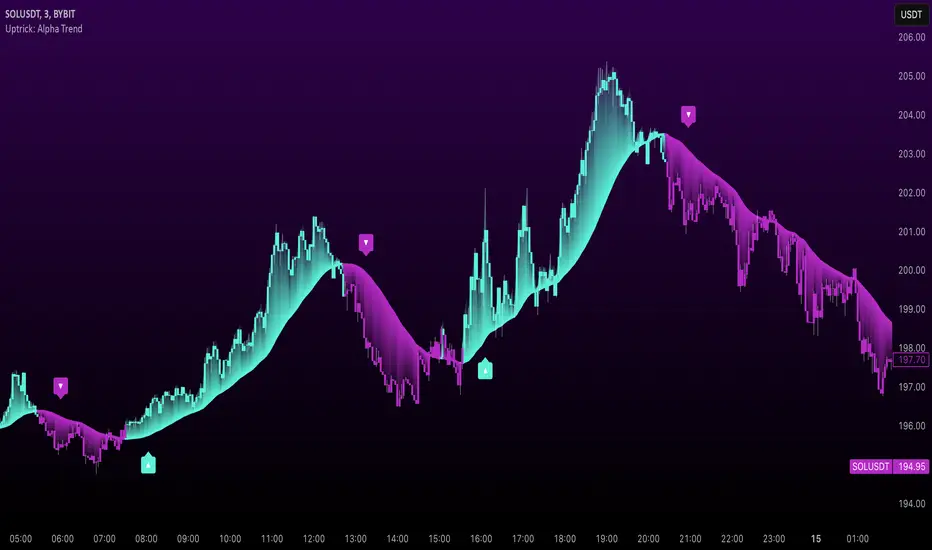

Uptrick: Alpha TrendIntroduction

Uptrick: Alpha Trend is a comprehensive technical analysis indicator designed to provide traders with detailed insights into market trends, momentum, and risk metrics. It adapts to various trading styles—from quick scalps to longer-term positions—by dynamically adjusting its calculations and visual elements. By combining multiple smoothing techniques, advanced color schemes, and customizable data tables, the indicator offers a holistic view of market behavior.

Originality

The Alpha Trend indicator distinguishes itself by blending established technical concepts with innovative adaptations. It employs three different smoothing techniques tailored to specific trading modes (Scalp, Swing, and Position), and it dynamically adjusts its parameters to match the chosen mode. The indicator also offers a wide range of color palettes and multiple on-screen tables that display key metrics. This unique combination of features, along with its ability to adapt in real time, sets it apart as a versatile tool for both novice and experienced traders.

Features

1. Multi-Mode Trend Line

The indicator automatically selects a smoothing method based on the trading mode:

- Scalp Mode uses the Hull Moving Average (HMA) for rapid responsiveness.

- Swing Mode employs the Exponential Moving Average (EMA) for balanced reactivity.

- Position Mode applies the Weighted Moving Average (WMA) for smoother, long-term trends.

Each method is chosen to best capture the price action dynamics appropriate to the trader’s timeframe.

2. Adaptive Momentum Thresholds

It tracks bullish and bearish momentum with counters that increment as the trend confirms directional movement. When these counters exceed a user-defined threshold, the indicator generates optional buy or sell signals. This approach helps filter out minor fluctuations and highlights significant market moves.

3. Gradient Fills

Two types of fills enhance visual clarity:

- Standard Gradient Fill displays ATR-based zones above and below the trend line, indicating potential bullish and bearish areas.

- Fading Gradient Fill creates a smooth transition between the trend line and the price, visually emphasizing the distance between them.

4. Bar Coloring and Signal Markers

The indicator can color-code bars based on market conditions—bullish, bearish, or neutral—allowing for immediate visual assessment. Additionally, signal markers such as buy and sell arrows are plotted when momentum thresholds are breached.

5. Comprehensive Data Tables

Uptrick: Alpha Trend offers several optional tables for detailed analysis:

- Insider Info: Displays key metrics like the current trend value, bullish/bearish momentum counts, and ATR.

- Indicator Metrics: Lists input settings such as trend length, damping, signal threshold, and net momentum.

- Market Analysis: Summarizes overall trend direction, trend strength, Sortino ratio, return, and volatility.

- Price & Trend Dynamics: Details price deviation from the trend, trend slope, and ATR ratio.

- Momentum & Volatility Insights: Presents RSI, standard deviation (volatility), and net momentum.

- Performance & Acceleration Metrics: Focuses on the Sortino ratio, trend acceleration, return, and trend strength.

Each table can be positioned flexibly on the chart, allowing traders to customize the layout according to their needs.

Why It Combines Specific Smoothing Techniques

Smoothing techniques are essential for filtering out market noise and revealing underlying trends. The indicator combines three smoothing methods for the following reasons:

- The Hull Moving Average (HMA) in Scalp Mode minimizes lag and responds quickly to price changes, which is critical for short-term trading.

- The Exponential Moving Average (EMA) in Swing Mode gives more weight to recent data, striking a balance between speed and smoothness. This makes it suitable for mid-term trend analysis.

- The Weighted Moving Average (WMA) in Position Mode smooths out short-term fluctuations, offering a clear view of longer-term trends and reducing the impact of transient market volatility.

By using these specific methods in their respective trading modes, the indicator ensures that the trend line is appropriately responsive for the intended time frame, enhancing decision-making while maintaining clarity.

Inputs

1. Trend Length (Default: 30)

Defines the lookback period for the smoothing calculation. A shorter trend length results in a more responsive line, while a longer length produces a smoother, less volatile trend.

2. Trend Damping (Default: 0.75)

Controls the degree of smoothing applied to the trend line. Lower values lead to a smoother curve, whereas higher values increase sensitivity to price fluctuations.

3. Signal Strength Threshold (Default: 5)

Specifies the number of consecutive bullish or bearish bars required to trigger a signal. Higher thresholds reduce the frequency of signals, focusing on stronger moves.

4. Enable Bar Coloring (Default: True)

Toggles whether each price bar is colored to indicate bullish, bearish, or neutral conditions.

5. Enable Signals (Default: True)

When enabled, this option plots buy or sell arrows on the chart once the momentum thresholds are met.

6. Enable Standard Gradient Fill (Default: False)

Activates ATR-based gradient fills around the trend line to visualize potential support and resistance zones.

7. Enable Fading Gradient Fill (Default: True)

Draws a gradual color transition between the trend line and the current price, emphasizing their divergence.

8. Trading Mode (Options: Scalp, Swing, Position)

Determines which smoothing method and ATR period to use, adapting the indicator’s behavior to short-term, medium-term, or long-term trading.

9. Table Position Inputs

Allows users to select from nine possible chart positions (top, middle, bottom; left, center, right) for each data table.

10. Show Table Booleans

Separate toggles control the display of each table (Insider Info, Indicator Metrics, Market Analysis, and the three Deep Tables), enabling a customized view of the data.

Color Schemes

(Default) - The colors in the preview image of the indicator.

(Emerald)

(Sapphire)

(Golden Blaze)

(Mystic)

(Monochrome)

(Pastel)

(Vibrant)

(Earth)

(Neon)

Calculations

1. Trend Line Methods

- Scalp Mode: Utilizes the Hull Moving Average (HMA), which computes two weighted moving averages (one at half the length and one at full length), subtracts them, and then applies a final weighted average based on the square root of the length. This method minimizes lag and increases responsiveness.

- Swing Mode: Uses the Exponential Moving Average (EMA), which assigns greater weight to recent prices, thus balancing quick reaction with smoothness.

- Position Mode: Applies the Weighted Moving Average (WMA) to focus on longer-term trends by emphasizing the entire lookback period and reducing the impact of short-term volatility.

2. Momentum Tracking

The indicator maintains separate counters for bullish and bearish momentum. These counters increase as the trend confirms directional movement and reset when the trend reverses. When a counter exceeds the defined signal strength threshold, a corresponding signal (buy or sell) is triggered.

3. Volatility and ATR Zones

The Average True Range (ATR) is calculated using a period that adapts to the selected trading mode (shorter for Scalp, longer for Position). The ATR value is then used to define upper and lower zones around the trend line, highlighting the current level of market volatility.

4. Return and Trend Acceleration

- Return is calculated as the difference between the current and previous closing prices, providing a simple measure of price change.

- Trend Acceleration is derived from the change in the trend line’s movement (its first derivative) compared to the previous bar. This metric indicates whether the trend is gaining or losing momentum.

5. Sortino Ratio and Standard Deviation

- The Sortino Ratio measures risk-adjusted performance by comparing returns to downside volatility (only considering negative price changes).

- Standard Deviation is computed over the lookback period to assess the extent of price fluctuations, offering insights into market stability.

Usage

This indicator is suitable for various time frames and market instruments. Traders can enable or disable specific visual elements such as gradient fills, bar coloring, and signal markers based on their preference. For a minimalist approach, one might choose to display only the primary trend line. For a deeper analysis, enabling multiple tables can provide extensive data on momentum, volatility, trend dynamics, and risk metrics.

Important Note on Risk

Trading involves inherent risk, and no indicator can eliminate the uncertainty of the markets. Past performance is not indicative of future results. It is essential to use proper risk management, test any new tool thoroughly, and consult multiple sources or professional advice before making trading decisions.

Conclusion

Uptrick: Alpha Trend unifies a diverse set of calculations, adaptive smoothing techniques, and customizable visual elements into one powerful tool. By combining the Hull, Exponential, and Weighted Moving Averages, the indicator is able to provide a trend line that is both responsive and smooth, depending on the trading mode. Its advanced color schemes, gradient fills, and detailed data tables deliver a comprehensive analysis of market trends, momentum, and risk. Whether you are a short-term trader or a long-term investor, this indicator aims to clarify price action and assist you in making more informed trading decisions.

[SHORT ONLY] ATR Sell the Rip Mean Reversion Strategy█ STRATEGY DESCRIPTION

The "ATR Sell the Rip Mean Reversion Strategy" is a contrarian system that targets overextended price moves on stocks and ETFs. It calculates an ATR‐based trigger level to identify shorting opportunities. When the current close exceeds this smoothed ATR trigger, and if the close is below a 200-period EMA (if enabled), the strategy initiates a short entry, aiming to profit from an anticipated corrective pullback.

█ HOW IS THE ATR SIGNAL BAND CALCULATED?

This strategy computes an ATR-based signal trigger as follows:

Calculate the ATR

The strategy computes the Average True Range (ATR) using a configurable period provided by the user:

atrValue = ta.atr(atrPeriod)

Determine the Threshold

Multiply the ATR by a predefined multiplier and add it to the current close:

atrThreshold = close + atrValue * atrMultInput

Smooth the Threshold

Apply a Simple Moving Average over a specified period to smooth out the threshold, reducing noise:

signalTrigger = ta.sma(atrThreshold, smoothPeriodInput)

█ SIGNAL GENERATION

1. SHORT ENTRY

A Short Signal is triggered when:

The current close is above the smoothed ATR signal trigger.

The trade occurs within the specified trading window (between Start Time and End Time).

If the EMA filter is enabled, the close must also be below the 200-period EMA.

2. EXIT CONDITION

An exit Signal is generated when the current close falls below the previous bar’s low (close < low ), indicating a potential bearish reversal and prompting the strategy to close its short position.

█ ADDITIONAL SETTINGS

ATR Period: The period used to calculate the ATR, allowing for adaptability to different volatility conditions (default is 20).

ATR Multiplier: The multiplier applied to the ATR to determine the raw threshold (default is 1.0).

Smoothing Period: The period over which the raw ATR threshold is smoothed using an SMA (default is 10).

Start Time and End Time: Defines the time window during which trades are allowed.

EMA Filter (Optional): When enabled, short entries are only executed if the current close is below the 200-period EMA, confirming a bearish trend.

█ PERFORMANCE OVERVIEW

This strategy is designed for use on the Daily timeframe, targeting stocks and ETFs by capitalizing on overextended price moves.

It utilizes a dynamic, ATR-based trigger to identify when prices have potentially peaked, setting the stage for a mean reversion short entry.

The optional EMA filter helps align trades with broader market trends, potentially reducing false signals.

Backtesting is recommended to fine-tune the ATR multiplier, smoothing period, and EMA settings to match the volatility and behavior of specific markets.

MTF Signal XpertMTF Signal Xpert – Detailed Description

Overview:

MTF Signal Xpert is a proprietary, open‑source trading signal indicator that fuses multiple technical analysis methods into one cohesive strategy. Developed after rigorous backtesting and extensive research, this advanced tool is designed to deliver clear BUY and SELL signals by analyzing trend, momentum, and volatility across various timeframes. Its integrated approach not only enhances signal reliability but also incorporates dynamic risk management, helping traders protect their capital while navigating complex market conditions.

Detailed Explanation of How It Works:

Trend Detection via Moving Averages

Dual Moving Averages:

MTF Signal Xpert computes two moving averages—a fast MA and a slow MA—with the flexibility to choose from Simple (SMA), Exponential (EMA), or Hull (HMA) methods. This dual-MA system helps identify the prevailing market trend by contrasting short-term momentum with longer-term trends.

Crossover Logic:

A BUY signal is initiated when the fast MA crosses above the slow MA, coupled with the condition that the current price is above the lower Bollinger Band. This suggests that the market may be emerging from a lower price region. Conversely, a SELL signal is generated when the fast MA crosses below the slow MA and the price is below the upper Bollinger Band, indicating potential bearish pressure.

Recent Crossover Confirmation:

To ensure that signals reflect current market dynamics, the script tracks the number of bars since the moving average crossover event. Only crossovers that occur within a user-defined “candle confirmation” period are considered, which helps filter out outdated signals and improves overall signal accuracy.

Volatility and Price Extremes with Bollinger Bands

Calculation of Bands:

Bollinger Bands are calculated using a 20‑period simple moving average as the central basis, with the upper and lower bands derived from a standard deviation multiplier. This creates dynamic boundaries that adjust according to recent market volatility.

Signal Reinforcement:

For BUY signals, the condition that the price is above the lower Bollinger Band suggests an undervalued market condition, while for SELL signals, the price falling below the upper Bollinger Band reinforces the bearish bias. This volatility context adds depth to the moving average crossover signals.

Momentum Confirmation Using Multiple Oscillators

RSI (Relative Strength Index):

The RSI is computed over 14 periods to determine if the market is in an overbought or oversold state. Only readings within an optimal range (defined by user inputs) validate the signal, ensuring that entries are made during balanced conditions.

MACD (Moving Average Convergence Divergence):

The MACD line is compared with its signal line to assess momentum. A bullish scenario is confirmed when the MACD line is above the signal line, while a bearish scenario is indicated when it is below, thus adding another layer of confirmation.

Awesome Oscillator (AO):

The AO measures the difference between short-term and long-term simple moving averages of the median price. Positive AO values support BUY signals, while negative values back SELL signals, offering additional momentum insight.

ADX (Average Directional Index):

The ADX quantifies trend strength. MTF Signal Xpert only considers signals when the ADX value exceeds a specified threshold, ensuring that trades are taken in strongly trending markets.

Optional Stochastic Oscillator:

An optional stochastic oscillator filter can be enabled to further refine signals. It checks for overbought conditions (supporting SELL signals) or oversold conditions (supporting BUY signals), thus reducing ambiguity.

Multi-Timeframe Verification

Higher Timeframe Filter:

To align short-term signals with broader market trends, the script calculates an EMA on a higher timeframe as specified by the user. This multi-timeframe approach helps ensure that signals on the primary chart are consistent with the overall trend, thereby reducing false signals.

Dynamic Risk Management with ATR

ATR-Based Calculations:

The Average True Range (ATR) is used to measure current market volatility. This value is multiplied by a user-defined factor to dynamically determine stop loss (SL) and take profit (TP) levels, adapting to changing market conditions.

Visual SL/TP Markers:

The calculated SL and TP levels are plotted on the chart as distinct colored dots, enabling traders to quickly identify recommended exit points.

Optional Trailing Stop:

An optional trailing stop feature is available, which adjusts the stop loss as the trade moves favorably, helping to lock in profits while protecting against sudden reversals.

Risk/Reward Ratio Calculation:

MTF Signal Xpert computes a risk/reward ratio based on the dynamic SL and TP levels. This quantitative measure allows traders to assess whether the potential reward justifies the risk associated with a trade.

Condition Weighting and Signal Scoring

Binary Condition Checks:

Each technical condition—ranging from moving average crossovers, Bollinger Band positioning, and RSI range to MACD, AO, ADX, and volume filters—is assigned a binary score (1 if met, 0 if not).

Cumulative Scoring:

These individual scores are summed to generate cumulative bullish and bearish scores, quantifying the overall strength of the signal and providing traders with an objective measure of its viability.

Detailed Signal Explanation:

A comprehensive explanation string is generated, outlining which conditions contributed to the current BUY or SELL signal. This explanation is displayed on an on‑chart dashboard, offering transparency and clarity into the signal generation process.

On-Chart Visualizations and Debug Information

Chart Elements:

The indicator plots all key components—moving averages, Bollinger Bands, SL and TP markers—directly on the chart, providing a clear visual framework for understanding market conditions.

Combined Dashboard:

A dedicated dashboard displays key metrics such as RSI, ADX, and the bullish/bearish scores, alongside a detailed explanation of the current signal. This consolidated view allows traders to quickly grasp the underlying logic.

Debug Table (Optional):

For advanced users, an optional debug table is available. This table breaks down each individual condition, indicating which criteria were met or not met, thus aiding in further analysis and strategy refinement.

Mashup Justification and Originality

MTF Signal Xpert is more than just an aggregation of existing indicators—it is an original synthesis designed to address real-world trading complexities. Here’s how its components work together:

Integrated Trend, Volatility, and Momentum Analysis:

By combining moving averages, Bollinger Bands, and multiple oscillators (RSI, MACD, AO, ADX, and an optional stochastic), the indicator captures diverse market dynamics. Each component reinforces the others, reducing noise and filtering out false signals.

Multi-Timeframe Analysis:

The inclusion of a higher timeframe filter aligns short-term signals with longer-term trends, enhancing overall reliability and reducing the potential for contradictory signals.

Adaptive Risk Management:

Dynamic stop loss and take profit levels, determined using ATR, ensure that the risk management strategy adapts to current market conditions. The optional trailing stop further refines this approach, protecting profits as the market evolves.

Quantitative Signal Scoring:

The condition weighting system provides an objective measure of signal strength, giving traders clear insight into how each technical component contributes to the final decision.

How to Use MTF Signal Xpert:

Input Customization:

Adjust the moving average type and period settings, ATR multipliers, and oscillator thresholds to align with your trading style and the specific market conditions.

Enable or disable the optional stochastic oscillator and trailing stop based on your preference.

Interpreting the Signals:

When a BUY or SELL signal appears, refer to the on‑chart dashboard, which displays key metrics (e.g., RSI, ADX, bullish/bearish scores) along with a detailed breakdown of the conditions that triggered the signal.

Review the SL and TP markers on the chart to understand the associated risk/reward setup.

Risk Management:

Use the dynamically calculated stop loss and take profit levels as guidelines for setting your exit points.

Evaluate the provided risk/reward ratio to ensure that the potential reward justifies the risk before entering a trade.

Debugging and Verification: