Dynamic RSI Mean Reversion StrategyDynamic RSI Mean Reversion Strategy

Overview:

This strategy uses an RSI with ATR-Adjusted OB/OS levels in order to enhance the quality of it's mean reversion trades. It also incorporates a form of trend filtering in an effort to minimize downside and maximize upside. The backtest has fewer trades, as it uses substantial filtering to enhance trade quality. As you can see, I didn't cherry pick the results, so the results aren't the most beautiful thing you'll see in your life. I did this to ensure nobody gets misled. If you need a higher frequency of trades, consider removing the trend filter or increasing the length of the EMAs used for trend detection.

Features:

Dynamic OB/OS Levels: Uses ATR to adjust overbought and oversold thresholds dynamically, making the RSI more responsive in varying volatility conditions. This approach enhances signal strength by expanding the RSI range in high volatility and tightening it in low volatility.

Mean Reversion Focus: Designed for mean reversion but incorporates a trend-following filter to reduce countertrend trades. When the RSI is high, it often indicates an uptrend, so a trend filter prevents shorting in these cases and the same goes for downtrends and longing.

Trend Filtering: A moving average cross trend filter checks for the trend direction, with the RSI signal line color-coded to reflect trend shifts. Entries occur when the RSI crosses above or below the dynamic thresholds and is not a countertrend trade.

Stop Losses: Stop losses are set based on ATR distance from the entry price, providing volatility-adjusted protection.

Note:

If you're using this strategy on assets with a higher price, remember to increase the initial capital in the strategy settings. Otherwise, the strategy won't generate any (or many) trades and you'll end up with some inaccurate results.

Recommended Use:

Test it on different assets and timeframes. I’ve found the best results with standard RSI inputs, a relatively slow ATR, and a slower MA cross for trend filtering. Thus, the defaults are set that way. If the trend metrics are too slow, you’ll filter out too many good trades while allowing crummy ones; if too fast, most trades may be filtered out. As always, this has a lot of configurability so experiment to find the balance that works for your trading style.

Average True Range (ATR)

Fibonacci ATR Fusion - Strategy [presentTrading]Open-script again! This time is also an ATR-related strategy. Enjoy! :)

If you have any questions, let me know, and I'll help make this as effective as possible.

█ Introduction and How It Is Different

The Fibonacci ATR Fusion Strategy is an advanced trading approach that uniquely integrates Fibonacci-based weighted averages with the Average True Range (ATR) to identify and capitalize on significant market trends.

Unlike traditional strategies that rely on single indicators or static parameters, this method combines multiple timeframes and dynamic volatility measurements to enhance precision and adaptability. Additionally, it features a 4-step Take Profit (TP) mechanism, allowing for systematic profit-taking at various levels, which optimizes both risk management and return potential in long and short market positions.

BTCUSD 6hr Performance

█ Strategy, How It Works: Detailed Explanation

The Fibonacci ATR Fusion Strategy utilizes a combination of technical indicators and weighted averages to determine optimal entry and exit points. Below is a breakdown of its key components and operational logic.

🔶 1. Enhanced True Range Calculation

The strategy begins by calculating the True Range (TR) to measure market volatility accurately.

TR = max(High - Low, abs(High - Previous Close), abs(Low - Previous Close))

High and Low: Highest and lowest prices of the current trading period.

Previous Close: Closing price of the preceding trading period.

max: Selects the largest value among the three calculations to account for gaps and limit movements.

🔶 2. Buying Pressure (BP) Calculation

Buying Pressure (BP) quantifies the extent to which buyers are driving the price upwards within a period.

BP = Close - True Low

Close: Current period's closing price.

True Low: The lower boundary determined in the True Range calculation.

🔶 3. Ratio Calculation for Different Periods

To assess the strength of buying pressure relative to volatility, the strategy calculates a ratio over various Fibonacci-based timeframes.

Ratio = 100 * (Sum of BP over n periods) / (Sum of TR over n periods)

n: Length of the period (e.g., 8, 13, 21, 34, 55).

Sum of BP: Cumulative Buying Pressure over n periods.

Sum of TR: Cumulative True Range over n periods.

This ratio normalizes buying pressure, making it comparable across different timeframes.

🔶 4. Weighted Average Calculation

The strategy employs a weighted average of ratios from multiple Fibonacci-based periods to smooth out signals and enhance trend detection.

Weighted Avg = (w1 * Ratio_p1 + w2 * Ratio_p2 + w3 * Ratio_p3 + w4 * Ratio_p4 + Ratio_p5) / (w1 + w2 + w3 + w4 + 1)

w1, w2, w3, w4: Weights assigned to each ratio period.

Ratio_p1 to Ratio_p5: Ratios calculated for periods p1 to p5 (e.g., 8, 13, 21, 34, 55).

This weighted approach emphasizes shorter periods more heavily, capturing recent market dynamics while still considering longer-term trends.

🔶 5. Simple Moving Average (SMA) of Weighted Average

To further smooth the weighted average and reduce noise, a Simple Moving Average (SMA) is applied.

Weighted Avg SMA = SMA(Weighted Avg, m)

- m: SMA period (e.g., 3).

This smoothed line serves as the primary signal generator for trade entries and exits.

🔶 6. Trading Condition Thresholds

The strategy defines specific threshold values to determine optimal entry and exit points based on crossovers and crossunders of the SMA.

Long Condition = Crossover(Weighted Avg SMA, Long Entry Threshold)

Short Condition = Crossunder(Weighted Avg SMA, Short Entry Threshold)

Long Exit = Crossunder(Weighted Avg SMA, Long Exit Threshold)

Short Exit = Crossover(Weighted Avg SMA, Short Exit Threshold)

Long Entry Threshold (T_LE): Level at which a long position is triggered.

Short Entry Threshold (T_SE): Level at which a short position is triggered.

Long Exit Threshold (T_LX): Level at which a long position is exited.

Short Exit Threshold (T_SX): Level at which a short position is exited.

These conditions ensure that trades are only executed when clear trends are identified, enhancing the strategy's reliability.

Previous local performance

🔶 7. ATR-Based Take Profit Mechanism

When enabled, the strategy employs a 4-step Take Profit system to systematically secure profits as the trade moves in the desired direction.

TP Price_1 Long = Entry Price + (TP1ATR * ATR Value)

TP Price_2 Long = Entry Price + (TP2ATR * ATR Value)

TP Price_3 Long = Entry Price + (TP3ATR * ATR Value)

TP Price_1 Short = Entry Price - (TP1ATR * ATR Value)

TP Price_2 Short = Entry Price - (TP2ATR * ATR Value)

TP Price_3 Short = Entry Price - (TP3ATR * ATR Value)

- ATR Value: Calculated using ATR over a specified period (e.g., 14).

- TPxATR: User-defined multipliers for each take profit level.

- TPx_percent: Percentage of the position to exit at each TP level.

This multi-tiered exit strategy allows for partial position closures, optimizing profit capture while maintaining exposure to potential further gains.

█ Trade Direction

The Fibonacci ATR Fusion Strategy is designed to operate in both long and short market conditions, providing flexibility to traders in varying market environments.

Long Trades: Initiated when the SMA of the weighted average crosses above the Long Entry Threshold (T_LE), indicating strong upward momentum.

Short Trades: Initiated when the SMA of the weighted average crosses below the Short Entry Threshold (T_SE), signaling robust downward momentum.

Additionally, the strategy can be configured to trade exclusively in one direction—Long, Short, or Both—based on the trader’s preference and market analysis.

█ Usage

Implementing the Fibonacci ATR Fusion Strategy involves several steps to ensure it aligns with your trading objectives and market conditions.

1. Configure Strategy Parameters:

- Trading Direction: Choose between Long, Short, or Both based on your market outlook.

- Trading Condition Thresholds: Set the Long Entry, Short Entry, Long Exit, and Short Exit thresholds to define when to enter and exit trades.

2. Set Take Profit Levels (if enabled):

- ATR Multipliers: Define how many ATRs away from the entry price each take profit level is set.

- Take Profit Percentages: Allocate what percentage of the position to close at each TP level.

3. Apply to Desired Chart:

- Add the strategy to the chart of the asset you wish to trade.

- Observe the plotted Fibonacci ATR and SMA Fibonacci ATR indicators for visual confirmation.

4. Monitor and Adjust:

- Regularly review the strategy’s performance through backtesting.

- Adjust the input parameters based on historical performance and changing market dynamics.

5. Risk Management:

- Ensure that the sum of take profit percentages does not exceed 100% to avoid over-closing positions.

- Utilize the ATR-based TP levels to adapt to varying market volatilities, maintaining a balanced risk-reward ratio.

█ Default Settings

Understanding the default settings is crucial for optimizing the Fibonacci ATR Fusion Strategy's performance. Here's a precise and simple overview of the key parameters and their effects:

🔶 Key Parameters and Their Effects

1. Trading Direction (`tradingDirection`)

- Default: Both

- Effect: Determines whether the strategy takes both long and short positions or restricts to one direction. Selecting Both allows maximum flexibility, while Long or Short can be used for directional bias.

2. Trading Condition Thresholds

Long Entry (long_entry_threshold = 58.0): Higher values reduce false positives but may miss trades.

Short Entry (short_entry_threshold = 42.0): Lower values capture early short trends but may increase false signals.

Long Exit (long_exit_threshold = 42.0): Exits long positions early, securing profits but potentially cutting trends short.

Short Exit (short_exit_threshold = 58.0): Delays short exits to capture favorable movements, avoiding premature exits.

3. Take Profit Configuration (`useTakeProfit` = false)

- Effect: When enabled, the strategy employs a 4-step TP mechanism to secure profits at multiple levels. By default, it is disabled to allow users to opt-in based on their trading style.

4. ATR-Based Take Profit Multipliers

TP1 (tp1ATR = 3.0): Sets the first TP at 3 ATRs for initial profit capture.

TP2 (tp2ATR = 8.0): Targets larger trends, though less likely to be reached.

TP3 (tp3ATR = 14.0): Optimizes for extreme price moves, seldom triggered.

5. Take Profit Percentages

TP Level 1 (tp1_percent = 12%): Secures 12% at the first TP.

TP Level 2 (tp2_percent = 12%): Exits another 12% at the second TP.

TP Level 3 (tp3_percent = 12%): Closes an additional 12% at the third TP.

6. Weighted Average Parameters

Ratio Periods: Fibonacci-based intervals (8, 13, 21, 34, 55) balance responsiveness.

Weights: Emphasizes recent data for timely responses to market trends.

SMA Period (weighted_avg_sma_period = 3): Smoothens data with minimal lag, balancing noise reduction and responsiveness.

7. ATR Period (`atrPeriod` = 14)

Effect: Sets the ATR calculation length, impacting TP sensitivity to volatility.

🔶 Impact on Performance

- Sensitivity and Responsiveness:

- Shorter Ratio Periods and Higher Weights: Make the weighted average more responsive to recent price changes, allowing quicker trade entries and exits but increasing the likelihood of false signals.

- Longer Ratio Periods and Lower Weights: Provide smoother signals with fewer false positives but may delay trade entries, potentially missing out on significant price moves.

- Profit Taking:

- ATR Multipliers: Higher multipliers set take profit levels further away, targeting larger price movements but reducing the probability of reaching these levels.

- Fixed Percentages: Allocating equal percentages at each TP level ensures consistent profit realization and risk management, preventing overexposure.

- Trade Direction Control:

- Selecting Specific Directions: Restricting trades to Long or Short can align the strategy with market trends or personal biases, potentially enhancing performance in trending markets.

- Risk Management:

- Take Profit Percentages: Dividing the position into smaller percentages at multiple TP levels helps lock in profits progressively, reducing risk and allowing the remaining position to ride further trends.

- Market Adaptability:

- Weighted Averages and ATR: By combining multiple timeframes and adjusting to volatility, the strategy adapts to different market conditions, maintaining effectiveness across various asset classes and timeframes.

---

If you want to know more about ATR, can also check "SuperATR 7-Step Profit".

Enjoy trading.

XAUUSD 10-Minute StrategyThis XAUUSD 10-Minute Strategy is designed for trading Gold vs. USD on a 10-minute timeframe. By combining multiple technical indicators (MACD, RSI, Bollinger Bands, and ATR), the strategy effectively captures both trend-following and reversal opportunities, with adaptive risk management for varying market volatility. This approach balances high-probability entries with robust volatility management, making it suitable for traders seeking to optimise entries during significant price movements and reversals.

Key Components and Logic:

MACD (12, 26, 9):

Generates buy signals on MACD Line crossovers above the Signal Line and sell signals on crossovers below the Signal Line, helping to capture momentum shifts.

RSI (14):

Utilizes oversold (below 35) and overbought (above 65) levels as a secondary filter to validate entries and avoid overextended price zones.

Bollinger Bands (20, 2):

Uses upper and lower Bollinger Bands to identify potential overbought and oversold conditions, aiming to enter long trades near the lower band and short trades near the upper band.

ATR-Based Stop Loss and Take Profit:

Stop Loss and Take Profit levels are dynamically set as multiples of ATR (3x for stop loss, 5x for take profit), ensuring flexibility with market volatility to optimise exit points.

Entry & Exit Conditions:

Buy Entry: T riggered when any of the following conditions are met:

MACD Line crosses above the Signal Line

RSI is oversold

Price drops below the lower Bollinger Band

Sell Entry: Triggered when any of the following conditions are met:

MACD Line crosses below the Signal Line

RSI is overbought

Price moves above the upper Bollinger Band

Exit Strategy: Trades are closed based on opposing entry signals, with adaptive spread adjustments for realistic exit points.

Backtesting Configuration & Results:

Backtesting Period: July 21, 2024, to October 30, 2024

Symbol Info: XAUUSD, 10-minute timeframe, OANDA data source

Backtesting Capital: Initial capital of $700, with each trade set to 10 contracts (equivalent to approximately 0.1 lots based on the broker’s contract size for gold).

Users should confirm their broker's contract size for gold, as this may differ. This script uses 10 contracts for backtesting purposes, aligned with 0.1 lots on brokers offering a 100-contract specification.

Key Backtesting Performance Metrics:

Net Profit: $4,733.90 USD (676.27% increase)

Total Closed Trades: 526

Win Rate: 53.99%

Profit Factor: 1.44 (1.96 for Long trades, 1.14 for Short trades)

Max Drawdown: $819.75 USD (56.33% of equity)

Sharpe Ratio: 1.726

Average Trade: $9.00 USD (0.04% of equity per trade)

This backtest reflects realistic conditions, with a spread adjustment of 38 points and no slippage or commission applied. The settings aim to simulate typical retail trading conditions. However, please adjust the initial capital, contract size, and other settings based on your account specifics for best results.

Usage:

This strategy is tuned specifically for XAUUSD on a 10-minute timeframe, ideal for both trend-following and reversal trades. The ATR-based stop loss and take profit levels adapt dynamically to market volatility, optimising entries and exits in varied conditions. To backtest this script accurately, ensure your broker’s contract specifications for gold align with the parameters used in this strategy.

SuperATR 7-Step Profit - Strategy [presentTrading] Long time no see!

█ Introduction and How It Is Different

The SuperATR 7-Step Profit Strategy is a multi-layered trading approach that integrates adaptive Average True Range (ATR) calculations with momentum-based trend detection. What sets this strategy apart is its sophisticated 7-step take-profit mechanism, which combines four ATR-based exit levels and three fixed percentage levels. This hybrid approach allows traders to dynamically adjust to market volatility while systematically capturing profits in both long and short market positions.

Traditional trading strategies often rely on static indicators or single-layered exit strategies, which may not adapt well to changing market conditions. The SuperATR 7-Step Profit Strategy addresses this limitation by:

- Using Adaptive ATR: Enhances the standard ATR by making it responsive to current market momentum.

- Incorporating Momentum-Based Trend Detection: Identifies stronger trends with higher probability of continuation.

- Employing a Multi-Step Take-Profit System: Allows for gradual profit-taking at predetermined levels, optimizing returns while minimizing risk.

BTCUSD 6hr Performance

█ Strategy, How It Works: Detailed Explanation

The strategy revolves around detecting strong market trends and capitalizing on them using an adaptive ATR and momentum indicators. Below is a detailed breakdown of each component of the strategy.

🔶 1. True Range Calculation with Enhanced Volatility Detection

The True Range (TR) measures market volatility by considering the most significant price movements. The enhanced TR is calculated as:

TR = Max

Where:

High and Low are the current bar's high and low prices.

Previous Close is the closing price of the previous bar.

Abs denotes the absolute value.

Max selects the maximum value among the three calculations.

🔶 2. Momentum Factor Calculation

To make the ATR adaptive, the strategy incorporates a Momentum Factor (MF), which adjusts the ATR based on recent price movements.

Momentum = Close - Close

Stdev_Close = Standard Deviation of Close over n periods

Normalized_Momentum = Momentum / Stdev_Close (if Stdev_Close ≠ 0)

Momentum_Factor = Abs(Normalized_Momentum)

Where:

Close is the current closing price.

n is the momentum_period, a user-defined input (default is 7).

Standard Deviation measures the dispersion of closing prices over n periods.

Abs ensures the momentum factor is always positive.

🔶 3. Adaptive ATR Calculation

The Adaptive ATR (AATR) adjusts the traditional ATR based on the Momentum Factor, making it more responsive during volatile periods and smoother during consolidation.

Short_ATR = SMA(True Range, short_period)

Long_ATR = SMA(True Range, long_period)

Adaptive_ATR = /

Where:

SMA is the Simple Moving Average.

short_period and long_period are user-defined inputs (defaults are 3 and 7, respectively).

🔶 4. Trend Strength Calculation

The strategy quantifies the strength of the trend to filter out weak signals.

Price_Change = Close - Close

ATR_Multiple = Price_Change / Adaptive_ATR (if Adaptive_ATR ≠ 0)

Trend_Strength = SMA(ATR_Multiple, n)

🔶 5. Trend Signal Determination

If (Short_MA > Long_MA) AND (Trend_Strength > Trend_Strength_Threshold):

Trend_Signal = 1 (Strong Uptrend)

Elif (Short_MA < Long_MA) AND (Trend_Strength < -Trend_Strength_Threshold):

Trend_Signal = -1 (Strong Downtrend)

Else:

Trend_Signal = 0 (No Clear Trend)

🔶 6. Trend Confirmation with Price Action

Adaptive_ATR_SMA = SMA(Adaptive_ATR, atr_sma_period)

If (Trend_Signal == 1) AND (Close > Short_MA) AND (Adaptive_ATR > Adaptive_ATR_SMA):

Trend_Confirmed = True

Elif (Trend_Signal == -1) AND (Close < Short_MA) AND (Adaptive_ATR > Adaptive_ATR_SMA):

Trend_Confirmed = True

Else:

Trend_Confirmed = False

Local Performance

🔶 7. Multi-Step Take-Profit Mechanism

The strategy employs a 7-step take-profit system

█ Trade Direction

The SuperATR 7-Step Profit Strategy is designed to work in both long and short market conditions. By identifying strong uptrends and downtrends, it allows traders to capitalize on price movements in either direction.

Long Trades: Initiated when the market shows strong upward momentum and the trend is confirmed.

Short Trades: Initiated when the market exhibits strong downward momentum and the trend is confirmed.

█ Usage

To implement the SuperATR 7-Step Profit Strategy:

1. Configure the Strategy Parameters:

- Adjust the short_period, long_period, and momentum_period to match the desired sensitivity.

- Set the trend_strength_threshold to control how strong a trend must be before acting.

2. Set Up the Multi-Step Take-Profit Levels:

- Define ATR multipliers and fixed percentage levels according to risk tolerance and profit goals.

- Specify the percentage of the position to close at each level.

3. Apply the Strategy to a Chart:

- Use the strategy on instruments and timeframes where it has been tested and optimized.

- Monitor the positions and adjust parameters as needed based on performance.

4. Backtest and Optimize:

- Utilize TradingView's backtesting features to evaluate historical performance.

- Adjust the default settings to optimize for different market conditions.

█ Default Settings

Understanding default settings is crucial for optimal performance.

Short Period (3): Affects the responsiveness of the short-term MA.

Effect: Lower values increase sensitivity but may produce more false signals.

Long Period (7): Determines the trend baseline.

Effect: Higher values reduce noise but may delay signals.

Momentum Period (7): Influences adaptive ATR and trend strength.

Effect: Shorter periods react quicker to price changes.

Trend Strength Threshold (0.5): Filters out weaker trends.

Effect: Higher thresholds yield fewer but stronger signals.

ATR Multipliers: Set distances for ATR-based exits.

Effect: Larger multipliers aim for bigger moves but may reduce hit rate.

Fixed TP Levels (%): Control profit-taking on smaller moves.

Effect: Adjusting these levels affects how quickly profits are realized.

Exit Percentages: Determine how much of the position is closed at each TP level.

Effect: Higher percentages reduce exposure faster, affecting risk and reward.

Adjusting these variables allows you to tailor the strategy to different market conditions and personal risk preferences.

By integrating adaptive indicators and a multi-tiered exit strategy, the SuperATR 7-Step Profit Strategy offers a versatile tool for traders seeking to navigate varying market conditions effectively. Understanding and adjusting the key parameters enables traders to harness the full potential of this strategy.

Simple RSI stock Strategy [1D] The "Simple RSI Stock Strategy " is designed to long-term traders. Strategy uses a daily time frame to capitalize on signals generated by the Relative Strength Index (RSI) and the Simple Moving Average (SMA). This strategy is suitable for low-leverage trading environments and focuses on identifying potential buy opportunities when the market is oversold, while incorporating strong risk management with both dynamic and static Stop Loss mechanisms.

This strategy is recommended for use with a relatively small amount of capital and is best applied by diversifying across multiple stocks in a strong uptrend, particularly in the S&P 500 stock market. It is specifically designed for equities, and may not perform well in other markets such as commodities, forex, or cryptocurrencies, where different market dynamics and volatility patterns apply.

Indicators Used in the Strategy:

1. RSI (Relative Strength Index):

- The RSI is a momentum oscillator used to identify overbought and oversold conditions in the market.

- This strategy enters long positions when the RSI drops below the oversold level (default: 30), indicating a potential buying opportunity.

- It focuses on oversold conditions but uses a filter (SMA 200) to ensure trades are only made in the context of an overall uptrend.

2. SMA 200 (Simple Moving Average):

- The 200-period SMA serves as a trend filter, ensuring that trades are only executed when the price is above the SMA, signaling a bullish market.

- This filter helps to avoid entering trades in a downtrend, thereby reducing the risk of holding positions in a declining market.

3. ATR (Average True Range):

- The ATR is used to measure market volatility and is instrumental in setting the Stop Loss.

- By multiplying the ATR value by a custom multiplier (default: 1.5), the strategy dynamically adjusts the Stop Loss level based on market volatility, allowing for flexibility in risk management.

How the Strategy Works:

Entry Signals:

The strategy opens long positions when RSI indicates that the market is oversold (below 30), and the price is above the 200-period SMA. This ensures that the strategy buys into potential market bottoms within the context of a long-term uptrend.

Take Profit Levels:

The strategy defines three distinct Take Profit (TP) levels:

TP 1: A 5% from the entry price.

TP 2: A 10% from the entry price.

TP 3: A 15% from the entry price.

As each TP level is reached, the strategy closes portions of the position to secure profits: 33% of the position is closed at TP 1, 66% at TP 2, and 100% at TP 3.

Visualizing Target Points:

The strategy provides visual feedback by plotting plotshapes at each Take Profit level (TP 1, TP 2, TP 3). This allows traders to easily see the target profit levels on the chart, making it easier to monitor and manage positions as they approach key profit-taking areas.

Stop Loss Mechanism:

The strategy uses a dual Stop Loss system to effectively manage risk:

ATR Trailing Stop: This dynamic Stop Loss adjusts based on the ATR value and trails the price as the position moves in the trader’s favor. If a price reversal occurs and the market begins to trend downward, the trailing stop closes the position, locking in gains or minimizing losses.

Basic Stop Loss: Additionally, a fixed Stop Loss is set at 25%, limiting potential losses. This basic Stop Loss serves as a safeguard, automatically closing the position if the price drops 25% from the entry point. This higher Stop Loss is designed specifically for low-leverage trading, allowing more room for market fluctuations without prematurely closing positions.

to determine the level of stop loss and target point I used a piece of code by RafaelZioni, here is the script from which a piece of code was taken

Together, these mechanisms ensure that the strategy dynamically manages risk while offering robust protection against significant losses in case of sharp market downturns.

The position size has been estimated by me at 75% of the total capital. For optimal capital allocation, a recommended value based on the Kelly Criterion, which is calculated to be 59.13% of the total capital per trade, can also be considered.

Enjoy !

Crypto Volatility Bitcoin Correlation Strategy Description:

The Crypto Volatility Bitcoin Correlation Strategy is designed to leverage market volatility specifically in Bitcoin (BTC) using a combination of volatility indicators and trend-following techniques. This strategy utilizes the VIXFix (a volatility indicator adapted for crypto markets) and the BVOL7D (Bitcoin 7-Day Volatility Index from BitMEX) to identify periods of high volatility, while confirming trends with the Exponential Moving Average (EMA). These components work together to offer a comprehensive system that traders can use to enter positions when volatility and trends are aligned in their favor.

Key Features:

VIXFix (Volatility Index for Crypto Markets): This indicator measures the highest price of Bitcoin over a set period and compares it with the current low price to gauge market volatility. A rise in VIXFix indicates increasing market volatility, signaling that large price movements could occur.

BVOL7D (Bitcoin 7-Day Volatility Index): This volatility index, provided by BitMEX, measures the volatility of Bitcoin over the past 7 days. It helps traders monitor the recent volatility trend in the market, particularly useful when making short-term trading decisions.

Exponential Moving Average (EMA): The 50-period EMA acts as a trend indicator. When the price is above the EMA, it suggests the market is in an uptrend, and when the price is below the EMA, it suggests a downtrend.

How It Works:

Long Entry: A long position is triggered when both the VIXFix and BVOL7D indicators are rising, signaling increased volatility, and the price is above the 50-period EMA, confirming that the market is trending upward.

Exit: The strategy exits the position when the price crosses below the 50-period EMA, which signals a potential weakening of the uptrend and a decrease in volatility.

This strategy ensures that traders only enter positions when the volatility aligns with a clear trend, minimizing the risk of entering trades during periods of market uncertainty.

Testing and Timeframe:

This strategy has been tested on Bitcoin using the daily timeframe, which provides a longer-term perspective on market trends and volatility. However, users can adjust the timeframe according to their trading preferences. It is crucial to note that this strategy does not include comprehensive risk management, aside from the exit condition when the price crosses below the EMA. Users are strongly advised to implement their own risk management techniques, such as setting appropriate stop-loss levels, to safeguard their positions during high volatility periods.

Utility:

The Crypto Volatility Bitcoin Correlation Strategy is particularly well-suited for traders who aim to capitalize on the high volatility often seen in the Bitcoin market. By combining volatility measurements (VIXFix and BVOL7D) with a trend-following mechanism (EMA), this strategy helps identify optimal moments for entering and exiting trades. This approach ensures that traders participate in potentially profitable market moves while minimizing exposure during times of uncertainty.

Use Cases:

Volatility-Based Entries: Traders looking to take advantage of market volatility spikes will find this strategy useful for timing entry points during market swings.

Trend Confirmation: By using the EMA as a confirmation tool, traders can avoid entering trades that go against the trend, which can result in significant losses during volatile market conditions.

Risk Management: While the strategy exits when price falls below the EMA, it is important to recognize that this is not a full risk management system. Traders should use caution and integrate additional risk measures, such as stop-losses and position sizing, to better manage potential losses.

How to Use:

Step 1: Monitor the VIXFix and BVOL7D indicators. When both are rising and the Bitcoin price is above the EMA, the strategy will trigger a long entry, indicating that the market is experiencing increased volatility with a confirmed uptrend.

Step 2: Exit the position when the price drops below the 50-period EMA, signaling that the trend may be reversing or weakening, reducing the likelihood of continued upward price movement.

This strategy is open-source and is intended to help traders navigate volatile market conditions, particularly in Bitcoin, using proven indicators for volatility and trend confirmation.

Risk Disclaimer:

This strategy has been tested on the daily timeframe of Bitcoin, but users should be aware that it does not include built-in risk management except for the below-EMA exit condition. Users should be extremely cautious when using this strategy and are encouraged to implement their own risk management, such as using stop-losses, position sizing, and setting appropriate limits. Trading involves significant risk, and this strategy does not guarantee profits or prevent losses. Past performance is not indicative of future results. Always test any strategy in a demo environment before applying it to live markets.

Trend Signals with TP & SL [UAlgo] StrategyThe "Trend Signals with TP & SL Strategy" is a trading strategy designed to capture trend continuation signals while incorporating sophisticated risk management techniques. This strategy is tailored for traders who wish to capitalize on trending market conditions with precise entry and exit points, automatically calculating Take Profit (TP) and Stop Loss (SL) levels based on either Average True Range (ATR) or percentage values. The strategy aims to enhance trade management by preventing multiple simultaneous positions and dynamically adapting to changing market conditions.

This strategy is highly configurable, allowing traders to adjust sensitivity, the ATR calculation method, and the cloud moving average length. Additionally, the strategy can display buy and sell signals directly on the chart, along with visual representation of entry points, stop losses, and take profits. It also features a cloud-based trend analysis using a MACD-driven color fill that indicates the strength and direction of the trend.

🔶 Key Features

Configurable Trend Continuation Signals:

Source Selection: The strategy uses the midpoint of the high-low range as the default source, but it is adjustable.

Sensitivity: The sensitivity of the trend signals can be adjusted using a multiplier, ranging from 0.5 to 5.

ATR Calculation: The strategy allows users to choose between two ATR calculation methods for better adaptability to different market conditions.

Cloud Moving Average: Traders can adjust the cloud moving average length, which is used in conjunction with MACD to provide a visual trend indication.

Take Profit & Stop Loss Management:

ATR-Based or Percent-Based: The strategy offers flexibility in setting TP and SL levels, allowing traders to choose between ATR-based multipliers or fixed percentage values.

Dynamic Adjustment: TP and SL levels are dynamically adjusted according to the selected method, ensuring trades are managed based on real-time market conditions.

Prevention of Multiple Positions:

Single Position Control: To reduce risk and enhance strategy reliability, the strategy includes an option to prevent multiple positions from being opened simultaneously.

Visual Trade Indicators:

Buy/Sell Signals: Clearly displays buy and sell signals on the chart for easy interpretation.

Entry, SL, and TP Lines: Draws lines for entry price, stop loss, and take profit directly on the chart, helping traders to monitor trades visually.

Trend Cloud: A color-filled cloud based on MACD and the cloud moving average provides a visual cue of the trend’s direction and strength.

Performance Summary Table:

In-Chart Statistics: A table in the top right of the chart displays key performance metrics, including total trades, wins, losses, and win rate percentage, offering a quick overview of the strategy’s effectiveness.

🔶 Interpreting the Indicator

Trend Signals: The strategy identifies trend continuation signals based on price action relative to an ATR-based threshold. A buy signal is generated when the price crosses above a key level, indicating an uptrend. Conversely, a sell signal occurs when the price crosses below a level, signaling a downtrend.

Cloud Visualization: The cloud, derived from MACD and moving averages, changes color to reflect the current trend. A positive cloud in aqua suggests an uptrend, while a red cloud indicates a downtrend. The transparency of the cloud offers further nuance, with more solid colors denoting stronger trends.

Entry and Exit Management: Once a trend signal is generated, the strategy automatically sets TP and SL levels based on your chosen method (ATR or percentage). The stop loss and take profit lines will appear on the chart, showing where the strategy will exit the trade. If the price reaches either the SL or TP, the trade is closed, and the respective line is deleted from the chart.

Performance Metrics: The strategy’s performance is tracked in real-time with an in-chart table. This table provides essential information about the number of trades executed, the win/loss ratio, and the overall win rate. This information helps traders assess the strategy's effectiveness and make necessary adjustments.

This strategy is designed for those who seek to engage with trending markets, offering robust tools for entry, exit, and overall trade management. By understanding and leveraging these features, traders can potentially improve their trading outcomes and risk management.

🔷 Related Script

🔶 Disclaimer

Use with Caution: This indicator is provided for educational and informational purposes only and should not be considered as financial advice. Users should exercise caution and perform their own analysis before making trading decisions based on the indicator's signals.

Not Financial Advice: The information provided by this indicator does not constitute financial advice, and the creator (UAlgo) shall not be held responsible for any trading losses incurred as a result of using this indicator.

Backtesting Recommended: Traders are encouraged to backtest the indicator thoroughly on historical data before using it in live trading to assess its performance and suitability for their trading strategies.

Risk Management: Trading involves inherent risks, and users should implement proper risk management strategies, including but not limited to stop-loss orders and position sizing, to mitigate potential losses.

No Guarantees: The accuracy and reliability of the indicator's signals cannot be guaranteed, as they are based on historical price data and past performance may not be indicative of future results.

Multi-Factor StrategyThis trading strategy combines multiple technical indicators to create a systematic approach for entering and exiting trades. The goal is to capture trends by aligning several key indicators to confirm the direction and strength of a potential trade. Below is a detailed description of how the strategy works:

Indicators Used

MACD (Moving Average Convergence Divergence):

MACD Line: The difference between the 12-period and 26-period Exponential Moving Averages (EMAs).

Signal Line: A 9-period EMA of the MACD line.

Usage: The strategy looks for crossovers between the MACD line and the Signal line as entry signals. A bullish crossover (MACD line crossing above the Signal line) indicates a potential upward movement, while a bearish crossover (MACD line crossing below the Signal line) signals a potential downward movement.

RSI (Relative Strength Index):

Usage: RSI is used to gauge the momentum of the price movement. The strategy uses specific thresholds: below 70 for long positions to avoid overbought conditions and above 30 for short positions to avoid oversold conditions.

ATR (Average True Range):

Usage: ATR measures market volatility and is used to set dynamic stop-loss and take-profit levels. A stop loss is set at 2 times the ATR, and a take profit at 3 times the ATR, ensuring that risk is managed relative to market conditions.

Simple Moving Averages (SMA):

50-day SMA: A short-term trend indicator.

200-day SMA: A long-term trend indicator.

Usage: The strategy uses the relationship between the 50-day and 200-day SMAs to determine the overall market trend. Long positions are taken when the price is above the 50-day SMA and the 50-day SMA is above the 200-day SMA, indicating an uptrend. Conversely, short positions are taken when the price is below the 50-day SMA and the 50-day SMA is below the 200-day SMA, indicating a downtrend.

Entry Conditions

Long Position:

-MACD Crossover: The MACD line crosses above the Signal line.

-RSI Confirmation: RSI is below 70, ensuring the asset is not overbought.

-SMA Confirmation: The price is above the 50-day SMA, and the 50-day SMA is above the 200-day SMA, indicating a strong uptrend.

Short Position:

MACD Crossunder: The MACD line crosses below the Signal line.

RSI Confirmation: RSI is above 30, ensuring the asset is not oversold.

SMA Confirmation: The price is below the 50-day SMA, and the 50-day SMA is below the 200-day SMA, indicating a strong downtrend.

Opposite conditions for shorts

Exit Strategy

Stop Loss: Set at 2 times the ATR from the entry price. This dynamically adjusts to market volatility, allowing for wider stops in volatile markets and tighter stops in calmer markets.

Take Profit: Set at 3 times the ATR from the entry price. This ensures a favorable risk-reward ratio of 1:1.5, aiming for higher rewards on successful trades.

Visualization

SMAs: The 50-day and 200-day SMAs are plotted on the chart to visualize the trend direction.

MACD Crossovers: Bullish and bearish MACD crossovers are highlighted on the chart to identify potential entry points.

Summary

This strategy is designed to align multiple indicators to increase the probability of successful trades by confirming trends and momentum before entering a position. It systematically manages risk with ATR-based stop loss and take profit levels, ensuring that trades are exited based on market conditions rather than arbitrary points. The combination of trend indicators (SMAs) with momentum and volatility indicators (MACD, RSI, ATR) creates a robust approach to trading in various market environments.

Negroni Opening Range StrategyStrategy Summary:

This tool can be used to help identify breakouts from a range during a time-zone of your choosing. It plots a pre-market range, an opening range, it also includes moving average levels that can be used as confluence, as well as plotting previous day SESSION highs and lows.

There are several options on how you wish to close out the trades, all described in more detail below.

Back-testing Inputs:

You define your timezone.

You define how many trades to open on any given day.

You decide to go: long only, short only, or long & short (CAREFUL: "Long & Short" can open trades that effectively closes-out existing ones, for better AND worse!)

You define between which times the strategy will open trades.

You define when it closes any open trades (preventing overnight trades, or leaving trades open into US data times!!).

This hopefully helps make back-testing reflect YOUR trading hours.

NOTE: Renko or Heikin-Ashi charts

For ALL strategies, don’t use Renko or Heikin-Ashi charts unless you know EXACTLY the implications.

Specific to my strategy, using a renko chart can make this 85-90% profitable (I wish it was!!) Although they can be useful, renko charts don’t always capture real wicks, so the renko chart may show your trade up-only but your broker (who is not using renko!!) will have likely stopped you out on a wick somewhere along the line.

NOTE: TradingView ‘Deep backtesting’

For ALL strategies, be cynical of all backtesting (e.g. repainting issues etc) as well as ‘Deep backtesting’ results.

Specific to this strategy, the default settings here SHOULD BE OK, but unfortunately at the time of writing, we can’t see on the chart what exactly ‘deep backtesting’ is calculating. In the past I have noted a number of trades that were not closed at the end of the day, despite my ‘end of day’ trade closing being enabled, so there were big winners and losers that would not have materialized otherwise. As I say, this seems ok at these settings but just always be cynical!!

Opening Range Inputs

You define a pre-market range (example: 08:00 - 09:00).

You define an opening range (example: 09:00 - 09:30).

The strategy will give an update at the close of the opening range to let you know if the opening range has broken out the pre-market range (OR Breakout), or if it has remained inside (OR Inside). The label appears at the end of the opening range NOT at the bar that ‘broke-out’.

This is just a visual cue for you, it has no bearing on what the strategy will do.

The strategy default will trade off the pre-market range, but you can untick this if you prefer to trade off the opening range.

Opening Trades:

Strategy goes long when the bar (CLOSE) crosses-over the ‘pre-market’ high (not the ‘opening range’ high); and the time is within your trading session, and you have not maxed out your number of trades for the day!

Strategy goes short when the bar (CLOSE) crosses-under the ‘pre-market’ low (not the ‘opening range low); and the time is within your trading session, and you have not maxed out your number of trades for the day!

Remember, you can untick this if you prefer to trade off the opening range instead.

NOTES:

Using momentum indicators can help (RSI and MACD): especially to trade range plays in failed breakouts, when momentum shifts… but the strategy won’t do this for you!

Using an anchored vwap at the session open can also provide nice confluence, as well as take-profit levels at the upper/lower of 3x standard deviation.

CLOSING TRADES:

You have 6 take-profit (TP) options:

1) Full TP: uses ATR Multiplier - Full TP at the ATR parameters as defined in inputs.

2) Take Partial profits: ATR Multiplier - Takes partial profits based on parameters as defined in inputs (i.e close 40% of original trade at TP1, close another 40% of original trade at TP2, then the remainder at Full TP as set in option 1.).

3) Full TP: Trailing Stop - Applies a Trailing Stop at the number of points, as defined in inputs.

4) Full TP: MA cross - Takes profit when price crosses ‘Trend MA’ as defined in inputs.

5) Scalp: Points - closes at a set number of points, as defined in inputs.

6) Full TP: PMKT Multiplier - places a SL at opposite pre-market Hi/Low (we go long at a break-out of the pre-market high, 50% would place a SL at the pre-market range mid-point; 100% would place a SL at the pre-market low)'. This takes profit at the input set in option 1).

Multi-Step FlexiSuperTrend - Strategy [presentTrading]At the heart of this endeavor is a passion for continuous improvement in the art of trading

█ Introduction and How it is Different

The "Multi-Step FlexiSuperTrend - Strategy " is an advanced trading strategy that integrates the well-known SuperTrend indicator with a nuanced and dynamic approach to market trend analysis. Unlike conventional SuperTrend strategies that rely on static thresholds and fixed parameters, this strategy introduces multi-step take profit mechanisms that allow traders to capitalize on varying market conditions in a more controlled and systematic manner.

What sets this strategy apart is its ability to dynamically adjust to market volatility through the use of an incremental factor applied to the SuperTrend calculation. This adjustment ensures that the strategy remains responsive to both minor and major market shifts, providing a more accurate signal for entries and exits. Additionally, the integration of multi-step take profit levels offers traders the flexibility to scale out of positions, locking in profits progressively as the market moves in their favor.

BTC 6hr Long/Short Performance

█ Strategy, How it Works: Detailed Explanation

The Multi-Step FlexiSuperTrend strategy operates on the foundation of the SuperTrend indicator, but with several enhancements that make it more adaptable to varying market conditions. The key components of this strategy include the SuperTrend Polyfactor Oscillator, a dynamic normalization process, and multi-step take profit levels.

🔶 SuperTrend Polyfactor Oscillator

The SuperTrend Polyfactor Oscillator is the heart of this strategy. It is calculated by applying a series of SuperTrend calculations with varying factors, starting from a defined "Starting Factor" and incrementing by a specified "Increment Factor." The indicator length and the chosen price source (e.g., HLC3, HL2) are inputs to the oscillator.

The SuperTrend formula typically calculates an upper and lower band based on the average true range (ATR) and a multiplier (the factor). These bands determine the trend direction. In the FlexiSuperTrend strategy, the oscillator is enhanced by iteratively applying the SuperTrend calculation across different factors. The iterative process allows the strategy to capture both minor and significant trend changes.

For each iteration (indexed by `i`), the following calculations are performed:

1. ATR Calculation: The Average True Range (ATR) is calculated over the specified `indicatorLength`:

ATR_i = ATR(indicatorLength)

2. Upper and Lower Bands Calculation: The upper and lower bands are calculated using the ATR and the current factor:

Upper Band_i = hl2 + (ATR_i * Factor_i)

Lower Band_i = hl2 - (ATR_i * Factor_i)

Here, `Factor_i` starts from `startingFactor` and is incremented by `incrementFactor` in each iteration.

3. Trend Determination: The trend is determined by comparing the indicator source with the upper and lower bands:

Trend_i = 1 (uptrend) if IndicatorSource > Upper Band_i

Trend_i = 0 (downtrend) if IndicatorSource < Lower Band_i

Otherwise, the trend remains unchanged from the previous value.

4. Output Calculation: The output of each iteration is determined based on the trend:

Output_i = Lower Band_i if Trend_i = 1

Output_i = Upper Band_i if Trend_i = 0

This process is repeated for each iteration (from 0 to 19), creating a series of outputs that reflect different levels of trend sensitivity.

Local

🔶 Normalization Process

To make the oscillator values comparable across different market conditions, the deviations between the indicator source and the SuperTrend outputs are normalized. The normalization method can be one of the following:

1. Max-Min Normalization: The deviations are normalized based on the range of the deviations:

Normalized Value_i = (Deviation_i - Min Deviation) / (Max Deviation - Min Deviation)

2. Absolute Sum Normalization: The deviations are normalized based on the sum of absolute deviations:

Normalized Value_i = Deviation_i / Sum of Absolute Deviations

This normalization ensures that the oscillator values are within a consistent range, facilitating more reliable trend analysis.

For more details:

🔶 Multi-Step Take Profit Mechanism

One of the unique features of this strategy is the multi-step take profit mechanism. This allows traders to lock in profits at multiple levels as the market moves in their favor. The strategy uses three take profit levels, each defined as a percentage increase (for long trades) or decrease (for short trades) from the entry price.

1. First Take Profit Level: Calculated as a percentage increase/decrease from the entry price:

TP_Level1 = Entry Price * (1 + tp_level1 / 100) for long trades

TP_Level1 = Entry Price * (1 - tp_level1 / 100) for short trades

The strategy exits a portion of the position (defined by `tp_percent1`) when this level is reached.

2. Second Take Profit Level: Similar to the first level, but with a higher percentage:

TP_Level2 = Entry Price * (1 + tp_level2 / 100) for long trades

TP_Level2 = Entry Price * (1 - tp_level2 / 100) for short trades

The strategy exits another portion of the position (`tp_percent2`) at this level.

3. Third Take Profit Level: The final take profit level:

TP_Level3 = Entry Price * (1 + tp_level3 / 100) for long trades

TP_Level3 = Entry Price * (1 - tp_level3 / 100) for short trades

The remaining portion of the position (`tp_percent3`) is exited at this level.

This multi-step approach provides a balance between securing profits and allowing the remaining position to benefit from continued favorable market movement.

█ Trade Direction

The strategy allows traders to specify the trade direction through the `tradeDirection` input. The options are:

1. Both: The strategy will take both long and short positions based on the entry signals.

2. Long: The strategy will only take long positions.

3. Short: The strategy will only take short positions.

This flexibility enables traders to tailor the strategy to their market outlook or current trend analysis.

█ Usage

To use the Multi-Step FlexiSuperTrend strategy, traders need to set the input parameters according to their trading style and market conditions. The strategy is designed for versatility, allowing for various market environments, including trending and ranging markets.

Traders can also adjust the multi-step take profit levels and percentages to match their risk management and profit-taking preferences. For example, in highly volatile markets, traders might set wider take profit levels with smaller percentages at each level to capture larger price movements.

The normalization method and the incremental factor can be fine-tuned to adjust the sensitivity of the SuperTrend Polyfactor Oscillator, making the strategy more responsive to minor market shifts or more focused on significant trends.

█ Default Settings

The default settings of the strategy are carefully chosen to provide a balanced approach between risk management and profit potential. Here is a breakdown of the default settings and their effects on performance:

1. Indicator Length (10): This parameter controls the lookback period for the ATR calculation. A shorter length makes the strategy more sensitive to recent price movements, potentially generating more signals. A longer length smooths out the ATR, reducing sensitivity but filtering out noise.

2. Starting Factor (0.618): This is the initial multiplier used in the SuperTrend calculation. A lower starting factor makes the SuperTrend bands closer to the price, generating more frequent trend changes. A higher starting factor places the bands further away, filtering out minor fluctuations.

3. Increment Factor (0.382): This parameter controls how much the factor increases with each iteration of the SuperTrend calculation. A smaller increment factor results in more gradual changes in sensitivity, while a larger increment factor creates a wider range of sensitivity across the iterations.

4. Normalization Method (None): The default is no normalization, meaning the raw deviations are used. Normalization methods like Max-Min or Absolute Sum can make the deviations more consistent across different market conditions, improving the reliability of the oscillator.

5. Take Profit Levels (2%, 8%, 18%): These levels define the thresholds for exiting portions of the position. Lower levels (e.g., 2%) capture smaller profits quickly, while higher levels (e.g., 18%) allow positions to run longer for more significant gains.

6. Take Profit Percentages (30%, 20%, 15%): These percentages determine how much of the position is exited at each take profit level. A higher percentage at the first level locks in more profit early, reducing exposure to market reversals. Lower percentages at higher levels allow for a portion of the position to benefit from extended trends.

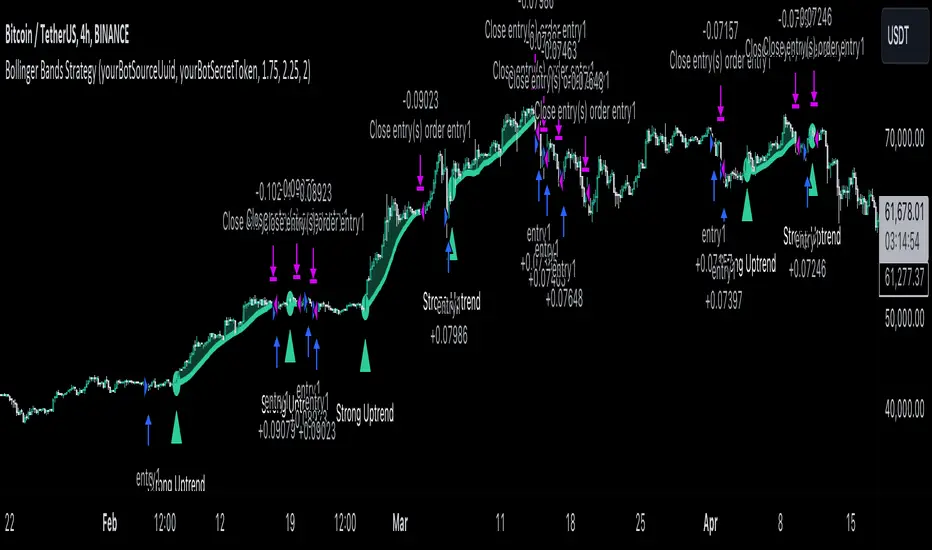

Bollinger Bands Enhanced StrategyOverview

The common practice of using Bollinger bands is to use it for building mean reversion or squeeze momentum strategies. In the current script Bollinger Bands Enhanced Strategy we are trying to combine the strengths of both strategies types. It utilizes Bollinger Bands indicator to buy the local dip and activates trailing profit system after reaching the user given number of Average True Ranges (ATR). Also it uses 200 period EMA to filter trades only in the direction of a trend. Strategy can execute only long trades.

Unique Features

Trailing Profit System: Strategy uses user given number of ATR to activate trailing take profit. If price has already reached the trailing profit activation level, scrip will close long trade if price closes below Bollinger Bands middle line.

Configurable Trading Periods: Users can tailor the strategy to specific market windows, adapting to different market conditions.

Major Trend Filter: Strategy utilizes 100 period EMA to take trades only in the direction of a trend.

Flexible Risk Management: Users can choose number of ATR as a stop loss (by default = 1.75) for trades. This is flexible approach because ATR is recalculated on every candle, therefore stop-loss readjusted to the current volatility.

Methodology

First of all, script checks if currently price is above the 200-period exponential moving average EMA. EMA is used to establish the current trend. Script will take long trades on if this filtering system showing us the uptrend. Then the strategy executes the long trade if candle’s low below the lower Bollinger band. To calculate the middle Bollinger line, we use the standard 20-period simple moving average (SMA), lower band is calculated by the substruction from middle line the standard deviation multiplied by user given value (by default = 2).

When long trade executed, script places stop-loss at the price level below the entry price by user defined number of ATR (by default = 1.75). This stop-loss level recalculates at every candle while trade is open according to the current candle ATR value. Also strategy set the trailing profit activation level at the price above the position average price by user given number of ATR (by default = 2.25). It is also recalculated every candle according to ATR value. When price hit this level script plotted the triangle with the label “Strong Uptrend” and start trail the price at the middle Bollinger line. It also started to be plotted as a green line.

When price close below this trailing level script closes the long trade and search for the next trade opportunity.

Risk Management

The strategy employs a combined and flexible approach to risk management:

It allows positions to ride the trend as long as the price continues to move favorably, aiming to capture significant price movements. It features a user-defined ATR stop loss parameter to mitigate risks based on individual risk tolerance. By default, this stop-loss is set to a 1.75*ATR drop from the entry point, but it can be adjusted according to the trader's preferences.

There is no fixed take profit, but strategy allows user to define user the ATR trailing profit activation parameter. By default, this stop-loss is set to a 2.25*ATR growth from the entry point, but it can be adjusted according to the trader's preferences.

Justification of Methodology

This strategy leverages Bollinger bangs indicator to open long trades in the local dips. If price reached the lower band there is a high probability of bounce. Here is an issue: during the strong downtrend price can constantly goes down without any significant correction. That’s why we decided to use 200-period EMA as a trend filter to increase the probability of opening long trades during major uptrend only.

Usually, Bollinger Bands indicator is using for mean reversion or breakout strategies. Both of them have the disadvantages. The mean reversion buys the dip, but closes on the return to some mean value. Therefore, it usually misses the major trend moves. The breakout strategies usually have the issue with too high buy price because to have the breakout confirmation price shall break some price level. Therefore, in such strategies traders need to set the large stop-loss, which decreases potential reward to risk ratio.

In this strategy we are trying to combine the best features of both types of strategies. Script utilizes ate ATR to setup the stop-loss and trailing profit activation levels. ATR takes into account the current volatility. Therefore, when we setup stop-loss with the user-given number of ATR we increase the probability to decrease the number of false stop outs. The trailing profit concept is trying to add the beat feature from breakout strategies and increase probability to stay in trade while uptrend is developing. When price hit the trailing profit activation level, script started to trail the price with middle line if Bollinger bands indicator. Only when candle closes below the middle line script closes the long trade.

Backtest Results

Operating window: Date range of backtests is 2020.10.01 - 2024.07.01. It is chosen to let the strategy to close all opened positions.

Commission and Slippage: Includes a standard Binance commission of 0.1% and accounts for possible slippage over 5 ticks.

Initial capital: 10000 USDT

Percent of capital used in every trade: 30%

Maximum Single Position Loss: -9.78%

Maximum Single Profit: +25.62%

Net Profit: +6778.11 USDT (+67.78%)

Total Trades: 111 (48.65% win rate)

Profit Factor: 2.065

Maximum Accumulated Loss: 853.56 USDT (-6.60%)

Average Profit per Trade: 61.06 USDT (+1.62%)

Average Trade Duration: 76 hours

These results are obtained with realistic parameters representing trading conditions observed at major exchanges such as Binance and with realistic trading portfolio usage parameters.

How to Use

Add the script to favorites for easy access.

Apply to the desired timeframe and chart (optimal performance observed on 4h BTC/USDT).

Configure settings using the dropdown choice list in the built-in menu.

Set up alerts to automate strategy positions through web hook with the text: {{strategy.order.alert_message}}

Disclaimer:

Educational and informational tool reflecting Skyrex commitment to informed trading. Past performance does not guarantee future results. Test strategies in a simulated environment before live implementation

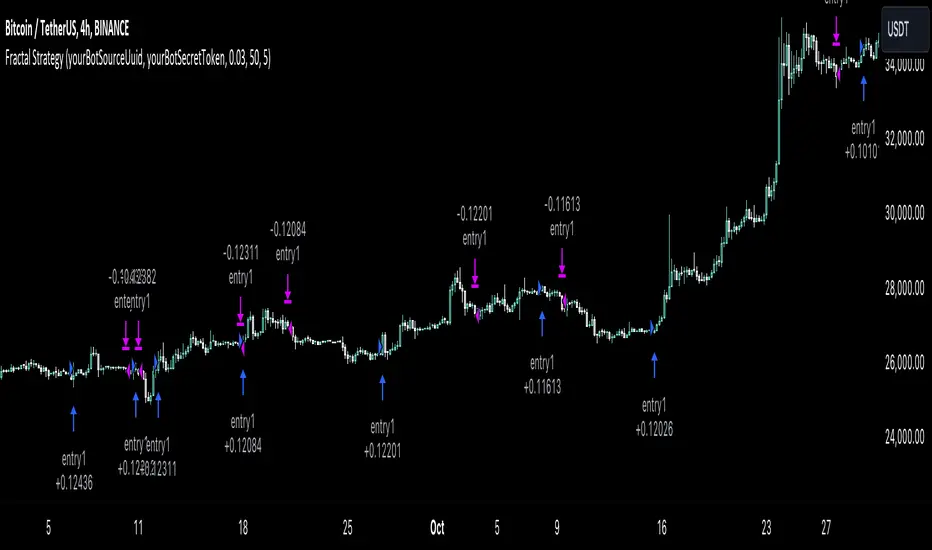

Fractal Breakout Trend Following StrategyOverview

The Fractal Breakout Trend Following Strategy is a trend-following system which utilizes the Willams Fractals and Alligator to execute the long trades on the fractal's breakouts which have a high probability to be the new uptrend phase beginning. This system also uses the normalized Average True Range indicator to filter trades after a large moves, because it's more likely to see the trend continuation after a consolidation period. Strategy can execute only long trades.

Unique Features

Trend and volatility filtering system: Strategy uses Williams Alligator to filter the counter-trend fractals breakouts and normalized Average True Range to avoid the trades after large moves, when volatility is high

Configurable Trading Periods: Users can tailor the strategy to specific market windows, adapting to different market conditions.

Flexible Risk Management: Users can choose the stop-loss percent (by default = 3%) for trades, but strategy also has the dynamic stop-loss level using down fractals.

Methodology

The strategy places stop order at the last valid fractal breakout level. Validity of this fractal is defined by the Williams Alligator indicator. If at the moment of time when price breaking the last fractal price is higher than Alligator's teeth line (8 period SMA shifted 5 bars in the future) this is a valid breakout. Moreover strategy has the additional volatility filtering system using normalized ATR. It calculates the average normalized ATR for last user-defined number of bars and if this value lower than the user-defined threshold value the long trade is executed.

When trade is opened, script places the stop loss at the price higher of two levels: user defined stop-loss from the position entry price or down fractal validation level. The down fractal is valid with the rule, opposite as the up fractal validation. Price shall break to the downside the last down fractal below the Willians Alligator's teeth line.

Strategy has no fixed take profit. Exit level changes with the down fractal validation level. If price is in strong uptrend trade is going to be active until last down fractal is not valid. Strategy closes trade when price hits the down fractal validation level.

Risk Management

The strategy employs a combined approach to risk management:

It allows positions to ride the trend as long as the price continues to move favorably, aiming to capture significant price movements. It features a user-defined stop-loss parameter to mitigate risks based on individual risk tolerance. By default, this stop-loss is set to a 3% drop from the entry point, but it can be adjusted according to the trader's preferences.

Justification of Methodology

This strategy leverages Williams Fractals to open long trade when price has broken the key resistance level to the upside. This resistance level is the last up fractal and is shall be broken above the Williams Alligator's teeth line to be qualified as the valid breakout according to this strategy. The Alligator filtering increases the probability to avoid the false breakouts against the current trend.

Moreover strategy has an additional filter using Average True Range(ATR) indicator. If average value of ATR for the last user-defined number of bars is lower than user-defined threshold strategy can open the long trade according to open trade condition above. The logic here is following: we want to open trades after period of price consolidation inside the range because before and after a big move price is more likely to be in sideways, but we need a trend move to have a profit.

Another one important feature is how the exit condition is defined. On the one hand, strategy has the user-defined stop-loss (3% below the entry price by default). It's made to give users the opportunity to restrict their losses according to their risk-tolerance. On the other hand, strategy utilizes the dynamic exit level which is defined by down fractal activation. If we assume the breaking up fractal is the beginning of the uptrend, breaking down fractal can be the start of downtrend phase. We don't want to be in long trade if there is a high probability of reversal to the downside. This approach helps to not keep open trade if trend is not developing and hold it if price continues going up.

Backtest Results

Operating window: Date range of backtests is 2023.01.01 - 2024.05.01. It is chosen to let the strategy to close all opened positions.

Commission and Slippage: Includes a standard Binance commission of 0.1% and accounts for possible slippage over 5 ticks.

Initial capital: 10000 USDT

Percent of capital used in every trade: 30%

Maximum Single Position Loss: -3.19%

Maximum Single Profit: +24.97%

Net Profit: +3036.90 USDT (+30.37%)

Total Trades: 83 (28.92% win rate)

Profit Factor: 1.953

Maximum Accumulated Loss: 963.98 USDT (-8.29%)

Average Profit per Trade: 36.59 USDT (+1.12%)

Average Trade Duration: 72 hours

These results are obtained with realistic parameters representing trading conditions observed at major exchanges such as Binance and with realistic trading portfolio usage parameters.

How to Use

Add the script to favorites for easy access.

Apply to the desired timeframe and chart (optimal performance observed on 4h and higher time frames and the BTC/USDT).

Configure settings using the dropdown choice list in the built-in menu.

Set up alerts to automate strategy positions through web hook with the text: {{strategy.order.alert_message}}

Disclaimer:

Educational and informational tool reflecting Skyrex commitment to informed trading. Past performance does not guarantee future results. Test strategies in a simulated environment before live implementation

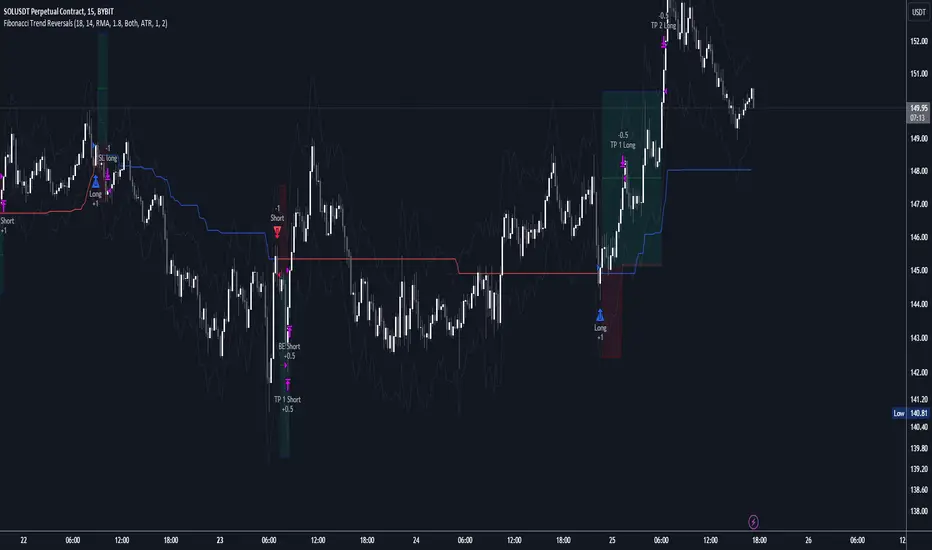

Fibonacci Trend Reversal StrategyIntroduction

This publication introduces the " Fibonacci Retracement Trend Reversal Strategy, " tailored for traders aiming to leverage shifts in market momentum through advanced trend analysis and risk management techniques. This strategy is designed to pinpoint potential reversal points, optimizing trading opportunities.

Overview

The strategy leverages Fibonacci retracement levels derived from @IMBA_TRADER's lance Algo to identify potential trend reversals. It's further enhanced by a method called " Trend Strength Over Time " (TSOT) (by @federalTacos5392b), which utilizes percentile rankings of price action to measure trend strength. This also has implemented Dynamic SL finder by utilizing @veryfid's ATR Stoploss Finder which works pretty well

Indicators:

Fibonacci Retracement Levels : Identifies critical reversal zones at 23.6%, 50%, and 78.6% levels.

TSOT (Trend Strength Over Time) : Employs percentile rankings across various timeframes to gauge the strength and direction of trends, aiding in the confirmation of Fibonacci-based signals.

ATR (Average True Range) : Implements dynamic stop-loss settings for both long and short positions, enhancing trade security.

Strategy Settings :

- Sensitivity: Set default at 18, adjustable for more frequent or sparse signals based on market volatility.

- ATR Stop Loss Finder: Multiplier set at 3.5, applying the ATR value to determine stop losses dynamically.

- ATR Length: Default set to 14 with RMA smoothing.

- TSOT Settings: Hard-coded to identify percentile ranks, with no user-adjustable inputs due to its intrinsic calculation method.

Trade Direction Options : Configurable to support long, short, or both directions, adaptable to the trader's market assessment.

Entry Conditions :

- Long Entry: Triggered when the price surpasses the mid Fibonacci level (50%) with a bullish TSOT signal.

- Short Entry: Activated when the price falls below the mid Fibonacci level with a bearish TSOT indication.

Exit Conditions :

- Employs ATR-based dynamic stop losses, calibrated according to current market volatility, ensuring effective risk management.

Strategy Execution :

- Risk Management: Features adjustable risk-reward settings and enables partial take profits by default to systematically secure gains.

- Position Reversal: Includes an option to reverse positions based on new TSOT signals, improving the strategy's responsiveness to evolving market conditions.

The strategy is optimized for the BYBIT:WIFUSDT.P market on a scalping (5-minute) timeframe, using the default settings outlined above.

I spent a lot of time creating the dynamic exit strategies for partially taking profits and reversing positions so please make use of those and feel free to adjust the settings, tool tips are also provided.

For Developers: this is published as open-sourced code so that developers can learn something especially on dynamic exits and partial take profits!

Good Luck!

Disclaimer

This strategy is shared for educational purposes and must be thoroughly tested under diverse market conditions. Past performance does not guarantee future results. Traders are advised to integrate this strategy with other analytical tools and tailor it to specific market scenarios. I was only sharing what I've crafted while strategizing over a Solana Meme Coin.

Supertrend & CCI Strategy ScalpThis strategy is based on 2 Super Trend Indicators along with CCI .

The longer factor length gives you the current trend and the deviation in the short factor length gives us the opportunity to enter in the trade .

CCI indicator is used to determine the overbought and oversold levels.

Setup :

Long : When atrLength1 > close and atrLength2 < close and CCI < -100 we look for long trades as the longer factor length will be bullish .

Short : When atrLength1 < close and atrLength2 > close and CCI > 100 we look for short trades as the longer factor length will be bearish .

Please tune the settings according to your use .

Trade what you see not what you feel .

Please consult with your financial advisor before you deploy any real money for trading .

PresentTrend RMI Synergy - Strategy [presentTrading] █ Introduction and How it is Different

The "PresentTrend RMI Synergy Strategy" is the combined power of the Relative Momentum Index (RMI) and a custom presentTrend indicator. This strategy introduces a multifaceted approach, integrating momentum analysis with trend direction to offer traders a more nuanced and responsive trading mechanism.

BTCUSD 6h L/S Performance

Local

█ Strategy, How It Works: Detailed Explanation

The "PresentTrend RMI Synergy Strategy" intricately combines the Relative Momentum Index (RMI) and a custom SuperTrend indicator to create a powerful tool for traders.

🔶 Relative Momentum Index (RMI)

The RMI is a variation of the Relative Strength Index (RSI), but instead of using price closes against itself, it measures the momentum of up and down movements in price relative to previous prices over a given period. The RMI for a period length `N` is calculated as follows:

RMI = 100 - 100/ (1 + U/D)

where:

- `U` is the average upward price change over `N` periods,

- `D` is the average downward price change over `N` periods.

The RMI oscillates between 0 and 100, with higher values indicating stronger upward momentum and lower values suggesting stronger downward momentum.

RMI = 21

RMI = 42

For more information - RMI Trend Sync - Strategy :

🔶 presentTrend Indicator

The presentTrend indicator combines the Average True Range (ATR) with a moving average to determine trend direction and dynamic support or resistance levels. The presentTrend for a period length `M` and a multiplier `F` is defined as:

- Upper Band: MA + (ATR x F)

- Lower Band: MA - (ATR x F)

where:

- `MA` is the moving average of the close price over `M` periods,

- `ATR` is the Average True Range over the same period,

- `F` is the multiplier to adjust the sensitivity.

The trend direction switches when the price crosses the presentTrend bands, signaling potential entry or exit points.

presentTrend length = 3

presentTrend length = 10

For more information - PresentTrend - Strategy :

🔶 Strategy Logic

Entry Conditions:

- Long Entry: Triggered when the RMI exceeds a threshold, say 60, indicating a strong bullish momentum, and when the price is above the presentTrend, confirming an uptrend.

- Short Entry: Occurs when the RMI drops below a threshold, say 40, showing strong bearish momentum, and the price is below the present trend, indicating a downtrend.

Exit Conditions with Dynamic Trailing Stop:

- Long Exit: Initiated when the price crosses below the lower presentTrend band or when the RMI falls back towards a neutral level, suggesting a weakening of the bullish momentum.

- Short Exit: Executed when the price crosses above the upper presentTrend band or when the RMI rises towards a neutral level, indicating a reduction in bearish momentum.

Equations for Dynamic Trailing Stop:

- For Long Positions: The exit price is set at the lower SuperTrend band once the entry condition is met.

- For Short Positions: The exit price is determined by the upper SuperTrend band post-entry.

These dynamic trailing stops adjust as the market moves, providing a method to lock in profits while allowing room for the position to grow.

This strategy's strength lies in its dual analysis approach, leveraging RMI for momentum insights and presentTrend for trend direction and dynamic stops. This combination offers traders a robust framework to navigate various market conditions, aiming to capture trends early and exit positions strategically to maximize gains and minimize losses.

█ Trade Direction

The strategy provides flexibility in trade direction selection, offering "Long," "Short," or "Both" options to cater to different market conditions and trader preferences. This adaptability ensures that traders can align the strategy with their market outlook, risk tolerance, and trading goals.

█ Usage

To utilize the "PresentTrend RMI Synergy Strategy," traders should input their preferred settings in the Pine Script™ and apply the strategy to their charts. Monitoring RMI for momentum shifts and adjusting positions based on SuperTrend signals can optimize entry and exit points, enhancing potential returns while managing risk.

█ Default Settings

1. RMI Length: 21

The 21-period RMI length strikes a balance between capturing momentum and filtering out market noise, offering a medium-term outlook on market trends.

2. Super Trend Length: 7

A SuperTrend length of 7 periods is chosen for its responsiveness to price movements, providing a dynamic framework for trend identification without excessive sensitivity.

3. Super Trend Multiplier: 4.0

The multiplier of 4.0 for the SuperTrend indicator widens the trend bands, focusing on significant market moves and reducing the impact of minor fluctuations.

---

The "PresentTrend RMI Synergy Strategy" represents a significant step forward in trading strategy development, blending momentum and trend analysis in a unique way. By providing a detailed framework for understanding market dynamics, this strategy empowers traders to make more informed decisions.

AI SuperTrend x Pivot Percentile - Strategy [PresentTrading]█ Introduction and How it is Different