Fourier For Loop [BackQuant]Fourier For Loop

PLEASE Read the following, as understanding an indicator's functionality is essential before integrating it into a trading strategy. Knowing the core logic behind each tool allows for a sound and strategic approach to trading.

Introducing BackQuant's Fourier For Loop (FFL) — a cutting-edge trading indicator that combines Fourier transforms with a for-loop scoring mechanism. This innovative approach leverages mathematical precision to extract trends and reversals in the market, helping traders make informed decisions. Let's break down the components, rationale, and potential use-cases of this indicator.

Understanding Fourier Transform in Trading

The Fourier Transform decomposes price movements into their frequency components, allowing for a detailed analysis of cyclical behavior in the market. By transforming the price data from the time domain into the frequency domain, this indicator identifies underlying patterns that traditional methods may overlook.

In this script, Fourier transforms are applied to the specified calculation source (defaulted to HLC3). The transformation yields magnitude values that can be used to score market movements over a defined range. This scoring process helps uncover long and short signals based on relative strength and trend direction.

Why Use Fourier Transforms?

Fourier Transforms excel in identifying recurring cycles and smoothing noisy data, making them ideal for fast-paced markets where price movements may be erratic. They also provide a unique perspective on market volatility, offering traders additional insights beyond standard indicators.

Calculation Logic: For-Loop Scoring Mechanism

The For Loop Scoring mechanism compares the magnitude of each transformed point in the series, summing the results to generate a score. This score forms the backbone of the signal generation system.

Long Signals: Generated when the score surpasses the defined long threshold (default set at 40). This indicates a strong bullish trend, signaling potential upward momentum.

Short Signals: Triggered when the score crosses under the short threshold (default set at -10). This suggests a bearish trend or potential downside risk.'

Thresholds & Customization

The indicator offers customizable settings to fit various trading styles:

Calculation Periods: Control how many periods the Fourier transform covers.

Long/Short Thresholds: Adjust the sensitivity of the signals to match different timeframes or risk preferences.

Visualization Options: Traders can visualize the thresholds, change the color of bars based on trend direction, and even color the background for enhanced clarity.

Trading Applications

This Fourier For Loop indicator is designed to be versatile across various market conditions and timeframes. Some of its key use-cases include:

Cycle Detection: Fourier transforms help identify recurring patterns or cycles, giving traders a head-start on market direction.

Trend Following: The for-loop scoring system helps confirm the strength of trends, allowing traders to enter positions with greater confidence.

Risk Management: With clearly defined long and short signals, traders can manage their positions effectively, minimizing exposure to false signals.

Final Note

Incorporating this indicator into your trading strategy adds a layer of mathematical precision to traditional technical analysis. Be sure to adjust the calculation start/end points and thresholds to match your specific trading style, and remember that no indicator guarantees success. Always backtest thoroughly and integrate the Fourier For Loop into a balanced trading system.

Thus following all of the key points here are some sample backtests on the 1D Chart

Disclaimer: Backtests are based off past results, and are not indicative of the future .

INDEX:BTCUSD

INDEX:ETHUSD

BINANCE:SOLUSD

Backtest

Interest Rate Trading (Manually Added Rate Decisions) [TANHEF]Interest Rate Trading: How Interest Rates Can Guide Your Next Move.

How were interest rate decisions added?

All interest rate decision dates were manually retrieved from the 'Record of Policy Actions' and 'Minutes of Actions' on the Federal Reserve's website due to inconsistent dates from other sources. These were manually added as Pine Script currently only identifies rate changes, not pauses.

█ Simple Explanation:

This script is designed for analyzing and backtesting trading strategies based on U.S. interest rate decisions which occur during Federal Open Market Committee (FOMC) meetings, to make trading decisions. No trading strategy is perfect, and it's important to understand that expectations won't always play out. The script leverages historical interest rate changes, including increases, decreases, and pauses, across multiple economic time periods from 1971 to the present. The tool integrates two key data sources for interest rates—USINTR and FEDFUNDS—to support decision-making around rate-based trades. The focus is on identifying opportunities and tracking trades driven by interest rate movements.

█ Interest Rate Decision Sources:

As noted above, each decision date has been manually added from the 'Record of Policy Actions' and 'Minutes of Actions' documents on the Federal Reserve's website. This includes +50 years of more than 600 rate decisions.

█ Interest Rate Data Sources:

USINTR: Reflects broader U.S. interest rate trends, including Treasury yields and various benchmarks. This is the preferred option as it corresponds well to the rate decision dates.

FEDFUNDS: Tracks the Federal Funds Rate, which is a more specific rate targeted by the Federal Reserve. This does not change on the exact same days as the rate decisions that occur at FOMC meetings.

█ Trade Criteria:

A variety of trading conditions are predefined to suit different trading strategies. These conditions include:

Increase/Decrease: Standard rate increases or decreases.

Double/Triple Increase/Decrease: A series of consecutive changes.

Aggressive Increase/Decrease: Rate changes that exceed recent movements.

Pause: Identification of no changes (pauses) between rate decisions, including double or triple pauses.

Complex Patterns: Combinations of pauses, increases, or decreases, such as "Pause after Increase" or "Pause or Increase."

█ Trade Execution and Exit:

The script allows automated trade execution based on selected criteria:

Auto-Entry: Option to enter trades automatically at the first valid period.

Max Trade Duration: Optional exit of trades after a specified number of bars (candles).

Pause Days: Minimum duration (in days) to validate rate pauses as entry conditions. This is especially useful for earlier periods (prior to the 2000s), where rate decisions often seemed random compared to the consistency we see today.

█ Visualization:

Several visual elements enhance the backtesting experience:

Time Period Highlighting: Economic time periods are visually segmented on the chart, each with a unique color. These periods include historical phases such as "Stagflation (1971-1982)" and "Post-Pandemic Recovery (2021-Present)".

Trade and Holding Results: Displays the profit and loss of trades and holding results directly on the chart.

Interest Rate Plot: Plots the interest rate movements on the chart, allowing for real-time tracking of rate changes.

Trade Status: Highlights active long or short positions on the chart.

█ Statistics and Criteria Display:

Stats Table: Summarizes trade results, including wins, losses, and draw percentages for both long and short trades.

Criteria Table: Lists the selected entry and exit criteria for both long and short positions.

█ Economic Time Periods:

The script organizes interest rate decisions into well-defined economic periods, allowing traders to backtest strategies specific to historical contexts like:

(1971-1982) Stagflation

(1983-1990) Reaganomics and Deregulation

(1991-1994) Early 1990s (Recession and Recovery)

(1995-2001) Dot-Com Bubble

(2001-2006) Housing Boom

(2007-2009) Global Financial Crisis

(2009-2015) Great Recession Recovery

(2015-2019) Normalization Period

(2019-2021) COVID-19 Pandemic

(2021-Present) Post-Pandemic Recovery

█ User-Configurable Inputs:

Rate Source Selection: Choose between USINTR or FEDFUNDS as the primary interest rate source.

Trade Criteria Customization: Users can select the criteria for long and short trades, specifying when to enter or exit based on changes in the interest rate.

Time Period: Select the time period that you want to isolate testing a strategy with.

Auto-Entry and Pause Settings: Options to automatically enter trades and specify the number of days to confirm a rate pause.

Max Trade Duration: Limits how long trades can remain open, defined by the number of bars.

█ Trade Logic:

The script manages entries and exits for both long and short trades. It calculates the profit or loss percentage based on the entry and exit prices. The script tracks ongoing trades, dynamically updating the profit or loss as price changes.

█ Examples:

One of the most popular opinions is that when rate starts begin you should sell, then buy back in when rate cuts stop dropping. However, this can be easily proven to be a difficult task. Predicting the end of a rate cut is very difficult to do with the the exception that assumes rates will not fall below 0.25%.

2001-2009

Trade Result: +29.85%

Holding Result: -27.74%

1971-2024

Trade Result: +533%

Holding Result: +5901%

█ Backtest and Real-Time Use:

This backtester is useful for historical analysis and real-time trading. By setting up various entry and exit rules tied to interest rate movements, traders can test and refine strategies based on real historical data and rate decision trends.

This powerful tool allows traders to customize strategies, backtest them through different economic periods, and get visual feedback on their trading performance, helping to make more informed decisions based on interest rate dynamics. The main goal of this indicator is to challenge the belief that future events must mirror the 2001 and 2007 rate cuts. If everyone expects something to happen, it usually doesn’t.

Descriptive Backtesting Framework (DBF)As the name suggests, this is a backtesting framework made to offer full backtesting functionality to any custom indicator in a visually descriptive way.

Any trade taken will be very clear to visualize on the chart and the equity line will be updated live allowing us to use the REPLAY feature to view the strategy performing in real time.

Stops and Targets will also get draw on the chart with labels and tooltips and there will be a table on the top right corner displaying lots of descriptive metrics to measure your strategy's performance.

IF YOU DECIDE TO USE THIS FRAMEWORK, PLEASE READ **EVERYTHING** BELOW

HOW TO USE IT

Step 1 - Insert Your Strategy Indicators:

Inside this framework's code, right at the beginning, you will find a dedicated section where you can manually insert any set of indicators you desire.

Just replace the example code in there with your own strategy indicators.

Step 2 - Specify The Conditions To Take Trades:

After that, there will be another section where you need to specify your strategy's conditions to enter and exit trades.

When met, those conditions will fire the trading signals to the trading engine inside the framework.

If you don't wish to use some of the available signals, please just assign false to the signal.

DO NOT DELETE THE SIGNAL VARIABLES

Step 3 - Specify Entry/Exit Prices, Stops & Targets:

Finally you'll reach the last section where you'll be able to specify entry/exit prices as well as add stops and targets.

On most cases, it's easier and more reliable to just use the close price to enter and exit trades.

If you decide to use the open price instead, please remember to change step 2 so that trades are taken on the open price of the next candle and not the present one to avoid the look ahead bias.

Stops and targets can be set in any way you want.

Also, please don't forget to update the spread. If your broker uses commissions instead of spreads or a combination of both, you'll need to manually incorporate those costs in this step.

And that's it! That's all you have to do.

Below this section you'll now see a sign warning you about not making any changes to the code below.

From here on, the framework will take care of executing the trades and calculating the performance metrics for you and making sure all calculations are consistent.

VISUAL FEATURES:

Price candles get painted according to the current trade.

They will be blue during long trades, purple on shorts and white when no trade is on.

When the framework receives the signals to start or close a trade, it will display those signals as shapes on the upper and lower limits of the chart:

DIAMOND: represents a signal to open a trade, the trade direction is represented by the shape's color;

CROSS: means a stop loss was triggered;

FLAG: means a take profit was triggered;

CIRCLE: means an exit trade signal was fired;

Hovering the mouse over the trade labels will reveal:

Asset Quantity;

Entry/Exit Prices;

Stops & Targets;

Trade Profit;

Profit As Percentage Of Trade Volume;

**Please note that there's a limit as to how many labels can be drawn on the chart at once.**

If you which to see labels from the beginning of the chart, you'll probably need to use the replay feature.

PERFORMANCE TABLE:

The performance table displays several performance metrics to evaluate the strategy.

All the performance metrics here are calculated by the framework. It does not uses the oficial pine script strategy tester.

All metrics are calculated in real time. If using the replay feature, they will be updated up to the last played bar.

Here are the available metrics and their definition:

INITIAL EQUITY: the initial amount of money we had when the strategy started, obviously...;

CURRENT EQUITY: the amount of money we have now. If using the replay feature, it will show the current equity up to the last bar played. The number on it's right side shows how many times our equity has been multiplied from it's initial value;

TRADE COUNT: how many trades were taken;

WIN COUNT: how many of those trades were wins. The percentage at the right side is the strategy WIN RATE;

AVG GAIN PER TRADE: the average percentage gain per trade. Very small values can indicate a fragile strategy that can behave in unexpected ways under high volatility conditions;

AVG GAIN PER WIN: the average percentage gain of trades that were profitable;

AVG GAIN PER LOSS: the average percentage loss on trades that were not profitable;

EQUITY MAX DD: the maximum drawdown experienced by our equity during the entire strategy backtest;

TRADE MAX DD: the maximum drawdown experienced by our equity after one single trade;

AVG MONTHLY RETURN: the compound monthly return that our strategy was able to create during the backtested period;

AVG ANNUAL RETURN: this is the strategy's CAGR (compound annual growth rate);

ELAPSED MONTHS: number of months since the backtest started;

RISK/REWARD RATIO: shows how profitable the strategy is for the amount of risk it takes. Values above 1 are very good (and rare). This is calculated as follows: (Avg Annual Return) / mod(Equity Max DD). Where mod() is the same as math.abs();

AVAILABLE SETTINGS:

SPREAD: specify your broker's asset spread

ENABLE LONGS / SHORTS: you can keep both enable or chose to take trades in only one direction

MINIMUM BARS CLOSED: to avoid trading before indicators such as a slow moving average have had time to populate, you can manually set the number of bars to wait before allowing trades.

INITIAL EQUITY: you can specify your starting equity

EXPOSURE: is the percentage of equity you wish to risk per trade. When using stops, the strategy will automatically calculate your position size to match the exposure with the stop distance. If you are not using stops then your trade volume will be the percentage of equity specified here. 100 means you'll enter trades with all your equity and 200 means you'll use a 2x leverage.

MAX LEVERAGE ALLOWED: In some situations a short stop distance can create huge levels of leverage. If you want to limit leverage to a maximum value you can set it here.

SEVERAL PLOTTING OPTIONS: You'll be able to specify which of the framework visuals you wish to see drawn on the chart.

FRAMEWORK **LIMITATIONS**:

When stop and target are both triggered in the same candle, this framework isn't able to enter faster timeframes to check which one was triggered first, so it will take the pessimistic assumption and annul the take profit signal;

This framework doesn't support pyramiding;

This framework doesn't support both long and short positions to be active at the same time. So for example, if a short signal is received while a long trade is open, the framework will close the long trade and then open a short trade;

FINAL CONSIDERATIONS:

I've been using this framework for a good time and I find it's better to use and easier to analyze a strategy's performance then relying on the oficial pine script strategy tester. However, I CANNOT GUARANTEE IT TO BE BUG FREE.

**PLEASE PERFORM A MANUAL BACKTEST BEFORE USING ANY STRATEGY WITH REAL MONEY**

Filtered MACD with Backtest [UAlgo]The "Filtered MACD with Backtest " indicator is an advanced trading tool designed for the TradingView platform. It combines the Moving Average Convergence Divergence (MACD) with additional filters such as Moving Average (MA) and Average Directional Index (ADX) to enhance trading signals. This indicator aims to provide more reliable entry and exit points by filtering out noise and confirming trends. Additionally, it includes a comprehensive backtesting module to simulate trading strategies and assess their performance based on historical data. The visual backtest module allows traders to see potential trades directly on the chart, making it easier to evaluate the effectiveness of the strategy.

🔶 Customizable Parameters :

Price Source Selection: Users can choose their preferred price source for calculations, providing flexibility in analysis.

Filter Parameters:

MA Filter: Option to use a Moving Average filter with types such as EMA, SMA, WMA, RMA, and VWMA, and a customizable length.

ADX Filter: Option to use an ADX filter with adjustable length and threshold to determine trend strength.

MACD Parameters: Customizable fast length, slow length, and signal smoothing for the MACD indicator.

Backtest Module:

Entry Type: Supports "Buy and Sell", "Buy", and "Sell" strategies.

Stop Loss Types: Choose from ATR-based, fixed point, or X bar high/low stop loss methods.

Reward to Risk Ratio: Set the desired take profit level relative to the stop loss.

Backtest Visuals: Display entry, stop loss, and take profit levels directly on the chart with

colored backgrounds.

Alerts: Configurable alerts for buy and sell signals.

🔶 Filtered MACD : Understanding How Filters Work with ADX and MA

ADX Filter:

The Average Directional Index (ADX) measures the strength of a trend. The script calculates ADX using the user-defined length and applies a threshold value.

Trading Signals with ADX Filter:

Buy Signal: A regular MACD buy signal (crossover of MACD line above the signal line) is only considered valid if the ADX is above the set threshold. This suggests a stronger uptrend to potentially capitalize on.

Sell Signal: Conversely, a regular MACD sell signal (crossunder of MACD line below the signal line) is only considered valid if the ADX is above the threshold, indicating a stronger downtrend for potential shorting opportunities.

Benefits: The ADX filter helps avoid whipsaws or false signals that might occur during choppy market conditions with weak trends.

MA Filter:

You can choose from various Moving Average (MA) types (EMA, SMA, WMA, RMA, VWMA) for the filter. The script calculates the chosen MA based on the user-defined length.

Trading Signals with MA Filter:

Buy Signal: A regular MACD buy signal is only considered valid if the closing price is above the MA value. This suggests a potential uptrend confirmed by the price action staying above the moving average.

Sell Signal: Conversely, a regular MACD sell signal is only considered valid if the closing price is below the MA value. This suggests a potential downtrend confirmed by the price action staying below the moving average.

Benefits: The MA filter helps identify potential trend continuation opportunities by ensuring the price aligns with the chosen moving average direction.

Combining Filters:

You can choose to use either the ADX filter, the MA filter, or both depending on your strategy preference. Using both filters adds an extra layer of confirmation for your signals.

🔶 Backtesting Module

The backtesting module in this script allows you to visually assess how the filtered MACD strategy would have performed on historical data. Here's a deeper dive into its features:

Backtesting Type: You can choose to backtest for buy signals only, sell signals only, or both. This allows you to analyze the strategy's effectiveness in different market conditions.

Stop-Loss Types: You can define how stop-loss orders are placed:

ATR (Average True Range): This uses a volatility measure (ATR) multiplied by a user-defined factor to set the stop-loss level.

Fixed Point: This allows you to specify a fixed dollar amount or percentage value as the stop-loss.

X bar High/Low: This sets the stop-loss at a certain number of bars (defined by the user) above/below the bar's high (for long positions) or low (for short positions).

Reward-to-Risk Ratio: Define the desired ratio between your potential profit and potential loss on each trade. The backtesting module will calculate take-profit levels based on this ratio and the stop-loss placement.

🔶 Disclaimer:

Use with Caution: This indicator is provided for educational and informational purposes only and should not be considered as financial advice. Users should exercise caution and perform their own analysis before making trading decisions based on the indicator's signals.

Not Financial Advice: The information provided by this indicator does not constitute financial advice, and the creator (UAlgo) shall not be held responsible for any trading losses incurred as a result of using this indicator.

Backtesting Recommended: Traders are encouraged to backtest the indicator thoroughly on historical data before using it in live trading to assess its performance and suitability for their trading strategies.

Risk Management: Trading involves inherent risks, and users should implement proper risk management strategies, including but not limited to stop-loss orders and position sizing, to mitigate potential losses.

No Guarantees: The accuracy and reliability of the indicator's signals cannot be guaranteed, as they are based on historical price data and past performance may not be indicative of future results.

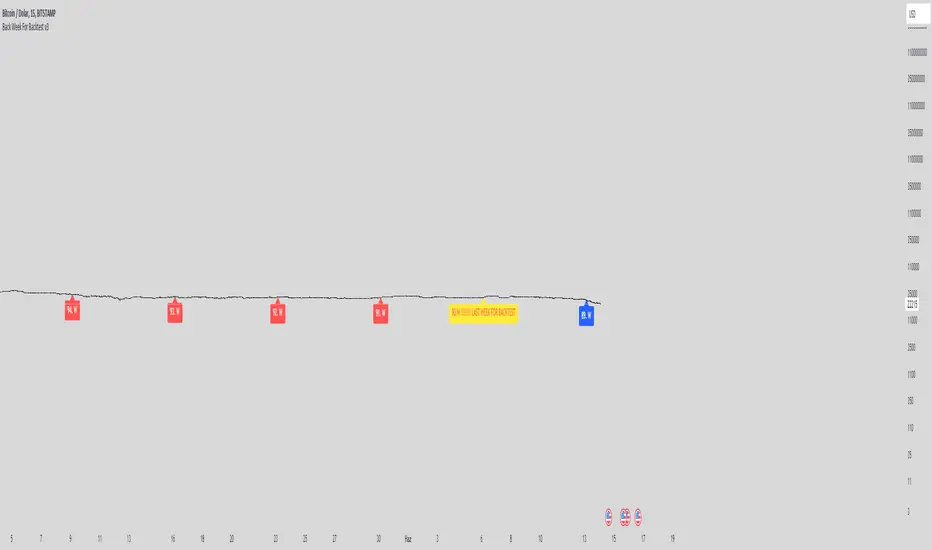

Back Week For BacktestIt is Backtest Calculator For Essential and Plus plan holders, the length of available intraday data is calculated as follows: from now to 6 weeks back multiplied by timeframe(in minutes), i.e. you can go 6 weeks back on the 1-minute chart, 12 weeks back on the 2-minute chart, 30 weeks back on the 5-minute chart, 90 weeks back on the 15-minute chart and so on. The higher timeframe is selected, the more intraday data is available.

This show creates a weekday label based on the data in the plans allowed by TradingView. This show creates a weekday label based on the data in the plans allowed by TradingView. How much data is available for Bar Replay? According to the article, we can replay 6 weeks backwards for a 1-minute chart. This indicator is a label that shows how far we can go back, consisting of multiplying each minute by 6 between 1 minute and 60 minutes.

1 minute => 6 week backtest

2 minutes => 12 week backtest

.....

15 minutes => 90 week backtest

...

59 minutes => 354 week backtest

Session candles & reversals / quantifytools— Overview

Like traditional candles, session based candles are a visualization of open, high, low and close values, but based on session time periods instead of typical timeframes such as daily or weekly. Session candles are formed by fetching price at session start (open), highest price during session (high), lowest price during session (low) and price at session end (close). On top of candles, session based moving average is formed and session reversals detected. Session reversals are also backtested, using win rate and magnitude metrics to better understand what to expect from session reversals and which ones have historically performed the best.

By default, following session time periods are used:

Session #1: London (08:00 - 17:00, UTC)

Session #2: New York (13:00 - 22:00, UTC)

Session #3: Sydney (21:00 - 06:00, UTC)

Session #4: Tokyo (00:00 - 09:00, UTC)

Session time periods can be changed via input menu.

— Reversals

Session reversals are patterns that show a rapid change in direction during session. These formations are more familiarly known as wicks or engulfing candles. Following criteria must be met to qualify as a session reversal:

Wick up:

Lower high, lower low, close >= 65% of session range (0% being the very low, 100% being the very high) and open >= 40% of session range.

Wick down:

Higher high, higher low, close <= 35% of session range and open <= 60% of session range.

Engulfing up:

Higher high, lower low, close >= 65% of session range.

Engulfing down:

Higher high, lower low, close <= 35% of session range.

Session reversals are always based on prior corresponding session , e.g. to qualify as a NY session engulfing up, NY session must have a higher high and lower low relative to prior NY session , not just any session that has taken place in between. Session reversals should be viewed the same way wicks/engulfing formations are viewed on traditional timeframe based candles. Essentially, wick reversals (light green/red labels) tell you most of the motion during session was reversed. Engulfing reversals (dark green/red labels) on the other hand tell you all of the motion was reversed and new direction set.

— Backtesting

Session reversals are backtested using win rate and magnitude metrics. A session reversal is considered successful when next corresponding session closes higher/lower than session reversal close . Win rate is formed by dividing successful session reversal count with total reversal count, e.g. 5 successful reversals up / 10 reversals up total = 50% win rate. Win rate tells us what are the odds (historically) of session reversal producing a clean supporting move that was persistent enough to close that way too.

When a session reversal is successful, its magnitude is measured using percentage increase/decrease from session reversal close to next corresponding session high/low . If NY session closes higher than prior NY session that was a reversal up, the percentage increase from prior session close (reversal close) to current session high is measured. If NY session closes lower than prior NY session that was a reversal down, the percentage decrease from prior session close to current session low is measured.

Average magnitude is formed by dividing all percentage increases/decreases with total reversal count, e.g. 10 total reversals up with 1% increase each -> 10% net increase from all reversals -> 10% total increase / 10 total reversals up = 1% average magnitude. Magnitude metric supports win rate by indicating the depth of successful session reversal moves.

To better understand the backtesting calculations and more importantly to verify their validity, backtesting visuals for each session can be plotted on the chart:

All backtesting results are shown in the backtesting panel on top right corner, with highest win rates and magnitude metrics for both reversals up and down marked separately. Note that past performance is not a guarantee of future performance and session reversals as they are should not be viewed as a complete strategy for long/short plays. Always make sure reversal count is sufficient to draw reliable conclusions of performance.

— Session moving average

Users can form a session based moving average with their preferred smoothing method (SMA , EMA , HMA , WMA , RMA) and length, as well as choose which sessions to include in the moving average. For example, a moving average based on New York and Tokyo sessions can be formed, leaving London and Sydney completely out of the calculation.

— Visuals

By default, script hides your candles/bars, although in the case of candles borders will still be visible. Switching to bars/line will make your regular chart visuals 100% hidden. This setting can be turned off via input menu. As some sessions overlap, each session candle can be separately offsetted forward, clearing the overlaps. Users can also choose which session candles to show/hide.

Session periods can be highlighted on the chart as a background color, applicable to only session candles that are activated. By default, session reversals are referred to as L (London), N (New York), S (Sydney) and T (Tokyo) in both reversal labels and backtesting table. By toggling on "Numerize sessions", these will be replaced with 1, 2, 3 and 4. This will be helpful when using a custom session that isn't any of the above.

Visual settings example:

Session candles are plotted in two formats, using boxes and lines as well as plotcandle() function. Session candles constructed using boxes and lines will be clear and much easier on the eyes, but will apply only to first 500 bars due to Tradingview related limitations. Rest of the session candles go back indefinitely, but won't be as clean:

All colors can be customized via input menu.

— Timeframe & session time period considerations

As a rule of thumb, session candles should be used on timeframes at or below 1H, as higher timeframes might not match with session period start/end, leading to incorrect plots. Using 1 hour timeframe will bring optimal results as greatest amount historical data is available without sacrificing accuracy of OHLC values. If you are using a custom session that is not based on hourly period (e.g. 08:00 - 15:00 vs. 08.00 - 15.15) make sure you are using a timeframe that allows correct plots.

Session time periods applied by default are rough estimates and might be out of bounds on some charts, like NYSE listed equities. This is rarely a problem on assets that have extensive trading hours, like futures or cryptocurrency. If a session is out of bounds (asset isn't traded during the set session time period) the script won't plot given session candle and its backtesting metrics will be NA. This can be fixed by changing the session time periods to match with given asset trading hours, although you will have to consider whether or not this defeats the purpose of having candles based on sessions.

— Practical guide

Whether based on traditional timeframes or sessions, reversals should always be considered as only one piece of evidence of price turning. Never react to them without considering other factors that might support the thesis, such as levels and multi-timeframe analysis. In short, same basic charting principles apply with session candles that apply with normal candles. Use discretion.

Example #1 : Focusing efforts on session reversals at distinct support/resistance levels

A reversal against a level holds more value than a reversal by itself, as you know it's a placement where liquidity can be expected. A reversal serves as a confirming reaction for this expectation.

Example #2 : Focusing efforts on highest performing reversals and avoiding poorly performing ones

As you have data backed evidence of session reversal performance, it makes sense to focus your efforts on the ones that perform best. If some session reversal is clearly performing poorly, you would want to avoid it, since there's nothing backing up its validity.

Example #3 : Reversal clusters

Two is better than one, three is better than two and so on. If there are rapid changes in direction within multiple sessions consecutively, there's heavier evidence of a dynamic shift in price. In such case, it makes sense to hold more confidence in price halting/turning.

Quantitative Backtesting Panel + ROI Table - ShortsThis script is an aggregate of a backtesting panel with quantitative metrics, ROI table and open ROI reader. It also contains a mechanism for having a fixed percentage stop loss, similar to native TV backtester. For shorts only.

Backtesting Panel:

- Certain metrics are color coded, with green being good performance, orange being neutral, red being undesirable.

• ROI : return with the system, in %

• ROI(COMP=1): return if money is compounded at a rate of 100%

• Hit rate: accuracy of the system, as a %

• Profit factor: gross profit/gross loss

• Maximum drawdown: the maximum value from a peak to a successive trough of the system's equity curve

• MAE: Maximum Adverse Excursion. The biggest loss of a trade suffered while the position is still open

• Total trades: total number of closed trades

• Max gain/max loss: shows the biggest win over the biggest loss suffered

• Sharpe ratio: measures the performance of the system with adjusted risk (no comparison to risk-free asset)

• CAGR: Compound Annual Growth Rate. The mean annual rate of growth of the system of n years (provided n>1)

• Kurtosis: measures how heavily the tails of the distribution differ from that of a normal distribution (symmetric on both sides of mean where mean=0, standard deviation=1). A normal distribution has a kurtosis of 3, and skewness of 0. The kurtosis indicates whether or not the tails of the returns contain extreme values

• Skewness: measures the symmetry of the distribution of returns

- Leptokurtic: K > 0. Having more kurtosis than a normal distribution. It's stretched up and to the side too (2nd pic down). High kurtosis (leptokurtic) is bad as the wider tails (called heavy tails) suggest there is relatively high probability of extreme events

- Mesokurtic: K =0. Having the same kurtosis as a normal distribution

- Platykurtic: K < 0. Having less kurtosis than a normal distribution. This suggests there are light tails and fewer extreme events in the distribution

- Skewness is good: +/- 0.5 (fairly symmetrical)

- Skewness is average: -1 to -0.5 or 0.5 to 1 (moderately skewed)

- Skewness is bad: > +/- 1 (highly skewed)

Evolving ROI table:

- The table of ROI values evolve with the year and month. The sum of each year is given. Please avoid using it on non-cryptocurrencies or any market whose trading session is not 24/7

Open ROI reader:

- At the top center is the open ROI of a trade

Quantitative Backtesting Panel + ROI Table - LongsThis script is an aggregate of a backtesting panel with quantitative metrics, ROI table and open ROI reader. It also contains a mechanism for having a fixed percentage stop loss, similar to native TV backtester. For longs only.

Backtesting Panel:

- Certain metrics are color coded, with green being good performance, orange being neutral, red being undesirable.

• ROI : return with the system, in %

• ROI(COMP=1): return if money is compounded at a rate of 100%

• Hit rate: accuracy of the system, as a %

• Profit factor: gross profit/gross loss

• Maximum drawdown: the maximum value from a peak to a successive trough of the system's equity curve

• MAE: Maximum Adverse Excursion. The biggest loss of a trade suffered while the position is still open

• Total trades: total number of closed trades

• Max gain/max loss: shows the biggest win over the biggest loss suffered

• Sharpe ratio: measures the performance of the system with adjusted risk (no comparison to risk-free asset)

• CAGR: Compound Annual Growth Rate. The mean annual rate of growth of the system of n years (provided n>1)

• Kurtosis: measures how heavily the tails of the distribution differ from that of a normal distribution (symmetric on both sides of mean where mean=0, standard deviation=1). A normal distribution has a kurtosis of 3, and skewness of 0. The kurtosis indicates whether or not the tails of the returns contain extreme values

• Skewness: measures the symmetry of the distribution of returns

- Leptokurtic: K > 0. Having more kurtosis than a normal distribution. It's stretched up and to the side too (2nd pic down). High kurtosis (leptokurtic) is bad as the wider tails (called heavy tails) suggest there is relatively high probability of extreme events

- Mesokurtic: K =0. Having the same kurtosis as a normal distribution

- Platykurtic: K < 0. Having less kurtosis than a normal distribution. This suggests there are light tails and fewer extreme events in the distribution

- Skewness is good: +/- 0.5 (fairly symmetrical)

- Skewness is average: -1 to -0.5 or 0.5 to 1 (moderately skewed)

- Skewness is bad: > +/- 1 (highly skewed)

Evolving ROI table:

- The table of ROI values evolve with the year and month. The sum of each year is given. Please avoid using it on non-cryptocurrencies or any market whose trading session is not 24/7

Open ROI reader:

- At the top center is the open ROI of a trade

Regression Channel, Candles and Candlestick Patterns by MontyRegression Candles by ugurvu

Regression Channel by Tradingview

All Candlestick Patterns By Tradingview

This script was combined for a friend of mine who needed this.

This Script has regression candles by ugurvu, Regression channel and Candlestick patterns by tradingview.

The intention was to fuse these together so more information can be processed on the cost of a single indicator.

EMA Cross (data chaining template)Hello Traders! This is the source code for a simple EMA Cross indicator that can be chained to other indicators or another instance of itself as a filter.

The code is fully commented to guide you in building your own chain of indicators based on your ideas and trading plans.

All the best,

Val - Protervus Trading

Breakout Probability (Expo)█ Overview

Breakout Probability is a valuable indicator that calculates the probability of a new high or low and displays it as a level with its percentage. The probability of a new high and low is backtested, and the results are shown in a table— a simple way to understand the next candle's likelihood of a new high or low. In addition, the indicator displays an additional four levels above and under the candle with the probability of hitting these levels.

The indicator helps traders to understand the likelihood of the next candle's direction, which can be used to set your trading bias.

█ Calculations

The algorithm calculates all the green and red candles separately depending on whether the previous candle was red or green and assigns scores if one or more lines were reached. The algorithm then calculates how many candles reached those levels in history and displays it as a percentage value on each line.

█ Example

In this example, the previous candlestick was green; we can see that a new high has been hit 72.82% of the time and the low only 28.29%. In this case, a new high was made.

█ Settings

Percentage Step

The space between the levels can be adjusted with a percentage step. 1% means that each level is located 1% above/under the previous one.

Disable 0.00% values

If a level got a 0% likelihood of being hit, the level is not displayed as default. Enable the option if you want to see all levels regardless of their values.

Number of Lines

Set the number of levels you want to display.

Show Statistic Panel

Enable this option if you want to display the backtest statistics for that a new high or low is made. (Only if the first levels have been reached or not)

█ Any Alert function call

An alert is sent on candle open, and you can select what should be included in the alert. You can enable the following options:

Ticker ID

Bias

Probability percentage

The first level high and low price

█ How to use

This indicator is a perfect tool for anyone that wants to understand the probability of a breakout and the likelihood that set levels are hit.

The indicator can be used for setting a stop loss based on where the price is most likely not to reach.

The indicator can help traders to set their bias based on probability. For example, look at the daily or a higher timeframe to get your trading bias, then go to a lower timeframe and look for setups in that direction.

-----------------

Disclaimer

The information contained in my Scripts/Indicators/Ideas/Algos/Systems does not constitute financial advice or a solicitation to buy or sell any securities of any type. I will not accept liability for any loss or damage, including without limitation any loss of profit, which may arise directly or indirectly from the use of or reliance on such information.

All investments involve risk, and the past performance of a security, industry, sector, market, financial product, trading strategy, backtest, or individual's trading does not guarantee future results or returns. Investors are fully responsible for any investment decisions they make. Such decisions should be based solely on an evaluation of their financial circumstances, investment objectives, risk tolerance, and liquidity needs.

My Scripts/Indicators/Ideas/Algos/Systems are only for educational purposes!

Backtesting- IndicatorFor anyone interested, Here is an example of how to put backtesting results into an Indicator. This calculates the same values as you find in the Summary Screen of the built in Strategy backtester. This will use the same result size as the standard backtester i.e. 5 minute chart grabs roughly 1 month of data, 1 minute chart grabs 1 week of data, etc... I tried to keep this as self-contained as possible so I put most of the code for the results in the bottom of the Indicator. The results stop at the last completed trade signal i.e. a Buy has a Sell to it. This is the same indicator I posted earlier with the PCT Trailing StopLoss so you will see that code in here as well. As said in my previous posting, the indicator is just a simple EMA crossover to give it something to do and I would not recommend using this indicator on its own, but instead copy the code to your own indicator if you find it useful. I also left the code in so that you can switch back to a Strategy if you want to verify the results.

Additional Notes:

- The results are within an acceptable margin of error due to the fact that the Indicator is having to calculate based on when the Buy and Sell Signal occur as opposed to when actual trades occur like in the Strategy Backtester

- I was trying to find a way to set the number of Buy Signals to use i.e. show me the results from the past 100 trades but couldn't sort out the logic. I am open to suggestions. Also keep in mind I am not a coder by profession so if you have any ideas on that front, please explain it to me as though I am a 5 year old child and provide code examples if possible :)

- I included the Strategy results in the Screen Shots so that you can see where the results line up.

Additional Additional Note:

This is not financial advice. Use at your own risk.

Manual Backtest - Flat the ChartThis script is an utility tool for manual backtesting.

The main problem in backtesting a discretionary strategy is the bias of knowing the future result of the market, in this way all the market will be crushed into a flat line, this way you can avoid bias.

The way to use this indicator is easy and made by 4 step:

Step 1 : add to an asset you won't backtest and put the auto scale on

Step 2 : go to the asset you will backtest and scroll left until the date you want to start

Step 3 : use the replay function of tradingview (15 min chart won't go back more than 18 month)

Step 4: toggle off the indicator or remove from the chart (untill next asset to backtest)

That's not a complex indicator but is what you need to do a fair backtesting

Zendog SHORT DCA Trigger RSI+StochRSIThis is a script that generates a SELL signal by combining RSI and Stochastic RSI into the same script and that can easily be integrated into an external Backtester like the one I published.

The script uses default values for RSI and Stochastic RSI overbought conditions.

They should be adjusted for specific assets and timeframes so they better match the current trend. Please beware you might overfit settings to match a short timeframe trend (like a few days or hours). If this is the case once the trend changes the signals will not be accurate.

The purpose of this script is to provide some pine code that can be used to further combine multiple indicators into a SHORT Deal Start signal.

Integration with the Zendog Backtster:

- add the backtester on the chart

- add this script on the chart

- in the Zendog backtester Deal start type select "External indicator"

- in the Zendog backtester Indicator source and value select "Zendog SHORT DCA Trigger RSI+StochRSI: SIGNAL"

Zendog LONG DCA Trigger RSI+StochRSIThis is a script that generates a BUY signal by combining RSI and Stochastic RSI into the same script and that can easily be integrated into an external Backtester like the one I published.

The script uses default values for RSI and Stochastic RSI oversold conditions.

They should be adjusted for specific assets and timeframes so they better match the current trend. Please beware you might overfit settings to match a short timeframe trend (like a few days or hours). If this is the case once the trend changes the signals will not be accurate.

The purpose of this script is to provide some pine code that can be used to further combine multiple indicators into a LONG Deal Start signal.

Integration with the Zendog Backtster:

- add the backtester on the chart

- add this script on the chart

- in the Zendog backtester Deal start type select "External indicator"

- in the Zendog backtester Indicator source and value select "Zendog LONG DCA Trigger RSI+StochRSI: SIGNAL"

QFL bull bypassThis bypass indicator triggers plots 1 when the price is above the QFL base.

This can be used as a "bypass" by a consumer indicator that can skip trades when the bypass is triggering.

You can use it for long and short strategies, to prevent using buy or sell signals in areas were the price is either overextended.

QFL works better in 1, 2 or 4 hours timeframes.

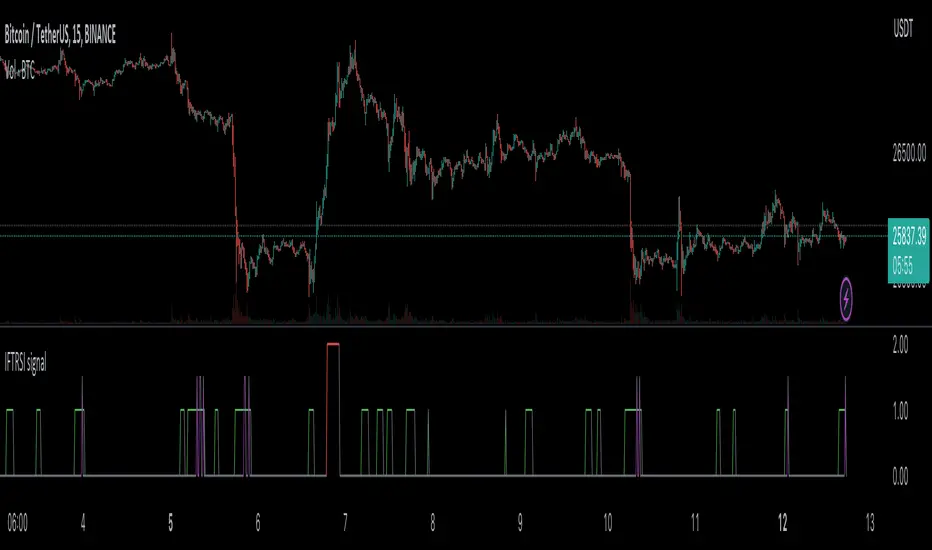

Inverse Fisher Transform on RSI for backtest w/alertsThis version of the Inverse Fisher Transform on RSI comes with support for

1) Backtesting with Gavin's backtest script

2) Bypass, you can use another indicator to pause buy signals from this indicator. Just create another indicator that plots "1" whenever you want to activate the bypass on the IFTRSI signal.

3) Independent buy and sell level thresholds. Some tokens perform better with a higher sell level, even levels as high as 0.996, sometimes the buy level can also be relaxed to even 0.6 and get incredible results on the 5 minute chart.

4) alerts for Buy and Sell signals

Make sure you add Gavin's backtest and select external signal and this indicator as the source.

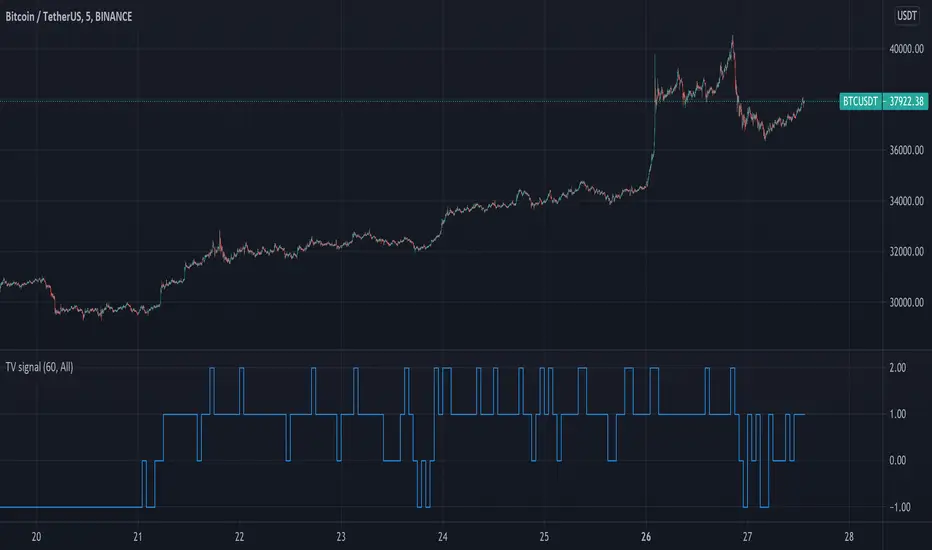

TV signal for DCA backtestThis script allows you to backtest Trading View's "Technical Ratings" (Buy, Strong buy, Sell, Strong Sell) using Gavin's backtest script.

To use it add the backtest script to the chart together with this script and then from the back test settings connect the external indicator. You should select "TV Signal" as the source.

Backtesting works best on the 5m chart, but you can still change this script from its settings to higher timeframes.

Encoding

Buy is 1

Strong Buy is 2

Sell is -1

Strong Sell is -2

In the backtest script you can decide which rating you want to use for open deal and which one for close deal.

For example, if you were backtesting a long bot you could enter a long position when TV signal is Buy (1) and close the deal when TV signal is Sell (-1).

You have the full flexibility to decide which technical rating to use for your backtesting.

Enjoy!

Smart AlertsThis indicator provides back-tested signals and alerts from multiple technical indicators.

No more guessing whether or not you should trust an indicator. See your indicators' past performance at a glance.

No more false alarms. Disable re-painting of signals.

When multiple indicators overlap, a Confluence indicator will print (large triangle). With your settings properly tuned, this will show a HIGH probability of a move.

Current Signal/Alert Options (more to come):

RSI Oversold

RSI Overbought

EMA Crossing Up

EMA Crossing Down

Buy Signal Confluence

Sell Signal Confluence

Instructions:

-Enable/disable individual indicators so you can fine tune one at a time

-Adjust the indicator's settings

-Adjust your trade parameters (Max Wait, Take Profit %). Signals that would have given the desired profit in the time allowed will be painted orange.

-Repeat this process with each indicator until you're satisfied

-Set-up alerts

Smart EMA SignalsThis indicator starts by plotting each time the price action crosses above or below the EMA, of which you can tune the timeframe and duration.

It then takes it a step further and plots whether or not that indicator would have given you a profitable trade, of which you can also tune the parameters (Max wait time, and % Profit).

Once you have your EMA tuned to your liking, set up alerts to notify you of a golden opportunity.

QFL single TF with alertsBacktesting compatible QFL pine script w/alerts

This version of QFL was made based on this one:

From author:

www.tradingview.com

I made the following additions according to my requirements:

- I need to use pine script 4

- I needed to avoid repainting issues so I'm not calling directly security, I'm using the wrapper function.

- There might be still repainting issues when you use "max base age" which uses the function "barssince" so be careful, you can disable it by setting its value to zero.

- Alerts so I can use it for automated trading and bots

- In order to make this signal compatible with the backtest script there's an option provided in the settings. If you enable this option this indicator will plot 1 whenever there's a BUY signal. This will allow the backtest to pick the "QFL Buy" from external indicator so it can perform the backtest.

I recommend some of these settings to start playing with the chart in 15 min / QFL in 1, 2 or 4 hours.

The higher the TF the more conservative.

QFL with 3.5% is pretty popular but you can try higher QFL percentage settings for a more conservative approach.

MACD With Trend Filter: Visual Backtest Module TemplateSample Strategy: MACD Crossover with trend filter options

MA Filter : Price Close Above MA, Search for Buy, Price Close Below MA, Search for Sell

ADX Filter : Take trade only when ADX is above certain treshold

MACD Signal : MACD Cross above signal line while under 0 line indicate Buy Signal

MACD Cross below signal line while above 0 line indicate Sell Signal

-----------------------------

Using Alert Module:

Enable Alert --> Enable TV's alert and plot signal to chart

Alert Type --> Set to take Buy only, Sell only or Both alert

----------------------------

Using Backtest Module:

Enable Backtest --> Enable Backtest simulation

Backtest Type --> Set to take Buy only, Sell only or Both

SL Type -->

ATR : Set SL in ATR times Multiplier below/above entry price

Fixed : Set SL in fixed point below entry point (in 'Dollar'). e.g. for Stocks -> 0.5 equals to 50cent while for EURUSD currency -> 0.005 equal to 50 pips

HiLo Bar : Set SL at highest/lowest wick of previous bar plus/minus Fixed point. e.g. EURUSD HiLo=3 and Fixed Point = 0.0005, buy trade will place SL 5 Pips below lowest of previous 3 bar

SL ATR Period --> Set Lookback Period used for SL's ATR calculation

SL ATR Multi --> Set ATR Multiplier for SL

SL Fixed --> Set Fixed Level for SL (Use when SL Type is either Fixed or HiLo Bar)

SL Bar --> Set Number of previous bar to check for SL placement

TP RR Ratio --> Set TP based on RR multiplier. e.g. 2 means TP level will be twice further from entry point compared to Entry-SL distance.

Notes: The point is for preliminary testing, so it only supports 1 trade at a time and no Trailing Stop

----------------------------

Disclaimer:

This script main objective is to create my personal indicator template so that i just have to modify the indicator module for preliminary testing in future.

Testing Alert Module so i can re-use it as template in future study/indicator

Testing Visual Backtest Module so i can re-use it as template in future study/indicator

i believe using Strategy function is a better approach for this but the entry/exit level seems to be hit n miss (at least for me, still trying to figure what i did wrong)

also, i rather code the strategy in other platform where i can use the more accurate tick data if i want to validate backtest statistics.

My study scripts was built only to test/visualize an idea to see its viability and if it can be used to optimize existing strategy.

credit: ADX code are originally from "ADX and DI" by @BeikabuOyaji although i re-wrote so i can have cleaner read and use RMA instead of SMA

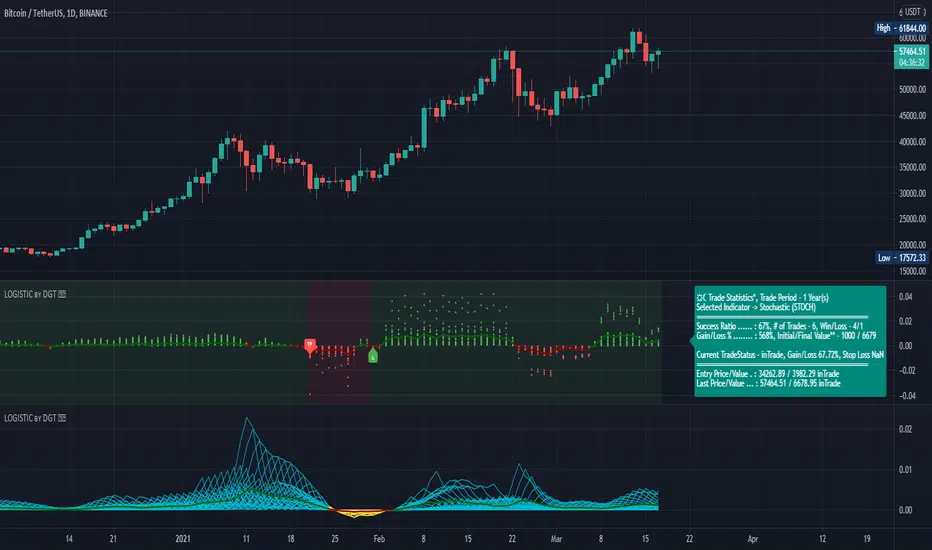

Logistic RSI, STOCH, ROC, AO, ... by DGTExperimental attemt of applying Logistic Map Equation for some of widly used indicators.

With this study "Awesome Oscillator (AO)", "Rate of Change (ROC)", "Relative Strength Index (RSI)", "Stochastic (STOCH)" and a custom interpretation of Logistic Map Equation is presented

Calculations with Logistic Map Equation makes sense when the calculated results are iterated many times within the same equation.

Here is the Logistic Map Equation : Xn+1 = r * Xn * (1 - Xn)

Where, the value of r is the key for this equation which changes amazingly the behaviour of the Logistic Map.

The value we have asigned for r is less then 1 and greater than 0 ( 0 < r < 1) and in this case the iterations performed with the maximum number of output series allowed by Pine is quite enough for our purpose and thanks to arrays we can easiliy store them for further processing

What we have as output:

Each iteration result is then plotted (excluding plotting the first iteration), as circles or line based on user preference

Values above and below zero level (0) are coloured differently to emphasis bull and bear power

Finally Standard Deviation of Array's Elements is ploted as line. Users may choose to display this line only

So where it comes the indicators "Awesome Oscillator (AO)", "Rate of Change (ROC)", "Relative Strength Index (RSI)", "Stochastic (STOCH)".

Those are the indicators whose values are assigned to our key varaiable in the Logistic Map equation forulma which is r

Further details regarding Logistic Map can found under the description of “Logistic EMA w/ Signals by DGT” study

Disclaimer:

Trading success is all about following your trading strategy and the indicators should fit within your trading strategy, and not to be traded upon solely

The script is for informational and educational purposes only. Use of the script does not constitute professional and/or financial advice. You alone have the sole responsibility of evaluating the script output and risks associated with the use of the script. In exchange for using the script, you agree not to hold dgtrd TradingView user liable for any possible claim for damages arising from any decision you make based on use of the script