Katalyst's Opening Range BreakoutKatalyst's Opening Range Breakout + No Trade Zone

📜 Overview:

This indicator allows traders to visualize the high and low of the opening range for a user-selected timeframe (e.g., 30s, 1m, 5m, 15m). It features fully customizable lines, labels, and an optional **No Trade Zone** fill to help you identify breakout levels with ease.

---

🎯 Key Features:

1. **Customizable Opening Range**:

- Select your preferred opening range duration: **30 seconds, 1 minute, 2 minutes, 5 minutes, 10 minutes, or 15 minutes**.

- The indicator calculates and plots the **high** and **low** of the selected opening range.

2. **Dynamic Line Styling**:

- Choose the **line color**, **transparency**, and **style**: **Solid, Dashed, or Dotted**.

- Lines extend to the right of the chart for clarity.

3. **No Trade Zone** *(Optional / Disabled by default)*:

- When enabled, fills the area between the high and low lines with a customizable **color and transparency**.

- Helps visually identify consolidation areas where trading might be avoided.

4. **Labels for Precision**:

- Clearly displays the **Opening Range High** and **Low** values.

- Labels are color-coded and positioned dynamically for easy interpretation.

5. **Clean and Efficient Updates**:

- The indicator deletes old lines, labels, and fills before creating new ones, ensuring a clutter-free chart.

---

⚙️ How to Use:

1. **Select Your Timeframe**:

- From the settings, choose your desired opening range duration: 30s, 1m, 2m, 5m, 10m, or 15m.

2. **Customize the Visuals**:

- Adjust line color, style, and transparency.

- Enable the **No Trade Zone** for a transparent background fill between the high and low lines.

3. **Interpret the Breakout**:

- Watch for price movements above or below the **opening range** to identify potential breakout opportunities.

---

🛠 Settings:

Opening Range Duration: Select the timeframe for the opening range (30s, 1m, 2m, 5m, 10m, 15m).

Line Color: Set the color of the range lines.

Line Transparency: Adjust the transparency of the lines (0 = solid, 100 = invisible).

Line Style: Choose line style: Solid, Dashed, or Dotted.

Label Colors: Customize the label colors for the high and low values.

Enable No Trade Zone: Fill the area between high and low lines with a transparent color.

No Trade Zone Color: Set the fill color for the no trade zone.

No Trade Zone Transparency: Adjust the transparency of the no trade zone fill.

---

📈 Ideal For

Day traders and scalpers looking to trade **breakouts**.

Traders who want to identify areas of consolidation visually.

Anyone who relies on the **opening range** for their trading strategy.

---

🔍 Example Usage:

Set the opening range to **5 minutes** and enable the **No Trade Zone** with a light red fill.

Watch for price to break above or below the high/low lines to signal potential trade opportunities.

---

✨ Why Use This Indicator?

This script simplifies your breakout strategy by providing a clear, visually appealing representation of the opening range. The flexible customization options and the optional **No Trade Zone** make it a powerful tool for identifying high-probability trades.

---

Let me know if you need any additional tweaks or clarifications for this description. It's all set to help traders understand and use your powerful script! 🚀📈

Chop Zone

Advanced Choppiness Indicator with CPMA"The Advanced Choppiness Indicator with CPMA is a technical analysis tool designed to assist traders in identifying choppy market conditions and determining trend direction. It combines two key components: the Choppiness Index and a Custom Price Moving Average (CPMA).

The Choppiness Index is calculated using the Average True Range (ATR), which measures market volatility. It compares the ATR to the highest high and lowest low over a specified period. A higher Choppiness Index value indicates choppier market conditions, while a lower value suggests smoother and more directional price movements.

The CPMA is a custom moving average that takes into account various price types, including the close, high, low, and other combinations. It calculates the average of these price types over a specific length. The CPMA provides a smoother trend line that can help identify support and resistance levels more accurately than traditional moving averages.

When using this indicator, pay attention to the following elements:

Yellow range boxes: These indicate choppy zones, where market conditions are characterized by low momentum and erratic price action. Avoid entering trades during these periods.

Histogram bars: Green bars suggest an uptrend, while red bars indicate a downtrend. These bars are based on the CPMA and can help confirm the prevailing trend direction.

CPMA angle: The angle of the CPMA line provides further insight into the trend. A positive angle indicates an uptrend, while a negative angle suggests a downtrend.

Choppiness thresholds: The indicator includes user-defined thresholds for choppiness. Values above the high threshold indicate high choppiness, while values below the low threshold suggest low choppiness.

Trade decisions: Consider the information provided by the indicator to make informed trading decisions. Avoid trading during choppy zones and consider entering trades in the direction of the prevailing trend.

Remember that the indicator's parameters, such as ATR length and CPMA length, can be adjusted to suit your trading preferences and timeframe. However, it's important to use this indicator in conjunction with other technical analysis tools and your trading strategy for comprehensive market analysis."

By combining the Choppiness Index, CPMA, and other visual cues, this indicator aims to help traders identify suitable trading conditions and make more informed decisions based on market trends and volatility.

Simple Chop ZoneThe original Chop Zone indicator by Trading View is good, but has a few limitations which I've addressed in this one

Too many colors which confuse and/or overwhelm users like me

Inability to change the EMA period

This one has just 3 customizable colors for

Uptrend - default = Turquoise

Downtrend - default = red

Everything else - default = lime

And you can set your own EMA length. The default is 34 as per the original Chop Zone indicator

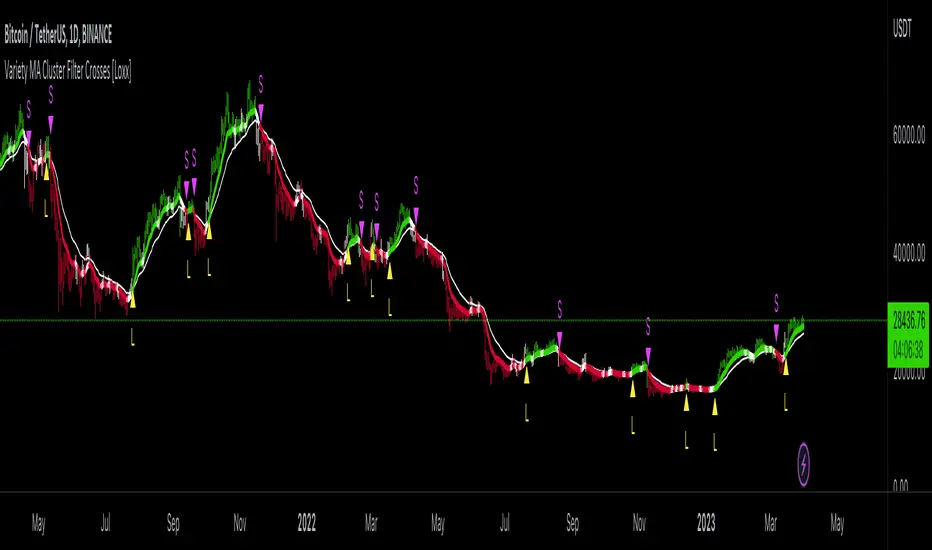

Variety MA Cluster Filter Crosses [Loxx]What is a Cluster Filter?

One of the approaches to determining a useful signal (trend) in stream data. Small filtering (smoothing) tests applied to market quotes demonstrate the potential for creating non-lagging digital filters (indicators) that are not redrawn on the last bars.

Standard Approach

This approach is based on classical time series smoothing methods. There are lots of articles devoted to this subject both on this and other websites. The results are also classical:

1. The changes in trends are displayed with latency;

2. Better indicator (digital filter) response achieved at the expense of smoothing quality decrease;

3. Attempts to implement non-lagging indicators lead to redrawing on the last samples (bars).

And whereas traders have learned to cope with these things using persistence of economic processes and other tricks, this would be unacceptable in evaluating real-time experimental data, e.g. when testing aerostructures.

The Main Problem

It is a known fact that the majority of trading systems stop performing with the course of time, and that the indicators are only indicative over certain intervals. This can easily be explained: market quotes are not stationary. The definition of a stationary process is available in Wikipedia:

A stationary process is a stochastic process whose joint probability distribution does not change when shifted in time.

Judging by this definition, methods of analysis of stationary time series are not applicable in technical analysis. And this is understandable. A skillful market-maker entering the market will mess up all the calculations we may have made prior to that with regard to parameters of a known series of market quotes.

Even though this seems obvious, a lot of indicators are based on the theory of stationary time series analysis. Examples of such indicators are moving averages and their modifications. However, there are some attempts to create adaptive indicators. They are supposed to take into account non-stationarity of market quotes to some extent, yet they do not seem to work wonders. The attempts to "punish" the market-maker using the currently known methods of analysis of non-stationary series (wavelets, empirical modes and others) are not successful either. It looks like a certain key factor is constantly being ignored or unidentified.

The main reason for this is that the methods used are not designed for working with stream data. All (or almost all) of them were developed for analysis of the already known or, speaking in terms of technical analysis, historical data. These methods are convenient, e.g., in geophysics: you feel the earthquake, get a seismogram and then analyze it for few months. In other words, these methods are appropriate where uncertainties arising at the ends of a time series in the course of filtering affect the end result.

When analyzing experimental stream data or market quotes, we are focused on the most recent data received, rather than history. These are data that cannot be dealt with using classical algorithms.

Cluster Filter

Cluster filter is a set of digital filters approximating the initial sequence. Cluster filters should not be confused with cluster indicators.

Cluster filters are convenient when analyzing non-stationary time series in real time, in other words, stream data. It means that these filters are of principal interest not for smoothing the already known time series values, but for getting the most probable smoothed values of the new data received in real time.

Unlike various decomposition methods or simply filters of desired frequency, cluster filters create a composition or a fan of probable values of initial series which are further analyzed for approximation of the initial sequence. The input sequence acts more as a reference than the target of the analysis. The main analysis concerns values calculated by a set of filters after processing the data received.

In the general case, every filter included in the cluster has its own individual characteristics and is not related to others in any way. These filters are sometimes customized for the analysis of a stationary time series of their own which describes individual properties of the initial non-stationary time series. In the simplest case, if the initial non-stationary series changes its parameters, the filters "switch" over. Thus, a cluster filter tracks real time changes in characteristics.

Cluster Filter Design Procedure

Any cluster filter can be designed in three steps:

1. The first step is usually the most difficult one but this is where probabilistic models of stream data received are formed. The number of these models can be arbitrary large. They are not always related to physical processes that affect the approximable data. The more precisely models describe the approximable sequence, the higher the probability to get a non-lagging cluster filter.

2. At the second step, one or more digital filters are created for each model. The most general condition for joining filters together in a cluster is that they belong to the models describing the approximable sequence.

3. So, we can have one or more filters in a cluster. Consequently, with each new sample we have the sample value and one or more filter values. Thus, with each sample we have a vector or artificial noise made up of several (minimum two) values. All we need to do now is to select the most appropriate value.

An Example of a Simple Cluster Filter

For illustration, we will implement a simple cluster filter corresponding to the above diagram, using market quotes as input sequence. You can simply use closing prices of any time frame.

1. Model description. We will proceed on the assumption that:

The aproximate sequence is non-stationary, i.e. its characteristics tend to change with the course of time.

The closing price of a bar is not the actual bar price. In other words, the registered closing price of a bar is one of the noise movements, like other price movements on that bar.

The actual price or the actual value of the approximable sequence is between the closing price of the current bar and the closing price of the previous bar.

The approximable sequence tends to maintain its direction. That is, if it was growing on the previous bar, it will tend to keep on growing on the current bar.

2. Selecting digital filters. For the sake of simplicity, we take two filters:

The first filter will be a variety filter calculated based on the last closing prices using the slow period. I believe this fits well in the third assumption we specified for our model.

Since we have a non-stationary filter, we will try to also use an additional filter that will hopefully facilitate to identify changes in characteristics of the time series. I've chosen a variety filter using the fast period.

3. Selecting the appropriate value for the cluster filter.

So, with each new sample we will have the sample value (closing price), as well as the value of MA and fast filter. The closing price will be ignored according to the second assumption specified for our model. Further, we select the МА or ЕМА value based on the last assumption, i.e. maintaining trend direction:

For an uptrend, i.e. CF(i-1)>CF(i-2), we select one of the following four variants:

if CF(i-1)fastfilter(i), then CF(i)=slowfilter(i);

if CF(i-1)>slowfilter(i) and CF(i-1)slowfilter(i) and CF(i-1)>fastfilter(i), then CF(i)=MAX(slowfilter(i),fastfilter(i)).

For a downtrend, i.e. CF(i-1)slowfilter(i) and CF(i-1)>fastfilter(i), then CF(i)=MAX(slowfilter(i),fastfilter(i));

if CF(i-1)>slowfilter(i) and CF(i-1)fastfilter(i), then CF(i)=fastfilter(i);

if CF(i-1)<slowfilter(i) and CF(i-1)<fastfilter(i), then CF(i)=MIN(slowfilter(i),fastfilter(i)).

Where:

CF(i) – value of the cluster filter on the current bar;

CF(i-1) and CF(i-2) – values of the cluster filter on the previous bars;

slowfilter(i) – value of the slow filter

fastfilter(i) – value of the fast filter

MIN – the minimum value;

MAX – the maximum value;

What is Variety MA Cluster Filter Crosses?

For this indicator we calculate a fast and slow filter of the same filter and then we run a cluster filter between the fast and slow filter outputs to detect areas of chop/noise. The output is the uptrend is denoted by green color, downtrend by red color, and chop/noise/no-trade zone by white color. As a trader, you'll likely want to avoid trading during areas of chop/noise so you'll want to avoid trading when the color turns white.

Extras

Bar coloring

Alerts

Loxx's Expanded Source Types, see here:

Loxx's Moving Averages, see here:

An example of filtered chop, see the yellow circles. The cluster filter identifies chop zones so you don't get stuck in a sideways market.

MM Chop FilterBased On the "Chop and explode Indicator by fhenry0331

We Updated to Pine 5

- Added break out alerts and Signals

-Customize thresholds

How To use

when the line is blue confirmed Buy

Line is Red confirmed Sell

ALWAYS use in confirmation with your strategy and Trade with the trend.

Match with the on chart version for best results

Chop Zone - SamXThis is my spin on the Chop Zone indicator. It was forked from the built-in TradingView Chop Zone indicator. There were several reasons for this effort...

The built-in indicator version had no real configuration options

It was hard-coded to use the 34-period EMA with fixed span sizes for identifying price range

There was no real context to the meaning of default color scheme

The separation points of the chop zone bars was at a fixed 1.43-degree scale

Note: If left at default settings, this indicator will exactly match the built-in Chop Zone indicator.

WARNING : Please be sure you understand the potential impact and implications before adjusting any of the settings in the "Advanced Configuration" section!!!

Chop Zone with discrete/standard coloring:

Chop Zone with gradient fill:

Moving Average angle plot with gradient fill:

Choppiness Index TileA simple tile on the chart that indicates the choppiness index on the chart for the chart's timeframe. The index tile will show 3 different colors based on the value of the choppiness index. 61.8 for the high threshold and 38.2 for the lower threshold.

Woodies CCI + CZ + SW indicatorsBased on

Changes:

- red bars removed and replaced by silver ones

- yellow bar (start of new trend) had been added

- more parameters can be set in settings dialogue (SW constants as well)

Chop and explodeThe purpose of this script is to decipher chop zones from runs/movement/explosion

The chop is RSI movement between 40 and 60

tight chop is RSI movement between 45 and 55. There should be an explosion after RSI breaks through 60 (long) or 40 (short). Tight chop bars are colored black, a series of black bars is tight consolidation and should explode imminently. The longer the chop the longer the explosion will go for. tighter the better.

Loose chop (whip saw/yellow bars) will range between 40 and 60.

the move begins with blue bars for long and purple bars for short.

Couple it with your trading system to help stay out of chop and enter when there is movement. Use with "Simple Trender."

Best of luck in all you do. Get money.

Woodies CCI with ChopZone and Sidewinder indicatorExcelente indicador a mi parecer, bastante complejo pero muy bien acoplado; dejo aquí las fuentes para aprender a utilizarlo:

www.x-trader.net

www.x-trader.net www.x-trader.net www.x-trader.net

h chop filter v1.1

Chop Filter based on Chaikin's Volatility but faster with 0 lag.

Use it to filter out (in brown) when it is not worth trading as we are in chop zone.