NormalDistributionFunctionsLibrary "NormalDistributionFunctions"

The NormalDistributionFunctions library encompasses a comprehensive suite of statistical tools for financial market analysis. It provides functions to calculate essential statistical measures such as mean, standard deviation, skewness, and kurtosis, alongside advanced functionalities for computing the probability density function (PDF), cumulative distribution function (CDF), Z-score, and confidence intervals. This library is designed to assist in the assessment of market volatility, distribution characteristics of asset returns, and risk management calculations, making it an invaluable resource for traders and financial analysts.

meanAndStdDev(source, length)

Calculates and returns the mean and standard deviation for a given data series over a specified period.

Parameters:

source (float) : float: The data series to analyze.

length (int) : int: The lookback period for the calculation.

Returns: Returns an array where the first element is the mean and the second element is the standard deviation of the data series for the given period.

skewness(source, mean, stdDev, length)

Calculates and returns skewness for a given data series over a specified period.

Parameters:

source (float) : float: The data series to analyze.

mean (float) : float: The mean of the distribution.

stdDev (float) : float: The standard deviation of the distribution.

length (int) : int: The lookback period for the calculation.

Returns: Returns skewness value

kurtosis(source, mean, stdDev, length)

Calculates and returns kurtosis for a given data series over a specified period.

Parameters:

source (float) : float: The data series to analyze.

mean (float) : float: The mean of the distribution.

stdDev (float) : float: The standard deviation of the distribution.

length (int) : int: The lookback period for the calculation.

Returns: Returns kurtosis value

pdf(x, mean, stdDev)

pdf: Calculates the probability density function for a given value within a normal distribution.

Parameters:

x (float) : float: The value to evaluate the PDF at.

mean (float) : float: The mean of the distribution.

stdDev (float) : float: The standard deviation of the distribution.

Returns: Returns the probability density function value for x.

cdf(x, mean, stdDev)

cdf: Calculates the cumulative distribution function for a given value within a normal distribution.

Parameters:

x (float) : float: The value to evaluate the CDF at.

mean (float) : float: The mean of the distribution.

stdDev (float) : float: The standard deviation of the distribution.

Returns: Returns the cumulative distribution function value for x.

confidenceInterval(mean, stdDev, size, confidenceLevel)

Calculates the confidence interval for a data series mean.

Parameters:

mean (float) : float: The mean of the data series.

stdDev (float) : float: The standard deviation of the data series.

size (int) : int: The sample size.

confidenceLevel (float) : float: The confidence level (e.g., 0.95 for 95% confidence).

Returns: Returns the lower and upper bounds of the confidence interval.

Confidence_interval

Outlier Detector with N-Sigma Confidence IntervalsA detrended series that oscilates around zero is obtained after first differencing a time series (i.e. subtracting the closing price for a candle from the one immediately before, for example). Hypothetically, assuming that every detrended closing price is independent of each other (what might not be true!), these values will follow a normal distribution with mean zero and unknown variance sigma squared (assuming equal variance, what is also probably not true as volatility changes over time for different pairs). After studentizing, they follow a Student's t-distribution, but as the sample size increases (back periods > 30, at least), they follow a standard normal distribution.

This script was developed for personal use and the idea is spotting candles that are at least 99% bigger than average (using N = 3) as they will cross the upper and lower confidence interval limits. N = 2 would roughly provide a 95% confidence interval.

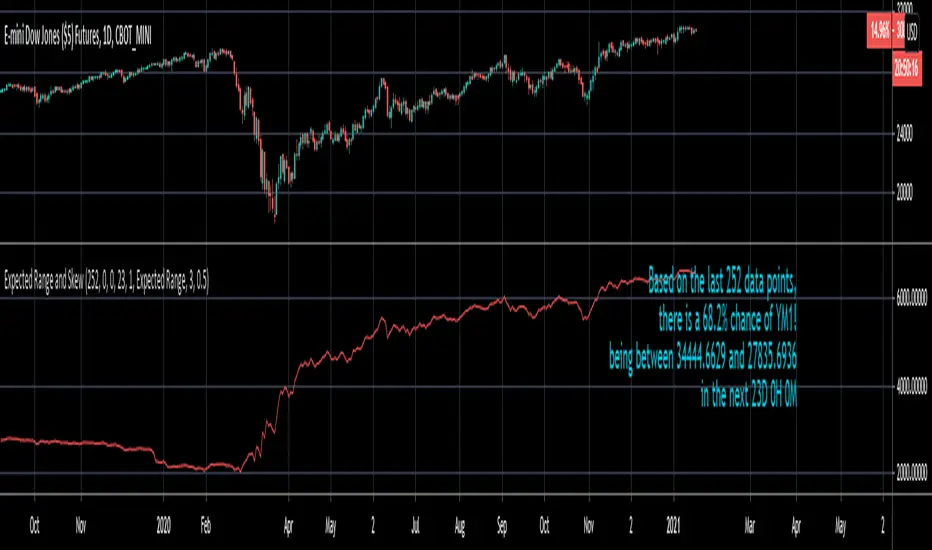

Expected Range and SkewThis is an open source and updated version of my previous "Confidence Interval" script. This script provides you with the expected range over a given time period in the future and the skew of that range. For example, if you wanted to know the expected 1 standard deviation range of MSFT over the next 20 days, this will tell you that. Additionally, this script will also tell you the skew of the expected range.

How to use this script:

1) Enter the length, this will determine the number of data points used in the calculation of the expected range.

2) Enter the amount of time you want projected forward in minutes, hours, and days.

3) Input standard deviation of the expected range.

4) Pick the type of data you want shown from the dropdown menu. Your choices are either the expected range or the skew of the expected range.

5) Enter the x and y coordinates of the label (optional). This is useful so it doesn't impede your view of the plot.

Here are a few notes about this script:

First, the expected range line gives you the width of said range (upper bound - lower bound), and the label will tell you specifically what the upper and lower bounds of the expected range are.

Second, this script will work on any of the default timeframes, but you need to be careful with how far out you try to project the expected range depending on the timeframe you're using. For example, if you're using the 1min timeframe, it probably won't do you any good trying to project the expected range over the next 20 days; or if you're using the daily timeframe it doesn't make sense to try to project the expected range for the next 5 hours. You can tell if the time horizon you're trying to project doesn't work well with the chart timeframe you're using if the current price is outside of either the upper or lower bounds provided in the label. If the current price is within the upper and lower bounds provided in the label, then the time horizon that you're projecting over is reasonable for the chart timeframe you're using.

Third, this script does not countdown automatically, so the time provided in the label will stay the same. For example, in the picture above, the expected range of Dow Futures over the next 23 days from January 12th, 2021 is calculated. But when tomorrow comes it won't count down to 22 days, instead it will show the range over the next 23 days from January 13th, 2021. So if you want the time horizon to change as time goes on you will have to update this yourself manually.

Lastly, if you try to set an alert on this script, you will get a warning about it possibly repainting. This is because of the label, not the plot itself. The label constantly updates itself, which triggers the warning. I tested setting alerts on this script both with and without the inclusion of the label, and without the label the repainting warning did not occur. So remember, if you set an alert on this script you will get a warning about it possibly repainting, but this is because of the label constantly updating, not the plot itself.

Fuzzy SMAs - Confidence Interval BBSimilar to Bollinger Bands, with the difference being the use of confidence intervals instead of stdev multiples to define the band regions.