Cruce de Medias AvanzadoLa estrategia es muy simple, es cruce de medias móviles, por defecto la rápida es 50 y la lenta 200 pero se pueden personalizar, es una estrategia a largo plazo que ha demostrado ser muy rentable en cualquiera de sus medias con índices en gráficos diarios.

Se pueden elegir distintos tipos de medias móviles existentes y ajustar la rentabilidad de cada una y ajustar sus medias móviles a para aumentar la rentabilidad.

Aquí tienes una descripción de las medias móviles añadidas al script y sus características:

Simple SMA (Media Móvil Simple):

Calcula el promedio simple de los precios de cierre durante un período específico.

Es la más básica y fácil de interpretar, pero puede ser lenta para reaccionar a los cambios bruscos en el precio.

Exponencial EMA (Media Móvil Exponencial):

Da más peso a los precios recientes, lo que la hace más sensible a los cambios de precio.

Responde más rápidamente a las fluctuaciones del mercado en comparación con la SMA, lo que ayuda a detectar cambios de tendencia más temprano.

Ponderada WMA (Media Móvil Ponderada):

Asigna más peso a los datos más recientes de forma lineal.

Proporciona un balance entre la sensibilidad de la EMA y la suavidad de la SMA, siendo útil para seguir tendencias a corto plazo.

Volumen Ponderada VWMA (Media Móvil Ponderada por Volumen):

Pondera los precios según el volumen de negociación, dándole más importancia a los precios con mayor volumen.

Es útil para analizar si los movimientos de precio están respaldados por un volumen alto, lo que indica mayor relevancia.

Hull HMA (Media Móvil de Hull):

Diseñada para minimizar el retraso y aumentar la sensibilidad al mismo tiempo.

Combina el suavizado y la rápida respuesta al precio, lo que la hace adecuada para traders que necesitan detectar cambios de tendencia rápidamente.

Media Suavizada RMA (Media Móvil Suavizada):

Es similar a la EMA pero con un suavizado diferente, proporcionando un promedio que filtra de forma más efectiva el ruido de precios.

Suele usarse para análisis de tendencias a medio plazo.

Media de Arnaud Legoux ALMA (Media Móvil ALMA):

Utiliza un algoritmo especial de suavizado con control de sesgo para reducir el ruido y mejorar la detección de tendencias.

Permite ajustar los parámetros de sesgo y suavizado para adaptarse a diferentes necesidades de trading.

Es conocida por su capacidad de mantener una respuesta rápida al precio al tiempo que suprime el ruido.

Estas medias móviles ofrecen diferentes enfoques para seguir y analizar las tendencias en los precios. Dependiendo de tu estrategia de trading, puedes elegir la media móvil que mejor se adapte a tus necesidades: desde una respuesta rápida con la HMA o EMA, hasta un enfoque más estable y menos reactivo con la SMA o RMA.

Cycles

Average Monthly Closing Direction StrategyEstrategia que diseñé, que combina patrones históricos y filtros técnicos para mejorar las probabilidades de éxito en trading. La idea es simple: he identificado ciertos días específicos del mes que, según los datos históricos, tienen tendencia a cerrar en positivo (suben) o en negativo (bajan).

US 30 Daily Breakout Strategy The US 30 Daily Breakout Strategy (Single Trade Per Breakout/Breakdown) is a trading approach for the US 30 (Dow Jones Industrial Average) that aims to capture breakout or breakdown moves based on the previous day’s high and low levels. The strategy includes mechanisms to take only one trade per breakout (or breakdown) each day and ensures that each trade is executed only when no other trade is open.

Entry Conditions:

Long Trade (Breakout): The strategy initiates a long position if the current candle closes above the previous day's high, indicating an upward breakout. Only one breakout trade can occur per day, regardless of whether the price remains above the previous high.

Short Trade (Breakdown): The strategy initiates a short position if the current candle closes below the previous day's low, indicating a downward breakdown. Similarly, only one breakdown trade can occur per day.

Risk Management:

Take Profit and Stop Loss: Each trade has a take profit and stop loss of 50 points, aiming to cap profit and limit loss effectively for each position.

Daily Reset Mechanism:

At the start of each new day (based on New York time), the strategy resets its flags, allowing it to look for new breakout or breakdown trades. This reset ensures that only one trade can be taken per breakout or breakdown level each day.

Execution Logic

Flags for Trade Limitation: Flags (breakout_traded and breakdown_traded) are used to ensure only one breakout or breakdown trade is taken per day. These flags reset daily.

Dynamic Plotting: The previous day’s high and low are plotted on the chart, providing a visual reference for potential breakout or breakdown levels.

Overall Objective

This strategy is designed to capture single-directional daily moves by identifying significant breakouts or breakdowns beyond the previous day’s range. The fixed profit and loss limits ensure the trades are managed with controlled risk, while the daily reset feature prevents overtrading and limits each trade opportunity to one breakout and one breakdown attempt per day.

S&P 100 Option Expiration Week StrategyThe Option Expiration Week Strategy aims to capitalize on increased volatility and trading volume that often occur during the week leading up to the expiration of options on stocks in the S&P 100 index. This period, known as the option expiration week, culminates on the third Friday of each month when stock options typically expire in the U.S. During this week, investors in this strategy take a long position in S&P 100 stocks or an equivalent ETF from the Monday preceding the third Friday, holding until Friday. The strategy capitalizes on potential upward price pressures caused by increased option-related trading activity, rebalancing, and hedging practices.

The phenomenon leveraged by this strategy is well-documented in finance literature. Studies demonstrate that options expiration dates have a significant impact on stock returns, trading volume, and volatility. This effect is driven by various market dynamics, including portfolio rebalancing, delta hedging by option market makers, and the unwinding of positions by institutional investors (Stoll & Whaley, 1987; Ni, Pearson, & Poteshman, 2005). These market activities intensify near option expiration, causing price adjustments that may create short-term profitable opportunities for those aware of these patterns (Roll, Schwartz, & Subrahmanyam, 2009).

The paper by Johnson and So (2013), Returns and Option Activity over the Option-Expiration Week for S&P 100 Stocks, provides empirical evidence supporting this strategy. The study analyzes the impact of option expiration on S&P 100 stocks, showing that these stocks tend to exhibit abnormal returns and increased volume during the expiration week. The authors attribute these patterns to intensified option trading activity, where demand for hedging and arbitrage around options expiration causes temporary price adjustments.

Scientific Explanation

Research has found that option expiration weeks are marked by predictable increases in stock returns and volatility, largely due to the role of options market makers and institutional investors. Option market makers often use delta hedging to manage exposure, which requires frequent buying or selling of the underlying stock to maintain a hedged position. As expiration approaches, their activity can amplify price fluctuations. Additionally, institutional investors often roll over or unwind positions during expiration weeks, creating further demand for underlying stocks (Stoll & Whaley, 1987). This increased demand around expiration week typically leads to temporary stock price increases, offering profitable opportunities for short-term strategies.

Key Research and Bibliography

Johnson, T. C., & So, E. C. (2013). Returns and Option Activity over the Option-Expiration Week for S&P 100 Stocks. Journal of Banking and Finance, 37(11), 4226-4240.

This study specifically examines the S&P 100 stocks and demonstrates that option expiration weeks are associated with abnormal returns and trading volume due to increased activity in the options market.

Stoll, H. R., & Whaley, R. E. (1987). Program Trading and Expiration-Day Effects. Financial Analysts Journal, 43(2), 16-28.

Stoll and Whaley analyze how program trading and portfolio insurance strategies around expiration days impact stock prices, leading to temporary volatility and increased trading volume.

Ni, S. X., Pearson, N. D., & Poteshman, A. M. (2005). Stock Price Clustering on Option Expiration Dates. Journal of Financial Economics, 78(1), 49-87.

This paper investigates how option expiration dates affect stock price clustering and volume, driven by delta hedging and other option-related trading activities.

Roll, R., Schwartz, E., & Subrahmanyam, A. (2009). Options Trading Activity and Firm Valuation. Journal of Financial Markets, 12(3), 519-534.

The authors explore how options trading activity influences firm valuation, finding that higher options volume around expiration dates can lead to temporary price movements in underlying stocks.

Cao, C., & Wei, J. (2010). Option Market Liquidity and Stock Return Volatility. Journal of Financial and Quantitative Analysis, 45(2), 481-507.

This study examines the relationship between options market liquidity and stock return volatility, finding that increased liquidity needs during expiration weeks can heighten volatility, impacting stock returns.

Summary

The Option Expiration Week Strategy utilizes well-researched financial market phenomena related to option expiration. By positioning long in S&P 100 stocks or ETFs during this period, traders can potentially capture abnormal returns driven by option market dynamics. The literature suggests that options-related activities—such as delta hedging, position rollovers, and portfolio adjustments—intensify demand for underlying assets, creating short-term profit opportunities around these key dates.

Payday Anomaly StrategyThe "Payday Effect" refers to a predictable anomaly in financial markets where stock returns exhibit significant fluctuations around specific pay periods. Typically, these are associated with the beginning, middle, or end of the month when many investors receive wages and salaries. This influx of funds, often directed automatically into retirement accounts or investment portfolios (such as 401(k) plans in the United States), temporarily increases the demand for equities. This phenomenon has been linked to a cycle where stock prices rise disproportionately on and around payday periods due to increased buy-side liquidity.

Academic research on the payday effect suggests that this pattern is tied to systematic cash flows into financial markets, primarily driven by employee retirement and savings plans. The regularity of these cash infusions creates a calendar-based pattern that can be exploited in trading strategies. Studies show that returns on days around typical payroll dates tend to be above average, and this pattern remains observable across various time periods and regions.

The rationale behind the payday effect is rooted in the behavioral tendencies of investors, specifically the automatic reinvestment mechanisms used in retirement funds, which align with monthly or semi-monthly salary payments. This regular injection of funds can cause market microstructure effects where stock prices temporarily increase, only to stabilize or reverse after the funds have been invested. Consequently, the payday effect provides traders with a potentially profitable opportunity by predicting these inflows.

Scientific Bibliography on the Payday Effect

Ma, A., & Pratt, W. R. (2017). Payday Anomaly: The Market Impact of Semi-Monthly Pay Periods. Social Science Research Network (SSRN).

This study provides a comprehensive analysis of the payday effect, exploring how returns tend to peak around payroll periods due to semi-monthly cash flows. The paper discusses how systematic inflows impact returns, leading to predictable stock performance patterns on specific days of the month.

Lakonishok, J., & Smidt, S. (1988). Are Seasonal Anomalies Real? A Ninety-Year Perspective. The Review of Financial Studies, 1(4), 403-425.

This foundational study explores calendar anomalies, including the payday effect. By examining data over nearly a century, the authors establish a framework for understanding seasonal and monthly patterns in stock returns, which provides historical support for the payday effect.

Owen, S., & Rabinovitch, R. (1983). On the Predictability of Common Stock Returns: A Step Beyond the Random Walk Hypothesis. Journal of Business Finance & Accounting, 10(3), 379-396.

This paper investigates predictability in stock returns beyond random fluctuations. It considers payday effects among various calendar anomalies, arguing that certain dates yield predictable returns due to regular cash inflows.

Loughran, T., & Schultz, P. (2005). Liquidity: Urban versus Rural Firms. Journal of Financial Economics, 78(2), 341-374.

While primarily focused on liquidity, this study provides insight into how cash flows, such as those from semi-monthly paychecks, influence liquidity levels and consequently impact stock prices around predictable pay dates.

Ariel, R. A. (1990). High Stock Returns Before Holidays: Existence and Evidence on Possible Causes. The Journal of Finance, 45(5), 1611-1626.

Ariel’s work highlights stock return patterns tied to certain dates, including paydays. Although the study focuses on pre-holiday returns, it suggests broader implications of predictable investment timing, reinforcing the calendar-based effects seen with payday anomalies.

Summary

Research on the payday effect highlights a repeating pattern in stock market returns driven by scheduled payroll investments. This cyclical increase in stock demand aligns with behavioral finance insights and market microstructure theories, offering a valuable basis for trading strategies focused on the beginning, middle, and end of each month.

Customizable BTC Seasonality StrategyThis strategy leverages intraday seasonality effects in Bitcoin, specifically targeting hours of statistically significant returns during periods when traditional financial markets are closed. Padysak and Vojtko (2022) demonstrate that Bitcoin exhibits higher-than-average returns from 21:00 UTC to 23:00 UTC, a period in which all major global exchanges, such as the New York Stock Exchange (NYSE), Tokyo Stock Exchange, and London Stock Exchange, are closed. The absence of competing trading activity from traditional markets during these hours appears to contribute to these statistically significant returns.

The strategy proceeds as follows:

Entry Time: A long position in Bitcoin is opened at a user-specified time, which defaults to 21:00 UTC, aligning with the beginning of the identified high-return window.

Holding Period: The position is held for two hours, capturing the positive returns typically observed during this period.

Exit Time: The position is closed at a user-defined time, defaulting to 23:00 UTC, allowing the strategy to exit as the favorable period concludes.

This simple seasonality strategy aims to achieve a 33% annualized return with a notably reduced volatility of 20.93% and maximum drawdown of -22.45%. The results suggest that investing only during these high-return hours is more stable and less risky than a passive holding strategy (Padysak & Vojtko, 2022).

References

Padysak, M., & Vojtko, R. (2022). Seasonality, Trend-following, and Mean reversion in Bitcoin.

Harmony Signal Flow By ArunThis Pine Script strategy, titled "Harmony Signal Flow By Arun," uses the Relative Strength Index (RSI) indicator to generate buy and sell signals based on custom thresholds. The script incorporates stop-loss and target management and restricts new trades until the previous position closes. Here's a detailed description:

Custom RSI Metric:

The strategy calculates a 5-period RSI based on the closing price, aiming for a more responsive measure of price momentum.

RSI thresholds are defined:

Lower threshold (30): Indicates oversold conditions, triggering a potential buy.

Upper threshold (70): Indicates overbought conditions, prompting a possible sell.

Entry Conditions:

Buy Signal: The strategy initiates a buy order when the RSI crosses above the lower threshold (30), indicating a shift from oversold conditions.

Sell Signal: A sell order is triggered when the RSI crosses below the upper threshold (70), suggesting an overbought reversal.

Only one order (buy or sell) can be active at a time, ensuring that a new trade begins only when there’s no existing position.

Stop-Loss and Target Management:

For each trade, stop-loss and target conditions are applied to manage risk and secure profits.

For Buy Positions:

Stop-loss is set 100 points below the entry price.

Target is set 150 points above the entry price.

For Sell Positions:

Stop-loss is set 100 points above the entry price.

Target is 150 points below the entry price.

The strategy closes the trade when either the stop-loss or target is met, marking the trade as "closed" and allowing a new trade entry.

Trade Sequencing:

A new trade (buy or sell) is only permitted after the previous position hits either its stop-loss or target, preventing overlapping trades and ensuring clear trade sequences.

This sequential approach enhances risk management by ensuring only one active position at any time.

End-of-Day Closure:

All open positions are closed automatically at 3:25 PM (Indian market time) to avoid overnight exposure, ensuring the strategy remains strictly intraday.

The flag for trade entry is reset at the end of each day, enabling fresh trades the next day.

Chart Indicators:

The script plots buy and sell signals directly on the chart with visible labels.

It also displays the custom RSI metric with horizontal lines for the lower and upper thresholds, providing visual cues for entry and exit points.

Summary

This strategy is a momentum-based intraday trading approach that uses the RSI for identifying potential reversals and manages trades through predefined stop-loss and target levels. By enforcing trade sequencing and closing positions at the end of the trading day, it prioritizes risk management and seeks to capitalize on short-term trends while avoiding overnight market risks.

Advanced Multi-Seasonality StrategyThe Multi-Seasonality Strategy is a trading system based on seasonal market patterns. Seasonality refers to recurring market trends driven by predictable calendar-based events. These patterns emerge due to economic cycles, corporate activities (e.g., earnings reports), and investor behavior around specific times of the year. Studies have shown that such effects can influence asset prices over defined periods, leading to opportunities for traders who exploit these patterns (Hirshleifer, 2001; Bouman & Jacobsen, 2002).

How the Strategy Works:

The strategy allows the user to define four distinct periods within a calendar year. For each period, the trader selects:

Entry Date (Month and Day): The date to enter the trade.

Holding Period: The number of trading days to remain in the trade after the entry.

Trade Direction: Whether to take a long or short position during that period.

The system is designed with flexibility, enabling the user to activate or deactivate each of the four periods. The idea is to take advantage of seasonal patterns, such as buying during historically strong periods and selling during weaker ones. A well-known example is the "Sell in May and Go Away" phenomenon, which suggests that stock returns are higher from November to April and weaker from May to October (Bouman & Jacobsen, 2002).

Seasonality in Financial Markets:

Seasonal effects have been documented across different asset classes and markets:

Equities: Stock markets tend to exhibit higher returns during certain months, such as the "January effect," where prices rise after year-end tax-loss selling (Haugen & Lakonishok, 1987).

Commodities: Agricultural commodities often follow seasonal planting and harvesting cycles, which impact supply and demand patterns (Fama & French, 1987).

Forex: Currency pairs may show strength or weakness during specific quarters based on macroeconomic factors, such as fiscal year-end flows or central bank policy decisions.

Scientific Basis:

Research shows that market anomalies like seasonality are linked to behavioral biases and institutional practices. For example, investors may respond to tax incentives at the end of the year, and companies may engage in window dressing (Haugen & Lakonishok, 1987). Additionally, macroeconomic factors, such as monetary policy shifts and holiday trading volumes, can also contribute to predictable seasonal trends (Bouman & Jacobsen, 2002).

Risks of Seasonal Trading:

While the strategy seeks to exploit predictable patterns, there are inherent risks:

Market Changes: Seasonal effects observed in the past may weaken or disappear as market conditions evolve. Increased algorithmic trading, globalization, and policy changes can reduce the reliability of historical patterns (Lo, 2004).

Overfitting: One of the risks in seasonal trading is overfitting the strategy to historical data. A pattern that worked in the past may not necessarily work in the future, especially if it was based on random chance or external factors that no longer apply (Sullivan, Timmermann, & White, 1999).

Liquidity and Volatility: Trading during specific periods may expose the trader to low liquidity, especially around holidays or earnings seasons, leading to slippage and larger-than-expected price swings.

Economic and Geopolitical Shocks: External events such as pandemics, wars, or political instability can disrupt seasonal patterns, leading to unexpected market behavior.

Conclusion:

The Multi-Seasonality Strategy capitalizes on the predictable nature of certain calendar-based patterns in financial markets. By entering and exiting trades based on well-established seasonal effects, traders can potentially capture short-term profits. However, caution is necessary, as market dynamics can change, and seasonal patterns are not guaranteed to persist. Rigorous backtesting, combined with risk management practices, is essential to successfully implementing this strategy.

References:

Bouman, S., & Jacobsen, B. (2002). The Halloween Indicator, "Sell in May and Go Away": Another Puzzle. American Economic Review, 92(5), 1618-1635.

Fama, E. F., & French, K. R. (1987). Commodity Futures Prices: Some Evidence on Forecast Power, Premiums, and the Theory of Storage. Journal of Business, 60(1), 55-73.

Haugen, R. A., & Lakonishok, J. (1987). The Incredible January Effect: The Stock Market's Unsolved Mystery. Dow Jones-Irwin.

Hirshleifer, D. (2001). Investor Psychology and Asset Pricing. Journal of Finance, 56(4), 1533-1597.

Lo, A. W. (2004). The Adaptive Markets Hypothesis: Market Efficiency from an Evolutionary Perspective. Journal of Portfolio Management, 30(5), 15-29.

Sullivan, R., Timmermann, A., & White, H. (1999). Data-Snooping, Technical Trading Rule Performance, and the Bootstrap. Journal of Finance, 54(5), 1647-1691.

This strategy harnesses the power of seasonality but requires careful consideration of the risks and potential changes in market behavior over time.

Scalping Strategy By TradingConTotoScript Description: "Scalping Strategy By TradingConToto"

This scalping strategy is designed to trade in volatile markets, taking advantage of rapid price movements. It uses pivots to identify key entry and exit points, along with exponential moving averages (EMAs) to determine the overall trend.

Key Features:

Dynamic Pivots: Calculates pivot highs and lows to identify support and resistance zones, improving entry accuracy.

Market Trend Analysis: Utilizes a 100-period EMA for long-term trend analysis and a 25-period EMA for short-term trends, facilitating informed decision-making.

Automated Entry and Exit: Generates buy and sell signals based on EMA crossovers and specific market conditions, ensuring you don't miss opportunities.

Risk Management: Allows you to set take profit and stop loss levels tailored to market volatility, using the ATR for effective risk management.

User-Friendly Interface: Easily customize strategy parameters such as pivot range, stop loss and take profit pips, and spread.

Requirements:

Ideal for use on short time frames during high activity sessions, like the configured scalping session.

Activate buy and sell options according to your preference and analyze performance using TradingView’s tools.

Note:

This script is a tool and does not guarantee results. It is recommended to test in a simulated environment before applying it to real accounts.

Optimize your scalping operations and enhance your market performance with this effective strategy!

Parent Session Sweeps + Alert Killzone Ranges with Parent Session Sweep

Key Features:

1. Multiple Session Support: The script tracks three major trading sessions - Asia, London, and New York. Users can customize the timing of these sessions.

2. Killzone Visualization: The strategy visually represents each session's range, either as filled boxes or lines, allowing traders to easily identify key price levels.

3. Parent Session Logic: The core of the strategy revolves around identifying a "parent" session - a session that encompasses the range of the following session. This parent session becomes the basis for potential trade setups.

4. Sweep and Reclaim Setups: The strategy looks for price movements that sweep (break above or below) the parent session's high or low, followed by a reclaim of that level. This price action often indicates a potential reversal.

5. Risk-Reward Filtering: Each potential setup is evaluated based on a user-defined minimum risk-reward ratio, ensuring that only high-quality trade opportunities are considered.

6. Candle Close Filter: An optional filter that checks the characteristics of the candle that reclaims the parent session level, adding an extra layer of confirmation to the setup.

7. Performance Tracking: The strategy keeps track of bullish and bearish setup success rates, providing valuable feedback on its performance over time.

8. Visual Aids: The script draws lines to mark the parent session's high and low, making it easy for traders to identify key levels.

How It Works:

1. The script continuously monitors price action across the defined sessions.

2. When a session fully contains the range of the next session, it's identified as a potential parent session.

3. The strategy then waits for price to sweep either the high or low of this parent session.

4. If a sweep occurs, it looks for a reclaim of the swept level within the parameters set by the user.

5. If a valid setup is identified, the script generates an alert and places a trade (if backtesting or running live).

6. The strategy continues to monitor the trade for either reaching the target (opposite level of the parent session) or hitting the stop loss.

Considerations for Signals:

- Sweep: A break of the parent session's high or low.

- Reclaim: A close back inside the parent session range after a sweep.

- Candle Characteristics: Optional filter for the reclaim candle (e.g., bullish candle for long setups).

- Risk-Reward: Each setup must meet or exceed the user-defined minimum risk-reward ratio.

- Session Timing: The strategy is sensitive to the defined session times, which should be set according to the trader's preferred time zone.

This strategy aims to capitalize on institutional order flow and liquidity patterns in the forex market, providing traders with a systematic approach to identifying potential reversal points with favorable risk-reward profiles.

Trade Entry Detector, Wick to Body Ratio Trade Entry Detector: Wick-to-Body Ratio Strategy with Bollinger Bands

Overview

The Trade Entry Detector is a custom strategy for TradingView that leverages the Bollinger Bands and a unique wick-to-body ratio approach to capture precise entry opportunities. This indicator is designed for traders who want to pinpoint high-probability reversal points when price interacts with Bollinger Bands, all while offering flexible entry fill options.

The strategy performs primary analysis on the daily time frame, regardless of your current chart setting, allowing you to view daily Bollinger Band levels and entry signals even on lower time frames. This approach is suitable for swing traders and short-term traders looking to align intraday moves with higher time frame signals.

How the Strategy Works

1. Bollinger Band Analysis on the Daily Time Frame

Bollinger Bands are calculated using a 20-period simple moving average (SMA) and a standard deviation multiplier (default is 2). These bands dynamically expand and contract based on market volatility, making them ideal for identifying overbought and oversold conditions:

* Upper Band: Indicates potential overbought levels.

* Lower Band: Indicates potential oversold levels.

2. Wick-to-Body Ratio Condition

This strategy places significant emphasis on candle wicks relative to the candle body. Here’s why:

* A large upper wick relative to the body signals potential selling pressure after testing the upper Bollinger Band.

* A large lower wick relative to the body indicates buying support after testing the lower Bollinger Band.

* Ratio Threshold: You can set a minimum wick-to-body ratio (default is 1.0), meaning that the wick must be at least equal in size to the body. This ensures only candles with significant reversals are considered for entry.

3. Flexible Entry Timing

To adapt to various trading styles, the indicator allows you to choose the entry fill timing:

* Daily Close: Enter at the close of the daily candle.

* Daily Open: Enter at the open of the following daily candle.

* HOD (High of Day): Set entry at the daily high, for those who want confirmation of upward momentum.

* LOD (Low of Day): Set entry at the daily low, ideal for confirming downward movement.

4. Position Sizing and Risk Management

The strategy calculates position size based on a fixed risk percentage of your account balance (default is 1%). This approach dynamically adjusts position sizes based on stop-loss distance:

* Stop Loss: Placed at the nearest swing high (for shorts) or swing low (for longs).

* Take Profit: Exits are triggered when the price reaches the opposite Bollinger Band.

5. Order Expiration

Each pending order (long or short) expires after two days if unfilled, allowing for new setups on subsequent candles if conditions are met again.

Using the Trade Entry Detector

Step-by-Step Guide

1. Set the Primary Time Frame

The core calculations run on the daily time frame, but the strategy can be applied to intraday charts (e.g., 65-minute or 15-minute) for deeper insights.

2. Adjust Bollinger Band Settings

* Length: Default is 20, which determines the period for calculating the moving average.

* Standard Deviation Multiplier: Default is 2.0, which sets the width of the bands. Adjusting this can help you capture broader or tighter volatility ranges.

3. Define the Wick-to-Body Ratio

Set the minimum ratio between wick and body (default 1.0). Higher values filter out candles with less wick-to-body contrast, focusing on stronger rejection moves.

4. Choose Entry Fill Timing

Select your preferred fill condition:

* Daily Close: Confirms the trade at the end of the daily session.

* Daily Open: Executes the entry at the open of the next day.

* HOD/LOD: Uses the daily high or low as an additional confirmation for upward or downward moves.

5. Position Sizing and Risk Management

* Set your account balance and risk percentage. The strategy automatically calculates position sizes based on the stop distance to manage risk efficiently.

* Stop Loss and Take Profit points are automatically set based on swing highs/lows and opposing Bollinger Bands, respectively.

Practical Example

Let’s say SPY (S&P 500 ETF) tests the lower Bollinger Band on the daily time frame, with a lower wick that is twice the size of the body (meeting the 1.0 ratio threshold). Here’s how the strategy might proceed:

1. Signal: The lower wick on SPY suggests buying interest at the lower Bollinger Band.

2. Entry Fill Timing: If you’ve selected "Daily Open," the entry order will be placed at the next day's open price.

3. Stop Loss: Positioned at the nearest daily swing low to minimize risk.

4. Take Profit: If SPY price moves up and reaches the upper Bollinger Band, the position is automatically closed.

Indicator Features and Benefits

* Multi-Time Frame Compatibility: Perform daily analysis while tracking signals on any intraday chart.

* Automatic Position Sizing: Tailor risk per trade based on account balance and desired risk percentage.

* Flexible Entry Options: Choose from close, open, HOD, or LOD for optimal timing.

* Effective Trend Reversal Identification: Uses wick-to-body ratio and Bollinger Band interaction to pinpoint potential reversals.

* Dynamic Visualization: Bollinger Bands are displayed on your chosen time frame, allowing seamless intraday tracking.

Summary

The Trade Entry Detector provides a unique, data-driven way to spot reversal points with customizable entry options. By combining Bollinger Bands with wick-to-body ratio conditions, it identifies potential trade setups where price has tested extremes and shown reversal signals. With its flexible entry timing, risk management features, and multi-time frame compatibility, this indicator is ideal for traders looking to blend daily market context with shorter-term execution.

Tips for Usage:

* For swing trading, consider the Daily Open or Close entry options.

* For momentum entries, HOD or LOD may offer better alignment with the direction of the wick.

* Backtest on different assets to find optimal Bollinger Band and wick-to-body settings for your market.

Use this indicator to enhance your understanding of price behavior at key levels and improve the precision of your entry points. Happy trading!

Unlock the Power of Seasonality: Monthly Performance StrategyThe Monthly Performance Strategy leverages the power of seasonality—those cyclical patterns that emerge in financial markets at specific times of the year. From tax deadlines to industry-specific events and global holidays, historical data shows that certain months can offer strong opportunities for trading. This strategy was designed to help traders capture those opportunities and take advantage of recurring market patterns through an automated and highly customizable approach.

The Inspiration Behind the Strategy:

This strategy began with the idea that market performance is often influenced by seasonal factors. Historically, certain months outperform others due to a variety of reasons, like earnings reports, holiday shopping, or fiscal year-end events. By identifying these periods, traders can better time their market entries and exits, giving them an advantage over those who solely rely on technical indicators or news events.

The Monthly Performance Strategy was built to take this concept and automate it. Instead of manually analyzing market data for each month, this strategy enables you to select which months you want to focus on and then executes trades based on predefined rules, saving you time and optimizing the performance of your trades.

Key Features:

Customizable Month Selection: The strategy allows traders to choose specific months to test or trade on. You can select any combination of months—for example, January, July, and December—to focus on based on historical trends. Whether you’re targeting the historically strong months like December (often driven by the 'Santa Rally') or analyzing quieter months for low volatility trades, this strategy gives you full control.

Automated Monthly Entries and Exits: The strategy automatically enters a long position on the first day of your selected month(s) and exits the trade at the beginning of the next month. This makes it perfect for traders who want to benefit from seasonal patterns without manually monitoring the market. It ensures precision in entering and exiting trades based on pre-set timeframes.

Re-entry on Stop Loss or Take Profit: One of the standout features of this strategy is its ability to re-enter a trade if a position hits the stop loss (SL) or take profit (TP) level during the selected month. If your trade reaches either a SL or TP before the month ends, the strategy will automatically re-enter a new trade the next trading day. This feature ensures that you capture multiple trading opportunities within the same month, instead of exiting entirely after a successful or unsuccessful trade. Essentially, it keeps your capital working for you throughout the entire month, not just when conditions align perfectly at the beginning.

Built-in Risk Management: Risk management is a vital part of this strategy. It incorporates an Average True Range (ATR)-based stop loss and take profit system. The ATR helps set dynamic levels based on the market’s volatility, ensuring that your stops and targets adjust to changing market conditions. This not only helps limit potential losses but also maximizes profit potential by adapting to market behavior.

Historical Performance Testing: You can backtest this strategy on any period by setting the start year. This allows traders to analyze past market data and optimize their strategy based on historical performance. You can fine-tune which months to trade based on years of data, helping you identify trends and patterns that provide the best trading results.

Versatility Across Asset Classes: While this strategy can be particularly effective for stock market indices and sector rotation, it’s versatile enough to apply to other asset classes like forex, commodities, and even cryptocurrencies. Each asset class may exhibit different seasonal behaviors, allowing you to explore opportunities across various markets with this strategy.

How It Works:

The trader selects which months to test or trade, for example, January, April, and October.

The strategy will automatically open a long position on the first trading day of each selected month.

If the trade hits either the take profit or stop loss within the month, the strategy will close the current position and re-enter a new trade on the next trading day, provided the month has not yet ended. This ensures that the strategy continues to capture any potential gains throughout the month, rather than stopping after one successful trade.

At the start of the next month, the position is closed, and if the next month is also selected, a new trade is initiated following the same process.

Risk Management and Dynamic Adjustments:

Incorporating risk management with this strategy is as easy as turning on the ATR-based system. The strategy will automatically calculate stop loss and take profit levels based on the market’s current volatility, adjusting dynamically to the conditions. This ensures that the risk is controlled while allowing for flexibility in capturing profits during both high and low volatility periods.

Maximizing the Seasonal Edge:

By automating entries and exits based on specific months and combining that with dynamic risk management, the Ultimate Monthly Performance Strategy takes advantage of seasonal patterns without requiring constant monitoring. The added re-entry feature after hitting a stop loss or take profit ensures that you are always in the game, maximizing your chances to capture profitable trades during favorable seasonal periods.

Who Can Benefit from This Strategy?

This strategy is perfect for traders who:

Want to exploit the predictable, recurring patterns that occur during specific months of the year.

Prefer a hands-off, automated trading approach that allows them to focus on other aspects of their portfolio or life.

Seek to manage risk effectively with ATR-based stop losses and take profits that adjust to market conditions.

Appreciate the ability to re-enter trades when a take profit or stop loss is hit within the month, ensuring that they don't miss out on multiple opportunities during a favorable period.

In summary, the Ultimate Monthly Performance Strategy provides traders with a comprehensive tool to capitalize on seasonal trends, optimize their trading opportunities throughout the year, and manage risk effectively. The built-in re-entry system ensures you continue to benefit from the market even after hitting targets within the same month, making it a robust strategy for traders looking to maximize their edge in any market.

Risk Disclaimer:

Trading financial markets involves significant risk and may not be suitable for all investors. The Monthly Performance Strategy is designed to help traders identify seasonal trends, but past performance does not guarantee future results. It is important to carefully consider your risk tolerance, financial situation, and trading goals before using any strategy. Always use appropriate risk management and consult with a professional financial advisor if necessary. The use of this strategy does not eliminate the risk of losses, and traders should be prepared for the possibility of losing their entire investment. Be sure to test the strategy on a demo account before applying it in live markets.

Monthly Breakout StrategyThis Monthly High/Low Breakout Strategy is designed to take long or short positions based on breakouts from the high or low of the previous month. Users can select whether they want to go long at a breakout above the previous month’s high, short at a breakdown below the previous month’s low, or use the reverse logic. Additionally, it includes a month filter, allowing trades to be executed only during user-specified months.

Breakout strategies, particularly those based on monthly highs and lows, aim to capitalize on price momentum. These systems rely on the assumption that once a significant price level is breached (such as the previous month's high or low), the market is likely to continue moving in the same direction due to increased volatility and trend-following behaviors by traders. Studies have demonstrated the potential effectiveness of breakout strategies in financial markets.

Scientific Evidence Supporting Breakout Strategies:

Momentum in Financial Markets:

Research on momentum-based strategies, which include breakout trading, shows that securities breaking key levels of support or resistance tend to continue their price movement in the direction of the breakout. Jegadeesh and Titman (1993) found that stocks with strong performance over a given period tend to continue performing well in subsequent periods, a principle also applied to breakout strategies.

Behavioral Finance:

The psychological factor of herd behavior is one of the driving forces behind breakout strategies. When prices break out of a key level (such as a monthly high), it triggers increased buying or selling pressure as traders join the trend. Barberis, Shleifer, and Vishny (1998) explained how cognitive biases, such as overconfidence and sentiment, can amplify price trends, which breakout strategies attempt to exploit.

Market Efficiency:

While markets are generally efficient, periods of inefficiency can occur, particularly around the breakouts of significant price levels. These inefficiencies often result in temporary price trends, which breakout strategies can exploit before the market corrects itself (Fama, 1970).

Risk Considerations:

Despite the potential for profit, the Monthly Breakout Strategy comes with several risks:

False Breakouts:

One of the most common risks in breakout strategies is the occurrence of false breakouts. These happen when the price temporarily moves above (or below) a key level but quickly reverses direction, causing losses for traders who entered positions too early. This is particularly risky in low-volatility environments.

Market Volatility:

Monthly breakout strategies rely on momentum, which may not be consistent across different market conditions. During periods of low volatility, price breakouts might lack the follow-through required for the strategy to succeed, leading to poor performance.

Whipsaw Risk:

The strategy is vulnerable to whipsaw markets, where prices oscillate around key levels without establishing a clear direction. This can result in frequent entry and exit signals that lead to losses, especially if trading costs are not managed properly.

Overfitting to Past Data:

If the month-selection filter is overly optimized based on historical data, the strategy may suffer from overfitting—performing well in backtests but poorly in real-time trading. This happens when strategies are tailored to past market conditions that may not repeat.

Conclusion:

While monthly breakout strategies can be effective in markets with strong momentum, they are subject to several risks, including false breakouts, volatility dependency, and whipsaw behavior. It is crucial to backtest this strategy thoroughly and ensure it aligns with your risk tolerance before implementing it in live trading.

References:

Jegadeesh, N., & Titman, S. (1993). Returns to Buying Winners and Selling Losers: Implications for Stock Market Efficiency. Journal of Finance, 48(1), 65-91.

Barberis, N., Shleifer, A., & Vishny, R. (1998). A Model of Investor Sentiment. Journal of Financial Economics, 49(3), 307-343.

Fama, E. F. (1970). Efficient Capital Markets: A Review of Theory and Empirical Work. Journal of Finance, 25(2), 383-417.

ETH Signal 15m

This strategy uses the Supertrend indicator combined with RSI to generate buy and sell signals, with stop loss (SL) and take profit (TP) conditions based on ATR (Average True Range). Below is a detailed explanation of each part:

1. General Information BINANCE:ETHUSDT.P

Strategy Name: "ETH Signal 15m"

Designed for use on the 15-minute time frame for the ETH pair.

Default capital allocation is 15% of total equity for each trade.

2. Backtest Period

start_time and end_time: Define the start and end time of the backtest period.

start_time = 2024-08-01: Start date of the backtest.

end_time = 2054-01-01: End date of the backtest.

The strategy will only run when the current time falls within this specified range.

3. Supertrend Indicator

Supertrend is a trend-following indicator that provides buy or sell signals based on the direction of price changes.

factor = 2.76: The multiplier used in the Supertrend calculation (increasing this value makes the Supertrend less sensitive to price movements).

atrPeriod = 12: Number of periods used to calculate ATR.

Output:

direction: Determines the buy/sell direction based on Supertrend.

If direction decreases, it signals a buy (Long).

If direction increases, it signals a sell (Short).

4. RSI Indicator

RSI (Relative Strength Index) is a momentum indicator, often used to identify overbought or oversold conditions.

rsiLength = 12: Number of periods used to calculate RSI.

rsiOverbought = 70: RSI level considered overbought.

rsiOversold = 30: RSI level considered oversold.

5. Entry Conditions

Long Entry:

Supertrend gives a buy signal (ta.change(direction) < 0).

RSI must be below the overbought level (rsi < rsiOverbought).

Short Entry:

Supertrend gives a sell signal (ta.change(direction) > 0).

RSI must be above the oversold level (rsi > rsiOversold).

The strategy will only execute trades if the current time is within the backtest period (in_date_range).

6. Stop Loss (SL) and Take Profit (TP) Conditions

ATR (Average True Range) is used to calculate the distance for Stop Loss and Take Profit based on price volatility.

atr = ta.atr(atrPeriod): ATR is calculated using 12 periods.

Stop Loss and Take Profit are calculated as follows:

Long Trade:

Stop Loss: Set at close - 4 * atr (current price minus 4 times the ATR).

Take Profit: Set at close + 2 * atr (current price plus 2 times the ATR).

Short Trade:

Stop Loss: Set at close + 4 * atr (current price plus 4 times the ATR).

Take Profit: Set at close - 2.237 * atr (current price minus 2.237 times the ATR).

Summary:

This strategy enters a Long trade when the Supertrend indicates an upward trend and RSI is not in the overbought region. Conversely, a Short trade is entered when Supertrend signals a downtrend, and RSI is not oversold.

The trade is exited when the price reaches the Stop Loss or Take Profit levels, which are determined based on price volatility (ATR).

Disclaimer:

The content provided in this strategy is for informational and educational purposes only. It is not intended as financial, investment, or trading advice. Trading in cryptocurrency, stocks, or any financial markets involves significant risk, and you may lose more than your initial investment. Past performance is not indicative of future results, and no guarantee of profit can be made. You should consult with a professional financial advisor before making any investment decisions. The creator of this strategy is not responsible for any financial losses or damages incurred as a result of following this strategy. All trades are executed at your own risk.

Monthly Day Long Strategy with VIX and Risk ManagementThis trading strategy is designed to open long positions on a specific day of the month, with the conditions for entry and exit based on the VIX index and additional risk management techniques. The strategy includes stop-loss and take-profit features to manage risk and lock in profits.

Inputs:

Entry Day of the Month (entry_day): Specifies which day of the month to consider for initiating a trade. The default value is the 27th.

Hold Duration (Days) (hold_duration_days): Defines how many days to hold the position after opening. The default value is 4 days.

VIX Threshold (vix_threshold): Sets the maximum acceptable value for the VIX index to consider an entry. If the VIX is below this threshold, it signals a potential trade. The default value is 20.0.

Stop Loss (%) (stop_loss_percentage): Determines the percentage below the entry price where the stop-loss will be triggered. The default value is 2.0%.

Take Profit (%) (take_profit_percentage): Sets the percentage above the entry price where the take-profit will be triggered. The default value is 5.0%.

Functions:

next_weekday(date): Adjusts the entry date to the next Monday if it falls on a weekend (Saturday or Sunday). This ensures trades do not occur on non-trading days.

Logic:

Entry Conditions:

Date Check: Opens a long position if the current date matches the adjusted entry date (the 27th or the next Monday if the 27th falls on a weekend).

VIX Filter: The VIX index value must be below the specified threshold (e.g., 20.0) to consider an entry.

Exit Conditions:

Time-Based Exit: Closes the position after the hold duration of 4 days.

Stop-Loss: Automatically closes the position if the price drops to a level that is a specified percentage below the entry price (e.g., 2.0%).

Take-Profit: Closes the position if the price rises to a level that is a specified percentage above the entry price (e.g., 5.0%).

Plots:

VIX Plot: Displays the VIX index on the chart for visual reference.

VIX Threshold Line: A horizontal line representing the VIX threshold value.

Summary:

The strategy aims to take advantage of specific entry days while filtering trades based on VIX levels to ensure market conditions are favorable. Risk management is enhanced through stop-loss and take-profit settings, which help in controlling potential losses and securing profits. The strategy ensures trades are only made on trading days and not on weekends, adjusting automatically to the next Monday if needed.

ChatGPT kann Fehler machen. Überprüfe wichtige Informationen.

Friday Bond Short StrategyStrategy: Friday Bond Short Strategy (1H Timeframe)

Objective:

This strategy aims to open short positions on a specified day and hour (Eastern Time) and close those positions on another specified day and hour. The background color of the chart will turn green when a position is active, providing a visual cue of an open trade.

Parameters:

1. Entry Day:

• Defines the day of the week on which the short position will be opened.

• Value: 6 for Friday (Pine Script’s weekday numbering: Monday = 2, Friday = 6).

2. Entry Hour:

• Specifies the hour (Eastern Time) when the short position will be opened.

• Value: 13 for 13:00 ET (1:00 PM).

3. Exit Day:

• Defines the day of the week on which the short position will be closed.

• Value: 2 for Monday.

4. Exit Hour:

• Specifies the hour (Eastern Time) when the position will be closed.

• Value: 13 for 13:00 ET (1:00 PM).

How It Works:

1. Time Adjustment to Eastern Time:

• The script converts all time references to Eastern Time (America/New_York) to ensure the strategy operates according to the desired time zone.

2. Entry Conditions:

• The strategy checks if the current day of the week matches the specified entry_day and if the current hour matches the specified entry_hour.

• If both conditions are met, a short position is opened (strategy.entry("Short", strategy.short)).

3. Exit Conditions:

• Similarly, the strategy checks if the current day of the week matches the specified exit_day and if the current hour matches the specified exit_hour.

• If both conditions are met, the open short position is closed (strategy.close("Short")).

4. Background Color:

• The background color of the chart is adjusted based on whether there is an open position:

• Green Background: If the strategy has an open position (strategy.position_size > 0), the background is set to light green.

• No Background Color: If there is no open position, the background color is not set (na).

Summary:

The Friday Bond Short Strategy is designed to enter short positions on Fridays at 1:00 PM ET and close them on Mondays at 1:00 PM ET. The chart background color turns green when a short position is active, providing a clear visual indication of when the strategy is engaged in a trade.

Simple Fibonacci Retracement Strategy This strategy uses Fibonacci retracement to identify key levels in the market and helps traders find good entry and exit points. By understanding and using this strategy, traders can improve their trading decisions and increase their chances of success in the market.

This strategy, called the "Simple Fibonacci Retracement Strategy," is designed to help traders identify potential entry and exit points in the market based on Fibonacci retracement levels. The code is written in Pine Script and runs on the TradingView platform.

Overall Function

The strategy uses Fibonacci retracement levels to identify potential support and resistance levels in the market. This helps traders find good entry and exit points for trades, as well as set stop-loss and take-profit levels to minimize risk and maximize gains.

Main Components of the Code

1. Input Parameters

Lookback Period: The number of bars used to identify the highest high and lowest low.

Fibonacci Direction: The choice of whether Fibonacci levels are calculated from top to bottom or bottom to top.

Fibonacci Levels: Specific Fibonacci levels (23.6%, 38.2%, 50%, 61.8%) used to identify important price levels.

Take Profit and Stop Loss: The number of pips used to set take profit and stop loss levels.

2. Identification of Highest and Lowest Points

The code uses the lookback period to find the highest high (highestHigh) and the lowest low (lowestLow). These levels form the basis for calculating the Fibonacci levels.

3. Calculation of Fibonacci Levels

Based on the direction chosen by the user, the code calculates the various Fibonacci levels (0%, 23.6%, 38.2%, 50%, 61.8%, 100%).

4. Trading Logic

Long Signal: Generated when the price crosses above the 61.8% Fibonacci level from bottom to top.

Short Signal: Generated when the price crosses below the 38.2% Fibonacci level from top to bottom.

When a long or short signal is generated, the strategy opens a position and sets take profit and stop loss levels based on the input parameters.

5. Visualization

The strategy plots the Fibonacci levels on the chart to provide a visual representation of the calculated levels. This helps traders see where the levels are in relation to the current price.

6. Alerts

The code also has functionality to create alerts (commented out), which can notify traders of buy or sell signals.

How to Use the Strategy

Configure Parameters: Adjust the lookback period, Fibonacci direction, and levels for take profit and stop loss to your preferences.

View the Chart: The Fibonacci levels will be plotted on the chart, providing a visual overview of potential support and resistance levels.

Trade Signals: Follow the generated buy and sell signals. Set your parameters in settings and adjust according to the generated buy and sell signals in the strategy tester. The strategy will automatically set your take profit and stop loss levels.

Evaluation and Adjustment: Monitor the performance of the strategy and make adjustments as needed to optimize the results.

Norwegian

Denne strategien, kalt "Simple Fibonacci Retracement Strategy", er designet for å hjelpe tradere med å identifisere mulige inngangs- og utgangspunkter i markedet basert på Fibonacci-retracementnivåer. Koden er skrevet i Pine Script og kjøres på TradingView-plattformen.

Overordnet Funksjon

Strategien bruker Fibonacci-retracementnivåer for å identifisere potensielle støtte- og motstandsnivåer i markedet. Dette hjelper tradere med å finne gode inngangs- og utgangspunkter for handler, samt å sette stop-loss og take-profit nivåer for å minimere risiko og maksimere gevinster.

Hovedkomponenter i Koden

1. Input Parametere

Lookback Period: Antall barer som brukes til å identifisere høyeste høydepunkt og laveste lavpunkt.

Fibonacci Direction: Valg om Fibonacci-nivåene skal beregnes fra topp til bunn eller bunn til topp.

Fibonacci Levels: Spesifikke Fibonacci-nivåer (23.6%, 38.2%, 50%, 61.8%) som brukes til å identifisere viktige prisnivåer.

Take Profit og Stop Loss: Antall pips som brukes til å sette take profit og stop loss nivåer.

2. Identifikasjon av Høyeste og Laveste Punkt

Koden bruker lookback perioden for å finne det høyeste høydepunktet (highestHigh) og det laveste lavpunktet (lowestLow). Disse nivåene er grunnlaget for å beregne Fibonacci-nivåene.

3. Beregning av Fibonacci-nivåer

Basert på retningen valgt av brukeren, beregner koden de forskjellige Fibonacci-nivåene (0%, 23.6%, 38.2%, 50%, 61.8%, 100%).

4. Handelslogikk

Long Signal: Genereres når prisen krysser over 61.8% Fibonacci-nivået fra bunn til topp.

Short Signal: Genereres når prisen krysser under 38.2% Fibonacci-nivået fra topp til bunn.

Når et long eller short signal genereres, åpner strategien en posisjon og setter take profit og stop loss nivåer basert på inputparametrene.

5. Visualisering

Strategien plottet Fibonacci-nivåene på chartet for å gi en visuell representasjon av de beregnede nivåene. Dette hjelper tradere med å se hvor nivåene er i forhold til den nåværende prisen.

6. Varsler

Koden har også funksjonalitet for å lage varsler (kommentert ut), som kan varsle tradere om kjøps- eller salgssignaler.

Slik Bruker Du Strategien

Konfigurer Parametere: Juster lookback perioden, Fibonacci-retningen, og nivåene for take profit og stop loss til dine preferanser.

Se på Chartet: Fibonacci-nivåene vil bli plottet på chartet, noe som gir deg en visuell oversikt over potensielle støtte- og motstandsnivåer.

Handle Signaler: Sett dine parametere i innstillinger og juster etter genererte kjøps- og salgssignalene i strategy testeren. Strategien vil automatisk sette dine take profit og stop loss nivåer.

Evaluering og Justering: Overvåk ytelsen til strategien og gjør justeringer etter behov for å optimalisere resultatene.

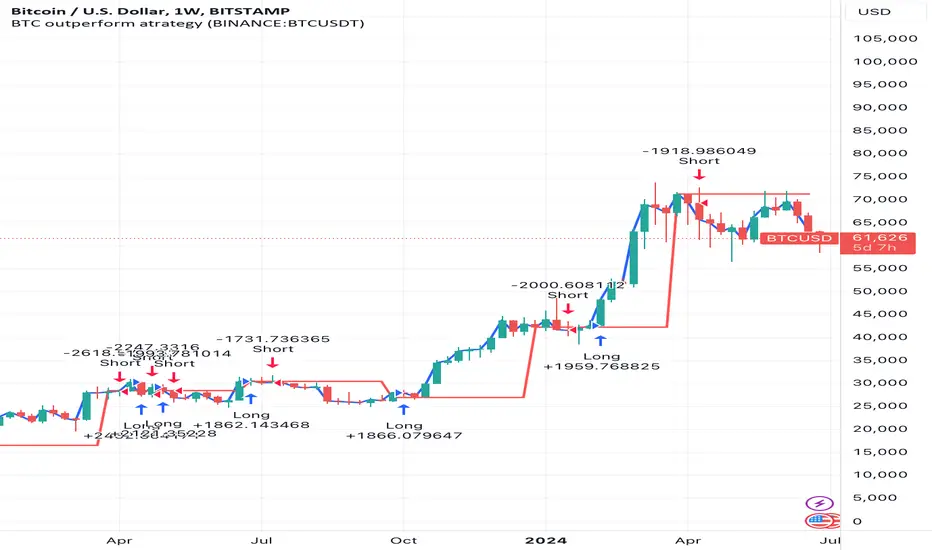

BTC outperform atrategy### Code Description

This Pine Script™ code implements a simple trading strategy based on the relative prices of Bitcoin (BTC) on a weekly and a three-month basis. The script plots the weekly and three-month closing prices of Bitcoin on the chart and generates trading signals based on the comparison of these prices. The code can also be applied to Ethereum (ETH) with similar effectiveness.

### Explanation

1. **Inputs and Variables**:

- The user selects the trading symbol (default is "BINANCE:BTCUSDT").

- `weeklyPrice` retrieves the closing price of the selected symbol on a weekly interval.

- `monthlyPrice` retrieves the closing price of the selected symbol on a three-month interval.

2. **Plotting Data**:

- The weekly price is plotted in blue.

- The three-month price is plotted in red.

3. **Trading Conditions**:

- A long position is suggested if the weekly price is greater than the three-month price.

- A short position is suggested if the three-month price is greater than the weekly price.

4. **Strategy Execution**:

- If the long condition is met, the strategy enters a long position.

- If the short condition is met, the strategy enters a short position.

This script works equally well for Ethereum (ETH) by changing the symbol input to "BINANCE:ETHUSDT" or any other desired Ethereum trading pair.

Mateo's Time of Day Analysis LEThis strategy takes a trade every day at a specified time and then closes it at a specified time.

The purpose of this strategy is to help determine if there are better times to day to buy or sell.

I was originally inspired to write this when a YouTuber stated that SPX had been up during the last 30 minutes of the day over 80% of the time the past year. No matter who says it, test it, and in my opinion, TradingView is one of the easiest placed to do that! Unfortunately, that particular claim did not turn out to be accurate, but this tool remains for those who want to optimize timing their entries and exits at specific times of day.

trend_switch

█ Description

Asset price data was time series data, commonly consisting of trends, seasonality, and noise. Many applicable indicators help traders to determine between trend or momentum to make a better trading decision based on their preferences. In some cases, there is little to no clear market direction, and price range. It feels much more appropriate to use a shorter trend identifier, until clearly defined market trend. The indicator/strategy developed with the notion aims to automatically switch between shorter and longer trend following indicator. There were many methods that can be applied and switched between, however in this indicator/strategy will be limited to the use of predictive moving average and MESA adaptive moving average (Ehlers), by first determining if there is a strong trend identified by calculating the slope, if slope value is between upper and lower threshold assumed there is not much price direction.

█ Formula

// predictive moving average

predict = (2*wma1-wma2)

trigger = (4*predict+3*predict +2*predict *predict)

// MESA adaptive moving average

mama = alpha*src+(1-alpha)*mama

fama = .5*alpha*mama+(1-.5-alpha)*fama

█ Feature

The indicator will have a specified default parameter of:

source = ohlc4

lookback period = 10

threshold = 10

fast limit = 0.5

slow limit = 0.05

Strategy type can be switched between Long/Short only and Long-Short strategy

Strategy backtest period

█ How it works

If slope between the upper (red) and lower (green) threshold line, assume there is little to no clear market direction, thus signal predictive moving average indicator

If slope is above the upper (red) or below the lower (green) threshold line, assume there is a clear trend forming, the signal generated from the MESA adaptive moving average indicator

█ Example 1 - Slope fall between the Threshold - activate shorter trend

█ Example 2 - Slope fall above/below Threshold - activate longer trend

Hurst Future Lines of Demarcation StrategyJ. M. Hurst introduced a concept in technical analysis known as the Future Line of Demarcation (FLD), which serves as a forward-looking tool by incorporating a simple yet profound line into future projections on a financial chart. Specifically, the FLD is constructed by offsetting the price half a cycle ahead into the future on the time axis, relative to the Hurst Cycle of interest. For instance, in the context of a 40 Day Cycle, the FLD would be represented by shifting the current price data 20 days forward on the chart, offering an idea of future price movement anticipations.

The utility of FLDs extends into three critical areas of insight, which form the backbone of the FLD Trading Strategy:

A price crossing the FLD signifies the confirmation of either a peak or trough formation, indicating pivotal moments in price action.

Such crossings also help determine precise price targets for the upcoming peak or trough, aligned with the cycle of examination.

Additionally, the occurrence of a peak in the FLD itself signals a probable zone where the price might experience a trough, helping to anticipate of future price movements.

These insights by Hurst in his "Cycles Trading Course" during the 1970s, are instrumental for traders aiming to determine entry and exit points, and to forecast potential price movements within the market.

To use the FLD Trading Strategy, for example when focusing on the 40 Day Cycle, a trader should primarily concentrate on the interplay between three Hurst Cycles:

The 20 Day FLD (Signal) - Half the length of the Trade Cycle

The 40 Day FLD (Trade) - The Cycle you want to trade

The 80 Day FLD (Trend) - Twice the length of the Trade Cycle

Traders can gauge trend or consolidation by watching for two critical patterns:

Cascading patterns, characterized by several FLDs running parallel with a consistent separation, typically emerge during pronounced market trends, indicating strong directional momentum.

Consolidation patterns, on the other hand, occur when multiple FLDs intersect and navigate within the same price bandwidth, often reversing direction to traverse this range multiple times. This tangled scenario results in the formation of Pause Zones, areas where price momentum is likely to temporarily stall or where the emergence of a significant trend might be delayed.

This simple FLD indicator provides 3 FLDs with optional source input and smoothing, A-through-H FLD interaction background, adjustable “Close the Trade” triggers, and a simple strategy for backtesting it all.

The A-through-H FLD interactions are a framework designed to classify the different types of price movements as they intersect with or diverge from the Future Line of Demarcation (FLD). Each interaction (designated A through H by color) represents a specific phase or characteristic within the cycle, and understanding these can help traders anticipate future price movements and make informed decisions.

The adjustable “Close the Trade” triggers are for setting the crossover/under that determines the trade exits. The options include: Price, Signal FLD, Trade FLD, or Trend FLD. For example, a trader may want to exit trades only when price finally crosses the Trade FLD line.

Shoutouts & Credits for all the raw code, helpful information, ideas & collaboration, conversations together, introductions, indicator feedback, and genuine/selfless help:

🏆 @TerryPascoe

🏅 @Hpotter

👏 @parisboy

Yeong RRGThe code outlines a trading strategy that leverages Relative Strength (RS) and Rate of Change (RoC) to make trading decisions. Here's a detailed breakdown of the tactic described by the code:

Ticker and Period Selection: The strategy begins by selecting a stock ticker symbol and defining a period (len) for the calculations, which defaults to 14 but can be adjusted by the user.

Stock and Index Data Retrieval: It fetches the closing price (stock_close) of the chosen stock and calculates its 25-period exponential moving average (stock_ema). Additionally, it retrieves the closing price of the S&P 500 Index (index_close), used as a benchmark for calculating Relative Strength.

Relative Strength Calculation: The Relative Strength (rs) is computed by dividing the stock's closing price by the index's closing price, then multiplying by 100 to scale the result. This metric is used to assess the stock's performance relative to the broader market.

Moving RS Ratio and Rate of Change: The strategy calculates a Simple Moving Average (sma) of the RS over the specified period to get the RS Ratio (rs_ratio). It then computes the Rate of Change (roc) of this RS Ratio over the same period to get the RM Ratio (rm_ratio).

Normalization: The RS Ratio and RM Ratio are normalized using a formula that adjusts their values based on the mean and standard deviation of their respective series over the specified window. This normalization process helps in standardizing the indicators, making them easier to interpret and compare.

Indicator Plotting: The normalized RS Ratio (jdk_rs_ratio) and RM Ratio (jdk_rm_ratio) are plotted on the chart with different colors for visual analysis. A horizontal line (hline) at 100 serves as a reference point, indicating a neutral level for the indicators.

State Color Logic: The script includes a logic to determine the state color (statecolor) based on the previous state color and the current values of jdk_rs_ratio and jdk_rm_ratio. This color coding is intended to visually represent different market states: green for bullish, red for bearish, yellow for hold, and blue for watch conditions.

Signal Generation: The strategy generates buy, sell, hold, and watch signals based on the state color and the indicators' values relative to 100. For example, a buy signal is generated when both jdk_rs_ratio and jdk_rm_ratio are above 100, and the background color is set to green to reflect this bullish condition.

Trade Execution: Finally, the strategy executes trades based on the generated signals. A "BUY" trade is entered when a buy signal is present, and it is closed when a sell signal occurs.

Overall, the strategy uses a combination of RS and RoC indicators, normalized for better comparison, to identify potential buy and sell opportunities based on the stock's performance relative to the market and its momentum.

PS January Barometer BacktesterPS January Barometer Backtester (PS JBB)

The PS January Barometer Backtester (PS JBB) is a simple strategy designed to test the "January Effect" hypothesis in financial markets. This effect theorizes that stock market performance in January can predict the trend for the rest of the year. The script operates on a monthly timeframe, focusing on capturing and analyzing the price movements in January and their subsequent influence on the market until the end of each year.

User Input:

January Trifecta Selectors

These are user-selectable options allowing traders to incorporate additional criteria into their market analysis.

The Santa Claus Rally refers to a stock market increase typically seen in the last week of December through the first two trading days in January.

The First Five Days Indicator assesses market performance during the initial five days of the year.

Script Operation:

The script automatically detects the start of each year, tracks January's high, and signals entry and exit points for trades based on the strategy's logic. It's an excellent tool for traders and investors looking to explore the January Effect's validity and its potential impact on their trading decisions.

In essence, the "PS January Barometer Backtester" is designed to exploit specific seasonal market trends, particularly focusing on the early part of the year, by analyzing and acting upon defined market movements. This strategy is ideal for traders who focus on yearly cyclical patterns and seek to incorporate historical trends into their trading decisions.

Note: This script is intended for educational and research purposes and should not be construed as financial advice. Always conduct your own due diligence before making trading/investment decisions.