[COG]Adaptive Volatility Bands# Adaptive Volatility Bands (AVB) Indicator Guide for Traders

## Special Acknowledgment 🙌

This script is inspired by and builds upon the foundational work of **DonovanWall**, a respected contributor to the trading community. His innovative approach to adaptive indicators has been instrumental in developing this advanced trading tool.

## What is the Adaptive Volatility Bands Indicator?

The Adaptive Volatility Bands (AVB) is a sophisticated technical analysis tool designed to help traders understand market dynamics by creating dynamic, responsive price channels that adapt to changing market conditions. Unlike traditional static indicators, this script uses advanced mathematical techniques to create flexible bands that adjust to market volatility in real-time.

## Key Features and Inputs

### 1. Price and Filtering Options

- **Price Source**: Determines the base price used for calculations (default is HLC3 - Average of High, Low, and Close)

- **Filter Poles**: Controls the smoothness of the indicator (1-9 poles)

- Lower values: More responsive, more noise

- Higher values: Smoother, but slower to react

### 2. Volatility and Band Settings

- **Sample Length**: Determines how many bars are used to calculate volatility (default 144)

- **Volatility Multiplier**: Adjusts the width of the main bands (default 1.414)

- **Outer Band Multiplier**: Controls the width of the outer bands (default 2.5)

- **Inner Band Ratio**: Positions the inner bands between the center and outer bands (default 0.25)

### 3. Advanced Processing Options

- **Lag Reduction Mode**: Helps reduce indicator delay

- **Fast Response Mode**: Makes the indicator more responsive to recent price changes

### 4. Signal and Visualization Options

- **Show Entry Signals**: Displays buy and sell signals

- **Signal Display Style**: Choose between labels or shapes

- **Range Filter**: Adds an additional filter for signal validation

## How the Indicator Works

The Adaptive Volatility Bands create a dynamic price channel with three key components:

1. **Center Line**: Represents the core trend direction

2. **Inner Bands**: Closer to the center line

3. **Outer Bands**: Wider bands that show broader price potential

### Color Dynamics

- The indicator uses a smart color gradient system

- Colors change based on price position within the bands

- Helps visualize bullish (green/blue) and bearish (red) market conditions

## Trading Strategies for Beginners

### Basic Entry Signals

- **Buy Signal**:

- Price touches the center line from below

- Candle is bullish (closes higher than it opens)

- Price is above the center line

- Trend is upward

- **Sell Signal**:

- Price touches the center line from above

- Candle is bearish (closes lower than it opens)

- Price is below the center line

- Trend is downward

### Risk Management Tips

1. Use the bands to identify:

- Potential trend changes

- Volatility levels

- Support and resistance areas

2. Combine with other indicators for confirmation

3. Always use stop-loss orders

4. Adjust parameters to match your trading style and asset

## When to Use This Indicator

Best suited for:

- Trending markets

- Swing trading

- Identifying potential entry and exit points

- Understanding market volatility

### Recommended Markets

- Stocks

- Forex

- Cryptocurrencies

- Futures

## Customization

The script offers extensive customization:

- Adjust smoothness

- Change band multipliers

- Modify color schemes

- Enable/disable features like lag reduction

## Important Considerations for Beginners

🚨 **Disclaimer**:

- No indicator guarantees profits

- Always practice with a demo account first

- Learn and understand the indicator before live trading

- Market conditions change, so continually adapt your strategy

## Getting Started

1. Add the script to your TradingView chart

2. Experiment with different settings

3. Backtest on historical data

4. Start with small positions

5. Continuously learn and improve

Happy Trading! 📈🔍

Cycles

Dow Theory Trend StrategyDow Theory Trend Strategy (Pine Script)

Overview

This Pine Script implements a trading strategy based on the core principles of Dow Theory. It visually identifies trends (uptrend, downtrend) by analyzing pivot highs and lows and executes trades when the trend direction changes. This script is an improved version that features refined trend determination logic and strategy implementation.

Core Concept: Dow Theory

The script uses a fundamental Dow Theory concept for trend identification:

Uptrend: Characterized by a series of Higher Highs (HH) and Higher Lows (HL).

Downtrend: Characterized by a series of Lower Highs (LH) and Lower Lows (LL).

How it Works

Pivot Point Detection:

It uses the built-in ta.pivothigh() and ta.pivotlow() functions to identify significant swing points (potential highs and lows) in the price action.

The pivotLookback input determines the number of bars to the left and right required to confirm a pivot. Note that this introduces a natural lag (equal to pivotLookback bars) before a pivot is confirmed.

Improved Trend Determination:

The script stores the last two confirmed pivot highs and the last two confirmed pivot lows.

An Uptrend (trendDirection = 1) is confirmed only when the latest pivot high is higher than the previous one (HH) AND the latest pivot low is higher than the previous one (HL).

A Downtrend (trendDirection = -1) is confirmed only when the latest pivot high is lower than the previous one (LH) AND the latest pivot low is lower than the previous one (LL).

Key Improvement: If neither a clear uptrend nor a clear downtrend is confirmed based on the latest pivots, the script maintains the previous trend state (trendDirection := trendDirection ). This differs from simpler implementations that might switch to a neutral/range state (e.g., trendDirection = 0) more frequently. This approach aims for smoother trend following, acknowledging that trends often persist through periods without immediate new HH/HL or LH/LL confirmations.

Trend Change Detection:

The script monitors changes in the trendDirection variable.

changedToUp becomes true when the trend shifts to an Uptrend (from Downtrend or initial state).

changedToDown becomes true when the trend shifts to a Downtrend (from Uptrend or initial state).

Visualizations

Background Color: The chart background is colored to reflect the currently identified trend:

Blue: Uptrend (trendDirection == 1)

Red: Downtrend (trendDirection == -1)

Gray: Initial state or undetermined (trendDirection == 0)

Pivot Points (Optional): Small triangles (shape.triangledown/shape.triangleup) can be displayed above pivot highs and below pivot lows if showPivotPoints is enabled.

Trend Change Signals (Optional): Labels ("▲ UP" / "▼ DOWN") can be displayed when a trend change is confirmed (changedToUp / changedToDown) if showTrendChange is enabled. These visually mark the potential entry points for the strategy.

Strategy Logic

Entry Conditions:

Enters a long position (strategy.long) using strategy.entry("L", ...) when changedToUp becomes true.

Enters a short position (strategy.short) using strategy.entry("S", ...) when changedToDown becomes true.

Position Management: The script uses strategy.entry(), which automatically handles position reversal. If the strategy is long and a short signal occurs, strategy.entry() will close the long position and open a new short one (and vice-versa).

Inputs

pivotLookback: The number of bars on each side to confirm a pivot high/low. Higher values mean pivots are confirmed later but may be more significant.

showPivotPoints: Toggle visibility of pivot point markers.

showTrendChange: Toggle visibility of the trend change labels ("▲ UP" / "▼ DOWN").

Key Improvements from Original

Smoother Trend Logic: The trend state persists unless a confirmed reversal pattern (opposite HH/HL or LH/LL) occurs, reducing potential whipsaws in choppy markets compared to logic that frequently resets to neutral.

Strategy Implementation: Converted from a pure indicator to a strategy capable of executing backtests and potentially live trades based on the Dow Theory trend changes.

Disclaimer

Dow Theory signals are inherently lagging due to the nature of pivot confirmation.

The effectiveness of the strategy depends heavily on the market conditions and the chosen pivotLookback setting.

This script serves as a basic template. Always perform thorough backtesting and implement proper risk management (e.g., stop-loss, take-profit, position sizing) before considering any live trading.

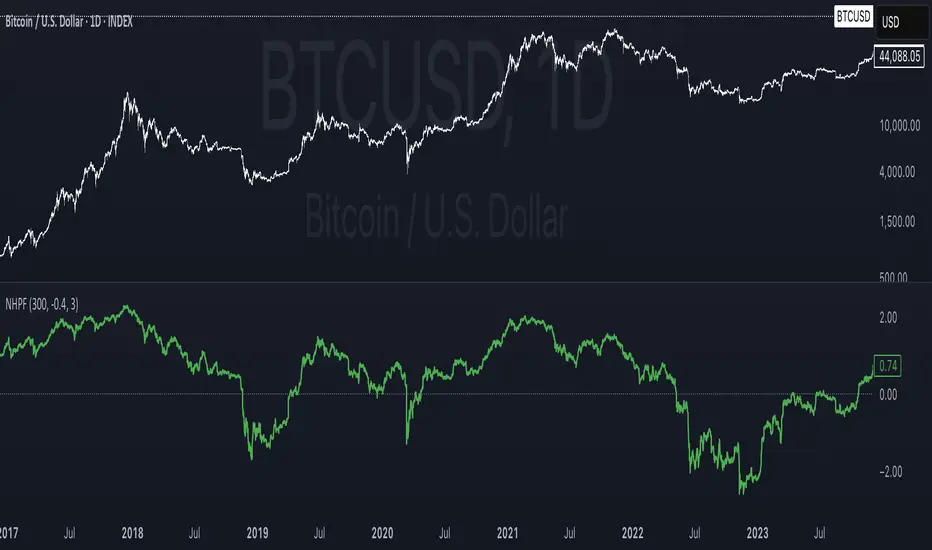

NHPF (Normalized Hodrick-Prescott Filter)This indicator applies a normalized Hodrick–Prescott filter (NHPF) to Bitcoin’s price data. It separates the underlying trend from short-term cyclical fluctuations by recursively smoothing the price using a user-defined lambda (HP Filter Period). The raw trend is then normalized by calculating a ratio between the trend and the current price, which is scaled and shifted according to subjective parameters (Mean and Scale). The result is a dimensionless value that highlights deviations from the long-term trend—serving as a signal for potential overbought (positive values) or oversold (negative values) market conditions. A zero line provides a clear reference, allowing traders to visually gauge when Bitcoin’s price is significantly above or below its expected trajectory.

Feel free to adjust the inputs to best match your analysis preferences.

CCI with Subjective NormalizationCCI (Commodity Channel Index) with Subjective Normalization

This indicator computes the classic CCI over a user-defined length, then applies a subjective mean and scale to transform the raw CCI into a pseudo Z‑score range. By adjusting the “Subjective Mean” and “Subjective Scale” inputs, you can shift and rescale the oscillator to highlight significant tops and bottoms more clearly in historical data.

1. CCI Calculation:

- Uses the standard formula \(\text{CCI} = \frac{\text{price} - \text{SMA(price, length)}}{0.015 \times \text{mean deviation}}\) over a user-specified length (default 500 bars).

2. Subjective Normalization:

- After CCI is calculated, it is divided by “Subjective Scale” and offset by “Subjective Mean.”

- This step effectively re-centers and re-scales the oscillator, helping you align major lows or highs at values like –2 or +2 (or any desired range).

3. Usage Tips:

- CCI Length controls how far back the script measures average price and deviation. Larger values emphasize multi-year cycles.

- Subjective Mean and Scale let you align the oscillator’s historical lows and highs with numeric levels you prefer (e.g., near ±2).

- Adjust these parameters to fit your particular market analysis or to match known cycle tops/bottoms.

4. Plot & Zero Line:

- The indicator plots the normalized CCI in yellow, along with a zero line for quick reference.

- Positive values suggest price is above its long-term mean, while negative values suggest it’s below.

This approach offers a straightforward momentum oscillator (CCI) combined with a customizable normalization, making it easier to spot historically significant overbought/oversold conditions without writing complex code yourself.

ES vs Bond ROCThis Pine Script plots the Relative Rate of Change (ROC) between the S&P 500 E-mini Futures (ES) and 30-Year Treasury Bond Futures (ZB) over a specified period. It helps identify when equities are overperforming or underperforming relative to long-term bonds—an insight often used to detect risk-on/risk-off sentiment shifts in the market.

DOPT---

## 🔍 **DOPT - Daily Open & Price Time Markers**

This script is designed to support directional bias development and price behavior analysis around key time-based reference points on the **1H and 4H timeframes**.

### ✨ **What It Does**

- **1800 Open Marker** (6 PM NY time): Plots the **daily open** from 1800 in **black dotted lines**.

- **0000 Open Marker** (Midnight NY time): Plots the **midnight open** in **blue dotted lines**.

- **Day Letters**: Each 1800 open is labeled with the corresponding **day of the week** (e.g., M, T, W...), helping visually segment your chart.

- **Hour Labels**: Select specific candles (e.g., 0000 = '0', 0800 = '8') to be labeled above the bar. These are fully customizable.

- **Candle Midpoints**: Option to mark the **50% level** of a specific candle (good for CE or CRT references).

- **CRT High/Low Tracking**: Ability to plot **extended high and low lines** from a selected candle back (e.g., for CRT modeling).

- **4H Timeframe Candle Numbering**: Helpful when analyzing sequences on the 4-hour timeframe. Candles are numbered `1`, `5`, and `9` for reference.

---

### 🧠 **How I Use It**

- I mostly use this on the **1-hour timeframe** to decide **directional bias** for the day:

- If price **closes above 1800 open**, I consider that a **green daily close** — potential bullish sentiment.

- If price **closes below**, I treat it as a **red daily close** — potential bearish behavior.

- Price often uses these opens as **support/resistance**, so I watch for reactions there.

- On the **4H**, the candle numbers help track structure and flow.

- Combine with CRT tools to mark **key candle highs/lows** and their **equilibrium (50%)** — great for refining entries or understanding how price is respecting a particular candle.

---

### ⚠️ **Note on Daylight Savings**

This is a **daylight saving time-dependent script**. When DST kicks in or out, you’ll need to **adjust the time inputs** accordingly to keep the opens accurate (e.g., 1800 might shift to 1700 depending on the season).

---

### 🔁 **Backtesting & Reference**

- The **1800 and 0000 opens** are plotted for **as far back** as your chart loads, making it great for backtesting historical reactions.

- The CRT marking tools only go back **50 candles max**, so use that for recent structure only.

---

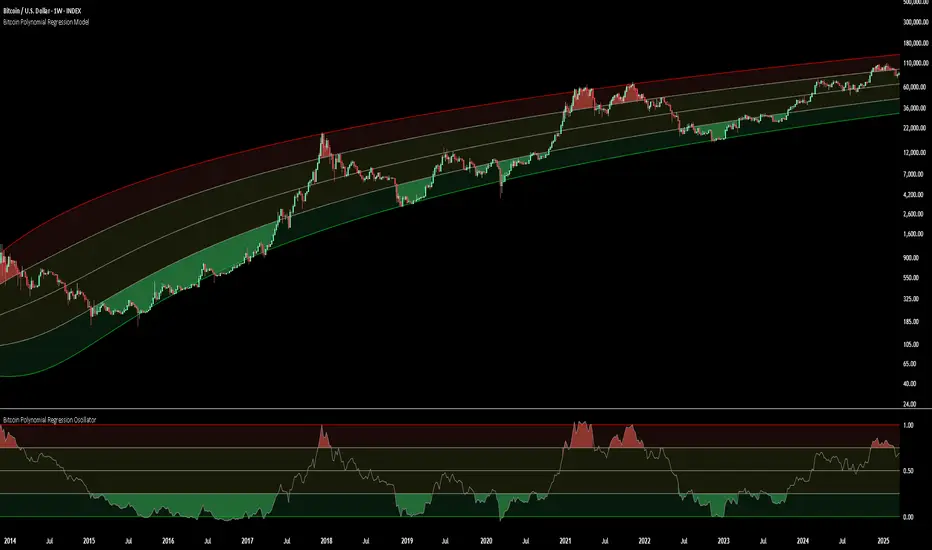

Bitcoin Polynomial Regression ModelThis is the main version of the script. Click here for the Oscillator part of the script.

💡Why this model was created:

One of the key issues with most existing models, including our own Bitcoin Log Growth Curve Model , is that they often fail to realistically account for diminishing returns. As a result, they may present overly optimistic bull cycle targets (hence, we introduced alternative settings in our previous Bitcoin Log Growth Curve Model).

This new model however, has been built from the ground up with a primary focus on incorporating the principle of diminishing returns. It directly responds to this concept, which has been briefly explored here .

📉The theory of diminishing returns:

This theory suggests that as each four-year market cycle unfolds, volatility gradually decreases, leading to more tempered price movements. It also implies that the price increase from one cycle peak to the next will decrease over time as the asset matures. The same pattern applies to cycle lows and the relationship between tops and bottoms. In essence, these price movements are interconnected and should generally follow a consistent pattern. We believe this model provides a more realistic outlook on bull and bear market cycles.

To better understand this theory, the relationships between cycle tops and bottoms are outlined below:https://www.tradingview.com/x/7Hldzsf2/

🔧Creation of the model:

For those interested in how this model was created, the process is explained here. Otherwise, feel free to skip this section.

This model is based on two separate cubic polynomial regression lines. One for the top price trend and another for the bottom. Both follow the general cubic polynomial function:

ax^3 +bx^2 + cx + d.

In this equation, x represents the weekly bar index minus an offset, while a, b, c, and d are determined through polynomial regression analysis. The input (x, y) values used for the polynomial regression analysis are as follows:

Top regression line (x, y) values:

113, 18.6

240, 1004

451, 19128

655, 65502

Bottom regression line (x, y) values:

103, 2.5

267, 211

471, 3193

676, 16255

The values above correspond to historical Bitcoin cycle tops and bottoms, where x is the weekly bar index and y is the weekly closing price of Bitcoin. The best fit is determined using metrics such as R-squared values, residual error analysis, and visual inspection. While the exact details of this evaluation are beyond the scope of this post, the following optimal parameters were found:

Top regression line parameter values:

a: 0.000202798

b: 0.0872922

c: -30.88805

d: 1827.14113

Bottom regression line parameter values:

a: 0.000138314

b: -0.0768236

c: 13.90555

d: -765.8892

📊Polynomial Regression Oscillator:

This publication also includes the oscillator version of the this model which is displayed at the bottom of the screen. The oscillator applies a logarithmic transformation to the price and the regression lines using the formula log10(x) .

The log-transformed price is then normalized using min-max normalization relative to the log-transformed top and bottom regression line with the formula:

normalized price = log(close) - log(bottom regression line) / log(top regression line) - log(bottom regression line)

This transformation results in a price value between 0 and 1 between both the regression lines. The Oscillator version can be found here.

🔍Interpretation of the Model:

In general, the red area represents a caution zone, as historically, the price has often been near its cycle market top within this range. On the other hand, the green area is considered an area of opportunity, as historically, it has corresponded to the market bottom.

The top regression line serves as a signal for the absolute market cycle peak, while the bottom regression line indicates the absolute market cycle bottom.

Additionally, this model provides a predicted range for Bitcoin's future price movements, which can be used to make extrapolated predictions. We will explore this further below.

🔮Future Predictions:

Finally, let's discuss what this model actually predicts for the potential upcoming market cycle top and the corresponding market cycle bottom. In our previous post here , a cycle interval analysis was performed to predict a likely time window for the next cycle top and bottom:

In the image, it is predicted that the next top-to-top cycle interval will be 208 weeks, which translates to November 3rd, 2025. It is also predicted that the bottom-to-top cycle interval will be 152 weeks, which corresponds to October 13th, 2025. On the macro level, these two dates align quite well. For our prediction, we take the average of these two dates: October 24th 2025. This will be our target date for the bull cycle top.

Now, let's do the same for the upcoming cycle bottom. The bottom-to-bottom cycle interval is predicted to be 205 weeks, which translates to October 19th, 2026, and the top-to-bottom cycle interval is predicted to be 259 weeks, which corresponds to October 26th, 2026. We then take the average of these two dates, predicting a bear cycle bottom date target of October 19th, 2026.

Now that we have our predicted top and bottom cycle date targets, we can simply reference these two dates to our model, giving us the Bitcoin top price prediction in the range of 152,000 in Q4 2025 and a subsequent bottom price prediction in the range of 46,500 in Q4 2026.

For those interested in understanding what this specifically means for the predicted diminishing return top and bottom cycle values, the image below displays these predicted values. The new values are highlighted in yellow:

And of course, keep in mind that these targets are just rough estimates. While we've done our best to estimate these targets through a data-driven approach, markets will always remain unpredictable in nature. What are your targets? Feel free to share them in the comment section below.

Bitcoin Polynomial Regression OscillatorThis is the oscillator version of the script. Click here for the other part of the script.

💡Why this model was created:

One of the key issues with most existing models, including our own Bitcoin Log Growth Curve Model , is that they often fail to realistically account for diminishing returns. As a result, they may present overly optimistic bull cycle targets (hence, we introduced alternative settings in our previous Bitcoin Log Growth Curve Model).

This new model however, has been built from the ground up with a primary focus on incorporating the principle of diminishing returns. It directly responds to this concept, which has been briefly explored here .

📉The theory of diminishing returns:

This theory suggests that as each four-year market cycle unfolds, volatility gradually decreases, leading to more tempered price movements. It also implies that the price increase from one cycle peak to the next will decrease over time as the asset matures. The same pattern applies to cycle lows and the relationship between tops and bottoms. In essence, these price movements are interconnected and should generally follow a consistent pattern. We believe this model provides a more realistic outlook on bull and bear market cycles.

To better understand this theory, the relationships between cycle tops and bottoms are outlined below:https://www.tradingview.com/x/7Hldzsf2/

🔧Creation of the model:

For those interested in how this model was created, the process is explained here. Otherwise, feel free to skip this section.

This model is based on two separate cubic polynomial regression lines. One for the top price trend and another for the bottom. Both follow the general cubic polynomial function:

ax^3 +bx^2 + cx + d.

In this equation, x represents the weekly bar index minus an offset, while a, b, c, and d are determined through polynomial regression analysis. The input (x, y) values used for the polynomial regression analysis are as follows:

Top regression line (x, y) values:

113, 18.6

240, 1004

451, 19128

655, 65502

Bottom regression line (x, y) values:

103, 2.5

267, 211

471, 3193

676, 16255

The values above correspond to historical Bitcoin cycle tops and bottoms, where x is the weekly bar index and y is the weekly closing price of Bitcoin. The best fit is determined using metrics such as R-squared values, residual error analysis, and visual inspection. While the exact details of this evaluation are beyond the scope of this post, the following optimal parameters were found:

Top regression line parameter values:

a: 0.000202798

b: 0.0872922

c: -30.88805

d: 1827.14113

Bottom regression line parameter values:

a: 0.000138314

b: -0.0768236

c: 13.90555

d: -765.8892

📊Polynomial Regression Oscillator:

This publication also includes the oscillator version of the this model which is displayed at the bottom of the screen. The oscillator applies a logarithmic transformation to the price and the regression lines using the formula log10(x) .

The log-transformed price is then normalized using min-max normalization relative to the log-transformed top and bottom regression line with the formula:

normalized price = log(close) - log(bottom regression line) / log(top regression line) - log(bottom regression line)

This transformation results in a price value between 0 and 1 between both the regression lines.

🔍Interpretation of the Model:

In general, the red area represents a caution zone, as historically, the price has often been near its cycle market top within this range. On the other hand, the green area is considered an area of opportunity, as historically, it has corresponded to the market bottom.

The top regression line serves as a signal for the absolute market cycle peak, while the bottom regression line indicates the absolute market cycle bottom.

Additionally, this model provides a predicted range for Bitcoin's future price movements, which can be used to make extrapolated predictions. We will explore this further below.

🔮Future Predictions:

Finally, let's discuss what this model actually predicts for the potential upcoming market cycle top and the corresponding market cycle bottom. In our previous post here , a cycle interval analysis was performed to predict a likely time window for the next cycle top and bottom:

In the image, it is predicted that the next top-to-top cycle interval will be 208 weeks, which translates to November 3rd, 2025. It is also predicted that the bottom-to-top cycle interval will be 152 weeks, which corresponds to October 13th, 2025. On the macro level, these two dates align quite well. For our prediction, we take the average of these two dates: October 24th 2025. This will be our target date for the bull cycle top.

Now, let's do the same for the upcoming cycle bottom. The bottom-to-bottom cycle interval is predicted to be 205 weeks, which translates to October 19th, 2026, and the top-to-bottom cycle interval is predicted to be 259 weeks, which corresponds to October 26th, 2026. We then take the average of these two dates, predicting a bear cycle bottom date target of October 19th, 2026.

Now that we have our predicted top and bottom cycle date targets, we can simply reference these two dates to our model, giving us the Bitcoin top price prediction in the range of 152,000 in Q4 2025 and a subsequent bottom price prediction in the range of 46,500 in Q4 2026.

For those interested in understanding what this specifically means for the predicted diminishing return top and bottom cycle values, the image below displays these predicted values. The new values are highlighted in yellow:

And of course, keep in mind that these targets are just rough estimates. While we've done our best to estimate these targets through a data-driven approach, markets will always remain unpredictable in nature. What are your targets? Feel free to share them in the comment section below.

Master Litecoin Miner Sell PressureBrief Description:

Purpose: The indicator overlays on a chart to highlight periods of high miner sell pressure for Litecoin.

Data Sources:

miner_out: Fetches daily Litecoin miner outflows (amount of LTC moved out by miners) using the INTOTHEBLOCK:LTC_MINEROUTFLOWS dataset.

miner_res: Fetches daily Litecoin miner reserves (amount of LTC held by miners) using the INTOTHEBLOCK:LTC_MINERRESERVES dataset.

Calculation:

Computes a ratio m by taking the 14-day sum of miner outflows and dividing it by the 14-day simple moving average (SMA) of miner reserves.

Calculates Bollinger Bands around m:

bbl: Lower band (200-day SMA of m minus 1 standard deviation).

bbu: Upper band (200-day SMA of m plus 1 standard deviation).

Visualization:

If the ratio m exceeds the upper Bollinger Band (bbu), the background is colored blue with 30% opacity, indicating potential high sell pressure from miners.

Fourier Trend Energy (Prototype)Fourier Trend Energy (Prototype)

This indicator brings the logic of Fourier-based trend analysis into Pine Script.

It estimates two key components:

Low-Frequency Energy — representing the strength of the underlying trend

High-Frequency Energy — representing noise, volatility, or deviation from the trend

🔹 Green line → trend strength

🔸 Orange line → short-term noise

🟩🟥 Background color → shows whether trend energy is increasing or decreasing

You can use it to:

Detect early trend formation

Filter fakeouts during consolidation

Spot momentum shifts based on energy crossovers

This is not a traditional oscillator — it’s a frequency-inspired tool to help you understand when the market is charging for a move.

Fuzzy SMA with DCTI Confirmation[FibonacciFlux]FibonacciFlux: Advanced Fuzzy Logic System with Donchian Trend Confirmation

Institutional-grade trend analysis combining adaptive Fuzzy Logic with Donchian Channel Trend Intensity for superior signal quality

Conceptual Framework & Research Foundation

FibonacciFlux represents a significant advancement in quantitative technical analysis, merging two powerful analytical methodologies: normalized fuzzy logic systems and Donchian Channel Trend Intensity (DCTI). This sophisticated indicator addresses a fundamental challenge in market analysis – the inherent imprecision of trend identification in dynamic, multi-dimensional market environments.

While traditional indicators often produce simplistic binary signals, markets exist in states of continuous, graduated transition. FibonacciFlux embraces this complexity through its implementation of fuzzy set theory, enhanced by DCTI's structural trend confirmation capabilities. The result is an indicator that provides nuanced, probabilistic trend assessment with institutional-grade signal quality.

Core Technological Components

1. Advanced Fuzzy Logic System with Percentile Normalization

At the foundation of FibonacciFlux lies a comprehensive fuzzy logic system that transforms conventional technical metrics into degrees of membership in linguistic variables:

// Fuzzy triangular membership function with robust error handling

fuzzy_triangle(val, left, center, right) =>

if na(val)

0.0

float denominator1 = math.max(1e-10, center - left)

float denominator2 = math.max(1e-10, right - center)

math.max(0.0, math.min(left == center ? val <= center ? 1.0 : 0.0 : (val - left) / denominator1,

center == right ? val >= center ? 1.0 : 0.0 : (right - val) / denominator2))

The system employs percentile-based normalization for SMA deviation – a critical innovation that enables self-calibration across different assets and market regimes:

// Percentile-based normalization for adaptive calibration

raw_diff = price_src - sma_val

diff_abs_percentile = ta.percentile_linear_interpolation(math.abs(raw_diff), normLookback, percRank) + 1e-10

normalized_diff_raw = raw_diff / diff_abs_percentile

normalized_diff = useClamping ? math.max(-clampValue, math.min(clampValue, normalized_diff_raw)) : normalized_diff_raw

This normalization approach represents a significant advancement over fixed-threshold systems, allowing the indicator to automatically adapt to varying volatility environments and maintain consistent signal quality across diverse market conditions.

2. Donchian Channel Trend Intensity (DCTI) Integration

FibonacciFlux significantly enhances fuzzy logic analysis through the integration of Donchian Channel Trend Intensity (DCTI) – a sophisticated measure of trend strength based on the relationship between short-term and long-term price extremes:

// DCTI calculation for structural trend confirmation

f_dcti(src, majorPer, minorPer, sigPer) =>

H = ta.highest(high, majorPer) // Major period high

L = ta.lowest(low, majorPer) // Major period low

h = ta.highest(high, minorPer) // Minor period high

l = ta.lowest(low, minorPer) // Minor period low

float pdiv = not na(L) ? l - L : 0 // Positive divergence (low vs major low)

float ndiv = not na(H) ? H - h : 0 // Negative divergence (major high vs high)

float divisor = pdiv + ndiv

dctiValue = divisor == 0 ? 0 : 100 * ((pdiv - ndiv) / divisor) // Normalized to -100 to +100 range

sigValue = ta.ema(dctiValue, sigPer)

DCTI provides a complementary structural perspective on market trends by quantifying the relationship between short-term and long-term price extremes. This creates a multi-dimensional analysis framework that combines adaptive deviation measurement (fuzzy SMA) with channel-based trend intensity confirmation (DCTI).

Multi-Dimensional Fuzzy Input Variables

FibonacciFlux processes four distinct technical dimensions through its fuzzy system:

Normalized SMA Deviation: Measures price displacement relative to historical volatility context

Rate of Change (ROC): Captures price momentum over configurable timeframes

Relative Strength Index (RSI): Evaluates cyclical overbought/oversold conditions

Donchian Channel Trend Intensity (DCTI): Provides structural trend confirmation through channel analysis

Each dimension is processed through comprehensive fuzzy sets that transform crisp numerical values into linguistic variables:

// Normalized SMA Deviation - Self-calibrating to volatility regimes

ndiff_LP := fuzzy_triangle(normalized_diff, norm_scale * 0.3, norm_scale * 0.7, norm_scale * 1.1)

ndiff_SP := fuzzy_triangle(normalized_diff, norm_scale * 0.05, norm_scale * 0.25, norm_scale * 0.5)

ndiff_NZ := fuzzy_triangle(normalized_diff, -norm_scale * 0.1, 0.0, norm_scale * 0.1)

ndiff_SN := fuzzy_triangle(normalized_diff, -norm_scale * 0.5, -norm_scale * 0.25, -norm_scale * 0.05)

ndiff_LN := fuzzy_triangle(normalized_diff, -norm_scale * 1.1, -norm_scale * 0.7, -norm_scale * 0.3)

// DCTI - Structural trend measurement

dcti_SP := fuzzy_triangle(dcti_val, 60.0, 85.0, 101.0) // Strong Positive Trend (> ~85)

dcti_WP := fuzzy_triangle(dcti_val, 20.0, 45.0, 70.0) // Weak Positive Trend (~30-60)

dcti_Z := fuzzy_triangle(dcti_val, -30.0, 0.0, 30.0) // Near Zero / Trendless (~+/- 20)

dcti_WN := fuzzy_triangle(dcti_val, -70.0, -45.0, -20.0) // Weak Negative Trend (~-30 - -60)

dcti_SN := fuzzy_triangle(dcti_val, -101.0, -85.0, -60.0) // Strong Negative Trend (< ~-85)

Advanced Fuzzy Rule System with DCTI Confirmation

The core intelligence of FibonacciFlux lies in its sophisticated fuzzy rule system – a structured knowledge representation that encodes expert understanding of market dynamics:

// Base Trend Rules with DCTI Confirmation

cond1 = math.min(ndiff_LP, roc_HP, rsi_M)

strength_SB := math.max(strength_SB, cond1 * (dcti_SP > 0.5 ? 1.2 : dcti_Z > 0.1 ? 0.5 : 1.0))

// DCTI Override Rules - Structural trend confirmation with momentum alignment

cond14 = math.min(ndiff_NZ, roc_HP, dcti_SP)

strength_SB := math.max(strength_SB, cond14 * 0.5)

The rule system implements 15 distinct fuzzy rules that evaluate various market conditions including:

Established Trends: Strong deviations with confirming momentum and DCTI alignment

Emerging Trends: Early deviation patterns with initial momentum and DCTI confirmation

Weakening Trends: Divergent signals between deviation, momentum, and DCTI

Reversal Conditions: Counter-trend signals with DCTI confirmation

Neutral Consolidations: Minimal deviation with low momentum and neutral DCTI

A key innovation is the weighted influence of DCTI on rule activation. When strong DCTI readings align with other indicators, rule strength is amplified (up to 1.2x). Conversely, when DCTI contradicts other indicators, rule impact is reduced (as low as 0.5x). This creates a dynamic, self-adjusting system that prioritizes high-conviction signals.

Defuzzification & Signal Generation

The final step transforms fuzzy outputs into a precise trend score through center-of-gravity defuzzification:

// Defuzzification with precise floating-point handling

denominator = strength_SB + strength_WB + strength_N + strength_WBe + strength_SBe

if denominator > 1e-10

fuzzyTrendScore := (strength_SB * STRONG_BULL + strength_WB * WEAK_BULL +

strength_N * NEUTRAL + strength_WBe * WEAK_BEAR +

strength_SBe * STRONG_BEAR) / denominator

The resulting FuzzyTrendScore ranges from -1.0 (Strong Bear) to +1.0 (Strong Bull), with critical threshold zones at ±0.3 (Weak trend) and ±0.7 (Strong trend). The histogram visualization employs intuitive color-coding for immediate trend assessment.

Strategic Applications for Institutional Trading

FibonacciFlux provides substantial advantages for sophisticated trading operations:

Multi-Timeframe Signal Confirmation: Institutional-grade signal validation across multiple technical dimensions

Trend Strength Quantification: Precise measurement of trend conviction with noise filtration

Early Trend Identification: Detection of emerging trends before traditional indicators through fuzzy pattern recognition

Adaptive Market Regime Analysis: Self-calibrating analysis across varying volatility environments

Algorithmic Strategy Integration: Well-defined numerical output suitable for systematic trading frameworks

Risk Management Enhancement: Superior signal fidelity for risk exposure optimization

Customization Parameters

FibonacciFlux offers extensive customization to align with specific trading mandates and market conditions:

Fuzzy SMA Settings: Configure baseline trend identification parameters including SMA, ROC, and RSI lengths

Normalization Settings: Fine-tune the self-calibration mechanism with adjustable lookback period, percentile rank, and optional clamping

DCTI Parameters: Optimize trend structure confirmation with adjustable major/minor periods and signal smoothing

Visualization Controls: Customize display transparency for optimal chart integration

These parameters enable precise calibration for different asset classes, timeframes, and market regimes while maintaining the core analytical framework.

Implementation Notes

For optimal implementation, consider the following guidance:

Higher timeframes (4H+) benefit from increased normalization lookback (800+) for stability

Volatile assets may require adjusted clamping values (2.5-4.0) for optimal signal sensitivity

DCTI parameters should be aligned with chart timeframe (higher timeframes require increased major/minor periods)

The indicator performs exceptionally well as a trend filter for systematic trading strategies

Acknowledgments

FibonacciFlux builds upon the pioneering work of Donovan Wall in Donchian Channel Trend Intensity analysis. The normalization approach draws inspiration from percentile-based statistical techniques in quantitative finance. This indicator is shared for educational and analytical purposes under Attribution-NonCommercial-ShareAlike 4.0 International (CC BY-NC-SA 4.0) license.

Past performance does not guarantee future results. All trading involves risk. This indicator should be used as one component of a comprehensive analysis framework.

Shout out @DonovanWall

Fuzzy SMA Trend Analyzer (experimental)[FibonacciFlux]Fuzzy SMA Trend Analyzer (Normalized): Advanced Market Trend Detection Using Fuzzy Logic Theory

Elevate your technical analysis with institutional-grade fuzzy logic implementation

Research Genesis & Conceptual Framework

This indicator represents the culmination of extensive research into applying fuzzy logic theory to financial markets. While traditional technical indicators often produce binary outcomes, market conditions exist on a continuous spectrum. The Fuzzy SMA Trend Analyzer addresses this limitation by implementing a sophisticated fuzzy logic system that captures the nuanced, multi-dimensional nature of market trends.

Core Fuzzy Logic Principles

At the heart of this indicator lies fuzzy logic theory - a mathematical framework designed to handle imprecision and uncertainty:

// Improved fuzzy_triangle function with guard clauses for NA and invalid parameters.

fuzzy_triangle(val, left, center, right) =>

if na(val) or na(left) or na(center) or na(right) or left > center or center > right // Guard checks

0.0

else if left == center and center == right // Crisp set (single point)

val == center ? 1.0 : 0.0

else if left == center // Left-shoulder shape (ramp down from 1 at center to 0 at right)

val >= right ? 0.0 : val <= center ? 1.0 : (right - val) / (right - center)

else if center == right // Right-shoulder shape (ramp up from 0 at left to 1 at center)

val <= left ? 0.0 : val >= center ? 1.0 : (val - left) / (center - left)

else // Standard triangle

math.max(0.0, math.min((val - left) / (center - left), (right - val) / (right - center)))

This implementation of triangular membership functions enables the indicator to transform crisp numerical values into degrees of membership in linguistic variables like "Large Positive" or "Small Negative," creating a more nuanced representation of market conditions.

Dynamic Percentile Normalization

A critical innovation in this indicator is the implementation of percentile-based normalization for SMA deviation:

// ----- Deviation Scale Estimation using Percentile -----

// Calculate the percentile rank of the *absolute* deviation over the lookback period.

// This gives an estimate of the 'typical maximum' deviation magnitude recently.

diff_abs_percentile = ta.percentile_linear_interpolation(math.abs(raw_diff), normLookback, percRank) + 1e-10

// ----- Normalize the Raw Deviation -----

// Divide the raw deviation by the estimated 'typical max' magnitude.

normalized_diff = raw_diff / diff_abs_percentile

// ----- Clamp the Normalized Deviation -----

normalized_diff_clamped = math.max(-3.0, math.min(3.0, normalized_diff))

This percentile normalization approach creates a self-adapting system that automatically calibrates to different assets and market regimes. Rather than using fixed thresholds, the indicator dynamically adjusts based on recent volatility patterns, significantly enhancing signal quality across diverse market environments.

Multi-Factor Fuzzy Rule System

The indicator implements a comprehensive fuzzy rule system that evaluates multiple technical factors:

SMA Deviation (Normalized): Measures price displacement from the Simple Moving Average

Rate of Change (ROC): Captures price momentum over a specified period

Relative Strength Index (RSI): Assesses overbought/oversold conditions

These factors are processed through a sophisticated fuzzy inference system with linguistic variables:

// ----- 3.1 Fuzzy Sets for Normalized Deviation -----

diffN_LP := fuzzy_triangle(normalized_diff_clamped, 0.7, 1.5, 3.0) // Large Positive (around/above percentile)

diffN_SP := fuzzy_triangle(normalized_diff_clamped, 0.1, 0.5, 0.9) // Small Positive

diffN_NZ := fuzzy_triangle(normalized_diff_clamped, -0.2, 0.0, 0.2) // Near Zero

diffN_SN := fuzzy_triangle(normalized_diff_clamped, -0.9, -0.5, -0.1) // Small Negative

diffN_LN := fuzzy_triangle(normalized_diff_clamped, -3.0, -1.5, -0.7) // Large Negative (around/below percentile)

// ----- 3.2 Fuzzy Sets for ROC -----

roc_HN := fuzzy_triangle(roc_val, -8.0, -5.0, -2.0)

roc_WN := fuzzy_triangle(roc_val, -3.0, -1.0, -0.1)

roc_NZ := fuzzy_triangle(roc_val, -0.3, 0.0, 0.3)

roc_WP := fuzzy_triangle(roc_val, 0.1, 1.0, 3.0)

roc_HP := fuzzy_triangle(roc_val, 2.0, 5.0, 8.0)

// ----- 3.3 Fuzzy Sets for RSI -----

rsi_L := fuzzy_triangle(rsi_val, 0.0, 25.0, 40.0)

rsi_M := fuzzy_triangle(rsi_val, 35.0, 50.0, 65.0)

rsi_H := fuzzy_triangle(rsi_val, 60.0, 75.0, 100.0)

Advanced Fuzzy Inference Rules

The indicator employs a comprehensive set of fuzzy rules that encode expert knowledge about market behavior:

// --- Fuzzy Rules using Normalized Deviation (diffN_*) ---

cond1 = math.min(diffN_LP, roc_HP, math.max(rsi_M, rsi_H)) // Strong Bullish: Large pos dev, strong pos roc, rsi ok

strength_SB := math.max(strength_SB, cond1)

cond2 = math.min(diffN_SP, roc_WP, rsi_M) // Weak Bullish: Small pos dev, weak pos roc, rsi mid

strength_WB := math.max(strength_WB, cond2)

cond3 = math.min(diffN_SP, roc_NZ, rsi_H) // Weakening Bullish: Small pos dev, flat roc, rsi high

strength_N := math.max(strength_N, cond3 * 0.6) // More neutral

strength_WB := math.max(strength_WB, cond3 * 0.2) // Less weak bullish

This rule system evaluates multiple conditions simultaneously, weighting them by their degree of membership to produce a comprehensive trend assessment. The rules are designed to identify various market conditions including strong trends, weakening trends, potential reversals, and neutral consolidations.

Defuzzification Process

The final step transforms the fuzzy result back into a crisp numerical value representing the overall trend strength:

// --- Step 6: Defuzzification ---

denominator = strength_SB + strength_WB + strength_N + strength_WBe + strength_SBe

if denominator > 1e-10 // Use small epsilon instead of != 0.0 for float comparison

fuzzyTrendScore := (strength_SB * STRONG_BULL +

strength_WB * WEAK_BULL +

strength_N * NEUTRAL +

strength_WBe * WEAK_BEAR +

strength_SBe * STRONG_BEAR) / denominator

The resulting FuzzyTrendScore ranges from -1 (strong bearish) to +1 (strong bullish), providing a smooth, continuous evaluation of market conditions that avoids the abrupt signal changes common in traditional indicators.

Advanced Visualization with Rainbow Gradient

The indicator incorporates sophisticated visualization using a rainbow gradient coloring system:

// Normalize score to for gradient function

normalizedScore = na(fuzzyTrendScore) ? 0.5 : math.max(0.0, math.min(1.0, (fuzzyTrendScore + 1) / 2))

// Get the color based on gradient setting and normalized score

final_color = get_gradient(normalizedScore, gradient_type)

This color-coding system provides intuitive visual feedback, with color intensity reflecting trend strength and direction. The gradient can be customized between Red-to-Green or Red-to-Blue configurations based on user preference.

Practical Applications

The Fuzzy SMA Trend Analyzer excels in several key applications:

Trend Identification: Precisely identifies market trend direction and strength with nuanced gradation

Market Regime Detection: Distinguishes between trending markets and consolidation phases

Divergence Analysis: Highlights potential reversals when price action and fuzzy trend score diverge

Filter for Trading Systems: Provides high-quality trend filtering for other trading strategies

Risk Management: Offers early warning of potential trend weakening or reversal

Parameter Customization

The indicator offers extensive customization options:

SMA Length: Adjusts the baseline moving average period

ROC Length: Controls momentum sensitivity

RSI Length: Configures overbought/oversold sensitivity

Normalization Lookback: Determines the adaptive calculation window for percentile normalization

Percentile Rank: Sets the statistical threshold for deviation normalization

Gradient Type: Selects the preferred color scheme for visualization

These parameters enable fine-tuning to specific market conditions, trading styles, and timeframes.

Acknowledgments

The rainbow gradient visualization component draws inspiration from LuxAlgo's "Rainbow Adaptive RSI" (used under CC BY-NC-SA 4.0 license). This implementation of fuzzy logic in technical analysis builds upon Fermi estimation principles to overcome the inherent limitations of crisp binary indicators.

This indicator is shared under Attribution-NonCommercial-ShareAlike 4.0 International (CC BY-NC-SA 4.0) license.

Remember that past performance does not guarantee future results. Always conduct thorough testing before implementing any technical indicator in live trading.

Super Cycle Low FinderHow the Indicator Works

1. Inputs

Users can adjust the cycle lengths:

Daily Cycle: Default is 40 days (within 36-44 days).

Weekly Cycle: Default is 26 weeks (182 days, within 22-31 weeks).

Yearly Cycle: Default is 4 years (1460 days).

2. Cycle Low Detection

Function: detect_cycle_low finds the lowest low over the specified period and confirms it with a bullish candle (close > open).

Timeframes: Daily lows are calculated directly; weekly and yearly lows use request.security to fetch data from higher timeframes.

3. Half Cycle Lows

Detected over half the cycle length, plotted to show mid-cycle strength or weakness.

4. Cycle Translation

Logic: Compares the position of the highest high to the cycle’s midpoint.

Output: "R" for right translated (bullish), "L" for left translated (bearish), displayed above bars.

5. Cycle Failure

Flags when a new low falls below the previous cycle low, indicating a breakdown.

6. Visualization

Cycle Lows: Diamonds below bars (yellow for daily, green for weekly, blue for yearly).

Half Cycle Lows: Circles below bars (orange, lime, aqua).

Translations: "R" or "L" above bars in distinct colors.

Failures: Downward triangles below bars (red, orange, purple).

TimeMapTimeMap is a visual price-reference indicator designed to help traders rapidly visualize how current price levels relate to significant historical closing prices. It overlays your chart with reference lines representing past weekly, monthly, quarterly (3-month), semi-annual (6-month), and annual closing prices. By clearly plotting these historical price references, TimeMap helps traders quickly gauge price position relative to historical market structure, aiding in the identification of trends, support/resistance levels, and potential reversals.

How it Works:

The indicator calculates the precise number of historical bars corresponding to weekly, monthly, quarterly, semi-annual, and annual intervals, dynamically adjusting according to your chart’s timeframe (intraday, daily, weekly, monthly) and chosen market type (Stocks US, Crypto, Forex, or Futures). Historical closing prices from these periods are plotted directly on your chart as horizontal reference lines.

For intraday traders, the script accurately calculates historical offsets considering regular and extended trading sessions (e.g., pre-market and after-hours sessions for US stocks), ensuring correct positioning of historical lines.

User-Configurable Inputs Explained in Detail:

Market Type:

Allows you to specify your trading instrument type, automatically adjusting calculations for:

- Stocks US (default): 390 minutes per regular session (780 minutes if extended hours enabled), 5 trading days/week.

- Crypto: 1440 minutes/day, 7 trading days/week.

- Forex: 1440 minutes/day, 5 trading days/week.

- Futures: 1320 minutes/day, 5 trading days/week.

Show Weekly Close:

When enabled, plots a line at the exact closing price from one week ago. Provides short-term context and helps identify recent price momentum.

Show Monthly Close:

When enabled, plots a line at the exact closing price from one month ago. Helpful for evaluating medium-term price positioning and monthly trend strength.

Show 3-Month Close:

When enabled, plots a line at the exact closing price from three months ago. Useful for assessing quarterly market shifts, intermediate trend changes, and broader market sentiment.

Show 6-Month Close:

When enabled, plots a line at the exact closing price from six months ago. Useful for identifying semi-annual trends, significant price pivots, and longer-term support/resistance levels.

Show 1-Year Close:

When enabled, plots a line at the exact closing price from one year ago. Excellent for assessing long-term market direction and key annual price levels.

Enable Smoothing:

Activates a Simple Moving Average (SMA) smoothing of historical reference lines, reducing volatility and providing clearer visual references. Recommended for traders preferring less volatile reference levels.

Smoothing Length:

Determines the number of bars used in calculating the SMA smoothing of historical lines. Higher values result in smoother but slightly delayed reference lines; lower values offer more immediate yet more volatile levels.

Use Extended Hours (Intraday Only):

When enabled (only applicable for Stocks US), it accounts for pre-market and after-hours trading sessions, providing accurate intraday historical line calculations based on extended sessions (typically 780 minutes/day total).

Important Notes and Compliance:

- This indicator does not provide trading signals, recommendations, or predictions. It serves purely as a visual analytical tool to supplement traders’ existing methods.

- Historical lines plotted are strictly based on past available price data; the indicator never accesses future data or data outside the scope of Pine Script’s standard capabilities.

- The script incorporates built-in logic to avoid runtime errors if insufficient historical data exists for a selected timeframe, ensuring robustness even with limited historical bars.

- TimeMap is original work developed exclusively by Julien Eche (@Julien_Eche). It does not reuse or replicate third-party or existing open-source scripts.

Recommended Best Practices:

- Use TimeMap as a complementary analytical reference, not as a standalone strategy or trade decision-making tool.

- Adapt displayed historical periods and smoothing settings based on your trading style and market approach.

- Default plot colors are optimized for readability on dark-background charts; adjust as necessary according to your preference and chart color scheme.

This script is published open-source to benefit the entire TradingView community and fully complies with all TradingView script publishing rules and guidelines.

True Open CalculationsIndicator Description: True Open Calculations

This custom Pine Script indicator calculates and plots key "True Open" levels based on specific time intervals and trading sessions. The True Open levels represent significant price points on the chart, helping traders identify key reference points tied to various market opening times. These levels are important for understanding price action in relation to market sessions and trading cycles. The indicator is designed to plot lines corresponding to different "True Opens" on the chart and display labels with the associated information.

Key Features:

True Year Open:

This represents the opening price on the first Monday of April each year. It serves as a reference point for the yearly price level.

Plot Color: Green.

True Month Open:

This represents the opening price on the second Monday of each month. It helps in identifying monthly trends and provides a key reference for monthly price movements.

Plot Color: Blue.

True Week Open:

This represents the opening price every Monday at 6:00 PM. It gives traders a level to track weekly opening movements and can be useful for weekly trend analysis.

Plot Color: Orange.

True Day Open:

This represents the opening price at 12:00 AM (midnight) each day. It serves as a daily benchmark for price action at the start of the trading day.

Plot Color: Red.

True New York Session Open:

This represents the opening price at 7:30 AM (New York session start time). This level is crucial for traders focused on the New York trading session.

Plot Color: Purple.

Additional Features:

Labels: The indicator displays labels to the right of each plotted line to describe which "True Open" it represents (e.g., "True Year Open," "True Month Open," etc.).

Dynamic Plotting: The lines are only plotted on the current candle, and the lines are dynamically updated for each time period based on the corresponding "True Open."

Visual Cues: The colors of the plotted lines (green, blue, orange, red, purple) help quickly distinguish between different "True Open" levels, making it easy for traders to track price action and make informed decisions.

Use Cases:

Yearly, Monthly, Weekly, Daily, and Session Benchmarking: This indicator provides traders with important price levels to use as benchmarks for the current year, month, week, and day, helping to identify trends and potential reversals.

Session Awareness: It is particularly useful for traders who want to track key market sessions, such as the New York session, and their impact on price movement.

Long-term Analysis: By including the yearly open, this indicator helps traders gain a broader perspective on market trends and provides context for analyzing shorter-term price movements.

Benefits:

Helps identify important reference points for longer-term trends (yearly, monthly) as well as shorter-term moves (daily, weekly, and session).

Visually intuitive with color-coded lines and labels, allowing quick and easy identification of key market open levels.

Dynamic and real-time: The indicator plots and updates the True Open levels dynamically as the market progresses.

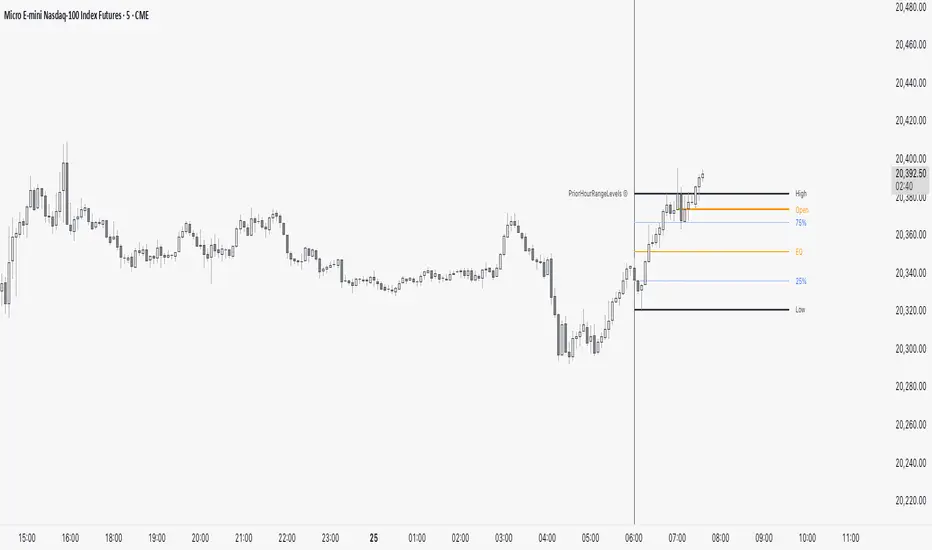

PriorHourRangeLevels_v0.1PriorHourRangeLevels_v0.1

Created by dc_77 | © 2025 | Mozilla Public License 2.0

Overview

"PriorHourRangeLevels_v0.1" is a versatile Pine Script™ indicator designed to help traders visualize and analyze price levels based on the prior hour’s range. It overlays key levels—High, Low, 75%, 50% (EQ), and 25%—from the previous hour onto the current price chart, alongside the current hour’s opening price. With customizable display options and time zone support, it’s ideal for intraday traders looking to identify support, resistance, and breakout zones.

How It Works

Hourly Reset: The indicator detects the start of each hour based on your chosen time zone (e.g., "America/New_York" by default).

Prior Hour Range: It calculates the High and Low of the previous hour, then derives three additional levels:

75%: 75% of the range above the Low.

EQ (50%): The midpoint of the range.

25%: 25% of the range above the Low.

Current Hour Open: Displays the opening price of the current hour.

Projection: Lines extend forward (default: 24 bars) to project these levels into the future, aiding in real-time analysis.

Alerts: Triggers alerts when the price crosses any of the prior hour’s levels (High, 75%, EQ, 25%, Low).

Key Features

Time Zone Flexibility: Choose from options like UTC, New York, Tokyo, or London to align with your trading session.

Visual Customization:

Toggle visibility for each level (High, Low, 75%, EQ, 25%, Open, and Anchor).

Adjust line styles (Solid, Dashed, Dotted), colors, and widths.

Show or hide labels with adjustable sizes (Tiny, Small, Normal, Large).

Anchor Line: A vertical line marks the start of the prior hour, with optional labeling.

Alert Conditions: Set up notifications for price crossings to catch key moments without watching the chart.

Usage Tips

Use the High and Low as potential breakout levels, while 75%, EQ, and 25% act as intermediate support/resistance zones.

Trend Confirmation: Watch how price interacts with the EQ (50%) level to gauge momentum.

Session Planning: Adjust the time zone to match your market (e.g., "Europe/London" for FTSE trading).

Projection Offset: Extend or shorten the lines (via "Projection Offset") based on your chart timeframe.

Inputs

Time Zone: Select your preferred market time zone.

Anchor Settings: Show/hide the prior hour start line, style, color, width, and label.

Level Settings: Customize visibility, style, color, width, and labels for Open, High, 75%, EQ, 25%, and Low.

Display: Set projection length and label size.

SessionRangeLevels_v0.1SessionRangeLevels_v0.1

Overview:

SessionRangeLevels_v0.1 is a customizable Pine Script (v6) indicator designed to plot key price levels based on a user-defined trading session. It identifies the high and low of the session and calculates intermediate levels (75%, 50% "EQ", and 25%) within that range. These levels are projected forward as horizontal lines with accompanying labels, providing traders with dynamic support and resistance zones. The indicator supports extensive customization for session timing, time zones, line styles, colors, and more.

Key Features:

Session-Based Range Detection: Tracks the high and low prices during a specified session (e.g., 0600-0900) and updates them dynamically as the session progresses.

Customizable Levels: Displays High, 75%, EQ (50%), 25%, and Low levels, each with independent toggle options, styles (Solid, Dashed, Dotted), colors, and widths.

Session Anchor: Optional vertical line marking the session start, with customizable style, color, and width.

Projection Offset: Extends level lines forward by a user-defined number of bars (default: 24) for future price reference.

Labels: Toggleable labels for each level (e.g., "High," "75%," "EQ") with adjustable size (Tiny, Small, Normal, Large).

Time Zone Support: Aligns session timing to a selected time zone (e.g., America/New_York, UTC, Asia/Tokyo, etc.).

Alert Conditions: Triggers alerts when the price crosses any of the plotted levels (High, 75%, EQ, 25%, Low).

Inputs:

Session Time (HHMM-HHMM): Define the session range (e.g., "0600-0900" for 6:00 AM to 9:00 AM).

Time Zone: Choose from options like UTC, America/New_York, Europe/London, etc.

Anchor Settings: Toggle the session start line, adjust its style (default: Dotted), color (default: Black), and width (default: 1).

Level Settings:

High (Solid, Black, Width 2)

75% (Dotted, Blue, Width 1)

EQ/50% (Dotted, Orange, Width 1)

25% (Dotted, Blue, Width 1)

Low (Solid, Black, Width 2)

Each level includes options to show/hide, set style, color, width, and label visibility.

Projection Offset: Number of bars to extend lines (default: 24).

Label Size: Set label size (default: Small).

How It Works:

The indicator detects the start and end of the user-defined session based on the specified time and time zone.

During the session, it tracks the highest high and lowest low, updating the levels in real-time.

At the session start, it plots the High, Low, and intermediate levels (75%, 50%, 25%), projecting them forward.

Lines and labels dynamically adjust as new highs or lows occur within the session.

Alerts notify users when the price crosses any active level.

Usage:

Ideal for traders who focus on session-based strategies (e.g., London or New York open). Use it to identify key price zones, monitor breakouts, or set targets. Customize the appearance to suit your chart preferences and enable alerts for real-time trading signals.

Notes:

Ensure your chart’s timeframe aligns with your session duration for optimal results (e.g., 1-minute or 5-minute charts for short sessions).

The indicator overlays directly on the price chart for easy integration with other tools.

BTC & SPX vs Yield Curve: Recession Risk ZonesBTC & SPX vs Yield Curve – Recession Risk Zones

This tool helps you track Bitcoin (BTC) and the S&P 500 (SPX) against key macro signals from the U.S. yield curve to spot potential recession risks.

🟪 Color Legend:

🔴 Red = Yield curve is inverted (warning starts)

🟡 Yellow = Projected 6–18 month recession risk (if inversion still active)

🟠 Orange = Active 6–18 month risk window (after inversion ends)

💜 Fuchsia = Real historical U.S. recessions

📈 What’s Plotted:

🔵 BTCUSD (blue line) – Normalized price

🟢 S&P 500 (green line) – Normalized price

🟠 10Y–2Y Yield Spread – Macro signal for risk

✅ Use it to:

Spot macro pressure zones

See how BTC and SPX behave around economic stress

Stay cautious when red/orange/yellow areas appear

Let me know if you'd like to enable toggles to hide/show BTC or SPX independently!

alphaJohnny Dynamic RSI IndicatorAlphaJohnny Dynamic RSI Indicator (Dyn RSI)

The Dynamic RSI Indicator (Dyn RSI) is a custom Pine Script tool designed for TradingView that aggregates Relative Strength Index (RSI) signals from multiple timeframes to provide a comprehensive view of market momentum. It combines RSI data from Weekly, Daily, 4-hour, 1-hour, and 30-minute intervals, offering traders a flexible and customizable way to analyze trends across different periods.

Key Features:

Multi-Timeframe RSI Aggregation: Combines RSI signals from user-selected timeframes for a holistic momentum assessment.

Dynamic or Equal Weighting: Choose between correlation-based dynamic weights (adjusting based on each timeframe’s correlation with price changes) or equal weights for simplicity.

Smoothed Momentum Line: A visually intuitive line that reflects the strength of the aggregate signal, smoothed for clarity.

Color-Coded Signal Strength:

Dark Green: Strong buy signal

Light Green: Weak buy signal

Yellow: Neutral

Light Red: Weak sell signal

Dark Red: Strong sell signal

Visual Markers: Large green triangles at the bottom for strong buy signals and red triangles at the top for strong sell signals.

How to Use:

Apply to Chart: Add the indicator to your TradingView chart (it will appear in a separate pane).

Customize Settings: Adjust inputs like RSI period, signal thresholds, included timeframes, weighting method, and smoothing period to fit your trading style.

Interpret Signals:

Momentum Line: Watch for color changes to gauge market conditions.

Triangles: Green at the bottom for strong buy opportunities, red at the top for strong sell opportunities.

Notes:

The indicator is designed for a separate pane (overlay=false), with triangles positioned relative to the pane’s range.

Fine-tune thresholds and weights based on your strategy and the asset being analyzed.

The source code is open for modification to suit your needs.

This indicator is ideal for traders seeking a multi-timeframe perspective on RSI to identify potential trend reversals and momentum shifts.

M2SL/DXY RatioThis is the ratio of M2 money supply (M2SL) to the U.S. dollar index (DXY), taking into account the impact of U.S. dollar strength and weakness on liquidity.

M2SL/DXY better represents the current impact of the United States on cryptocurrency prices.

Lukiano BTC 369 Close MarkerThis indicator highlights candles where the closing price reduces to 3, 6, or 9 based on digital root calculation (sum of digits).

🔵 Blue dot = 3

🟢 Green dot = 6

🔴 Red dot = 9

Inspired by Tesla’s 369 theory and adapted for BTC traders who want to explore alternative energy-based signals.

Created by @Lukiano

Suppot and resistance & BUY SELL SIGNALSThis indicator is highly customizable and suitable for traders of all experience levels. By adjusting the input settings, traders can tailor the indicator to their specific needs and trading strategies.

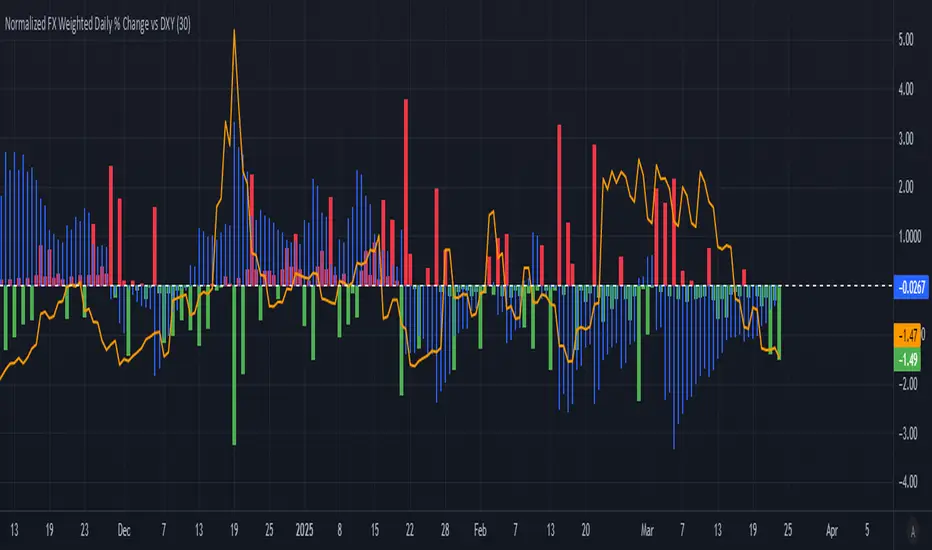

Normalized FX Weighted Daily % Change vs DXYThis indicator tracks international liquidity flows by measuring the USD’s relative strength against major currencies—EUR, CNY, JPY, GBP, and CAD. It calculates the weighted percentage change of each pair over a specified interval. A positive reading means the USD is weakening (liquidity flowing out of the US), while a negative reading indicates the USD is strengthening (liquidity flowing in). Additionally, the indicator incorporates the DXY index and VIX, with all components normalized using Z-scores for clear, comparable insights into market dynamics.