Crystal Order BlockThe Crystal Order Block Indicator is a powerful tool designed to help traders identify key institutional order blocks with high precision. This indicator is ideal for traders following Smart Money Concepts (SMC) and Institutional Trading Strategies, providing clear insights into potential high-probability trade setups.

🔹 Key Features:

✔ Automatic Order Block Detection: Identifies valid bullish & bearish order blocks.

✔ Unmitigated Order Blocks Highlighted: Focuses on fresh order blocks for improved trade opportunities.

✔ Trend-Focused Trading: Works best when combined with market structure analysis.

✔ Multi-Timeframe Support: Suitable for scalping, swing trading, and intraday trading.

✔ Risk Management Enhancement: Helps traders refine entries and exits based on institutional price movements.

📈 How to Use the Crystal Order Block Indicator:

🔹 Identifying Order Blocks:

➡ The indicator automatically detects order blocks formed by institutional trading activity.

➡ Unmitigated order blocks are highlighted, indicating areas where price may react.

🔹 High-Probability Trade Setups:

➡ Buy Setup: Look for a bullish order block in an uptrend, confirming strength.

➡ Sell Setup: Identify a bearish order block in a downtrend for potential short trades.

🔹 Order Block Mitigation:

➡ The updated version filters out mitigated order blocks, allowing traders to focus on fresh trading opportunities.

📊 Best Practices & Timeframes:

🔸 Works on all timeframes, but higher accuracy is observed on M30 and above.

🔸 Best suited for Smart Money Trading, Institutional Trading, and Price Action Strategies.

🔸 Should be used with liquidity concepts and market structure analysis for enhanced precision.

⚠ Important Note:

This indicator is a technical tool designed to assist traders in market analysis. It does not guarantee success and should be used alongside proper risk management and trading discipline.

Cycles

Flat NumbersCustomizable Price Range: Set the start price and end price to define the range in which horizontal lines will be plotted.

Line Color: Choose the color of the horizontal lines to match your chart's theme or personal preference.

Line Width: Adjust the width of the lines (from 1 to 5) to control their visibility.

Price Step Size: By default, the script plots lines every 100 price units within the range, but this step size can be customized if desired.

Dynamic Line Plotting: The script automatically calculates the number of lines needed and plots them at each interval between the start and end prices.

Hanzo_Wave_Price %Hanzo_Wave_Price % is a custom indicator for the TradingView platform that combines RSI (Relative Strength Index) and Stochastic RSI while also displaying the percentage price change over a specified period. This indicator helps traders identify overbought and oversold conditions, analyze price waves, and forecast potential market movements.

How It Works

1. RSI and Stochastic RSI Calculation

RSI is calculated based on the selected price source (default: close) with a user-defined Main Line period.

Stochastic RSI is then applied and smoothed using a moving average.

The Main Line represents the smoothed Stochastic RSI, serving as a wave indicator to help identify potential entry and exit points.

2. Overbought and Oversold Zones

The 70 and 30 levels indicate overbought and oversold zones, displayed as dashed lines on the chart.

Additional 20% and 10% levels provide a visual reference for historical price changes, aiding in future predictions.

3. Percentage Price Change Calculation

The indicator calculates the percentage price change over a Barsback period (default: 30 candles).

Users can choose a multiplier (100 or 1000) for better visualization (1000 scales the values by dividing by 10).

The data is displayed as a colored area:

Red (Short) → Negative price change.

Green (Buy) → Positive price change.

Settings & Parameters

Multiplier 💪 – Selects the scaling factor (100 or 1000) for percentage values.

Main Line ✈️ – Stochastic smoothing period (smoothK).

Don't touch ✋ – Reserved value (do not modify).

RSI 🔴 – RSI calculation period.

Stochastic 🔵 – Stochastic RSI calculation period.

Source ⚠️ – Price source for calculations (default: close).

Price changes % 🔼🔽 – Enables percentage price change display.

Barsback ↩️ – Number of candles used to calculate price change.

Visual Representation

Gray Line (Takeprofit Line 🎯) – Smoothed Stochastic RSI.

Red Dashed Line (70) – Overbought zone.

Blue Dashed Line (30) – Oversold zone.

Percentage Price Change Display:

Green Fill → Price increase.

Red Fill → Price decrease.

Advantages

✅ Combined Analysis – Uses RSI and Stochastic RSI for more accurate market condition identification.

✅ Flexibility – Customizable parameters allow adaptation for different markets and strategies.

✅ Visual Clarity – Clearly defined zones and dynamic percentage change display.

✅ Additional Market Insights – The percentage price change helps assess market volatility.

Disadvantages

⚠ Lagging Signals – Smoothing may cause delayed response.

⚠ False Breakouts – The 70/30 levels may not always work effectively for all assets.

⚠ IMPORTANT!

This indicator is for informational and educational purposes only. Past performance does not guarantee future profits! Use it in combination with other technical analysis tools. 🚀

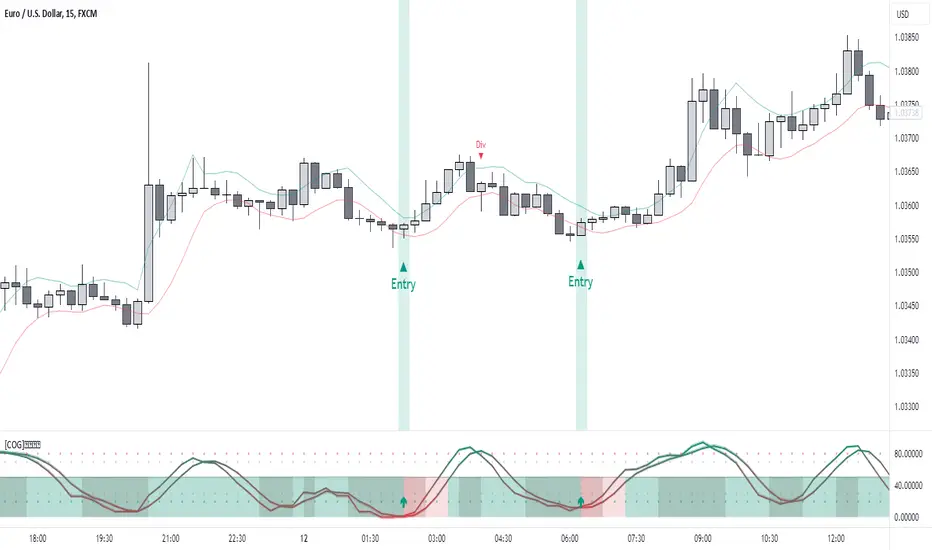

Example 1: Identifying a Long Position

📌 Scenario:

The asset price has dropped significantly (1-hour timeframe), and the Main Line (gray line) crosses below the 30 level. This signals oversold conditions, which may indicate a potential reversal or upward correction.

✅ How to Use:

1️⃣ Identifying the Entry Zone:

If the Main Line is below 30, consider looking for a long entry point.

2️⃣ Confirming the Signal:

Place a vertical line at the moment when the Main Line crosses the 30 level from below.

3️⃣ Confirmation on a Lower Timeframe:

Switch to a 30-minute timeframe and wait for the Main Line to cross above the 70 level.

Enter a long position at this point.

4️⃣ Analyzing Percentage Price Change:

Check the historical indicator behavior:

If a similar past movement resulted in a ~10% price increase (green fill), this may indicate potential upward momentum.

5️⃣ Setting Take-Profit:

Set a take-profit level at 10%, based on previous price movements.

Also, monitor when the Main Line crosses the 70 level, as this may signal a potential profit-taking point.

📊 Conclusion:

This method helps to precisely determine entry points by confirming signals across multiple timeframes and analyzing the historical volatility of the asset. 🚀

Example 2: Analyzing Percentage Price Change

📌 Scenario:

You have set the Barsback parameter to 30, and the indicator shows +3.5%. This means that over the last 30 candles, the price has increased by 3.5%.

However, such small changes might be visually difficult to notice. To improve visibility, you can enable the multiplier (1000), which will scale the displayed percentage change to 35%. This is purely for visual convenience—the actual price movement remains 3.5%.

✅ How to Use:

1️⃣ Identifying Trend Direction:

If the percentage change is positive (green area) → Uptrend.

If the percentage change is negative (red area) → Downtrend.

2️⃣ Analyzing Movement Strength:

Compare the current percentage change with previous waves to evaluate the strength of the movement.

For example:

If previous waves reached 10% or more, a current wave of 3.5% might indicate a weak trend or a local correction.

3️⃣ Additional Filtering with the Main Line (Gray Line):

Use the Main Line to confirm the trend.

If the percentage change shows an increase, but the Main Line is still below 30, further upward movement can be expected.

If the percentage change indicates a decline, but the Main Line is above 70, there is a higher probability of a downward reversal.

"It's unfortunate that TradingView restricts adding images to indicator descriptions unless you have a paid subscription. This makes it harder to share free tools effectively."

Window Seasonality IndicatorThis is a time window seasonal returns indicator. That is, it will provide the mean returns for a given time window based on a given number of lookbacks set by the user. The script finds matching time windows, e.g., 1st week of March going back 5 years or 9:00-10:00 window of every day going 50 days, and then calculates an average return for that window close price with respect to the close price in the immediately preceding time window, e.g. last week of February or 8:00-9:00 close price, respectively.

There are 4 input options:

1) Historical Periods to Average: Set the number of matching historical windows with which to calculate an average price. The max is 730 lookback windows. Note: for monthly or weekly windows, setting too large a number will cause the script to error out.

2) Use Open Price: calculates the seasonal returns using the open price rather than close price.

3) Show Bands: select from 1 Gaussian standard deviation or a nonparamateric ranked confidence interval. As a rough heuristic, the Gaussian band requires at least 30 lookback periods, and the ranked confidence interval requires 50 or more.

4) Upper Percentile: set the upper cutoff for ranked confidence interval.

5) Lower Percentile: set the lower cutoff for ranked confidence interval.

Please be aware, this indicator does not use rigorous statistical methodology and does not imply predictive power. You'll notice the range bands are very wide. Do not trade solely based on this indicator! Certain time windows, such as weekly and monthly, will make more sense applied to commodities, where annual cycles play a role in its supply and demand dynamics. Hourly windows are more useful in looking at equities markets. I like to look at equities with 1-hr windows to see if there is some pattern to overnight behavior or for market open and close.

New Day DividerPlots vertical dividers on your chart to mark the beginning of a new trading day based on your preferred time convention.

✅ Customizable New Day Start Time:

"Use Midnight" → Marks the start of a new day at 00:00 (midnight) in the selected timezone.

"Use Digital Open" → Marks the start of a new day at 18:00 New York time, commonly used for digital asset trading.

✅ Full Timezone Support:

Choose from all U.S. time zones (default: New York).

Supports UTC and full UTC offset adjustments for global traders.

✅ Customizable Line Appearance:

Select divider color, width, and style (Solid, Dashed, or Dotted).

Supertrend Strategy with Money Ocean TradeStrategy Overview

The Supertrend Strategy with Trend Change Confirmation leverages the Supertrend indicator to identify potential buy and sell signals based on changes in trend direction and subsequent price action. The strategy is designed to work with any financial instrument (symbol) and aims to provide clear entry and exit signals.

Key Components

Supertrend Indicator: The core of this strategy is the Supertrend indicator, calculated using a length of 3 and a factor of 1. The Supertrend line is plotted on the chart to visually represent trend direction.

Direction 1: Indicates an uptrend (bullish).

Direction -1: Indicates a downtrend (bearish).

Trend Change Detection: The strategy monitors changes in the trend direction. When a trend change is detected, it checks if the next candle confirms the trend change by breaking above or below the Supertrend line.

Entry Conditions:

Long Entry (Buy): When the Supertrend direction changes to 1 (uptrend) and the next candle closes above the Supertrend line.

Short Entry (Sell): When the Supertrend direction changes to -1 (downtrend) and the next candle closes below the Supertrend line.

Exit Conditions: The strategy closes the position based on the opposite signal.

Long Exit: When the Supertrend direction changes to -1 (downtrend) and the next candle closes below the Supertrend line.

Short Exit: When the Supertrend direction changes to 1 (uptrend) and the next candle closes above the Supertrend line.

Visual Signals: The strategy plots buy and sell signals on the chart using plotshape:

BUY: A green label below the bar when a long entry is triggered.

SELL: A red label above the bar when a short entry is triggered.

Alerts: Alerts are set up to notify when a buy or sell signal is triggered.

Script Summary

This strategy helps traders identify potential trading opportunities based on trend changes and confirms the trend by checking the next candle's price action. The visual signals and dashboard enhance the user's ability to monitor and manage trades effectively.

Feel free to test and adjust the parameters to suit your trading preferences! If you need further customizations or explanations, let me know.

RSI Signal Pro[UgurTash]Introducing RSI Signal Pro for TradingView

RSI Signal Pro is a refined version of the standard Relative Strength Index (RSI) , designed to improve signal accuracy by generating alerts in real-time instead of waiting for multiple candle confirmations. This enhancement allows traders to react faster to market movements while maintaining the familiar RSI structure.

What Makes RSI Signal Pro Unique?

✅ Real-Time RSI Signals: Unlike the traditional RSI, which waits for candle confirmations, this version provides immediate buy and sell signals upon key level crossovers.

✅ Dual Trading Modes: Choose between Simple Mode (standard RSI crossovers) and Advanced Mode (momentum-adjusted signals with price validation).

✅ Customizable RSI-Based Moving Average (MA): Optionally apply SMA, EMA, WMA, or VWMA to smooth RSI fluctuations and identify longer-term trends.

✅ Adaptive Signal Filtering: The Advanced Mode reduces false signals by filtering RSI movements with a momentum threshold and historical RSI validation.

✅ User-Friendly Interface: Simple ON/OFF toggles allow easy customization of the indicator's behavior.

How This Indicator Works

🔹 Simple Mode: Identical to traditional RSI, triggering signals when RSI crosses 30 (bullish) or 70 (bearish).

🔹 Advanced Mode: Uses historical RSI pivots, momentum verification, and price confirmation to refine signal accuracy—ideal for traders looking for more precise entries.

🔹 RSI-Based MA: Optionally overlay moving averages onto the RSI, providing additional trend confirmation.

How to Use RSI Signal Pro

1️⃣ Select a mode: Use Simple Mode for frequent alerts or Advanced Mode for refined signals.

2️⃣ Enable RSI-Based MA: Apply SMA, EMA, WMA, or VWMA to smooth RSI fluctuations.

3️⃣ Set alerts: TradingView notifications allow you to react to real-time RSI movements instantly.

4️⃣ Apply to multiple markets: Effective for crypto, forex, stocks, and commodities.

Why Use RSI Signal Pro Instead of Standard RSI?

While RSI Signal Pro maintains the core functionality of the standard RSI, its real-time signal generation allows traders to make faster decisions without the typical delay caused by waiting for candle confirmations. Additionally, the optional momentum filtering and moving average smoothing ensure fewer false signals and better trade accuracy.

RSI Divergence[UgurTash] – Real-Time📈 RSI Divergence – Real-Time, Adaptive, and Intelligent RSI Divergence Detection

🚀 What Does This Indicator Do?

RSI Divergence is a real-time divergence detection tool that helps traders identify bullish and bearish divergences between price and the Relative Strength Index (RSI). Unlike traditional RSI-based indicators, this script offers:

✅ Real-time detection – No need to wait for bar closes or repainting.

✅ Dynamic time-frame adaptation – The script automatically adjusts RSI settings based on the selected chart time frame.

✅ Multi-layered divergence analysis – Supports short-term, medium-term, and long-term divergence detection with an optional all-term mode that dynamically selects the best configuration.

🛠 How Does It Work?

Pivot-Based Divergence Detection:

The script analyzes pivot points on both price and RSI to determine valid divergences.

Bullish divergence occurs when price forms a lower low but RSI trends higher, indicating potential upward momentum.

Bearish divergence occurs when price forms a higher high but RSI trends lower, signaling possible weakness.

Adaptive RSI Calculation:

The RSI length is dynamically adjusted based on the chosen time frame:

Short-Term: RSI (7) for 1-5 min charts.

Medium-Term: RSI (14) for 15-60 min charts.

Long-Term: RSI (28) for 4H+ charts.

In All-Term Mode, the script automatically determines the best RSI length based on the active chart timeframe.

Smart Visualization & Alerts:

Bullish divergences are marked with green lines & labels.

Bearish divergences are highlighted in red.

Users can customize symbol size, divergence labels, and colors.

Instant alerts notify traders as soon as a divergence is detected.

🎯 How to Use This Indicator?

📌 For Trend Reversals: Look for bullish divergences at key support levels and bearish divergences at resistance zones.

📌 For Trend Continuation: Combine divergence signals with moving averages, volume analysis, or price action strategies to confirm trades.

📌 For Scalping & Swing Trading: Adjust the time-frame settings to match your trading style.

🏆 What Makes This Indicator Original?

🔹 Unlike standard RSI divergence indicators, this script features real-time analysis with no repainting, allowing for instant trading decisions.

🔹 The time-frame adaptive RSI makes it dynamic and suitable for any market condition.

🔹 The multi-term divergence detection offers flexibility, giving traders a precise view of both short-term & long-term market structure.

⚠ Note: No indicator guarantees 100% accuracy. Always use additional confirmations and sound risk management strategies.

If you find this tool useful, don’t forget to support & share! 🚀

Dynamic 50% Indicator of the selected range!This is a indicator which shows you the 50% level of the selected timeframe range. This is a good tool because price tends to bounce of of 50% levels.

Introducing the 50% Range Level Indicator, designed for traders who seek accuracy and strategic insights in their market analysis. This tool calculates and visually displays the midpoint (50% level) of any selected price range, helping you identify key equilibrium zones where price action often reacts.

Why Use This Indicator?

Key Market Equilibrium – The 50% level is a crucial reference point where price often consolidates, reverses, or gathers momentum.

Custom Range Selection – Simply select your desired price range, and the indicator will dynamically plot the midpoint.

Enhance Your Trading Strategy – Use it for support & resistance confirmation, retracement analysis, or confluence with other indicators.

Works on All Timeframes & Assets – Suitable for stocks, forex, crypto, and indices.

Gain an Edge in the Market

Whether you’re a day trader, swing trader, or long-term investor, the 50% Range Level Indicator can enhance your technical analysis and decision-making.

Stock ETF Tracker 2.0The Stock Sector ETF tracker with Indicators is a versatile tool designed to track the performance of sector-specific ETFs relative to the current asset. It automatically identifies the sector of the underlying symbol and displays the corresponding ETF’s price action alongside key technical indicators. This helps traders analyze sector trends and correlations in real time.

---

Key Features

Automatic Sector Detection:

Fetches the sector of the current asset (e.g., "Technology" for AAPL).

Maps the sector to a user-defined ETF (default: SPDR sector ETFs) .

Technical Indicators:

Simple Moving Average (SMA): Tracks the ETF’s trend.

Bollinger Bands: Highlights volatility and potential reversals.

Donchian High (52-Week High): Identifies long-term resistance levels.

SPY Regime Filter: Red background color if SP500 is below 200 day SMA.

Customizable Inputs:

Adjust indicator parameters (length, visibility).

Override default ETFs for specific sectors.

Informative Table:

Displays the current sector and ETF symbol in the bottom-right corner.

---

Input Settings

SMA Settings

SMA Length: Period for calculating the Simple Moving Average (default: 200).

Show SMA: Toggle visibility of the SMA line.

Bollinger Bands Settings

BB Length: Period for Bollinger Bands calculation (default: 20).

BB Multiplier: Standard deviation multiplier (default: 2.0).

Show Bollinger Bands: Toggle visibility of the bands.

Donchian High (52-Week High)

Daily High Length: Days used to calculate the high (default: 252, approx. 1 year).

Show High: Toggle visibility of the 52-week high line.

Sector Selections

Customize ETFs for each sector (e.g., replace XLU with another utilities ETF).

---

Example Use Cases

Trend Analysis: Compare a stock’s price action to its sector ETF’s SMA for trend confirmation.

Volatility Signals: Use Bollinger Bands to spot ETF price squeezes or breakouts.

Sector Strength: Monitor if the ETF is approaching its 52-week high to gauge sector momentum.

Enjoy tracking sector trends with ease! 🚀

Killzone Session Lines [odnac]This Pine Script indicator displays vertical lines marking the start of key market sessions, known as Killzones, for both today and yesterday. These lines help traders identify important trading hours for the Asia, Europe, and New York sessions.

Killzone Vertical Lines:

Draws vertical lines for the start of the Asia, Europe, and New York sessions.

Displays lines for both today and the previous day to compare price action across sessions.

Customizable Time Settings:

Users can set the exact start hour and minute for each Killzone.

Time zones adjust automatically based on the chart's time zone.

Visual Customization:

Change the color, width, and style of the vertical lines (solid, dotted, dashed).

Toggle each session's lines individually for a cleaner chart.

Previous Start Lines:

Optional lines for the opening of today, the previous day, and the previous week, providing historical context for support and resistance levels.

Why Use This Indicator?

Session Awareness: Know exactly when major market sessions start to identify potential volatility spikes.

Historical Context: Compare today’s price action with previous sessions to spot recurring patterns.

Clean Charting: Automatic updates prevent clutter, keeping your workspace organized.

Flexible Customization: Tailor the display to fit your trading style and preferences.

Trading Sessions Highs/Lows | InvrsROBINHOODTrading Sessions Highs/Lows | InvrsROBINHOOD

🚀 A powerful indicator for tracking key trading sessions and the highs and lows of each session!

📌 Description

The Trading Sessions Highs/Lows indicator visually marks the most critical trading sessions—Asia, London, and New York—using small colored dots at the bottom of the candle. It also tracks and plots the highs and lows of each session, along with the Daily Open and Weekly Open levels.

This tool is designed to help traders identify session-based liquidity zones, price reactions, and potential trade setups with minimal chart clutter.

Key Features:

✅ Session markers (Asia, London, NY AM, NY Lunch, NY PM) plotted as small dots

✅ Plots session highs and lows for market structure insights

✅ Daily Open line for intraday reference

✅ Weekly Open line for higher timeframe bias

✅ Alerts for session high/low breaks to capture momentum shifts

✅ User-defined UTC offset for global traders

✅ Customizable session colors for personal preference

📖 How to Use the Indicator

1️⃣ Understanding the Sessions

Asia Session (Yellow Dot) → Marks liquidity buildup & pre-London moves

London Session (Blue Dot) → Strong volatility, breakout opportunities

New York AM Session (Green Dot) → Major trends & institutional participation

New York Lunch (Red Dot) → Low volume, ranging market

New York PM Session (Dark Green Dot) → End-of-day movements & reversals

2️⃣ Session Highs & Lows for Market Structure

Session Highs can act as resistance or breakout points.

Session Lows can act as support or stop-hunt zones.

Break of a session high/low with volume may indicate continuation or reversal.

3️⃣ Using the Daily & Weekly Open

The Daily Open (Black Line) helps gauge the intraday trend.

Above Daily Open → Bearish Bias

Below Daily Open → Bullish Bias

The Weekly Open (Red Line) sets the higher timeframe directional bias.

4️⃣ Alerts for Breakouts

The indicator will trigger alerts when price breaks session highs or lows.

Useful for setting stop-losses, breakout trades, and risk management.

💡 Why This Indicator is Important for Beginners

1️⃣ Avoids Overtrading:

Many beginners trade in low-volume periods (NY Lunch, Asia session) and get stuck in choppy price action.

This indicator highlights when volatility is high so traders focus on better opportunities.

2️⃣ Session-Based Liquidity Traps:

Market makers often run stops at session highs/lows before reversing.

Watching session breaks prevents traders from falling into liquidity grabs.

3️⃣ Reduces Emotional Trading:

If price is above the Daily Open, a beginner shouldn’t look for shorts.

If price is below a key session low, it may signal a fake breakout.

4️⃣ Aligns with Institutional Trading:

Smart money traders use session highs/lows to set stop hunts & reversals.

Beginners can use this indicator to spot these zones before entering trades.

🛡️ How to Mitigate Risk with This Indicator

✅ Wait for Confirmations – Don’t trade blindly at session highs/lows. Look for wicks, rejections, or break/retests.

✅ Use Stop-Loss Above/Below Session Levels – If you’re going long, set SL below a session low. If short, set SL above a session high.

✅ Watch Volume & News Events – Breakouts without strong volume or news may be fake moves.

✅ Combine with Other Strategies – Use price action, trendlines, or EMAs with this indicator for higher probability trades.

✅ Use the Weekly Open for Trend Bias – If price stays below the Weekly Open, avoid bullish setups unless key support holds.

🎯 Who is This Indicator For?

📌 Beginners who need clear session-based trading levels.

📌 Day traders & scalpers looking to refine their intraday setups.

📌 Smart money traders using liquidity concepts.

📌 Swing traders tracking higher timeframe momentum shifts.

🚀 Final Thoughts

This indicator is an essential tool for traders who want to understand market structure, liquidity, and volatility cycles. Whether you’re trading forex, stocks, or crypto, it helps you stay on the right side of the market and avoid unnecessary risks.

🔹 Set it up, customize your colors, define your UTC offset, and start trading smarter today! 🏆📈

Cryptolabs Global Liquidity Cycle Momentum IndicatorCryptolabs Global Liquidity Cycle Momentum Indicator (LMI-BTC)

This open-source indicator combines global central bank liquidity data with Bitcoin price movements to identify medium- to long-term market cycles and momentum phases. It is designed for traders who want to incorporate macroeconomic factors into their Bitcoin analysis.

How It Works

The script calculates a Liquidity Index using balance sheet data from four central banks (USA: ECONOMICS:USCBBS, Japan: FRED:JPNASSETS, China: ECONOMICS:CNCBBS, EU: FRED:ECBASSETSW), augmented by the Dollar Index (TVC:DXY) and Chinese 10-year bond yields (TVC:CN10Y). This index is:

- Logarithmically scaled (math.log) to better represent large values like central bank balances and Bitcoin prices.

- Normalized over a 50-period range to balance fluctuations between minimum and maximum values.

- Compared to prior-year values, with the number of bars dynamically adjusted based on the timeframe (e.g., 252 for 1D, 52 for 1W), to compute percentage changes.

The liquidity change is analyzed using a Chande Momentum Oscillator (CMO) (period: 24) to measure momentum trends. A Weighted Moving Average (WMA) (period: 10) acts as a signal line. The Bitcoin price is also plotted logarithmically to highlight parallels with liquidity cycles.

Usage

Traders can use the indicator to:

- Identify global liquidity cycles influencing Bitcoin price trends, such as expansive or restrictive monetary policies.

- Detect momentum phases: Values above 50 suggest overbought conditions, below -50 indicate oversold conditions.

- Anticipate trend reversals by observing CMO crossovers with the signal line.

It performs best on higher timeframes like daily (1D) or weekly (1W) charts. The visualization includes:

- CMO line (green > 50, red < -50, blue neutral), signal line (white), Bitcoin price (gray).

- Horizontal lines at 50, 0, and -50 for improved readability.

Originality

This indicator stands out from other momentum tools like RSI or basic price analysis due to:

- Unique Data Integration: Combines four central bank datasets, DXY, and CN10Y as macroeconomic proxies for Bitcoin.

- Dynamic Prior-Year Analysis: Calculates liquidity changes relative to historical values, adjustable by timeframe.

- Logarithmic Normalization: Enhances visibility of extreme values, critical for cryptocurrencies and macro data.

This combination offers a rare perspective on the interplay between global liquidity and Bitcoin, unavailable in other open-source scripts.

Settings

- CMO Period: Default 24, adjustable for faster/slower signals.

- Signal WMA: Default 10, for smoothing the CMO line.

- Normalization Window: Default 50 periods, customizable.

Users can modify these parameters in the Pine Editor to tailor the indicator to their strategy.

Note

This script is designed for medium- to long-term analysis, not scalping. For optimal results, combine it with additional analyses (e.g., on-chain data, support/resistance levels). It does not guarantee profits but supports informed decisions based on macroeconomic trends.

Data Sources

- Bitcoin: INDEX:BTCUSD

- Liquidity: ECONOMICS:USCBBS, FRED:JPNASSETS, ECONOMICS:CNCBBS, FRED:ECBASSETSW

- Additional: TVC:DXY, TVC:CN10Y

Motivational Text TableRelease Notes - Motivational Text Table Indicator v1.0

Standalone Indicator:

A new, standalone Pine Script v6 indicator that displays a motivational text table directly on the chart.

Customizable Text:

Users can set their own motivational message through the "Custom Motivational Text" input.

Configurable Appearance:

Change the text color and background color of the table.

Adjust the text size by choosing from "tiny", "small", "normal", "large", or "huge".

Select the table’s position on the chart from multiple preset locations (e.g., top_left, middle_center, bottom_right, etc.).

Static Display:

The table is drawn on the last bar, ensuring that the motivational text remains static during realtime updates.

User-Friendly Design:

The interface is simple and easy to customize, making it perfect for users who need a daily dose of motivation directly on their TradingView charts.

Enjoy your motivational boost on every chart!

Time-based Alerts for Trading Windows🌟 Time-based Alerts for Trading Windows 🌐📈

This is a re-uploaded script as the previous one got hidden.

This Time-based Alerts for Trading Windows script is a highly customizable and reliable tool designed to assist traders in managing automated strategies or manually monitoring specific market conditions. Inspired by CrossTrade's Time-based Alert, this script is tailored for those who rely on precise time windows to trigger actions, such as sending webhook signals or managing Expert Advisors (EAs).

Whether you are a scalper, day trader, or algorithmic trader, this script empowers you to stay on top of your trades with fully customizable time-based alerts.

🛠️ Customizable Time Alerts

This indicator allows you to create up to 12 unique time windows by specifying the exact hour and minute for each alert. Each time window corresponds to an individual alert condition, making it perfect for managing trades during specific market sessions or key time periods.

For example:

Alert 1 can be set at 9:30 AM (market open).

Alert 2 can be set at 3:55 PM (just before market close).

Each alert can be toggled on or off in the indicator settings, allowing you to manage alerts without having to reconfigure your script.

You can adjust the colours to fit any colour scheme you like!

🕒 Odd and Even Time Alerts

The script comes with three built-in alert type categories:

Odd Alerts (marked with a green triangle on the chart): These correspond to odd-numbered inputs like Alert 1, Alert 3, Alert 5, and so on.

Even Alerts (marked with a red triangle on the chart): These correspond to even-numbered inputs like Alert 2, Alert 4, Alert 6, and so on.

You can also customize all 12 alerts individually to include a custom alert message

These alerts serve as a convenient way to differentiate between multiple trading strategies or market conditions. You can customize alert messages for odd and even alerts directly from TradingView’s alert panel.

🔗 Webhook Integration for Automation

This script is fully compatible with webhook-based automation. By configuring your alerts in TradingView, you can send signals to trading bots, EAs, or any third-party system. For example, you can:

Turn off an EA at a specific time (e.g., 3:55 PM EST).

Send buy/sell signals to your bot during predefined trading windows.

Simply use TradingView’s alert message editor to format webhook payloads for your automation system.

🌐 Timezone Flexibility

Trading happens across multiple time zones, and this script accounts for that. You can toggle between:

Eastern Time (New York): Ideal for most US-based markets.

Central Time (Exchange): Useful for futures and commodities traders.

This ensures your alerts are always in sync with your preferred time zone, eliminating confusion.

🎨 Visual Indicators

The script plots visual markers directly on your chart to indicate active alerts:

Up Facing Triangles: Represent odd-numbered alerts, providing a quick reference for these time windows.

Down Facing Triangles: Represent even-numbered alerts, helping you track different strategies or conditions.

These visual markers make it easy to see when alerts are triggered, even at a glance.

📈 Practical Use Case

Let’s say you’re trading the USTEC index on a 1-minute chart. You want to:

Turn off your trading bot at 16:55 EST to avoid after-market volatility.

Trigger a re-entry signal at 17:30 EST to capture moves during the Asian session.

Visually monitor these actions on your chart for easy reference.

This script makes it possible with precision alerts and webhook integration. Simply configure the time windows in the settings and set up your alerts in TradingView.

🚨 How to Set Up Alerts

Enable or Disable Alerts: Use the script’s settings to toggle specific alerts on or off as needed.

Set Custom Time Windows: Define the hour and minute for each alert in the settings panel.

Create Alerts in TradingView:

Go to the TradingView alert panel.

Select the condition (e.g., "Odd Time-based Alert (Green)" or "Even Time-based Alert (Red)").

Customize the alert message for webhook integration or personal notification.

Choose the trigger type: Once Per Bar or Once Per Bar Close to keep the alert active.

Integrate with Webhooks: Use the alert message field to format payloads for automation systems like MT4, MT5, or third-party bots.

📋 Key Notes

Alerts can trigger indefinitely if set to "Once Per Bar" or "Once Per Bar Close".

Always ensure the expiration date is set far in the future to avoid unexpected alert deactivation.

Test webhook messages and alert configurations thoroughly before using them in live trading.

This script is a powerful addition to your trading toolbox, offering precision, flexibility, and automation capabilities. Whether you’re turning off an EA, managing trades during market sessions, or automating strategies via webhooks, this script is here to support you.

Start using the Time-based Alerts for Trading Windows today and trade with confidence! 🚀✨

Float Turnover Signal

The *Float Turnover Signal* indicator helps traders analyze the relationship between price changes and trading volume relative to the stock's free float. It generates signals based on turnover ratios, providing insights into liquidity-driven price movements.

**How It Works**

- The indicator calculates the **percentage change** in closing price from two days ago to the previous day.

- It retrieves the **free float** (the number of publicly available shares) from TradingView.

- It then calculates the **turnover percentage**, which represents the previous day's trading volume as a percentage of the free float.

- The **turnover ratio** is derived by dividing the price change percentage by the turnover percentage.

- Based on this ratio, the indicator generates **color-coded signals**:

- 🟢 **Green Signal** – Indicates a balanced turnover ratio (0.8 to 1.2), suggesting a stable price-volume relationship.

- 🟡 **Yellow Signal** – Indicates a near-optimal but not perfect ratio (0.6-0.8 or 1.2-1.5), suggesting caution.

**Customization & Features**

✅ **Adjustable Signal Display** – Users can choose how many recent bars will display signals using the `"Number of Bars to Display Signal"` setting.

✅ **Works on Any Timeframe** – The indicator adapts to different chart resolutions.

✅ **Helps Identify Volume-Driven Moves** – Ideal for spotting potential breakouts, liquidity shifts, and confirming price action validity.

RoGr75 - Global Exchange Open/Close SignalsGlobal Exchange Open/Close Signals Indicator

This indicator helps traders track market hours for major global exchanges (NYSE, LSE, TSE, HKEX, and ASX) with these key features:

• Real-time Status Dashboard: Shows which exchanges are currently open/closed with an easy-to-read color-coded display (Green = Open, Red = Closed)

• Visual Market Open/Close Signals: Displays gradient background lines when your selected exchange opens (green) or closes (red)

• Timezone Adjustment: Easily adapt the indicator to your local timezone using the UTC offset setting

Supported Exchanges and Trading Hours (UTC):

• NYSE: 13:30 - 20:00 (9:30 AM - 4:00 PM ET)

• LSE: 08:00 - 16:30 (8:00 AM - 4:30 PM London)

• TSE: 00:00 - 06:30 (9:00 AM - 3:30 PM Tokyo)

• HKEX: 01:30 - 08:00 (9:30 AM - 4:00 PM HK)

• ASX: 00:00 - 06:00 (10:00 AM - 4:00 PM Sydney)

Settings:

• Select Exchange: Choose which exchange to monitor for open/close signals

• Show Dashboard: Toggle the exchange status dashboard on/off

• User Timezone Offset: Adjust the display to your local timezone (in UTC)

Use Cases:

• Monitor multiple exchange hours simultaneously

• Get visual alerts for market opens and closes

• Coordinate trading across different time zones

• Plan entries and exits around market hours

• Manage global trading portfolios effectively

Note: The indicator handles timezone conversions and markets crossing midnight automatically. Times are based on standard trading sessions and may not reflect holidays or special trading hours.

Bitcoin Log Growth Curve OscillatorThis script presents the oscillator version of the Bitcoin Logarithmic Growth Curve 2024 indicator, offering a new perspective on Bitcoin’s long-term price trajectory.

By transforming the original logarithmic growth curve into an oscillator, this version provides a normalized view of price movements within a fixed range, making it easier to identify overbought and oversold conditions.

For a comprehensive explanation of the mathematical derivation, underlying concepts, and overall development of the Bitcoin Logarithmic Growth Curve, we encourage you to explore our primary script, Bitcoin Logarithmic Growth Curve 2024, available here . This foundational script details the regression-based approach used to model Bitcoin’s long-term price evolution.

Normalization Process

The core principle behind this oscillator lies in the normalization of Bitcoin’s price relative to the upper and lower regression boundaries. By applying Min-Max Normalization, we effectively scale the price into a bounded range, facilitating clearer trend analysis. The normalization follows the formula:

normalized price = (upper regresionline − lower regressionline) / (price − lower regressionline)

This transformation ensures that price movements are always mapped within a fixed range, preventing distortions caused by Bitcoin’s exponential long-term growth. Furthermore, this normalization technique has been applied to each of the confidence interval lines, allowing for a structured and systematic approach to analyzing Bitcoin’s historical and projected price behavior.

By representing the logarithmic growth curve in oscillator form, this indicator helps traders and analysts more effectively gauge Bitcoin’s position within its long-term growth trajectory while identifying potential opportunities based on historical price tendencies.

Buy on VolumeThis script has several weaknesses:

1. **Overly Simplistic Logic** – The buy signal is based on just two conditions (DEMA crossing above a Lorentzian Line and a volume spike), which may not be robust enough for real trading conditions.

2. **Lack of Sell Signals** – The script only focuses on buy signals without any exit strategy, making it incomplete for practical trading.

3. **Volume Confirmation May Be Unreliable** – The threshold for volume confirmation (50% above average) is arbitrary and may produce frequent false positives or fail in low-liquidity conditions.

4. **No Risk Management** – There is no stop-loss, take-profit, or risk-adjustment mechanism, making it unsuitable for serious trading.

5. **Potential for Late Entries** – The reliance on moving averages (DEMA) can introduce lag, causing buy signals to appear late after a price move has already occurred.

6. **Limited Adaptability** – The fixed parameter settings (e.g., DEMA period of 6, Lorentzian length of 21) may not work across different market conditions or assets.

7. **No Consideration for Market Trends** – The script does not account for broader market trends, which could lead to poor entries in bearish conditions.

8. **Visual Clutter** – The plotted signals and indicators might create unnecessary chart noise, making it difficult to analyze price action effectively.

9. **Alert Spam Potential** – Without additional filtering conditions, the script may trigger frequent buy alerts, leading to signal fatigue.

Full Moon and New Moon IndicatorThe Full Moon & New Moon Indicator is a custom Pine Script indicator which marks Full Moon (Pournami) and New Moon (Amavasya) events on the price chart. This indicator helps traders who incorporate lunar cycles into their market analysis, as certain traders believe these cycles influence market sentiment and price action. The current script is added for the year 2024 and 2025 and the dates are considered as per the Telugu calendar.

Features

✅ Identifies and labels Full Moon & New Moon days on the chart for the year 2024 and 2025

How it Works!

On a Full Moon day, it places a yellow label ("Pournami") above the corresponding candle.

On a New Moon day, it places a blue label ("Amavasya") above the corresponding candle.

Example Usage

When a Full Moon label appears, check for potential trend reversals or high volatility.

When a New Moon label appears, watch for market consolidation or a shift in sentiment.

Combine with candlestick patterns, support/resistance, or momentum indicators for a stronger trading setup.

🚀 Add this indicator to your TradingView chart and explore the market’s reaction to lunar cycles! 🌕

US 20Y Treasury YieldWhat This Indicator Does

This Pine Script creates a custom indicator for TradingView that displays the US 20-Year Treasury Yield (US20Y) on your chart. Here's what it does step by step:

1. What Is the US 20-Year Treasury Yield?

The US 20-Year Treasury Yield is a financial metric that shows the interest rate (or yield) investors earn when they buy US government bonds that mature in 20 years. It’s an important indicator of the economy and can influence other markets like stocks, bonds, and currencies.

2. How Does the Indicator Work?

The indicator fetches the latest data for the US 20-Year Treasury Yield from TradingView's database.

It then plots this data in a separate pane below your main chart, so you can easily monitor the yield without cluttering your price chart.

3. What Does the Indicator Show?

A blue line is drawn in the separate pane, showing the movement of the US 20-Year Treasury Yield over time.

A gray dashed line is added at the 4.0% level as a reference point. You can use this line to quickly see when the yield is above or below 4.0%.

5. Why Use This Indicator?

Monitor Economic Trends : The US 20-Year Treasury Yield is a key economic indicator. By plotting it on your chart, you can stay informed about changes in interest rates and their potential impact on other markets.

[COG]StochRSI Zenith📊 StochRSI Zenith

This indicator combines the traditional Stochastic RSI with enhanced visualization features and multi-timeframe analysis capabilities. It's designed to provide traders with a comprehensive view of market conditions through various technical components.

🔑 Key Features:

• Advanced StochRSI Implementation

- Customizable RSI and Stochastic calculation periods

- Multiple moving average type options (SMA, EMA, SMMA, LWMA)

- Adjustable signal line parameters

• Visual Enhancement System

- Dynamic wave effect visualization

- Energy field display for momentum visualization

- Customizable color schemes for bullish and bearish signals

- Adaptive transparency settings

• Multi-Timeframe Analysis

- Higher timeframe confirmation

- Synchronized market structure analysis

- Cross-timeframe signal validation

• Divergence Detection

- Automated bullish and bearish divergence identification

- Customizable lookback period

- Clear visual signals for confirmed divergences

• Signal Generation Framework

- Price action confirmation

- SMA-based trend filtering

- Multiple confirmation levels for reduced noise

- Clear entry signals with customizable display options

📈 Technical Components:

1. Core Oscillator

- Base calculation: 13-period RSI (adjustable)

- Stochastic calculation: 8-period (adjustable)

- Signal lines: 5,3 smoothing (adjustable)

2. Visual Systems

- Wave effect with three layers of visualization

- Energy field display with dynamic intensity

- Reference bands at 20/30/50/70/80 levels

3. Confirmation Mechanisms

- SMA trend filter

- Higher timeframe alignment

- Price action validation

- Divergence confirmation

⚙️ Customization Options:

• Visual Parameters

- Wave effect intensity and speed

- Energy field sensitivity

- Color schemes for bullish/bearish signals

- Signal display preferences

• Technical Parameters

- All core calculation periods

- Moving average types

- Divergence detection settings

- Signal confirmation criteria

• Display Settings

- Chart and indicator signal placement

- SMA line visualization

- Background highlighting options

- Label positioning and size

🔍 Technical Implementation:

The indicator combines several advanced techniques to generate signals. Here are key components with code examples:

1. Core StochRSI Calculation:

// Base RSI calculation

rsi = ta.rsi(close, rsi_length)

// StochRSI transformation

stochRSI = ((ta.highest(rsi, stoch_length) - ta.lowest(rsi, stoch_length)) != 0) ?

(100 * (rsi - ta.lowest(rsi, stoch_length))) /

(ta.highest(rsi, stoch_length) - ta.lowest(rsi, stoch_length)) : 0

2. Signal Generation System:

// Core signal conditions

crossover_buy = crossOver(sk, sd, cross_threshold)

valid_buy_zone = sk < 30 and sd < 30

price_within_sma_bands = close <= sma_high and close >= sma_low

// Enhanced signal generation

if crossover_buy and valid_buy_zone and price_within_sma_bands and htf_allows_long

if is_bullish_candle

long_signal := true

else

awaiting_bull_confirmation := true

3. Multi-Timeframe Analysis:

= request.security(syminfo.tickerid, mtf_period,

)

The HTF filter looks at a higher timeframe (default: 4H) to confirm the trend

It only allows:

Long trades when the higher timeframe is bullish

Short trades when the higher timeframe is bearish

📈 Trading Application Guide:

1. Signal Identification

• Oversold Opportunities (< 30 level)

- Look for bullish crosses of K-line above D-line

- Confirm with higher timeframe alignment

- Wait for price action confirmation (bullish candle)

• Overbought Conditions (> 70 level)

- Watch for bearish crosses of K-line below D-line

- Verify higher timeframe condition

- Confirm with bearish price action

2. Divergence Trading

• Bullish Divergence

- Price makes lower lows while indicator makes higher lows

- Most effective when occurring in oversold territory

- Use with support levels for entry timing

• Bearish Divergence

- Price makes higher highs while indicator shows lower highs

- Most reliable in overbought conditions

- Combine with resistance levels

3. Wave Effect Analysis

• Strong Waves

- Multiple wave lines moving in same direction indicate momentum

- Wider wave spread suggests increased volatility

- Use for trend strength confirmation

• Energy Field

- Higher intensity in trading zones suggests stronger moves

- Use for momentum confirmation

- Watch for energy field convergence with price action

The energy field is like a heat map that shows momentum strength

It gets stronger (more visible) when:

Price is in oversold (<30) or overbought (>70) zones

The indicator lines are moving apart quickly

A strong signal is forming

Think of it as a "strength meter" - the more visible the energy field, the stronger the potential move

4. Risk Management Integration

• Entry Confirmation

- Wait for all signal components to align

- Use higher timeframe for trend direction

- Confirm with price action and SMA positions

• Stop Loss Placement

- Consider placing stops beyond recent swing points

- Use ATR for dynamic stop calculation

- Account for market volatility

5. Position Management

• Partial Profit Taking

- Consider scaling out at overbought/oversold levels

- Use wave effect intensity for exit timing

- Monitor energy field for momentum shifts

• Trade Duration

- Short-term: Use primary signals in trading zones

- Swing trades: Focus on divergence signals

- Position trades: Utilize higher timeframe signals

⚠️ Important Usage Notes:

• Avoid:

- Trading against strong trends

- Relying solely on single signals

- Ignoring higher timeframe context

- Over-leveraging based on signals

Remember: This tool is designed to assist in analysis but should never be used as the sole decision-maker for trades. Always maintain proper risk management and combine with other forms of analysis.

[SHORT ONLY] 10 Bar Low Pullback█ STRATEGY DESCRIPTION

The "10 Bar Low Pullback" strategy is a contrarian short trading system designed to capture pullbacks after a new 10‐bar low is made. it identifies a potential short opportunity when the current bar’s low breaks below the lowest low of the previous 10 bars, provided that the bar exhibits strong internal momentum as measured by its IBS value. An optional trend filter further refines entries by requiring that the close is below a 200-period EMA.

█ WHAT IS INTERNAL BAR STRENGTH (IBS)?

Internal Bar Strength (IBS) measures where the closing price falls within the high-low range of a bar. It is calculated as:

ibs = (close - low) / (high - low)

- Low IBS (≤ 0.2): Indicates the close is near the bar's low, suggesting oversold conditions.

- High IBS (≥ 0.8): Indicates the close is near the bar's high, suggesting overbought conditions.

█ SIGNAL GENERATION

1. SHORT ENTRY

A Short Signal is triggered when:

The current bar’s low is below the lowest low of the past X bars (default: 10).

The bar’s IBS is greater than the specified threshold (default: 0.85).

The signal occurs within the defined trading window (between Start Time and End Time).

If the EMA Filter is enabled, the close must be below the 200-period EMA.

2. EXIT CONDITION

An exit Signal is generated when the current close falls below the previous bar’s low (close < low ), indicating a potential bearish reversal and prompting the strategy to close its short position.

█ ADDITIONAL SETTINGS

Lookback Period: Defines the number of bars (default is 10) over which the lowest low is calculated.

IBS Threshold: Sets the minimum required IBS value (default is 0.85) to qualify as a pullback.

Trading Window: Trades are only executed between the user-defined Start Time and End Time.

EMA Filter (Optional): When enabled, short entries are only considered if the current close is below the 200-period EMA, with the EMA period being adjustable (default is 200).

█ PERFORMANCE OVERVIEW

Designed for shorting opportunities, this strategy aims to capture pullbacks following an aggressive 10-bar low break.

It leverages a combination of a lookback low and IBS measurement to identify overextended bullish moves that may revert.

The optional EMA filter helps confirm a bearish market environment by ensuring the price remains under the trend line.

Suitable for use on various assets, including stocks and ETFs, on daily or similar timeframes.

Backtesting and parameter optimization are recommended to tailor the strategy to specific market conditions.