Choch Pattern Levels [BigBeluga] + AlertsChoch Pattern Levels highlights key structural breaks that can mark the start of new trends. By combining precise break detection with volume analytics and automatic cleanup, it provides actionable insights into the true intent behind price moves — giving traders a clean edge in spotting early reversals and key reaction zones. Added support for alarms.

Cycles

Daily High/Low Close Breakout - GOLD### **Daily High/Low Close Breakout Indicator**

This indicator is a powerful tool for identifying potential breakout opportunities based on the previous day's price action. It's built on a unique time-based logic that defines key support and resistance levels for the trading day.

---

### **How the Indicator Works**

The indicator operates in two main phases:

1. **Calculation Period (00:00 to 16:30 Tehran Time):** The indicator first observes the price action from the start of the day until 16:30. During this time, it records the highest and lowest **closing prices** of all candles. The chart background is shaded gray to visually mark this period.

2. **Trading Period (16:30 to 16:30 the next day):** At 16:30, the highest and lowest close levels are finalized and drawn as horizontal lines. These levels then become the primary breakout zones for the next 24 hours. The indicator will generate signals whenever the price crosses these lines.

---

### **Trading Signals**

The indicator uses a simple and effective crossover logic for its signals:

* **BUY Signal:** A signal is generated when a candle's closing price **crosses above** the high close line.

* **SELL Signal:** A signal is generated when a candle's closing price **crosses below** the low close line.

---

### **Important Usage Guidelines**

For optimal performance, please follow these specific recommendations:

* **Timeframe:** This indicator is designed and optimized to be used exclusively on the **15-minute timeframe**. Using it on other timeframes may produce inconsistent or unreliable results.

* **Primary Asset:** The logic for this indicator was developed and backtested primarily for **Gold (XAUUSD)**. Its performance and win rate have been observed to be the most consistent on this asset.

* **Asset Restriction:** It is strongly recommended to **avoid using this indicator on other currency pairs or assets**, as it has not been optimized for their specific market behavior.

---

### **Disclaimer**

*This indicator is provided for informational and educational purposes only. It is not financial advice. Past performance is not a guarantee of future results. All trading decisions should be based on your own research and risk analysis. Always use proper risk management.*

Market Extension Quantifier SniperIt's a combination of ATR, Moving Average, Bollinger Bands and RSI. And the idea is to find a very extended move which creates a probability that the market is due to a reversion.

Benford's Law Actual [Tagstrading]Benford’s Law Chart — First Digit Analysis of Percentage Price Drops

This script visualizes the distribution of the leading digit in the percentage change of price drops, and compares it to the theoretical distribution expected by Benford’s Law.

It helps traders, analysts, and quants to detect anomalies, unnatural behavior, or price manipulation in any asset or timeframe.

How to Use

Add to any chart or symbol (stocks, crypto, FX, etc.) and select the timeframe you wish to analyze.

Set the “Number of Bars to Analyze” input (default: 500) to control the length of the historical window.

The chart will display, for the latest window:

A blue line: the actual leading-digit distribution for percentage price changes between bars.

A red line: the expected distribution per Benford’s Law.

Labels below and above: digit markers and the expected (theoretical) percentages.

Summary panel on the right: frequency counts and actual vs. theoretical % for each digit.

Interpretation:

If your actual (blue) curve or digit counts are significantly different from the red Benford’s Law curve, it could indicate unnatural price action, fraud, bot activity, or structural anomalies.

Why is this useful for TradingView?

Financial forensics: Benford’s Law is a classic tool for detecting data manipulation and fraud in accounting. On charts, it can reveal if price movements are statistically “natural.”

Transparency and confidence: Helps communities audit markets, brokers, or exchanges for irregularities.

Adaptable: Works on any market, any timeframe.

What makes this script unique?

Focuses on % price changes, not raw prices.

This provides a fair comparison across assets, symbols, and timeframes.

Measures only the direction and magnitude of drops/rises — more suitable for detecting manipulation in active markets.

Clear and customizable visualization:

The Benford line, actual data, and summary are all visible and readable in one glance.

Optimized for speed and clarity (runs efficiently on all major charts).

How is it different from stg44’s Benford’s Law script?

This script analyzes the leading digit of percentage price changes (i.e., how much the price drops or rises in %),

while the original by stg44 analyzes the leading digit of price itself.

Results are less sensitive to price scale and more comparable across volatile and non-volatile assets.

The summary panel clearly shows ( ) for actual and for Benford theoretical values.

Full code is commented and open for the community.

Credits and Inspiration

This script was inspired by “Benford’s Law” by stg44:

Thanks to the TradingView community for sharing powerful visual ideas.

—

By tags trading

RSI Custom ADX VWAP Swing Signals Anmol Singh point.Anmol Singh

This indicator combines RSI, a custom ADX, VWAP, and Swing High/Low Break signals to identify potential buy and sell opportunities. It provides visual signals and alerts, helping traders spot trends and reversals more effectively on NASDAQ 1-minute charts.

Inside Bar With Alert - RajThis indicator helps you reduce your screen time by giving you consistent alerts on the formation of inside bar candle and it gives you bullish and bearish alerts on breakout of the mother candle. So if you believe in inside strategy this indicator will be helpful for you.

Inside Bar Breakout Alert - RajThis indicator is based on the inside bar strategy it help you to cut down your screen time by giving you constant alerts when a inside bar forms while also gives you alert on bullish and bearish break out of the mother candle.

MA Cross 7-21MA Crossover

Definition

This indicator calculates and plots two moving averages, the MA7 and MA21, and highlights candlesticks where they cross. It indicates when a trend is changing, becoming weaker or stronger, in the short term.

Summary

The Moving Average Crossover indicator sounds simple enough. It measures two moving averages and detects when they cross. The two moving averages measured are the MA7 and MA21. A crossover indicates that the MA7 is now above the MA21, and vice versa. This indicator can be used in conjunction with other moving averages or trend-following indicators to better understand momentum.

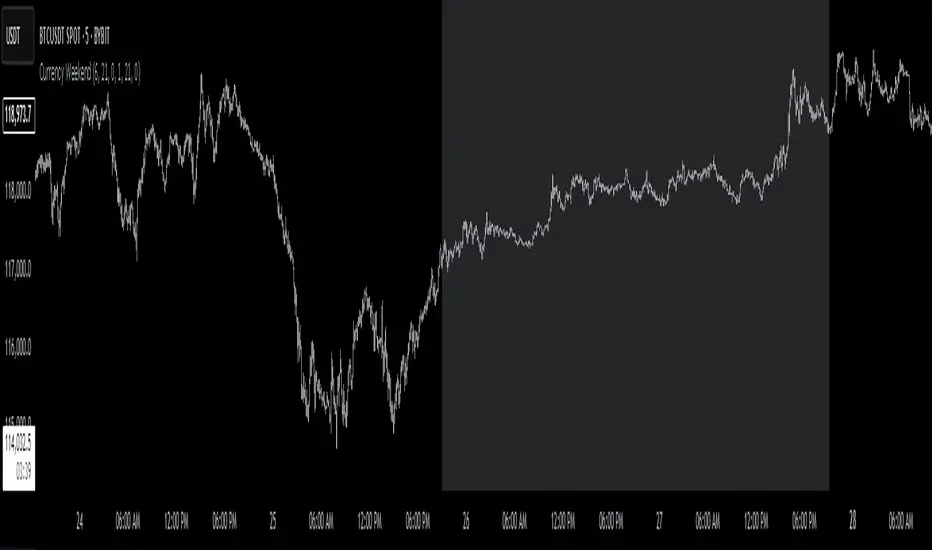

Currency Weekend - shading weekend trading// ─────────────────────────────────────────────────────────────────────────────

// © 2025, Steve / Steven Anthony – "Currency Weekend"

// This script highlights the low-liquidity weekend window that often affects

// both fiat currency markets and cryptocurrencies like Bitcoin.

//

// ╭─────────────────────────────── DESCRIPTION ───────────────────────────────╮

// | This indicator shades a customizable time window on your chart, |

// | originally set to highlight the **forex weekend lull** from |

// | **Friday 21:00 UTC to Sunday 21:00 UTC**, when traditional fiat |

// | currency markets close. |

// | |

// | Traders who observe Bitcoin, Ethereum, or other crypto assets may |

// | notice reduced liquidity or increased erratic moves during this time, |

// | due to overlapping behaviors from professional forex traders who |

// | trade both markets. |

// ╰──────────────────────────────────────────────────────────────────────────╯

//

// 🔧 Flexible Configuration:

// - Define your own start and end **day + time** for shading

// - Useful for shading other custom quiet periods or session transitions

//

// 💡 Use Cases:

// - Avoid trading during low-liquidity periods

// - Spot potential weekend traps or price gaps

// - Align crypto behavior with fiat market hours

//

// 📍 Default Settings:

// - Start: Friday 21:00 UTC

// - End: Sunday 21:00 UTC

//

// Timezone is normalized to the chart’s timezone for seamless integration.

//

// ─────────────────────────────────────────────────────────────────────────────

India Session 06:30–21:30 [IST] (Custom)this indicator is made specially for indian traders whos trading 9 to 9 . theth the can backtest thair strategys on this time frame.

WRX.v2 | Option Resonance + Charm TrackerINSPIRED by RIPSTER

Charm tracker

Options use only

Charm vomma

Ichimoku Trend CycleIchimoku Trend Cycle

A precision dual-trend system combining Ichimoku-based ATR Supertrends — engineered for clarity, reliability, and smart trend detection.

🔷 What is Ichimoku Trend Cycle?

The Ichimoku Trend Cycle harnesses the power of traditional Ichimoku analysis with modern ATR-based supertrend technology:

Alpha Trend: Primary trend detection using Ichimoku conversion & baseline logic

Beta Trend: Secondary confirmation trend with independent ATR calculations

Dual Confirmation Engine : Both trends must align for signal generation

This powerful combination delivers clean, non-repainting Buy/Sell signals while filtering out market noise and false breakouts.

🔍 How It Works

Blue Alpha + Red Beta Trends Align Bullish → BUY Signal

Both Trends Turn Bearish → SELL Signal

You get ONE signal per trend change — no spam, no noise, just crystal-clear direction changes.

⚙️ Core Features

✅ Ichimoku-Enhanced Supertrends

Traditional Ichimoku conversion/baseline logic powering modern ATR bands.

✅ Dual-Trend Confirmation

Alpha and Beta trends must agree — eliminates false signals.

✅ One Alert Per Trend Shift

Clean entries, zero noise, no repeated signals.

✅ Visual Excellence

Color-coded trend lines with high-contrast BUY/SELL labels.

✅ Fully Customizable

Independent settings for both trend systems plus smoothing options.

🎯 Perfect For

Swing Traders wanting confirmed trend changes

Position Traders seeking major trend shifts

Anyone who values clean charts with sharp decision points

🛠 Settings Breakdown

Alpha Trend Settings: Primary trend with conversion/baseline periods + ATR multiplier

Beta Trend Settings: Secondary confirmation trend with independent parameters

Smoothing MA Settings: Optional MA smoothing with Bollinger Bands support

Alert Settings: Customize signal confirmation periods

Candle Color Settings: Fully customizable trend and candle color schemes

✅ Built-in Smart Alerts — Never miss a trend change again

⚡ Zero-lag Performance — Works flawlessly across all timeframes

📈 Strategy-Ready Code — Professional-grade, non-repainting signals

Transform your trading with the precision of Ichimoku and the reliability of dual-trend confirmation.

SMA50 - Relleno + AlertasThis is about the 50 SMA and its relationship to price. When the price is above the 50 SMA, it is colored green, indicating a bullish trend. If the price is below the 50 SMA, it is colored red, indicating a bearish trend. It also has alerts when the trend crosses the 50 SMA.

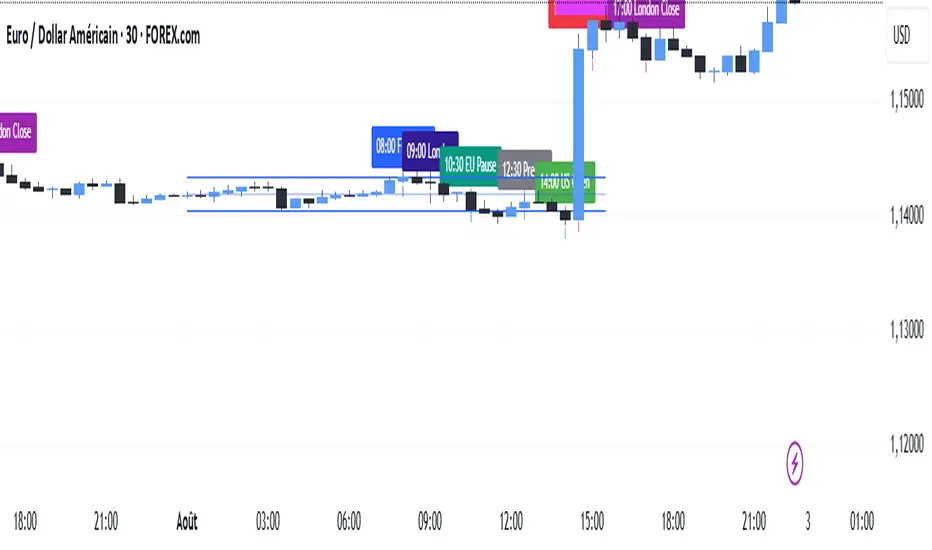

SMC TimingThis indicator (“SMC Timing”) visually marks the exact moments when the market typically experiences large liquidity injections—moments that often trigger strong directional moves. By plotting dashed vertical lines and labels at key session boundaries and news events (Frankfurt open, London open, EU mid-session pause, Pre-US, US open, 14:30 U.S. news releases, 15:00 breakout window, and the London close), it draws your attention to the times when stop-runs and institutional orders tend to pile into the market.

Traders can use these timing zones to:

Anticipate liquidity sweeps where smart-money often liquidates weak positions or hunts stops.

Plan higher-probability entries just before or directly after these injections, reducing slippage and improving execution.

Improve win-rate consistency by aligning your trades with the natural ebb and flow of institutional flow rather than fading it.

With customizable session toggles, a “today-only” filter, and a small vertical offset to keep markers clear of price bars, this tool seamlessly integrates into any chart. Positioning yourself around these highlighted times helps you capture the bulk of intraday moves and avoids getting caught in low-liquidity chop.

Entry HelperEntry Helper is a precision tool designed to enhance clarity and support decision-making in fast-paced trading environments.

It adapts intelligently to different timeframes, offering visual guidance based on your chosen context — without the need to manually adjust settings.

Specially optimized for scalping assets like XAUUSD, NASDAQ, and SP500, it delivers exactly what you need, when you need it.

⚡ Just switch the chart… and it adjusts itself.

Developed by WAKEUP | Maggifx

Mara JPY Strength (USDJPY+EURJPY+GBPJPY)/3 + DXYJPY, USDJPY, EURJPY, GBPJPY, smart money, bias, index, forex indicator, DXY, strength meter, professional, trading tool, price action

✅ BACKTEST: UT Bot + RSIRSI levels widened (60/40) — more signals.

Removed ATR volatility filter (to let trades fire).

Added inputs for TP and SL using ATR — fully dynamic.

Cleaned up conditions to ensure alignment with market structure.

Ratio-Adjusted McClellan Summation Index RASI NASIRatio-Adjusted McClellan Summation Index (RASI NASI)

In Book "The Complete Guide to Market Breadth Indicators" Author Gregory L. Morris states

"It is the author’s opinion that the McClellan indicators, and in particular, the McClellan Summation Index, is the single best breadth indicator available. If you had to pick just one, this would be it."

What It Does: The Ratio-Adjusted McClellan Summation Index (RASI) is a market breadth indicator that tracks the cumulative strength of advancing versus declining issues for a user-selected exchange (NASDAQ, NYSE, or AMEX). Derived from the McClellan Oscillator, it calculates ratio-adjusted net advances, applies 19-day and 39-day EMAs, and sums the oscillator values to produce the RASI. This indicator helps traders assess market health, identify bullish or bearish trends, and detect potential reversals through divergences.

Key features:

Exchange Selection : Choose NASDAQ (USI:ADVN.NQ, USI:DECL.NQ), NYSE (USI:ADVN.NY, USI:DECL.NY), or AMEX (USI:ADVN.AM, USI:DECL.AM) data.

Trend-Based Coloring : RASI line displays user-defined colors (default: black for uptrend, red for downtrend) based on its direction.

Customizable Moving Average: Add a moving average (SMA, EMA, WMA, VWMA, or RMA) with user-defined length and color (default: EMA, 21, green).

Neutral Line at Zero: Marks the neutral level for trend interpretation.

Alerts: Six custom alert conditions for trend changes, MA crosses, and zero-line crosses.

How to Use

Add to Chart: Apply the indicator to any TradingView chart. Ensure access to advancing and declining issues data for the selected exchange.

Select Exchange: Choose NASDAQ, NYSE, or AMEX in the input settings.

Customize Settings: Adjust EMA lengths, RASI colors, MA type, length, and color to match your trading style.

Interpret the Indicator :

RASI Line: Black (default) indicates an uptrend (RASI rising); red indicates a downtrend (RASI falling).

Above Zero: Suggests bullish market breadth (more advancing issues).

Below Zero : Indicates bearish breadth (more declining issues).

MA Crosses: RASI crossing above its MA signals bullish momentum; crossing below signals bearish momentum.

Divergences: Compare RASI with the market index (e.g., NASDAQ Composite) to identify potential reversals.

Large Moves : A +3,600-point move from a low (e.g., -1,550 to +1,950) may signal a significant bull run.

Set Alerts:

Add the indicator to your chart, open the TradingView alert panel, and select from six conditions (see Alerts section).

Configure notifications (e.g., email, webhook, or popup) for each condition.

Settings

Market Selection:

Exchange: Select NASDAQ, NYSE, or AMEX for advancing/declining issues data.

EMA Settings:

19-day EMA Length: Period for the shorter EMA (default: 19).

39-day EMA Length: Period for the longer EMA (default: 39).

RASI Settings:

RASI Uptrend Color: Color for rising RASI (default: black).

RASI Downtrend Color: Color for falling RASI (default: red).

RASI MA Settings:

MA Type: Choose SMA, EMA, WMA, VWMA, or RMA (default: EMA).

MA Length: Set the MA period (default: 21).

MA Color: Color for the MA line (default: green).

Alerts

The indicator uses alertcondition() to create custom alerts. Available conditions:

RASI Trend Up: RASI starts rising (based on RASI > previous RASI, shown as black line).

RASI Trend Down: RASI starts falling (based on RASI ≤ previous RASI, shown as red line).

RASI Above MA: RASI crosses above its moving average.

RASI Below MA: RASI crosses below its moving average.

RASI Bullish: RASI crosses above zero (bullish market breadth).

RASI Bearish: RASI crosses below zero (bearish market breadth).

To set alerts, add the indicator to your chart, open the TradingView alert panel, and select the desired condition.

Notes

Data Requirements: Requires access to advancing/declining issues data (e.g., USI:ADVN.NQ, USI:DECL.NQ for NASDAQ). Some symbols may require a TradingView premium subscription.

Limitations: RASI is a medium- to long-term indicator and may lag in volatile or range-bound markets. Use alongside other technical tools for confirmation.

Data Reliability : Verify the selected exchange’s data accuracy, as inconsistencies can affect results.

Debugging: If no data appears, check symbol validity (e.g., try $ADVN/Q, $DECN/Q for NASDAQ) or contact TradingView support.

Credits

Based on the Ratio-Adjusted McClellan Summation Index methodology by McClellan Financial Publications. No external code was used; the implementation is original, inspired by standard market breadth concepts.

Disclaimer

This indicator is for informational purposes only and does not constitute financial advice. Past performance is not indicative of future results. Conduct your own research and combine with other tools for informed trading decisions.

Patrón Mecha ProfundaThis pattern must be combined with a 20-period moving average. It is used to know the direction of the price. When the pattern appears and the price is above the 20-period moving average, it is a bullish signal and vice versa.

Peak & Valley Screener RadarThis Pine Script indicator is designed to help traders and investors analyze the percentage distance of stock prices from their recent All-Time High (ATH) and All-Time Low (ALH) over a user-defined number of bars.

It functions as a multi-stock screener, scanning a customizable list of stocks (default: 40 BIST 500 stocks) and displaying results in a dynamic table on the chart.

The script identifies stocks that have pulled back more than a specified percentage from their ATH (potential buying opportunities) or risen less than a specified percentage from their ALH (potential caution zones).

Key Features:

Customizable Stock List: Users can input a comma-separated list of stock tickers (e.g., "AAPL,GOOGL,MSFT") to scan any symbols available on TradingView.

User-Defined Parameters: Adjust the lookback period (bars back, default 250), ATH pullback threshold (default 10%), and ALH rise threshold (default 10%).

Dynamic Table Display: Results are shown in a table with two columns: "Distance to TOP" (ATH pullbacks in red) and "Distance to BOTTOM" (ALH rises in green). The table includes input parameters for quick reference and can be positioned anywhere on the chart (top/bottom left/center/right).

Optional Plots: Toggle plots to visualize the percentage distances for the current chart symbol (red for ATH, green for ALH).

Efficient Data Handling: Uses request.security with tuples for optimized multi-symbol data fetching, supporting up to ~80 stocks without exceeding Pine Script limits (adjust table rows if needed for more).

Real-Time Updates: The table updates only on the last bar for performance efficiency.

How It Works:

The script calculates the highest high and lowest low over the specified bars for each stock.

It computes the percentage difference from the current close: negative for ATH (pullback) and positive for ALH (rise).

Stocks meeting the thresholds are listed in the table with their exact percentages.

Usage Tips:

Apply this indicator to any chart (e.g., a BIST index or stock) to run the screener in the background.

Ideal for swing traders scanning for undervalued stocks near ATH or overbought near ALH.

Note: Performance may vary with large stock lists due to TradingView's security call limits (~40-50 calls per script). Test with smaller lists if needed.

You can bypass the 40-stock limit by adding the indicator twice to the chart, entering 40 different stocks in the second indicator and setting a different table position from the first one, allowing you to scan 80 stocks simultaneously. In fact, this way, you can scan as many stocks as your plan's limits allow.

This script is released under the Mozilla Public License 2.0. Feedback and suggestions are welcome, but please adhere to TradingView's House Rules—no guarantees of profitability, use at your own risk.Disclaimer: This is not financial advice. Past performance does not predict future results. Always conduct your own research.

Patrón Mecha Profunda

This pattern must be combined with a 20-period moving average. It is used to know the direction of the price. When the pattern appears and the price is above the 20-period moving average, it is a bullish signal and vice versa.