[SHORT ONLY] ATR Sell the Rip Mean Reversion Strategy█ STRATEGY DESCRIPTION

The "ATR Sell the Rip Mean Reversion Strategy" is a contrarian system that targets overextended price moves on stocks and ETFs. It calculates an ATR‐based trigger level to identify shorting opportunities. When the current close exceeds this smoothed ATR trigger, and if the close is below a 200-period EMA (if enabled), the strategy initiates a short entry, aiming to profit from an anticipated corrective pullback.

█ HOW IS THE ATR SIGNAL BAND CALCULATED?

This strategy computes an ATR-based signal trigger as follows:

Calculate the ATR

The strategy computes the Average True Range (ATR) using a configurable period provided by the user:

atrValue = ta.atr(atrPeriod)

Determine the Threshold

Multiply the ATR by a predefined multiplier and add it to the current close:

atrThreshold = close + atrValue * atrMultInput

Smooth the Threshold

Apply a Simple Moving Average over a specified period to smooth out the threshold, reducing noise:

signalTrigger = ta.sma(atrThreshold, smoothPeriodInput)

█ SIGNAL GENERATION

1. SHORT ENTRY

A Short Signal is triggered when:

The current close is above the smoothed ATR signal trigger.

The trade occurs within the specified trading window (between Start Time and End Time).

If the EMA filter is enabled, the close must also be below the 200-period EMA.

2. EXIT CONDITION

An exit Signal is generated when the current close falls below the previous bar’s low (close < low ), indicating a potential bearish reversal and prompting the strategy to close its short position.

█ ADDITIONAL SETTINGS

ATR Period: The period used to calculate the ATR, allowing for adaptability to different volatility conditions (default is 20).

ATR Multiplier: The multiplier applied to the ATR to determine the raw threshold (default is 1.0).

Smoothing Period: The period over which the raw ATR threshold is smoothed using an SMA (default is 10).

Start Time and End Time: Defines the time window during which trades are allowed.

EMA Filter (Optional): When enabled, short entries are only executed if the current close is below the 200-period EMA, confirming a bearish trend.

█ PERFORMANCE OVERVIEW

This strategy is designed for use on the Daily timeframe, targeting stocks and ETFs by capitalizing on overextended price moves.

It utilizes a dynamic, ATR-based trigger to identify when prices have potentially peaked, setting the stage for a mean reversion short entry.

The optional EMA filter helps align trades with broader market trends, potentially reducing false signals.

Backtesting is recommended to fine-tune the ATR multiplier, smoothing period, and EMA settings to match the volatility and behavior of specific markets.

Cycles

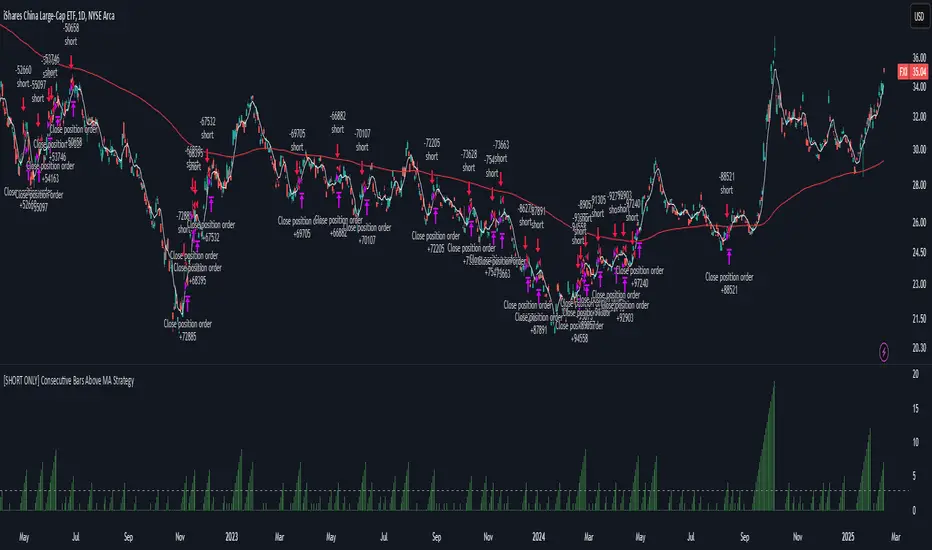

[SHORT ONLY] Consecutive Bars Above MA Strategy█ STRATEGY DESCRIPTION

The "Consecutive Bars Above MA Strategy" is a contrarian trading system aimed at exploiting overextended bullish moves in stocks and ETFs. It monitors the number of consecutive bars that close above a chosen short-term moving average (which can be either a Simple Moving Average or an Exponential Moving Average). Once the count reaches a preset threshold and the current bar’s close exceeds the previous bar’s high within a designated trading window, a short entry is initiated. An optional EMA filter further refines entries by requiring that the current close is below the 200-period EMA, helping to ensure that trades are taken in a bearish environment.

█ HOW ARE THE CONSECUTIVE BULLISH COUNTS CALCULATED?

The strategy utilizes a counter variable, `bullCount`, to track consecutive bullish bars based on their relation to the short-term moving average. Here’s how the count is determined:

Initialize the Counter

The counter is initialized at the start:

var int bullCount = na

Bullish Bar Detection

For each bar, if the close is above the selected moving average (either SMA or EMA, based on user input), the counter is incremented:

bullCount := close > signalMa ? (na(bullCount) ? 1 : bullCount + 1) : 0

Reset on Non-Bullish Condition

If the close does not exceed the moving average, the counter resets to zero, indicating a break in the consecutive bullish streak.

█ SIGNAL GENERATION

1. SHORT ENTRY

A short signal is generated when:

The number of consecutive bullish bars (i.e., bars closing above the short-term MA) meets or exceeds the defined threshold (default: 3).

The current bar’s close is higher than the previous bar’s high.

The signal occurs within the specified trading window (between Start Time and End Time).

Additionally, if the EMA filter is enabled, the entry is only executed when the current close is below the 200-period EMA.

2. EXIT CONDITION

An exit signal is triggered when the current close falls below the previous bar’s low, prompting the strategy to close the short position.

█ ADDITIONAL SETTINGS

Threshold: The number of consecutive bullish bars required to trigger a short entry (default is 3).

Trading Window: The Start Time and End Time inputs define when the strategy is active.

Moving Average Settings: Choose between SMA and EMA, and set the MA length (default is 5), which is used to assess each bar’s bullish condition.

EMA Filter (Optional): When enabled, this filter requires that the current close is below the 200-period EMA, supporting entries in a downtrend.

█ PERFORMANCE OVERVIEW

This strategy is designed for stocks and ETFs and can be applied across various timeframes.

It seeks to capture mean reversion by shorting after a series of bullish bars suggests an overextended move.

The approach employs a contrarian short entry by waiting for a breakout (close > previous high) following consecutive bullish bars.

The adjustable moving average settings and optional EMA filter allow for further optimization based on market conditions.

Comprehensive backtesting is recommended to fine-tune the threshold, moving average parameters, and filter settings for optimal performance.

[SHORT ONLY] Consecutive Close>High[1] Mean Reversion Strategy█ STRATEGY DESCRIPTION

The "Consecutive Close > High " Mean Reversion Strategy is a contrarian daily trading system for stocks and ETFs. It identifies potential shorting opportunities by counting consecutive days where the closing price exceeds the previous day's high. When this consecutive day count reaches a predetermined threshold, and if the close is below a 200-period EMA (if enabled), a short entry is triggered, anticipating a corrective pullback.

█ HOW ARE THE CONSECUTIVE BULLISH COUNTS CALCULATED?

The strategy uses a counter variable called `bullCount` to track how many consecutive bars meet a bullish condition. Here’s a breakdown of the process:

Initialize the Counter

var int bullCount = 0

Bullish Bar Detection

Every time the close exceeds the previous bar's high, increment the counter:

if close > high

bullCount += 1

Reset on Bearish Bar

When there is a clear bearish reversal, the counter is reset to zero:

if close < low

bullCount := 0

█ SIGNAL GENERATION

1. SHORT ENTRY

A Short Signal is triggered when:

The count of consecutive bullish closes (where close > high ) reaches or exceeds the defined threshold (default: 3).

The signal occurs within the specified trading window (between Start Time and End Time).

2. EXIT CONDITION

An exit Signal is generated when the current close falls below the previous bar’s low (close < low ), prompting the strategy to exit the position.

█ ADDITIONAL SETTINGS

Threshold: The number of consecutive bullish closes required to trigger a short entry (default is 3).

Start Time and End Time: The time window during which the strategy is allowed to execute trades.

EMA Filter (Optional): When enabled, short entries are only triggered if the current close is below the 200-period EMA.

█ PERFORMANCE OVERVIEW

This strategy is designed for Stocks and ETFs on the Daily timeframe and targets overextended bullish moves.

It aims to capture mean reversion by entering short after a series of consecutive bullish closes.

Further optimization is possible with additional filters (e.g., EMA, volume, or volatility).

Backtesting should be used to fine-tune the threshold and filter settings for specific market conditions.

[SHORT ONLY] Internal Bar Strength (IBS) Mean Reversion Strategy█ STRATEGY DESCRIPTION

The "Internal Bar Strength (IBS) Strategy" is a mean-reversion strategy designed to identify trading opportunities based on the closing price's position within the daily price range. It enters a short position when the IBS indicates overbought conditions and exits when the IBS reaches oversold levels. This strategy is Short-Only and was designed to be used on the Daily timeframe for Stocks and ETFs.

█ WHAT IS INTERNAL BAR STRENGTH (IBS)?

Internal Bar Strength (IBS) measures where the closing price falls within the high-low range of a bar. It is calculated as:

IBS = (Close - Low) / (High - Low)

- Low IBS (≤ 0.2) : Indicates the close is near the bar's low, suggesting oversold conditions.

- High IBS (≥ 0.8) : Indicates the close is near the bar's high, suggesting overbought conditions.

█ SIGNAL GENERATION

1. SHORT ENTRY

A Short Signal is triggered when:

The IBS value rises to or above the Upper Threshold (default: 0.9).

The Closing price is greater than the previous bars High (close>high ).

The signal occurs within the specified time window (between `Start Time` and `End Time`).

2. EXIT CONDITION

An exit Signal is generated when the IBS value drops to or below the Lower Threshold (default: 0.3). This prompts the strategy to exit the position.

█ ADDITIONAL SETTINGS

Upper Threshold: The IBS level at which the strategy enters trades. Default is 0.9.

Lower Threshold: The IBS level at which the strategy exits short positions. Default is 0.3.

Start Time and End Time: The time window during which the strategy is allowed to execute trades.

█ PERFORMANCE OVERVIEW

This strategy is designed for Stocks and ETFs markets and performs best when prices frequently revert to the mean.

The strategy can be optimized further using additional conditions such as using volume or volatility filters.

It is sensitive to extreme IBS values, which help identify potential reversals.

Backtesting results should be analyzed to optimize the Upper/Lower Thresholds for specific instruments and market conditions.

IPO Date ScreenerThis script, the IPO Date Screener, allows traders to visually identify stocks that are relatively new, based on the number of bars (days) since their IPO. The user can set a custom threshold for the number of days (bars) after the IPO, and the script will highlight new stocks that fall below that threshold.

Key Features:

Customizable IPO Days Threshold: Set the threshold for considering a stock as "new." Since Pine screener limits number bars to 500, it will work for stocks having trading days below 500 since IPO which almost 2 years.

Column Days since IPO: Sort this column from low to high to see newest to oldest STOCK with 500 days of trading.

Since a watchlist is limited to 1000 stocks, use this pines script to screen stocks within the watch list having trading days below 500 or user can select lower number of days from settings.

This is not helpful to add on chart, this is to use on pine screener as utility.

2xSPYTIPS Strategy by Fra public versionThis is a test strategy with S&P500, open source so everyone can suggest everything, I'm open to any advice.

Rules of the "2xSPYTIPS" Strategy :

This trading strategy is designed to operate on the S&P 500 index and the TIPS ETF. Here’s how it works:

1. Buy Conditions ("BUY"):

- The S&P 500 must be above its **200-day simple moving average (SMA 200)**.

- This condition is checked at the **end of each month**.

2. Position Management:

- If leverage is enabled (**2x leverage**), the purchase quantity is increased based on a configurable percentage.

3. Take Profit:

- A **Take Profit** is set at a fixed percentage above the entry price.

4. Visualization & Alerts:

- The **SMA 200** for both S&P 500 and TIPS is plotted on the chart.

- A **BUY signal** appears visually and an alert is triggered.

What This Strategy Does NOT Do

- It does not use a **Stop Loss** or **Trailing Stop**.

- It does not directly manage position exits except through Take Profit.

Blockchain Fundamentals: Liquidity Cycle MomentumLiquidity Cycle Momentum Indicator

Overview:

This indicator analyzes global liquidity trends by calculating a unique Liquidity Index and measuring its year-over-year (YoY) percentage change. It then applies a momentum oscillator to the YoY change, providing insights into the cyclical momentum of liquidity. The indicator incorporates a limited historical data workaround to ensure accurate calculations even when the chart’s history is short.

Features Breakdown:

1. Limited Historical Data Workaround

Function: The limit(length) function adjusts the lookback period when there isn’t enough historical data (i.e., near the beginning of the chart), ensuring that calculations do not break due to insufficient data.

2. Global Liquidity Calculation

Data Sources:

TVC:CN10Y (10-year yield from China)

TVC:DXY (US Dollar Index)

ECONOMICS:USCBBS (US Central Bank Balance Sheet)

FRED:JPNASSETS (Japanese assets)

ECONOMICS:CNCBBS (Chinese Central Bank Balance Sheet)

FRED:ECBASSETSW (ECB assets)

Calculation Methodology:

A ratio is computed (cn10y / dxy) to adjust for currency influences.

The Liquidity Index is then derived by multiplying this ratio with the sum of the other liquidity components.

3. Year-over-Year (YoY) Percent Change

Computation:

The indicator determines the number of bars that approximately represent one year.

It then compares the current Liquidity Index to its value one year ago, calculating the YoY percentage change.

4. Momentum Oscillator on YoY Change

Oscillator Components:

1. Calculated using the Chande Momentum Oscillator (CMO) applied to the YoY percent change with a user-defined momentum length.

2. A weighted moving average (WMA) that smooths the momentum signal.

3. Overbought and Oversold zones

Signal Generation:

Buy Signal: Triggered when the momentum crosses upward from an oversold condition, suggesting a potential upward shift in liquidity momentum.

Sell Signal: Triggered when crosses below an overbought condition, indicating potential downward momentum.

State Management:

The indicator maintains a state variable to avoid repeated signals, ensuring that a new buy or sell signal is only generated when there’s a clear change in momentum.

5. Visual Presentation and Alerts

Plots:

The oscillator value and signalline are plotted for visual analysis.

Overbought and oversold levels are marked with dashed horizontal lines.

Signal Markers:

Buy and sell signals are marked with green and maroon circles, respectively.

Background Coloration:

Optionally, the chart’s background bars are colored (yellow for buy signals and fuchsia for sell signals) to enhance visual cues when signals are triggered.

Conclusion

In summary, the Liquidity Cycle Momentum Indicator provides a robust framework to analyze liquidity trends by combining global liquidity data, YoY changes, and momentum oscillation. This makes it an effective tool for traders and analysts looking to identify cyclical shifts in liquidity conditions and potential turning points in the market.

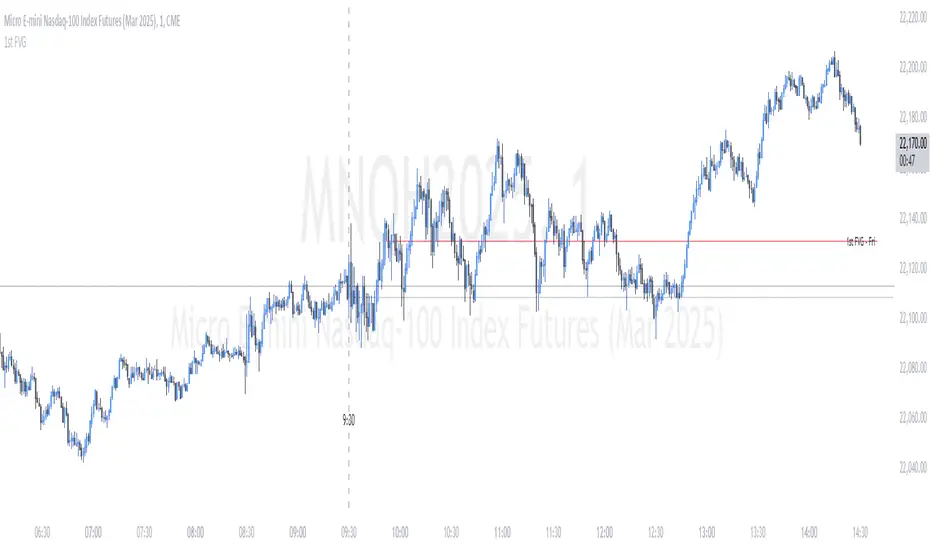

ICT First Presented FVG - NY Open [LuckyAlgo]

This indicator identifies the first Fair Value Gap (FVG) that occurs during the New York trading session, combined with NY session opening price levels. It's an essential tool for traders who follow ICT concepts and focus on the NY trading session.

ICT refers to this as the First Presented FVG, while other traders may call it the 9:30 FVG.

This indicator is best for the 1 minute timeframe, while 5 minute also works.

Detects and marks the first FVG of the NY session

Displays both bullish (green) and bearish (red) FVGs with customizable transparency

Shows the NY session opening price with clear labels

Includes optional vertical line at 9:30 AM NY open

Maintains clean chart visibility with adjustable maximum display days

Includes session date and time labels for easy reference

The indicator helps traders identify potential reversal zones and continuation opportunities by combining two powerful concepts: Fair Value Gaps and NY session opening price. This makes it particularly valuable for day traders and swing traders who want to capitalize on institutional order flow patterns during the most liquid trading session.

You can customize the indicator's appearance, including FVG box colors, time range display, and whether to show the NY open markers. This flexibility allows you to integrate it seamlessly with your existing trading setup.

Correlated asset and Daye's Quarterly TheoryThis indicator is based on the Quarterly Theory concepts from Daye. You can find him mainly on X as traderdaye.

It works on a new panel and the quarters will be drawn over the chart of the correlated that you set on its settings.

You can use every asset to compare with the main one to make easier to find divergences between days, sessions and 90 minutes cycles.

In different timeframes, the indicator could show more or less information about quarters, but will always show the compared asset one. This is due to limitations of the candles start (for example, the Session's Q2 open won't be shown on an hourly chart because it starts after 30 minutes of candle's open).

What can this indicator do for you?

- Show the correlated asset chart.

- Show daily, session and 90 minutes cycle boxes.

- Show Midnight and every session's Q2 open.

- Make easier for the trained eye to determine if the model is AMDX or XAMD, find PO3, turtle soups, SMT divergences, etc.

Do you have any suggestion? Please, leave it on the comments. I'll try to improve this indicator regularly.

Smart Trend Tracker Name: Smart Trend Tracker

Description:

The Smart Trend Tracker indicator is designed to analyze market cycles and identify key trend reversal points. It automatically marks support and resistance levels based on price dynamics, helping traders better navigate market structure.

Application:

Trend Analysis: The indicator helps determine when a trend may be nearing a reversal, which is useful for making entry or exit decisions.

Support and Resistance Levels: Automatically marks key levels, simplifying chart analysis.

Reversal Signals: Provides visual signals for potential reversal points, which can be used for counter-trend trading strategies.

How It Works:

Candlestick Sequence Analysis: The indicator tracks the number of consecutive candles in one direction (up or down). If the price continues to move N bars in a row in one direction, the system records this as an impulse phase.

Trend Exhaustion Detection: After a series of directional bars, the market may reach an overbought or oversold point. If the price continues to move in the same direction but with weakening momentum, the indicator records a possible trend slowdown.

Chart Display: The indicator marks potential reversal points with numbers or special markers. It can also display support and resistance levels based on key cycle points.

Settings:

Cycle Length: The number of bars after which the possibility of a reversal is assessed.

Trend Sensitivity: A parameter that adjusts sensitivity to trend movements.

Dynamic Levels: Setting for displaying key levels.

Название: Smart Trend Tracker

Описание:

Индикатор Smart Trend Tracker предназначен для анализа рыночных циклов и выявления ключевых точек разворота тренда. Он автоматически размечает уровни поддержки и сопротивления, основываясь на динамике цены, что помогает трейдерам лучше ориентироваться в структуре рынка.

Применение:

Анализ трендов: Индикатор помогает определить моменты, когда тренд может быть близок к развороту, что полезно для принятия решений о входе или выходе из позиции.

Определение уровней поддержки и сопротивления: Автоматически размечает ключевые уровни, что упрощает анализ графика.

Сигналы разворота: Индикатор предоставляет визуальные сигналы о возможных точках разворота, что может быть использовано для стратегий, основанных на контртрендовой торговле.

Как работает:

Анализ последовательности свечей: Индикатор отслеживает количество последовательных свечей в одном направлении (вверх или вниз). Если цена продолжает движение N баров подряд в одном направлении, система фиксирует это как импульсную фазу.

Выявление истощения тренда: После серии направленных баров рынок может достичь точки перегрева. Если цена продолжает двигаться в том же направлении, но с ослаблением импульса, индикатор фиксирует возможное замедление тренда.

Отображение на графике: Индикатор отмечает точки потенциального разворота номерами или специальными маркерами. Также возможен вывод уровней поддержки и сопротивления, основанных на ключевых точках цикла.

Настройки:

Длина цикла (Cycle Length): Количество баров, после которых оценивается возможность разворота.

Фильтрация тренда (Trend Sensitivity): Параметр, регулирующий чувствительность к трендовым движениям.

Уровни поддержки/сопротивления (Dynamic Levels): Настройка для отображения ключевых уровней.

High-Impact News Events with ALERTHigh-Impact News Events with ALERT

This indicator is builds upon the original by adding alert capabilities, allowing traders to receive notifications before and after economic events to manage risk effectively.

This indicator is updated version of the Live Economic Calendar by @toodegrees ( ) which allows user to set alert for the news events.

Key Features

Customizable Alert Selection: Users can choose which impact levels to restrict (High, Medium, Low).

User-Defined Restriction Timing: Set alerts to X minutes before or after the event.

Real-Time Economic Event Detection: Fetches live news data from Forex Factory.

Multi-Event Support: Detects and processes multiple news events dynamically.

Automatic Trading Restriction: user can use this script to stop trades in news events.

Visual Markers:

Vertical dashed lines indicate the start and end of restriction periods.

Background color changes during restricted trading times.

Alerts notify traders during the news events.

How It Works

The user selects which news impact levels should restrict trading.

The script retrieves real-time economic event data from Forex Factory.

Trading can be restricted for X minutes before and after each event.

The script highlights restricted periods with a background color.

Alerts notify traders all time during the news events is active as per the defined time to prevent unexpected volatility exposure.

Customization Options

Choose which news impact levels (High, Medium, Low) should trigger trading restrictions.

Define time limits before and after each news event for restriction.

Enable or disable alerts for restricted trading periods.

How to Use

Apply the indicator to any TradingView chart.

Configure the news event impact levels you want to restrict.

Set the pre- and post-event restriction durations as needed.

The indicator will automatically apply restrictions, plot visual markers, and trigger alerts accordingly.

Limitations

This script relies on Forex Factory data and may have occasional update delays.

TradingView does not support external API connections, so data is updated through internal methods.

The indicator does not execute trades automatically; it only provides visual alerts and restriction signals.

Reference & Credit

This script is based on the Live Economic Calendar by @toodegrees ( ), adding enhanced pre- and post-event alerting capabilities to help traders prepare for market-moving news.

Disclaimer

This script is for informational purposes only and does not constitute financial advice. Users should verify economic data independently and exercise caution when trading around news events. Past performance is not indicative of future results.

Retrograde Periods (Multi-Planet)**Retrograde Periods (Multi-Planet) Indicator**

This TradingView script overlays your chart with a dynamic visualization of planetary retrograde periods. Built in Pine Script v6, it computes and displays the retrograde status of eight planets—Mercury, Venus, Mars, Jupiter, Saturn, Uranus, Neptune, and Pluto—using hard-coded retrograde intervals from 2009 to 2026.

**Key Features:**

- Dynamic Background Coloring:

The indicator changes the chart’s background color based on the current retrograde status of the planets. The colors follow a priority order (Mercury > Venus > Mars > Jupiter > Saturn > Uranus > Neptune > Pluto) so that if multiple planets are retrograde simultaneously, the highest-priority planet’s color is displayed.

- Interactive Planet Selection:

User-friendly checkboxes allow you to choose which planets to list in the table’s “Selected” row. Note that while these checkboxes control the display of the planet names in the table, the retrograde calculations remain independent of these selections.

- Real-Time Retrograde Status Table:

A table in the top-right corner displays each planet’s retrograde status in real time. “Yes” is shown in red for a planet in retrograde and “No” in green when it isn’t. This offers an at-a-glance view of the cosmic conditions influencing your charts.

- Astrological & Astronomical Insights:

Whether you’re into sidereal astrology or simply fascinated by celestial mechanics, this script lets you visualize those retrograde cycles. In astrology, retrograde periods are often seen as times for reflection and re-evaluation, while in astronomy they reflect the natural orbital motions seen from our perspective on Earth.

Enhance your trading setup by integrating cosmic cycles into your technical analysis. Happy trading and cosmic exploring!

52-Week & 5-Year High/Low with DatesThis indicator is designed to help traders quickly identify key price levels and their historical context by displaying the 52-week high/low and 5-year high/low prices along with their respective dates. It provides a clear visual representation of these levels directly on the chart and in a dashboard table for easy reference.

Key Features

52-Week High/Low:

Displays the highest and lowest prices over the last 252 trading days (approximately 52 weeks).

Includes the exact date when these levels were reached.

5-Year High/Low:

Displays the highest and lowest prices over the last 1260 trading days (approximately 5 years).

Includes the exact date when these levels were reached.

Visual Labels:

High and low levels are marked on the chart with labels that include the price and date.

Dashboard Table:

A table in the top-right corner of the chart summarizes the 52-week and 5-year high/low prices and their dates for quick reference.

Customizable Date Format:

Dates are displayed in the YYYY-MM-DD format for clarity and consistency.

Trading ChecklistTrading Checklist Indicator - Your Trading Plan Companion

A clean and efficient visual checklist to maintain trading discipline and consistency. This indicator helps traders follow their trading plan systematically by providing an easy-to-use checklist of key confirmation points.

Features:

- Visual checklist with clear green/red status indicators

- Clean, non-intrusive interface

- Real-time status updates

- Easy toggle controls for each item

Key Checkpoints:

1. HTF Structure Analysis

2. Order Flow Confirmation

3. SD/OB/FVG (HTF POI) Identification

4. Liquidity Grab Verification

5. Reversal Alignment Check

Final Confirmations:

- Trade Validity Check

- POI & Stop Loss Safety

- Set and Forget Status

How to Use:

1. Add the indicator to your chart

2. Use the Settings panel to toggle each condition

3. Green dots indicate confirmed conditions

4. Red dots show pending confirmations

5. Verify all conditions before executing trades

Note: This indicator helps maintain trading discipline but should be used alongside proper technical and fundamental analysis.

Tags: #TradingChecklist #RiskManagement #TradingPlan #Trading #Technical #Strategy #Discipline

Volume HighlightBar colouring: this indicator is simple but effective, it repaints higher than normal candles a certain colour (by default gold/yellow) it helps to know what are valuable areas to trade around for longs and shorts.

Changing the volume multiplier manually helps you to screen volume relevant to the timeframe you are trading on.

For example, some charts 1min the best filter/setting would be 12-35 multiplier where others like btc 1-4 hourly, the filter/setting might be 8-12.

The key is having only the highest/most relevant 3-4 volume candles showing as they often represent supports and resistances.

Grouped EMAsThis indicator displays grouped EMAs across multiple timeframes (5m, 15m, 30m, and 60m) on a single chart. It allows traders to easily track key EMA levels across different timeframes for better trend analysis and decision-making.

Key Features:

Adjustable EMA Length: Change the EMA period once, and it updates across all timeframes simultaneously.

Multi-Timeframe Support: Displays 365 EMA High and Low for 5-minute, 15-minute, 30-minute, and 60-minute intervals.

Clear Color Coding: Each timeframe is color-coded for quick visual recognition.

How to Use:

Adjust the EMA length using the input option to set your preferred period.

Observe the EMAs across different timeframes to identify support, resistance, and trend directions.

Combine with other indicators or price action strategies for enhanced trading insights.

This tool is ideal for traders looking to simplify multi-timeframe analysis while maintaining flexibility with the EMA period.

Enjoy more informed trading and enhanced trend analysis with Grouped EMAs!

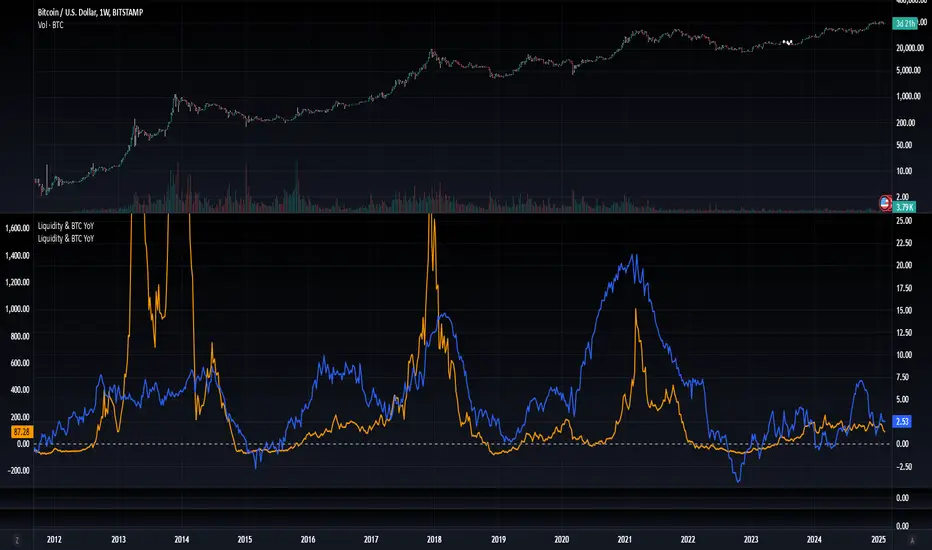

Blockchain Fundamentals: Liquidity & BTC YoYLiquidity & BTC YoY Indicator

Overview:

This indicator calculates the Year-over-Year (YoY) percentage change for two critical metrics: a custom Liquidity Index and Bitcoin's price. The Liquidity Index is derived from a blend of economic and forex data representing the M2 money supply, while the BTC price is obtained from a reliable market source. A dedicated limit(length) function is implemented to handle limited historical data, ensuring that the YoY calculations are available immediately—even when the chart's history is short.

Features Breakdown:

1. Limited Historical Data Workaround

- Functionality: limit(length) The function dynamically adjusts the lookback period when there isn’t enough historical data. This prevents delays in displaying YoY metrics at the beginning of the chart.

2. Liquidity Calculation

- Data Sources: Combines multiple data streams:

USM2, ECONOMICS:CNM2, USDCNY, ECONOMICS:JPM2, USDJPY, ECONOMICS:EUM2, USDEUR

- Formula:

Liquidity Index = USM2 + (CNM2 / USDCNY) + (JPM2 / USDJPY) + (EUM2 / USDEUR)

[b3. Bitcoin Price Calculation

- Data Source: Retrieves Bitcoin's price from BITSTAMP:BTCUSD on the user-selected timeframe for its historical length.

4. Year-over-Year (YoY) Percent Change Calculation

- Methodology:

- The indicator uses a custom function, to autodetect the proper number of bars, based on the selected timeframe.

- It then compares the current value to that from one year ago for both the Liquidity Index and BTC price, calculating the YoY percentage change.

5. Visual Presentation

- Plotting:

- The YoY percentage changes for Liquidity (plotted in blue) and BTC price (plotted in orange) are clearly displayed.

- A horizontal zero line is added for visual alignment, making it easier to compare the two copies of the metric. You add one copy and only display the BTC YoY. Then you add another copy and only display the M2 YoY.

-The zero lines are then used to align the scripts to each other by interposing them. You scale each chart the way you like, then move each copy individually to align both zero lines on top of each other.

This indicator is ideal for analysts and investors looking to monitor macroeconomic liquidity trends alongside Bitcoin's performance, providing immediate insights.

Previous Hour High and Low### **🔷 Previous Hour High & Low Indicator – Description**

#### 📌 **Overview**

The **Previous Hour High & Low Indicator** is designed to help traders identify key levels from the last completed hourly candle. These levels often act as **support and resistance zones**, helping traders make informed decisions about potential breakouts, reversals, and liquidity grabs.

#### 🎯 **How It Works**

- At the start of every new hour, the indicator **locks in** the **high and low** from the **previous fully completed hour**.

- It then **draws horizontal lines** on the chart, marking these levels.

- Works **only on intraday timeframes** (e.g., 1m, 5m, 15m, 30m), ensuring clean and relevant levels.

- Updates dynamically **every new hour** without repainting.

#### 🔑 **Why Is This Useful?**

✔ **Identifies Key Liquidity Zones** – The market often reacts to previous hour highs/lows, making them useful for stop hunts, liquidity grabs, and order block setups.

✔ **Works Well with ICT Concepts** – If you're trading **ICT kill zones**, these levels can help in finding optimal trade entries.

✔ **Helps with Breakout & Rejection Setups** – Traders can watch for price breaking or rejecting these levels for trade confirmation.

✔ **Useful for Scalping & Day Trading** – Works best for short-term traders looking for intraday movements.

#### ⚙ **Customization Options**

- The high and low levels are color-coded:

🔵 **Previous Hour High (Blue)** → Acts as potential resistance or breakout point.

🔴 **Previous Hour Low (Red)** → Acts as potential support or breakdown level.

#### 📊 **Best Timeframes to Use This On**

- **1-minute, 5-minute, 15-minute, 30-minute charts** → Most effective for intraday trading.

- Avoid using on **hourly or higher timeframes**, as these levels become less relevant.

---

🚀 **This indicator is perfect for traders looking to track short-term price reactions at key levels.** Let me know if you want to add alerts, zone shading, or any other enhancements! 🔥

Multi-Asset Ratio (20 vs 5) - LuchapThis indicator calculates and displays the ratio between the sum of the prices of several base assets and the sum of the prices of several quote assets. You can select up to 20 base assets and 5 quote assets, and enable or disable each asset individually to refine your analysis. This ratio allows you to quickly evaluate the relative performance of different groups of assets.

SNR Quarter Pointsfor btmm swingers

this is qp /quater point find in trading view

Here's a description for your TradingView Pine Script indicator:

---

**Support & Resistance (SNR) Lines Indicator**

This TradingView indicator automatically draws Support and Resistance (SNR) lines on the chart at every 250-pip level, starting from 0.0000. The indicator aims to help traders identify key price levels where the market is likely to experience reversal or consolidation. By plotting lines at regular intervals, the script provides a clear visual representation of potential support and resistance zones, aiding traders in making more informed trading decisions. The levels are dynamically adjusted based on market price movement, ensuring they stay relevant for active trading.

---

Let me know if you’d like to tweak it further!

Master Litecoin Dominance Network Value ModelUse this indicator on the LTC.D (Litecoin daily) chart to get a comprehensive view of Litecoin's network value relative to Bitcoin. It analyzes on-chain metrics and market data to help assess Litecoin's intrinsic worth and market trends.

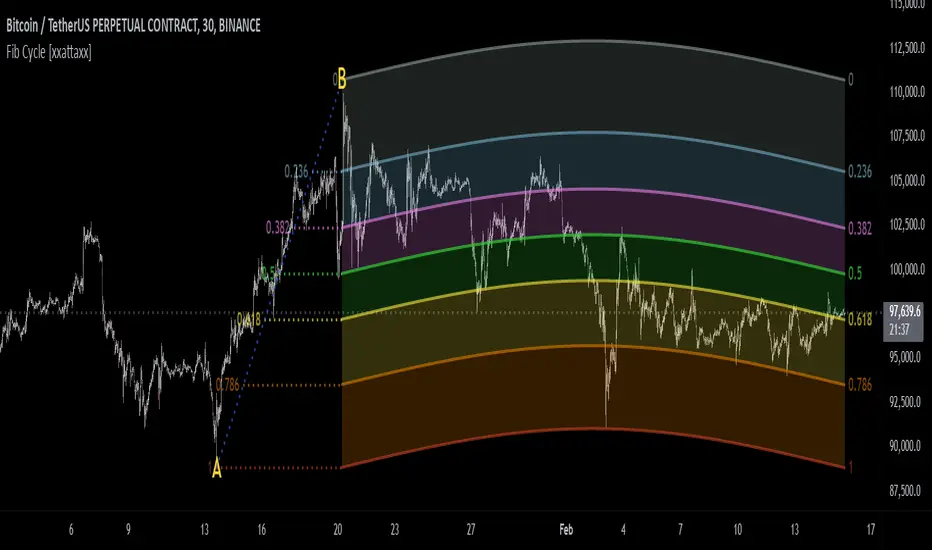

Fibonacci Cycle Finder🟩 Fibonacci Cycle Finder is an indicator designed to explore Fibonacci-based waves and cycles through visualization and experimentation, introducing a trigonometric approach to market structure analysis. Unlike traditional Fibonacci tools that rely on static horizontal levels, this indicator incorporates the dynamic nature of market cycles, using adjustable wavelength, phase, and amplitude settings to visualize the rhythm of price movements. By applying a sine function, it provides a structured way to examine Fibonacci relationships in a non-linear context.

Fibonacci Cycle Finder unifies Fibonacci principles with a wave-based method by employing adjustable parameters to align each wave with real-time price action. By default, the wave begins with minimal curvature, preserving the structural familiarity of horizontal Fibonacci retracements. By adjusting the input parameters, the wave can subtly transition from a horizontal line to a more pronounced cycle,visualizing cyclical structures within price movement. This projective structure extends potential cyclical outlines on the chart, opening deeper exploration of how Fibonacci relationships may emerge over time.

Fibonacci Cycle Finder further underscores a non-linear representation of price by illustrating how wave-based logic can uncover shifts that are missed by static retracement tools. Rather than imposing immediate oscillatory behavior, the indicator encourages a progressive approach, where the parameters may be incrementally modified to align wave structures with observed price action. This refinement process deepens the exploration of Fibonacci relationships, offering a systematic way to experiment with non-linear price dynamics. In doing so, it revisits fundamental Fibonacci concepts, demonstrating their broader adaptability beyond fixed horizontal retracements.

🌀 THEORY & CONCEPT 🌀

What if Fibonacci relationships could be visualized as dynamic waves rather than confined to fixed horizontal levels? Fibonacci Cycle Finder introduces a trigonometric approach to market structure analysis, offering a different perspective on Fibonacci-based cycles. This tool provides a way to visualize market fluctuations through cyclical wave motion, opening the door to further exploration of Fibonacci’s role in non-linear price behavior.

Traditional Fibonacci tools, such as retracements and extensions, have long been used to identify potential support and resistance levels. While valuable for analyzing price trends, these tools assume linear price movement and rely on static horizontal levels. However, market fluctuations often exhibit cyclical tendencies , where price follows natural wave-like structures rather than strictly adhering to fixed retracement points. Although Fibonacci-based tools such as arcs, fans, and time zones attempt to address these patterns, they primarily apply geometric projections. The Fibonacci Cycle Finder takes a different approach by mapping Fibonacci ratios along structured wave cycles, aligning these relationships with the natural curvature of market movement rather than forcing them onto rigid price levels.

Rather than replacing traditional Fibonacci methods, the Fibonacci Cycle Finder supplements existing Fibonacci theory by introducing an exploratory approach to price structure analysis. It encourages traders to experiment with how Fibonacci ratios interact with cyclical price structures, offering an additional layer of insight beyond static retracements and extensions. This approach allows Fibonacci levels to be examined beyond their traditional static form, providing deeper insights into market fluctuations.

📊 FIBONACCI WAVE IMPLEMENTATION 📊

The Fibonacci Cycle Finder uses two user-defined swing points, A and B, as the foundation for projecting these Fibonacci waves. It first establishes standard horizontal levels that correspond to traditional Fibonacci retracements, ensuring a baseline reference before wave adjustments are applied. By default, the wave is intentionally subtle— Wavelength is set to 1 , Amplitude is set to 1 , and Phase is set to 0 . In other words, the wave starts as “stretched out.” This allows a slow, measured start, encouraging users to refine parameters incrementally rather than producing abrupt oscillations. As these parameters are increased, the wave takes on more distinct sine and cosine characteristics, offering a flexible approach to exploring Fibonacci-based cyclicity within price action.

Three parameters control the shape of the Fibonacci wave:

1️⃣ Wavelength Controls the horizontal spacing of the wave along the time axis, determining the length of one full cycle from peak to peak (or trough to trough). In this indicator, Wavelength acts as a scaling input that adjusts how far the wave extends across time, rather than a strict mathematical “wavelength.” Lower values further stretch the wave, increasing the spacing between oscillations, while higher values compress it into a more frequent cycle. Each full cycle is divided into four quarter-cycle segments, a deliberate design choice to minimize curvature by default. This allows for subtle oscillations and smoother transitions, preventing excessive distortion while maintaining flexibility in wave projections. The wavelength is calculated relative to the A-B swing, ensuring that its scale adapts dynamically to the selected price range.

2️⃣ Amplitude Defines the vertical displacement of the wave relative to the baseline Fibonacci level. Higher values increase the height of oscillations, while lower values reduce the height, Negative values will invert the wave’s initial direction. The amplitude is dynamically applied in relation to the A-B swing direction, ensuring that an upward swing results in upward oscillations and a downward swing results in downward oscillations.

3️⃣ Phase Shifts the wave’s starting position along its cycle, adjusting alignment relative to the swing points. A phase of 0 aligns with a sine wave, where the cycle starts at zero and rises. A phase of 25 aligns with a cosine wave, starting at a peak and descending. A phase of 50 inverts the sine wave, beginning at zero but falling first, while a phase of 75 aligns with an inverted cosine , starting at a trough and rising. Intermediate values between these phases create gradual shifts in wave positioning, allowing for finer alignment with observed market structures.

By fine-tuning these parameters, users can adapt Fibonacci waves to better reflect observed market behaviors. The wave structure integrates with price movements rather than simply overlaying static levels, allowing for a more dynamic representation of cyclical price tendencies. This indicator serves as an exploratory tool for understanding potential market rhythms, encouraging traders to test and visualize how Fibonacci principles extend beyond their traditional applications.

🖼️ CHART EXAMPLES 🖼️

Following this downtrend, price interacts with curved Fibonacci levels, highlighting resistance at the 0.236 and 0.382 levels, where price stalls before pulling back. Support emerges at the 0.5, 0.618, and 0.786 levels, where price finds stability and rebounds

In this Fibonacci retracement, price initially finds support at the 1.0 level, following the natural curvature of the cycle. Resistance forms at 0.786, leading to a pullback before price breaks through and tests 0.618 as resistance. Once 0.618 is breached, price moves upward to test 0.5, illustrating how Fibonacci-based cycles may align with evolving market structure beyond static, horizontal retracements.

Following this uptrend, price retraces downward and interacts with the Fibonacci levels, demonstrating both support and resistance at key levels such as 0.236, 0.382, 0.5, and 0.618.

With only the 0.5 and 1.0 levels enabled, this chart remains uncluttered while still highlighting key price interactions. The short cycle length results in a mild curvature, aligning smoothly with market movement. Price finds resistance at the 0.5 level while showing strong support at 1.0, which follows the natural flow of the market. Keeping the focus on fewer levels helps maintain clarity while still capturing how price reacts within the cycle.

🛠️ CONFIGURATION AND SETTINGS 🛠️

Wave Parameters

Wavelength : Stretches or compresses the wave along the time axis, determining the length of one full cycle. Higher values extend the wave across more bars, while lower values compress it into a shorter time frame.

Amplitude : Expands or contracts the wave along the price axis, determining the height of oscillations relative to Fibonacci levels. Higher values increase the vertical range, while negative values invert the wave’s initial direction.

Phase : Offsets the wave along the time axis, adjusting where the cycle begins. Higher values shift the starting position forward within the wave pattern.

Fibonacci Levels

Levels : Enable or disable specific Fibonacci levels (0.0, 0.236, 0.382, 0.5, 0.618, 0.786, 1.0) to focus on relevant price zones.

Color : Modify level colors for enhanced visual clarity.

Visibility

Trend Line/Color : Toggle and customize the trend line connecting swing points A and B.

Setup Lines : Show or hide lines linking Fibonacci levels to projected waves.

A/B Labels Visibility : Control the visibility of swing point labels.

Left/Right Labels : Manage the display of Fibonacci level labels on both sides of the chart.

Fill % : Adjust shading intensity between Fibonacci levels (0% = no fill, 100% = maximum fill).

A and B Points (Time/Price):

These user-defined anchor points serve as the basis for Fibonacci wave calculations and can be manually set. A and B points can also be adjusted directly on the chart, with automatic synchronization to the settings panel, allowing for seamless modifications without needing to manually input values.

⚠️ DISCLAIMER ⚠️

The Fibonacci Cycle Finder is a visual analysis tool designed to illustrate Fibonacci relationships and serve as a supplement to traditional Fibonacci tools. While the indicator employs mathematical and geometric principles, no guarantee is made that its calculations will align with other Fibonacci tools or proprietary methods. Like all technical and visual indicators, the Fibonacci levels generated by this tool may appear to visually align with key price zones in hindsight. However, these levels are not intended as standalone signals for trading decisions. This indicator is intended for educational and analytical purposes, complementing other tools and methods of market analysis.

🧠 BEYOND THE CODE 🧠

Fibonacci Cycle Finder is the latest indicator in the Fibonacci Geometry Series. Building on the concepts of the Fibonacci Time-Price Zones and the Fibonacci 3-D indicators, this tool introduces a trigonometric approach to market structure analysis.

The Fibonacci Cycle Finder indicator, like other xxattaxx indicators , is designed to encourage both education and community engagement. Your feedback and insights are invaluable to refining and enhancing the Fibonacci Cycle Finder indicator. We look forward to the creative applications, observations, and discussions this tool inspires within the trading community.

Volume Alert with Adaptive Trend - MissouriTimElevate your market analysis with our "Volume Alert with Adaptive Trend" indicator. This powerful tool combines real-time volume spike notifications with a sophisticated adaptive trend channel, providing traders with both immediate and long-term market insights. Customize your trading experience with adjustable volume alert thresholds and trend visualization options.

Features Summary

Volume Alert Features:

Volume Spike Detection:

Alerts you when volume exceeds a user-defined multiplier of the 20-period Simple Moving Average (SMA) of volume, helping identify potential market interest or significant price movements.

Visual Notification:

A "Volume Alert" label appears on the chart in a striking purple color (#7300E6) with white text, making high volume bars easily noticeable.

Customizable Sensitivity:

The volume spike threshold is adjustable, allowing you to set how sensitive the alert should be to volume changes, tailored to your trading strategy.

Alerts:

An alert condition is set to notify you when a volume spike occurs, ensuring you don't miss potential trading opportunities.

Adaptive Trend Features

Adaptive Channel:

Visualizes market trends through a dynamic channel that adjusts to price movements, offering insights into trend direction, strength, and potential reversal points.

Lookback Period:

Choose between short-term or long-term trend analysis with a toggle that adjusts the calculation period for the trend channel.

Channel Customization:

Fine-tune the trend channel with options for deviation multiplier, line styles, colors, transparency, and extension preferences to match your visual trading preferences.

Non-Repainting:

The trend lines are updated only on the current bar, ensuring the integrity of historical data for backtesting and strategy development.

Integrated Utility

Combination of Tools: This indicator marries the immediacy of volume alerts with the strategic depth of trend analysis, offering a comprehensive view of market dynamics.

User Customization: With inputs for both volume alerts and trend visualization, the indicator can be tailored to suit various trading styles, from scalping to swing trading.

This indicator ensures you're always in tune with market movements, providing crucial information at a glance to inform your trading decisions.