Trend Range Detector (Zeiierman)█ Overview

Trend Range Detector (Zeiierman) is a market structure tool that identifies and tracks periods of price compression by forming adaptive range boxes based on volatility and price movement. When prices remain stable within a defined band, the script dynamically draws a range box; when prices break out of that structure, the box highlights the breakout in real-time.

By combining a volatility-based envelope with a custom weighted centerline, this tool filters out noise and isolates truly stable zones — providing a clean framework for traders who focus on accumulation, distribution, breakout anticipation, and reversion opportunities.

Whether you're range trading, spotting trend consolidations, or looking for volatility contractions before major moves, the Trend Range Detector gives you a mathematically adaptive, visually intuitive structure that maps the heartbeat of the market.

█ How It Works

⚪ Range Formation Engine

The core of this indicator revolves around two conditions:

Distance Filter: The maximum distance between all recent closes and a dynamic centerline must remain within a volatility envelope.

Volatility Envelope: Based on an ATR(2000) multiplied by a user-defined factor to account for broader market volatility trends.

If both conditions are satisfied over the most recent length bars, a range box is drawn to visually anchor the zone.

⚪ Dynamic Breakout Coloring

When price breaks out of the top or bottom of the active range box, the box color shifts in real-time:

Blue Boxes represent areas where price has remained within a defined volatility envelope over a sustained number of bars. These zones reflect stable, low-volatility periods, often associated with consolidation, equilibrium, or market indecision.

Green Boxes for bullish breakouts.

Red Boxes for bearish breakdowns.

This allows traders to visually spot transitions from consolidation to expansion phases without relying on lagging signals.

█ Why Use a Weighted Close Instead of SMA?

A standard Simple Moving Average (SMA) treats all past closes equally, which works well in theory, but not in dynamic, fast-shifting markets. In this script, we replace the traditional SMA with a speed-weighted average that reflects how aggressively the market has moved bar-to-bar.

⚪ Here's why it matters:

Bars with higher momentum (larger price differences between closes) are given more weight.

Slow, sideways candles (typical in noise or low volume) contribute less to the calculated centerline.

This method creates a more accurate snapshot of market behavior, especially during volatile phases. As a result, the indicator adapts to market conditions more effectively, helping traders identify real consolidation zones, not just average lines distorted by flat bars or noise.

█ How to Use

⚪ Range Detection

Boxes form only when price remains consistently close to the speed-weighted mean.

Helps identify sideways zones, consolidations, and low-volatility structures where price is “charging up.”

⚪ Breakout Confirmation

Once price exits the top or bottom boundary, the box immediately highlights the direction of the break.

Use this signal in conjunction with your own momentum, volume, or trend filters for higher-confidence trades.

█ Settings

Minimum Range Length: Number of candles required for a valid range to form.

Range Width Multiplier: Adjusts the envelope around the weighted average using ATR(2000).

Highlight Box Breaks: Enables real-time coloring of breakouts and breakdowns for immediate visual feedback.

-----------------

Disclaimer

The content provided in my scripts, indicators, ideas, algorithms, and systems is for educational and informational purposes only. It does not constitute financial advice, investment recommendations, or a solicitation to buy or sell any financial instruments. I will not accept liability for any loss or damage, including without limitation any loss of profit, which may arise directly or indirectly from the use of or reliance on such information.

All investments involve risk, and the past performance of a security, industry, sector, market, financial product, trading strategy, backtest, or individual's trading does not guarantee future results or returns. Investors are fully responsible for any investment decisions they make. Such decisions should be based solely on an evaluation of their financial circumstances, investment objectives, risk tolerance, and liquidity needs.

Indicators and strategies

BE-Indicator Aggregator toolkit█ Overview:

BE-Indicator Aggregator toolkit is a toolkit which is built for those we rely on taking multi-confirmation from different indicators available with the traders. This Toolkit aid's traders in understanding their custom logic for their trade setups and provides the summarized results on how it performed over the past.

█ How It Works:

Load the external indicator plots in the indicator input setting

Provide your custom logic for the trade setup

Set your expected SL & TP values

█ Legends, Definitions & Logic Building Rules:

Building the logic for your trade setup plays a pivotal role in the toolkit, it shall be broken into parts and toolkit aims to understand each of the logical parts of your setup and interpret the outcome as trade accuracy.

Toolkit broadly aims to understand 4 types of inputs in "Condition Builder"

Comments : Line which starts with single quotation ( ' ) shall be ignored by toolkit while understanding the logic.

Note: Blank line space or less than 3 characters are treated equally to comments.

Long Condition: Line which starts with " L- " shall be considered for identifying Long setups.

Short Condition: Line which starts with " S- " shall be considered for identifying Short setups.

Variables: Line which starts with " VAR- " shall be considered as variables. Variables can be one such criteria for Long or short condition.

Building Rules: Define all variables first then specify the condition. The usual declare and assign concept of programming. :p)

Criteria Rules: Criteria are individual logic for your one parent condition. multiple criteria can be present in one condition. Each parameter should be delimited with ' | ' key and each criteria should be delimited with ' , ' (Comma with a space - IMPORTANT!!!)

█ Sample Codes for Conditional Builder:

For Trading Long when Open = Low

For Trading Short when Open = High with a Red candle

'Long Setup <---- Comment

L-O|E|L

' E <- in the above line refers to Equals ' = '

'Short Setup

S-AND:O|E|H, O|G|C

' 2 Criteria for used building one condition. Since, both have to satisfied used "AND:" logic.

Understanding of Operator Legends:

"E" => Refers to Equals

"NE" => Refers to Not Equals

"NEOR" => Logical value is Either Comparing value 1 or Comparing value 2

"NEAND" => Logical value is Comparing value 1 And Comparing value 2

"G" => Logical value Greater than Comparing value 1

"GE" => Logical value Greater than and equal to Comparing value 1

"L" => Logical value Lesser than Comparing value 1

"LE" => Logical value Lesser than and equal to Comparing value 1

"B" => Logical value is Between Comparing value 1 & Comparing value 2

"BE" => Logical value is Between or Equal to Comparing value 1 & Comparing value 2

"OSE" => Logical value is Outside of Comparing value 1 & Comparing value 2

"OSI" => Logical value is Outside or Equal to Comparing value 1 & Comparing value 2

"ERR" => Logical value is 'na'

"NERR" => Logical value is not 'na'

"CO" => Logical value Crossed Over Comparing value 1

"CU" => Logical value Crossed Under Comparing value 1

Understanding of Condition Legends:

AND: -> All criteria's to be satisfied for the condition to be True.

NAND: -> Output of AND condition shall be Inversed for the condition to be True.

OR: -> One of criteria to be satisfied for the condition to be True.

NOR: -> Output of OR condition shall be Inversed for the condition to be True.

ATLEAST:X: -> At-least X no of criteria to be satisfied for the condition to be True.

Note: "X" can be any number

NATLEAST:X: -> Output of ATLEAST condition shall be Inversed for the condition to be True

WASTRUE:X: -> Single criteria WAS TRUE within X bar in past for the condition to be True.

Note: "X" can be any number.

ISTRUE:X: -> Single criteria is TRUE since X bar in past for the condition to be True.

Note: "X" can be any number.

Understanding of Variable Legends:

While Condition Supports 8 Types, Variable supports only 6 Types listed below

AND: -> All criteria's to be satisfied for the Variable to be True.

NAND: -> Output of AND condition shall be Inversed for the Variable to be True.

OR: -> One of criteria to be satisfied for the Variable to be True.

NOR: -> Output of OR condition shall be Inversed for the Variable to be True.

ATLEAST:X: -> At-least X no of criteria to be satisfied for the Variable to be True.

Note: "X" can be any number

NATLEAST:X: -> Output of ATLEAST condition shall be Inversed for the Variable to be True

█ Sample Outputs with Logics:

1. RSI Indicator + Technical Indicator: StopLoss: 2.25 against Reward ratio of 1.75 (3.94 value)

Plots Used in Indicator Settings:

Source 1:- RSI

Source 2:- RSI Based MA

Source 3:- Strong Buy

Source 4:- Strong Sell

Logic Used:

For Long Setup : RSI Should be above RSI Based MA, RSI has been Rising when compared to 3 candles ago, Technical Indicator signaled for a Strong Buy on the current candle, however in last 6 candles Technical indicator signaled for Strong Sell.

Similarly Inverse for Short Setup.

L-AND:ES1|GE|ES2, ES1|G|ES1

L-ES3|E|1

L-OR:ES4 |E|1, ES4 |E|1, ES4 |E|1, ES4 |E|1, ES4 |E|1, ES4 |E|1

S-AND:ES1|LE|ES2, ES1|L|ES1

S-ES4|E|1

S-OR:ES3 |E|1, ES3 |E|1, ES3 |E|1, ES3 |E|1, ES3 |E|1, ES3 |E|1

'Note: Last OR condition can also be written by using WASTRUE definition like below

'L-WASTRUE:6:ES4|E|1

'S-WASTRUE:6:ES3|E|1

Output:

2. Volumatic Support / Resistance Levels :

Plots Used in Indicator Settings:

Source 1:- Resistance

Source 2:- Support

Logic Used:

For Long Setup : Long Trade on Liquidity Support.

For Short Setup : Short Trade on Liquidity Resistance.

'Variable Named "ChkLowTradingAbvSupport" is declared to check if last 3 candles is trading above support line of liquidity.

VAR-ChkLowTradingAbvSupport:AND:L|G|ES2, L |G|ES2, L |G|ES2

'Variable Named "ChkCurBarClsdAbv4thBarHigh" is declared to check if current bar closed above the high of previous candle where the Liquidity support is taken (4th Bar).

VAR-ChkCurBarClsdAbv4thBarHigh:OR:C|GE|H , L|G|H

'Combining Condition and Variable to Initiate Long Trade Logic

L-L |LE|ES2

L-AND:ChkLowTradingAbvSupport, ChkCurBarClsdAbv4thBarHigh

VAR-ChkHghTradingBlwRes:AND:H|L|ES1, H |L|ES1, H |L|ES1

VAR-ChkCurBarClsdBlw4thBarLow:OR:C|LE|L , H|L|L

S-H |GE|ES1

S-AND:ChkHghTradingBlwRes, ChkCurBarClsdBlw4thBarLow

Output 1: Day Trading Version

Output 2: Scalper Version

Output 3: Position Version

Synthetic VX3! & VX4! continuous /VX futuresTradingView is missing continuous 3rd and 4th month VIX (/VX) futures, so I decided to try to make a synthetic one that emulates what continuous maturity futures would look like. This is useful for backtesting/historical purposes as it enables traders to see how their further out VX contracts would've performed vs the front month contract.

The indicator pulls actual realtime data (if you subscribe to the CBOE data package) or 15 minute delayed data for the VIX spot (the actual non-tradeable VIX index), the continuous front month (VX1!), and the continuous second month (VX2!) continually rolled contracts. Then the indicator's script applies a formula to fairly closely estimate how 3rd and 4th month continuous contracts would've moved.

It uses an exponential mean‑reversion to a long‑run level formula using:

σ(T) = θ+(σ0−θ)e−kT

You can expect it to be off by ~5% or so (in times of backwardation it might be less accurate).

Intrabar Efficiency Ratio█ OVERVIEW

This indicator displays a directional variant of Perry Kaufman's Efficiency Ratio, designed to gauge the "efficiency" of intrabar price movement by comparing the sum of movements of the lower timeframe bars composing a chart bar with the respective bar's movement on an average basis.

█ CONCEPTS

Efficiency Ratio (ER)

Efficiency Ratio was first introduced by Perry Kaufman in his 1995 book, titled "Smarter Trading". It is the ratio of absolute price change to the sum of absolute changes on each bar over a period. This tells us how strong the period's trend is relative to the underlying noise. Simply put, it's a measure of price movement efficiency. This ratio is the modulator utilized in Kaufman's Adaptive Moving Average (KAMA), which is essentially an Exponential Moving Average (EMA) that adapts its responsiveness to movement efficiency.

ER's output is bounded between 0 and 1. A value of 0 indicates that the starting price equals the ending price for the period, which suggests that price movement was maximally inefficient. A value of 1 indicates that price had travelled no more than the distance between the starting price and the ending price for the period, which suggests that price movement was maximally efficient. A value between 0 and 1 indicates that price had travelled a distance greater than the distance between the starting price and the ending price for the period. In other words, some degree of noise was present which resulted in reduced efficiency over the period.

As an example, let's say that the price of an asset had moved from $15 to $14 by the end of a period, but the sum of absolute changes for each bar of data was $4. ER would be calculated like so:

ER = abs(14 - 15)/4 = 0.25

This suggests that the trend was only 25% efficient over the period, as the total distanced travelled by price was four times what was required to achieve the change over the period.

Intrabars

Intrabars are chart bars at a lower timeframe than the chart's. Each 1H chart bar of a 24x7 market will, for example, usually contain 60 intrabars at the LTF of 1min, provided there was market activity during each minute of the hour. Mining information from intrabars can be useful in that it offers traders visibility on the activity inside a chart bar.

Lower timeframes (LTFs)

A lower timeframe is a timeframe that is smaller than the chart's timeframe. This script determines which LTF to use by examining the chart's timeframe. The LTF determines how many intrabars are examined for each chart bar; the lower the timeframe, the more intrabars are analyzed, but fewer chart bars can display indicator information because there is a limit to the total number of intrabars that can be analyzed.

Intrabar precision

The precision of calculations increases with the number of intrabars analyzed for each chart bar. As there is a 100K limit to the number of intrabars that can be analyzed by a script, a trade-off occurs between the number of intrabars analyzed per chart bar and the chart bars for which calculations are possible.

Intrabar Efficiency Ratio (IER)

Intrabar Efficiency Ratio applies the concept of ER on an intrabar level. Rather than comparing the overall change to the sum of bar changes for the current chart's timeframe over a period, IER compares single bar changes for the current chart's timeframe to the sum of absolute intrabar changes, then applies smoothing to the result. This gives an indication of how efficient changes are on the current chart's timeframe for each bar of data relative to LTF bar changes on an average basis. Unlike the standard ER calculation, we've opted to preserve directional information by not taking the absolute value of overall change, thus allowing it to be utilized as a momentum oscillator. However, by taking the absolute value of this oscillator, it could potentially serve as a replacement for ER in the design of adaptive moving averages.

Since this indicator preserves directional information, IER can be regarded as similar to the Chande Momentum Oscillator (CMO) , which was presented in 1994 by Tushar Chande in "The New Technical Trader". Both CMO and ER essentially measure the same relationship between trend and noise. CMO simply differs in scale, and considers the direction of overall changes.

█ FEATURES

Display

Three different display types are included within the script:

• Line : Displays the middle length MA of the IER as a line .

Color for this display can be customized via the "Line" portion of the "Visuals" section in the script settings.

• Candles : Displays the non-smooth IER and two moving averages of different lengths as candles .

The `open` and `close` of the candle are the longest and shortest length MAs of the IER respectively.

The `high` and `low` of the candle are the max and min of the IER, longest length MA of the IER, and shortest length MA of the IER respectively.

Colors for this display can be customized via the "Candles" portion of the "Visuals" section in the script settings.

• Circles : Displays three MAs of the IER as circles .

The color of each plot depends on the percent rank of the respective MA over the previous 100 bars.

Different colors are triggered when ranks are below 10%, between 10% and 50%, between 50% and 90%, and above 90%.

Colors for this display can be customized via the "Circles" portion of the "Visuals" section in the script settings.

With either display type, an optional information box can be displayed. This box shows the LTF that the script is using, the average number of lower timeframe bars per chart bar, and the number of chart bars that contain LTF data.

Specifying intrabar precision

Ten options are included in the script to control the number of intrabars used per chart bar for calculations. The greater the number of intrabars per chart bar, the fewer chart bars can be analyzed.

The first five options allow users to specify the approximate amount of chart bars to be covered:

• Least Precise (Most chart bars) : Covers all chart bars by dividing the current timeframe by four.

This ensures the highest level of intrabar precision while achieving complete coverage for the dataset.

• Less Precise (Some chart bars) & More Precise (Less chart bars) : These options calculate a stepped LTF in relation to the current chart's timeframe.

• Very precise (2min intrabars) : Uses the second highest quantity of intrabars possible with the 2min LTF.

• Most precise (1min intrabars) : Uses the maximum quantity of intrabars possible with the 1min LTF.

The stepped lower timeframe for "Less Precise" and "More Precise" options is calculated from the current chart's timeframe as follows:

Chart Timeframe Lower Timeframe

Less Precise More Precise

< 1hr 1min 1min

< 1D 15min 1min

< 1W 2hr 30min

> 1W 1D 60min

The last five options allow users to specify an approximate fixed number of intrabars to analyze per chart bar. The available choices are 12, 24, 50, 100, and 250. The script will calculate the LTF which most closely approximates the specified number of intrabars per chart bar. Keep in mind that due to factors such as the length of a ticker's sessions and rounding of the LTF, it is not always possible to produce the exact number specified. However, the script will do its best to get as close to the value as possible.

Specifying MA type

Seven MA types are included in the script for different averaging effects:

• Simple

• Exponential

• Wilder (RMA)

• Weighted

• Volume-Weighted

• Arnaud Legoux with `offset` and `sigma` set to 0.85 and 6 respectively.

• Hull

Weighting

This script includes the option to weight IER values based on the percent rank of absolute price changes on the current chart's timeframe over a specified period, which can be enabled by checking the "Weigh using relative close changes" option in the script settings. This places reduced emphasis on IER values from smaller changes, which may help to reduce noise in the output.

█ FOR Pine Script™ CODERS

• This script imports the recently published lower_ltf library for calculating intrabar statistics and the optimal lower timeframe in relation to the current chart's timeframe.

• This script uses the recently released request.security_lower_tf() Pine Script™ function discussed in this blog post .

It works differently from the usual request.security() in that it can only be used on LTFs, and it returns an array containing one value per intrabar.

This makes it much easier for programmers to access intrabar information.

• This script implements a new recommended best practice for tables which works faster and reduces memory consumption.

Using this new method, tables are declared only once with var , as usual. Then, on the first bar only, we use table.cell() to populate the table.

Finally, table.set_*() functions are used to update attributes of table cells on the last bar of the dataset.

This greatly reduces the resources required to render tables.

Look first. Then leap.

Strategy█ OVERVIEW

This library is a Pine Script™ programmer’s tool containing a variety of strategy-related functions to assist in calculations like profit and loss, stop losses and limits. It also includes several useful functions one can use to convert between units in ticks, price, currency or a percentage of the position's size.

█ CONCEPTS

The library contains three types of functions:

1 — Functions beginning with `percent` take either a portion of a price, or the current position's entry price and convert it to the value outlined in the function's documentation.

Example: Converting a percent of the current position entry price to ticks, or calculating a percent profit at a given level for the position.

2 — Functions beginning with `tick` convert a tick value to another form.

These are useful for calculating a price or currency value from a specified number of ticks.

3 — Functions containing `Level` are used to calculate a stop or take profit level using an offset in ticks from the current entry price.

These functions can be used to plot stop or take profit levels on the chart, or as arguments to the `limit` and `stop` parameters in strategy.exit() function calls.

Note that these calculated levels flip automatically with the position's bias.

For example, using `ticksToStopLevel()` will calculate a stop level under the entry price for a long position, and above the entry price for a short position.

There are also two functions to assist in calculating a position size using the entry's stop and a fixed risk expressed as a percentage of the current account's equity. By varying the position size this way, you ensure that entries with different stop levels risk the same proportion of equity.

█ NOTES

Example code using some of the library's functions is included at the end of the library. To see it in action, copy the library's code to a new script in the Pine Editor, and “Add to chart”.

For each trade, the code displays:

• The entry level in orange.

• The stop level in fuchsia.

• The take profit level in green.

The stop and take profit levels automatically flip sides based on whether the current position is long or short.

Labels near the last trade's levels display the percentages used to calculate them, which can be changed in the script's inputs.

We plot markers for entries and exits because strategy code in libraries does not display the usual markers for them.

Look first. Then leap.

█ FUNCTIONS

percentToTicks(percent) Converts a percentage of the average entry price to ticks.

Parameters:

percent : (series int/float) The percentage of `strategy.position_avg_price` to convert to ticks. 50 is 50% of the entry price.

Returns: (float) A value in ticks.

percentToPrice(percent) Converts a percentage of the average entry price to a price.

Parameters:

percent : (series int/float) The percentage of `strategy.position_avg_price` to convert to price. 50 is 50% of the entry price.

Returns: (float) A value in the symbol's quote currency (USD for BTCUSD).

percentToCurrency(price, percent) Converts the percentage of a price to money.

Parameters:

price : (series int/float) The symbol's price.

percent : (series int/float) The percentage of `price` to calculate.

Returns: (float) A value in the symbol's currency.

percentProfit(exitPrice) Calculates the profit (as a percentage of the position's `strategy.position_avg_price` entry price) if the trade is closed at `exitPrice`.

Parameters:

exitPrice : (series int/float) The potential price to close the position.

Returns: (float) Percentage profit for the current position if closed at the `exitPrice`.

priceToTicks(price) Converts a price to ticks.

Parameters:

price : (series int/float) Price to convert to ticks.

Returns: (float) A quantity of ticks.

ticksToPrice(price) Converts ticks to a price offset from the average entry price.

Parameters:

price : (series int/float) Ticks to convert to a price.

Returns: (float) A price level that has a distance from the entry price equal to the specified number of ticks.

ticksToCurrency(ticks) Converts ticks to money.

Parameters:

ticks : (series int/float) Number of ticks.

Returns: (float) Money amount in the symbol's currency.

ticksToStopLevel(ticks) Calculates a stop loss level using a distance in ticks from the current `strategy.position_avg_price` entry price. This value can be plotted on the chart, or used as an argument to the `stop` parameter of a `strategy.exit()` call. NOTE: The stop level automatically flips based on whether the position is long or short.

Parameters:

ticks : (series int/float) The distance in ticks from the entry price to the stop loss level.

Returns: (float) A stop loss level for the current position.

ticksToTpLevel(ticks) Calculates a take profit level using a distance in ticks from the current `strategy.position_avg_price` entry price. This value can be plotted on the chart, or used as an argument to the `limit` parameter of a `strategy.exit()` call. NOTE: The take profit level automatically flips based on whether the position is long or short.

Parameters:

ticks : (series int/float) The distance in ticks from the entry price to the take profit level.

Returns: (float) A take profit level for the current position.

calcPositionSizeByStopLossTicks(stopLossTicks, riskPercent) Calculates the position size needed to implement a given stop loss (in ticks) corresponding to `riskPercent` of equity.

Parameters:

stopLossTicks : (series int) The stop loss (in ticks) that will be used to protect the position.

riskPercent : (series int/float) The maximum risk level as a percent of current equity (`strategy.equity`).

Returns: (int) A quantity of contracts.

calcPositionSizeByStopLossPercent(stopLossPercent, riskPercent, entryPrice) Calculates the position size needed to implement a given stop loss (%) corresponding to `riskPercent` of equity.

Parameters:

stopLossPercent : (series int/float) The stop loss in percent that will be used to protect the position.

riskPercent : (series int/float) The maximum risk level as a percent of current equity (`strategy.equity`).

entryPrice : (series int/float) The entry price of the position.

Returns: (int) A quantity of contracts.

exitPercent(id, lossPercent, profitPercent, qty, qtyPercent, comment, when, alertMessage) A wrapper of the `strategy.exit()` built-in which adds the possibility to specify loss & profit in as a value in percent. NOTE: this function may work incorrectly with pyramiding turned on due to the use of `strategy.position_avg_price` in its calculations of stop loss and take profit offsets.

Parameters:

id : (series string) The order identifier of the `strategy.exit()` call.

lossPercent : (series int/float) Stop loss as a percent of the entry price.

profitPercent : (series int/float) Take profit as a percent of the entry price.

qty : (series int/float) Number of contracts/shares/lots/units to exit a trade with. The default value is `na`.

qtyPercent : (series int/float) The percent of the position's size to exit a trade with. If `qty` is `na`, the default value of `qty_percent` is 100.

comment : (series string) Optional. Additional notes on the order.

when : (series bool) Condition of the order. The order is placed if it is true.

alertMessage : (series string) An optional parameter which replaces the {{strategy.order.alert_message}} placeholder when it is used in the "Create Alert" dialog box's "Message" field.

Signs of the Times [LucF]█ OVERVIEW

This oscillator calculates the directional strength of bars using a primitive weighing mechanism based on a small number of what I consider to be fundamental properties of a bar. It does not consider the amplitude of price movements, so can be used as a complement to momentum-based oscillators. It thus belongs to the same family of indicators as my Bar Balance , Volume Ticks , Efficient work , Volume Buoyancy or my Delta Volume indicators.

█ CONCEPTS

The calculations underlying Signs of the Times (SOTT) use a simple, oft-explored concept: measure bar attributes, assign a weight to them, and aggregate results to provide an evaluation of a bar's directional strength. Bull and bear weights are added independently, then subtracted and divided by the maximum possible weight, so the final calculation looks like this:

(up - dn) / weightRange

SOTT has a zero centerline and oscillates between +1 and -1. Ten elementary properties are evaluated. Most carry a weight of one, a few are doubly weighted. All properties are evaluated using only the current bar's values or by comparing its values to those of the preceding bar. The bull conditions follow; their inverse applies to bear conditions:

Weight of 1

• Bar's close is greater than the bar's open (bar is considered to be of "up" polarity)

• Rising open

• Rising high

• Rising low

• Rising close

• Bar is up and its body size is greater than that of the previous bar

• Bar is up and its body size is greater than the combined size of wicks

Weight of 2

• Gap to the upside

• Efficient Work when it is positive

• Bar is up and volume is greater than that of the previous bar (this only kicks in if volume is actually available on the chart's data feed)

Except for the Efficient Work weight, which is a +1 to -1 float value multiplied by 2, all weights are discrete; either zero or the full weight of 1 or 2 is generated. This will cause any gap, for example, to generate a weight of +2 or -2, regardless of the gap's size. That is the reason why the oscillator is oblivious to the amplitude of price movements.

You can see the code used to calculate SOTT in my ta library 's `sott()` function.

█ HOW TO USE THE INDICATOR

No videos explain this indicator and none are planned; reading this description or the script's code is the only way to understand what Signs of the Times does.

Load the indicator on an active chart (see here if you don't know how).

The default configuration displays:

• An Arnaud-Legoux moving average of length 20 of the instant SOTT value. This is the signal line.

• A fill between the MA and the centerline.

• Levels at arbitrary values of +0.3 and -0.3.

• A channel between the signal line and its MA (a simple MA of length 20), which can be one of four colors:

• Bull (green): The signal line is above its MA.

• Strong bull (lime): The bull condition is fulfilled and the signal line is above the centerline.

• Bear (red): The signal line is below its MA.

• Strong bear (pink): The bear condition is fulfilled and the signal line is below the centerline.

The script's "Inputs" tab allows you to:

• Choose a higher timeframe to calculate the indicator's values. This can be useful to get a wider perspective of the indicator's values.

If you elect to use a higher timeframe, make sure that your chart's timeframe is always lower than the higher timeframe you specified,

as calculating on a timeframe lower than the chart's does not make much sense because the indicator is then displaying only the value of the last intrabar in the chart bar.

• Specify the type of MA used to produce the signal line. Use a length of 1 or the Data Window to see the instant value of SOTT. It is quite noisy, thus the need to average it.

• Specify the type of MA applied to the signal line. The idea here is to provide context to the signal.

• Control the display and colors of the lines and fills.

The first pane of this publication's chart shows the default setup. The second one shows only a monochrome signal line.

Using the "Style" tab of the indicator's settings, you can change the type and width of the lines, and the level values.

█ INTERPRETATION

Remember that Signs of the Times evaluates directional bar strength — not price movement. Its highs and lows do not reflect price, but the strength of chart bars. The fact that SOTT knows nothing of how far price moves or of trends is easy to forget. As such, I think SOTT is best used as a confirmation tool. Chart movements may appear to be easy to read when looking at historical bars, but when you have to make go-no-go decisions on the last bar, the landscape often becomes murkier. By providing a quantitative evaluation of the strength of the last few bars, which is not always easily discernible by simply looking at them, SOTT aims to help you decide if the short-term past favors the bets you are considering. Can SOTT predict the future? Of course not.

While SOTT uses completely different calculations than classical momentum oscillators, its profile shares many of their characteristics. This could lead one to infer that directional bar strength correlates with price movement, which could in turn lead one to conclude that indicators such as this one are useless, or that they can be useful tools to confirm momentum oscillators or other models of price movement. The call is, of course, up to you. You can try, for example, to compare a Wilder MA of SOTT to an RSI of the same length.

One key difference with momentum oscillators is that SOTT is much less sensitive to large price movements. The default Arnaud-Legoux MA used for the signal line makes it quite active; you can use a more quiet SMA or EMA if you prefer to tone it down.

In systems where it can be useful to only enter or exit on short-term strength, an average of SOTT values over the last 3 to 5 bars can be used as a more quiet filter than a momentum oscillator would.

█ NOTES

My publications often go through a long gestation period where I use them on my charts or in systems before deciding if they are worth a publication. With an incubation period of more than three years, Signs of the Times holds the record. The properties SOTT currently evaluates result from the systematic elimination of contaminants over that lengthy period of time. It was long because of my usual, slow gear, but also because I had to try countless combinations of conditions before realizing that, contrary to my intuition, best results were achieved by:

• Keeping the number of evaluated properties to the absolute minimum.

• Limiting the evaluation's scope to the current and preceding bar.

• Choosing properties that, in my view, were unmistakably indicative of bullish/bearish conditions.

Repainting

As most oscillators, the indicator provides live realtime values that will recalculate with chart updates. It will thus repaint in real time, but not on historical values. To learn more about repainting, see the Pine Script™ User Manual's page on the subject .

Estimated Time At Price [Kioseff Trading]Hello!

This script uses the same formula as the recently released "Volume Delta" script to ascertain lower timeframe values.

Instead, this script looks to estimate the approximate time spent at price blocks; all time estimates are in minute.second format.

The image above shows functionality. Time spent at price levels/blocks are estimated in duration. The highest estimated block is the highlighted level and a POC line is extended right until violated. Colors, the presence of POC lines and whether they're removed subsequent violation are all configurable.

As show in the image above, the data is displayable in an additional format. When select the "non-classic" format shown above - precise price levels are calculated and the estimated time spent at those levels is summed and displayed right of the current bar. The off-colored level (yellow in the example) denotes the price level encompassing the highest *estimated* time spent.

You can deselect the neon effect and choose to have the script recalculate after any conceivable amount of time has passed.

The script can also calculate for the most current bar should you configure it to do so.

That's all! (for now). A quick/easy script building off an existing foundation.

If you've any ideas for features and ways to "spice up" this script please let me know (: I'll gladly incorporate requests.

Thank you!

Volume Profile, Pivot Anchored by DGTVolume Profile (also known as Price by Volume ) is an charting study that displays trading activity over a specified time period at specific price levels. It is plotted as a horizontal histogram on the finacial isntrumnet's chart that highlights the trader's interest at specific price levels. Specified time period with Pivots Anchored Volume Profile is determined by the Pivot Levels, where the Pivot Points High Low indicator is used and presented with this Custom indicator

Finally, Volume Weighted Colored Bars indicator is presneted with the study

Different perspective of Volume Profile applications;

Anchored to Session, Week, Month etc : Anchored-Volume-Profile

Custom Range, Interactive : Volume-Profile-Custom-Range

Fixed Range with Volume Indicator : Volume-Profile-Fixed-Range

Combined with Support and Resistance Indicator : Price-Action-Support-Resistance and Volume-Profile

Combined with Supply and Demand Zones, Interactive : Supply-Demand-and-Equilibrium-Zones

Disclaimer : Trading success is all about following your trading strategy and the indicators should fit within your trading strategy, and not to be traded upon solely

The script is for informational and educational purposes only. Use of the script does not constitutes professional and/or financial advice. You alone the sole responsibility of evaluating the script output and risks associated with the use of the script. In exchange for using the script, you agree not to hold dgtrd TradingView user liable for any possible claim for damages arising from any decision you make based on use of the script

Fair Value MSThis indicator introduces rigid rules to familiar concepts to better capture and visualize Market Structure and Areas of Support and Resistance in a way that is both rule-based and reactive to market movements.

Typical "Market Structure" or "Zig-Zag" methods determine swing points based on fixed thresholds (length or percentage). While this does provide rigid structure, the results may be lagging or confusing due to the timing, since it is fixed to static parameters.

I believe the concept of Fair Value Gaps can solve this problem.

As you will notice, there are no length settings in this indicator.

> FVG Market Structure

Fair Value Gaps are a well known concept used to indicate directional intent, forming when price moves aggressively in one direction, leaving behind an imbalance between buyers and sellers. While the term FVG was popularized by ICT, the underlying concept predates them, known historically as imbalances, inefficiencies, or liquidity voids in institutional trading.

Note: For simplicity, in this indicator they'll be called FVGs.

By reading into this, we are able to clearly and rigidly define market structure simply by "looking" at the chart, using objective price events rather than subjective interpretation, or lengths.

By using FVGs to determine structure direction, the length, and speed of identification lies entirely on the market. If an FVG Down occurs immediately after a New Higher High forms, it is reasonable to assume there was a seller at that point, so the script would indicate a New Swing High.

The script is NOT stuck, waiting for a % retrace, or # bars to pass to identify it as such.

Sometimes the market is in a steady trend in a single direction and no FVGs form; therefore, no structure forms. -> Why would we try to impose structure on a clear trend?

Ultimately, the FVG Structure Method uses real reactions from the market to determine Market structure, and is not fixed to specific parameters.

As with other market structure indicators, "Market Structure Breaks" are still identifiable when price moves outside the most recent swing points.

These are helpful to indicate larger direction. In the following section you will see how these help us determine when we should start the search for an "Area of Interest (AOI)".

> Areas of Interest (AOIs)

"Area of Interest (AOI)" is a generalized term, and could refer to many types of zones you might recognize under different names. While the AOIs in this indicator are specialized in their own way, I have chosen to simply use the term "Area of Interest" because it’s more important to understand how they behave and why they exist than to focus on what they’re called.

The goal of an AOI is to point out reasonable areas where buyers or sellers may be staging, as is typical with support and resistance.

In order to reasonably identify these areas, we look for cause and effect relationships. When considering these relationships, it's easier to understand the placement of the points to define each zone.

(Buyer Examples)

Cause: Strong Buyers step in at Swing Low

Effect: Fair Value Gap Forms

Cause: Sustained Buying Pressure

Effect: Market Structure Breaks

In this example, The zone is drawn from the Swing Low, to the Bottom of the FVG closest to the swing point.

In theory, the participation at the swing point was strong and aggressive enough to create the FVG imbalance. Which then found acceptance and continued into a Market Structure Break. So with these AOIs, we are trying to locate the aggressive Buyers or Sellers which were positioned BEFORE the FVG.

These Zones are intended to act as areas to look for reactions from market participants, to judge where price may be going. When revisiting these zones, we look for a reaction or a break, to further provide us information to if the buyers or sellers are still there.

As seen in the screenshot above, The information we gain is not from the creation of these zones, but from the behavior we witness when these zones are revisited.

Technical Note: In this indicator, Market Structure Breaks are only considered when price closes outside the recent swing points. Wicks are not considered as confirmation, therefore are not used to detect structural breaks.

Inside each AOI you can optionally display a readout of the volume which accumulated during the time starting at the swing point and going until the closing bar of the FVG.

Note: We are counting volume until the closing bar of the FVG since the FVG is a 3 bar formation, and aggressive volume is required throughout to create the imbalance.

There are multiple FVGs that typically occur in a single direction, but we do not look to every single one to be indicative of structure, only the first FVG in the opposite direction of the previous direction (which is determined by previous FVGs)

You will probably notice, the AOIs do not form from the closest swing or FVG to the break, this is because we are targeting larger directional changes to draw these AOIs from.

Since they do not always happen perfectly every time, the AOI formation waits for an FVG to occur AND a Market structure break to happen. One without the other will result in no Zone displaying.

> Reflection Lines

While they may seem slightly redundant, Reflection Lines serve as reminders of previous support and resistance pivots. They are drawn at the same Pivots where and AOI is formed, and extend beyond the mitigation of the AOI.

These lines are often points of price to look for "Support Flips", a re-test pattern where price trades through previous support (or resistance) then returns to it and rejects, continuing into a larger move or trend.

Their namesake is based on the behavior of price, "reflecting" at these levels.

The Reflection lines are simple and change color based on price's location.

If price is above, we would typically look to a reflection line in with support in mind.

As a basic filter, these lines use an average price to determine their color, this way they will not change their color as frequently in choppy situations.

> Session Start/End Lines

For analysis purposes and trade review, it is helpful to analyze with context.

For that reason, I have implemented start and end session lines into the indicator, these are helpful when reviewing historical charts to not provide additional context.

By default, they are set to the NYSE Session, but can be changed to fit any needs.

These lines are not advanced, and simply draw a line as the chart passes the start and end of the sessions. It's very likely that you may need to adjust the session for your specific needs.

Note: The Timezone can be adjusted within the code if needed. By Default, the indicator uses "America/New_York" Timezone.

> Conclusion

If you’ve ever felt like your structure tools were confusing or lagging, drawing zones too late, or zones that simply don't make sense, this should feel like a breath of fresh air.

By removing arbitrary length settings and instead using FVGs to define structure and as a basis for AOIs, you're getting a more accurate look at what price is doing and where it's reacting from.

This indicator is rule-based, reactive, and aims to keep things logical without fluff or false confidence.

Enjoy!

TextLibrary "Text"

library to format text in different fonts or cases plus a sort function.

🔸 Credits and Usage

This library is inspired by the work of three authors (in chronological order of publication date):

Unicode font function - JD - Duyck

UnicodeReplacementFunction - wlhm

font - kaigouthro

🔹 Fonts

Besides extra added font options, the toFont(fromText, font) method uses a different technique. On the first runtime bar (whether it is barstate.isfirst , barstate.islast , or between) regular letters and numbers and mapped with the chosen font. After this, each character is replaced using the build-in key - value pair map function .

Also an enum Efont is included.

Note: Some fonts are not complete, for example there isn't a replacement for every character in Superscript/Subscript.

Example of usage (besides the included table example):

import fikira/Text/1 as t

i_font = input.enum(t.Efont.Blocks)

if barstate.islast

sentence = "this sentence contains words"

label.new(bar_index, 0, t.toFont(fromText = sentence, font = str.tostring(i_font)), style=label.style_label_lower_right)

label.new(bar_index, 0, t.toFont(fromText = sentence, font = "Circled" ), style=label.style_label_lower_left )

label.new(bar_index, 0, t.toFont(fromText = sentence, font = "Wiggly" ), style=label.style_label_upper_right)

label.new(bar_index, 0, t.toFont(fromText = sentence, font = "Upside Latin" ), style=label.style_label_upper_left )

🔹 Cases

The script includes a toCase(fromText, case) method to transform text into snake_case, UPPER SNAKE_CASE, kebab-case, camelCase or PascalCase, as well as an enum Ecase .

Example of usage (besides the included table example):

import fikira/Text/1 as t

i_case = input.enum(t.Ecase.camel)

if barstate.islast

sentence = "this sentence contains words"

label.new(bar_index, 0, t.toCase(fromText = sentence, case = str.tostring(i_case)), style=label.style_label_lower_right)

label.new(bar_index, 0, t.toCase(fromText = sentence, case = "snake_case" ), style=label.style_label_lower_left )

label.new(bar_index, 0, t.toCase(fromText = sentence, case = "PascalCase" ), style=label.style_label_upper_right)

label.new(bar_index, 0, t.toCase(fromText = sentence, case = "SNAKE_CASE" ), style=label.style_label_upper_left )

🔹 Sort

The sort(strings, order, sortByUnicodeDecimalNumbers) method returns a sorted array of strings.

strings: array of strings, for example words = array.from("Aword", "beyond", "Space", "salt", "pepper", "swing", "someThing", "otherThing", "12345", "_firstWord")

order: "asc" / "desc" (ascending / descending)

sortByUnicodeDecimalNumbers: true/false; default = false

_____

• sortByUnicodeDecimalNumbers: every Unicode character is linked to a Unicode Decimal number ( wikipedia.org/wiki/List_of_Unicode_characters ), for example:

1 49

2 50

3 51

...

A 65

B 66

...

S 83

...

_ 95

` 96

a 97

b 98

...

o 111

p 112

q 113

r 114

s 115

...

This means, if we sort without adjusting ( sortByUnicodeDecimalNumbers = true ), in ascending order, the letter b (98 - small) would be after S (83 - Capital).

By disabling sortByUnicodeDecimalNumbers , Capital letters are intermediate transformed to str.lower() after which the Unicode Decimal number is retrieved from the small number instead of the capital number. For example S (83) -> s (115), after which the number 115 is used to sort instead of 83.

Example of usage (besides the included table example):

import fikira/Text/1 as t

if barstate.islast

aWords = array.from("Aword", "beyond", "Space", "salt", "pepper", "swing", "someThing", "otherThing", "12345", "_firstWord")

label.new(bar_index, 0, str.tostring(t.sort(strings= aWords, order = 'asc' , sortByUnicodeDecimalNumbers = false)), style=label.style_label_lower_right)

label.new(bar_index, 0, str.tostring(t.sort(strings= aWords, order = 'desc', sortByUnicodeDecimalNumbers = false)), style=label.style_label_lower_left )

label.new(bar_index, 0, str.tostring(t.sort(strings= aWords, order = 'asc' , sortByUnicodeDecimalNumbers = true )), style=label.style_label_upper_right)

label.new(bar_index, 0, str.tostring(t.sort(strings= aWords, order = 'desc', sortByUnicodeDecimalNumbers = true )), style=label.style_label_upper_left )

🔸 Methods/functions

method toFont(fromText, font)

toFont : Transforms text into the selected font

Namespace types: series string, simple string, input string, const string

Parameters:

fromText (string)

font (string)

Returns: `fromText` transformed to desired `font`

method toCase(fromText, case)

toCase : formats text to snake_case, UPPER SNAKE_CASE, kebab-case, camelCase or PascalCase

Namespace types: series string, simple string, input string, const string

Parameters:

fromText (string)

case (string)

Returns: `fromText` formatted to desired `case`

method sort(strings, order, sortByUnicodeDecimalNumbers)

sort : sorts an array of strings, ascending/descending and by Unicode Decimal numbers or not.

Namespace types: array

Parameters:

strings (array)

order (string)

sortByUnicodeDecimalNumbers (bool)

Returns: Sorted array of strings

Risk Distribution HistogramStatistical risk visualization and analysis tool for any ticker 📊

The Risk Distribution Histogram visualizes the statistical distribution of different risk metrics for any financial instrument. It converts risk data into histograms with quartile-based color coding, so that traders can understand their risk, tail-risks, exposure patterns and make data-driven decisions based on empirical evidence rather than assumptions.

The indicator supports multiple risk calculation methods, each designed for different aspects of market analysis, from general volatility assessment to tail risk analysis.

Risk Measurement Methods

Standard Deviation

Captures raw daily price volatility by measuring the dispersion of price movements. Ideal for understanding overall market conditions and timing volatility-based strategies.

Use case: Options trading and volatility analysis.

Average True Range (ATR)

Measures true range as a percentage of price, accounting for gaps and limit moves. Valuable for position sizing across different price levels.

Use case: Position sizing and stop-loss placement.

The chart above illustrates how ATR statistical distribution can be used by looking at the ATR % of price distribution. For example, 90% of the movements are below 5%.

Downside Deviation

Only considers negative price movements, making it ideal for checking downside risk and capital protection rather than capturing upside volatility.

Use case: Downside protection strategies and stop losses.

Drawdown Analysis

Tracks peak-to-trough declines, providing insight into maximum loss potential during different market conditions.

Use case: Risk management and capital preservation.

The chart above illustrates tale risk for the asset (TQQQ), showing that it is possible to have drawdowns higher than 20%.

Entropy-Based Risk (EVaR)

Uses information theory to quantify market uncertainty. Higher entropy values indicate more unpredictable price action, valuable for detecting regime changes.

Use case: Advanced risk modeling and tail-risk.

VIX Histogram

Incorporates the market's fear index directly into analysis, showing how current volatility expectations compare to historical patterns. The CAPITALCOM:VIX histogram is independent from the ticker on the chart.

Use case: Volatility trading and market timing.

Visual Features

The histogram uses quartile-based color coding that immediately shows where current risk levels stand relative to historical patterns:

Green (Q1): Low Risk (0-25th percentile)

Yellow (Q2): Medium-Low Risk (25-50th percentile)

Orange (Q3): Medium-High Risk (50-75th percentile)

Red (Q4): High Risk (75-100th percentile)

The data table provides detailed statistics, including:

Count Distribution: Historical observations in each bin

PMF: Percentage probability for each risk level

CDF: Cumulative probability up to each level

Current Risk Marker: Shows your current position in the distribution

Trading Applications

When current risk falls into upper quartiles (Q3 or Q4), it signals conditions are riskier than 50-75% of historical observations. This guides position sizing and portfolio adjustments.

Key applications:

Position sizing based on empirical risk distributions

Monitoring risk regime changes over time

Comparing risk patterns across timeframes

Risk distribution analysis improves trade timing by identifying when market conditions favor specific strategies.

Enter positions during low-risk periods (Q1)

Reduce exposure in high-risk periods (Q4)

Use percentile rankings for dynamic stop-loss placement

Time volatility strategies using distribution patterns

Detect regime shifts through distribution changes

Compare current conditions to historical benchmarks

Identify outlier events in tail regions

Validate quantitative models with empirical data

Configuration Options

Data Collection

Lookback Period: Control amount of historical data analyzed

Date Range Filtering: Focus on specific market periods

Sample Size Validation: Automatic reliability warnings

Histogram Customization

Bin Count: 10-50 bins for different detail levels

Auto/Manual Bin Width: Optimize for your data range

Visual Preferences: Custom colors and font sizes

Implementation Guide

Start with Standard Deviation on daily charts for the most intuitive introduction to distribution-based risk analysis.

Method Selection: Begin with Standard Deviation

Setup: Use daily charts with 20-30 bins

Interpretation: Focus on quartile transitions as signals

Monitoring: Track distribution changes for regime detection

The tool provides comprehensive statistics including mean, standard deviation, quartiles, and current position metrics like Z-score and percentile ranking.

Enjoy, and please let me know your feedback! 😊🥂

Crowding model ║ BullVision🔬 Overview

The Crypto Crowding Model Pro is a sophisticated analytical tool designed to visualize and quantify market conditions across multiple cryptocurrencies. By leveraging Relative Strength Index (RSI) and Z-score calculations, this indicator provides traders with an intuitive and detailed snapshot of current crypto market dynamics, highlighting areas of extreme momentum, crowded trades, and potential reversal points.

⚙️ Key Concepts

📊 RSI and Z-Score Analysis

RSI (Relative Strength Index) evaluates the momentum and strength of each cryptocurrency, identifying overbought or oversold conditions.

Z-Score Normalization measures each asset's current price deviation relative to its historical average, identifying statistically significant extremes.

🎯 Crowding Analytics

An integrated analytics panel provides real-time crowding metrics, quantifying market sentiment into four distinct categories:

🔥 FOMO (Fear of Missing Out): High momentum, potential exhaustion.

❄️ Fear: Low momentum, potential reversal or consolidation.

📈 Recovery: Moderate upward momentum after a downward trend.

💪 Strength: Stable bullish conditions with sustained momentum.

🖥️ Visual Scatter Plot

Assets are plotted on a dynamic scatter plot, positioning each cryptocurrency according to its RSI and Z-score.

Color coding, symbol shapes, and sizes help quickly identify main market segments (BTC, ETH, TOTAL, OTHERS) and individual asset conditions.

🧩 Quadrant Classification

Assets are categorized into four quadrants based on their momentum and deviation:

Overbought Extended: High RSI and positive Z-score.

Recovery Phase: Low RSI but positive Z-score.

Oversold Compressed: Low RSI and negative Z-score.

Strong Consolidation: High RSI but negative Z-score.

🔧 User Customization

🎨 Visual Settings

Bar Scale: Adjust the scatter plot visual scale.

Asset Visibility: Optionally display key market benchmarks (TOTAL, BTC, ETH, OTHERS).

Gradient Background: Enhances visual interpretation of asset clusters.

Crowding Analytics Panel: Toggle the analytics panel on/off.

📊 Indicator Parameters

RSI Length: Defines the calculation period for RSI.

Z-score Lookback: Historical lookback period for normalization.

Crowding Alert Threshold: Sets alert sensitivity for crowded market conditions.

🎯 Zone Settings

Quadrant Labels: Displays descriptive labels for each quadrant.

Danger Zones: Highlights extreme RSI levels indicative of heightened market risk.

📈 Visual Output

Dynamic Scatter Plot: Visualizes asset positioning clearly and intuitively.

Gradient and Grid: Professional gridlines and subtle gradient backgrounds assist visual assessment.

Danger Zone Highlights: Visually indicates RSI extremes to warn of potential market turning points.

Crowding Analytics Panel: Real-time summary of market sentiment and asset distribution.

🔍 Use Cases

This indicator is particularly beneficial for traders and analysts looking to:

Identify crowded trades and potential reversal points.

Quickly assess overall market sentiment and individual asset strength.

Integrate a robust momentum analysis into broader technical or fundamental strategies.

Enhance market timing and improve risk management decisions.

⚠️ Important Notes

This indicator does not provide explicit buy or sell signals.

It is intended solely for informational, analytical, and educational purposes.

Past performance and signals are not indicative of future market results.

Always combine with additional tools and analysis as part of comprehensive decision-making.

Dynamic Gap Probability ToolDynamic Gap Probability Tool measures the percentage gap between price and a chosen moving average, then analyzes your chart history to estimate the likelihood of the next candle moving up or down. It dynamically adjusts its sample size to ensure statistical robustness while focusing on the exact deviation level.

Originality and Value:

• Combines gap-based analysis with dynamic sample aggregation to balance precision and reliability.

• Automatically extends the sample when exact matches are scarce, avoiding misleading signals on rare extreme moves.

• Provides real “next-candle” probabilities based on historical occurrences rather than fixed thresholds or untested heuristics.

• Adds value by giving traders an evidence-based edge: you see how similar past deviations actually played out.

How It Works:

1. Calculate gap = (close – moving average) / moving average * 100.

2. Round the absolute gap to nearest percent (X%).

3. Count historical bars where gap ≥ X% above or ≤ –X% below.

4. If exact X% count is below the minimum occurrences threshold, include gaps at X+1%, X+2%, etc., until threshold is reached.

5. Compute “next-candle” green vs. red probabilities from the aggregated sample.

6. Display current gap, sample size, green probability, and red probability in a table.

Inputs:

• Moving Average Type (SMA, EMA, WMA, VWMA, HMA, SMMA, TMA)

• Moving Average Period (default 200)

• Minimum Occurrences Threshold (default 50)

• Table position and styling options

Examples:

• If price is 3% above the 200-period SMA and 120 occurrences ≥3% are found, with 84 green next candles (70%) and 36 red (30%), the script displays “3% | 120 | 70% green | 30% red.”

• If price is 8% below the SMA but only 20 exact matches exist, the script will include 9% and 10% gaps until it reaches 50 samples, then calculate probabilities from that broader set.

Why It’s Useful:

• Mean-reversion traders see green-probability signals at extreme overbought or oversold levels.

• Trend-followers identify continuation likelihood when red probability is high.

• Risk managers gauge reliability by inspecting sample size before acting on any signal.

Limitations:

• Historical probabilities do not guarantee future performance.

• Results depend on timeframe and symbol, backtest with your data before trading.

• Use realistic slippage and commission when overlaying on strategy scripts.

EVaR Indicator and Position SizingThe Problem:

Financial markets consistently show "fat-tailed" distributions where extreme events occur with higher frequency than predicted by normal distributions (Gaussian or even log-normal). These fat tails manifest in sudden price crashes, volatility spikes, and black swan events that traditional risk measures like volatility can underestimate. Standard deviation and conventional VaR calculations assume normally distributed returns, leaving traders vulnerable to severe drawdowns during market stress.

Cryptocurrencies and volatile instruments display particularly pronounced fat-tailed behavior, with extreme moves occurring 5-10 times more frequently than normal distribution models would predict. This reality demands a more sophisticated approach to risk measurement and position sizing.

The Solution: Entropic Value at Risk (EVAR)

EVaR addresses these limitations by incorporating principles from statistical mechanics and information theory through Tsallis entropy. This advanced approach captures the non-linear dependencies and power-law distributions characteristic of real financial markets.

Entropy is more adaptive than standard deviations and volatility measures.

I was inspired to create this indicator after reading the paper " The End of Mean-Variance? Tsallis Entropy Revolutionises Portfolio Optimisation in Cryptocurrencies " by by Sana Gaied Chortane and Kamel Naoui.

Key advantages of EVAR over traditional risk measures:

Superior tail risk capture: More accurately quantifies the probability of extreme market moves

Adaptability to market regimes: Self-calibrates to changing volatility environments

Non-parametric flexibility: Makes less assumptions about the underlying return distribution

Forward-looking risk assessment: Better anticipates potential market changes (just look at the charts :)

Mathematically, EVAR is defined as:

EVAR_α(X) = inf_{z>0} {z * log(1/α * M_X(1/z))}

Where the moment-generating function is calculated using q-exponentials rather than conventional exponentials, allowing precise modeling of fat-tailed behavior.

Technical Implementation

This indicator implements EVAR through a q-exponential approach from Tsallis statistics:

Returns Calculation: Price returns are calculated over the lookback period

Moment Generating Function: Approximated using q-exponentials to account for fat tails

EVAR Computation: Derived from the MGF and confidence parameter

Normalization: Scaled to for intuitive visualization

Position Sizing: Inversely modulated based on normalized EVAR

The q-parameter controls tail sensitivity—higher values (1.5-2.0) increase the weighting of extreme events in the calculation, making the model more conservative during potentially turbulent conditions.

Indicator Components

1. EVAR Risk Visualization

Dynamic EVAR Plot: Color-coded from red to green normalized risk measurement (0-1)

Risk Thresholds: Reference lines at 0.3, 0.5, and 0.7 delineating risk zones

2. Position Sizing Matrix

Risk Assessment: Current risk level and raw EVAR value

Position Recommendations: Percentage allocation, dollar value, and quantity

Stop Parameters: Mathematically derived stop price with percentage distance

Drawdown Projection: Maximum theoretical loss if stop is triggered

Interpretation and Application

The normalized EVAR reading provides a probabilistic risk assessment:

< 0.3: Low risk environment with minimal tail concerns

0.3-0.5: Moderate risk with standard tail behavior

0.5-0.7: Elevated risk with increased probability of significant moves

> 0.7: High risk environment with substantial tail risk present

Position sizing is automatically calculated using an inverse relationship to EVAR, contracting during high-risk periods and expanding during low-risk conditions. This is a counter-cyclical approach that ensures consistent risk exposure across varying market regimes, especially when the market is hyped or overheated.

Parameter Optimization

For optimal risk assessment across market conditions:

Lookback Period: Determines the historical window for risk calculation

Q Parameter: Controls tail sensitivity (higher values increase conservatism)

Confidence Level: Sets the statistical threshold for risk assessment

For cryptocurrencies and highly volatile instruments, a q-parameter between 1.5-2.0 typically provides the most accurate risk assessment because it helps capturing the fat-tailed behavior characteristic of these markets. You can also increase the q-parameter for more conservative approaches.

Practical Applications

Adaptive Risk Management: Quantify and respond to changing tail risk conditions

Volatility-Normalized Positioning: Maintain consistent exposure across market regimes

Black Swan Detection: Early identification of potential extreme market conditions

Portfolio Construction: Apply consistent risk-based sizing across diverse instruments

This indicator is my own approach to entropy-based risk measures as an alterative to volatility and standard deviations and it helps with fat-tailed markets.

Enjoy!

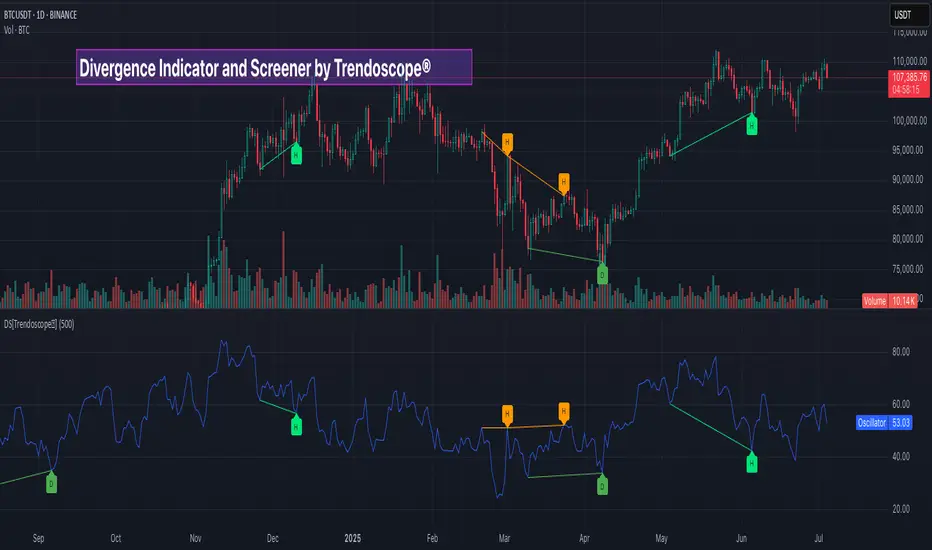

Divergence Screener [Trendoscope®]🎲Overview

The Divergence Screener is a powerful TradingView indicator designed to detect and visualize bullish and bearish divergences, including hidden divergences, between price action and a user-selected oscillator. Built with flexibility in mind, it allows traders to customize the oscillator type, trend detection method, and other parameters to suit various trading strategies. The indicator is non-overlay, displaying divergence signals directly on the oscillator plot, with visual cues such as lines and labels on the chart for easy identification.

This indicator is ideal for traders seeking to identify potential reversal or continuation signals based on price-oscillator divergences. It supports multiple oscillators, trend detection methods, and alert configurations, making it versatile for different markets and timeframes.

🎲Features

🎯Customizable Oscillator Selection

Built-in Oscillators : Choose from a variety of oscillators including RSI, CCI, CMO, COG, MFI, ROC, Stochastic, and WPR.

External Oscillator Support : Users can input an external oscillator source, allowing integration with custom or third-party indicators.

Configurable Length : Adjust the oscillator’s period (e.g., 14 for RSI) to fine-tune sensitivity.

🎯Divergence Detection

The screener identifies four types of divergences:

Bullish Divergence : Price forms a lower low, but the oscillator forms a higher low, signaling potential upward reversal.

Bearish Divergence : Price forms a higher high, but the oscillator forms a lower high, indicating potential downward reversal.

Bullish Hidden Divergence : Price forms a higher low, but the oscillator forms a lower low, suggesting trend continuation in an uptrend.

Bearish Hidden Divergence : Price forms a lower high, but the oscillator forms a higher high, suggesting trend continuation in a downtrend.

🎯Flexible Trend Detection

The indicator offers three methods to determine the trend context for divergence detection:

Zigzag : Uses zigzag pivots to identify trends based on higher highs (HH), higher lows (HL), lower highs (LH), and lower lows (LL).

MA Difference : Calculates the trend based on the difference in a moving average (e.g., SMA, EMA) between divergence pivots.

External Trend Signal : Allows users to input an external trend signal (positive for uptrend, negative for downtrend) for custom trend analysis.

🎯Zigzag-Based Pivot Analysis

Customizable Zigzag Length : Adjust the zigzag length (default: 13) to control the sensitivity of pivot detection.

Repaint Option : Choose whether divergence lines repaint based on the latest data or wait for confirmed pivots, balancing responsiveness and reliability.

🎯Visual and Alert Features

Divergence Visualization : Divergence lines are drawn between price pivots and oscillator pivots, color-coded for easy identification:

Bullish Divergence : Green

Bearish Divergence : Red

Bullish Hidden Divergence : Lime

Bearish Hidden Divergence : Orange

Labels and Tooltips : Labels (e.g., “D” for divergence, “H” for hidden) appear on price and oscillator pivots, with tooltips providing detailed information such as price/oscillator values, ratios, and pivot directions.

Alerts : Configurable alerts for each divergence type (bullish, bearish, bullish hidden, bearish hidden) trigger on bar close, ensuring timely notifications.

🎲 How It Works

🎯Oscillator Calculation

The indicator calculates the selected oscillator (or uses an external source) and plots it on the chart.

Oscillator values are stored in a map for reference during divergence calculations.

🎯Pivot Detection

A zigzag algorithm identifies pivots in the oscillator data, with configurable length and repainting options.

Price and oscillator pivots are compared to detect divergences based on their direction and ratio.

🎯Divergence Identification

The indicator compares price and oscillator pivot directions (HH, HL, LH, LL) to identify divergences.

Trend context is determined using the selected method (Zigzag, MA Difference, or External).

Divergences are classified as bullish, bearish, bullish hidden, or bearish hidden based on price-oscillator relationships and trend direction.

🎯Visualization and Alerts

Valid divergences are drawn as lines connecting price and oscillator pivots, with corresponding labels.

Alerts are triggered for allowed divergence types, providing detailed information via tooltips.

🎯Validation

Divergence lines are validated to ensure no intermediate bars violate the divergence condition, enhancing signal reliability.

🎲 Usage Instructions as Indicator

🎯Add to Chart:

Add the “Divergence Screener ” to your TradingView chart.

The indicator appears in a separate pane below the price chart, plotting the oscillator and divergence signals.

🎯Configure Settings:

Adjust the oscillator type and length to match your trading style.

Select a trend detection method and configure related parameters (e.g., MA type/length or external signal).

Set the zigzag length and repainting preference.

Enable/disable alerts for specific divergence types.

I🎯nterpret Signals:

Bullish Divergence (Green) : Look for potential buy opportunities in a downtrend.

Bearish Divergence (Red) : Consider sell opportunities in an uptrend.

Bullish Hidden Divergence (Lime) : Confirm continuation in an uptrend.

Bearish Hidden Divergence (Orange): Confirm continuation in a downtrend.

Use tooltips on labels to review detailed pivot and divergence information.

🎯Set Alerts:

Create alerts for each divergence type to receive notifications via TradingView’s alert system.

Alerts include detailed text with price, oscillator, and divergence information.

🎲 Example Scenarios as Indicator

🎯 With External Oscillator (Use MACD Histogram as Oscillator)

In order to use MACD as an oscillator for divergence signal instead of the built in options, follow these steps.

Load MACD Indicator from Indicator library

From Indicator settings of Divergence Screener, set Use External Oscillator and select MACD Histograme from the dropdown

You can now see that the oscillator pane shows the data of selected MACD histogram and divergence signals are generated based on the external MACD histogram data.

🎯 With External Trend Signal (Supertrend Ladder ATR)

Now let's demonstrate how to use external direction signals using Supertrend Ladder ATR indicator. Please note that in order to use the indicator as trend source, the indicator should return positive integer for uptrend and negative integer for downtrend. Steps are as follows:

Load the desired trend indicator. In this example, we are using Supertrend Ladder ATR

From the settings of Divergence Screener, select "External" as Trend Detection Method

Select the trend detection plot Direction from the dropdown. You can now see that the divergence signals will rely on the new trend settings rather than the built in options.

🎲 Using the Script with Pine Screener

The primary purpose of the Divergence Screener is to enable traders to scan multiple instruments (e.g., stocks, ETFs, forex pairs) for divergence signals using TradingView’s Pine Screener, facilitating efficient comparison and identification of trading opportunities.

To use the Divergence Screener as a screener, follow these steps:

Add to Favorites : Add the Divergence Screener to your TradingView favorites to make it available in the Pine Screener.

Create a Watchlist : Build a watchlist containing the instruments (e.g., stocks, ETFs, or forex pairs) you want to scan for divergences.

Access Pine Screener : Navigate to the Pine Screener via TradingView’s main menu: Products -> Screeners -> Pine, or directly visit tradingview.com/pine-screener/.

Select Watchlist : Choose the watchlist you created from the Watchlist dropdown in the Pine Screener interface.

Choose Indicator : Select Divergence Screener from the Choose Indicator dropdown.

Configure Settings : Set the desired timeframe (e.g., 1 hour, 1 day) and adjust indicator settings such as oscillator type, zigzag length, or trend detection method as needed.

Select Filter Criteria : Select the condition on which the watchlist items needs to be filtered. Filtering can only be done on the plots defined in the script.

Run Scan : Press the Scan button to display divergence signals across the selected instruments. The screener will show which instruments exhibit bullish, bearish, bullish hidden, or bearish hidden divergences based on the configured settings.

🎲 Limitations and Possible Future Enhancements

Limitations are

Custom input for oscillator and trend detection cannot be used in pine screener.

Pine screener has max 500 bars available.

Repaint option is by default enabled. When in repaint mode expect the early signal but the signals are prone to repaint.

Possible future enhancements

Add more built-in options for oscillators and trend detection methods so that dependency on external indicators is limited

Multi level zigzag support

Logarithmic Moving Average (LMA) [QuantAlgo]🟢 Overview