ETF Leverage VerificationDo leveraged ETFs really return what they promise?

Do they return the exact 2x or 3x? Or a slightly different multiple?

How much do they deviate from the promised leverage multiples?

Do these deviations impact investors in a positive or negative manner?

These are the questions that I want to answer with this indicator.

The ETF Leverage Verification indicator challenges the conventional understanding of leveraged ETFs by measuring how they actually perform versus their theoretical targets.

Instead of assuming leveraged ETFs perfectly track their target multiple, this indicator quantifies the real-world behavior by comparing the expected returns versus the actual results on every trading day.

Key Features

Measures actual versus expected performance of leveraged ETFs

Tracks deviation patterns across thousands of trading days

Identifies asymmetric behavior in up versus down markets

Quantifies beneficial "cushioning effect" during market declines

Provides statistical summary of performance patterns

Works with any leverage factor (2x, 3x, -1x, etc.)

Compatible with all leveraged ETFs (equity, bond, commodity, volatility)

How to Use the Indicator

Enter the Expected Leverage Factor (default: 2.0)

Select the Base Asset (underlying index, e.g., SPX)

Select the Leveraged Asset (leveraged ETF, e.g., SSO)

Understanding the Results

Green markers: Days when the ETF outperformed its expected multiple

Red markers: Days when the ETF underperformed its expected multiple

Data Table:

Positive Deviations: Count of days with better-than-expected performance

Negative Deviations: Count of days with worse-than-expected performance

Avg Deviation: Average magnitude of deviation from expected returns

Frequency Skew: Difference between beneficial deviations in down vs. up markets

Impact: Overall assessment of pattern benefit to investors

Summary Label:

Percentage of positive deviations in up and down markets

Total sample size for statistical significance

Key Patterns to Look For

Positive Deviation in Negative Days:

This occurs when a leveraged ETF falls less than expected during market declines. For example, if SPX falls 1% and a 2x ETF falls only 1.8% (instead of the expected 2%), this creates a +0.2% deviation. This pattern is beneficial as it provides downside protection.

Negative Deviation in Positive Days:

This happens when a leveraged ETF rises less than expected during market advances. For example, if SPX rises 1% and a 2x ETF rises only 1.9% (instead of the expected 2%), this creates a -0.1% deviation. This pattern reduces upside performance.

Frequency Skew:

The most critical metric that measures how much more frequently beneficial deviations occur in down markets compared to up markets. A higher positive skew indicates a stronger asymmetric pattern that helps long-term performance.

Mathematical Background

The indicator computes the deviation between expected and actual performance:

Deviation = Actual Return - Expected Return

Where:

Expected Return = Base Asset Return × Leverage Factor

The deviation is then categorized into four possible outcomes:

Positive deviation on positive market days

Negative deviation on positive market days

Positive deviation on negative market days

Negative deviation on negative market days

In short, more positive deviations are good for investors.

Please feel free to criticize. I'm happy to improve the indicator.

Educational

Tuga SupertrendDescription

This strategy uses the Supertrend indicator enhanced with commission and slippage filters to capture trends on the daily chart. It’s designed to work on any asset but is especially effective in markets with consistent movements.

Use the date inputs to set the backtest period (default: from January 1, 2018, through today, June 30, 2025).

The default input values are optimized for the daily chart. For other timeframes, adjust the parameters to suit the asset you’re testing.

Release Notes

June 30, 2025

• Updated default backtest period to end on June 30, 2025.

• Default commission adjusted to 0.1 %.

• Slippage set to 3 ticks.

• Default slippage set to 3 ticks.

• Simplified the strategy name to “Tuga Supertrend”.

Default Parameters

Parameter Default Value

Supertrend Period 10

Multiplier (Factor) 3

Commission 0.1 %

Slippage 3 ticks

Start Date January 1, 2018

End Date June 30, 2025

Contrarian RSIContrarian RSI Indicator

Pairs nicely with Contrarian 100 MA (optional hide/unhide buy/sell signals)

Description

The Contrarian RSI is a momentum-based technical indicator designed to identify potential reversal points in price action by combining a unique RSI calculation with a predictive range model inspired by the "Contrarian 5 Levels" logic. Unlike traditional RSI, which measures price momentum based solely on price changes, this indicator integrates a smoothed, weighted momentum calculation and predictive price ranges to generate contrarian signals. It is particularly suited for traders looking to capture reversals in trending or range-bound markets.

This indicator is versatile and can be used across various timeframes, though it performs best on higher timeframes (e.g., 1H, 4H, or Daily) due to reduced noise and more reliable signals. Lower timeframes may require additional testing and careful parameter tuning to optimize performance.

How It Works

The Contrarian RSI combines two primary components:

Predictive Ranges (5 Levels Logic): This calculates a smoothed price average that adapts to market volatility using an ATR-based mechanism. It helps identify significant price levels that act as potential support or resistance zones.

Contrarian RSI Calculation: A modified RSI calculation that uses weighted momentum from the predictive ranges to measure buying and selling pressure. The result is smoothed and paired with a user-defined moving average to generate clear signals.

The indicator generates buy (long) and sell (exit) signals based on crossovers and crossunders of user-defined overbought and oversold levels, making it ideal for contrarian trading strategies.

Calculation Overview

Predictive Ranges (5 Levels Logic):

Uses a custom function (pred_ranges) to calculate a dynamic price average (avg) based on the ATR (Average True Range) multiplied by a user-defined factor (mult).

The average adjusts only when the price moves beyond the ATR threshold, ensuring responsiveness to significant price changes while filtering out noise.

This calculation is performed on a user-specified timeframe (tf5Levels) for multi-timeframe analysis.

Contrarian RSI:

Compares consecutive predictive range values to calculate gains (g) and losses (l) over a user-defined period (crsiLength).

Applies a Gaussian weighting function (weight = math.exp(-math.pow(i / crsiLength, 2))) to prioritize recent price movements.

Computes a "wave ratio" (net_momentum / total_energy) to normalize momentum, which is then scaled to a 0–100 range (qrsi = 50 + 50 * wave_ratio).

Smooths the result with a 2-period EMA (qrsi_smoothed) for stability.

Moving Average:

Applies a user-selected moving average (SMA, EMA, WMA, SMMA, or VWMA) with a customizable length (maLength) to the smoothed RSI (qrsi_smoothed) to generate the final indicator value (qrsi_ma).

Signal Generation:

Long Entry: Triggered when qrsi_ma crosses above the oversold level (oversoldLevel, default: 1).

Long Exit: Triggered when qrsi_ma crosses below the overbought level (overboughtLevel, default: 99).

Entry and Exit Rules

Long Entry: Enter a long position when the Contrarian RSI (qrsi_ma) crosses above the oversold level (default: 1). This suggests the asset is potentially oversold and due for a reversal.

Long Exit: Exit the long position when the Contrarian RSI (qrsi_ma) crosses below the overbought level (default: 99), indicating a potential overbought condition and a reversal to the downside.

Customization: Adjust overboughtLevel and oversoldLevel to fine-tune sensitivity. Lower timeframes may benefit from tighter levels (e.g., 20 for oversold, 80 for overbought), while higher timeframes can use extreme levels (e.g., 1 and 99) for stronger reversals.

Timeframe Considerations

Higher Timeframes (Recommended): The indicator is optimized for higher timeframes (e.g., 1H, 4H, Daily) due to its reliance on predictive ranges and smoothed momentum, which perform best with less market noise. These timeframes typically yield more reliable reversal signals.

Lower Timeframes: The indicator can be used on lower timeframes (e.g., 5M, 15M), but signals may be noisier and require additional confirmation (e.g., from price action or other indicators). Extensive backtesting and parameter optimization (e.g., adjusting crsiLength, maLength, or mult) are recommended for lower timeframes.

Inputs

Contrarian RSI Length (crsiLength): Length for RSI momentum calculation (default: 5).

RSI MA Length (maLength): Length of the moving average applied to the RSI (default: 1, effectively no MA).

MA Type (maType): Choose from SMA, EMA, WMA, SMMA, or VWMA (default: SMA).

Overbought Level (overboughtLevel): Upper threshold for exit signals (default: 99).

Oversold Level (oversoldLevel): Lower threshold for entry signals (default: 1).

Plot Signals on Main Chart (plotOnChart): Toggle to display signals on the price chart or the indicator panel (default: false).

Plotted on Lower:

Plotted on Chart:

5 Levels Length (length5Levels): Length for predictive range calculation (default: 200).

Factor (mult): ATR multiplier for predictive ranges (default: 6.0).

5 Levels Timeframe (tf5Levels): Timeframe for predictive range calculation (default: chart timeframe).

Visuals

Contrarian RSI MA: Plotted as a yellow line, representing the smoothed Contrarian RSI with the applied moving average.

Overbought/Oversold Lines: Red line for overbought (default: 99) and green line for oversold (default: 1).

Signals: Blue circles for long entries, white circles for long exits. Signals can be plotted on the main chart (plotOnChart = true) or the indicator panel (plotOnChart = false).

Usage Notes

Use the indicator in conjunction with other tools (e.g., support/resistance, trendlines, or volume) to confirm signals.

Test extensively on your chosen timeframe and asset to optimize parameters like crsiLength, maLength, and mult.

Be cautious with lower timeframes, as false signals may occur due to market noise.

The indicator is designed for contrarian strategies, so it works best in markets with clear reversal patterns.

Disclaimer

This indicator is provided for educational and informational purposes only. Always conduct thorough backtesting and risk management before using any indicator in live trading. The author is not responsible for any financial losses incurred.

Open Range Breakout (ORB) with Alerts

🚀 ChartsAlgo – Open Range Breakout (ORB) with Alerts

The Open Range Breakout (ORB) Indicator by ChartsAlg is designed for intraday traders looking to capitalize on price movements after the market’s opening range. This tool is especially effective for futures (MNQ, MES) and high-volatility stocks or crypto where initial volatility sets the tone for the session.

This indicator identifies a user-defined opening range window, plots the high/low lines of that range, and visually alerts users when price breaks out above or below the range — with options to customize breakout repetitions, background fill, and alerts.

💡 What is an Open Range Breakout (ORB)?

The opening range represents the high and low established during the first few minutes of the trading session — usually 15 or 30 minutes. Many intraday strategies are based on the idea that breaking out of this initial range often signals strong momentum and trend continuation.

Traders often enter:

Long when price breaks above the range high.

Short when price breaks below the range low.

⚙️ How It Works

You define a session window (e.g., 09:30–09:45 EST).

The indicator tracks the high and low during this time.

Once the session ends, the high and low become your range breakout levels.

The indicator then:

Plots lines for visual clarity

Optionally fills background between the range

Triggers breakout signals if price crosses the levels

Provides alerts when breakouts occur

🛠️ Settings Breakdown

🔹 Session Settings

Range Session: Set your preferred window (e.g., 0930–0945). Can be premarket, first 30 mins, or any custom time.

Time zone: Use "America/New York" for EST (default) or change to "GMT+0" for international traders.

🔹 Breakout Settings

Bullish Breakout Signals: Number of allowed breakout alerts above the range.

Bearish Breakout Signals: Number of allowed breakout alerts below the range.

This prevents repeated alerts once breakout has been confirmed.

🔹 Display Settings

Show Background Fill: Fills area between high/low of the range for easier visual analysis.

Show Breakout Signals: Triangle markers plotted on the chart when breakouts happen.

Only Show Today’s Range: Keeps the chart clean by showing only the most current day’s range.

🔹 Color Settings

Range High/Low Line Colors: Choose any color for clarity.

Range Fill Color: Customize the highlight area for your chart style.

📊 Chart Features

Range High/Low Lines: Automatically plotted after range session ends.

Visual Fill Box: Optional background shading between the opening range.

Triangle Breakout Markers: Appear at the breakout candle.

Alerts: Can be used with TradingView’s alert system to notify you of breakouts in real-time.

🔔 Alerts

Two alert conditions are built in:

Bullish Breakout: Triggers when price breaks above the high of the range.

Bearish Breakout: Triggers when price breaks below the low of the range.

Example Alert Message:

📈 “Bullish Breakout above Open Range on AAPL!”

To activate:

Click “🔔 Alerts” on TradingView.

Set condition to this script.

Choose “ORB Breakout Up” or “ORB Breakout Down”.

Choose alert frequency and notification method.

⚠️ DISCLAIMER

ChartsAlgo tools are for informational and educational purposes only.

They are not financial advice or signals. Past performance does not guarantee future results. Use at your own risk and always implement solid risk management.

By using this indicator, you agree that you are solely responsible for any trades or decisions made based on the information provided.

ALP AT + KAMA Crossover This indicator is a powerful combination of two adaptive trend-following concepts: the AlphaTrend by Kivanc Ozbilgic and the Kaufman's Adaptive Moving Average (KAMA), often credited to Perry Kaufman (with the specific implementation based on HPotter's interpretation of KAMA).

The primary goal of this indicator is to provide a robust trend detection and dynamic support/resistance system, adapting to market volatility.

How it Works:

AlphaTrend Component: The green/red line is the AlphaTrend. It dynamically adjusts to market volatility (using ATR) and momentum (using MFI or RSI, configurable). It provides faster signals for trend changes.

KAMA Component: The black line is the Kaufman's Adaptive Moving Average. KAMA is designed to filter out market noise during choppy periods and follow the price closely during trending periods, making it a smoother and more reliable long-term trend indicator.

Color-Coded Trend Zones: The AlphaTrend line is color-coded to visually represent the current market condition based on the price's position relative to both AlphaTrend and KAMA:

Strong Uptrend (Lime Green): Price is above both AlphaTrend and KAMA.

Strong Downtrend (Red): Price is below both AlphaTrend and KAMA.

Uptrend Uncertainty (Orange): Price is above KAMA but below AlphaTrend (suggests consolidation or weakening uptrend).

Downtrend Uncertainty (Blue): Price is below KAMA but above AlphaTrend (suggests consolidation or strengthening downtrend within a downtrend).

Gray: Default/unclassified state.

The underlying logic is based on:

Bullish Crossover (Potential Buy Signal): When the AlphaTrend line crosses above the KAMA line.

Bearish Crossover (Potential Sell Signal): When the AlphaTrend line crosses below the KAMA line.

These crossovers indicate a shift in the adaptive trend momentum.

Customization:

Users can customize various parameters in the indicator's settings, including:

AlphaTrend Multiplier and Common Period.

KAMA Lengths and Alpha values.

All the color codes for different trend zones and lines, allowing for full personalization of the visual output.

Disclaimer:

This indicator is for informational and educational purposes only and should not be considered as financial advice. Trading involves substantial risk, and past performance is not indicative of future results. Always conduct your own thorough research and analysis before making any trading or investment decisions. This indicator is NOT a buy/sell/hold recommendation. Use it as a tool to aid your analysis, not as a sole basis for your trades.

MFI Candles MTF TableMFI Candles + Multi-Timeframe Table | by julzALGO

This open-source script visualizes the Money Flow Index (MFI) in a new format — as candles instead of a traditional oscillator line. It provides a clean, volume-driven view of momentum and pressure, ideal for traders seeking more actionable and visual cues than a typical MFI plot.

What Makes It Unique:

• Plots "MFI Candles" — synthetic candles based on smoothed MFI values using a selected timeframe (default: 1D), giving a new way to read volume flow.

• Candles reflect momentum: green if MFI rises, red if it falls.

• Background turns red when MFI is overbought (≥ 80) or green when oversold (≤ 20).

Multi-Timeframe Strength Table:

• Displays MFI values from 15m, 1h, 4h, and 1D timeframes — all in one dashboard.

• Color-coded for quick recognition: 🔴 Overbought, 🟢 Oversold.

• Values are smoothed with linear regression for better clarity.

Custom Settings:

• MFI calculation length

• Smoothing factor

• Candle source timeframe

• Toggle table and OB/OS background

How to Use:

- Use MFI Candles to monitor momentum shifts based on money flow.

- Use the Multi-Timeframe Table to identify when multiple timeframes align — helpful for timing entries and exits.

- Watch the background for extreme conditions (OB/OS) that may signal upcoming reversals or pressure exhaustion.

Happy Trading!

BTC/Fiat Divergence & Spread Monitor📄 BTC/Fiat Divergence & Spread Monitor

This indicator visualizes Bitcoin’s relative performance across multiple fiat currencies and highlights periods of unusual divergence. It helps traders assess which fiat pairs BTC has outperformed or underperformed over a configurable lookback period and monitor the dynamic spread between the strongest and weakest pairs.

Features:

Relative Performance Matrix:

Ranks BTC returns in 6 fiat pairs, displaying a color-coded table of percentage changes and ranks.

Divergence Spread Oscillator:

Calculates the spread between the top and bottom performing pairs and normalizes this using a Z-Score. The oscillator helps identify when fiat pricing divergence is unusually high or compressed.

Dynamic Smoothing:

Optional Hull Moving Average smoothing to reduce noise in the spread signal.

Customizable Inputs:

Lookback period for percent change.

Z-Score normalization window.

Smoothing length.

Symbol selection for each fiat pair.

Visual Mode Toggle:

Switch between relative performance lines and spread oscillator view.

Potential Use Cases:

Fiat Rotation:

Identify which fiat is relatively weak or strong to optimize your exit currency when taking BTC profits.

Volatility Detection:

Use the spread Z-Score to detect periods of high divergence across fiat pairs, signaling macro FX volatility or dislocations.

Regime Analysis:

Track when fiat spreads are converging or expanding, potentially signaling market regime shifts.

Risk Management:

When divergence is extreme (Z-Score > +1), consider reducing position sizing or waiting for reversion.

Disclaimer:

This indicator is provided for educational and informational purposes only. It does not constitute financial advice or a recommendation to buy or sell any security or asset. Always do your own research and consult a qualified financial professional before making trading decisions. Use at your own risk.

Tip:

Experiment with different lookback periods and smoothing settings to adapt the indicator to your timeframe and trading style.

Volume Overbought/Oversold Zones📊 What You’ll See on the Chart

Red Background or Red Triangle ABOVE a Candle

🔺 Means: Overbought Volume

→ Volume on that bar is much higher than average (as defined by your settings).

→ Suggests strong activity, possible exhaustion in the trend or an emotional spike.

→ It’s a warning: consider watching for signs of reversal, especially if price is already stretched.

Green Background or Green Triangle BELOW a Candle

🔻 Means: Oversold Volume

→ Volume on that bar is much lower than normal.

→ Suggests the market may be losing momentum, or few sellers are left.

→ Could signal an upcoming reversal or recovery if confirmed by price action.

Orange Line Below the Candles (Volume Moving Average)

📈 Shows the "normal" average volume over the last X candles (default is 20).

→ Helps you visually compare each bar’s volume to the average.

Gray Columns (Actual Volume Bars)

📊 These are your regular volume bars — they rise and fall based on how active each candle is.

🔍 What This Indicator Does (In Simple Words)

This indicator looks at trading volume—which is how many shares/contracts were traded in a given period—and compares it to what's considered "normal" for recent history. When volume is unusually high or low, it highlights those moments on the chart.

It tells you:

• When volume is much higher than normal → market might be overheated or experiencing a buying/selling frenzy.

• When volume is much lower than normal → market might be quiet, potentially indicating lack of interest or indecision.

These conditions are marked visually, so you can instantly spot them.

💡 How It Helps You As a Trader

1. Spotting Exhaustion in Trends (Overbought Signals)

If a market is going up and suddenly volume spikes way above normal, it may mean:

• The move is getting crowded (lots of buyers are already in).

• A reversal or pullback could be near because smart money may be taking profits.

Trading idea: Wait for high-volume up bars, then look for price weakness to consider a short or exit.

2. Identifying Hidden Opportunities (Oversold Signals)

If price is falling but volume drops unusually low, it might mean:

• Panic is fading.

• Sellers are losing energy.

• A bounce or trend reversal could happen soon.

Trading idea: After a volume drop in a downtrend, watch for bullish price patterns or momentum shifts to consider a buy.

3. Confirming or Doubting Breakouts

Volume is critical for confirming breakouts:

• If price breaks a key level with strong volume, it's more likely to continue.

• A breakout without volume could be a fake-out.

This indicator highlights volume surges that can help you confirm such moves.

📈 How to Use It in Practice

• Combine it with candlestick patterns, support/resistance, or momentum indicators.

• Use the background colors or shapes as a visual cue to pause and analyze.

• Adjust the sensitivity to suit fast-moving markets (like crypto) or slow ones (like large-cap stocks).

Previous 2 Days High/LowCan you give me a summary of this indicator

The "Previous 2 Days High/Low" indicator, written in Pine Script v5 for TradingView, plots horizontal lines representing the combined high and low prices of the previous two trading days on a chart. Here's a summary of its functionality, purpose, and key features:

Purpose

The indicator helps traders identify significant price levels by displaying the highest high and lowest low from the previous two days, which can act as potential support or resistance levels. These levels are plotted as lines that extend across the current trading day, making it easier to visualize key price zones for trading decisions.

Key Features

Calculates Combined High and Low:

Retrieves the high and low prices of the previous day and the day before using request.security on the daily timeframe ("D").

Computes the combined high as the maximum of the two days' highs and the combined low as the minimum of the two days' lows.

Dynamic Line Plotting:

Draws two horizontal lines:

Red Line: Represents the combined high, plotted at the highest price of the previous two days.

Green Line: Represents the combined low, plotted at the lowest price of the previous two days.

Lines are created at the start of a new trading day and extended to the right edge of the chart using line.set_x2, ensuring they span the entire current day.

Labels for Clarity:

Adds labels to the right of the chart, displaying the exact price values of the combined high ("Combined High: ") and combined low ("Combined Low: ").

Labels are updated to move with the lines, maintaining alignment at the current bar.

Clutter Prevention:

Deletes old lines and labels at the start of each new trading day to avoid overlapping or excessive objects on the chart.

Dynamic Requests:

Uses dynamic_requests=true in the indicator() function to allow request.security calls within conditional blocks (if ta.change(time("D"))), enabling daily data retrieval within the script's logic.

Bollinger Bands Entry/Exit ThresholdsBollinger Bands Entry/Exit Thresholds

Author of enhancements: chuckaschultz

Inspired and adapted from the original 'Bollinger Bands Breakout Oscillator' by LuxAlgo

Overview

Pairs nicely with Contrarian 100 MA

The Bollinger Bands Entry/Exit Thresholds is a powerful momentum-based indicator designed to help traders identify potential entry and exit points in trending or breakout markets. By leveraging Bollinger Bands, this indicator quantifies price deviations from the bands to generate bullish and bearish momentum signals, displayed as an oscillator. It includes customizable entry and exit signals based on user-defined thresholds, with visual cues plotted either on the oscillator panel or directly on the price chart.

This indicator is ideal for traders looking to capture breakout opportunities or confirm trend strength, with flexible settings to adapt to various markets and trading styles.

How It Works

The Bollinger Bands Entry/Exit Thresholds calculates two key metrics:

Bullish Momentum (Bull): Measures the extent to which the price exceeds the upper Bollinger Band, expressed as a percentage (0–100).

Bearish Momentum (Bear): Measures the extent to which the price falls below the lower Bollinger Band, also expressed as a percentage (0–100).

The indicator generates:

Long Entry Signals: Triggered when the bearish momentum (bear) crosses below a user-defined Long Threshold (default: 40). This suggests weakening bearish pressure, potentially indicating a reversal or breakout to the upside.

Exit Signals: Triggered when the bullish momentum (bull) crosses below a user-defined Sell Threshold (default: 80), indicating a potential reduction in bullish momentum and a signal to exit long positions.

Signals are visualized as tiny colored dots:

Long Entry: Blue dots, plotted either at the bottom of the oscillator or below the price bar (depending on user settings).

Exit Signal: White dots, plotted either at the top of the oscillator or above the price bar.

Calculation Methodology

Bollinger Bands:

A user-defined Length (default: 14) is used to calculate an Exponential Moving Average (EMA) of the source price (default: close).

Standard deviation is computed over the same length, multiplied by a user-defined Multiplier (default: 1.0).

Upper Band = EMA + (Standard Deviation × Multiplier)

Lower Band = EMA - (Standard Deviation × Multiplier)

Bull and Bear Momentum:

For each bar in the lookback period (length), the indicator calculates:

Bullish Momentum: The sum of positive deviations of the price above the upper band, normalized by the total absolute deviation from the upper band, scaled to a 0–100 range.

Bearish Momentum: The sum of positive deviations of the price below the lower band, normalized by the total absolute deviation from the lower band, scaled to a 0–100 range.

Formula:

bull = (sum of max(price - upper, 0) / sum of abs(price - upper)) * 100

bear = (sum of max(lower - price, 0) / sum of abs(lower - price)) * 100

Signal Generation:

Long Entry: Triggered when bear crosses below the Long Threshold.

Exit: Triggered when bull crosses below the Sell Threshold.

Settings

Length: Lookback period for EMA and standard deviation (default: 14).

Multiplier: Multiplier for standard deviation to adjust Bollinger Band width (default: 1.0).

Source: Input price data (default: close).

Long Threshold: Bearish momentum level below which a long entry signal is generated (default: 40).

Sell Threshold: Bullish momentum level below which an exit signal is generated (default: 80).

Plot Signals on Main Chart: Option to display entry/exit signals on the price chart instead of the oscillator panel (default: false).

Style:

Bullish Color: Color for bullish momentum plot (default: #f23645).

Bearish Color: Color for bearish momentum plot (default: #089981).

Visual Features

Bull and Bear Plots: Displayed as colored lines with gradient fills for visual clarity.

Midline: Horizontal line at 50 for reference.

Threshold Lines: Dashed green line for Long Threshold and dashed red line for Sell Threshold.

Signal Dots:

Long Entry: Tiny blue dots (below price bar or at oscillator bottom).

Exit: Tiny white dots (above price bar or at oscillator top).

How to Use

Add to Chart: Apply the indicator to your TradingView chart.

Adjust Settings: Customize the Length, Multiplier, Long Threshold, and Sell Threshold to suit your trading strategy.

Interpret Signals:

Enter a long position when a blue dot appears, indicating bearish momentum dropping below the Long Threshold.

Exit the long position when a white dot appears, indicating bullish momentum dropping below the Sell Threshold.

Toggle Plot Location: Enable Plot Signals on Main Chart to display signals on the price chart for easier integration with price action analysis.

Combine with Other Tools: Use alongside other indicators (e.g., trendlines, support/resistance) to confirm signals.

Notes

This indicator is inspired by LuxAlgo’s Bollinger Bands Breakout Oscillator but has been enhanced with customizable entry/exit thresholds and signal plotting options.

Best used in conjunction with other technical analysis tools to filter false signals, especially in choppy or range-bound markets.

Adjust the Multiplier to make the Bollinger Bands wider or narrower, affecting the sensitivity of the momentum calculations.

Disclaimer

This indicator is provided for educational and informational purposes only.

Ticker Pulse Meter + Fear EKG StrategyDescription

The Ticker Pulse Meter + Fear EKG Strategy is a technical analysis tool designed to identify potential entry and exit points for long positions based on price action relative to historical ranges. It combines two proprietary indicators: the Ticker Pulse Meter (TPM), which measures price positioning within short- and long-term ranges, and the Fear EKG, a VIX-inspired oscillator that detects extreme market conditions. The strategy is non-repainting, ensuring signals are generated only on confirmed bars to avoid false positives. Visual enhancements, such as optional moving averages and Bollinger Bands, provide additional context but are not core to the strategy's logic. This script is suitable for traders seeking a systematic approach to capturing momentum and mean-reversion opportunities.

How It Works

The strategy evaluates price action using two key metrics:

Ticker Pulse Meter (TPM): Measures the current price's position within short- and long-term price ranges to identify momentum or overextension.

Fear EKG: Detects extreme selling pressure (akin to "irrational selling") by analyzing price behavior relative to historical lows, inspired by volatility-based oscillators.

Entry signals are generated when specific conditions align, indicating potential buying opportunities. Exits are triggered based on predefined thresholds or partial position closures to manage risk. The strategy supports customizable lookback periods, thresholds, and exit percentages, allowing flexibility across different markets and timeframes. Visual cues, such as entry/exit dots and a position table, enhance usability, while optional overlays like moving averages and Bollinger Bands provide additional chart context.

Calculation Overview

Price Range Calculations:

Short-Term Range: Uses the lowest low (min_price_short) and highest high (max_price_short) over a user-defined short lookback period (lookback_short, default 50 bars).

Long-Term Range: Uses the lowest low (min_price_long) and highest high (max_price_long) over a user-defined long lookback period (lookback_long, default 200 bars).

Percentage Metrics:

pct_above_short: Percentage of the current close above the short-term range.

pct_above_long: Percentage of the current close above the long-term range.

Combined metrics (pct_above_long_above_short, pct_below_long_below_short) normalize price action for signal generation.

Signal Generation:

Long Entry (TPM): Triggered when pct_above_long_above_short crosses above a user-defined threshold (entryThresholdhigh, default 20) and pct_below_long_below_short is below a low threshold (entryThresholdlow, default 40).

Long Entry (Fear EKG): Triggered when pct_below_long_below_short crosses under an extreme threshold (orangeEntryThreshold, default 95), indicating potential oversold conditions.

Long Exit: Triggered when pct_above_long_above_short crosses under a profit-taking level (profitTake, default 95). Partial exits are supported via a user-defined percentage (exitAmt, default 50%).

Non-Repainting Logic: Signals are calculated using data from the previous bar ( ) and only plotted on confirmed bars (barstate.isconfirmed), ensuring reliability.

Visual Enhancements:

Optional moving averages (SMA, EMA, WMA, VWMA, or SMMA) and Bollinger Bands can be enabled for trend context.

A position table displays real-time metrics, including open positions, Fear EKG, and Ticker Pulse values.

Background highlights mark periods of high selling pressure.

Entry Rules

Long Entry:

TPM Signal: Occurs when the price shows strength relative to both short- and long-term ranges, as defined by pct_above_long_above_short crossing above entryThresholdhigh and pct_below_long_below_short below entryThresholdlow.

Fear EKG Signal: Triggered by extreme selling pressure, when pct_below_long_below_short crosses under orangeEntryThreshold. This signal is optional and can be toggled via enable_yellow_signals.

Entries are executed only on confirmed bars to prevent repainting.

Exit Rules

Long Exit: Triggered when pct_above_long_above_short crosses under profitTake.

Partial exits are supported, with the strategy closing a user-defined percentage of the position (exitAmt) up to four times per position (exit_count limit).

Exits can be disabled or adjusted via enable_short_signal and exitPercentage settings.

Inputs

Backtest Start Date: Defines the start of the backtesting period (default: Jan 1, 2017).

Lookback Periods: Short (lookback_short, default 50) and long (lookback_long, default 200) periods for range calculations.

Resolution: Timeframe for price data (default: Daily).

Entry/Exit Thresholds:

entryThresholdhigh (default 20): Threshold for TPM entry.

entryThresholdlow (default 40): Secondary condition for TPM entry.

orangeEntryThreshold (default 95): Threshold for Fear EKG entry.

profitTake (default 95): Exit threshold.

exitAmt (default 50%): Percentage of position to exit.

Visual Options: Toggle for moving averages and Bollinger Bands, with customizable types and lengths.

Notes

The strategy is designed to work across various timeframes and assets, with data sourced from user-selected resolutions (i_res).

Alerts are included for long entry and exit signals, facilitating integration with TradingView's alert system.

The script avoids repainting by using confirmed bar data and shifted calculations ( ).

Visual elements (e.g., SMA, Bollinger Bands) are inspired by standard Pine Script practices and are optional, not integral to the core logic.

Usage

Apply the script to a chart, adjust input settings to suit your trading style, and use the visual cues (entry/exit dots, position table) to monitor signals. Enable alerts for real-time notifications.

Designed to work best on Daily timeframe.

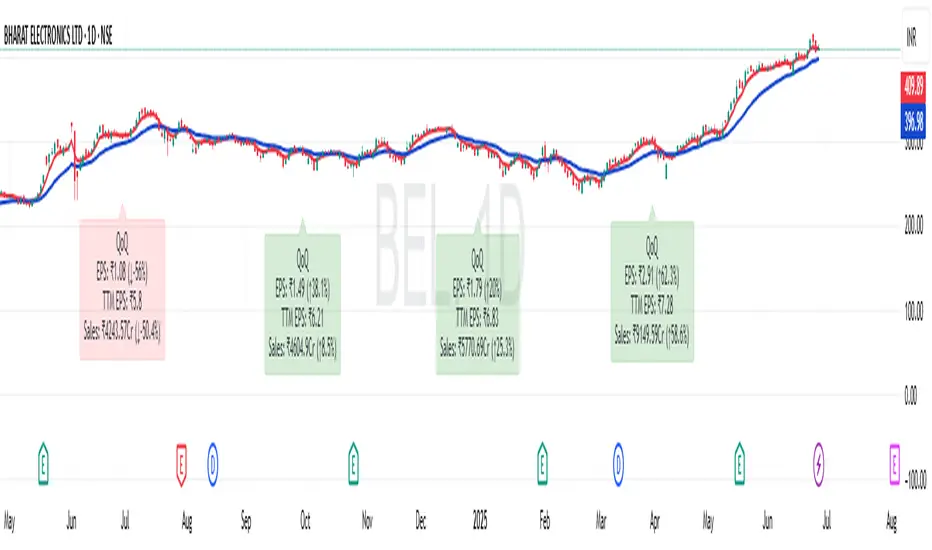

EPS and Sales Magic Indicator V2EPS and Sales Magic Indicator V2

EPS and Sales Magic Indicator V2

Short Title: EPS V2

Author: Trading_Tomm

Platform: TradingView (Pine Script v6)

License: Free for public use under fair usage guidelines

Overview

The EPS and Sales Magic Indicator V2 is a powerful stock fundamental visualization tool built specifically for TradingView users who wish to incorporate earnings intelligence directly onto their price chart. Designed and developed by Trading_Tomm, this upgraded version of the original 'EPS and Sales Magic Indicator' includes an enriched and more insightful presentation of company performance metrics — now with TTM EPS support, advanced color-coding, label sizing, and refined control options.

This indicator is tailored for retail traders, swing investors, and long-term fundamental analysts who need to view Quarter-over-Quarter (QoQ) earnings and revenue changes directly on the price chart without switching tabs or breaking focus.

What Does It Display?

The EPS and Sales Magic Indicator V2 intelligently detects quarterly financial updates and displays the following data points via labels:

1. EPS (Earnings Per Share) – Current Quarterly Value

This is the most recent Diluted EPS published by the company, fetched using TradingView’s request.financial() function.

Displayed in the format: EPS: ₹20.45

2. EPS QoQ Percentage Change

Shows the percentage change in EPS compared to the previous quarter.

Highlights improvement or decline using arrows (up for improvement, down for decline).

Displayed in the format: EPS: ₹20.45 (up 15.3 percent)

3. Sales (Revenue) – Current Quarterly Value

Fetches and displays Total Revenue of the company in ₹Crores for easier Indian-market readability.

Displayed in the format: Sales: ₹460Cr

4. Sales QoQ Percentage Change

Measures and presents the quarter-over-quarter percentage change in total revenue.

Uses arrows to indicate growth or contraction.

Displayed in the format: Sales: ₹460Cr (down 3.8 percent)

5. EPS TTM (Trailing Twelve Months)

You now get the TTM EPS — the sum of the last four quarterly EPS values.

This value provides a better long-term earnings snapshot compared to a single quarter.

Displayed in the format: TTM EPS: ₹78.12

All of these values are automatically calculated and displayed only on the bars where a new financial report is detected, keeping your chart clean and insightful.

Customization Features

This indicator is built with user control in mind, allowing you to personalize how and what you want to see:

Show EPS in Label: Enable or disable the display of EPS and EPS QoQ values.

Show Sales in Label: Toggle the visibility of revenue and sales change percentage.

Color Options for Label Themes: The label background color is automatically determined based on performance.

Green: Both EPS and Sales increased QoQ.

Red: Both decreased.

Orange: One increased and the other decreased.

Gray: Default color (if values are unavailable or mixed).

Label Text Size: Choose from Tiny, Small (default), or Normal.

Visual Design

Placement: The labels are positioned just below the candlesticks using yloc.belowbar, so they do not obstruct price action or interfere with technical indicators.

Anchor: Aligned precisely with the financial reporting bars to maintain clarity in historical comparisons.

Background Style: Clean, semi-transparent styling with soft text colors for comfortable viewing.

How It Works

The indicator relies on TradingView’s powerful request.financial() function to extract fiscal quarterly financials (FQ). Internally, it uses detection logic to identify fresh data updates by comparing current vs. previous values, arithmetic to compute QoQ percentage changes in EPS and Sales, logic to build formatted labels dynamically based on user selections, and conditional color and sizing logic to enhance interpretability.

Use Cases

For Long-Term Investors: Quickly identify if a company’s profitability and revenue are improving over time.

For Swing Traders: Combine recent earnings trends with price action to evaluate if post-result momentum has real backing.

For Technical and Fundamental Traders: Layer it with moving averages, RSI, or volume to create a hybrid analysis environment.

Limitations and Notes

Financial data is provided by TradingView’s financial API, and occasional missing values may occur for less-covered stocks.

This tool does not repaint but depends on the timing of the official financial updates.

All values are rounded and formatted to prioritize readability.

Works best on Daily or higher timeframes (weekly or monthly also supported).

License and Fair Use

This script is free to use and share under TradingView’s open-use guidelines. You may copy, fork, and build upon this indicator for personal or educational purposes, but commercial usage requires attribution to the author: Trading_Tomm.

Future Enhancements (Planned)

Addition of Net Profit (QoQ and TTM)

Inclusion of Operating Margin, Profit Margin, and Book Value

Option to switch between numeric and graphical display (table mode)

Alerts on extreme earnings deviation or sales slumps

Final Thoughts

The EPS and Sales Magic Indicator V2 represents a clean, visual, and smart way to monitor a company’s core performance from your chart screen. It helps you align fundamental strength with technical strategies and provides instant financial clarity, which is especially vital in today’s fast-moving markets.

Whether you’re preparing for an earnings season or scanning past performance to pick your next investment, this indicator saves time, enhances insights, and sharpens decisions.

Price-EMA Z-Score Backgroundhe “Price‑to‑EMA Z‑Score Background” indicator is designed to give you a clear, visual sense of when price has moved unusually far away from its smoothed trend, and to highlight those moments as potential overextension or mean‑reversion opportunities. Under the hood, it first computes a standard exponential moving average (EMA) of your chosen lookback length, then measures the raw difference between the current close and that EMA on every bar. To make that raw deviation comparable across different markets and timeframes, it converts the series of differences into a z‑score—subtracting the rolling mean of the deviations and dividing by their rolling standard deviation over a second lookback window.

Once you’ve normalized price‑to‑EMA distance into z‑score units, you can set two simple trigger levels: one upper threshold and one lower threshold. Whenever the z‑score climbs above the upper threshold, the chart background glows green, signaling that price is extended far above its EMA (and might be ripe for a pullback). Whenever the z‑score falls below the lower threshold, the background turns red, calling out an equally extreme move below the EMA (and a possible oversold bounce). Between those bands, no shading appears, letting you know price is trading within its “normal” range around the trend.

By adjusting the EMA period, the z‑score lookback, and the two trigger levels, you can dial in early warning signals (e.g. ±1 σ) or wait for very stretched moves (±2 σ or more). Used in concert with your favorite momentum or pattern tools—or even as a standalone visual cue—this simple background‑shading approach makes it easy to spot when a market is running too hot or too cold relative to its own recent average.

Yield Curve Regime Shading with LegendTakes two symbols (e.g. two futures contracts, two FX pairs, etc.) as inputs.

Calculates the “regime” as the sign of the change in their difference over an n‑period lookback.

Lets you choose whether you want to color the bars themselves or shade the background.

How it works

Inputs

symbolA, symbolB: the two tickers you’re comparing.

n: lookback in bars to measure the change in the spread.

mode: pick between “Shading” or “Candle Color”.

Data fetching

We use request.security() to pull each series at the chart’s timeframe.

Regime calculation

spread = priceA – priceB

spreadPrev = ta.valuewhen(not na(spread), spread , 0) (i.e. the spread n bars ago)

If spread > spreadPrev → bullish regime

If spread < spreadPrev → bearish regime

Plotting

Shading: apply bgcolor() in green/red.

Candle Color: use barcolor() to override the bar color.

ICT Setup 04 [TradingFinder] SFP Sweep Liquidity Fake CHoCH/BOS🔵 Introduction

In smart money and ICT based trading, liquidity is never random. Some of the most meaningful market moves begin with a liquidity sweep where price intentionally hunts a previous swing high or swing low to trigger stop loss orders and absorb volume.

This manipulation is often followed by a sharp reversal from a reaction zone, creating ideal conditions for a high probability entry. This indicator is built to detect exactly that. It identifies a valid swing point and defines a reaction zone where price is likely to react.

For short setups, the zone lies between the swing high and the maximum of the candle’s open or close. For long setups, it’s drawn from the swing low to the minimum of the open or close.

When price returns to this zone and forms a qualified confirmation candle typically a doji or a small bodied candle that closes inside the zone while sweeping the liquidity this is a potential sign of reversal.

The candle must show both the sweep and the inability to hold above or below the key level, signaling a fake breakout or failed move. By combining elements of liquidity hunt, reaction zone rejection, and candle based entry confirmation, this tool highlights sniper entry points used by smart money to trap retail traders and reverse the trend. It helps filter out noise and enhances timing, making it ideal for trading in alignment with institutional order flow.

Long Position :

Short Position :

🔵 How to Use

This indicator is designed to highlight precise moments where price sweeps liquidity and reacts within a high probability reversal zone. By identifying clean swing highs and lows and defining a smart reaction zone around them, it filters out weak fakeouts and focuses only on setups with strong institutional footprints.

The tool works best when combined with market structure analysis and is suitable for both scalping and intraday trading. Below is a breakdown of how to interpret the signals for long and short positions based on the visual setups provided.

🟣 Long Setup

In a long setup, the indicator first detects a valid swing low where liquidity has likely accumulated below. A reaction zone is then drawn between the swing low and the minimum of the open or close of the swing candle.

When price returns to this zone, it must sweep the previous low and form a precise confirmation candle, such as a doji or a small bodied candle, that closes inside the zone. This candle must also reject the lower level, showing failure to continue downward.

As shown in the chart, once the liquidity grab is complete and the confirmation candle forms, a clean long signal is issued, indicating a potential bullish reversal backed by smart money behavior.

🟣 Short Setup

In a short setup, the indicator identifies a swing high where buy-side liquidity is resting. It then constructs a reaction zone between the high and the maximum of the open or close of the swing candle. Price must return to this zone, sweep the swing high, and form a bearish confirmation candle inside the zone.

A classic example is a doji or rejection candle that traps breakout buyers and fails to hold above the previous high. In the provided chart, the price aggressively hunts the liquidity above the swing high, but the close within the reaction zone signals exhaustion, prompting a short signal with high reversal probability.

These setups represent moments where price action, liquidity behavior, and candle structure align to offer strong entries. By focusing on clean sweeps and reactive confirmations, the indicator helps traders stay on the side of smart money and avoid common breakout traps.

🔵 Settings

🟣 Logical settings

Swing period : You can set the swing detection period.

Max Swing Back Method : It is in two modes "All" and "Custom". If it is in "All" mode, it will check all swings, and if it is in "Custom" mode, it will check the swings to the extent you determine.

Max Swing Back : You can set the number of swings that will go back for checking.

Maximum Distance Between Swing and Signal :The maximum number of candles allowed between the swing point and the potential signal. The default value is 50, ensuring that only recent and relevant price reactions are considered valid.

🟣 Display settings

Displaying or not displaying swings and setting the color of labels and lines.

🟣 Alert Settings

Alert SFP : Enables alerts for Swing Failure Pattern.

Message Frequency : Determines the frequency of alerts. Options include 'All' (every function call), 'Once Per Bar' (first call within the bar), and 'Once Per Bar Close' (final script execution of the real-time bar). Default is 'Once per Bar'.

Show Alert Time by Time Zone : Configures the time zone for alert messages. Default is 'UTC'.

🔵 Conclusion

This indicator is built for traders who rely on liquidity driven setups and smart money principles. By combining swing structure analysis with precision reaction zones and strict entry confirmation, it isolates the exact moments where price sweeps liquidity and fails to continue. These are high value points where institutional activity often reveals itself, and retail traps unfold.

Unlike generic breakout tools, this script focuses on quality over quantity by requiring both a sweep of a swing high or low and a confirmed rejection candle that closes inside a predefined zone. With customizable swing depth, proximity filters, visual highlights, and alert functions, it offers a complete framework for identifying and acting on fake breakouts with confidence. Whether you trade forex, crypto, or indices, this tool enhances your ability to align with true order flow and take entries where liquidity is most likely to shift.

Watermark Clarity V33🌟 Introducing Watermark Clarity V33 – Banner 🌟

Watermark Clarity V33 is a visual utility tool designed to enhance chart awareness, focus, and clean aesthetics without adding market noise. Unlike traditional indicators, this script does not generate buy/sell signals or perform technical analysis. Instead, it provides a customizable on-chart watermark banner that clearly communicates your current mindset, risk awareness, or trading bias directly on the chart — helping traders stay aligned with their pre-defined plans and reducing impulsive behavior.

Whether you’re a discretionary trader, scalper, or swing trader, Watermark Clarity V33 offers an adaptive display that blends clarity with minimalism, keeping your chart clean while remaining informative.

🛠 Customizable Parameters

• Dual Text Banners: Configure two independent headers to reflect trading goals, risk posture, or emotional cues.

• Smart Animation Toggle: Optionally animate between messages to help reinforce shifting market awareness or draw attention during high-alert periods.

• Size, Color & Positioning: Adjust the info box’s text size, banner dimensions, background color, transparency, and placement (top/middle/bottom – left/center/right).

• Transparent Mode: Switch to semi-transparent mode for cleaner overlays during live sessions or screen recording.

🚀 New Feature – Custom Alerts & Smart Animation Control

• Market-Aware Animation Logic:

When Enable Animation is turned on and both Heading 1 and Heading 2 are filled:

• 📈 During Market Hours → The banner alternates smoothly between both headings, helping maintain awareness and visual engagement.

• 💤 Outside Market Hours → The banner remains fixed on Heading 1. This acts as a subtle visual cue that markets are currently closed — giving you peace of mind and a cleaner screen.

✨ Visual Utility Use Cases

• Accountability Layer: Keep yourself accountable to your trading rules or session checklist.

• Mindset Anchor: Display motivational or tactical reminders that guide your trading behavior.

• Multi-Timeframe Syncing: Use different watermarks across charts to stay aligned across timeframes or instruments.

📘 How to Use

1. Add the Indicator: Apply “Watermark Clarity V33 – Banner” to your chart.

2. Configure Inputs: Adjust the banner texts, size, color scheme, and screen position to your liking.

4. Focus & Trade: Let the visual cue support your decision-making environment without interfering with price action.

❗ Important Notes

• This indicator does not analyze price data or generate signals. It is designed solely for visual clarity and trader discipline support.

• All display logic runs in real-time and responds to your settings only, no repainting or lookahead bias.

Initial balance - weeklyWeekly Initial Balance (IB) — Indicator Description

The Weekly Initial Balance (IB) is the price range (High–Low) established during the week’s first trading session (most commonly Monday). You can measure it over the entire day or just the first X hours (e.g. 60 or 120 minutes). Once that session ends, the IB High and IB Low define the key levels where the initial weekly range formed.

Why Measure the Weekly IB?

Week-Opening Sentiment:

Monday’s range often sets the tone for the rest of the week. Trading above the IB High signals bullish control; trading below the IB Low signals bearish control.

Key Liquidity Zones:

Large institutions tend to place orders around these extremes, so you’ll frequently see tests, breakouts, or rejections at these levels.

Support & Resistance:

The IB High and IB Low become natural barriers. Price will often return to them, bounce off them, or break through them—ideal spots for entries and exits.

Volatility Forecast:

The width of the IB (High minus Low) indicates whether to expect a volatile week (wide IB) or a quieter one (narrow IB).

Significance of IB Levels

Breakout:

A clear break above the IB High (for longs) or below the IB Low (for shorts) can ignite a strong trending move.

Fade:

A rejection off the IB High/Low during low momentum (e.g. low volume or pin-bar formations) offers a high-probability reversal trade.

Mid-Point:

The 50% level of the IB range often “magnetizes” price back to it, providing entry points for continuation or reversal strategies.

Three Core Monday IB Strategies

A. Breakout (Open-Range Breakout)

Entry: Wait for 1–2 candles (e.g. 5-minute) to close above IB High (long) or below IB Low (short).

Stop-Loss: A few pips below IB High (long) or above IB Low (short).

Profit-Target: 2–3× your risk (Reward:Risk ≥ 2:1).

Best When: You spot a clear impulse—such as a strong pre-open volume spike or news-driven move.

B. Fade (Reversal at Extremes)

Entry: When price tests IB High but shows weakening momentum (shrinking volume, upper-wick candles), enter short; vice versa for IB Low and longs.

Stop-Loss: Just beyond the IB extreme you’re fading.

Profit-Target: Back toward the IB mid-point (50% level) or all the way to the opposite IB extreme.

Best When: Monday’s action is range-bound and lacks a clear directional trend.

C. Mid-Point Trading

Entry: When price returns to the 50% level of the IB range.

In an up-trend: buy if it bounces off mid-point back toward IB High.

In a down-trend: sell if it reverses off mid-point back toward IB Low.

Stop-Loss: Just below the nearest swing-low (for longs) or above the nearest swing-high (for shorts).

Profit-Target: To the corresponding IB extreme (High or Low).

Best When: You see a strong initial move away from the IB, followed by a pullback to the mid-point.

Usage Steps

Configure your session: Measure IB over your chosen Monday timeframe (whole day or first X hours).

Choose your strategy: Align Breakout, Fade, or Mid-Point entries with the current market context (trend vs. range).

Manage risk: Keep risk per trade ≤ 1% of account and maintain at least a 2:1 Reward:Risk ratio.

Backtest & forward-test: Verify performance over multiple Mondays and in a paper-trading environment before going live.

15m ORB Pip Run with Range HighlightThis marks up the first 15 minute range of the NYSE at 9:30 AM EST.

Then it counts the number of pips that price has run in the direction of the breakout.

The script it not anything amazing.

I just wrote it to help me backtest the 15 minute ORB strategy quickly.

ATR FX DashboardATR FX Dashboard – Multi-Timeframe Volatility Monitor

Overview:

The ATR FX Dashboard provides a quick, at-a-glance view of market volatility across multiple timeframes for any forex pair. It uses the well-known Average True Range (ATR) indicator to display real-time volatility information in both pips and percentage terms, helping traders assess potential risk, position sizing, and market conditions.

How It Works:

This dashboard displays:

✔ ATR in Pips — The average price movement over a given timeframe, converted to pips for easy interpretation, automatically adjusting for JPY pairs.

✔ ATR as a Percentage of Price — Shows how significant the ATR is relative to the current price. Higher percentages often signal higher volatility or more active markets.

✔ Color-Coded Volatility Highlights — On the daily timeframe, ATR % cells are color-coded:

Green: High volatility

Orange: Moderate volatility

Red: Low volatility

Timeframes Displayed:

15 Minutes

1 Hour

4 Hour

Daily

This gives traders a clear, multi-timeframe view of short-term and broader market volatility conditions, directly on the chart.

Ideal For:

✅ Forex traders seeking quick, reliable volatility reference points

✅ Day traders and swing traders needing help with risk assessment and position sizing

✅ Anyone using ATR-based strategies or simply wanting to stay aware of changing market conditions

Additional Features:

Toggle option to display or hide ATR % relative to price

Automatic pip conversion for JPY pairs

Simple, clean table layout in the bottom-right corner of the chart

Supports all forex symbols

Disclaimer:

This tool is for informational purposes only and is not financial advice. As with all technical indicators, it should be used in conjunction with other tools and proper risk management.

S4_IBS_Mean_Rev_3candleExitOverview:

This is a rules-based, mean reversion strategy designed to trade pullbacks using the Internal Bar Strength (IBS) indicator. The system looks for oversold conditions based on IBS, then enters long trades , holding for a maximum of 3 bars or until the trade becomes profitable.

The strategy includes:

✅ Strict entry rules based on IBS

✅ Hardcoded exit conditions for risk management

✅ A clean visual table summarizing key performance metrics

How It Works:

1. Internal Bar Strength (IBS) Setup:

The IBS is calculated using the previous bar’s price range:

IBS = (Previous Close - Previous Low) / (Previous High - Previous Low)

IBS values closer to 0 indicate price is near the bottom of the previous range, suggesting oversold conditions.

2. Entry Conditions:

IBS must be ≤ 0.25, signaling an oversold setup.

Trade entries are only allowed within a user-defined backtest window (default: 2024).

Only one trade at a time is permitted (long-only strategy).

3. Exit Conditions:

If the price closes higher than the entry price, the trade exits with a profit.

If the trade has been open for 3 bars without showing profit, the trade is forcefully exited.

All trades are closed automatically at the end of the backtest window if still open.

Additional Features:

📊 A real-time performance metrics table is displayed on the chart, showing:

- Total trades

- % of profitable trades

- Total P&L

- Profit Factor

- Max Drawdown

- Best/Worst trade performance

📈 Visual markers indicate trade entries (green triangle) and exits (red triangle) for easy chart interpretation.

Who Is This For?

This strategy is designed for:

✅ Traders exploring systematic mean reversion approaches

✅ Those who prefer strict, rules-based setups with no subjective decision-making

✅ Traders who want built-in performance tracking directly on the chart

Note: This strategy is provided for educational and research purposes. It is a backtested model and past performance does not guarantee future results. Users should paper trade and validate performance before considering real capital.

Gap % Distribution Table (2% Bins)Description

This indicator displays a Gap % Distribution Table categorized in 2% bins ranging from `< -20%` to `> +20%`. It calculates the gap between today’s open and the previous day’s close, and groups occurrences into defined bins. The table includes:

Gap range, count, and percentage for each bin

A total row summarizing all entries

Customizable appearance including:

Font color, cell background fill (with transparency), and table border color

Column headers and full outer border

Date filtering using selectable start and end dates

Position control for placing the table on the chart area

Ideal for analyzing the historical behavior of opening gaps for any instrument.

80% Rule Indicator (ETH Session + SVP Prior Session)I created this script to show the 80% opportunity on chart if setting lines up.

"80% rule: Open outside the vah or Val. Spend 30 mins outside there then break back inside spend 15 mins below or above depending which way u broke. Then come back and retest the vah/val and take it to the poc as a first target with the final target being the other Val/vah "

📌 Script Summary

The "80% Rule Indicator (ETH Session + SVP Prior Session)" overlays your chart with prior session value area levels (VAH, VAL, and POC) calculated from extended-hours 30-minute data. It tracks when the price reenters the value area and confirms 80% Rule setups during your chosen trading session. You can optionally trigger alerts, show/hide market sessions, and fine-tune line appearance for a clean, modular workflow.

⚙️ Options & Settings Breakdown

- Use 24-Hour Session (All Markets)

When checked, the indicator ignores time zones and tracks signals during a full 24-hour period (0000-0000), helpful if you're outside U.S. trading hours or want consistent behavior globally.

- Market Session

Dropdown to select one of three key market zones:

- New York (09:30–16:00 ET)

- London (08:00–16:30 local)

- Tokyo (09:00–15:00 local)

Used to gate entry signals during relevant hours unless you choose the 24-hour option.

- Show PD VAH/VAL/POC Lines

Toggle to show or hide prior day’s levels (based on the 30-min extended session). Turning this off removes both the lines and their white text labels.

- Extend Lines Right

When enabled, the VAH/VAL/POC lines extend into the current day’s session. If disabled, they appear only at their anchor point.

- Highlight Selected Session

Adds a soft blue background to help visualize the active session you selected.

- Enable Alert Conditions

Allows TradingView alerts to be created for long/short 80% Rule entries.

- Enable Audible Alerts

Plays an in-chart sound with a popup message (“80% Rule LONG” or “SHORT”) when signals trigger. Requires the chart to be active and sounds enabled in TradingView.

Universal Sentiment Oscillator with Trade RecommendationsUniversal Sentiment Oscillator & Strategy Guide

Summary

This all-in-one indicator is designed to be a comprehensive co-pilot for your trading journey. It moves beyond simple buy/sell signals by analyzing the underlying market sentiment and providing a dynamic, risk-assessed guide of potential trading strategies. Whether you're a novice learning the ropes or an expert seeking confirmation, this tool provides a structured framework for making smarter, more informed decisions in stocks, options, and futures.

How It Works

The core of the indicator is the Sentiment Oscillator, which calculates a score from -5 (Extremely Bearish) to +5 (Extremely Bullish) on every bar. This isn't just a single measurement; it's a weighted aggregate of several key technical conditions:

Trend Analysis: Price position relative to the 20, 50, and 200 EMAs.

Momentum Analysis: The current RSI value.

Hybrid Analysis: The state of the MACD and its signal line.

These factors are intelligently combined and normalized to produce a single, intuitive sentiment score, giving you an at-a-glance understanding of the market's pulse.

Core Features

Dynamic Trade Recommendation Table:

The informational heart of the indicator. This on-chart table provides a list of potential trades perfectly aligned with the current sentiment score.

Risk-Ranked Strategies:

All suggested trades are logically ordered by risk, helping you quickly identify strategies that match your comfort level.

Adjusted Trade Suggestions:

The indicator analyzes sentiment momentum (the score vs. its signal line) to provide proactive, forward-looking trade ideas based on where the market might be heading next.

Customizable Trading Styles:

Tell the indicator if you are a Conservative, Neutral, or Aggressive trader, and the "Adjusted Trade Suggestion" will automatically tailor its recommendations to your personal risk preference.

Context-Aware Futures Mode:

When viewing a futures contract, enable this mode to switch all recommendations from stock/options to futures-specific actions (e.g., "Cautious Long," "Monitor Range").

Predictive Sentiment Cone:

Visualize the potential short-term path of sentiment based on current momentum, helping you anticipate future conditions.

Fully Customizable:

Every parameter—from EMA lengths to trade filters—can be adjusted, allowing you to fine-tune the indicator to your exact specifications.

How to Use This Indicator

This tool is flexible and can be integrated into many trading systems. Here is a powerful, professional approach:

Top-Down Analysis (for Swing or Position Trading):

Establish the Trend: Start on the higher timeframes (Monthly, Weekly, Daily). Use the oscillator's color and score to define the dominant, long-term market sentiment. You only want to look for trades that align with this macro trend.

Refine the Entry: Drop down to the medium timeframes (4-Hour, 1-Hour). Wait for the sentiment on these charts to come into alignment with the higher-timeframe trend. This pullback or consolidation is your "zone of interest."

Pinpoint the Execution: Move to a lower timeframe (e.g., 15-Minute). Use the Adjusted Trade Suggestion and Sentiment Momentum to find a precise entry as momentum begins to shift back in the direction of the primary trend. You can set alerts on the oscillator's zero-line for early warnings of a sentiment shift.

As a Confirmation Tool: If you have an existing trade idea, use the indicator to validate it. Does the sentiment score align with your bullish or bearish thesis? Does the momentum confirm that now is a good time to enter?

As an Idea Generation Tool: Unsure what to trade? Browse different assets and let the indicator's "Primary Trades" and "Adjusted Trade Suggestion" present you with a list of risk-assessed ideas that you can then investigate further.

Disclaimer: This is an analysis tool and should not be considered financial advice. All forms of trading involve substantial risk. You should not trade with money you cannot afford to lose. Always perform your own due diligence and use this indicator as one component of a complete trading plan.