TargetPredictor 5MA ForecastThis indicator consists of five moving averages. 7, 20, 50, 100 and 200.

Moving averages usually represent dynamic supports or resistances and are very useful in trading.

In addition, this indicator predicts where these moving averages will be located three candlesticks ahead and predicts their projected movement.

I hope you enjoy it and enjoy using it.

Forecast

Universal logarithmic growth curves, with support and resistanceLogarithmic regression is used to model data where growth or decay accelerates rapidly at first and then slows over time. This model is for the long term series data (such as 10 years time span).

The user can consider entering the market when the price below 25% or 5% confidence and consider take profit when the price goes above 75% or 95% confidence line.

This script is:

- Designed to be usable in all tickers. (not only for bitcoin now!)

- Logarithmic regression and shows support-resistance level

- Shape of lines are all linear adjustable

- Height difference of levels and zones are customizable

- Support and resistance levels are highlighted

Input panel:

- Steps of drawing: Won't change it unless there are display problems.

- Resistance, support, other level color: self-explanatory.

- Stdev multipliers: A constant variable to adjust regression boundaries.

- Fib level N: Base on the relative position of top line and base line. If you don't want all fib levels, you might set all fib levels = 0.5.

- Linear lift up: vertically lift up the whole set of lines. By linear multiplication.

- Curvature constant: It is the base value of the exponential transform before converting it back to the chart and plotting it. A bigger base value will make a more upward curvy line.

FAQ:

Q: How to use it?

A: Click "Fx" in your chart then search this script to get it into your chart. Then right click the price axis, then select "Logarithmic" scale to show the curves probably.

Q: Why release this script?

A: - This script is intended to to fix the current issues of bitcoins growth curve script, and to provide a better version of the logarithmic curve, which is not only for bitcoin , but for all kinds of tickers.

- In the public library there is a hardcoded logarithmic growth curve by @quantadelic . But unfortunately that curve was hardcoded by his manual inputs, which makes the curve stop updating its value since 2019 the date he publish that code. Many users of that script love using it but they realize it was stop updating, many users out there based on @quantadelic version of "bitcoin logarithmic growth curves" and they tried their best to update the coordinates with their own hardcode input values. Eventually, a lot of redundant hardcoded "Bitcoin growth curve" scripts was born in the public library. Which is not a good thing.

Q: What about looking at the regression result with a log scale price axis?

A: You can use this script that I published in a year ago. This script display the result in a log scale price axis.

FunctionForecastLinearLibrary "FunctionForecastLinear"

Method for linear Forecast, same as found in excel and other sheet packages.

forecast(sample_x, sample_y, target_x) linear forecast method.

Parameters:

sample_x : float array, sample data X value.

sample_y : float array, sample data Y value.

target_x : float, target X to get Y forecast value.

Returns: float

The Echo Forecast [LuxAlgo]This indicator uses a simple time series forecasting method derived from the similarity between recent prices and similar/dissimilar historical prices. We named this method "ECHO".

This method originally assumes that future prices can be estimated from a historical series of observations that are most similar to the most recent price variations. This similarity is quantified using the correlation coefficient. Such an assumption can prove to be relatively effective with the forecasting of a periodic time series. We later introduced the ability to select dissimilar series of observations for further experimentation.

This forecasting technique is closely inspired by the analogue method introduced by Lorenz for the prediction of atmospheric data.

1. Settings

Evaluation Window: Window size used for finding historical observations similar/dissimilar to recent observations. The total evaluation window is equal to "Forecast Window" + "Evaluation Window"

Forecast Window: Determines the forecasting horizon.

Forecast Mode: Determines whether to choose historical series similar or dissimilar to the recent price observations.

Forecast Construction: Determines how the forecast is constructed. See "Usage" below.

Src: Source input of the forecast

Other style settings are self-explanatory.

2. Usage

This tool can be used to forecast future trends but also to indicate which historical variations have the highest degree of similarity/dissimilarity between the observations in the orange zone.

The forecasting window determines the prices segment (in orange) to be used as a reference for the search of the most similar/dissimilar historical price segment (in green) within the gray area.

Most forecasting techniques highly benefit from a detrended series. Due to the nature of this method, we highly recommend applying it to a detrended and periodic series.

You can see above the method is applied on a smooth periodic oscillator and a momentum oscillator.

The construction of the forecast is made from the price changes obtained in the green area, denoted as w(t) . Using the "Cumulative" options we construct the forecast from the cumulative sum of w(t) . Finally, we add the most recent price value to this cumulated series.

Using the "Mean" options will add the series w(t) with the mean of the prices within the orange segment.

Finally the "Linreg" will add the series w(t) to an extrapolated linear regression fit to the prices within the orange segment.

vol_signalNote: This description is copied from the script comments. Please refer to the comments and release notes for updated information, as I am unable to edit and update this description.

----------

USAGE

This script gives signals based on a volatility forecast, e.g. for a stop

loss. It is a simplified version of my other script "trend_vol_forecast", which incorporates a trend following system and measures performance. The "X" labels indicate when the price touches (exceeds) a forecast. The signal occurs when price crosses "fcst_up" or "fcst_down".

There are only three parameters:

- volatility window: this is the number of periods (bars) used in the

historical volatility calculation. smaller number = reacts more

quickly to changes, but is a "noisier" signal.

- forecast periods: the number of periods for projecting a volatility

forecast. for example, "21" on a daily chart means the plots will

show the forecast from 21 days ago.

- forecast stdev: the number of standard deviations in the forecast.

for example, "2" means that price is expected to remain within

the forecast plot ~95% of the time. A higher number produces a

wider forecast.

The output table shows:

- realized vol: the volatility over the previous N periods, where N =

"volatility window".

- forecast vol: the realized volatility from N periods ago, where N =

"forecast periods"

- up/down fcst (level): the price level of the forecast for the next

N bars, where N = "forecast periods".

- up/down fcst (%): the difference between the current and forecast

price, expressed as a whole number percentage.

The plots show:

- blue/red plot: the upper/lower forecast from "forecast periods" ago.

- blue/red line: the upper/lower forecast for the next

"forecast periods".

- red/blue labels: an "X" where the price touched the forecast from

"forecast periods" ago.

+ NOTE: pinescript only draws a limited number of labels.

They will not appear very far into the past.

pricing_tableThis script helps you evaluate the fair value of an option. It poses the question "if I bought or sold an option under these circumstances in the past, would it have expired in the money, or worthless? What would be its expected value, at expiration, if I opened a position at N standard deviations, given the volatility forecast, with M days to expiration at the close of every previous trading day?"

The default (and only) "hv" volatility forecast is based on the assumption that today's volatility will hold for the next M days.

To use this script, only one step is mandatory. You must first select days to expiration. The script will not do anything until this value is changed from the default (-1). These should be CALENDAR days. The script will convert to these to business days for forecasting and valuation, as trading in most contracts occurs over ~250 business days per year.

Adjust any other variables as desired:

model: the volatility forecasting model

window: the number of periods for a lagged model (e.g. hv)

filter: a filter to remove forecasts from the sample

filter type: "none" (do not use the filter), "less than" (keep forecasts when filter < volatility), "greater than" (keep forecasts when filter > volatility)

filter value: a whole number percentage. see example below

discount rate: to discount the expected value to present value

precision: number of decimals in output

trim outliers: omit upper N % of (generally itm) contracts

The theoretical values are based on history. For example, suppose days to expiration is 30. On every bar, the 30 days ago N deviation forecast value is compared to the present price. If the price is above the forecast value, the contract has expired in the money; otherwise, it has expired worthless. The theoretical value is the average of every such sample. The itm probabilities are calculated the same way.

The default (and only) volatility model is a 20 period EWMA derived historical (realized) volatility. Feel free to extend the script by adding your own.

The filter parameters can be used to remove some forecasts from the sample.

Example A:

filter:

filter type: none

filter value:

Default: the filter is not used; all forecasts are included in the the sample.

Example B:

filter: model

filter type: less than

filter value: 50

If the model is "hv", this will remove all forecasts when the historical volatility is greater than fifty.

Example C:

filter: rank

filter type: greater than

filter value: 75

If the model volatility is in the top 25% of the previous year's range, the forecast will be included in the sample apart from "model" there are some common volatility indexes to choose from, such as Nasdaq (VXN), crude oil (OVX), emerging markets (VXFXI), S&P; (VIX) etc.

Refer to the middle-right table to see the current forecast value, its rank among the last 252 days, and the number of business days until

expiration.

NOTE: This script is meant for the daily chart only.

Pivot High/Low Analysis & Forecast [LuxAlgo]Returns pivot points high/low alongside the percentage change between one pivot and the previous one (Δ%) and the distance between the same type of pivots in bars (Δt). The trailing mean for each of these metrics is returned on a dashboard on the chart. The indicator also returns an estimate of the future time position of the pivot points.

This indicator by its very nature is not real-time and is meant for descriptive analysis alongside other components of the script. This is normal behavior for scripts detecting pivots as a part of a system and it is important you are aware the pivot labels are not designed to be traded in real-time themselves

🔶 USAGE

The indicator can provide information helping the user to infer the position of future pivot points. This information is directly used in the indicator to provide such forecasting. Note that each metric is calculated relative to the same type of pivot points.

It is also common for analysts to use pivot points for the construction of various figures, getting the percentage change and distance for each pivot point can allow them to eventually filter out points of non-interest.

🔹 Forecast

We use the trailing mean of the distance between respective pivots to estimate the time position of future pivot points, this can be useful to estimate the location of future tops/bottoms. The time position of the forecasted pivot is given by a vertical dashed line on the chart.

We can see a successful application of this method below:

Above we see the forecasted pivots for BTCUSD15. The forecast of interest being the pivot high. We highlight the forecast position with a blue dotted line for reference.

After some time we obtain a new pivot high with a new forecast. However, we can see that the time location of this new pivot high matches perfectly with the prior forecast.

The position in time for the forecast is given by:

x1_ph + E

x1_pl + E

where x1_ph denotes the position in time of the most recent pivot high. x1_pl denotes the position in time of the most recent pivot low and E the average distance between respective pivot points.

🔶 SETTINGS

Length: Window size for the detection of pivot points.

Show Forecasted Pivots: Display forecast of future pivot points.

🔹 Dashboard

Dashboard Location: Location of the dashboard on the chart

Dashboard Size: Size of the dashboard on the chart

Text/Frame Color: Determines the color of the frame grid as well as the text color

Multiple Regression Polynomial ForecastEXPERIMENTAL:

Forecasting using a polynomial regression over the estimates of multiple linear regression forecasts.

note: on low data the estimates are skewd away of initial value, i added the i_min_estimate option in to try curve this issue with limited success "o_o.

Function - Forecast LinearFunction to calculate a forecast using a linear regression approach, this is the same function used on excel and other data sheet programs.

reference:

- support.microsoft.com

- stackoverflow.com

Multi Moving Average with ForecastThis script allows to use 5 different MAs with prediction of the next five periods.

BTC ATH ROIThis indicator shows the ROI % of Bitcoin from when it passed its ATH of the previous bull cycle. I found it interesting that each time it crossed its ATH it took around 260-280 days to peak for each one. This bull run seems to follow between both of the previous bull runs including this recent dip.

There are a couple issues I want to fix but can't figure out:

1. You need to completely scroll out and move towards 2013 on the Daily chart for all 3 lines to show up. Would be nice to load all of that data at the start.

2. I can't query the value of the plots after they have been offset. This would be useful to create a prediction bias for the current plot so would could see where btc might go.

If you peeps know of a way to load all data or query plot values after offsets, please share. That would be awesome.

Monte Carlo Range Forecast [DW]This is an experimental study designed to forecast the range of price movement from a specified starting point using a Monte Carlo simulation.

Monte Carlo experiments are a broad class of computational algorithms that utilize random sampling to derive real world numerical results.

These types of algorithms have a number of applications in numerous fields of study including physics, engineering, behavioral sciences, climate forecasting, computer graphics, gaming AI, mathematics, and finance.

Although the applications vary, there is a typical process behind the majority of Monte Carlo methods:

-> First, a distribution of possible inputs is defined.

-> Next, values are generated randomly from the distribution.

-> The values are then fed through some form of deterministic algorithm.

-> And lastly, the results are aggregated over some number of iterations.

In this study, the Monte Carlo process used generates a distribution of aggregate pseudorandom linear price returns summed over a user defined period, then plots standard deviations of the outcomes from the mean outcome generate forecast regions.

The pseudorandom process used in this script relies on a modified Wichmann-Hill pseudorandom number generator (PRNG) algorithm.

Wichmann-Hill is a hybrid generator that uses three linear congruential generators (LCGs) with different prime moduli.

Each LCG within the generator produces an independent, uniformly distributed number between 0 and 1.

The three generated values are then summed and modulo 1 is taken to deliver the final uniformly distributed output.

Because of its long cycle length, Wichmann-Hill is a fantastic generator to use on TV since it's extremely unlikely that you'll ever see a cycle repeat.

The resulting pseudorandom output from this generator has a minimum repetition cycle length of 6,953,607,871,644.

Fun fact: Wichmann-Hill is a widely used PRNG in various software applications. For example, Excel 2003 and later uses this algorithm in its RAND function, and it was the default generator in Python up to v2.2.

The generation algorithm in this script takes the Wichmann-Hill algorithm, and uses a multi-stage transformation process to generate the results.

First, a parent seed is selected. This can either be a fixed value, or a dynamic value.

The dynamic parent value is produced by taking advantage of Pine's timenow variable behavior. It produces a variable parent seed by using a frozen ratio of timenow/time.

Because timenow always reflects the current real time when frozen and the time variable reflects the chart's beginning time when frozen, the ratio of these values produces a new number every time the cache updates.

After a parent seed is selected, its value is then fed through a uniformly distributed seed array generator, which generates multiple arrays of pseudorandom "children" seeds.

The seeds produced in this step are then fed through the main generators to produce arrays of pseudorandom simulated outcomes, and a pseudorandom series to compare with the real series.

The main generators within this script are designed to (at least somewhat) model the stochastic nature of financial time series data.

The first step in this process is to transform the uniform outputs of the Wichmann-Hill into outputs that are normally distributed.

In this script, the transformation is done using an estimate of the normal distribution quantile function.

Quantile functions, otherwise known as percent-point or inverse cumulative distribution functions, specify the value of a random variable such that the probability of the variable being within the value's boundary equals the input probability.

The quantile equation for a normal probability distribution is μ + σ(√2)erf^-1(2(p - 0.5)) where μ is the mean of the distribution, σ is the standard deviation, erf^-1 is the inverse Gauss error function, and p is the probability.

Because erf^-1() does not have a simple, closed form interpretation, it must be approximated.

To keep things lightweight in this approximation, I used a truncated Maclaurin Series expansion for this function with precomputed coefficients and rolled out operations to avoid nested looping.

This method provides a decent approximation of the error function without completely breaking floating point limits or sucking up runtime memory.

Note that there are plenty of more robust techniques to approximate this function, but their memory needs very. I chose this method specifically because of runtime favorability.

To generate a pseudorandom approximately normally distributed variable, the uniformly distributed variable from the Wichmann-Hill algorithm is used as the input probability for the quantile estimator.

Now from here, we get a pretty decent output that could be used itself in the simulation process. Many Monte Carlo simulations and random price generators utilize a normal variable.

However, if you compare the outputs of this normal variable with the actual returns of the real time series, you'll find that the variability in shocks (random changes) doesn't quite behave like it does in real data.

This is because most real financial time series data is more complex. Its distribution may be approximately normal at times, but the variability of its distribution changes over time due to various underlying factors.

In light of this, I believe that returns behave more like a convoluted product distribution rather than just a raw normal.

So the next step to get our procedurally generated returns to more closely emulate the behavior of real returns is to introduce more complexity into our model.

Through experimentation, I've found that a return series more closely emulating real returns can be generated in a three step process:

-> First, generate multiple independent, normally distributed variables simultaneously.

-> Next, apply pseudorandom weighting to each variable ranging from -1 to 1, or some limits within those bounds. This modulates each series to provide more variability in the shocks by producing product distributions.

-> Lastly, add the results together to generate the final pseudorandom output with a convoluted distribution. This adds variable amounts of constructive and destructive interference to produce a more "natural" looking output.

In this script, I use three independent normally distributed variables multiplied by uniform product distributed variables.

The first variable is generated by multiplying a normal variable by one uniformly distributed variable. This produces a bit more tailedness (kurtosis) than a normal distribution, but nothing too extreme.

The second variable is generated by multiplying a normal variable by two uniformly distributed variables. This produces moderately greater tails in the distribution.

The third variable is generated by multiplying a normal variable by three uniformly distributed variables. This produces a distribution with heavier tails.

For additional control of the output distributions, the uniform product distributions are given optional limits.

These limits control the boundaries for the absolute value of the uniform product variables, which affects the tails. In other words, they limit the weighting applied to the normally distributed variables in this transformation.

All three sets are then multiplied by user defined amplitude factors to adjust presence, then added together to produce our final pseudorandom return series with a convoluted product distribution.

Once we have the final, more "natural" looking pseudorandom series, the values are recursively summed over the forecast period to generate a simulated result.

This process of generation, weighting, addition, and summation is repeated over the user defined number of simulations with different seeds generated from the parent to produce our array of initial simulated outcomes.

After the initial simulation array is generated, the max, min, mean and standard deviation of this array are calculated, and the values are stored in holding arrays on each iteration to be called upon later.

Reference difference series and price values are also stored in holding arrays to be used in our comparison plots.

In this script, I use a linear model with simple returns rather than compounding log returns to generate the output.

The reason for this is that in generating outputs this way, we're able to run our simulations recursively from the beginning of the chart, then apply scaling and anchoring post-process.

This allows a greater conservation of runtime memory than the alternative, making it more suitable for doing longer forecasts with heavier amounts of simulations in TV's runtime environment.

From our starting time, the previous bar's price, volatility, and optional drift (expected return) are factored into our holding arrays to generate the final forecast parameters.

After these parameters are computed, the range forecast is produced.

The basis value for the ranges is the mean outcome of the simulations that were run.

Then, quarter standard deviations of the simulated outcomes are added to and subtracted from the basis up to 3σ to generate the forecast ranges.

All of these values are plotted and colorized based on their theoretical probability density. The most likely areas are the warmest colors, and least likely areas are the coolest colors.

An information panel is also displayed at the starting time which shows the starting time and price, forecast type, parent seed value, simulations run, forecast bars, total drift, mean, standard deviation, max outcome, min outcome, and bars remaining.

The interesting thing about simulated outcomes is that although the probability distribution of each simulation is not normal, the distribution of different outcomes converges to a normal one with enough steps.

In light of this, the probability density of outcomes is highest near the initial value + total drift, and decreases the further away from this point you go.

This makes logical sense since the central path is the easiest one to travel.

Given the ever changing state of markets, I find this tool to be best suited for shorter term forecasts.

However, if the movements of price are expected to remain relatively stable, longer term forecasts may be equally as valid.

There are many possible ways for users to apply this tool to their analysis setups. For example, the forecast ranges may be used as a guide to help users set risk targets.

Or, the generated levels could be used in conjunction with other indicators for meaningful confluence signals.

More advanced users could even extrapolate the functions used within this script for various purposes, such as generating pseudorandom data to test systems on, perform integration and approximations, etc.

These are just a few examples of potential uses of this script. How you choose to use it to benefit your trading, analysis, and coding is entirely up to you.

If nothing else, I think this is a pretty neat script simply for the novelty of it.

----------

How To Use:

When you first add the script to your chart, you will be prompted to confirm the starting date and time, number of bars to forecast, number of simulations to run, and whether to include drift assumption.

You will also be prompted to confirm the forecast type. There are two types to choose from:

-> End Result - This uses the values from the end of the simulation throughout the forecast interval.

-> Developing - This uses the values that develop from bar to bar, providing a real-time outlook.

You can always update these settings after confirmation as well.

Once these inputs are confirmed, the script will boot up and automatically generate the forecast in a separate pane.

Note that if there is no bar of data at the time you wish to start the forecast, the script will automatically detect use the next available bar after the specified start time.

From here, you can now control the rest of the settings.

The "Seeding Settings" section controls the initial seed value used to generate the children that produce the simulations.

In this section, you can control whether the seed is a fixed value, or a dynamic one.

Since selecting the dynamic parent option will change the seed value every time you change the settings or refresh your chart, there is a "Regenerate" input built into the script.

This input is a dummy input that isn't connected to any of the calculations. The purpose of this input is to force an update of the dynamic parent without affecting the generator or forecast settings.

Note that because we're running a limited number of simulations, different parent seeds will typically yield slightly different forecast ranges.

When using a small number of simulations, you will likely see a higher amount of variance between differently seeded results because smaller numbers of sampled simulations yield a heavier bias.

The more simulations you run, the smaller this variance will become since the outcomes become more convergent toward the same distribution, so the differences between differently seeded forecasts will become more marginal.

When using a dynamic parent, pay attention to the dispersion of ranges.

When you find a set of ranges that is dispersed how you like with your configuration, set your fixed parent value to the parent seed that shows in the info panel.

This will allow you to replicate that dispersion behavior again in the future.

An important thing to note when settings alerts on the plotted levels, or using them as components for signals in other scripts, is to decide on a fixed value for your parent seed to avoid minor repainting due to seed changes.

When the parent seed is fixed, no repainting occurs.

The "Amplitude Settings" section controls the amplitude coefficients for the three differently tailed generators.

These amplitude factors will change the difference series output for each simulation by controlling how aggressively each series moves.

When "Adjust Amplitude Coefficients" is disabled, all three coefficients are set to 1.

Note that if you expect volatility to significantly diverge from its historical values over the forecast interval, try experimenting with these factors to match your anticipation.

The "Weighting Settings" section controls the weighting boundaries for the three generators.

These weighting limits affect how tailed the distributions in each generator are, which in turn affects the final series outputs.

The maximum absolute value range for the weights is . When "Limit Generator Weights" is disabled, this is the range that is automatically used.

The last set of inputs is the "Display Settings", where you can control the visual outputs.

From here, you can select to display either "Forecast" or "Difference Comparison" via the "Output Display Type" dropdown tab.

"Forecast" is the type displayed by default. This plots the end result or developing forecast ranges.

There is an option with this display type to show the developing extremes of the simulations. This option is enabled by default.

There's also an option with this display type to show one of the simulated price series from the set alongside actual prices.

This allows you to visually compare simulated prices alongside the real prices.

"Difference Comparison" allows you to visually compare a synthetic difference series from the set alongside the actual difference series.

This display method is primarily useful for visually tuning the amplitude and weighting settings of the generators.

There are also info panel settings on the bottom, which allow you to control size, colors, and date format for the panel.

It's all pretty simple to use once you get the hang of it. So play around with the settings and see what kinds of forecasts you can generate!

----------

ADDITIONAL NOTES & DISCLAIMERS

Although I've done a number of things within this script to keep runtime demands as low as possible, the fact remains that this script is fairly computationally heavy.

Because of this, you may get random timeouts when using this script.

This could be due to either random drops in available runtime on the server, using too many simulations, or running the simulations over too many bars.

If it's just a random drop in runtime on the server, hide and unhide the script, re-add it to the chart, or simply refresh the page.

If the timeout persists after trying this, then you'll need to adjust your settings to a less demanding configuration.

Please note that no specific claims are being made in regards to this script's predictive accuracy.

It must be understood that this model is based on randomized price generation with assumed constant drift and dispersion from historical data before the starting point.

Models like these not consider the real world factors that may influence price movement (economic changes, seasonality, macro-trends, instrument hype, etc.), nor the changes in sample distribution that may occur.

In light of this, it's perfectly possible for price data to exceed even the most extreme simulated outcomes.

The future is uncertain, and becomes increasingly uncertain with each passing point in time.

Predictive models of any type can vary significantly in performance at any point in time, and nobody can guarantee any specific type of future performance.

When using forecasts in making decisions, DO NOT treat them as any form of guarantee that values will fall within the predicted range.

When basing your trading decisions on any trading methodology or utility, predictive or not, you do so at your own risk.

No guarantee is being issued regarding the accuracy of this forecast model.

Forecasting is very far from an exact science, and the results from any forecast are designed to be interpreted as potential outcomes rather than anything concrete.

With that being said, when applied prudently and treated as "general case scenarios", forecast models like these may very well be potentially beneficial tools to have in the arsenal.

Forecast OscillatorThe Forecast Oscillator is a technical indicator that compares a security close price to its time series forecast. The time series forecast function name is "tsf" and it calculates the projection of the price trend for the next bar.

The Forecast Oscillator and therefore the time series forecast are based on linear regression. The time series forecast indicator is equal to the sum of two other indicators: the linear regression (LinearReg) and the linear regression slope (LinearReg_Slope).

If the Forecast Oscillator stays above the zero line for an extended period, then it signals that the price may rise in the future and if it stays below the zero line for an extended period, then it signals a coming fall in the security price.

The indicator name is "Forecast Oscillator" and it accepts two arguments. The first argument is the time series that is used in the next bar forecast (It is usually the close price) and the second one is the period that will be passed to the time series forecast function during calculation . The technical analysis indicator returns a value in percentage that corresponds to the close price minus the previous value of the time series forecast, multiplied by 100 and divided by the close price.

Author's Note:

Just look at the exaggerated movements of the oscillator especially in trend changes . Some examples can be experienced on the chart in rectangles.

Kıvanç Özbilgiç

Moving RegressionMoving Regression is a generalization of moving average and polynomial regression.

The procedure approximates a specified number of prior data points with a polynomial function of a user-defined degree. Then, polynomial interpolation of the last data point is used to construct a Moving Regression time series.

Application:

Moving Regression allows one to smooth noise on the analyzed chart, assess momentum, confirm trends, and establish areas of support and resistance.

In addition, it can be used as a simple stand-alone forecasting method to identify trend direction and trend reversal points. When the local polynomial is predicted to move up in the next time step, the color of the Moving Regression curve will be green. Otherwise, the color of the curve is red. This function is (de)activated using the Predict Trend Direction flag.

Selecting the model parameters:

The effects of the moving window Length and the Local Polynomial Degree are confounded. This allows for finding the optimal trade-off between noise (variance) and lag (bias). Higher Length and lower Polynomial Degree (such as 1, i.e. linear), will result in "smoother" time series but at the cost of greater lag. Increasing the Polynomial Degree to, for example, 2 (squared) while maintaining the Length will diminish the lag and thus compromise the noise-lag tradeoff.

Relation to other methods:

When the degree of the local polynomial is set to 0 (i.e., fitting data to a constant level), the Moving Regression time series exactly matches the Simple Moving Average of the same length.

Running Donchian ChannelsExperimental script to plot a forecast for the Donchian Channels indicator.

By using show_last = 2 , the forecast shows a solid line, this gets messed up on the bar when a new high or low is made.. Like the image below. I don't know how to fix that, please tell me if you do :)

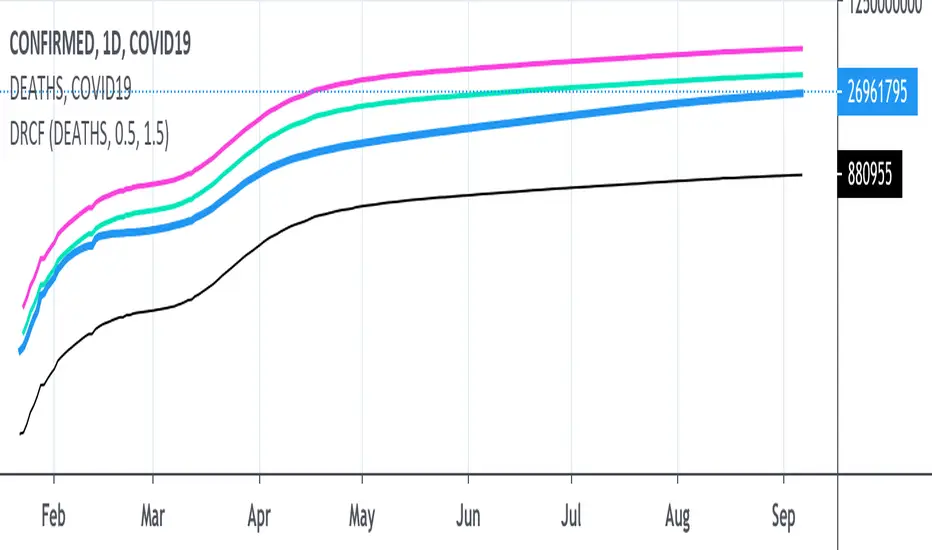

COVID19 Death Rate Cases Forecast (DRCF)The core idea is that given a deaths count and a death ratio, we can calculate how many cases must exist.

Total Cases <-> 100%

Deaths <-> Death Rate

This script plots the total cases for two different death rates.

Death Rate = (Deaths * 100) / Total Cases

Remember to update the DEATHS_X value in the script settings so that it matches the COMFIRMED_X graph you are viewing.

[RS]ZigZag Multiple Methods - Forecast - patterns - labelsexperimental:

zigzag indicator with all the zigzag methods that im aware of(that matter atleast), theres something for all tastes there :P

this will be the basis for zigzag tools i make in the future.

note: some zigzags REPAINT.

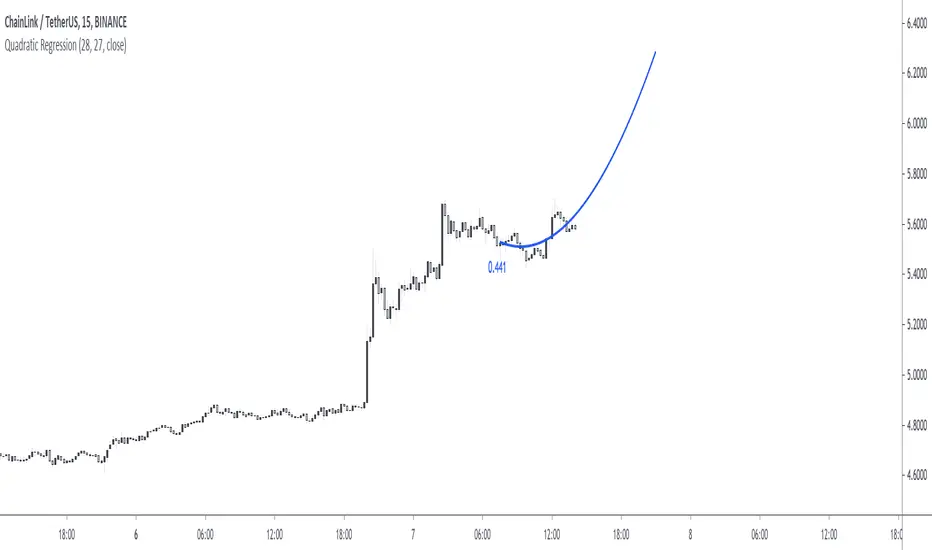

Quadratic RegressionFit a quadratic polynomial (parabola) to the last length data points by minimizing the sum of squares between the data and the fitted results. The script can extrapolate the results in the future and can also display the R-squared of the model. Note that this script is subject to some limitations (more in the "Notes" section).

Settings

Length : Number of data points to use as input.

Offset : Determine the number of past fitted values to be displayed, if 0 only the extrapolated values are displayed, if 55 only the past fitted values are displayed.

Src : Input data of the indicator

Show R2 : Determine if the value of the R-squared must be displayed, by default true.

Usage

When the underlying trend in the price is not linear, we might use more advanced models to estimate it, this is where using a higher-degree regression model might be required, as such a quadratic model (second-degree) is appropriate when the underlying trend is parabolic.

Here we can see that the quadratic regression (in blue) offer a better fit than a linear one.

Another advantage of the quadratic regression is that a linear one will always have the same direction, that's not the case with the quadratic regression and as such, it is possible to forecast reversals.

Above a linear regression (in red) and two quadratic regression (in blue) with both length = 54. Note that for the sake of clarity, the above image uses a quadratic regression to show all the past fitted values and another one to show all the forecasted values.

The R-Squared is also extremely useful when it comes to measuring the accuracy of the model, with values closer to 1 indicating that the model is appropriate, and thus suggesting that the underlying trend in the price is parabolic. The R-squared can also measure the strength of the trend.

Notes

The script uses the function line.new , as such only a maximum of 54 observations are displayed, getting more observations can be done by using an additional quadratic regression like we did in the previous section. Another thing is that line.new use xloc.bar_time , as such it is possible to observe some errors with the displayed results of the indicator, such as:

This will happen when applying the indicator to symbols with session breaks, I apologize for this inconvenience and I'll try to find solutions. Note however that the indicator will work perfectly on cryptos.

Summary

That's an indicator I really wanted to make, even if it is important to note that such models are rarely useful in stock markets, however it is more than possible to create a quadratic regression (with severe limitations) with pinescript.

Today I turn 21, while I should be celebrating I still wanted to share something with the community, it's also some kind of present to myself that tells me that I am a bit better at using pinescript than last year, and I am glad I could progress (instead of regress, regression , got it?). Thx a lot for reading!

[RS]Simple Forecast - Keltner WormsEXPERIMENTAL:

Using keltner channels with automatic multiplier finding, offsets and show_last cutoffs to generate a forecast area.

video showing why its named keltner worms :p..

streamable.com

[RS]Shotgun ForecastsExperimental:

its a play at linear forecasting.

use replay feature to see it in action:

streamable.com

Indicator: Weight Of Middle [xQT5]This is my original indicator that was inspired by "Mayer Multiple" and "Chande Forecast Oscillator" (CFO).

I decided to search truth of trend power with SMA and LinReg and found it in a somewhere of the middle. Also, I added a limit area, where you need to keep a more attention, because it can show a potential reversal.

You can change parametrs with a your own look.

One more signal for indicator:

- If "WOM" is above "1" - it's a bullish direction;

- If "WOM" is below "1" - it's a bearish direction.

Enjoy it!

Fancy Triple Moving Averages [BigBitsIO]This script is for three moving averages with as many features as I can possibly fit into a single moving average.

Features:

- Three moving averages (MA1, MA2, MA3).

- Standard MA inputs.

- MA type.

- MA period.

- MA price.

- MA resolution (time frame).

- Visibility toggle.

- MA Candle Type

- Fancy MA inputs.

- Toggle to show only candles included in the MA calculation ("Highlight inclusion") or display entire MA history.

- Toggle to show a ghost trail when Highlight inclusion is toggled on. Displays a shaded version of past MA history before the inclusion period (as seen on snapshot).

- Toggle to show forecast values for the MA.

- Other inputs related to forecasting:

- Forecast bias. (Neutral forecasts MA if the current price remains the same.)

- Forecast period.

- Forecast magnitude.

*** DISCLAIMER: For educational and entertainment purposes only. Nothing in this content should be interpreted as financial advice or a recommendation to buy or sell any sort of security or investment including all types of crypto. DYOR, TYOB. ***