Blockunity US Market Liquidity (BML)Get a clear view of US market liquidity and monitor its status at a glance to anticipate movements on risky assets.

The Idea

The BML aggregates and analyzes total USD market liquidity in trillions of dollars. It is used to monitor the liquidity of the USD market. When liquidity is good, all is well. If liquidity is low, the US will maneuver and sell treasury bills (debt) to replenish its treasury, which can lead to bearish pressure on markets, particularly those considered risky, such as Bitcoin.

How to Use

The indicator is very easy to use, there's nothing special about it. This tool is mainly intended to be used as fundamental information, and not for active trading.

Elements

The US Market Liquidity has several distinct components:

FED Balance Sheet

The Fed credits member banks’ Fed accounts with money, and in return, banks sell the Fed US Treasuries and/or US Mortgage-Backed Securities. This is how the Fed “prints” money to juice the financial system.

US Treasury General Account

The US Treasury General Account (TGA) balances with the NY Fed. When it decreases, it means the US Treasury is injecting money into the economy directly and creating activity. When it increases, it means the US Treasury is saving money and not stimulating economic activity. The TGA also increases when the Treasury sells bonds. This action removes liquidity from the market as buyers must pay for their bonds with dollars.

Overnight Reverse Repurchase Agreements

A reverse repurchase agreement (known as Reverse Repo or RRP) is a transaction in which the New York Fed under the authorization and direction of the Federal Open Market Committee sells a security to an eligible counterparty with an agreement to repurchase that same security at a specified price at a specific time in the future.

Earnings Remittances Due to the Treasury

The Federal Reserve Banks remit residual net earnings to the US Treasury after providing for the costs of operations, payment of dividends, and the amount necessary to maintain each Federal Reserve Bank’s allotted surplus cap. Positive amounts represent the estimated weekly remittances due to the US Treasury. Negative amounts represent the cumulative deferred asset position, which is incurred during a period when earnings are not sufficient to provide for the cost of operations, payment of dividends, and maintaining surplus.

Settings

Several parameters can be defined in the indicator configuration. You can:

Choose the smoothing and timeframe to be used in the plot.

Set the EMA lookback period and display it or not. This affects the color of the main plot.

Set the period to be taken into account when calculating the variation rate in the table.

Select the data to be taken into account in the calculation.

Activate or not the barcolor.

Lastly, you can modify all table parameters.

Fundamental Analysis

BTC Valuation

The BTC Valuation indicator

is a powerful tool designed to assist traders and analysts in evaluating the current state of Bitcoin's market valuation. By leveraging key moving averages and a logarithmic trendline, this indicator offers valuable insights into potential buying or selling opportunities based on historical price value.

Key Features:

200MA/P (200-day Moving Average to Price Ratio):

Provides a perspective on Bitcoin's long-term trend by comparing the current price to its 200-day Simple Moving Average (SMA).

A positive value suggests potential undervaluation, while a negative value may indicate overvaluation.

50MA/P (50-day Moving Average to Price Ratio):

Focuses on short-term trends, offering insights into the relationship between Bitcoin's current price and its 50-day SMA.

Helps traders identify potential bullish or bearish trends in the near term.

LTL/P (Logarithmic TrendLine to Price Ratio):

Incorporates a logarithmic trendline, considering Bitcoin's historical age in days.

Assists in evaluating whether the current price aligns with the long-term logarithmic trend, signaling potential overvaluation or undervaluation.

How to Use:

Z Score Indicator Integration:

The BTC Valuation indicator leverages the Z Score Indicator to score the ratios in a statistical way.

Statistical scoring provides a standardized measure of how far each ratio deviates from the mean, aiding in a more nuanced and objective evaluation.

Z Score Indicator

This BTC Valuation indicator provides a comprehensive view of Bitcoin's valuation dynamics, allowing traders to make informed decisions.

While indicators like BTC Valuation provide valuable insights, it's crucial to remember that no indicator guarantees market predictions.

Traders should use indicators as part of a comprehensive strategy and consider multiple factors before making trading decisions.

Historical performance is not indicative of future results. Exercise caution and continually refine your approach based on market dynamics.

Commitments of Traders Report [Advanced]This indicator displays the Commitment of Traders (COT) report data in a clear, table format similar to an Excel spreadsheet, with additional functionalities to analyze open interest and position changes. The COT report, published weekly by the Commodity Futures Trading Commission (CFTC), provides valuable insights into market sentiment by revealing the positioning of various trader categories.

Display:

Release Date: When the data was released.

Open Interest: Shows the total number of open contracts for the underlying instrument held by selected trader category.

Net Contracts: Shows the difference between long and short positions for selected trader category.

Long/Short OI: Displays the long and short positions held by selected trader category.

Change in Long/Short OI: Displays the change in long and short positions since the previous reporting period. This can highlight buying or selling pressure.

Long & Short Percentage: Displays the percentage of total long and short positions held by each category.

Trader Categories (Configurable)

Commercials: Hedgers who use futures contracts to manage risk associated with their underlying business (e.g., producers, consumers).

Non-Commercials (Large Speculators): Speculative traders with large positions who aim to profit from price movements (e.g., hedge funds, investment banks).

Non-Reportable (Small Speculators/Retail Traders): Smaller traders with positions below the CFTC reporting thresholds.

CFTC Code: If the indicator fails to retrieve data, you can manually enter the CFTC code for the specific instrument. The code for instrument can be found on CFTC's website.

Using the Indicator Effectively

Market Sentiment Gauge: Analyze the positioning of each trader category to gauge overall market sentiment.

High net longs by commercials might indicate a bullish outlook, while high net shorts could suggest bearish sentiment.

Changes in open interest and long/short positions can provide additional insights into buying and selling pressure.

Trend Confirmation: Don't rely solely on COT data for trade signals. Use it alongside price action and other technical indicators for confirmation.

Identify Potential Turning Points: Extreme readings in COT data, combined with significant changes in open interest or positioning, might precede trend reversals, but exercise caution and combine with other analysis tools.

Disclaimer

Remember, the COT report is just one piece of the puzzle. It should not be used for making isolated trading decisions. Consider incorporating it into a comprehensive trading strategy that factors in other technical and fundamental analysis.

Credit

A big shoutout to Nick from Transparent FX ! His expertise and thoughtful analysis have been a major inspiration in developing this COT Report indicator. To know more about this indicator and how to use it, be sure to check out his work.

IDX Financials v2This indicator adds financial data, ratios, and valuations to your chart. The main objective is to present financial overview that can be glanced quickly to add to your considerations.

The visualization of the indicator consists of two parts:

A. Plots (lines alongside the candlestick)

B. Financial table on the right. Drag your candlestick to the left to provide blank area for the table.

Programatically, the financial data is obtained by using these Pine API:

request.earnings(...) API for the EPS values that are used by the price at average PER line , and

request.financial(..) API for the rest of financial data required by the indicator.

See What financial data is available in Pine for more info on getting financial data in Pine.

A. THE PLOTS

The plots produces two lines, price at average PER in blue and price at average PBV line in pink, calculated over some adjustable time period (the default is one year). By default, only price at average PER line is shown.

Note that PER stands for Price to Earning Ratio.

The price at average PER line shows the price level at the average PER. It is calculated using formula as follows:

line = AVGPER * EPSTTM

where AVGPER is the average PER over some time period (default is one year, adjustable) and EPSTTM is the standardized EPS TTM.

Note that the EPS is updated at the actual time of earning report publication , and not at standard quarter dates such as March 31st, Dec 31st, etc.. This approach is chosen to represent the actual PE at the time.

The price at average PBV line (PBV stands for Price to Book Value), which can be enabled in settings, shows the price at average PBV. It is calculated using formula as follows:

line = AVGPBV * BVPS

where AVGPBV is the average PBV over some period of time (default is one year, adjustable) and BVPS is the book value per share. Note that the PBV is clipped to range to avoid values that are too small/large.

Also note that unlike PER, the BVPS is updated at each quarterly date (such as March 31st, Dec 31st, etc.).

Apart from those lines, some values are written to the status line (i.e. the numbers next to indicator name), which represent the corresponding value at the currently hovered bar:

PER TTM

Average PER

Std value (zvalue) of PER TTM (equal to = (PERTTM - AVGPER)/STDPER)

PBV

The meaning for these abbreviations should be straightforward.

Using the price at average PER line

There are several ways to use the price at average PER line .

You can quickly get the sense of current valuation by seeing the price relative to the price at average PER line . If the price is above the line, the valuation is higher than the average valuation, and vice versa if the price is lower.

The distance between the price and the average is measured in unit of standard deviation. This is represented by the third number in the status line. Value zero indicates the price is exactly at the average PER line. Positive value indicates price is higher than average, and negative if price is lower than average. Usually people use value +2 and -2 to indicate extreme positions.

The second way to use the line is to see how the line jumps up or down at the earning report date . If the line jumps up, this indicates the increase of EPSTTM. And vice versa when the line jumps down.

When EPSTTM is trending up over several quarters, or if EPSTTM is expected to go up, usually the price is also trending up and the valuation is over the average. And vice versa when EPSTTM is trending down or expected to go down. Deviation from this pattern may present some buying or selling opportunity.

B. THE FINANCIAL TABLE

The second visual part is the financial table. The financial table contains financial information at the last bar . It has four sections:

1. Revenue

2. Income

3. Valuations

4. Ratios

Let's discuss them in detail.

1. Revenue and income sections

The revenue and income table are organized into rows and columns.

Each row shows the data at the specified time frame, as follows:

The first four rows shows quarterly revenue/income of the last four quarters.

Then followed by TTM data.

Then followed by forecast of next quarter revenue/income, if such forecast exists. Note the "(F)" notation next to the quarter name.

Then followed by forecast of TTM data of next quarter (only for income), if such forecast exists. Note the "(F)" notation next to the TTM name.

The columns of revenue and income sections show the following:

The time frame information (such as quarter name, TTM, etc.)

The revenue/income value, in billions or millions (configurable).

YoY (year on year) growth, i.e. comparing the value with the value one year earlier, if any.

QoQ (quarter on quarter) growth, i.e. comparing the value with previous quarter value, if any.

GPM/NPM (gross profit margin or net profit margin), i.e. the margin on the specified time period.

Using the Revenue and Income table

The table provides quick way to see the revenue and income trend. You can see the YoY growth as well as QoQ, if that is applicable (non seasonal stocks). You can also see how the margins change over the periods.

The values are also presented with relevant background color . Green indicates "good" value and red indicates "bad" value. The intensity represents how good/bad the value is. The limits of the good and bad values are currently hardcoded in the script.

2. Valuations section

The valuation shows current stock valuation. The section is organized in rows and columns. Each row contains one type of valuation criteria, as follows:

PER (Price Earning Ratio)

Next quarter PER forecast (marked by "(F)" notation) when available

PBV (Price to Book value)

For each valuation criteria, several values are presented as columns:

The current value of the criteria. By current, it means the value at the last bar.

The one year standard deviation position

The three years standard deviation position

3. Ratios Section

The ratios section contains the following useful financial ratios:

ROA (Return on Asset), equal to: NET_INCOME_TTM / TOTAL_ASSETS

ROE (Return on Equity), equal to: NET_INCOME_TTM / BOOK_VALUE_PER_SHARE

PEG (PER to Growth Ratio), equal to PER_TTM / (INCOME_TTM_GROWTH*100)

DER (Debt to Equity Ratio), taken from request.financial(syminfo.tickerid, "DEBT_TO_EQUITY", "FQ")

DPR (Dividend Payout Ratio), taken from request.financial(syminfo.tickerid, "DIVIDEND_PAYOUT_RATIO", "FY")

Dividend yield, equal to (DPR * (NET_INCOME_TTM / TOTAL_SHARES_OUTSTANDING)) / close

KNOWN BUGS

Currently does not handle when the financial quarter contains gap, i.e. there is missing quarter. This usually happens on newly IPO stocks.

RP - Realized Price for Bitcoin (BTC) [Logue]Realized Price (RP) - The RP is summation of the value of each BTC when it last moved divided by the total number of BTC in circulation. This gives an estimation of the average "purchase" price of BTC on the bitcoin network based on when it was last transacted. This indicator tells us if the average network participant is in a state of profit or loss. This indicator is normally used to detect BTC bottoms, but an extension can be used to detect when the bitcoin network is "highly" overvalued. Because the "strength" of the BTC tops has decreased over the cycles, a logarithmic function for the extension was created by fitting past cycles as log extension = slope * time + intercept. This indicator triggers when the BTC price is above the realized price extension. For the bottoms, the RP is shifted downwards at a default value of 80%. The slope, intercept, and RP bottom shift can all be modified in the script.

CVDD - Coin Value Days Destroyed for Bitcoin (BTC) [Logue]Cumulative Value Days Destroyed (CVDD) - The CVDD was created by Willy Woo and is the ratio of the cumulative value of Coin Days Destroyed in USD and the market age (in days). While this indicator is used to detect bottoms normally, an extension is used to allow detection of BTC tops. When the BTC price goes above the CVDD extension, BTC is generally considered to be overvalued. Because the "strength" of the BTC tops has decreased over the cycles, a logarithmic function for the extension was created by fitting past cycles as log extension = slope * time + intercept. This indicator is triggered for a top when the BTC price is above the CVDD extension. For the bottoms, the CVDD is shifted upwards at a default value of 120%. The slope, intercept, and CVDD bottom shift can all be modified in the script.

MVRVZ - MVRVZ Top and Bottom Indicator for BTC [Logue]Market Value-Realized Value Z-score (MVRVZ) - The MVRV-Z score measures the value of the bitcoin network by comparing the market cap to the realized value and dividing by the standard deviation of the market cap (market cap – realized cap) / std(market cap)). When the market value is significantly higher than the realized value, the bitcoin network is "overvalued". Very high values have signaled cycle tops in the past and low values have signaled bottoms. For tops, the default trigger value is above 6.85. For bottoms, the indicator is triggered when the MVRVZ is below -0.25 (default).

Bond Yield SpreadThe Bond Yield Spread Script is developed for forex traders, offering an automated tool to calculate the bond yield spread between two countries associated with the forex pair displayed on the chart.

Functionality:

The script starts by identifying the base and quote currencies of the current forex pair and aligns them with their corresponding national bond symbols based on user-selected maturity, with options ranging from 01Y to 30Y. It calculates the yield spread by subtracting the bond yield associated with the quote country from that of the base country, following the formula:

Yield Spread = Yield(Base Country) − Yield(Quote Country)

which is then displayed as a plot line on the chart.

This script relies solely on TradingView's internal yield symbols, with the following calculation:

"currency" => "first two letters" + maturity

And maturity, in this case, is the value that is configured in the indicator settings, for example:

"EUR" => "EU" + "02Y" will result in EU02Y -> which will be used in the formula, depending on the quote or base currency.

Application in Trading:

This indicator is invaluable for traders employing carry trading strategies or assessing currency strength based on traded interest rates as an indicator. A higher yield spread typically indicates a stronger currency, because the return obtained for holding the currency is higher.

Originality and Practicality:

This script is self-developed, aiming to fill the gap in automatic bond yield comparisons within the TradingView environment. It is particularly beneficial for traders focusing on macroeconomic factors affecting forex markets. Unlike other scripts, it integrates various bond maturities into one tool, enhancing its utility and application range.

Conclusion:

Designed for traders incorporating macroeconomics in their strategy, this script will be useful to calculate the bond yield differences automatically without having to enter a new formula for every new currency pair.

Compliance and Limitations:

The script complies with TradingView scripting standards, ensuring no lookahead bias and maintaining real-time data integrity. However, its utility depends on the comprehensive availability of bond yield data within TradingView. As not all countries issue bonds for each listed maturity, this may limit the script’s application for certain currency pairs or specific maturities.

NUPL - Net Unrealized Profit-Loss BTC Tops/Bottoms [Logue]Net Unrealized Profit Loss (NUPL) - The NUPL measures the profit state of the bitcoin network to determine if past transfers of BTC are currently in an unrealized profit or loss state.

Values above zero indicate that the network is in overall profit, while values below zero indicate the network is in overall loss. Highly positive NUPL values indicate overvaluation of the BTC network and relatively negative NUPL values indicate an undervaluation of the BTC network.

For tops: The default setting for tops is based on decreasing "strength" of BTC tops. A decreasing linear function (trigger = slope * time + intercept) was fit to past cycle tops for this indicator and is used as the default to signal macro tops. The user can change the slope and intercept of the line by changing the slope and/or intercept factor. The user also has the option to indicate tops based on a horizontal line via a settings selection. This horizontal line default value is 73. This indicator is triggered for a top when the NUPL is above the trigger value.

For bottoms: Bottoms are displayed based on a horizontal line with a default setting of -13. The indicator is triggered for a bottom when the NUPL is below the bottom trigger value.

Blockunity Miners Synthesis (BMS)Track the status of Bitcoin and Ethereum Miners' Netflows and their asset reserves.

The Idea

The goal is to provide a simple tool for visualizing the changes in miners' flows and reserves.

How to Use

Analysing the behaviour of miners enables you to detect long-term opportunities, in particular with the state of reserves, but also in the shorter term with the visualization of Netflows.

Elements

Miners Reserves

Miners Reserves represent the balances of addresses belonging to mining pools (in BTC or ETH).

This data can also be displayed in USD via the indicator parameters:

Miners Netflow

The Netflow is calculated by subtracting the outflows from the inflows originating from addresses associated with mining pools. When this result is negative, it indicates that more funds are exiting the miners' accounts than the funds they are receiving. Consequently, negative miner netflows suggests selling activity.

This data can also be displayed in USD via the indicator parameters. You can also choose the timeframe. For example, selecting "Yearly" will give a Netflow daily average taking into account the last 365 days:

Settings

In the settings, you can first choose which asset to view, between Bitcoin and Ethereum. Here are the reserves of Ethereum miners:

As with Bitcoin, Netflow can also be displayed in the timeframe of your choice. Here you can see the average daily netflow of Ethereum miners in USD over the last 30 days:

Here are all the parameters:

Asset Selector: Choose between Bitcoin or Ethereum miner data.

Get values in USD: Displays values in USD instead of assets.

Switch between Netflow and Reserve : If checked, displays Miners' Reserves data. If unchecked, displays Miners' Netflow data.

Display timeframe: Allows you to select the timeframe for displaying the Netflow plot.

Period Lookback (in days): Select the period to be taken into account when calculating the variation percentage of Miners' Reserves.

Lastly, you can modify all table and labels parameters.

PUELL - PUELL Top and Bottom Indicator for BTC [Logue]Puell Multiple Indicator (PUELL) - The Puell multiple is the ratio between the daily coin issuance in USD and its 365-day moving average. This multiple helps to measure miner profitability. The PUELL indicator smooths the Puell multiple using a 14-day simple moving average. When the PUELL goes to high values relative to historical values, it indicates the profitability of the miners is high and a top may be near. When the PUELL is low relative to historical values, it indicates the profitability of the minors is low and a bottom may be near. The default trigger values are PUELL values above 3.0 for a "top" and below 0.5 for a "bottom".

TFS - Bitcoin (BTC) Transaction Fee Spike Top Indicator [Logue]Transaction Fee Spike (TFS) - For bitcoin (BTC), transaction fees on the bitcoin network can signal a mania phase when they increase well above historical values. This mania phase may indicate we are near a top in the BTC price. The transaction fee in USD is directly retrieved from Glassnode. The default trigger for this indicator fires when the transaction fees increase above $44/transaction.

Greenblatts Magic Formula - A multiple approachThis indicator is supposed to help find undervalued stocks. Inspired by Joel Greenblatt's strategy where he ranks stocks with the lowest EV/EBIT and the highest ROC. Inspired by the ERP5 strategy I have added Earnings Yield together with ROC.

My approach and how I use the indicator is to see Magic Formula score as a multiple, rather than ranking the numbers between different stocks. Like P/E for comparison. Different kinds of companies trades at different multiples so you have to compare the current MF Score in relation to historical MF Score to get an idea if it truly is undervalued. You also want to see that price actually reacts to a low MF Score.

As i general rule for myself I stay away from companies with EV/EBIT above 13 and generally want to see MF Score below 6-7. A company trading at a negative MF Score indicates that the company may be heavily undervalued.

Red line = EV/EBIT

Green line = ROC + EY / 2

Yellow line = "MF Score" EVEBIT - (ROC+EY/2)

Blue line = The 50 EMA of MF score

The strategy is simple. Look for companies which might be undervalued. Compare the current MF score to it's history. If it's trading near a previous bottom it indicates that the company might be undervalued. You can also use the MF EMA to see a more smooth curve to interpret the multiple.

Historical PE ratio vs medianThe Trailing Twelve-Month Price-to-Earnings (TTM P/E) Ratio vs. Median Value Indicator is a financial analytical tool designed to assess the current valuation of a stock or index in comparison to its historical norm. This is achieved by calculating the P/E ratio using the sum of the entity's earnings per share (EPS) over the past twelve months and dividing it by its current share price. The resulting TTM P/E ratio is then compared against the median P/E ratio calculated over a specified historical period.

The median P/E ratio serves as a benchmark, representing the midpoint of the entity's valuation over the selected timeframe, thus smoothing out short-term volatility and anomalies. By comparing the current TTM P/E ratio to this median, the indicator provides a relative measure of whether the stock or index is currently overvalued, undervalued, or trading at its historical valuation norms.

VEMA_LTFVEMA indicator is based on lower time frame volume data and it has 3 lines.

20, 50, 100 moving averages of the close price in each candle with the highest volume.

Effectively working fine and hence sharing.

Will Add more information with examples in next update

Weekend Analysis

There are always discussions about how the weekend affects Crypto-Coins.

It seems that on Monday, the price usually returns to Friday's level.

To make a qualified statement, I wrote this script that tests exactly that

and provides an evaluation.

It displays a candle for Saturday and Sunday.

Either green or red, but also blue if there was hardly any movement.

This threshold is set at 2%, but can be changed in the settings.

If the relative distance from Saturday's open to Friday's close is less than this value,

it counts as the same.

The timeframe should be between day and hour so that Tradingview goes back far enough in the past.

The output (here for BTC)

Total: 477

Lower: 20%

Equal: 55%

Higher: 25%

is displayed in the chart, but also output via the log function.

Optimal Buy Day (Zeiierman)█ Overview

The Optimal Buy Day (Zeiierman) indicator identifies optimal buying days based on historical price data, starting from a user-defined year. It simulates investing a fixed initial capital and making regular monthly contributions. The unique aspect of this indicator involves comparing systematic investment on specific days of the month against a randomized buying day each month, aiming to analyze which method might yield more shares or a better average price over time. By visualizing the potential outcomes of systematic versus randomized buying, traders can better understand the impact of market timing and how regular investments might accumulate over time.

These statistics are pivotal for traders and investors using the script to analyze historical performance and strategize future investments. By understanding which days offered more shares for their money or lower average prices, investors can tailor their buying strategies to potentially enhance returns.

█ Key Statistics

⚪ Shares

Definition: Represents the total number of shares acquired on a particular day of the month across the entire simulation period.

How It Works: The script calculates how many shares can be bought each day, given the available capital or monthly contribution. This calculation takes into account the day's opening price and accumulates the total shares bought on that day over the simulation period.

Interpretation: A higher number of shares indicates that the day consistently offered better buying opportunities, allowing the investor to acquire more shares for the same amount of money. This metric is crucial for understanding which days historically provided more value.

⚪ AVG Price

Definition: The average price paid per share on a particular day of the month, averaged over the simulation period.

How It Works: Each time shares are bought, the script calculates the average price per share, factoring in the new shares purchased at the current price. This average evolves over time as more shares are bought at varying prices.

Interpretation: The average price gives insight into the cost efficiency of buying shares on specific days. A lower average price suggests that buying on that day has historically led to better pricing, making it a potentially more attractive investment strategy.

⚪ Buys

Definition: The total number of transactions or buys executed on a particular day of the month throughout the simulation.

How It Works: This metric increments each time shares are bought on a specific day, providing a count of all buying actions taken.

Interpretation: The number of buys indicates the frequency of investment opportunities. A higher count could mean more consistent opportunities for investment, but it's important to consider this in conjunction with the average price and the total shares acquired to assess overall strategy effectiveness.

⚪ Most Shares

Definition: Identifies the day of the month on which the highest number of shares were bought, highlighting the specific day and the total shares acquired.

How It Works: After simulating purchases across all days of the month, the script identifies which day resulted in the highest total number of shares bought.

Interpretation: This metric points out the most opportune day for volume buying. It suggests that historically, this day provided conditions that allowed for maximizing the quantity of shares purchased, potentially due to lower prices or other factors.

⚪ Best Price

Definition: Highlights the day of the month that offered the lowest average price per share, indicating both the day and the price.

How It Works: The script calculates the average price per share for each day and identifies the day with the lowest average.

Interpretation: This metric is key for investors looking to minimize costs. The best price day suggests that historically, buying on this day led to acquiring shares at a more favorable average price, potentially maximizing long-term investment returns.

⚪ Randomized Shares

Definition: This metric represents the total number of shares acquired on a randomly selected day of the month, simulated across the entire period.

How It Works: At the beginning of each month within the simulation, the script selects a random day when the market is open and calculates how many shares can be purchased with the available capital or monthly contribution at that day's opening price. This process is repeated each month, and the total number of shares acquired through these random purchases is tallied.

Interpretation: Randomized shares offer a comparison point to systematic buying strategies. By comparing the total shares acquired through random selection against those bought on the best or worst days, investors can gauge the impact of timing and market fluctuations on their investment strategy. A higher total in randomized shares might indicate that over the long term, the specific days chosen for investment might matter less than consistent market participation. Conversely, if systematic strategies yield significantly more shares, it suggests that timing could indeed play a crucial role in maximizing investment returns.

⚪ Randomized Price

Definition: The average price paid per share for the shares acquired on the randomly selected days throughout the simulation period.

How It Works: Each time shares are bought on a randomly chosen day, the script calculates the average price paid for all shares bought through this randomized strategy. This average price is updated as the simulation progresses, reflecting the cost efficiency of random buying decisions.

Interpretation: The randomized price metric helps investors understand the cost implications of a non-systematic, random investment approach. Comparing this average price to those achieved through more deliberate, systematic strategies can reveal whether consistent investment timing strategies outperform random investment actions in terms of cost efficiency. A lower randomized price suggests that random buying might not necessarily result in higher costs, while a higher average price indicates that systematic strategies might provide better control over investment costs.

█ How to Use

Traders can use this tool to analyze historical data and simulate different investment strategies. By inputting their initial capital, regular contribution amount, and start year, they can visually assess which days might have been more advantageous for buying, based on historical price actions. This can inform future investment decisions, especially for those employing dollar-cost averaging strategies or looking to optimize entry points.

█ Settings

StartYear: This setting allows the user to specify the starting year for the investment simulation. Changing this value will either extend or shorten the period over which the simulation is run. If a user increases the value, the simulation begins later and covers a shorter historical period; decreasing the value starts the simulation earlier, encompassing a longer time frame.

Capital: Determines the initial amount of capital with which the simulation begins. Increasing this value simulates starting with more capital, which can affect the number of shares that can be initially bought. Decreasing this value simulates starting with less capital.

Contribution: Sets the monthly financial contribution added to the investment within the simulation. A higher contribution increases the investment each month and could lead to more shares being purchased over time. Lowering the contribution decreases the monthly investment amount.

-----------------

Disclaimer

The information contained in my Scripts/Indicators/Ideas/Algos/Systems does not constitute financial advice or a solicitation to buy or sell any securities of any type. I will not accept liability for any loss or damage, including without limitation any loss of profit, which may arise directly or indirectly from the use of or reliance on such information.

All investments involve risk, and the past performance of a security, industry, sector, market, financial product, trading strategy, backtest, or individual's trading does not guarantee future results or returns. Investors are fully responsible for any investment decisions they make. Such decisions should be based solely on an evaluation of their financial circumstances, investment objectives, risk tolerance, and liquidity needs.

My Scripts/Indicators/Ideas/Algos/Systems are only for educational purposes!

Crypto MVRV ZScore - Strategy [PresentTrading]█ Introduction and How it is Different

The "Crypto Valuation Extremes: MVRV ZScore - Strategy " represents a cutting-edge approach to cryptocurrency trading, leveraging the Market Value to Realized Value (MVRV) Z-Score. This metric is pivotal for identifying overvalued or undervalued conditions in the crypto market, particularly Bitcoin. It assesses the current market valuation against the realized capitalization, providing insights that are not apparent through conventional analysis.

BTCUSD 6h Long/Short Performance

Local

█ Strategy, How It Works: Detailed Explanation

The strategy leverages the Market Value to Realized Value (MVRV) Z-Score, specifically designed for cryptocurrencies, with a focus on Bitcoin. This metric is crucial for determining whether Bitcoin is currently undervalued or overvalued compared to its historical 'realized' price. Below is an in-depth explanation of the strategy's components and calculations.

🔶Conceptual Foundation

- Market Capitalization (MC): This represents the total dollar market value of Bitcoin's circulating supply. It is calculated as the current price of Bitcoin multiplied by the number of coins in circulation.

- Realized Capitalization (RC): Unlike MC, which values all coins at the current market price, RC is computed by valuing each coin at the price it was last moved or traded. Essentially, it is a summation of the value of all bitcoins, priced at the time they were last transacted.

- MVRV Ratio: This ratio is derived by dividing the Market Capitalization by the Realized Capitalization (The ratio of MC to RC (MVRV Ratio = MC / RC)). A ratio greater than 1 indicates that the current price is higher than the average price at which all bitcoins were purchased, suggesting potential overvaluation. Conversely, a ratio below 1 suggests undervaluation.

🔶 MVRV Z-Score Calculation

The Z-Score is a statistical measure that indicates the number of standard deviations an element is from the mean. For this strategy, the MVRV Z-Score is calculated as follows:

MVRV Z-Score = (MC - RC) / Standard Deviation of (MC - RC)

This formula quantifies Bitcoin's deviation from its 'normal' valuation range, offering insights into market sentiment and potential price reversals.

🔶 Spread Z-Score for Trading Signals

The strategy refines this approach by calculating a 'spread Z-Score', which adjusts the MVRV Z-Score over a specific period (default: 252 days). This is done to smooth out short-term market volatility and focus on longer-term valuation trends. The spread Z-Score is calculated as follows:

Spread Z-Score = (Market Z-Score - MVVR Ratio - SMA of Spread) / Standard Deviation of Spread

Where:

- SMA of Spread is the simple moving average of the spread over the specified period.

- Spread refers to the difference between the Market Z-Score and the MVRV Ratio.

🔶 Trading Signals

- Long Entry Condition: A long (buy) signal is generated when the spread Z-Score crosses above the long entry threshold, indicating that Bitcoin is potentially undervalued.

- Short Entry Condition: A short (sell) signal is triggered when the spread Z-Score falls below the short entry threshold, suggesting overvaluation.

These conditions are based on the premise that extreme deviations from the mean (as indicated by the Z-Score) are likely to revert to the mean over time, presenting opportunities for strategic entry and exit points.

█ Practical Application

Traders use these signals to make informed decisions about opening or closing positions in the Bitcoin market. By quantifying market valuation extremes, the strategy aims to capitalize on the cyclical nature of price movements, identifying high-probability entry and exit points based on historical valuation norms.

█ Trade Direction

A unique feature of this strategy is its configurable trade direction. Users can specify their preference for engaging in long positions, short positions, or both. This flexibility allows traders to tailor the strategy according to their risk tolerance, market outlook, or trading style, making it adaptable to various market conditions and trader objectives.

█ Usage

To implement this strategy, traders should first adjust the input parameters to align with their trading preferences and risk management practices. These parameters include the trade direction, Z-Score calculation period, and the thresholds for long and short entries. Once configured, the strategy automatically generates trading signals based on the calculated spread Z-Score, providing clear indications for potential entry and exit points.

It is advisable for traders to backtest the strategy under different market conditions to validate its effectiveness and adjust the settings as necessary. Continuous monitoring and adjustment are crucial, as market dynamics evolve over time.

█ Default Settings

- Trade Direction: Both (Allows for both long and short positions)

- Z-Score Calculation Period: 252 days (Approximately one trading year, capturing a comprehensive market cycle)

- Long Entry Threshold: 0.382 (Indicative of moderate undervaluation)

- Short Entry Threshold: -0.382 (Signifies moderate overvaluation)

These default settings are designed to balance sensitivity to market valuation extremes with a pragmatic approach to trade execution. They aim to filter out noise and focus on significant market movements, providing a solid foundation for both new and experienced traders looking to exploit the unique insights offered by the MVRV Z-Score in the cryptocurrency market.

LIT - Timings Fx MartinThe Asia Liquidity Points Indicator is a powerful tool designed for traders to identify key liquidity points during the Asia trading session. This script is tailored specifically to aid traders in capitalizing on the unique characteristics of Asian markets, providing invaluable insights into liquidity zones that can significantly enhance trading decisions.

Key Features:

Asia Session Focus: The indicator focuses exclusively on the Asia trading session, which encompasses the trading activity primarily in the Asian markets such as Tokyo, Hong Kong, Singapore, and others.

Liquidity Zones Identification: The script utilizes advanced algorithms to identify and map out liquidity zones within the Asia trading session. These zones represent areas where significant buying or selling pressure is likely to occur, thus presenting lucrative trading opportunities.

Customizable Parameters: Traders have the flexibility to customize various parameters such as time frame, sensitivity, and display options to suit their trading preferences and strategies.

Visual Alerts: The indicator provides visual alerts on the trading chart, clearly indicating the location and strength of liquidity points. This feature enables traders to quickly identify potential entry or exit points based on the liquidity dynamics in the market.

Real-Time Updates: The script continuously monitors market activity during the Asia session, providing real-time updates on liquidity points as they evolve. This ensures traders stay informed and adaptable to changing market conditions.

Integration with Trading Strategies: The Asia Liquidity Points Indicator seamlessly integrates with various trading strategies, serving as a valuable tool for both discretionary and algorithmic traders. Whether used in isolation or in combination with other technical analysis tools, this indicator can enhance trading performance and profitability.

User-Friendly Interface: The indicator boasts a user-friendly interface, making it accessible to traders of all levels of experience. Whether you are a novice trader or a seasoned professional, you can easily incorporate this tool into your trading arsenal.

In conclusion, the Asia Liquidity Points Indicator offers traders a strategic advantage in navigating the nuances of the Asia trading session. By identifying key liquidity zones and providing real-time insights, this script empowers traders to make informed decisions and capitalize on lucrative trading opportunities in the dynamic Asian markets.

Blockunity Address Synthesis (BAS)Track the address status of the various cryptoassets and their evolution.

The Idea

The goal is to provide a simple tool for visualizing the evolution of different types of crypto addresses.

How to Use

This tool is to be used as fundamental information. It is not intended for investment or trading purposes.

Elements

Active Addresses

Active Addresses represent the subset of total addresses that made one or more on-chain transaction on a given day.

New Addresses

New Addresses refer to addresses that receive their first deposit in the selected crypto-asset.

Zero Balance Addresses

Zero Balance Addresses are addresses that transferred out (potentially sold) all of their holdings for the selected crypto-asset.

Total Addresses

Total Addresses refer to the overall count of unique addresses that have been created on a blockchain network.

Settings

In the settings, you can :

Adjust line smoothing (in terms of number of days).

Change the lookback period used to calculate the different variations.

Display or not the different address types (for better visualization, Total Addresses should be shown alone).

Show or hide labels and configure their offset.

Lastly, you can modify all table parameters.

Crypto Stablecoin Supply - Indicator [presentTrading]█ Introduction and How it is Different

The "Stablecoin Supply - Indicator" differentiates itself by focusing on the aggregate supply of major stablecoins—USDT, USDC, and DAI—rather than traditional price-based metrics. Its premise is that fluctuations in the total supply of these stablecoins can serve as leading indicators for broader market movements, offering traders a unique vantage point to anticipate shifts in market sentiment.

BTCUSD 6h for recent bull market

BTCUSD 8h

█ Strategy, How it Works: Detailed Explanation

🔶 Data Collection

The strategy begins with the collection of the closing supply for USDT, USDC, and DAI stablecoins. This data is fetched using a specified timeframe (**`tfInput`**), allowing for flexibility in analysis periods.

🔶 Supply Calculation

The individual supplies of USDT, USDC, and DAI are then aggregated to determine the total stablecoin supply within the market at any given time. This combined figure serves as the foundation for the subsequent statistical analysis.

🔶 Z-Score Computation

The heart of the indicator's strategy lies in the computation of the Z-Score, which is a statistical measure used to identify how far a data point is from the mean, relative to the standard deviation. The formula for the Z-Score is:

Z = (X - μ) / σ

Where:

- Z is the Z-Score

- X is the current total stablecoin supply (TotalStablecoinClose)

- μ (mu) is the mean of the total stablecoin supply over a specified length (len)

- σ (sigma) is the standard deviation of the total stablecoin supply over the same length

A moving average of the Z-Score (**`zScore_ma`**) is calculated over a short period (defaulted to 3) to smooth out the volatility and provide a clearer signal.

🔶 Signal Interpretation

The Z-Score itself is plotted, with its color indicating its relation to a defined threshold (0.382), serving as a direct visual cue for market sentiment. Zones are also highlighted to show when the Z-Score is within certain extreme ranges, suggesting overbought or oversold conditions.

Bull -> Bear

█ Trade Direction

- **Entry Threshold**: A Z-Score crossing above 0.382 suggests an increase in stablecoin supply relative to its historical average, potentially indicating bullish market sentiment or incoming capital flow into cryptocurrencies.

- **Exit Threshold**: Conversely, a Z-Score dropping below -0.382 may signal a reduction in stablecoin supply, hinting at bearish sentiment or capital withdrawal.

█ Usage

Traders can leverage the "Stablecoin Supply - Indicator" to gain insights into the underlying market dynamics that are not immediately apparent through price analysis alone. It is particularly useful for identifying potential shifts in market sentiment before they are reflected in price movements. By integrating this indicator with other technical analysis tools, traders can develop a more rounded and informed trading strategy.

█ Default Settings

- Timeframe Input (`tfInput`): Allows users to specify the timeframe for data collection, adding flexibility to the analysis.

- Z-Score Length (`len`): Set to 252 by default, representing the period over which the mean and standard deviation of the stablecoin supply are calculated.

- Color Coding: Uses distinct colors (green for bullish, red for bearish) to indicate the Z-Score's position relative to its thresholds, enhancing visual clarity.

- Extreme Range Fill: Highlights areas between defined high and low Z-Score thresholds with distinct colors to indicate potential overbought or oversold conditions.

By integrating considerations of stablecoin supply into the analytical framework, the "Stablecoin Supply - Indicator" offers a novel perspective on cryptocurrency market dynamics, enabling traders to make more nuanced and informed decisions.

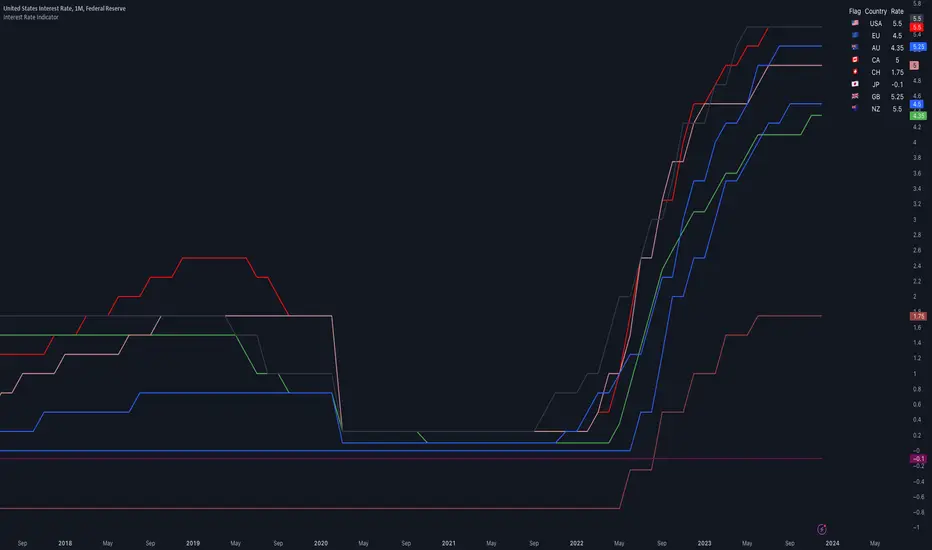

Interest Rate IndicatorThis script offers a overview of Year-over-Year (YoY) interest rates for key countries. The interest rate data utilized by default are sourced from TradingView Tickers, but they can be modified to any preferred source via the settings.

The script does not perform any calculations; its primary function is to present a comparative view of interest rates across different countries in a single indicator.

Key features include:

Interest rate data for the USA, European Union, Australia, Canada, Switzerland, Japan, United Kingdom, and New Zealand (Interest Rate Symbols are editable in the settings).

A table displaying country flags, names, and the latest interest rates, providing a clear and immediate comparison.

Country-representative colors for easy identification and visual distinction between different countries' data.

This indicator is designed for traders and analysts looking for a quick and efficient way to monitor and compare the interest rates of major economies directly within TradingView, facilitating better informed financial and investment decisions.

Debasement Adjusted CAGREquity growth may appear less significant when juxtaposed with the expansion of the money supply. This is because markets tend to adjust prices to reflect changes in money supply almost immediately.

Our indicator offers a unique perspective by adjusting the current ticker price for the M2 money supply and normalizing this data to show the percentage appreciation since the first visible bar on the chart. Users can also select alternative money supply measures, such as the EU-M2, via the indicator's settings.

This approach essentially redefines the price as the "growth of the relative share of the total money supply," providing a novel lens through which to view equity performance.

Additionally, the indicator computes both the Compound Annual Growth Rate (CAGR) and the total growth observed from this adjusted standpoint. These metrics are calculated within the context of the selected time range, adding depth to the analysis.

Although this indicator is compatible with all timeframes, it is primarily designed as a macroeconomic tool. It yields the most meaningful insights when applied to longer-term perspectives, such as weekly or monthly timeframes.

This tool builds upon the foundational work presented in the "Inflation Adjusted Performance Ticker," accessible at Inflation Adjusted Performance Ticker , enhancing its application by normalizing the results and computing CAGR and total growth.