🌀 Vortex Trap OscillatorVortex Oscillator Core

Calculates the difference between upward and downward directional price flow.

Spikes in either direction highlight strong directional bias or potential exhaustion.

Trap Signal Logic

A Bullish Trap is signaled when:

Vortex turns strongly negative (false bearish pressure)

There's a volume burst

Buy/sell tension favors buyers

An RSI bullish divergence is detected

A Bearish Trap is signaled under the inverse conditions.

Volume Burst Filter

Compares current volume to a moving average baseline.

Triggers only when volume surges past a dynamic threshold.

Tension Filter

Compares smoothed buy and sell volumes.

Confirms whether aggressive participants are truly in control.

RSI Divergence Filter

Uses pivot-based divergence detection to validate exhaustion signals.

Adds another layer of trap confirmation.

📈 How To Use:

Overlay Mode: Use alongside price action to visually confirm trap signals.

Entry Timing:

Look for trap markers (▲ for bullish traps below bar, ▼ for bearish traps above bar).

Use confirmation from your own system (e.g. candle patterns, support/resistance).

Exit or Fade Strategy:

Consider fading the trap (trading against the move) if it aligns with higher-timeframe confluence.

Watch for reversal candles near trap zones.

🛠 Settings Tips:

Adjust Vortex Period to control trap sensitivity (shorter = more signals, longer = smoother).

Use Volume Burst Threshold to filter out noise on low-volume assets.

RSI Divergence Depth can be increased on higher timeframes for cleaner divergence reads.

🧠 Best Used For:

Detecting false breakouts

Catching mean reversions after stop hunts

Identifying momentum traps in volatile markets

Filtering aggressive moves that lack volume confirmation

Fundamental Analysis

Nasdaq Market Direction ProbabilitiesA table in the bottom-left corner showing bullish, bearish, and neutral probabilities for Nasdaq market direction, calculated from weighted indicators (moving averages, RSI, volume trend, futures change, and sentiment).

A label on the chart with a recommendation ("Long", "Short", or "Monitor") based on the highest probability.

A histogram of the bullish probability in a separate pane.

The probabilities update on each confirmed bar, using the chart’s timeframe (ideally 60 minutes).

Ticker Industry and Competitor LookupThe Ticker Industry and Competitor Lookup is a comprehensive indicator that provides instant access to industry classification data and competitive intelligence for any ticker symbol. Built using the advanced SIC_TICKER_DATA library, this tool delivers professional-grade sector analysis with enterprise-level performance. It's a simple yet great tool for competitor research, sector studies, portfolio diversification, and investment decision-making.

This indicator is a simple tool built on based on our SIC_TICKER_DATA library to demonstrate the use cases of the library. In this case, you enter a ticker and it displays the sector, SIC or Standard Industrial Classification which is a SEC identifier, and more importantly, the competitors that are listed to be in the exact same SIC by SEC.

There isn't much to say about the indicator itself but we strongly recommend checking out the SIC_TICKER_DATA library we just published to learn more about the types of indicators you can build using it.

Correlation Coefficient with MA & BB中文版介紹

相關係數、移動平均線與布林帶指標 (Correlation Coefficient with MA & BB)

這個 Pine Script 指標是一款強大的工具,旨在幫助交易者和投資者深入分析兩個市場標的之間的關係強度與方向,並結合移動平均線 (MA) 和布林帶 (BB) 來進一步洞察這種關係的趨勢和波動性。

無論您是想尋找配對交易機會、管理投資組合風險,還是僅僅想更好地理解市場動態,這個指標都能提供有價值的見解。

指標特色與功能:

動態相關係數計算:

您可以選擇任何您想比較的股票、商品或加密貨幣代號(例如,預設為 GOOG)。

指標會自動計算當前圖表(主數據源,預設為收盤價)與您指定標的之間的相關係數。

相關係數值介於 -1 (完美負相關) 至 1 (完美正相關) 之間,0 表示無線性關係。

視覺化呈現相關係數線,並標示 1、0、-1 參考水平線,同時填充完美相關區間,讓您一目了然。

特別之處:程式碼中包含了 ticker.modify,確保比較標的數據考慮了股息調整或延長交易時段,使相關性分析更加精準。

相關係數的移動平均線 (MA):

為了平滑相關係數的短期波動,指標提供了多種移動平均線類型供您選擇,包括:SMA、EMA、WMA、SMMA。

您可以設定計算 MA 的週期長度(預設 20 週期)。

這條 MA 線有助於識別相關係數的長期趨勢,判斷兩者關係是趨於增強還是減弱。

相關係數的布林帶 (BB):

將布林帶應用於相關係數,以衡量其波動性和相對高低水平。

中軌與您選擇的移動平均線保持一致。

上軌和下軌則根據相關係數的標準差和您設定的 Z 值(預設 2.0 倍標準差)動態調整。

布林帶可以幫助您識別相關係數何時處於極端水平,可能預示著未來會回歸均值。

如何運用這個指標?

配對交易策略:當兩個通常高度相關的資產,其相關係數短期內顯著偏離平均水平(例如,一個資產價格上漲而另一個原地踏步),您可能可以考慮利用此「失衡」進行配對交易。

投資組合多元化:了解不同資產之間的相關性,有助於構建更穩健的投資組合,避免過度集中於同向變動的資產,有效分散風險。

市場趨勢洞察:透過觀察相關係數的趨勢和波動,您可以更好地理解不同市場板塊或資產類別之間的聯動性,為您的宏觀經濟分析提供數據支持。

請注意,相關性不等於因果性。使用此指標時,請結合您的整體交易策略、宏觀經濟分析以及其他技術指標進行綜合判斷。

English Version Introduction

Correlation Coefficient with Moving Average & Bollinger Bands Indicator (Correlation Coefficient with MA & BB)

This Pine Script indicator is a powerful tool designed to help traders and investors deeply analyze the strength and direction of the relationship between two market instruments. It integrates Moving Averages (MA) and Bollinger Bands (BB) to further insight into the trend and volatility of this relationship.

Whether you're looking for pair trading opportunities, managing portfolio risk, or simply aiming to better understand market dynamics, this indicator can provide valuable insights.

Indicator Features & Functionality:

Dynamic Correlation Coefficient Calculation:

You can select any symbol you wish to compare (e.g., default is GOOG), be it stocks, commodities, or cryptocurrencies.

The indicator automatically calculates the correlation coefficient between the current chart (main data source, default is close price) and your specified symbol.

Correlation values range from -1 (perfect negative correlation) to 1 (perfect positive correlation), with 0 indicating no linear relationship.

It visually plots the correlation line, marks 1, 0, -1 reference levels, and fills the perfect correlation zone for clear visualization.

Special Feature: The code includes ticker.modify, ensuring that the comparative symbol's data accounts for dividend adjustments or extended trading hours, leading to more precise correlation analysis.

Moving Average (MA) for Correlation:

To smooth out short-term fluctuations in the correlation coefficient, the indicator offers multiple MA types for you to choose from: SMA, EMA, WMA, SMMA.

You can set the length of the MA period (default 20 periods).

This MA line helps identify the long-term trend of the correlation coefficient, indicating whether the relationship between the two instruments is strengthening or weakening.

Bollinger Bands (BB) for Correlation:

Bollinger Bands are applied to the correlation coefficient itself to gauge its volatility and relative high/low levels.

The middle band aligns with your chosen Moving Average.

The upper and lower bands dynamically adjust based on the correlation coefficient's standard deviation and your set Z-score (default 2.0 standard deviations).

Bollinger Bands can help you identify when the correlation coefficient is at extreme levels, potentially signaling a future reversion to the mean.

How to Utilize This Indicator:

Pair Trading Strategies: When two typically highly correlated assets show a significant short-term deviation from their average correlation (e.g., one asset's price rises while the other stagnates), you might consider exploiting this "imbalance" for pair trading.

Portfolio Diversification: Understanding the correlation between different assets helps build a more robust investment portfolio, preventing over-concentration in co-moving assets and effectively diversifying risk.

Market Trend Insight: By observing the trend and volatility of the correlation coefficient, you can better understand the联动 (interconnectedness) between different market sectors or asset classes, providing data support for your macroeconomic analysis.

Please note that correlation does not imply causation. When using this indicator, combine it with your overall trading strategy, macroeconomic analysis, and other technical indicators for comprehensive decision-making.

ZYTX GKDDThe ZYTX High-Sell Low-Buy Indicator Strategy is a trend-following indicator that integrates multiple indicator resonances. It demonstrates the perfect performance of an automated trading robot, truly achieving the high-sell low-buy strategy in trading.

Ralph Indicator - ZaraTrust Smart MoneyThe Ralph Indicator – ZaraTrust Smart Money is a powerful yet simple Smart Money Concepts (SMC) based tool designed for traders who want to trade like institutions. It auto-detects high-probability Buy/Sell zones, Support/Resistance levels, and Demand/Supply areas on the chart — giving you clear, visual, and actionable signals without the clutter.

⸻

🔍 Key Features:

✅ Smart Money Structure

• Uses pivot-based logic to identify potential structure points

• Helps you understand market flow (e.g., BOS, CHoCH simplified logic)

✅ Automatic Support & Resistance

• Plots major levels based on significant highs and lows

• Helps catch key reversal or breakout zones

✅ Demand & Supply Zones

• Visually shows areas where price may react strongly

• Based on smart pivot detection from recent swings

✅ Buy/Sell Trade Signals

• Highlights buy when price breaks resistance (possible bullish shift)

• Highlights sell when price breaks support (possible bearish shift)

✅ Clean & Easy UI

• Toggle features on/off from settings panel

• Labels and shapes are plotted clearly on the chart for instant reading

⸻

🛠️ Recommended Use:

• Use on 15min to 4H timeframe for intraday or swing trading

• Combine with price action (e.g., confirmation candles, liquidity grab)

• Works best when paired with institutional logic (OBs, FVG, liquidity)

⸻

⚠️ Disclaimer:

This indicator is a tool, not a signal service.

It does not guarantee 98% accuracy, but it’s designed to highlight smart money zones and high-probability areas. Always do your own risk management and backtest before using on a live account.

10 EMA, 20 EMA & 50 SMAThis script plots three key moving averages on the price chart to help identify trends and potential trade opportunities:

10 EMA (Exponential Moving Average):

A fast-reacting average that captures short-term price momentum. Useful for spotting quick trend changes.

20 EMA (Exponential Moving Average):

A medium-term average that smooths out more noise while still being responsive to price changes.

50 SMA (Simple Moving Average):

A widely-used long-term trend indicator. It smooths price data over a longer period and is often used to define overall market direction.

VampFX Kill Zone🦇 VampFX Kill Zone Indicator

Built for Smart Money Traders by Vamp FX

This custom Kill Zone tool highlights the optimal institutional trading window — when volume, liquidity, and precision align.

🔹 What It Does:

• Shades the VampFX Kill Zone (default: 8:00 AM to 12:30 PM UTC-4 / New York)

• Designed for New York session scalping/sniping

• Helps isolate high-probability Smart Money setups (liquidity sweeps, FVGs, BOS entries)

🔧 Default Settings:

• Timezone: UTC -4 (New York)

• Session Start: 08:00

• Session End: 12:30

• Adjustable to fit your strategy or local session bias

⸻

📈 Why Use It:

The VampFX Kill Zone reflects when algos run, liquidity gets manipulated, and clean entries occur.

Avoid noise — trade when the market actually moves.

“We don’t chase the market. We wait inside the zone… then strike with precision.”

— 🦇 VampFX Code

Real 10Y Yield (DGS10 - T10YIE)The Real 10Y Yield (DGS10 – T10YIE) indicator computes the inflation-adjusted U.S. 10-year Treasury yield by subtracting the 10-year breakeven inflation rate (T10YIE) from the nominal 10-year Treasury yield (DGS10), both sourced directly from FRED. By filtering out inflation expectations, this script reveals the true, real borrowing cost over a 10-year horizon—one of the most reliable gauges of overall risk sentiment and capital–market health.

How It Works

Data Inputs

• DGS10 (Nominal 10-Year Treasury Yield)

• T10YIE (10-Year Breakeven Inflation Rate)

Both series are fetched on a daily timeframe via request.security from FRED.

Real Yield Calculation

pine

Copy

Edit

real10y = DGS10 – T10YIE

A positive value indicates that nominal yields exceed inflation expectations (real yields are positive), while a negative value signals deep-negative real rates.

Thresholds & Coloring

• Bullish Zone: Real yield < –0.1 %

• Bearish Zone: Real yield > +0.1 %

The background turns green when real yields drop below –0.1 %, reflecting an ultra-accommodative environment that historically aligns with risk-on rallies. It turns red when real yields exceed +0.1 %, indicating expensive real borrowing costs and a potential shift toward risk-off.

Alerts

• Deep-Negative Real Yields (Bullish): Triggers when real yield < –0.1 %

• High Real Yields (Bearish): Triggers when real yield > +0.1 %

Why It’s Powerful

Forward-Looking Sentiment Gauge

Real yields incorporate both market-implied inflation and nominal rates, making them a leading indicator for risk appetite, equity flows, and crypto demand.

Clear, Actionable Zones

The –0.1 % / +0.1 % thresholds cleanly delineate structurally bullish vs. bearish regimes, removing noise and false signals common in nominal-only yield studies.

Macro & Cross-Asset Confluence

Combine with equity indices, dollar strength (DXY), or credit spreads for a fully contextual macro view. When real yields break deeper negative alongside weakening dollar, it often precedes stretch in risk assets.

Automatic Alerts

Never miss regime shifts—alerts notify you the moment real yields breach key zones, so you can align your strategy with prevailing macro momentum.

How to Use

Add to a separate pane for unobstructed visibility.

Monitor breaks beneath –0.1 % for early “risk-on” signals in stocks, commodities, and crypto.

Watch for climbs above +0.1 % to hedge or rotate into defensive assets.

Combine with your existing trend-following or mean-reversion strategies to improve timing around major market turning points.

–––

Feel free to adjust the threshold lines to your preferred sensitivity (e.g., tighten to ±0.05 %), or overlay with moving averages to smooth out whipsaws. This script is ideal for macro traders, portfolio managers, and quantitative quants who demand a distilled, inflation-adjusted view of real rates.

National Financial Conditions Index (NFCI)This is one of the most important macro indicators in my trading arsenal due to its reliability across different market regimes. I'm excited to share this with the TradingView community because this Federal Reserve data is not only completely free but extraordinarily useful for portfolio management and risk assessment.

**Important Disclaimers**: Be aware that some NFCI components are updated only monthly but carry significant weighting in the composite index. Additionally, the Fed occasionally revises historical NFCI data, so historical backtests should be interpreted with some caution. Nevertheless, this remains a crucial leading indicator for financial stress conditions.

---

## What is the National Financial Conditions Index?

The National Financial Conditions Index (NFCI) is a comprehensive measure of financial stress and liquidity conditions developed by the Federal Reserve Bank of Chicago. This indicator synthesizes over 100 financial market variables into a single, interpretable metric that captures the overall state of financial conditions in the United States (Brave & Butters, 2011).

**Key Principle**: When the NFCI is positive, financial conditions are tighter than average; when negative, conditions are looser than average. Values above +1.0 historically coincide with financial crises, while values below -1.0 often signal bubble-like conditions.

## Scientific Foundation & Research

The NFCI methodology is grounded in extensive academic research:

### Core Research Foundation

- **Brave, S., & Butters, R. A. (2011)**. "Monitoring financial stability: A financial conditions index approach." *Economic Perspectives*, 35(1), 22-43.

- **Hatzius, J., Hooper, P., Mishkin, F. S., Schoenholtz, K. L., & Watson, M. W. (2010)**. "Financial conditions indexes: A fresh look after the financial crisis." *US Monetary Policy Forum Report*, No. 23.

- **Kliesen, K. L., Owyang, M. T., & Vermann, E. K. (2012)**. "Disentangling diverse measures: A survey of financial stress indexes." *Federal Reserve Bank of St. Louis Review*, 94(5), 369-397.

### Methodological Validation

The NFCI employs Principal Component Analysis (PCA) to extract common factors from financial market data, following the methodology established by **English, W. B., Tsatsaronis, K., & Zoli, E. (2005)** in "Assessing the predictive power of measures of financial conditions for macroeconomic variables." The index has been validated through extensive academic research (Koop & Korobilis, 2014).

## NFCI Components Explained

This indicator provides access to all five official NFCI variants:

### 1. **Main NFCI**

The primary composite index incorporating all financial market sectors. This serves as the main signal for portfolio allocation decisions.

### 2. **Adjusted NFCI (ANFCI)**

Removes the influence of credit market disruptions to focus on non-credit financial stress. Particularly useful during banking crises when credit markets may be impaired but other financial conditions remain stable.

### 3. **Credit Sub-Index**

Isolates credit market conditions including corporate bond spreads, commercial paper rates, and bank lending standards. Important for assessing corporate financing stress.

### 4. **Leverage Sub-Index**

Measures systemic leverage through margin requirements, dealer financing, and institutional leverage metrics. Useful for identifying leverage-driven market stress.

### 5. **Risk Sub-Index**

Captures market-based risk measures including volatility, correlation, and tail risk indicators. Provides indication of risk appetite shifts.

## Practical Trading Applications

### Portfolio Allocation Framework

Based on the academic research, the NFCI can be used for portfolio positioning:

**Risk-On Positioning (NFCI declining):**

- Consider increasing equity exposure

- Reduce defensive positions

- Evaluate growth-oriented sectors

**Risk-Off Positioning (NFCI rising):**

- Consider reducing equity exposure

- Increase defensive positioning

- Favor large-cap, dividend-paying stocks

### Academic Validation

According to **Oet, M. V., Eiben, R., Bianco, T., Gramlich, D., & Ong, S. J. (2011)** in "The financial stress index: Identification of systemic risk conditions," financial conditions indices like the NFCI provide early warning capabilities for systemic risk conditions.

**Illing, M., & Liu, Y. (2006)** demonstrated in "Measuring financial stress in a developed country: An application to Canada" that composite financial stress measures can be useful for predicting economic downturns.

## Advanced Features of This Implementation

### Dynamic Background Coloring

- **Green backgrounds**: Risk-On conditions - potentially favorable for equity investment

- **Red backgrounds**: Risk-Off conditions - time for defensive positioning

- **Intensity varies**: Based on deviation from trend for nuanced risk assessment

### Professional Dashboard

Real-time analytics table showing:

- Current NFCI level and interpretation (TIGHT/LOOSE/NEUTRAL)

- Individual sub-index readings

- Change analysis

- Portfolio guidance (Risk On/Risk Off)

### Alert System

Professional-grade alerts for:

- Risk regime changes

- Extreme stress conditions (NFCI > 1.0)

- Bubble risk warnings (NFCI < -1.0)

- Major trend reversals

## Optimal Usage Guidelines

### Best Timeframes

- **Daily charts**: Recommended for intermediate-term positioning

- **Weekly charts**: Suitable for longer-term portfolio allocation

- **Intraday**: Less effective due to weekly update frequency

### Complementary Indicators

For enhanced analysis, combine NFCI signals with:

- **VIX levels**: Confirm stress readings

- **Credit spreads**: Validate credit sub-index signals

- **Moving averages**: Determine overall market trend context

- **Economic surprise indices**: Gauge fundamental backdrop

### Position Sizing Considerations

- **Extreme readings** (|NFCI| > 1.0): Consider higher conviction positioning

- **Moderate readings** (|NFCI| 0.3-1.0): Standard position sizing

- **Neutral readings** (|NFCI| < 0.3): Consider reduced conviction

## Important Limitations & Considerations

### Data Frequency Issues

**Critical Warning**: While the main NFCI updates weekly (typically Wednesdays), some underlying components update monthly. Corporate bond indices and commercial paper rates, which carry significant weight, may cause delayed reactions to current market conditions.

**Component Update Schedule:**

- **Weekly Updates**: Main NFCI composite, most equity volatility measures

- **Monthly Updates**: Corporate bond spreads, commercial paper rates

- **Quarterly Updates**: Banking sector surveys

- **Impact**: Significant portion of index weight may lag current conditions

### Historical Revisions

The Federal Reserve occasionally revises NFCI historical data as new information becomes available or methodologies are refined. This means backtesting results should be interpreted cautiously, and the indicator works best for forward-looking analysis rather than precise historical replication.

### Market Regime Dependency

The NFCI effectiveness may vary across different market regimes. During extended sideways markets or regime transitions, signals may be less reliable. Consider combining with trend-following indicators for optimal results.

**Bottom Line**: Use NFCI for medium-term portfolio positioning guidance. Trust the directional signals while remaining aware of data revision risks and update frequency limitations. This indicator is particularly valuable during periods of financial stress when reliable guidance is most needed.

---

**Data Source**: Federal Reserve Bank of Chicago

**Update Frequency**: Weekly (typically Wednesdays)

**Historical Coverage**: 1973-present

**Cost**: Free (public Fed data)

*This indicator is for educational and analytical purposes. Always conduct your own research and risk assessment before making investment decisions.*

## References

Brave, S., & Butters, R. A. (2011). Monitoring financial stability: A financial conditions index approach. *Economic Perspectives*, 35(1), 22-43.

English, W. B., Tsatsaronis, K., & Zoli, E. (2005). Assessing the predictive power of measures of financial conditions for macroeconomic variables. *BIS Papers*, 22, 228-252.

Hatzius, J., Hooper, P., Mishkin, F. S., Schoenholtz, K. L., & Watson, M. W. (2010). Financial conditions indexes: A fresh look after the financial crisis. *US Monetary Policy Forum Report*, No. 23.

Illing, M., & Liu, Y. (2006). Measuring financial stress in a developed country: An application to Canada. *Bank of Canada Working Paper*, 2006-02.

Kliesen, K. L., Owyang, M. T., & Vermann, E. K. (2012). Disentangling diverse measures: A survey of financial stress indexes. *Federal Reserve Bank of St. Louis Review*, 94(5), 369-397.

Koop, G., & Korobilis, D. (2014). A new index of financial conditions. *European Economic Review*, 71, 101-116.

Oet, M. V., Eiben, R., Bianco, T., Gramlich, D., & Ong, S. J. (2011). The financial stress index: Identification of systemic risk conditions. *Federal Reserve Bank of Cleveland Working Paper*, 11-30.

Crowding model ║ BullVision🔬 Overview

The Crypto Crowding Model Pro is a sophisticated analytical tool designed to visualize and quantify market conditions across multiple cryptocurrencies. By leveraging Relative Strength Index (RSI) and Z-score calculations, this indicator provides traders with an intuitive and detailed snapshot of current crypto market dynamics, highlighting areas of extreme momentum, crowded trades, and potential reversal points.

⚙️ Key Concepts

📊 RSI and Z-Score Analysis

RSI (Relative Strength Index) evaluates the momentum and strength of each cryptocurrency, identifying overbought or oversold conditions.

Z-Score Normalization measures each asset's current price deviation relative to its historical average, identifying statistically significant extremes.

🎯 Crowding Analytics

An integrated analytics panel provides real-time crowding metrics, quantifying market sentiment into four distinct categories:

🔥 FOMO (Fear of Missing Out): High momentum, potential exhaustion.

❄️ Fear: Low momentum, potential reversal or consolidation.

📈 Recovery: Moderate upward momentum after a downward trend.

💪 Strength: Stable bullish conditions with sustained momentum.

🖥️ Visual Scatter Plot

Assets are plotted on a dynamic scatter plot, positioning each cryptocurrency according to its RSI and Z-score.

Color coding, symbol shapes, and sizes help quickly identify main market segments (BTC, ETH, TOTAL, OTHERS) and individual asset conditions.

🧩 Quadrant Classification

Assets are categorized into four quadrants based on their momentum and deviation:

Overbought Extended: High RSI and positive Z-score.

Recovery Phase: Low RSI but positive Z-score.

Oversold Compressed: Low RSI and negative Z-score.

Strong Consolidation: High RSI but negative Z-score.

🔧 User Customization

🎨 Visual Settings

Bar Scale: Adjust the scatter plot visual scale.

Asset Visibility: Optionally display key market benchmarks (TOTAL, BTC, ETH, OTHERS).

Gradient Background: Enhances visual interpretation of asset clusters.

Crowding Analytics Panel: Toggle the analytics panel on/off.

📊 Indicator Parameters

RSI Length: Defines the calculation period for RSI.

Z-score Lookback: Historical lookback period for normalization.

Crowding Alert Threshold: Sets alert sensitivity for crowded market conditions.

🎯 Zone Settings

Quadrant Labels: Displays descriptive labels for each quadrant.

Danger Zones: Highlights extreme RSI levels indicative of heightened market risk.

📈 Visual Output

Dynamic Scatter Plot: Visualizes asset positioning clearly and intuitively.

Gradient and Grid: Professional gridlines and subtle gradient backgrounds assist visual assessment.

Danger Zone Highlights: Visually indicates RSI extremes to warn of potential market turning points.

Crowding Analytics Panel: Real-time summary of market sentiment and asset distribution.

🔍 Use Cases

This indicator is particularly beneficial for traders and analysts looking to:

Identify crowded trades and potential reversal points.

Quickly assess overall market sentiment and individual asset strength.

Integrate a robust momentum analysis into broader technical or fundamental strategies.

Enhance market timing and improve risk management decisions.

⚠️ Important Notes

This indicator does not provide explicit buy or sell signals.

It is intended solely for informational, analytical, and educational purposes.

Past performance and signals are not indicative of future market results.

Always combine with additional tools and analysis as part of comprehensive decision-making.

Buy sell Trend VolumeThis indicator analyzes the flow of volume and price changes to identify potential trends.

Understanding Volume Indicator: A Comprehensive Guide

Introduction. The volume indicator is a vital tool investors and traders use to understand the liquidity and market activity in trading.

Auto LevelsSimple auto level tracker that automatically detects and plots the high/low for the current week, day, and month, as well as the previous week/day/month.

Includes a built-in dashboard that shows how close or far price is from each level, along with directional guidance (above/below). The closest level to current price is automatically highlighted for quick awareness.

Everything is fully toggleable to only show the levels and info that is needed.

Asset Premium/Discount Monitor📊 Overview

The Asset Premium/Discount Monitor is a tool for analyzing the relative value between two correlated assets. It measures when one asset is trading at a premium or discount compared to its historical relationship with another asset, helping traders identify potential mean reversion opportunities, or pairs trading opportunities.

🎯 Use Cases

Perfect for analyzing:

NASDAQ:MSTR vs CRYPTO:BTCUSD - MicroStrategy's premium/discount to Bitcoin

NASDAQ:COIN vs BITSTAMP:BTCUSD - Coinbase's relative value to Bitcoin

NASDAQ:TSLA vs NASDAQ:QQQ - Tesla's premium to tech sector

Regional banks AMEX:KRE vs AMEX:XLF - Individual bank stocks vs financial sector

Any two correlated assets where relative value matters

Example of a trade: MSTR vs BTC - When indicator shows MSTR at 95% percentile (extreme premium): Short MSTR, Buy BTC. Then exit when the spread reverts to the mean, say 40-60% percentile.

🔧 How It Works

Core Calculation

Ratio Analysis: Calculates the price ratio between your asset and the correlated asset

Historical Baseline: Establishes the "normal" relationship using a 252-day moving average. You can change this.

Premium Measurement: Measures current deviation from historical average as a percentage

Statistical Context: Provides percentile rankings and standard deviation bands

The Math

Premium % = (Current Ratio / Historical Average Ratio - 1) × 100

🎨 Customization Options

Correlated Asset: Choose any symbol for comparison

Lookback Period: Adjust historical baseline (50-1000 days)

Smoothing: Reduce noise with moving average (1-50 days)

Visual Toggles: Show/hide bands and percentile lines

Color Themes: Customize premium/discount colors

📊 Interpretation Guide

Premium/Discount Reading

Positive %: Asset trading above historical relationship (premium)

Negative %: Asset trading below historical relationship (discount)

Near 0%: Asset at fair value relative to correlation

Percentile Ranking

90%+: Near recent highs - potential selling opportunity

10% and below: Near recent lows - potential buying opportunity

25-75%: Normal trading range

Signal Classifications

🔴 SELL PREMIUM: Asset expensive relative to recent range

🟡 Premium Rich: Moderately expensive, monitor for reversal

⚪ NEUTRAL: Fair value territory

🟡 Discount Opportunity: Moderately cheap, potential accumulation zone

🟢 BUY DISCOUNT: Asset cheap relative to recent range

🚨 Built-in Alerts

Extreme Premium Alert: Triggers when percentile > 95%

Extreme Discount Alert: Triggers when percentile < 5%

⚠️ Important Notes

Works best with highly correlated assets

Historical relationships can change - monitor correlation strength

Not investment advice - use as one factor in your analysis

Backtest thoroughly before implementing any strategy

🔄 Updates & Future Features

This indicator will be continuously improved based on user feedback. So... please give me your feedback!

Price Ranged FVG📌 Price Ranged FVG

Is a clean and efficient tool designed to detect Fair Value Gaps (FVGs) with adjustable filters and structural context. It’s especially useful for traders looking to filter out insignificant gaps and focus on high-probability areas, particularly around swing breaks or structural shifts.

🧠 What is a Fair Value Gap (FVG)?

A Fair Value Gap appears when there’s a price imbalance between candles — typically after a strong move — where the market skips over certain price levels without trading there. These zones can act as potential areas for price to return to (mean reversion), or serve as support/resistance depending on market structure.

🔍 FVG Detection Types

You can choose between three different detection modes under the "FVG Detection" input:

Same Type: Only detects FVGs where the last 3 candles are in the same direction (all bullish or all bearish).

All: Detects any FVG, regardless of candle direction.

Twin Close: Detects FVGs only when the last two candles are in the same direction and close accordingly — offering a stricter confirmation.

🎯 FVG % Filters

To filter out noise or insignificant gaps, this indicator includes:

Minimum FVG % Filter: Ignores FVGs smaller than your specified percentage of the current close.

Maximum FVG % Filter: Ignores overly large gaps that may be unreliable or caused by anomalies.

These filters help focus on relevant FVGs that are more likely to act as reaction zones.

🏛 Structural Context (Swing Highs and Lows)

The indicator plots swing highs and swing lows with dots to provide structure-based context:

Set Swing Strength to 3 for detecting internal structure (shorter-term moves).

Use a higher setting like 5 to focus on external structure (more significant highs/lows).

These levels can help you determine whether an FVG is forming within a consolidation, breakout, or key structural transition.

✅ Use Case (My Personal Workflow)

I personally use this indicator to:

Filter out weak or irrelevant FVGs using the % filters.

Watch for price interaction at swing breaks — especially when an FVG aligns with a break in internal or external structure.

Refine entry and exit planning in confluence with other tools or strategies.

⚠️ Disclaimer

This indicator is not financial advice. It is a technical analysis tool intended to support your own decision-making process. Always do your own research and risk management.

Greer Value Yields Line📈 Greer Value Yields Line – Valuation Signal Without the Clutter

Part of the Greer Financial Toolkit, this streamlined indicator tracks four valuation-based yield metrics and presents them clearly via the Data Window, GVY Score badge, and an optional Yield Table:

Earnings Yield (EPS ÷ Price)

FCF Yield (Free Cash Flow ÷ Price)

Revenue Yield (Revenue per Share ÷ Price)

Book Value Yield (Book Value per Share ÷ Price)

✅ Each yield is compared against its historical average

✅ A point is scored for each metric above average (0–4 total)

✅ Color-coded GVY Score badge highlights valuation strength

✅ Yield trend-lines Totals (TVAVG & TVPCT) help assess direction

✅ Clean layout: no chart clutter – just actionable insights

🧮 GVY Score Color Coding (0–4):

⬜ 0 = None (White)

⬜ 1 = Weak (Gray)

🟦 2 = Neutral (Aqua)

🟩 3 = Strong (Green)

🟨 4 = Gold Exceptional (All metrics above average)

Total Value Average Line Color Coding:

🟥 Red – Average trending down

🟩 Green – Average trending up

Ideal for long-term investors focused on fundamental valuation, not short-term noise.

Enable the table and badge for a compact yield dashboard — or keep it minimal with just the Data Window and trend-lines.

Greer Book Value Yield📘 Script Title

Greer Book Value Yield – Valuation Insight Based on Balance Sheet Strength

🧾 Description

Greer Book Value Yield is a valuation-focused indicator in the Greer Financial Toolkit, designed to evaluate how much net asset value (book value) a company provides per share relative to its current market price. This script calculates the Book Value Per Share Yield (BV%) using the formula:

Book Value Yield (%) = Book Value Per Share ÷ Stock Price × 100

This yield helps investors assess whether a stock is trading at a discount or premium to its underlying assets. It dynamically highlights when the yield is:

🟢 Above its historical average (potentially undervalued)

🔴 Below its historical average (potentially overvalued)

🔍 Use Case

Analyze valuation through asset-based metrics

Identify buy opportunities when book value yield is historically high

Combine with other scripts in the Greer Financial Toolkit:

📘 Greer Value – Tracks year-over-year growth consistency across six key metrics

📊 Greer Value Yields Dashboard – Visualizes multiple valuation-based yields

🟢 Greer BuyZone – Highlights long-term technical buy zones

🛠️ Inputs & Data

Uses Book Value Per Share (BVPS) from TradingView’s financial database (Fiscal Year)

Calculates and compares against a static average yield to assess historical valuation

Clean visual feedback via dynamic coloring and overlays

⚠️ Disclaimer

This tool is for educational and informational purposes only and should not be considered financial advice. Always conduct your own research before making investment decisions.

Greer EPS Yield📘 Script Title

Greer EPS Yield – Valuation Insight Based on Earnings Productivity

🧾 Description

Greer EPS Yield is a valuation-focused indicator from the Greer Financial Toolkit, designed to evaluate how efficiently a company generates earnings relative to its current stock price. This script calculates the Earnings Per Share Yield (EPS%), using the formula:

EPS Yield (%) = Earnings Per Share ÷ Stock Price × 100

This yield metric provides a quick snapshot of valuation through the lens of profitability per share. It dynamically highlights when the EPS yield is:

🟢 Above its historical average (potentially undervalued)

🔴 Below its historical average (potentially overvalued)

🔍 Use Case

Quickly assess valuation attractiveness based on earnings yield.

Identify potential buy opportunities when EPS% is above its long-term average.

Combine with other indicators in the Greer Financial Toolkit for a fundamentals-driven investment strategy:

📘 Greer Value – Tracks year-over-year growth consistency across six key metrics

📊 Greer Value Yields Dashboard – Visualizes valuation-based yield metrics

🟢 Greer BuyZone – Highlights long-term technical buy zones

🛠️ Inputs & Data

Uses fiscal year EPS data from TradingView’s built-in financial database.

Tracks a static average EPS Yield to compare current valuation to historical norms.

Clean, intuitive visual with automatic color coding.

⚠️ Disclaimer

This tool is for educational and informational purposes only and should not be considered financial advice. Always conduct your own research before making investment decisions.

H turnoverTrading Value refers to the total monetary amount of all transactions for a particular stock or the entire market over a specific period. It is calculated by multiplying the trading volume (the number of shares traded) by the price at which they were traded. For example, if 10,000 shares of a stock are traded in a day at an average price of 50,000 KRW, the trading value for that day would be 500,000,000 KRW.

Key points about trading value:

Market Activity and Liquidity: A high trading value indicates an active and liquid market.

Flow of Investment Funds: Increasing trading value suggests more money is flowing into the market or a particular stock.

Relationship with Price Movements: When both trading value and price rise together, it often signals strong buying interest. Conversely, significant price changes with low trading value may be less reliable.

Market Sentiment Indicator: Changes in trading value can reflect shifts in investor interest and sentiment.

In summary, trading value is the total amount of money exchanged in trades and serves as an important indicator of market activity, liquidity, and investor sentiment.

Dynamic VWAP: Fair Value & Divergence SuiteDynamic VWAP: Fair Value & Divergence Suite

Dynamic VWAP: Fair Value & Divergence Suite is a comprehensive tool for tracking contextual valuation, overextension, and potential reversal signals in trending markets. Unlike traditional VWAP that anchors to the start of a session or a fixed period, this indicator dynamically resets the VWAP anchor to the most recent swing low. This design allows you to monitor how far price has extended from the most recent significant low, helping identify zones of potential profit-taking or reversion.

Deviation bands (standard deviations above the anchored VWAP) provide a clear visual framework to assess whether price is in a fair value zone (±1σ), moderately extended (+2σ), or in zones of extreme extension (+3σ to +5σ). The indicator also highlights contextual divergence signals, including slope deceleration, weak-volume retests, and deviation failures—giving you actionable confluence around potential reversal points.

Because the anchor updates dynamically, this tool is particularly well suited for trend-following assets like BTC or stocks in sustained moves, where price rarely returns to deep negative deviation zones. For this reason, the indicator focuses on upside extension rather than symmetrical reversion to a long-term mean.

🎯 Key Features

✅ Dynamic Swing Low Anchoring

Continuously re-anchors VWAP to the most recent swing low based on your chosen lookback period.

Provides context for trend progression and overextension relative to structural lows.

✅ Standard Deviation Bands

Plots up to +5σ deviation bands to visualize levels of overextension.

Extended bands (+3σ to +5σ) can be toggled for simplicity.

✅ Conditional Zone Fills

Colored background fills show when price is inside each valuation zone.

Helps you immediately see if price is in fair value, moderately extended, or highly stretched territory.

✅ Divergence Detection

VWAP Slope Divergence: Flags when price makes a higher high but VWAP slope decelerates.

Low Volume Retest: Highlights weak re-tests of VWAP on low volume.

Deviation Failure: Identifies when price reverts back inside +1σ after closing beyond +3σ.

✅ Volume Fallback

If volume is unavailable, uses high-low range as a proxy.

✅ Highly Customizable

Adjust lookbacks, show/hide extended bands, toggle fills, and enable or disable divergences.

🛠️ How to Use

Identify Buy and Sell Zones

Price in the fair value band (±1σ) suggests equilibrium.

Reaching +2σ to +3σ signals increasing overextension and potential areas to take profits.

+4σ to +5σ zones can be used to watch for exhaustion or mean-reversion setups.

Monitor Divergence Signals

Use slope divergence and deviation failures to look for confluence with overextension.

Low volume retests can flag rallies lacking conviction.

Adapt Swing Lookback

30–50 bars: Faster re-anchoring for swing trading.

75–100 bars: More stable anchors for longer-term trends.

🧭 Best Practices

Combine the anchored VWAP with higher timeframe structure.

Confirm signals with other tools (momentum, volume profiles, or trend filters).

Use extended deviation zones as context, not as standalone signals.

⚠️ Disclaimer

This script is for educational and informational purposes only. It does not constitute financial advice or a recommendation to buy or sell any security or asset. Always do your own research and consult a qualified financial professional before making any trading decisions. Past performance does not guarantee future results.

RISK## Main Purpose

The indicator calculates and displays risk levels based on margin requirements and daily settlement prices, helping traders visualize their potential risk exposure.

## Key Features

**Inputs:**

- **Margin for Calculation**: The CME long margin requirement for the asset

- **HTF Margin Line**: An anchor point for higher timeframe margin calculations

**Core Calculations:**

1. **Settlement Price Tracking**: Captures daily settlement prices during specific session times (6:58-6:59 PM ET for close, 6:00-6:01 PM ET for new day open)

2. **Risk Percentage**: Calculates `margin / (point value × settlement price)` - with special handling for Micro contracts (symbols starting with "M") that uses 10× point value

3. **Risk Intervals**: Determines price intervals representing one margin unit of risk

## Visual Display

The indicator plots multiple risk levels on the chart:

- **Settlement price** (orange circles)

- **Globex open** (green circles)

- **Upper/Lower Risk levels** (red circles) - one and two risk intervals away

- **Subdivision levels** (blue crosses) - 25%, 50%, and 75% of each risk interval

- **MHP+ level** (black crosses) - HTF anchor adjusted by risk percentage

- **HTF Anchor** (black crosses)

## Practical Use

This helps futures traders:

- Visualize how far price can move before hitting margin calls

- See risk levels relative to daily settlements

- Plan position sizing and risk management

- Understand exposure in terms of actual margin requirements

The indicator essentially transforms abstract margin numbers into concrete price levels on the chart, making risk management more visual and intuitive.

Opening Range Breakout🧭 Overview

The Open Range Breakout (ORB) indicator is designed to capture and display the initial price range of the trading day (typically the first 15 minutes), and help traders identify breakout opportunities beyond this range. This is a popular strategy among intraday and momentum traders.

🔧 Features

📊 ORB High/Low Lines

Plots horizontal lines for the session’s high and low

🟩 Breakout Zones

Background highlights when price breaks above or below the range

🏷️ Breakout Labels

Text labels marking breakout events

🧭 Session Control

Customizable session input (default: 09:15–09:30 IST)

📍 ORB Line Labels

Text labels anchored to the ORB high and low lines (aligned right)

🔔 Alerts

Configurable alerts for breakout events

⚙️ Adjustable Settings

Show/hide background, labels, session window, etc.

⏱️ Session Logic

• The ORB range is calculated during a defined session window (default: 09:15–09:30).

• During this window, the highest high and lowest low are recorded as ORB High and ORB Low.

📈 Breakout Detection

• Breakout Above: Triggered when price crosses above the ORB High.

• Breakout Below: Triggered when price crosses below the ORB Low.

• Each breakout can trigger:

• A background highlight (green/red)

• A text label (“Breakout ↑” / “Breakout ↓”)

• An optional alert

🔔 Alerts

Two built-in alert conditions:

1. Breakout Above ORB High

• Message: "🔼 Price broke above ORB High: {{close}}"

2. Breakout Below ORB Low

• Message: "🔽 Price broke below ORB Low: {{close}}"

You can create alerts in TradingView by selecting these from the Add Alert window.

📌 Best Use Cases

• Intraday momentum trading

• Breakout and scalping strategies

• First 15-minute range traders (NSE, BSE markets)

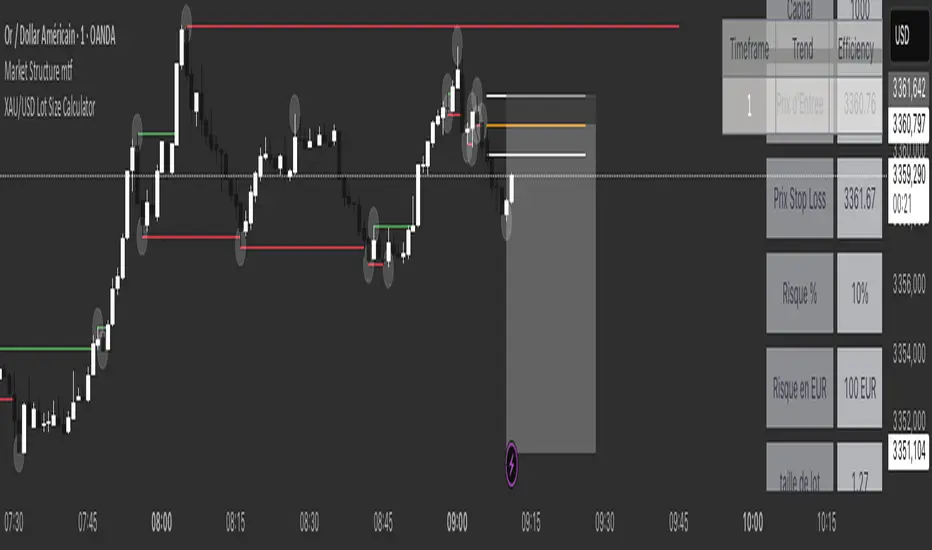

XAU/USD Lot Size CalculatorThis indicator automatically calculates the optimal lot size for XAUUSD (gold) based on the level of risk the trader wants to take. It is designed for traders using MetaTrader 4 or 5 and helps adjust position size according to the specific volatility of gold. The user can set the percentage of capital they are willing to risk on a single trade, for example 1%. The indicator also takes into account the stop loss level, which can be entered in pips or in dollars, as well as the account size (balance or equity).

Based on these parameters, it calculates the exact lot size that matches the risk amount. It then displays on the chart the recommended lot size, the risk amount in dollars, the pip value for XAUUSD, and a confirmation of the stop loss level. This type of indicator is useful for maintaining disciplined risk management and avoiding position sizing errors, especially on a highly volatile asset like gold.