Price Displacement - Candlestick (OHLC) CalculationsA Magical little helper friend for Candle Math.

When composing scripts, it is often necessary to manipulate the math around the OHLC. At times, you want a scalar (absolute) value others you want a vector (+/-). Sometimes you want the open - close and sometimes you want just the positive number of the body size. You might want it in ticks or you might want it in points or you might want in percentages. And every time you try to put it together you waste precious time and brain power trying to think about how to properly structure what you're looking for. Not to mention it's normally not that aesthetically pleasing to look at in the code.

So, this fixes all of that.

Using this library. A function like 'pd.pt(_exp)' can call any kind of candlestick math you need. The function returns the candlestick math you define using particular expressions.

Candle Math Functions Include:

Points:

pt(_exp) Absolute Point Displacement. Point quantity of given size parameters according to _exp.

vpt(_exp) Vector Point Displacement. Point quantity of given size parameters according to _exp.

Ticks:

tick(_exp) Absolute Tick Displacement. Tick quantity of given size parameters according to _exp.

vtick(_exp) Vector Tick Displacement. Tick quantity of given size parameters according to _exp.

Percentages:

pct(_exp, _prec) Absolute Percent Displacement. (w/rounding overload). Percent quantity of bar range of given size parameters according to _exp.

vpct(_exp, _prec) Vector Percent Displacement (w/rounding overload). Percent quantity of bar range of given size parameters according to _exp.

Expressions You Can Use with Formulas:

The expressions are simple (simple strings that is) and I did my best to make them sensible, generally using just the ohlc abreviations. I also included uw, lw, bd, and rg for when you're just trying to pull a candle component out. That way you don't have to think about which of the ohlc you're trying to get just use pd.tick("uw") and now the variable is assigned the length of the upper wick, absolute value, in ticks. If you wanted the vector in pts its pd.vpt("uw"). It also makes changing things easy too as I write it out.

Expression List:

Combinations

"oh" = open - high

"ol" = open - low

"oc" = open - close

"ho" = high - open

"hl" = high - low

"hc" = high - close

"lo" = low - open

"lh" = low - high

"lc" = low - close

"co" = close - open

"ch" = close - high

"cl" = close - low

Candle Components

"uw" = Upper Wick

"bd" = Body

"lw" = Lower Wick

"rg" = Range

Pct() Only

"scp" = Scalar Close Position

"sop" = Scalar Open Position

"vcp" = Vector Close Position

"vop" = Vector Open Position

The attributes are going to be available in the pop up dialogue when you mouse over the function, so you don't really have to remember them. I tried to make that look as efficient as possible. You'll notice it follows the OHLC pattern. Thus, "oh" precedes "ho" (heyo) because "O" would be first in the OHLC. Its a way to help find the expression you're looking for quickly. Like looking through an alphabetized list for traders.

There is a copy/paste console friendly helper list in the script itself.

Additional Notes on the Pct() Only functions:

This is the original reason I started writing this. These concepts place a rating/value on the bar based on candle attributes in one number. These formulas put a open or close value in a percentile of the bar relative to another aspect of the bar.

Scalar - Non-directional. Absolute Value.

Scalar Position: The position of the price attribute relative to the scale of the bar range (high - low)

Example: high = 100. low = 0. close = 25.

(A) Measure price distance C-L. How high above the low did the candle close (e.g. close - low = 25)

(B) Divide by bar range (high - low). 25 / (100 - 0) = .25

Explaination: The candle closed at the 25th percentile of the bar range given the bar range low = 0 and bar range high = 100.

Formula: scp = (close - low) / (high - low)

Vector = Directional.

Vector Position: The position of the price attribute relative to the scale of the bar midpoint (Vector Position at hl2 = 0)

Example: high = 100. low = 0. close = 25.

(A) Measure Price distance C-L: How high above the low did the candle close (e.g. close - low = 25)

(B) Measure Price distance H-C: How far below the high did the candle close (e.g. high - close = 75)

(C) Take Difference: A - B = C = -50

(D) Divide by bar range (high - low). -50 / (100 - 0) = -0.50

Explaination: Candle close at the midpoint between hl2 and the low.

Formula: vcp = { / (high - low) }

Thank you for checking this out. I hope no one else has already done this (because it took half the day) and I hope you find value in it. Be well. Trade well.

Library "PD"

Price Displacement

pt(_exp) Absolute Point Displacement. Point quantity of given size parameters according to _exp.

Parameters:

_exp : (string) Price Parameter

Returns: Point size of given expression as an absolute value.

vpt(_exp) Vector Point Displacement. Point quantity of given size parameters according to _exp.

Parameters:

_exp : (string) Price Parameter

Returns: Point size of given expression as a vector.

tick(_exp) Absolute Tick Displacement. Tick quantity of given size parameters according to _exp.

Parameters:

_exp : (string) Price Parameter

Returns: Tick size of given expression as an absolute value.

vtick(_exp) Vector Tick Displacement. Tick quantity of given size parameters according to _exp.

Parameters:

_exp : (string) Price Parameter

Returns: Tick size of given expression as a vector.

pct(_exp, _prec) Absolute Percent Displacement (w/rounding overload). Percent quantity of bar range of given size parameters according to _exp.

Parameters:

_exp : (string) Expression

_prec : (int) Overload - Place value precision definition

Returns: Percent size of given expression as decimal.

vpct(_exp, _prec) Vector Percent Displacement (w/rounding overload). Percent quantity of bar range of given size parameters according to _exp.

Parameters:

_exp : (string) Expression

_prec : (int) Overload - Place value precision definition

Returns: Percent size of given expression as decimal.

Inputs

honest personal libraryLibrary "honestpersonallibrary"

thestratnumber() this will return the number 1,2 or 3 using the logic from Rob Smiths #thestrat which uses these type of bars for setups

getBodySize() Gets the current candle's body size (in POINTS, divide by 10 to get pips)

Returns: The current candle's body size in POINTS

getTopWickSize() Gets the current candle's top wick size (in POINTS, divide by 10 to get pips)

Returns: The current candle's top wick size in POINTS

getBottomWickSize() Gets the current candle's bottom wick size (in POINTS, divide by 10 to get pips)

Returns: The current candle's bottom wick size in POINTS

getBodyPercent() Gets the current candle's body size as a percentage of its entire size including its wicks

Returns: The current candle's body size percentage

strictBearPinBar(float, float) This it to find pinbars with a very long wick compared to the body that are bearish

Parameters:

float : minTopMulitplier (default=4) The minimum number of times that the top wick has to be bigger than the candle body size

float : maxBottomMultiplier (default=2) The maximum number of times that the bottom wick can be bigger than the candle body size

Returns: a bool function true if current candle is withing the parameters

strictBullPinBar(float, float) This it to find pinbars with a very long wick compared to the body that are bearish

Parameters:

float : minTopMulitplier (default=4) The minimum number of times that the top wick has to be bigger than the candle body size

float : maxBottomMultiplier (default=2) The maximum number of times that the bottom wick can be bigger than the candle body size

Returns: a bool function true if current candle is withing the parameters

Cayoshi_LibraryLibrary "Cayoshi_Library"

fungtion show win loss and Netprofit Show

Library สำหรับเรียกใช้

1.Win_Loss_Show() การแสดง แพ้ ชนะ

2.NetProfit_Show() การแสดงผล Backtest

3.Count_Bar_Back_Test() กำหนดระยะเวลา หรือ แท่งบาร์ในการ Backtest

MovingAveragesLibraryLibrary "MovingAveragesLibrary"

This is a library allowing one to select between many different Moving Average formulas to smooth out any float variable.

You can use this library to apply a Moving Average function to any series of data as long as your source is a float.

The default application would be for applying Moving Averages onto your chart. However, the scope of this library is beyond that. Any indicator or strategy you are building can benefit from this library.

You can apply different types of smoothing and moving average functions to your indicators, momentum oscillators, average true range calculations, support and resistance zones, envelope bands, channels, and anything you can think of to attempt to smooth out noise while finding a delicate balance against lag.

If you are developing an indicator, you can use the 'ave_func' to allow your users to select any Moving Average for any function or variable by creating an input string with the following structure:

var_name = input.string(, , )

Where the types of Moving Average you would like to be provided would be included in options.

Example:

i_ma_type = input.string(title = "Moving Average Type", defval = "Hull Moving Average", options = )

Where you would add after options the strings I have included for you at the top of the PineScript for your convenience.

Then for the output you desire, simply call 'ave_func' like so:

ma = ave_func(source, length, i_ma_type)

Now the plotted Moving Average will be the same as what you or your users select from the Input.

ema(src, len) Exponential Moving Average.

Parameters:

src : Series to use ('close' is used if no argument is supplied).

len : Lookback length to use.

Returns: Float value.

sma(src, len) Simple Moving Average.

Parameters:

src : Series to use ('close' is used if no argument is supplied).

len : Lookback length to use.

Returns: Float value.

rma(src, len) Relative Moving Average.

Parameters:

src : Series to use ('close' is used if no argument is supplied).

len : Lookback length to use.

Returns: Float value.

wma(src, len) Weighted Moving Average.

Parameters:

src : Series to use ('close' is used if no argument is supplied).

len : Lookback length to use.

Returns: Float value.

dv2(len) Donchian V2 function.

Parameters:

len : Lookback length to use.

Returns: Open + Close / 2 for the selected length.

ModFilt(src, len) Modular Filter smoothing function.

Parameters:

src : Series to use ('close' is used if no argument is supplied).

len : Lookback length to use.

Returns: Float value.

EDSMA(src, len) Ehlers Dynamic Smoothed Moving Average.

Parameters:

src : Series to use ('close' is used if no argument is supplied).

len : Lookback length to use.

Returns: EDSMA smoothing.

dema(x, t) Double Exponential Moving Average.

Parameters:

x : Series to use ('close' is used if no argument is supplied).

t : Lookback length to use.

Returns: DEMA smoothing.

tema(src, len) Triple Exponential Moving Average.

Parameters:

src : Series to use ('close' is used if no argument is supplied).

len : Lookback length to use.

Returns: TEMA smoothing.

smma(x, t) Smoothed Moving Average.

Parameters:

x : Series to use ('close' is used if no argument is supplied).

t : Lookback length to use.

Returns: SMMA smoothing.

vwma(x, t) Volume Weighted Moving Average.

Parameters:

x : Series to use ('close' is used if no argument is supplied).

t : Lookback length to use.

Returns: VWMA smoothing.

hullma(x, t) Hull Moving Average.

Parameters:

x : Series to use ('close' is used if no argument is supplied).

t : Lookback length to use.

Returns: Hull smoothing.

covwma(x, t) Coefficient of Variation Weighted Moving Average.

Parameters:

x : Series to use ('close' is used if no argument is supplied).

t : Lookback length to use.

Returns: COVWMA smoothing.

frama(x, t) Fractal Reactive Moving Average.

Parameters:

x : Series to use ('close' is used if no argument is supplied).

t : Lookback length to use.

Returns: FRAMA smoothing.

kama(x, t) Kaufman's Adaptive Moving Average.

Parameters:

x : Series to use ('close' is used if no argument is supplied).

t : Lookback length to use.

Returns: KAMA smoothing.

donchian(len) Donchian Calculation.

Parameters:

len : Lookback length to use.

Returns: Average of the highest price and the lowest price for the specified look-back period.

tma(src, len) Triangular Moving Average.

Parameters:

src : Series to use ('close' is used if no argument is supplied).

len : Lookback length to use.

Returns: TMA smoothing.

VAMA(src, len) Volatility Adjusted Moving Average.

Parameters:

src : Series to use ('close' is used if no argument is supplied).

len : Lookback length to use.

Returns: VAMA smoothing.

Jurik(src, len) Jurik Moving Average.

Parameters:

src : Series to use ('close' is used if no argument is supplied).

len : Lookback length to use.

Returns: JMA smoothing.

MCG(src, len) McGinley smoothing.

Parameters:

src : Series to use ('close' is used if no argument is supplied).

len : Lookback length to use.

Returns: McGinley smoothing.

zlema(series, length) Zero Lag Exponential Moving Average.

Parameters:

series : Series to use ('close' is used if no argument is supplied).

length : Lookback length to use.

Returns: ZLEMA smoothing.

xema(src, len) Optimized Exponential Moving Average.

Parameters:

src : Series to use ('close' is used if no argument is supplied).

len : Lookback length to use.

Returns: XEMA smoothing.

EhlersSuperSmoother(src, lower) Ehlers Super Smoother.

Parameters:

src : Series to use ('close' is used if no argument is supplied).

lower : Smoothing value to use.

Returns: Ehlers Super smoothing.

EhlersEmaSmoother(sig, smoothK, smoothP) Ehlers EMA Smoother.

Parameters:

sig : Series to use ('close' is used if no argument is supplied).

smoothK : Lookback length to use.

smoothP : Smothing value to use.

Returns: Ehlers EMA smoothing.

ave_func(in_src, in_len, in_type) Returns the source after running it through a Moving Average function.

Parameters:

in_src : Series to use ('close' is used if no argument is supplied).

in_len : Lookback period to be used for the Moving Average function.

in_type : Type of Moving Average function to use. Must have a string input to select the options from that MUST match the type-casing in the function below.

Returns: The source as a float after running it through the Moving Average function.

utilsLibrary "utils"

ma_smooth(alg, src, len) Calculates various moving averages

Parameters:

alg : Smoothing algorithm to use

src : Source data

len : Length of moving average

Signal_transcoder_libraryLibrary "Signal_transcoder_library"

This is my 2nd iteration for sending Signals via Plots. (first one was the 8bit Version)

Now a cleaner approach (thanks for the hints @lonesometheblue)

_16bit_encode()

Input a 16 bool Array

Outputs a Float for transmitting via Plot

_16bit_decode()

Input a Float from plot via input-mapping

Outputs a Array of 16 bools

Future Ideas:

Transmitting 2-4 Ints (-127 to 127) and Bools

Signal_Data_2021_09_09__2021_11_18Library "Signal_Data_2021_09_09__2021_11_18"

Functions to support my timing signals system

import_start_time(harmonic) get the start time for each harmonic signal

Parameters:

harmonic : is an integer identifying the harmonic

Returns: the starting timestamp of the harmonic data

import_signal(index, harmonic) access point for pre-processed data imported here by copy paste

Parameters:

index : is the current data index, use 0 to initialize

harmonic : is the data set to index, use 0 to initialize

Returns: the data from the indicated harmonic array starting at index, and the starting timestamp of that data

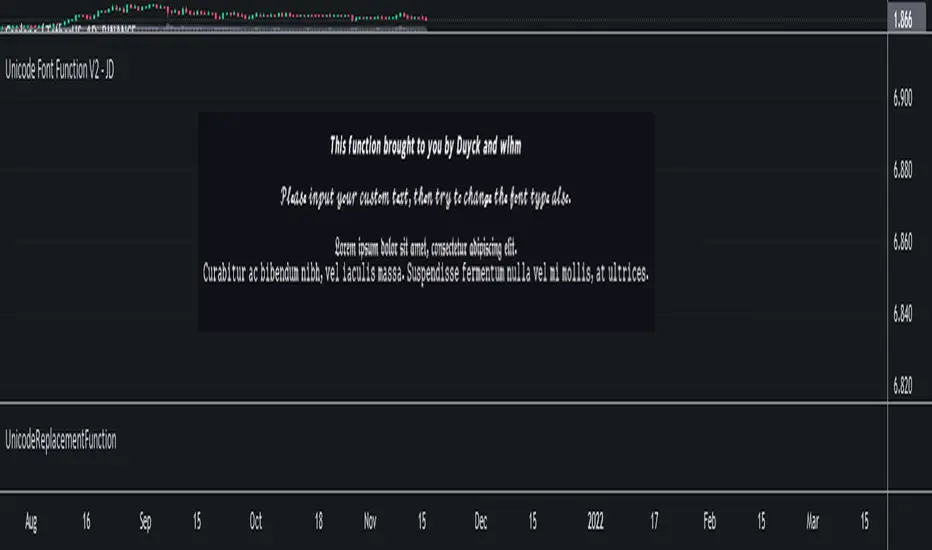

UnicodeReplacementFunctionLibrary "UnicodeReplacementFunction"

Unicode Characters Replacement function for strings.

replaceFont(_str, _fontType) Unicode Character Replace Function

Parameters:

_str : String input

_fontType : Font Type Selector

Returns: Replaced Char String with any custom font type choosed