Moving_AveragesLibrary "Moving_Averages"

This library contains majority important moving average functions with int series support. Which means that they can be used with variable length input. For conventional use, please use tradingview built-in ta functions for moving averages as they are more precise. I'll use functions in this library for my other scripts with dynamic length inputs.

ema(src, len)

Exponential Moving Average (EMA)

Parameters:

src : Source

len : Period

Returns: Exponential Moving Average with Series Int Support (EMA)

alma(src, len, a_offset, a_sigma)

Arnaud Legoux Moving Average (ALMA)

Parameters:

src : Source

len : Period

a_offset : Arnaud Legoux offset

a_sigma : Arnaud Legoux sigma

Returns: Arnaud Legoux Moving Average (ALMA)

covwema(src, len)

Coefficient of Variation Weighted Exponential Moving Average (COVWEMA)

Parameters:

src : Source

len : Period

Returns: Coefficient of Variation Weighted Exponential Moving Average (COVWEMA)

covwma(src, len)

Coefficient of Variation Weighted Moving Average (COVWMA)

Parameters:

src : Source

len : Period

Returns: Coefficient of Variation Weighted Moving Average (COVWMA)

dema(src, len)

DEMA - Double Exponential Moving Average

Parameters:

src : Source

len : Period

Returns: DEMA - Double Exponential Moving Average

edsma(src, len, ssfLength, ssfPoles)

EDSMA - Ehlers Deviation Scaled Moving Average

Parameters:

src : Source

len : Period

ssfLength : EDSMA - Super Smoother Filter Length

ssfPoles : EDSMA - Super Smoother Filter Poles

Returns: Ehlers Deviation Scaled Moving Average (EDSMA)

eframa(src, len, FC, SC)

Ehlrs Modified Fractal Adaptive Moving Average (EFRAMA)

Parameters:

src : Source

len : Period

FC : Lower Shift Limit for Ehlrs Modified Fractal Adaptive Moving Average

SC : Upper Shift Limit for Ehlrs Modified Fractal Adaptive Moving Average

Returns: Ehlrs Modified Fractal Adaptive Moving Average (EFRAMA)

ehma(src, len)

EHMA - Exponential Hull Moving Average

Parameters:

src : Source

len : Period

Returns: Exponential Hull Moving Average (EHMA)

etma(src, len)

Exponential Triangular Moving Average (ETMA)

Parameters:

src : Source

len : Period

Returns: Exponential Triangular Moving Average (ETMA)

frama(src, len)

Fractal Adaptive Moving Average (FRAMA)

Parameters:

src : Source

len : Period

Returns: Fractal Adaptive Moving Average (FRAMA)

hma(src, len)

HMA - Hull Moving Average

Parameters:

src : Source

len : Period

Returns: Hull Moving Average (HMA)

jma(src, len, jurik_phase, jurik_power)

Jurik Moving Average - JMA

Parameters:

src : Source

len : Period

jurik_phase : Jurik (JMA) Only - Phase

jurik_power : Jurik (JMA) Only - Power

Returns: Jurik Moving Average (JMA)

kama(src, len, k_fastLength, k_slowLength)

Kaufman's Adaptive Moving Average (KAMA)

Parameters:

src : Source

len : Period

k_fastLength : Number of periods for the fastest exponential moving average

k_slowLength : Number of periods for the slowest exponential moving average

Returns: Kaufman's Adaptive Moving Average (KAMA)

kijun(_high, _low, len, kidiv)

Kijun v2

Parameters:

_high : High value of bar

_low : Low value of bar

len : Period

kidiv : Kijun MOD Divider

Returns: Kijun v2

lsma(src, len, offset)

LSMA/LRC - Least Squares Moving Average / Linear Regression Curve

Parameters:

src : Source

len : Period

offset : Offset

Returns: Least Squares Moving Average (LSMA)/ Linear Regression Curve (LRC)

mf(src, len, beta, feedback, z)

MF - Modular Filter

Parameters:

src : Source

len : Period

beta : Modular Filter, General Filter Only - Beta

feedback : Modular Filter Only - Feedback

z : Modular Filter Only - Feedback Weighting

Returns: Modular Filter (MF)

rma(src, len)

RMA - RSI Moving average

Parameters:

src : Source

len : Period

Returns: RSI Moving average (RMA)

sma(src, len)

SMA - Simple Moving Average

Parameters:

src : Source

len : Period

Returns: Simple Moving Average (SMA)

smma(src, len)

Smoothed Moving Average (SMMA)

Parameters:

src : Source

len : Period

Returns: Smoothed Moving Average (SMMA)

stma(src, len)

Simple Triangular Moving Average (STMA)

Parameters:

src : Source

len : Period

Returns: Simple Triangular Moving Average (STMA)

tema(src, len)

TEMA - Triple Exponential Moving Average

Parameters:

src : Source

len : Period

Returns: Triple Exponential Moving Average (TEMA)

thma(src, len)

THMA - Triple Hull Moving Average

Parameters:

src : Source

len : Period

Returns: Triple Hull Moving Average (THMA)

vama(src, len, volatility_lookback)

VAMA - Volatility Adjusted Moving Average

Parameters:

src : Source

len : Period

volatility_lookback : Volatility lookback length

Returns: Volatility Adjusted Moving Average (VAMA)

vidya(src, len)

Variable Index Dynamic Average (VIDYA)

Parameters:

src : Source

len : Period

Returns: Variable Index Dynamic Average (VIDYA)

vwma(src, len)

Volume-Weighted Moving Average (VWMA)

Parameters:

src : Source

len : Period

Returns: Volume-Weighted Moving Average (VWMA)

wma(src, len)

WMA - Weighted Moving Average

Parameters:

src : Source

len : Period

Returns: Weighted Moving Average (WMA)

zema(src, len)

Zero-Lag Exponential Moving Average (ZEMA)

Parameters:

src : Source

len : Period

Returns: Zero-Lag Exponential Moving Average (ZEMA)

zsma(src, len)

Zero-Lag Simple Moving Average (ZSMA)

Parameters:

src : Source

len : Period

Returns: Zero-Lag Simple Moving Average (ZSMA)

evwma(src, len)

EVWMA - Elastic Volume Weighted Moving Average

Parameters:

src : Source

len : Period

Returns: Elastic Volume Weighted Moving Average (EVWMA)

tt3(src, len, a1_t3)

Tillson T3

Parameters:

src : Source

len : Period

a1_t3 : Tillson T3 Volume Factor

Returns: Tillson T3

gma(src, len)

GMA - Geometric Moving Average

Parameters:

src : Source

len : Period

Returns: Geometric Moving Average (GMA)

wwma(src, len)

WWMA - Welles Wilder Moving Average

Parameters:

src : Source

len : Period

Returns: Welles Wilder Moving Average (WWMA)

ama(src, _high, _low, len, ama_f_length, ama_s_length)

AMA - Adjusted Moving Average

Parameters:

src : Source

_high : High value of bar

_low : Low value of bar

len : Period

ama_f_length : Fast EMA Length

ama_s_length : Slow EMA Length

Returns: Adjusted Moving Average (AMA)

cma(src, len)

Corrective Moving average (CMA)

Parameters:

src : Source

len : Period

Returns: Corrective Moving average (CMA)

gmma(src, len)

Geometric Mean Moving Average (GMMA)

Parameters:

src : Source

len : Period

Returns: Geometric Mean Moving Average (GMMA)

ealf(src, len, LAPercLen_, FPerc_)

Ehler's Adaptive Laguerre filter (EALF)

Parameters:

src : Source

len : Period

LAPercLen_ : Median Length

FPerc_ : Median Percentage

Returns: Ehler's Adaptive Laguerre filter (EALF)

elf(src, len, LAPercLen_, FPerc_)

ELF - Ehler's Laguerre filter

Parameters:

src : Source

len : Period

LAPercLen_ : Median Length

FPerc_ : Median Percentage

Returns: Ehler's Laguerre Filter (ELF)

edma(src, len)

Exponentially Deviating Moving Average (MZ EDMA)

Parameters:

src : Source

len : Period

Returns: Exponentially Deviating Moving Average (MZ EDMA)

pnr(src, len, rank_inter_Perc_)

PNR - percentile nearest rank

Parameters:

src : Source

len : Period

rank_inter_Perc_ : Rank and Interpolation Percentage

Returns: Percentile Nearest Rank (PNR)

pli(src, len, rank_inter_Perc_)

PLI - Percentile Linear Interpolation

Parameters:

src : Source

len : Period

rank_inter_Perc_ : Rank and Interpolation Percentage

Returns: Percentile Linear Interpolation (PLI)

rema(src, len)

Range EMA (REMA)

Parameters:

src : Source

len : Period

Returns: Range EMA (REMA)

sw_ma(src, len)

Sine-Weighted Moving Average (SW-MA)

Parameters:

src : Source

len : Period

Returns: Sine-Weighted Moving Average (SW-MA)

vwap(src, len)

Volume Weighted Average Price (VWAP)

Parameters:

src : Source

len : Period

Returns: Volume Weighted Average Price (VWAP)

mama(src, len)

MAMA - MESA Adaptive Moving Average

Parameters:

src : Source

len : Period

Returns: MESA Adaptive Moving Average (MAMA)

fama(src, len)

FAMA - Following Adaptive Moving Average

Parameters:

src : Source

len : Period

Returns: Following Adaptive Moving Average (FAMA)

hkama(src, len)

HKAMA - Hilbert based Kaufman's Adaptive Moving Average

Parameters:

src : Source

len : Period

Returns: Hilbert based Kaufman's Adaptive Moving Average (HKAMA)

MATH

Price Displacement - Candlestick (OHLC) CalculationsA Magical little helper friend for Candle Math.

When composing scripts, it is often necessary to manipulate the math around the OHLC. At times, you want a scalar (absolute) value others you want a vector (+/-). Sometimes you want the open - close and sometimes you want just the positive number of the body size. You might want it in ticks or you might want it in points or you might want in percentages. And every time you try to put it together you waste precious time and brain power trying to think about how to properly structure what you're looking for. Not to mention it's normally not that aesthetically pleasing to look at in the code.

So, this fixes all of that.

Using this library. A function like 'pd.pt(_exp)' can call any kind of candlestick math you need. The function returns the candlestick math you define using particular expressions.

Candle Math Functions Include:

Points:

pt(_exp) Absolute Point Displacement. Point quantity of given size parameters according to _exp.

vpt(_exp) Vector Point Displacement. Point quantity of given size parameters according to _exp.

Ticks:

tick(_exp) Absolute Tick Displacement. Tick quantity of given size parameters according to _exp.

vtick(_exp) Vector Tick Displacement. Tick quantity of given size parameters according to _exp.

Percentages:

pct(_exp, _prec) Absolute Percent Displacement. (w/rounding overload). Percent quantity of bar range of given size parameters according to _exp.

vpct(_exp, _prec) Vector Percent Displacement (w/rounding overload). Percent quantity of bar range of given size parameters according to _exp.

Expressions You Can Use with Formulas:

The expressions are simple (simple strings that is) and I did my best to make them sensible, generally using just the ohlc abreviations. I also included uw, lw, bd, and rg for when you're just trying to pull a candle component out. That way you don't have to think about which of the ohlc you're trying to get just use pd.tick("uw") and now the variable is assigned the length of the upper wick, absolute value, in ticks. If you wanted the vector in pts its pd.vpt("uw"). It also makes changing things easy too as I write it out.

Expression List:

Combinations

"oh" = open - high

"ol" = open - low

"oc" = open - close

"ho" = high - open

"hl" = high - low

"hc" = high - close

"lo" = low - open

"lh" = low - high

"lc" = low - close

"co" = close - open

"ch" = close - high

"cl" = close - low

Candle Components

"uw" = Upper Wick

"bd" = Body

"lw" = Lower Wick

"rg" = Range

Pct() Only

"scp" = Scalar Close Position

"sop" = Scalar Open Position

"vcp" = Vector Close Position

"vop" = Vector Open Position

The attributes are going to be available in the pop up dialogue when you mouse over the function, so you don't really have to remember them. I tried to make that look as efficient as possible. You'll notice it follows the OHLC pattern. Thus, "oh" precedes "ho" (heyo) because "O" would be first in the OHLC. Its a way to help find the expression you're looking for quickly. Like looking through an alphabetized list for traders.

There is a copy/paste console friendly helper list in the script itself.

Additional Notes on the Pct() Only functions:

This is the original reason I started writing this. These concepts place a rating/value on the bar based on candle attributes in one number. These formulas put a open or close value in a percentile of the bar relative to another aspect of the bar.

Scalar - Non-directional. Absolute Value.

Scalar Position: The position of the price attribute relative to the scale of the bar range (high - low)

Example: high = 100. low = 0. close = 25.

(A) Measure price distance C-L. How high above the low did the candle close (e.g. close - low = 25)

(B) Divide by bar range (high - low). 25 / (100 - 0) = .25

Explaination: The candle closed at the 25th percentile of the bar range given the bar range low = 0 and bar range high = 100.

Formula: scp = (close - low) / (high - low)

Vector = Directional.

Vector Position: The position of the price attribute relative to the scale of the bar midpoint (Vector Position at hl2 = 0)

Example: high = 100. low = 0. close = 25.

(A) Measure Price distance C-L: How high above the low did the candle close (e.g. close - low = 25)

(B) Measure Price distance H-C: How far below the high did the candle close (e.g. high - close = 75)

(C) Take Difference: A - B = C = -50

(D) Divide by bar range (high - low). -50 / (100 - 0) = -0.50

Explaination: Candle close at the midpoint between hl2 and the low.

Formula: vcp = { / (high - low) }

Thank you for checking this out. I hope no one else has already done this (because it took half the day) and I hope you find value in it. Be well. Trade well.

Library "PD"

Price Displacement

pt(_exp) Absolute Point Displacement. Point quantity of given size parameters according to _exp.

Parameters:

_exp : (string) Price Parameter

Returns: Point size of given expression as an absolute value.

vpt(_exp) Vector Point Displacement. Point quantity of given size parameters according to _exp.

Parameters:

_exp : (string) Price Parameter

Returns: Point size of given expression as a vector.

tick(_exp) Absolute Tick Displacement. Tick quantity of given size parameters according to _exp.

Parameters:

_exp : (string) Price Parameter

Returns: Tick size of given expression as an absolute value.

vtick(_exp) Vector Tick Displacement. Tick quantity of given size parameters according to _exp.

Parameters:

_exp : (string) Price Parameter

Returns: Tick size of given expression as a vector.

pct(_exp, _prec) Absolute Percent Displacement (w/rounding overload). Percent quantity of bar range of given size parameters according to _exp.

Parameters:

_exp : (string) Expression

_prec : (int) Overload - Place value precision definition

Returns: Percent size of given expression as decimal.

vpct(_exp, _prec) Vector Percent Displacement (w/rounding overload). Percent quantity of bar range of given size parameters according to _exp.

Parameters:

_exp : (string) Expression

_prec : (int) Overload - Place value precision definition

Returns: Percent size of given expression as decimal.

Strategy Table LibraryLibrary "table_library"

TODO: With this library, you can add tables to your strategies.

strategy_table()

Returns: Strategy Profit Table

Adds a table to the graph of the strategy for which you are calling the function. You can see data such as net profit in this table.

No parameters. Just call the function inside the strategy.

Example Code :

import only_fibonacci/table_lib/1 as st

st.strategy_table()

AutoFiboRetraceLibrary "AutoFiboRetrace"

TODO: add library description here

fun(x) TODO: add function description here

Parameters:

x : TODO: add parameter x description here

Returns: TODO: add what function returns

honest personal libraryLibrary "honestpersonallibrary"

thestratnumber() this will return the number 1,2 or 3 using the logic from Rob Smiths #thestrat which uses these type of bars for setups

getBodySize() Gets the current candle's body size (in POINTS, divide by 10 to get pips)

Returns: The current candle's body size in POINTS

getTopWickSize() Gets the current candle's top wick size (in POINTS, divide by 10 to get pips)

Returns: The current candle's top wick size in POINTS

getBottomWickSize() Gets the current candle's bottom wick size (in POINTS, divide by 10 to get pips)

Returns: The current candle's bottom wick size in POINTS

getBodyPercent() Gets the current candle's body size as a percentage of its entire size including its wicks

Returns: The current candle's body size percentage

strictBearPinBar(float, float) This it to find pinbars with a very long wick compared to the body that are bearish

Parameters:

float : minTopMulitplier (default=4) The minimum number of times that the top wick has to be bigger than the candle body size

float : maxBottomMultiplier (default=2) The maximum number of times that the bottom wick can be bigger than the candle body size

Returns: a bool function true if current candle is withing the parameters

strictBullPinBar(float, float) This it to find pinbars with a very long wick compared to the body that are bearish

Parameters:

float : minTopMulitplier (default=4) The minimum number of times that the top wick has to be bigger than the candle body size

float : maxBottomMultiplier (default=2) The maximum number of times that the bottom wick can be bigger than the candle body size

Returns: a bool function true if current candle is withing the parameters

FunctionIntrabarCrossValueLibrary "FunctionIntrabarCrossValue"

intrabar_cross_value(a, b, step) Find the minimum difference of a intrabar cross and return its median value.

Parameters:

a : float, series a.

b : float, series b.

step : float, step to iterate x axis, default=0.01

Returns: float

OrdinaryLeastSquaresLibrary "OrdinaryLeastSquares"

One of the most common ways to estimate the coefficients for a linear regression is to use the Ordinary Least Squares (OLS) method.

This library implements OLS in pine. This implementation can be used to fit a linear regression of multiple independent variables onto one dependent variable,

as long as the assumptions behind OLS hold.

solve_xtx_inv(x, y) Solve a linear system of equations using the Ordinary Least Squares method.

This function returns both the estimated OLS solution and a matrix that essentially measures the model stability (linear dependence between the columns of 'x').

NOTE: The latter is an intermediate step when estimating the OLS solution but is useful when calculating the covariance matrix and is returned here to save computation time

so that this step doesn't have to be calculated again when things like standard errors should be calculated.

Parameters:

x : The matrix containing the independent variables. Each column is regarded by the algorithm as one independent variable. The row count of 'x' and 'y' must match.

y : The matrix containing the dependent variable. This matrix can only contain one dependent variable and can therefore only contain one column. The row count of 'x' and 'y' must match.

Returns: Returns both the estimated OLS solution and a matrix that essentially measures the model stability (xtx_inv is equal to (X'X)^-1).

solve(x, y) Solve a linear system of equations using the Ordinary Least Squares method.

Parameters:

x : The matrix containing the independent variables. Each column is regarded by the algorithm as one independent variable. The row count of 'x' and 'y' must match.

y : The matrix containing the dependent variable. This matrix can only contain one dependent variable and can therefore only contain one column. The row count of 'x' and 'y' must match.

Returns: Returns the estimated OLS solution.

standard_errors(x, y, beta_hat, xtx_inv) Calculate the standard errors.

Parameters:

x : The matrix containing the independent variables. Each column is regarded by the algorithm as one independent variable. The row count of 'x' and 'y' must match.

y : The matrix containing the dependent variable. This matrix can only contain one dependent variable and can therefore only contain one column. The row count of 'x' and 'y' must match.

beta_hat : The Ordinary Least Squares (OLS) solution provided by solve_xtx_inv() or solve().

xtx_inv : This is (X'X)^-1, which means we take the transpose of the X matrix, multiply that the X matrix and then take the inverse of the result.

This essentially measures the linear dependence between the columns of the X matrix.

Returns: The standard errors.

estimate(x, beta_hat) Estimate the next step of a linear model.

Parameters:

x : The matrix containing the independent variables. Each column is regarded by the algorithm as one independent variable. The row count of 'x' and 'y' must match.

beta_hat : The Ordinary Least Squares (OLS) solution provided by solve_xtx_inv() or solve().

Returns: Returns the new estimate of Y based on the linear model.

FunctionMatrixSolveLibrary "FunctionMatrixSolve"

Matrix Equation solution for Ax = B, finds the value of x.

solve(A, B) Solves Matrix Equation for Ax = B, finds value for x.

Parameters:

A : matrix, Square matrix with data values.

B : matrix, One column matrix with data values.

Returns: matrix with X, x = A^-1 b, assuming A is square and has full rank

introcs.cs.princeton.edu

FunctionPolynomialFitLibrary "FunctionPolynomialFit"

Performs Polynomial Regression fit to data.

In statistics, polynomial regression is a form of regression analysis in which

the relationship between the independent variable x and the dependent variable

y is modelled as an nth degree polynomial in x.

reference:

en.wikipedia.org

www.bragitoff.com

gauss_elimination(A, m, n) Perform Gauss-Elimination and returns the Upper triangular matrix and solution of equations.

Parameters:

A : float matrix, data samples.

m : int, defval=na, number of rows.

n : int, defval=na, number of columns.

Returns: float array with coefficients.

polyfit(X, Y, degree) Fits a polynomial of a degree to (x, y) points.

Parameters:

X : float array, data sample x point.

Y : float array, data sample y point.

degree : int, defval=2, degree of the polynomial.

Returns: float array with coefficients.

note:

p(x) = p * x**deg + ... + p

interpolate(coeffs, x) interpolate the y position at the provided x.

Parameters:

coeffs : float array, coefficients of the polynomial.

x : float, position x to estimate y.

Returns: float.

DominantCycleCollection of Dominant Cycle estimators. Length adaptation used in the Adaptive Moving Averages and the Adaptive Oscillators try to follow price movements and accelerate/decelerate accordingly (usually quite rapidly with a huge range). Cycle estimators, on the other hand, try to measure the cycle period of the current market, which does not reflect price movement or the rate of change (the rate of change may also differ depending on the cycle phase, but the cycle period itself usually changes slowly). This collection may become encyclopaedic, so if you have any working cycle estimator, drop me a line in the comments below. Suggestions are welcome. Currently included estimators are based on the work of John F. Ehlers

mamaPeriod(src, dynLow, dynHigh) MESA Adaptation - MAMA Cycle

Parameters:

src : Series to use

dynLow : Lower bound for the dynamic length

dynHigh : Upper bound for the dynamic length

Returns: Calculated period

Based on MESA Adaptive Moving Average by John F. Ehlers

Performs Hilbert Transform Homodyne Discriminator cycle measurement

Unlike MAMA Alpha function (in LengthAdaptation library), this does not compute phase rate of change

Introduced in the September 2001 issue of Stocks and Commodities

Inspired by the @everget implementation:

Inspired by the @anoojpatel implementation:

paPeriod(src, dynLow, dynHigh, preHP, preSS, preHP) Pearson Autocorrelation

Parameters:

src : Series to use

dynLow : Lower bound for the dynamic length

dynHigh : Upper bound for the dynamic length

preHP : Use High Pass prefilter (default)

preSS : Use Super Smoother prefilter (default)

preHP : Use Hann Windowing prefilter

Returns: Calculated period

Based on Pearson Autocorrelation Periodogram by John F. Ehlers

Introduced in the September 2016 issue of Stocks and Commodities

Inspired by the @blackcat1402 implementation:

Inspired by the @rumpypumpydumpy implementation:

Corrected many errors, and made small speed optimizations, so this could be the best implementation to date (still slow, though, so may revisit in future)

High Pass and Super Smoother prefilters are used in the original implementation

dftPeriod(src, dynLow, dynHigh, preHP, preSS, preHP) Discrete Fourier Transform

Parameters:

src : Series to use

dynLow : Lower bound for the dynamic length

dynHigh : Upper bound for the dynamic length

preHP : Use High Pass prefilter (default)

preSS : Use Super Smoother prefilter (default)

preHP : Use Hann Windowing prefilter

Returns: Calculated period

Based on Spectrum from Discrete Fourier Transform by John F. Ehlers

Inspired by the @blackcat1402 implementation:

High Pass, Super Smoother and Hann Windowing prefilters are used in the original implementation

phasePeriod(src, dynLow, dynHigh, preHP, preSS, preHP) Phase Accumulation

Parameters:

src : Series to use

dynLow : Lower bound for the dynamic length

dynHigh : Upper bound for the dynamic length

preHP : Use High Pass prefilter (default)

preSS : Use Super Smoother prefilter (default)

preHP : Use Hamm Windowing prefilter

Returns: Calculated period

Based on Dominant Cycle from Phase Accumulation by John F. Ehlers

High Pass and Super Smoother prefilters are used in the original implementation

doAdapt(type, src, len, dynLow, dynHigh, chandeSDLen, chandeSmooth, chandePower, preHP, preSS, preHP) Execute a particular Length Adaptation or Dominant Cycle Estimator from the list

Parameters:

type : Length Adaptation or Dominant Cycle Estimator type to use

src : Series to use

len : Reference lookback length

dynLow : Lower bound for the dynamic length

dynHigh : Upper bound for the dynamic length

chandeSDLen : Lookback length of Standard deviation for Chande's Dynamic Length

chandeSmooth : Smoothing length of Standard deviation for Chande's Dynamic Length

chandePower : Exponent of the length adaptation for Chande's Dynamic Length (lower is smaller variation)

preHP : Use High Pass prefilter for the Estimators that support it (default)

preSS : Use Super Smoother prefilter for the Estimators that support it (default)

preHP : Use Hann Windowing prefilter for the Estimators that support it

Returns: Calculated period (float, not limited)

doEstimate(type, src, dynLow, dynHigh, preHP, preSS, preHP) Execute a particular Dominant Cycle Estimator from the list

Parameters:

type : Dominant Cycle Estimator type to use

src : Series to use

dynLow : Lower bound for the dynamic length

dynHigh : Upper bound for the dynamic length

preHP : Use High Pass prefilter for the Estimators that support it (default)

preSS : Use Super Smoother prefilter for the Estimators that support it (default)

preHP : Use Hann Windowing prefilter for the Estimators that support it

Returns: Calculated period (float, not limited)

least_squares_regressionLibrary "least_squares_regression"

least_squares_regression: Least squares regression algorithm to find the optimal price interval for a given time period

basic_lsr(series, series, series) basic_lsr: Basic least squares regression algorithm

Parameters:

series : int t: time scale value array corresponding to price

series : float p: price scale value array corresponding to time

series : int array_size: the length of regression array

Returns: reg_slop, reg_intercept, reg_level, reg_stdev

trend_line_lsr(series, series, series, string, series, series) top_trend_line_lsr: Trend line fitting based on least square algorithm

Parameters:

series : int t: time scale value array corresponding to price

series : float p: price scale value array corresponding to time

series : int array_size: the length of regression array

string : reg_type: regression type in 'top' and 'bottom'

series : int max_iter: maximum fitting iterations

series : int min_points: the threshold of regression point numbers

Returns: reg_slop, reg_intercept, reg_level, reg_stdev, reg_point_num

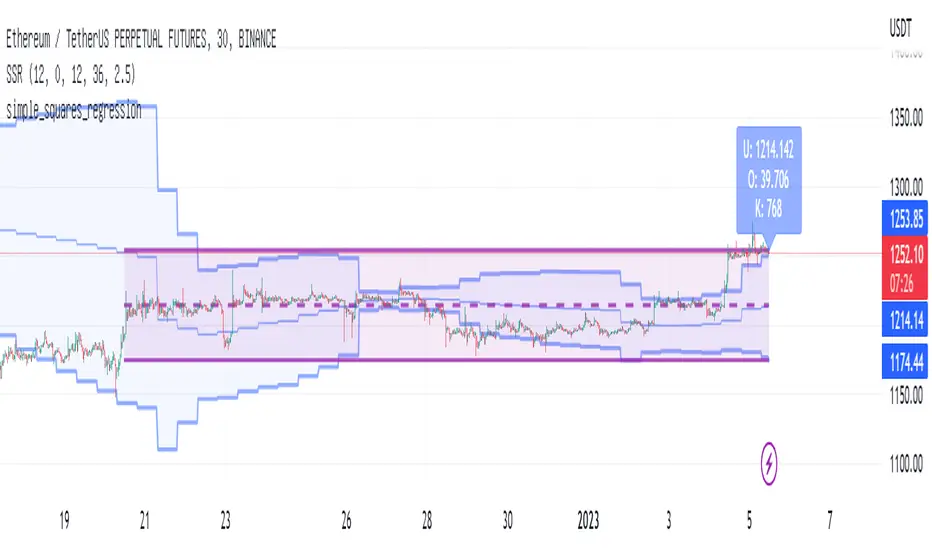

simple_squares_regressionLibrary "simple_squares_regression"

simple_squares_regression: simple squares regression algorithm to find the optimal price interval for a given time period

basic_ssr(series, series, series) basic_ssr: Basic simple squares regression algorithm

Parameters:

series : float src: the regression source such as close

series : int region_forward: number of candle lines at the right end of the regression region from the current candle line

series : int region_len: the length of regression region

Returns: left_loc, right_loc, reg_val, reg_std, reg_max_offset

search_ssr(series, series, series, series) search_ssr: simple squares regression region search algorithm

Parameters:

series : float src: the regression source such as close

series : int max_forward: max number of candle lines at the right end of the regression region from the current candle line

series : int region_lower: the lower length of regression region

series : int region_upper: the upper length of regression region

Returns: left_loc, right_loc, reg_val, reg_level, reg_std_err, reg_max_offset

on_balance_volumeLibrary "on_balance_volume"

on_balance_volume: custom on balance volume

obv_diff(string, simple) obv_diff: custom on balance volume diff version

Parameters:

string : type: the moving average type of on balance volume

simple : int len: the moving average length of on balance volume

Returns: obv_diff: custom on balance volume diff value

obv_diff_norm(string, simple) obv_diff_norm: custom normalized on balance volume diff version

Parameters:

string : type: the moving average type of on balance volume

simple : int len: the moving average length of on balance volume

Returns: obv_diff: custom normalized on balance volume diff value

moving_averageLibrary "moving_average"

moving_average: moving average variants

variant(string, series, simple) variant: moving average variants

Parameters:

string : type: type in

series : float src: the source series of moving average

simple : int len: the length of moving average

Returns: float: the moving average variant value

NormalizedOscillatorsLibrary "NormalizedOscillators"

Collection of some common Oscillators. All are zero-mean and normalized to fit in the -1..1 range. Some are modified, so that the internal smoothing function could be configurable (for example, to enable Hann Windowing, that John F. Ehlers uses frequently). Some are modified for other reasons (see comments in the code), but never without a reason. This collection is neither encyclopaedic, nor reference, however I try to find the most correct implementation. Suggestions are welcome.

rsi2(upper, lower) RSI - second step

Parameters:

upper : Upwards momentum

lower : Downwards momentum

Returns: Oscillator value

Modified by Ehlers from Wilder's implementation to have a zero mean (oscillator from -1 to +1)

Originally: 100.0 - (100.0 / (1.0 + upper / lower))

Ignoring the 100 scale factor, we get: upper / (upper + lower)

Multiplying by two and subtracting 1, we get: (2 * upper) / (upper + lower) - 1 = (upper - lower) / (upper + lower)

rms(src, len) Root mean square (RMS)

Parameters:

src : Source series

len : Lookback period

Based on by John F. Ehlers implementation

ift(src) Inverse Fisher Transform

Parameters:

src : Source series

Returns: Normalized series

Based on by John F. Ehlers implementation

The input values have been multiplied by 2 (was "2*src", now "4*src") to force expansion - not compression

The inputs may be further modified, if needed

stoch(src, len) Stochastic

Parameters:

src : Source series

len : Lookback period

Returns: Oscillator series

ssstoch(src, len) Super Smooth Stochastic (part of MESA Stochastic) by John F. Ehlers

Parameters:

src : Source series

len : Lookback period

Returns: Oscillator series

Introduced in the January 2014 issue of Stocks and Commodities

This is not an implementation of MESA Stochastic, as it is based on Highpass filter not present in the function (but you can construct it)

This implementation is scaled by 0.95, so that Super Smoother does not exceed 1/-1

I do not know, if this the right way to fix this issue, but it works for now

netKendall(src, len) Noise Elimination Technology by John F. Ehlers

Parameters:

src : Source series

len : Lookback period

Returns: Oscillator series

Introduced in the December 2020 issue of Stocks and Commodities

Uses simplified Kendall correlation algorithm

Implementation by @QuantTherapy:

rsi(src, len, smooth) RSI

Parameters:

src : Source series

len : Lookback period

smooth : Internal smoothing algorithm

Returns: Oscillator series

vrsi(src, len, smooth) Volume-scaled RSI

Parameters:

src : Source series

len : Lookback period

smooth : Internal smoothing algorithm

Returns: Oscillator series

This is my own version of RSI. It scales price movements by the proportion of RMS of volume

mrsi(src, len, smooth) Momentum RSI

Parameters:

src : Source series

len : Lookback period

smooth : Internal smoothing algorithm

Returns: Oscillator series

Inspired by RocketRSI by John F. Ehlers (Stocks and Commodities, May 2018)

rrsi(src, len, smooth) Rocket RSI

Parameters:

src : Source series

len : Lookback period

smooth : Internal smoothing algorithm

Returns: Oscillator series

Inspired by RocketRSI by John F. Ehlers (Stocks and Commodities, May 2018)

Does not include Fisher Transform of the original implementation, as the output must be normalized

Does not include momentum smoothing length configuration, so always assumes half the lookback length

mfi(src, len, smooth) Money Flow Index

Parameters:

src : Source series

len : Lookback period

smooth : Internal smoothing algorithm

Returns: Oscillator series

lrsi(src, in_gamma, len) Laguerre RSI by John F. Ehlers

Parameters:

src : Source series

in_gamma : Damping factor (default is -1 to generate from len)

len : Lookback period (alternatively, if gamma is not set)

Returns: Oscillator series

The original implementation is with gamma. As it is impossible to collect gamma in my system, where the only user input is length,

an alternative calculation is included, where gamma is set by dividing len by 30. Maybe different calculation would be better?

fe(len) Choppiness Index or Fractal Energy

Parameters:

len : Lookback period

Returns: Oscillator series

The Choppiness Index (CHOP) was created by E. W. Dreiss

This indicator is sometimes called Fractal Energy

er(src, len) Efficiency ratio

Parameters:

src : Source series

len : Lookback period

Returns: Oscillator series

Based on Kaufman Adaptive Moving Average calculation

This is the correct Efficiency ratio calculation, and most other implementations are wrong:

the number of bar differences is 1 less than the length, otherwise we are adding the change outside of the measured range!

For reference, see Stocks and Commodities June 1995

dmi(len, smooth) Directional Movement Index

Parameters:

len : Lookback period

smooth : Internal smoothing algorithm

Returns: Oscillator series

Based on the original Tradingview algorithm

Modified with inspiration from John F. Ehlers DMH (but not implementing the DMH algorithm!)

Only ADX is returned

Rescaled to fit -1 to +1

Unlike most oscillators, there is no src parameter as DMI works directly with high and low values

fdmi(len, smooth) Fast Directional Movement Index

Parameters:

len : Lookback period

smooth : Internal smoothing algorithm

Returns: Oscillator series

Same as DMI, but without secondary smoothing. Can be smoothed later. Instead, +DM and -DM smoothing can be configured

doOsc(type, src, len, smooth) Execute a particular Oscillator from the list

Parameters:

type : Oscillator type to use

src : Source series

len : Lookback period

smooth : Internal smoothing algorithm

Returns: Oscillator series

Chande Momentum Oscillator (CMO) is RSI without smoothing. No idea, why some authors use different calculations

LRSI with Fractal Energy is a combo oscillator that uses Fractal Energy to tune LRSI gamma, as seen here: www.prorealcode.com

doPostfilter(type, src, len) Execute a particular Oscillator Postfilter from the list

Parameters:

type : Oscillator type to use

src : Source series

len : Lookback period

Returns: Oscillator series

CommonFiltersLibrary "CommonFilters"

Collection of some common Filters and Moving Averages. This collection is not encyclopaedic, but to declutter my other scripts. Suggestions are welcome, though. Many filters here are based on the work of John F. Ehlers

sma(src, len) Simple Moving Average

Parameters:

src : Series to use

len : Filtering length

Returns: Filtered series

ema(src, len) Exponential Moving Average

Parameters:

src : Series to use

len : Filtering length

Returns: Filtered series

rma(src, len) Wilder's Smoothing (Running Moving Average)

Parameters:

src : Series to use

len : Filtering length

Returns: Filtered series

hma(src, len) Hull Moving Average

Parameters:

src : Series to use

len : Filtering length

Returns: Filtered series

vwma(src, len) Volume Weighted Moving Average

Parameters:

src : Series to use

len : Filtering length

Returns: Filtered series

hp2(src) Simple denoiser

Parameters:

src : Series to use

Returns: Filtered series

fir2(src) Zero at 2 bar cycle period by John F. Ehlers

Parameters:

src : Series to use

Returns: Filtered series

fir3(src) Zero at 3 bar cycle period by John F. Ehlers

Parameters:

src : Series to use

Returns: Filtered series

fir23(src) Zero at 2 bar and 3 bar cycle periods by John F. Ehlers

Parameters:

src : Series to use

Returns: Filtered series

fir234(src) Zero at 2, 3 and 4 bar cycle periods by John F. Ehlers

Parameters:

src : Series to use

Returns: Filtered series

hp(src, len) High Pass Filter for cyclic components shorter than langth. Part of Roofing Filter by John F. Ehlers

Parameters:

src : Series to use

len : Filtering length

Returns: Filtered series

supers2(src, len) 2-pole Super Smoother by John F. Ehlers

Parameters:

src : Series to use

len : Filtering length

Returns: Filtered series

filt11(src, len) Filt11 is a variant of 2-pole Super Smoother with error averaging for zero-lag response by John F. Ehlers

Parameters:

src : Series to use

len : Filtering length

Returns: Filtered series

supers3(src, len) 3-pole Super Smoother by John F. Ehlers

Parameters:

src : Series to use

len : Filtering length

Returns: Filtered series

hannFIR(src, len) Hann Window Filter by John F. Ehlers

Parameters:

src : Series to use

len : Filtering length

Returns: Filtered series

hammingFIR(src, len) Hamming Window Filter (inspired by John F. Ehlers). Simplified implementation as Pedestal input parameter cannot be supplied, so I calculate it from the supplied length

Parameters:

src : Series to use

len : Filtering length

Returns: Filtered series

triangleFIR(src, len) Triangle Window Filter by John F. Ehlers

Parameters:

src : Series to use

len : Filtering length

Returns: Filtered series

doPrefilter(type, src) Execute a particular Prefilter from the list

Parameters:

type : Prefilter type to use

src : Series to use

Returns: Filtered series

doMA(type, src, len) Execute a particular MA from the list

Parameters:

type : MA type to use

src : Series to use

len : Filtering length

Returns: Filtered series

math_utilsLibrary "math_utils"

Collection of math functions that are not part of the standard math library

num_of_non_decimal_digits(number) num_of_non_decimal_digits - The number of the most significant digits on the left of the dot

Parameters:

number : - The floating point number

Returns: number of non digits

num_of_decimal_digits(number) num_of_decimal_digits - The number of the most significant digits on the right of the dot

Parameters:

number : - The floating point number

Returns: number of decimal digits

floor(number, precision) floor - floor with precision to the given most significant decimal point

Parameters:

number : - The floating point number

precision : - The number of decimal places a.k.a the most significant decimal digit - e.g precision 2 will produce 0.01 minimum change

Returns: number floored to the decimal digits defined by the precision

ceil(number, precision) floor - ceil with precision to the given most significant decimal point

Parameters:

number : - The floating point number

precision : - The number of decimal places a.k.a the most significant decimal digit - e.g precision 2 will produce 0.01 minimum change

Returns: number ceiled to the decimal digits defined by the precision

clamp(number, lower, higher, precision) clamp - clamp with precision to the given most significant decimal point

Parameters:

number : - The floating point number

lower : - The lowerst number limit to return

higher : - The highest number limit to return

precision : - The number of decimal places a.k.a the most significant decimal digit - e.g precision 2 will produce 0.01 minimum change

Returns: number clamped to the decimal digits defined by the precision

ConditionalAverages█ OVERVIEW

This library is a Pine Script™ programmer’s tool containing functions that average values selectively.

█ CONCEPTS

Averaging can be useful to smooth out unstable readings in the data set, provide a benchmark to see the underlying trend of the data, or to provide a general expectancy of values in establishing a central tendency. Conventional averaging techniques tend to apply indiscriminately to all values in a fixed window, but it can sometimes be useful to average values only when a specific condition is met. As conditional averaging works on specific elements of a dataset, it can help us derive more context-specific conclusions. This library offers a collection of averaging methods that not only accomplish these tasks, but also exploit the efficiencies of the Pine Script™ runtime by foregoing unnecessary and resource-intensive for loops.

█ NOTES

To Loop or Not to Loop

Though for and while loops are essential programming tools, they are often unnecessary in Pine Script™. This is because the Pine Script™ runtime already runs your scripts in a loop where it executes your code on each bar of the dataset. Pine Script™ programmers who understand how their code executes on charts can use this to their advantage by designing loop-less code that will run orders of magnitude faster than functionally identical code using loops. Most of this library's function illustrate how you can achieve loop-less code to process past values. See the User Manual page on loops for more information. If you are looking for ways to measure execution time for you scripts, have a look at our LibraryStopwatch library .

Our `avgForTimeWhen()` and `totalForTimeWhen()` are exceptions in the library, as they use a while structure. Only a few iterations of the loop are executed on each bar, however, as its only job is to remove the few elements in the array that are outside the moving window defined by a time boundary.

Cumulating and Summing Conditionally

The ta.cum() or math.sum() built-in functions can be used with ternaries that select only certain values. In our `avgWhen(src, cond)` function, for example, we use this technique to cumulate only the occurrences of `src` when `cond` is true:

float cumTotal = ta.cum(cond ? src : 0) We then use:

float cumCount = ta.cum(cond ? 1 : 0) to calculate the number of occurrences where `cond` is true, which corresponds to the quantity of values cumulated in `cumTotal`.

Building Custom Series With Arrays

The advent of arrays in Pine has enabled us to build our custom data series. Many of this library's functions use arrays for this purpose, saving newer values that come in when a condition is met, and discarding the older ones, implementing a queue .

`avgForTimeWhen()` and `totalForTimeWhen()`

These two functions warrant a few explanations. They operate on a number of values included in a moving window defined by a timeframe expressed in milliseconds. We use a 1D timeframe in our example code. The number of bars included in the moving window is unknown to the programmer, who only specifies the period of time defining the moving window. You can thus use `avgForTimeWhen()` to calculate a rolling moving average for the last 24 hours, for example, that will work whether the chart is using a 1min or 1H timeframe. A 24-hour moving window will typically contain many more values on a 1min chart that on a 1H chart, but their calculated average will be very close.

Problems will arise on non-24x7 markets when large time gaps occur between chart bars, as will be the case across holidays or trading sessions. For example, if you were using a 24H timeframe and there is a two-day gap between two bars, then no chart bars would fit in the moving window after the gap. The `minBars` parameter mitigates this by guaranteeing that a minimum number of bars are always included in the calculation, even if including those bars requires reaching outside the prescribed timeframe. We use a minimum value of 10 bars in the example code.

Using var in Constant Declarations

In the past, we have been using var when initializing so-called constants in our scripts, which as per the Style Guide 's recommendations, we identify using UPPER_SNAKE_CASE. It turns out that var variables incur slightly superior maintenance overhead in the Pine Script™ runtime, when compared to variables initialized on each bar. We thus no longer use var to declare our "int/float/bool" constants, but still use it when an initialization on each bar would require too much time, such as when initializing a string or with a heavy function call.

Look first. Then leap.

█ FUNCTIONS

avgWhen(src, cond)

Gathers values of the source when a condition is true and averages them over the total number of occurrences of the condition.

Parameters:

src : (series int/float) The source of the values to be averaged.

cond : (series bool) The condition determining when a value will be included in the set of values to be averaged.

Returns: (float) A cumulative average of values when a condition is met.

avgWhenLast(src, cond, cnt)

Gathers values of the source when a condition is true and averages them over a defined number of occurrences of the condition.

Parameters:

src : (series int/float) The source of the values to be averaged.

cond : (series bool) The condition determining when a value will be included in the set of values to be averaged.

cnt : (simple int) The quantity of last occurrences of the condition for which to average values.

Returns: (float) The average of `src` for the last `x` occurrences where `cond` is true.

avgWhenInLast(src, cond, cnt)

Gathers values of the source when a condition is true and averages them over the total number of occurrences during a defined number of bars back.

Parameters:

src : (series int/float) The source of the values to be averaged.

cond : (series bool) The condition determining when a value will be included in the set of values to be averaged.

cnt : (simple int) The quantity of bars back to evaluate.

Returns: (float) The average of `src` in last `cnt` bars, but only when `cond` is true.

avgSince(src, cond)

Averages values of the source since a condition was true.

Parameters:

src : (series int/float) The source of the values to be averaged.

cond : (series bool) The condition determining when the average is reset.

Returns: (float) The average of `src` since `cond` was true.

avgForTimeWhen(src, ms, cond, minBars)

Averages values of `src` when `cond` is true, over a moving window of length `ms` milliseconds.

Parameters:

src : (series int/float) The source of the values to be averaged.

ms : (simple int) The time duration in milliseconds defining the size of the moving window.

cond : (series bool) The condition determining which values are included. Optional.

minBars : (simple int) The minimum number of values to keep in the moving window. Optional.

Returns: (float) The average of `src` when `cond` is true in the moving window.

totalForTimeWhen(src, ms, cond, minBars)

Sums values of `src` when `cond` is true, over a moving window of length `ms` milliseconds.

Parameters:

src : (series int/float) The source of the values to be summed.

ms : (simple int) The time duration in milliseconds defining the size of the moving window.

cond : (series bool) The condition determining which values are included. Optional.

minBars : (simple int) The minimum number of values to keep in the moving window. Optional.

Returns: (float) The sum of `src` when `cond` is true in the moving window.

MovingAveragesLibraryLibrary "MovingAveragesLibrary"

This is a library allowing one to select between many different Moving Average formulas to smooth out any float variable.

You can use this library to apply a Moving Average function to any series of data as long as your source is a float.

The default application would be for applying Moving Averages onto your chart. However, the scope of this library is beyond that. Any indicator or strategy you are building can benefit from this library.

You can apply different types of smoothing and moving average functions to your indicators, momentum oscillators, average true range calculations, support and resistance zones, envelope bands, channels, and anything you can think of to attempt to smooth out noise while finding a delicate balance against lag.

If you are developing an indicator, you can use the 'ave_func' to allow your users to select any Moving Average for any function or variable by creating an input string with the following structure:

var_name = input.string(, , )

Where the types of Moving Average you would like to be provided would be included in options.

Example:

i_ma_type = input.string(title = "Moving Average Type", defval = "Hull Moving Average", options = )

Where you would add after options the strings I have included for you at the top of the PineScript for your convenience.

Then for the output you desire, simply call 'ave_func' like so:

ma = ave_func(source, length, i_ma_type)

Now the plotted Moving Average will be the same as what you or your users select from the Input.

ema(src, len) Exponential Moving Average.

Parameters:

src : Series to use ('close' is used if no argument is supplied).

len : Lookback length to use.

Returns: Float value.

sma(src, len) Simple Moving Average.

Parameters:

src : Series to use ('close' is used if no argument is supplied).

len : Lookback length to use.

Returns: Float value.

rma(src, len) Relative Moving Average.

Parameters:

src : Series to use ('close' is used if no argument is supplied).

len : Lookback length to use.

Returns: Float value.

wma(src, len) Weighted Moving Average.

Parameters:

src : Series to use ('close' is used if no argument is supplied).

len : Lookback length to use.

Returns: Float value.

dv2(len) Donchian V2 function.

Parameters:

len : Lookback length to use.

Returns: Open + Close / 2 for the selected length.

ModFilt(src, len) Modular Filter smoothing function.

Parameters:

src : Series to use ('close' is used if no argument is supplied).

len : Lookback length to use.

Returns: Float value.

EDSMA(src, len) Ehlers Dynamic Smoothed Moving Average.

Parameters:

src : Series to use ('close' is used if no argument is supplied).

len : Lookback length to use.

Returns: EDSMA smoothing.

dema(x, t) Double Exponential Moving Average.

Parameters:

x : Series to use ('close' is used if no argument is supplied).

t : Lookback length to use.

Returns: DEMA smoothing.

tema(src, len) Triple Exponential Moving Average.

Parameters:

src : Series to use ('close' is used if no argument is supplied).

len : Lookback length to use.

Returns: TEMA smoothing.

smma(x, t) Smoothed Moving Average.

Parameters:

x : Series to use ('close' is used if no argument is supplied).

t : Lookback length to use.

Returns: SMMA smoothing.

vwma(x, t) Volume Weighted Moving Average.

Parameters:

x : Series to use ('close' is used if no argument is supplied).

t : Lookback length to use.

Returns: VWMA smoothing.

hullma(x, t) Hull Moving Average.

Parameters:

x : Series to use ('close' is used if no argument is supplied).

t : Lookback length to use.

Returns: Hull smoothing.

covwma(x, t) Coefficient of Variation Weighted Moving Average.

Parameters:

x : Series to use ('close' is used if no argument is supplied).

t : Lookback length to use.

Returns: COVWMA smoothing.

frama(x, t) Fractal Reactive Moving Average.

Parameters:

x : Series to use ('close' is used if no argument is supplied).

t : Lookback length to use.

Returns: FRAMA smoothing.

kama(x, t) Kaufman's Adaptive Moving Average.

Parameters:

x : Series to use ('close' is used if no argument is supplied).

t : Lookback length to use.

Returns: KAMA smoothing.

donchian(len) Donchian Calculation.

Parameters:

len : Lookback length to use.

Returns: Average of the highest price and the lowest price for the specified look-back period.

tma(src, len) Triangular Moving Average.

Parameters:

src : Series to use ('close' is used if no argument is supplied).

len : Lookback length to use.

Returns: TMA smoothing.

VAMA(src, len) Volatility Adjusted Moving Average.

Parameters:

src : Series to use ('close' is used if no argument is supplied).

len : Lookback length to use.

Returns: VAMA smoothing.

Jurik(src, len) Jurik Moving Average.

Parameters:

src : Series to use ('close' is used if no argument is supplied).

len : Lookback length to use.

Returns: JMA smoothing.

MCG(src, len) McGinley smoothing.

Parameters:

src : Series to use ('close' is used if no argument is supplied).

len : Lookback length to use.

Returns: McGinley smoothing.

zlema(series, length) Zero Lag Exponential Moving Average.

Parameters:

series : Series to use ('close' is used if no argument is supplied).

length : Lookback length to use.

Returns: ZLEMA smoothing.

xema(src, len) Optimized Exponential Moving Average.

Parameters:

src : Series to use ('close' is used if no argument is supplied).

len : Lookback length to use.

Returns: XEMA smoothing.

EhlersSuperSmoother(src, lower) Ehlers Super Smoother.

Parameters:

src : Series to use ('close' is used if no argument is supplied).

lower : Smoothing value to use.

Returns: Ehlers Super smoothing.

EhlersEmaSmoother(sig, smoothK, smoothP) Ehlers EMA Smoother.

Parameters:

sig : Series to use ('close' is used if no argument is supplied).

smoothK : Lookback length to use.

smoothP : Smothing value to use.

Returns: Ehlers EMA smoothing.

ave_func(in_src, in_len, in_type) Returns the source after running it through a Moving Average function.

Parameters:

in_src : Series to use ('close' is used if no argument is supplied).

in_len : Lookback period to be used for the Moving Average function.

in_type : Type of Moving Average function to use. Must have a string input to select the options from that MUST match the type-casing in the function below.

Returns: The source as a float after running it through the Moving Average function.

lib_MilitzerLibrary "lib_Militzer"

// This is a collection of functions either found on the internet, or made by me.

// This is only public so my other scripts that reference this can also be public.

// But if you find anything useful here, be my guest.

print()

strToInt()

timeframeToMinutes()

MathProbabilityDistributionLibrary "MathProbabilityDistribution"

Probability Distribution Functions.

name(idx) Indexed names helper function.

Parameters:

idx : int, position in the range (0, 6).

Returns: string, distribution name.

usage:

.name(1)

Notes:

(0) => 'StdNormal'

(1) => 'Normal'

(2) => 'Skew Normal'

(3) => 'Student T'

(4) => 'Skew Student T'

(5) => 'GED'

(6) => 'Skew GED'

zscore(position, mean, deviation) Z-score helper function for x calculation.

Parameters:

position : float, position.

mean : float, mean.

deviation : float, standard deviation.

Returns: float, z-score.

usage:

.zscore(1.5, 2.0, 1.0)

std_normal(position) Standard Normal Distribution.

Parameters:

position : float, position.

Returns: float, probability density.

usage:

.std_normal(0.6)

normal(position, mean, scale) Normal Distribution.

Parameters:

position : float, position in the distribution.

mean : float, mean of the distribution, default=0.0 for standard distribution.

scale : float, scale of the distribution, default=1.0 for standard distribution.

Returns: float, probability density.

usage:

.normal(0.6)

skew_normal(position, skew, mean, scale) Skew Normal Distribution.

Parameters:

position : float, position in the distribution.

skew : float, skewness of the distribution.

mean : float, mean of the distribution, default=0.0 for standard distribution.

scale : float, scale of the distribution, default=1.0 for standard distribution.

Returns: float, probability density.

usage:

.skew_normal(0.8, -2.0)

ged(position, shape, mean, scale) Generalized Error Distribution.

Parameters:

position : float, position.

shape : float, shape.

mean : float, mean, default=0.0 for standard distribution.

scale : float, scale, default=1.0 for standard distribution.

Returns: float, probability.

usage:

.ged(0.8, -2.0)

skew_ged(position, shape, skew, mean, scale) Skew Generalized Error Distribution.

Parameters:

position : float, position.

shape : float, shape.

skew : float, skew.

mean : float, mean, default=0.0 for standard distribution.

scale : float, scale, default=1.0 for standard distribution.

Returns: float, probability.

usage:

.skew_ged(0.8, 2.0, 1.0)

student_t(position, shape, mean, scale) Student-T Distribution.

Parameters:

position : float, position.

shape : float, shape.

mean : float, mean, default=0.0 for standard distribution.

scale : float, scale, default=1.0 for standard distribution.

Returns: float, probability.

usage:

.student_t(0.8, 2.0, 1.0)

skew_student_t(position, shape, skew, mean, scale) Skew Student-T Distribution.

Parameters:

position : float, position.

shape : float, shape.

skew : float, skew.

mean : float, mean, default=0.0 for standard distribution.

scale : float, scale, default=1.0 for standard distribution.

Returns: float, probability.

usage:

.skew_student_t(0.8, 2.0, 1.0)

select(distribution, position, mean, scale, shape, skew, log) Conditional Distribution.

Parameters:

distribution : string, distribution name.

position : float, position.

mean : float, mean, default=0.0 for standard distribution.

scale : float, scale, default=1.0 for standard distribution.

shape : float, shape.

skew : float, skew.

log : bool, if true apply log() to the result.

Returns: float, probability.

usage:

.select('StdNormal', __CYCLE4F__, log=true)

historicalrangeLibrary "historicalrange"

Library provices a method to calculate historical percentile range of series.

hpercentrank(source) calculates historical percentrank of the source

Parameters:

source : Source for which historical percentrank needs to be calculated. Source should be ranging between 0-100. If using a source which can beyond 0-100, use short term percentrank to baseline them.

Returns: pArray - percentrank array which contains how many instances of source occurred at different levels.

upperPercentile - percentile based on higher value

lowerPercentile - percentile based on lower value

median - median value of the source

max - max value of the source

distancefromath(source) returns stats on historical distance from ath in terms of percentage

Parameters:

source : for which stats are calculated

Returns: percentile and related historical stats regarding distance from ath

distancefromma(maType, length, source) returns stats on historical distance from moving average in terms of percentage

Parameters:

maType : Moving Average Type : Can be sma, ema, hma, rma, wma, vwma, swma, highlow, linreg, median

length : Moving Average Length

source : for which stats are calculated

Returns: percentile and related historical stats regarding distance from ath

bpercentb(source, maType, length, multiplier, sticky) returns percentrank and stats on historical bpercentb levels

Parameters:

source : Moving Average Source

maType : Moving Average Type : Can be sma, ema, hma, rma, wma, vwma, swma, highlow, linreg, median

length : Moving Average Length

multiplier : Standard Deviation multiplier

sticky : - sticky boundaries which will only change when value is outside boundary.

Returns: percentile and related historical stats regarding Bollinger Percent B

kpercentk(source, maType, length, multiplier, useTrueRange, sticky) returns percentrank and stats on historical kpercentk levels

Parameters:

source : Moving Average Source

maType : Moving Average Type : Can be sma, ema, hma, rma, wma, vwma, swma, highlow, linreg, median

length : Moving Average Length

multiplier : Standard Deviation multiplier

useTrueRange : - if set to false, uses high-low.

sticky : - sticky boundaries which will only change when value is outside boundary.

Returns: percentile and related historical stats regarding Keltener Percent K

dpercentd(useAlternateSource, alternateSource, length, sticky) returns percentrank and stats on historical dpercentd levels

Parameters:

useAlternateSource : - Custom source is used only if useAlternateSource is set to true

alternateSource : - Custom source

length : - donchian channel length

sticky : - sticky boundaries which will only change when value is outside boundary.

Returns: percentile and related historical stats regarding Donchian Percent D

oscillator(type, length, shortLength, longLength, source, highSource, lowSource, method, highlowLength, sticky) oscillator - returns Choice of oscillator with custom overbought/oversold range

Parameters:

type : - oscillator type. Valid values : cci, cmo, cog, mfi, roc, rsi, stoch, tsi, wpr

length : - Oscillator length - not used for TSI

shortLength : - shortLength only used for TSI

longLength : - longLength only used for TSI

source : - custom source if required

highSource : - custom high source for stochastic oscillator

lowSource : - custom low source for stochastic oscillator

method : - Valid values for method are : sma, ema, hma, rma, wma, vwma, swma, highlow, linreg, median

highlowLength : - length on which highlow of the oscillator is calculated

sticky : - overbought, oversold levels won't change unless crossed

Returns: percentile and related historical stats regarding oscillator

ArrayOperationsLibrary "ArrayOperations"

Array element wise basic operations.

add(sample_a, sample_b) Adds sample_b to sample_a and returns a new array.

Parameters:

sample_a : values to be added to.

sample_b : values to add.

Returns: array with added results.

- sample_a provides type format for output.

- arrays do not need to be symmetric.

- sample_a must have same or more elements than sample_b

subtract(sample_a, sample_b) Subtracts sample_b from sample_a and returns a new array.

sample_a : values to be subtracted from.

sample_b : values to subtract.

Returns: array with subtracted results.

- sample_a provides type format for output.

- arrays do not need to be symmetric.

- sample_a must have same or more elements than sample_b

multiply(sample_a, sample_b) multiply sample_a by sample_b and returns a new array.

sample_a : values to multiply.

sample_b : values to multiply with.

Returns: array with multiplied results.

- sample_a provides type format for output.

- arrays do not need to be symmetric.

- sample_a must have same or more elements than sample_b

divide(sample_a, sample_b) Divide sample_a by sample_b and returns a new array.

sample_a : values to divide.

sample_b : values to divide with.

Returns: array with divided results.

- sample_a provides type format for output.

- arrays do not need to be symmetric.

- sample_a must have same or more elements than sample_b

power(sample_a, sample_b) power sample_a by sample_b and returns a new array.

sample_a : values to power.

sample_b : values to power with.

Returns: float array with power results.

- sample_a provides type format for output.

- arrays do not need to be symmetric.

- sample_a must have same or more elements than sample_b

remainder(sample_a, sample_b) Remainder sample_a by sample_b and returns a new array.

sample_a : values to remainder.

sample_b : values to remainder with.

Returns: array with remainder results.

- sample_a provides type format for output.

- arrays do not need to be symmetric.

- sample_a must have same or more elements than sample_b

equal(sample_a, sample_b) Check element wise sample_a equals sample_b and returns a new array.

sample_a : values to check.

sample_b : values to check.

Returns: int array with results.

- sample_a provides type format for output.

- arrays do not need to be symmetric.

- sample_a must have same or more elements than sample_b

not_equal(sample_a, sample_b) Check element wise sample_a not equals sample_b and returns a new array.

sample_a : values to check.

sample_b : values to check.

Returns: int array with results.

- sample_a provides type format for output.

- arrays do not need to be symmetric.

- sample_a must have same or more elements than sample_b

over_or_equal(sample_a, sample_b) Check element wise sample_a over or equals sample_b and returns a new array.

sample_a : values to check.

sample_b : values to check.

Returns: int array with results.

- sample_a provides type format for output.

- arrays do not need to be symmetric.

- sample_a must have same or more elements than sample_b

under_or_equal(sample_a, sample_b) Check element wise sample_a under or equals sample_b and returns a new array.

sample_a : values to check.

sample_b : values to check.

Returns: int array with results.

- sample_a provides type format for output.

- arrays do not need to be symmetric.

- sample_a must have same or more elements than sample_b

over(sample_a, sample_b) Check element wise sample_a over sample_b and returns a new array.

sample_a : values to check.

sample_b : values to check.

Returns: int array with results.

- sample_a provides type format for output.

- arrays do not need to be symmetric.

- sample_a must have same or more elements than sample_b

under(sample_a, sample_b) Check element wise sample_a under sample_b and returns a new array.

sample_a : values to check.

sample_b : values to check.

Returns: int array with results.

- sample_a provides type format for output.

- arrays do not need to be symmetric.

- sample_a must have same or more elements than sample_b

and_(sample_a, sample_b) Check element wise sample_a and sample_b and returns a new array.

sample_a : values to check.

sample_b : values to check.

Returns: int array with results.

- sample_a provides type format for output.

- arrays do not need to be symmetric.

- sample_a must have same or more elements than sample_b

or_(sample_a, sample_b) Check element wise sample_a or sample_b and returns a new array.

sample_a : values to check.

sample_b : values to check.

Returns: int array with results.

- sample_a provides type format for output.

- arrays do not need to be symmetric.

- sample_a must have same or more elements than sample_b

all(sample) Check element wise if all numeric samples are true (!= 0).

sample : values to check.

Returns: int.

any(sample) Check element wise if any numeric samples are true (!= 0).

sample : values to check.

Returns: int.