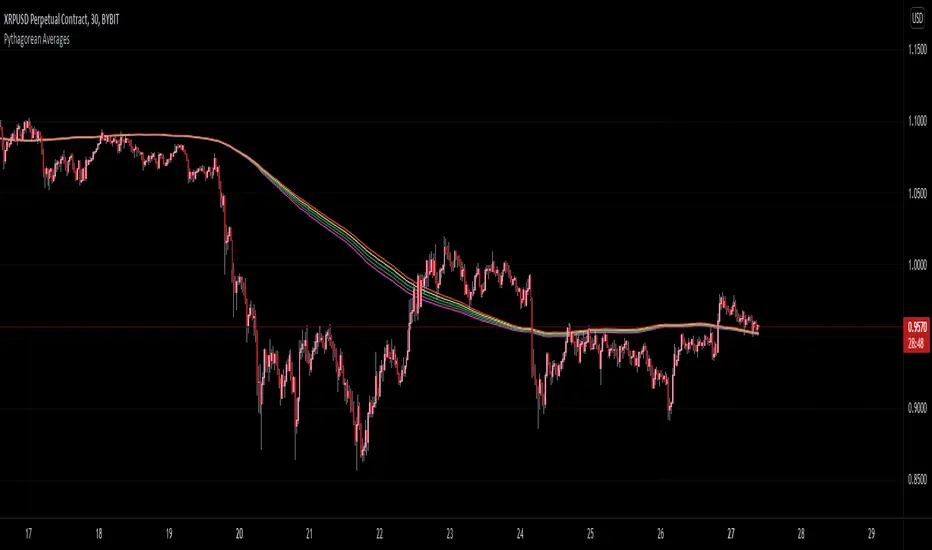

Pythagorean Moving Averages (and more)When you think of the question "take the mean of this dataset", you'd normally think of using the arithmetic mean because usually the norm is equal to 1; however, there are an infinite number of other types of means depending on the function norm (p).

Pythagoras' is credited for the main types of means: his harmonic mean, his geometric mean, and his arithmetic mean:

Harmonic Average (p = -1):

- Take the reciprocal of all the numbers in the dataset, add them all together, divide by the amount of numbers added together, then take the reciprocal of the final answer.

Geometric Average (p = 0):

- Multiply all the numbers in the dataset, then take the nth root where n is equal to the amount of number you multiplied together.

Arithmetic Mean (p = 1):

- Add all the numbers in the dataset, then divide by the amount of numbers you added by.

A couple other means included in this script were the quadratic mean (p = 2) and the cubic mean (p = 3).

Quadratic Mean (p = 2):

- Square every number in the dataset, then divide by the amount of numbers your added by, then take the square root.

Cubic Mean (p = 3):

- Cube every number in the dataset, then divide by the amount of numbers you added by, then take the cube root.

There are an infinite number of means for every scenario of p, but they begin to follow a pattern after p = 3.

Read more:

www.cs.uni.edu

en.wikipedia.org

en.wikipedia.org

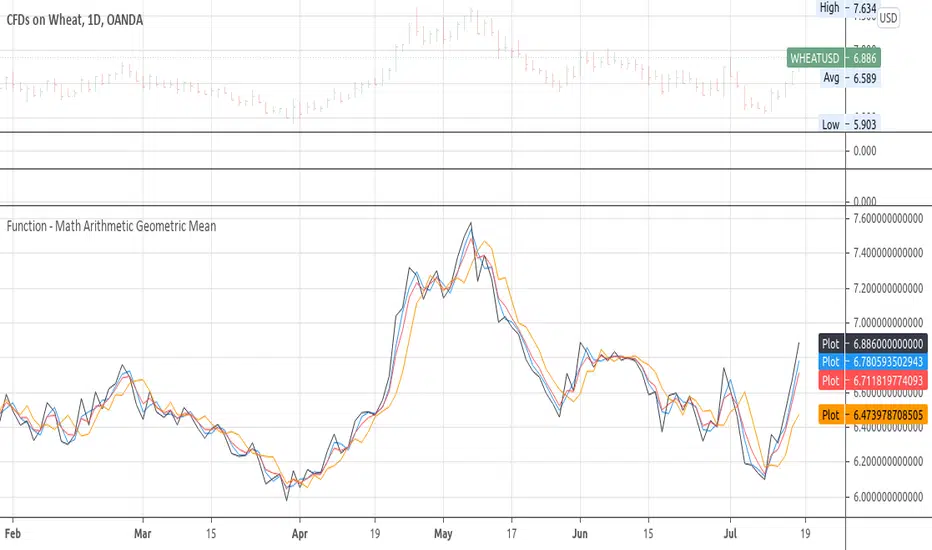

Note : I added the functions for the quadratic mean and cubic mean, but since market charts don't have those types of graphs, the functions don't usually work. It's the same reason why sometimes you'll see the harmonic average not working.

Disclaimer : This is not financial or mathematical advice, please look for someone certified before making any decisions.

Mean

Roc Mean Reversion (ValueRay)This Indicator shows the Absolute Rate of Change in correlation to its Moving Average.

Values over 3 (gray dotted line) can savely be considered as a breakout; values over 4.5 got a high mean-reverting chance (red dotted line).

This Indicator can be used in all timeframes, however, i recommend to use it <30m, when you want search for meaningful Mean-Reverting Signals.

Please like, share and subscribe. With your love, im encouraged to write and publish more Indicators.

Drift Study (Inspired by Monte Carlo Simulations with BM) [KL]Inspired by the Brownian Motion ("BM") model that could be applied to conducting Monte Carlo Simulations, this indicator plots out the Drift factor contributing to BM.

Interpretation : If the Drift value is positive, then prices are possibly moving in an uptrend. Vice versa for negative drifts.

Res/Sup With Concavity & Increasing / Decreasing Trend AnalysisPurple means the concavity is down blue means concavity is up which is good.

Yellow means increasing, Red means decreasing.

Sup = Green

Res = Red

Coefficient of variation (standard deviation over mean)Shows the coefficient of variation defined as standard deviation over mean (for the specified window).

Hurst ExponentMy first try to implement Full Hurst Exponent.

The Hurst exponent is used as a measure of long-term memory of time series. It relates to the autocorrelations of the time series and the rate at which these decrease as the lag between pairs of values increases

The Hurst exponent is referred to as the "index of dependence" or "index of long-range dependence". It quantifies the relative tendency of a time series either to regress strongly to the mean or to cluster in a direction.

In short, depending on the value you can spot the trending / reversing market.

Values 0.5 to 1 - market trending

Values 0 to 0.5 - market tend to mean revert

Hurst Exponent is computed using Rescaled range (R/S) analysis.

I split the lookback period (N) in the number of shorter samples (for ex. N/2, N/4, N/8, etc.). Then I calculate rescaled range for each sample size.

The Hurst exponent is estimated by fitting the power law. Basically finding the slope of log(samples_size) to log(RS).

You can choose lookback and sample sizes yourself. Max 8 possible at the moment, if you want to use less use 0 in inputs.

It's pretty computational intensive, so I added an input so you can limit from what date you want it to be calculated. If you hit the time limit in PineScript - limit the history you're using for calculations.

####################

Disclaimer

Please remember that past performance may not be indicative of future results.

Due to various factors, including changing market conditions, the strategy may no longer perform as good as in historical backtesting.

This post and the script don’t provide any financial advice.

Simple Hurst Exponent [QuantNomad]This is a simplified version of the Hurst Exponent indicator.

In the meantime, I'm working on the full version. It's computationally intensive, so it's a challenge to squeeze it to PineScript limits. It will require some time to optimize it, so I decided to publish a simplified version for now.

The Hurst exponent is used as a measure of long-term memory of time series. It relates to the autocorrelations of the time series, and the rate at which these decrease as the lag between pairs of values increases

The Hurst exponent is referred to as the "index of dependence" or "index of long-range dependence". It quantifies the relative tendency of a time series either to regress strongly to the mean or to cluster in a direction.

In short depend on value you can spot trending / reversing market.

Values 0.5 to 1 - market trending

Values 0 to 0.5 - market tend to mean revert

####################

Disclaimer

Please remember that past performance may not be indicative of future results.

Due to various factors, including changing market conditions, the strategy may no longer perform as good as in historical backtesting.

This post and the script don’t provide any financial advice.

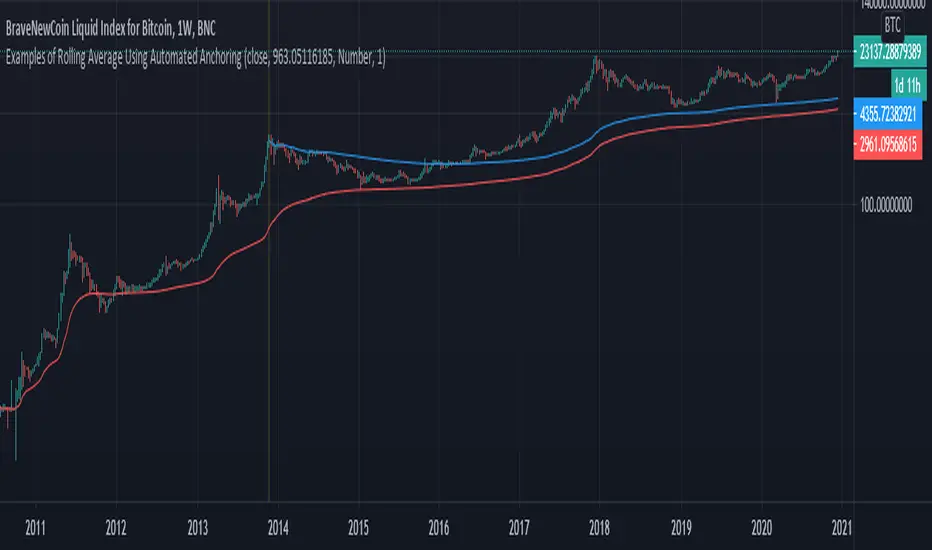

Examples of Rolling Average Using Automated AnchoringIn this study, I present a method to expose NaN values to development environment.

This exposure allows NaN values to be used by methods in scripts.

I also show how to use values, even NaN values, as anchors from which statistics can be computed from.

I demonstrate how to do this with constants and variables in methods for computing the cumulative/rolling average of a series.

I also show how to calculate the cumulative/rolling average from the start of a ticker series using the aforementioned methods.

Each method has a description on how some of their parts work as well as their constraints.

Method #1 - Can only be used for computing the rolling average on the ticker series.

Method #2 - The simple moving average from the Pine Script reference.

- Can be used to calculate the rolling average of the ticker series and number values of a series.

- This method seems to cause an error when there are many bars in the series.

Method #3 - The most versatile method due to the use of computing the rolling average using an array.

- Timeout will occur when computing the rolling average of an entire ticker series which is long.

- Timeout has not occurred when computing a rolling average of a series from NaN or non-NaN anchor points even when the series is long.

This is an attempt to get around the constraints of the built-in sma(source, length) function in which length cannot be dynamically adjusted.

Other Pine Script functions have that constraint which we can get around by defining our own functions.

Mean ExtremeA simple script that shows the distance from a the mean, expressed as a percentage.

Simple Moving Average, in this case.

Informational only.

Z-Score 'Bollinger Bands'The following script is an application of the Z-Score (previous script).

Z-Scores can be used in place of standard deviation (sigma) in 'Bollinger Bands'.

The average of the sample (x-bar) over 21 days (N)

21 average trading days per month, fixed value

The average of the population (mu) over 63 days (n)

63 days per quarter, default is set to 63

Z-Score is calculated by formula in previous script, and the absolute value is taken of "Z".

Z-High = absolute value of Z + (x-bar).

Z-Low = absolute value of Z - (x-bar).

Will update with Z from mu and Z from avg (working on UX and visualization details).

Z-Score The z-score is a way of counting the number of standard deviations between a given data value and the mean of the data set.

Z-score = (x̄ - μ) / (σ / √ n)

x̄ = sample mean (using the array.avg function = array(a,close ), where i = 1 to 21)

μ = population mean ( = avg(close, n))

σ = standard deviation of the population ( = stdev(close,n))

n = number of 'close' or trading day closes

n = input

... Note: The previous indicator is part of a larger series of indicators

Mean recursion envelopeFree for public consumption

There is very little original here, the idea is discussed in the underground traders alliance, (google em), and was apparently the basis of what was at one time myfxbooks most profitable strategy.

I can't find the original video that was floating around on youtube, but if i find it again, i'll link it here.

This is bascially just the TV default envelope code copied and modified.

The idea is to have an envelope based on a low length, exponential basis. Then to manually "tune" the percent input so that the envelopes engulf most bars. Whenever price goes outside the envelopes (especially at key levels), look for a change to enter a reversion back to the ema.

This manual tuning when switching between time-frames and symbols of the percentage input, becomes arduous.

Instead this script uses the TV envelope code, but gets a setting based on the average of true range and "autotunes" with this.

Anything that protrudes beyond that level, especially at key levels, is likely to revert back to the ema. Bear in mind, a run away trend will also push past the envelopes and continue running for several (3-5) bars so, use it mindfully and thoughtfully with all the usual cautions about risk management.

Spread by//Every spread & central tendency measure in 1 script with comfortable visualization, including scrips's status line.

Spread measures:

- Standard deviation (for most cases);

- Average deviation (if there are extreme values);

- GstDev - Geometric Standard Deviation (exclusively for Geometric Mean);

- HstDev - Harmonic Deviation (exclusively for Harmonic Mean).

These modified functions will calculate everything right, they will take source, length, AND basis of your choice, unlike the ones from TW.

Central tendency measures:

- Mean (if everything's cool & equal);

- Median (values clustering towards low/high part of the rolling window);

- Trimean (3/more distinguishable clusters of data);

- Midhinhe (2 distinguishable clusters of data);

- Geometric Mean ( |low.. ... ... .. .... ... . . . . . . . . . . . .high| this kinda data); <- Exp law

- Harmonic Mean { |low. . . . . . . . . . . . . . .. . . .high| kinda data). <- Reciprocal law

Listen:

1) Don't hesitate using Standard Deviation with non-mean, like "Midhinge Standard Devition", despite what ol' stats gurus gonna say, it works when it's appropriate;

2) Don't check log space while using Geometric Mean & Geometric Standard Deviation, these 2 implement log stuff by design, I mean unless u wanna make it double xd

3) You can use this script, modify it how you want, ask me questions whatever, just make money using it;

4) Use Midrange & Midpoints in tandem when data follows ~addition law (like this . . . . . . . . . . . . . . . . . . . . .). <- just addition law

Look at the data, choose spread measure first, then choose central tendency measure, not vice versa.

!!!

Ain't gonna place ® sign on standard deviations like one B guy did in 1980s lmao, but if your wanna use Harmonic Deviations in science/write about/cite it/whatever, pls give me a lil credit at least, I've never seen it anywhere and unfortunately had to develop it by myself. it's useful when your data develops by reciprocals law (opposite to exponential).

Peace TW

Harmonic MADsNo, it's not a new saturation plugin for your fruity loops.

...

These are Mean Average Deviations calculated from Harmonic Mean.

...

In my previous research I tried to develop "Harmonic Average Deviations", since applying stdevs on Harmonic Mean calculated from reciprocals ain't make sense. Din't work out, prolly cuz by definition stdevs doesn't like negatives. So in the end I ended up using Mean Average Deviations, and turned out it works great. Generally market data doesn't distribute normally, so t's a great tool, now weird kurtosis won't be a problem.

[R&D] Harmonic deviationsI'm publishing it for research purposes & welcome any ideas and/or explanations whether it's actually possible or nah to do what I'm doing right now.

...

Idea is simple - if we can do Harmonic Mean, can we do Harmonic Standard Deviations? It should be the same logic, the only difference is instead of actual datapoints we gotta use reciprocals.

In reality I've found smth really curios, it's possible to get these Harmonic Standard Deviations, however, somewhy, depends on your timeframe, u gotta do final sqrt different amount of times. And looks like... the market reacts to these levels.

That's why in the script settings there is a menu where you can choose how many times to perform sqrt operation.

Pls check it out, play with it, see maybe you'll see smth interesting.

Harmonic Moving AverageI was legitimately surprised no1 has already coded it out on TradingView, but you guys can copypaste & include it in Pine 5 if your see this xd

Here is it.

I've checked and double checked everything, the calculations are right, it can be proved by plotting mean, geometric mean & harmonic mean together and noticing that geometric mean will be always between Harmonic mean, which is always below, and Mean, which is always above.

...

Other central tendency measures are also here as well for usability.

Ehlers Zero Mean Roofing Filter [CC]The Zero Mean Roofing Filter was created by John Ehlers (Cycle Analytics For Traders pg 80) and this is a much more reactive roofing filter compared to Ehler's Roofing Filter which I also added for reference. Buy when the indicator rises over 0 and sell when the indicator falls below 0.

This was a special request so let me know if there are other indicators you would like to see me publish or if you want something custom done!

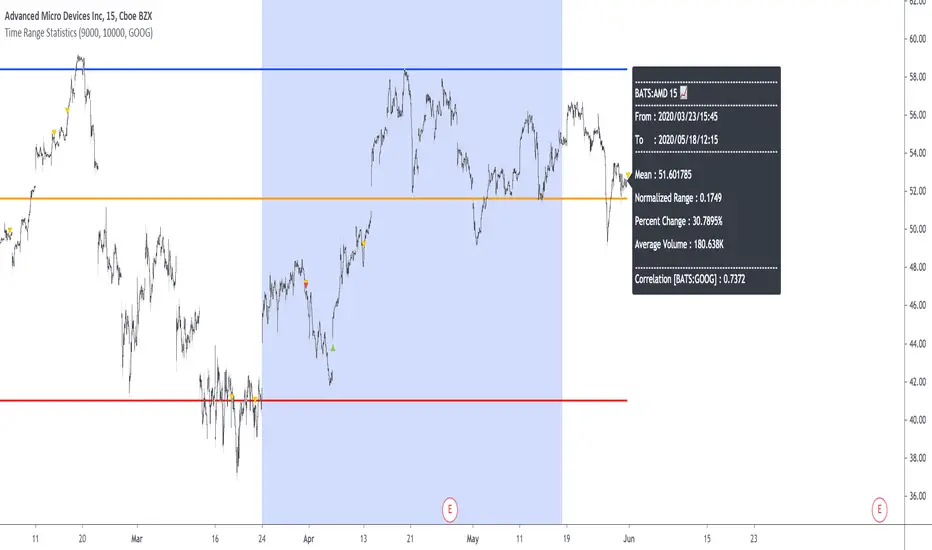

Time Range StatisticsA good amount of users requested a text box showing various price statistics, the following script returns various of these stats in a user-selected range, and include classical ones such as a central tendency measurement (mean), dispersion (normalized range) and percent change, but also include less common statistics such as average traded volume and number of gaps. The script also calculates the correlation between the closing price and another user-selected instrument.

The script is currently the longest one I ever made and took some efforts, as I wasn't satisfied with the statistics to be originally included. Big thx to Gael for the enormous feedback and the idea of the normalized range, to user @Cookiecrush for the feedback ( without ya I would have posted something bad you know umu ? ), and Lulidolce for the support, friendship is magic!

Selected Range

The setting Start determine the bar at which the range starts, while End determine at which bar the range end. To help you select these values, the current bar number (bar index) is displayed at the right of the indicator title in blue.

The setting evaluate to last bar will use a range starting at Start and ending at the last bar, as such you can use a full range by using Start = 0 and select evaluate to last bar

The range is highlighted by an area on the chart. By default Start = 9000 and End = 10000, you might not have this amount of data in your chart, as such use the displayed bar index to select Start and End, then set the settings as default.

Displayed Statistics

The statistics panel is displayed on the right side of the last bar, the panel has 3 sections, a title section who shows the symbol ticker, timeframe, and overall trends represented by a chart emoji, the overall trends are determined by comparing the number of higher highs with the number of lower low.

Below are displayed the date ranges with time format: year/month/day/hour:minute.

The second section shows the general statistics. The first one is the mean, also represented by the orange line in the chart, the blue line displayed represent the highest price value in the range, while the red one represents the lowest price value.

The second stat is the normalized range, and determine how spread is the price in the user-selected range, why not the standard deviation? Because the standard deviation might return results varying widely depending on the scale of the closing price, you could get measures such as 0.0156 or 16 or even 56 depending on the instrument, as such using a normalized range can be more appropriate as it lays in a range of (0,1). Lower values indicate a low degree of price variation. Note that I still want to find another measure in the future.

The percentage change (or relative change) indicates at which percentage the price has increased or decreased, and is calculated by subtracting the closing at bar Start with the price at bar End , divided by the price at bar End , the result is then multiplied by 100.

The average traded volume calculate the mean of the volume in the selected range, I used the same format used by the original volume indicator for clarity.

Finally, the last stats of the section is the number of gaps, this stat is by default hidden. An up gap is detected when the open price is superior to the previous high, while a down gap is detected when the open price is inferior to the previous low, this allow to only retain significant gaps.

The last section of the indicator panel shows the correlation between the closing price and another instrument, by default GOOG, this correlation is also calculated within the user-selected range. Positive values indicate a positive relationship, that is the two instruments tend to move in the same direction. Negative values indicate a negative relationship, both instruments tend to move in a direction opposite to each other. Values closer to 1 or -1 indicate a stronger relationship, while values closer to 0 indicate no relationship.

In Summary

The script shows various stats, each calculated within a user-selected range, in general one would be more interested in how these stats might evolve with time, but checking them in a custom range can be quite interesting.

Thx for reading. umu

Rolling deviationsSometimes the market data follows normal distribution, in these cases it is more appropriate to utilize mean-based statistical techniques. This script plots the special case of seven-number summary with 1st, 2nd & 3rd standard deviations below and above the mean.

It also has "Log-space" switch which should be checked while using logarithmic scale.

The next version with minor visual improvs might arrive soon

Bars above/below EMACount of previous bars above or below a chosen Exponential Moving Average. Typically price reconnects with well defined EMAs regularly. If the price has been above/below an EMA for too long, you can expect a reconnect in a short order and bet on mean reversion strategies.