Torben Moving MedianThis method was pointed it out by Torben Mogensen.

It is certainly not the fastest way of finding a median, but it has the very interesting property that it does not modify the input array when looking for the median. It becomes extremely powerful when the number of elements to consider starts to be large, and copying the input array may cause enormous overheads. For read-only input sets of several hundred megabytes in size, it is the solution of choice, also because it accesses elements sequentially and not randomly. Beware that it needs to read the array several times though: a first pass is only looking for min and max values, further passes go through the array and come out with the median in little more time. The number of iterations is probably O(log(n)), although I have no demonstration of that fact.

What is Median Filtering

Median filtering is a commonly used technique in signal processing. Typically used on signals that may contain outliers skewing the usual statistical estimators, it is usually considered too expensive to be implemented in real-time or CPU-intensive applications.

Let us define the median of N numerical values by:

The median of a list of N values is found by sorting the input array in increasing order, and taking the middle value.

The median of a list of N values has the property that in the list there are as many greater as smaller values than this element.

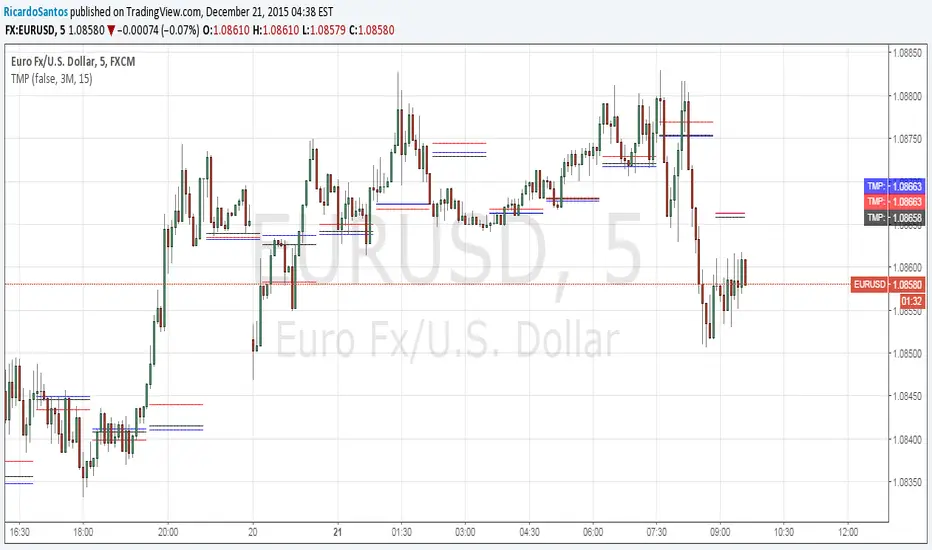

How To trade

Trading is quite intuitive

Buy when the Price breaks-out the price which breaked the Torben Moving Median

Median

Median CrossOver LevelsPlots levels representing the prices that the stock closed above its n-period moving median(default=100).

2 thickest lines represents the two most recent crossover levels.

Candles are colored green if the price is currently above its moving median and red if below.

Percentile Nearest Rank Using Arrays [LuxAlgo]The new array feature is extremely powerful, as it will allow pinescript users to do more complex things, or compute existing calculations more efficiently, it will also be possible to shine some light to some already existing functions, one of them being percentile_nearest_rank .

We have been working on this new feature with our pal alexgrover, and made this script which computes a rolling percentile using the nearest rank method.

Settings

Length: Window of the rolling percentile, determine the number of past data to be used.

Percentage: Return the current value if Percentage % of the data fall below that value, the setting is in a range (0,100).

Src: Input source of the indicator.

Usage

A rolling percentile can have many usages when it comes to technical analysis, this is due to its ability to return the value of three common rolling statistics, the rolling median, which can be obtained using a percentage equal to 50, the rolling maximum, obtained with a percentage equal to 100, and the rolling minimum, obtained with a percentage equal to 0.

When we use our rolling percentile as a rolling median, we can obtain a robust estimation of the underlying trend in the price, while using it as a rolling maximum/minimum can allow us to determine if the market is trending, and at which direction. The rolling maximum/minimum is a rolling statistic used to calculate the well known stochastic oscillator and Donchian channel indicator.

We can also compute rolling quartiles, which can be obtained using a percentage of 25 or 75, with one of 25 returning the lower quartile and 75 the upper quartile.

In blue the upper rolling quartile (%75), in orange the lower rolling quartile (%25), both using a window size of 100.

Details

In order to compute a rolling percentile nearest rank, we must first take the most recent length closing prices, then order them in ascending order, we then return the value of the ordered observations at index (percentage/100*length) - 1 (we use - 1 because our array index starts at 0).

Spread by//Every spread & central tendency measure in 1 script with comfortable visualization, including scrips's status line.

Spread measures:

- Standard deviation (for most cases);

- Average deviation (if there are extreme values);

- GstDev - Geometric Standard Deviation (exclusively for Geometric Mean);

- HstDev - Harmonic Deviation (exclusively for Harmonic Mean).

These modified functions will calculate everything right, they will take source, length, AND basis of your choice, unlike the ones from TW.

Central tendency measures:

- Mean (if everything's cool & equal);

- Median (values clustering towards low/high part of the rolling window);

- Trimean (3/more distinguishable clusters of data);

- Midhinhe (2 distinguishable clusters of data);

- Geometric Mean ( |low.. ... ... .. .... ... . . . . . . . . . . . .high| this kinda data); <- Exp law

- Harmonic Mean { |low. . . . . . . . . . . . . . .. . . .high| kinda data). <- Reciprocal law

Listen:

1) Don't hesitate using Standard Deviation with non-mean, like "Midhinge Standard Devition", despite what ol' stats gurus gonna say, it works when it's appropriate;

2) Don't check log space while using Geometric Mean & Geometric Standard Deviation, these 2 implement log stuff by design, I mean unless u wanna make it double xd

3) You can use this script, modify it how you want, ask me questions whatever, just make money using it;

4) Use Midrange & Midpoints in tandem when data follows ~addition law (like this . . . . . . . . . . . . . . . . . . . . .). <- just addition law

Look at the data, choose spread measure first, then choose central tendency measure, not vice versa.

!!!

Ain't gonna place ® sign on standard deviations like one B guy did in 1980s lmao, but if your wanna use Harmonic Deviations in science/write about/cite it/whatever, pls give me a lil credit at least, I've never seen it anywhere and unfortunately had to develop it by myself. it's useful when your data develops by reciprocals law (opposite to exponential).

Peace TW

Range identifier by medianThis study tries to highlight ranges

as they are defined by

TradingLatino TradingView user.

The study uses median values.

A range is defined as periods when the price does not move a lot.

Its default values are aimed at BTCUSDT pair and 4h timeframe.

HOW IT WORKS

For each of the bars a '5' median is calculated based on the 'highest of open and close'

For each of the bars a '5' median is calculated based on the 'lowest of open and close'

Thanks to the desviation setting both medians

have a tolerated maximum and a minimum

Condition 1:

The bar current 'highest of open and close'

needs to be between the respective tolerated

maximum and minimum

Condition 2:

The bar current 'lowest of open and close'

needs to be between the respective tolerated

maximum and minimum

If both conditions are met

then the bar is in a range

SETTINGS

Price range periods : How many previous periods are used to calculate the medians

Price range maximum desviation (%) ( > 0 ): Maximum positive desviation for range detection

Price range minimum desviation (%) ( > 0 ): Mininum negative desviation for range detection

Desviations should be both of them a positive number

WARNING

Despite the name indicator does not identify the entire range.

It identifies when you realise you are inside a range.

E.g. If a range length is 8 periods length this range indicator

will highlight only the last 6 periods of the range.

USAGE

If your strategy signals you an upwards trend

then you might use this range detector

to know when to exit your long position

Why?

Because most of the times

the price is found to be

in a range it goes down

FEEDBACK 1

My former attempt on calculating ranges

felt too much over complex that is why

I decided to implement it with medians.

It should be easier to modify if

I want to desviation inputs to be calculated

automatically in the future.

I'm interested on different approaches on how to detect ranges.

FEEDBACK 2

I have only used this identifier in BTCUSDT 4h timeframe.

Feel free to comment down below with your suggested settings

for your favourite pair and timeframe

PINE SCRIPT TRICK

This script simulates looping an string char by char

in pine script.

Rolling summaryStatistical methods based on mean cannot be effective all the time when attributed to financial data since it doesn't usually follow normal distribution, the data can be skewed or/and have extreme values which can be described as outliers.

In order to deal with this problem it is appropriate to use median-based techniques.

The most common one is called five-number summary/box plot, which plots median of the dataset, 25th (Q1) & 75th (Q3) percentiles (the medians of lower & upper parts of the original dataset divided by the original median), and whiskers calculated by taking range between Q1 and Q3, multiplying it by 1.5 and adding it to Q3 and subtracting it from Q1. The values which are outside the whiskers are considered outliers. Default settings of the script correspond to the classic box plot.

Seven-number summary can be also plotted by this script, by turning on 4 additional percentiles/Bowley’s seven-figure summary by turning on first 2 additional percentiles and changing their values to 10 and 90 respectively.

P.S.: Mean can be also turned in just to check the difference.

Recursive Median Oscillator & Fisher Transforms RibbonThis is a composite indicator made up of:

- modifided (rescaled) version of evergets version of recursive median oscillator.

- 1996anoojpatels Futur modification of Ehlers Fisher Transform Ribbons Indicator

I think Ehlers attempts to minimise latency in indicators are extremely valuable and some of my most use trading tools. Thanks to all the authors whose iterations keep moving these indicators toward perfection. Here is my contribution.

MCI and VCI - Modified CCI FormulasFor private peeps only

- Takes a modified version of the CCI formula into 2 parts

VCI - Volume Channel Index (Yellow Histogram)

- Measures accurate accumulation and distribution levels and times

MCI - Modified Channel Index

- Measures (when compared to VCI) levels where clearly buys are interested vs not interested.

Example:

If VCI > MCI

- Shows buyer's are more than interested in buying, you've either hit a bottom or heavy resistance

if MCI > VCI

- Show's buyer's aren't interested and will most likely result in a dump/lower price

Great for monitoring accumulation and distribution, these auto buy and sells look for the transition points over 0, works on EVERY commodity/stock/FOREX/Crypto

Results are from trading 1 BTC x25 leveraging. Not all trades will get in if put in at limit, but it does survive with profits after the massive 0.075 fee (results shown are after fees)

[RESEARCH] Custom Median vs Built-in MedianI compared custom median (using the sorting solution by @apozdnyakov) with built-in median (using percentile_nearest_rank function)

If you see the zero line this means the solutions give the same results.

The best results was achieved on the odd lengths.

Conclusions:

1) Do not try to reinvent the wheel.

2) Always check the Pine Script docs to find already implemented solutions.

Ehlers Smoothed Adaptive MomentumEhlers Smoothed Adaptive Momentum script.

This indicator was developed and described by John F. Ehlers in his book "Cybernetic Analysis for Stocks and Futures" (2004, Chapter 12: Adapting to the Trend).

Hampel FilterHampel Filter script.

This indicator was originally developed by Frank Rudolf Hampel (Journal of the American Statistical Association, 69, 382–393, 1974: The influence curve and its role in robust estimation).

The Hampel filter is a simple but effective filter to find outliers and to remove them from data. It performs better than a median filter.

Interquartile Range BandsInterquartile Range Bands script.

This indicator was originally developed by Alex Orekhov at his home.

The idea based on the interquartile range en.wikipedia.org

If price breaks out from the bands then it is `outlier` price.

After breakouts price always returns to its median.

Watch squeeze/expansion periods.

Anyway use it as a supplement to the other indicators.

I will glad to get your feedback.

Recursive Median FilterRecursive Median Filter indicator script.

This indicator was originally developed by John F. Ehlers (Stocks & Commodities V. 36:03 (8–11): Recursive Median Filters).

Recursive Median OscillatorRecursive Median Oscillator indicator script.

This indicator was originally developed by John F. Ehlers (Stocks & Commodities V. 36:03 (8–11): Recursive Median Filters).

Bill Williams Averages. 3Lines Strategy This indicator calculates 3 Moving Averages for default values of

13, 8 and 5 days, with displacement 8, 5 and 3 days: Median Price (High+Low/2).

The most popular method of interpreting a moving average is to compare

the relationship between a moving average of the security's price with

the security's price itself (or between several moving averages).

Function Mean Median Mode V0EXPERIMENTAL:

Request for GLAZ

Functions to handle Mean, Median, Mode Calculation.

% Median v1 This indicator shows the percentage amount the price is above or below the moving median value of the period.

This indicator is best used along with the moving median (set to the same period).

Based on the moving median developed with 4x4good

Moving MedianThis simple script was a collaborative effort with 4X4good.

It plots a moving median for the period using the 50th percentile value.

We wanted to know the median value of VIX but surprisingly, a median indicator wasn't yet available in the indicators library.

So we did a little research & put this together.

Simple Horizontal Value and Offsets [Auto Shift]Original (Simple Horizontal Value and Offsets/SHV) Requested by @TAFA94

Description:

Simple adjustable incremented horizontal offset lines extending up and down from a Median point.

Set full value for manual Median point control, or set an incremental rounding value for auto Median adjustment.

Source and look-back period inputs for fine tuning auto adjust.

Auto adjust on by default - can be toggled off for straight manual control.

**NOTE**

All values will likely need to be changed immediately on applying this script, in order to properly fit your charts specific price/value range and/or time resolution.

Cheers!

[RS]Temporal Median Price V1EXPERIMENTAL: previous custom time window median price and current time window open price in a neat package :p

(JeanLouisHardy) added option for bar count system, also added a donchian average.