GoatsGlowingRSIGoatsGlowingRSI is a visually enhanced and feature-rich RSI (Relative Strength Index) indicator designed for deeper market insight and clearer signal visualization. It combines standard RSI analysis with gradient-colored backgrounds, glowing effects, and automated divergence detection to help traders spot potential reversals and momentum shifts more effectively.

Key Features:

✅ Multi-Timeframe RSI:

Calculate RSI from any timeframe using the custom input. Leave it blank to use the current chart's timeframe.

✅ Dynamic Gradient Background:

A smooth gradient fill is applied between RSI levels from the lower band (30) to the upper band (70). The gradient shifts from blue (oversold) to red (overbought), visually highlighting the RSI's position and strength.

✅ Glowing RSI Line:

A three-layered glow effect surrounds the main RSI line, creating a striking white core with a purple aura that enhances visibility against dark or light chart themes.

✅ Custom RSI Levels:

Dashed horizontal lines at RSI 70 (overbought), RSI 30 (oversold), and a dotted midline at 50 help you interpret trend momentum and strength.

✅ Automatic Divergence Detection:

Built-in logic identifies bullish and bearish divergences by comparing RSI and price pivot points:

🟢 Bullish Divergence: RSI makes a higher low while price makes a lower low.

🔴 Bearish Divergence: RSI makes a lower high while price makes a higher high.

Divergences are marked on the RSI line with colored lines and labels ("Bull"/"Bear").

✅ Alerts Ready:

Get notified in real-time with alert conditions for both bullish and bearish divergence setups.

Oscillators

BK AK-Scope🔭 Introducing BK AK-Scope — Target Locked. Signal Acquired. 🔭

After building five precision weapons for traders, I’m proud to unveil the sixth.

BK AK-Scope — the eye of the arsenal.

This is not just an indicator. It’s an intelligence system for volatility, signal clarity, and rate-of-change dynamics — forged for elite vision in any market terrain.

🧠 Why “Scope”? And Why “AK”?

Every shooter knows: you can’t hit what you can’t see.

The Scope brings range, clarity, and target distinction. It filters motion from noise. Purpose from panic.

“AK” continues to honor the man who trained my sight — my mentor, A.K.

His discipline taught me to wait for alignment. To move with reason, not emotion.

His vision lives in every code line here.

🔬 What Is BK AK-Scope?

A Triple-Tier TSI Correlation Engine, fused with adaptive opacity logic, a volatility scoring system, and real-time signal clarity. It’s momentum dissected — by speed, depth, and rate of change.

Built to serve traders who:

Need visual hierarchy between fast, mid, and slow TSI responses.

Want adaptive fills that pulse with volatility — not static zones.

Require a volatility scoring overlay that reads the battlefield in real time.

⚙️ Core Systems: How BK AK-Scope Works

✅ Fast/Mid/Slow TSI →

Three layers of correlation: like scopes with zoom levels.

You track micro moves, mid swings, and macro flow simultaneously.

✅ Rate-of-Change Adaptive Opacity →

Momentum fills fade or flash based on speed — giving you movement density at a glance.

Bull vs. Bear zones adapt to strength. You feel the market’s pulse.

✅ Volatility Score Intelligence →

Custom algorithm measuring:

Range expansion

Rate-of-change differentials

ATR dynamics

Standard deviation pressure

All combined into a score from 0–100 with live icons:

🔥 = Extreme Heat (70+)

🧊 = Cold Zone (<30)

⚠️ = ROC Warning

• = Neutral drift

✅ Auto-Detect Volatility Modes →

Scalp = <15min

Swing = intraday/hourly

Macro = daily/weekly

Or override manually with total control.

🎯 How To Use BK AK-Scope

🔹 Trend Continuation → When all three TSI layers align in direction + volatility score climbs, ride with the trend.

🔹 Early Reversals → Opposing TSI + rapid opacity change + volatility shift = sniper reversal zone.

🔹 Consolidation Filter → Neutral fills + score < 30 = stay out, wait for signal surge.

🔹 Signal Confluence → Pair with:

• Gann fans or angles

• Fib time/price clusters

• Elliott Wave structure

• Harmonics or divergence

To isolate entry perfection.

🛡️ Why This Indicator Changes the Game

It's not just momentum. It’s TSI with depth hierarchy.

It’s not just color. It’s real-time strength visualization.

It’s not just volatility. It’s rate-weighted market intelligence.

This is market optics for the advanced trader — built for vision, clarity, and discipline.

🙏 Final Thoughts

🔹 In honor of A.K., my mentor. The man who taught me to see what others miss.

🔹 Inspired by the power of vision — because execution without clarity is chaos.

🔹 Powered by faith — because Gd alone gives sight beyond the visible.

“He gives sight to the blind and wisdom to the humble.” — Psalms 146

Every tool I build is a prayer in code — that it helps someone trade with clarity, integrity, and precision.

⚡ Zoom In. Focus Deep. Trade Clean.

BK AK-Scope — Lock on the target. See what others don’t.

🔫 Clarity is power. 🔫

Gd bless. 🙏

Z-Score Adaptive Connors RSIZ-Score Adaptive Connors RSI blends the classic three-component Connors RSI (RSI, Up/Down streak RSI, and Percentile Rank of 1-bar ROC) with a dynamic z-score filter that distinguishes trending vs. mean-reverting market regimes.

When the indicator detects an extreme deviation (|z-score| > threshold) , it switches to “trending” mode and tightens entry thresholds for capturing momentum. When markets are in a more neutral regime, it reverts to wider thresholds, hunting for overbought/oversold reversals.

Key Features

Connors RSI Core: Combines price momentum, streak measurements, and velocity for a robust baseline oscillator. Z-Score Regime Filter: Computes the z-score of the Connors RSI over a lookback window to adapt your trading style to trending vs. reverting environments.

Dynamic Thresholds: Separate user-configurable thresholds for trending (“tight” entries) and mean-reverting (“wide” entries) scenarios.

Inputs & Parameters

Connors RSI Settings

RSI Source: Price series for RSI calculation (default: Close)

RSI Length: Period for price‐change RSI (default: 24)

Up/Down Length: Period for streak RSI (default: 20)

ROC Length: Period for percentile‐rank of 1-bar return (default: 75)

Z-Score Filter

Lookback: Number of bars to compute mean and standard deviation of Connors RSI (default: 14)

Threshold: Minimum |z-score| to enter “trending” mode (default: 1.5)

Entry Thresholds

Trending Long/Short: Upper and lower RSI Thresholds when trending

Reverting Long/Short: Upper and lower RSI Thresholds when reverting

RSI Multi-TF TabRSI Multi-Timeframe Table 📊

A tool for multi-timeframe RSI analysis with visual overbought/oversold level highlighting.

Description

This indicator calculates the Relative Strength Index (RSI) for the current chart and displays RSI values across five additional timeframes (15m, 1h, 4h, 1d, 1w) in a dynamic table. The color-coded system simplifies identifying overbought (>70), oversold (<30), and neutral zones. Visual signals on the chart enhance analysis for the current timeframe.

Key Features

✅ Multi-Timeframe Analysis :

Track RSI across 15m, 1h, 4h, 1d, and 1w in a compact table.

Color-coded alerts:

🔴 Red — Overbought (potential pullback),

🔵 Blue — Oversold (potential rebound),

🟡 Yellow — Neutral zone.

✅ Visual Signals :

Background shading for oversold/overbought zones on the main chart.

Horizontal lines at 30 and 70 levels for reference.

✅ Customizable Settings :

Adjust RSI length (default: 14), source (close, open, high, etc.), and threshold levels.

How to Use

Table Analysis :

Compare RSI values across timeframes to spot divergences (e.g., overbought on 15m vs. oversold on D).

Use colors for quick decisions.

Chart Signals :

Blue background suggests bullish potential (oversold), red hints at bearish pressure (overbought).

Always confirm with other tools (volume, trends, or candlestick patterns).

Examples :

RSI(1h) > 70 while RSI(4h) < 30 → Possible reversal upward.

Sustained RSI(1d) above 50 may indicate a bullish trend.

Settings

RSI Length : Period for RSI calculation (default: 14).

RSI Source : Data source (close, open, high, low, hl2, hlc3, ohlc4).

Overbought/Oversold Levels : Thresholds for alerts (default: 70/30).

Important Notes

No direct trading signals : Use this as an analytical tool, not a standalone strategy.

Test strategies historically and consider market context before trading.

PCA Regime-Adjusted MomentumSummary

The PCA Regime-Adjusted Momentum (PCA-RAM) is an advanced market analysis tool designed to provide nuanced insights into market momentum and structural stability. It moves beyond traditional indicators by using Principal Component Analysis (PCA) to deconstruct market data into its most essential patterns.

The indicator provides two key pieces of information:

A smoothed momentum signal based on the market's dominant underlying trend.

A dynamic regime filter that gauges the stability and clarity of the market's structure, advising you when to trust or fade the momentum signals.

This allows traders to not only identify potential shifts in momentum but also to understand the context and confidence behind those signals.

Core Concepts & Methodology

The strength of this indicator lies in its sound, data-driven methodology.

1. Principal Component Analysis (PCA)

At its core, the indicator analyzes a rolling window (default 50 periods) of standardized market data (Open, High, Low, Close, and Volume). PCA is a powerful statistical technique that distills this complex, 5-dimensional data into its fundamental, uncorrelated components of variance. We focus on the First Principal Component (PC1), which represents the single most dominant pattern or "theme" driving the market's behavior in the lookback window.

2. The Momentum Signal

Instead of just looking at price, we project the current market data onto this dominant underlying pattern (PC1). This gives us a raw "projection score" that measures how strongly the current bar aligns with the historically dominant market structure. This raw score is then smoothed using two an exponential moving averages (a fast and a slow line) to create a clear, actionable momentum signal, similar in concept to a MACD.

3. The Dynamic Regime Filter

This is arguably the indicator's most powerful feature. It answers the question: "How clear is the current market picture?"

It calculates the Market Concentration Ratio, which is the percentage of total market variance explained by PC1 alone.

A high ratio indicates that the market is moving in a simple, one-dimensional way (e.g., a clear, strong trend).

A low ratio indicates the market is complex, multi-dimensional, and choppy, with no single dominant theme.

Crucially, this filter is dynamic. It compares the current concentration ratio to its own recent average, allowing it to adapt to any asset or timeframe. It automatically learns what "normal" and "choppy" look like for the specific chart you are viewing.

How to Interpret the Indicator

The indicator is displayed in a separate pane with two key visual elements:

The Momentum Lines (White & Gold)

White Line: The "Fast Line," representing the current momentum.

Gold Line: The "Slow Line," acting as the trend confirmation.

Bullish Signal: A crossover of the White Line above the Gold Line suggests a shift to positive momentum.

Bearish Signal: A crossover of the White Line below the Gold Line suggests a shift to negative momentum.

The Regime Filter (Purple & Dark Red Background)

This is your confidence gauge.

Navy Blue Background (High Concentration): The market structure is stable, simple, and trending. Momentum signals are more reliable and should be given higher priority.

Dark Red Background (Low Concentration): The market structure is complex, choppy, or directionless. Momentum signals are unreliable and prone to failure or "whipsaws." This is a signal to be cautious, tighten stops, or potentially stay out of the market.

Potential Trading Strategies

This tool is versatile and can be used in several ways:

1. Primary Signal Strategy

Condition: Wait for the background to turn Purple, confirming a stable, high-confidence regime.

Entry: Take the next crossover signal from the momentum lines (White over Gold for long, White under Gold for short).

Exit/Filter: Consider exiting positions or ignoring new signals when the background turns Navy.

2. As a Confirmation or Filter for Your Existing Strategy

Do you have a trend-following system? Only enable its long and short signals when the PCA-RAM background is Purple.

Do you have a range-trading or mean-reversion system? It might be most effective when the PCA-RAM background is Navy, indicating a lack of a clear trend.

3. Advanced Divergence Analysis

Look for classic divergences between price and the momentum lines. For example, if the price is making a new high, but the Gold Line is making a lower high, it may indicate underlying weakness in the trend, even on a Purple background. This divergence signal is more powerful because it shows that the new price high is not being confirmed by the market's dominant underlying pattern.

Laplace Momentum Percentile ║ BullVision 🔬 Overview

Laplace Momentum Percentile ║ BullVision is a custom-built trend analysis tool that applies Laplace-inspired smoothing to price action and maps the result to a historical percentile scale. This provides a contextual view of trend intensity, with optional signal refinement using a Kalman filter.

This indicator is designed for traders and analysts seeking a normalized, scale-independent perspective on market behavior. It does not attempt to predict price but instead helps interpret the relative strength or weakness of recent movements.

⚙️ Key Concepts

📉 Laplace-Based Smoothing

The core signal is built using a Laplace-style weighted average, applying an exponential decay to price values over a specified length. This emphasizes recent movements while still accounting for historical context.

🎯 Percentile Mapping

Rather than displaying the raw output, the filtered signal is converted into a percentile rank based on its position within a historical lookback window. This helps normalize interpretation across different assets and timeframes.

🧠 Optional Kalman Filter

For users seeking additional smoothing, a Kalman filter is included. This statistical method updates signal estimates dynamically, helping reduce short-term fluctuations without introducing significant lag.

🔧 User Settings

🔁 Transform Parameters

Transform Parameter (s): Controls the decay rate for Laplace weighting.

Calculation Length: Sets how many candles are used for smoothing.

📊 Percentile Settings

Lookback Period: Defines how far back to calculate the historical percentile ranking.

🧠 Kalman Filter Controls

Enable Kalman Filter: Optional toggle.

Process Noise / Measurement Noise: Adjust the filter’s responsiveness and tolerance to volatility.

🎨 Visual Settings

Show Raw Signal: Optionally display the pre-smoothed percentile value.

Thresholds: Customize upper and lower trend zone boundaries.

📈 Visual Output

Main Line: Smoothed percentile rank, color-coded based on strength.

Raw Line (Optional): The unsmoothed percentile value for comparison.

Trend Zones: Background shading highlights strong upward or downward regimes.

Live Label: Displays current percentile value and trend classification.

🧩 Trend Classification Logic

The indicator segments percentile values into five zones:

Above 80: Strong upward trend

50–80: Mild upward trend

20–50: Neutral zone

0–20: Mild downward trend

Below 0: Strong downward trend

🔍 Use Cases

This tool is intended as a visual and contextual aid for identifying trend regimes, assessing historical momentum strength, or supporting broader confluence-based analysis. It can be used in combination with other tools or frameworks at the discretion of the trader.

⚠️ Important Notes

This script does not provide buy or sell signals.

It is intended for educational and analytical purposes only.

It should be used as part of a broader decision-making process.

Past signal behavior should not be interpreted as indicative of future results.

Strategy Builder With IndicatorsThis strategy script is designed for traders who enjoy building systems using multiple indicators.

Please note: This script does not include any built-in indicators. Instead, it works by referencing the plot outputs of the indicators you’ve already added to your chart.

For example, if you add a MACD and an ATR indicator to your chart, you can assign their plot values as inputs in the settings panel of this strategy.

• MACD as a trigger

• ATR as a filter

How Filters Work

Filters check whether certain conditions are met before a trade can be opened. For instance, if you set a filter like ATR > 30, then no trade will be executed unless that condition is true — even if the trigger fires.

All filters are linked, meaning every active filter must be satisfied for a trade to occur.

How Triggers Work

Triggers are what actually fire a trade signal — such as a moving average crossover or RSI breaking above a specific level. Unlike filters, triggers are independent. Only one active trigger needs to be true for the trade to execute.

Thanks to its modular structure, this strategy can be used with any indicator of your choice.

⸻

Risk Management Features

In the settings, you’ll find flexible options for:

• Stop Loss (SL)

• Trailing Stop Loss (TSL)

• Multi Take-Profit (TP)

These features enhance trade safety and let you tailor your risk management.

SL types available:

• Tick-based SL

• Percent-based SL

• ATR-based SL

Once you select your preferred SL type, you can fine-tune its distance using the offset field.

Trailing SL allows your stop to follow price as it moves in your favor — helping to lock in profits.

Multi-TP lets you take profits at two different levels, helping you secure gains while leaving room for extended moves.

Breakeven option is also available to automatically move your SL to entry after reaching a profit threshold.

⸻

How to Build a Solid Strategy

Let’s break down a good setup into three key components:

1. Trend Filter

Avoid trading against the trend — that’s like swimming against the current.

Use a filter like:

• Supertrend

• Momentum indicators

• Candlestick bias, etc.

Example: In this case, I used Supertrend and filtered for trades only if the price is above the uptrend line.

2. Trigger Condition

Once we confirm the trend is on our side, we need a trigger to execute at the right moment. This can be:

• RSI cross

• Candlestick patterns

• Trendline breaks

• Moving average crossovers, etc.

Example: I used RSI crossing above 50 as the entry trigger.

3. Risk Management

Even in the right trend at the right time — anything can happen. That’s why you should always define Stop Loss and Take Profit levels.

⸻

And there you have it! Your strategy is ready to backtest, refine, and deploy with alerts for live trading.

Questions or suggestions? Feel free to reach out

Commodity Trend Reactor [BigBeluga]

🔵 OVERVIEW

A dynamic trend-following oscillator built around the classic CCI, enhanced with intelligent price tracking and reversal signals.

Commodity Trend Reactor extends the traditional Commodity Channel Index (CCI) by integrating trend-trailing logic and reactive reversal markers. It visualizes trend direction using a trailing stop system and highlights potential exhaustion zones when CCI exceeds extreme thresholds. This dual-level system makes it ideal for both trend confirmation and mean-reversion alerts.

🔵 CONCEPTS

Based on the CCI (Commodity Channel Index) oscillator, which measures deviation from the average price.

Trend bias is determined by whether CCI is above or below user-defined thresholds.

Trailing price bands are used to lock in trend direction visually on the main chart.

Extreme values beyond ±200 are treated as potential reversal zones.

🔵 FEATURES\

CCI-Based Trend Shifts:

Triggers a bullish bias when CCI crosses above the upper threshold, and bearish when it crosses below the lower threshold.

Adaptive Trailing Stops:

In bullish mode, a trailing stop tracks the lowest price; in bearish mode, it tracks the highest.

Top & Bottom Markers:

When CCI surpasses +200 or drops below -200, it plots colored squares both on the oscillator and on price, marking potential reversal zones.

Background Highlights:

Each time a trend shift occurs, the background is softly colored (lime for bullish, orange for bearish) to highlight the change.

🔵 HOW TO USE

Use the oscillator to monitor when CCI crosses above or below threshold values to detect trend activation.

Enter trades in the direction of the trailing band once the trend bias is confirmed.

Watch for +200 and -200 square markers as warnings of potential mean reversals.

Use trailing stop areas as dynamic support/resistance to manage stop loss and exit strategies.

The background color changes offer clean confirmation of trend transitions on chart.

🔵 CONCLUSION

Commodity Trend Reactor transforms the simple CCI into a complete trend-reactive framework. With real-time trailing logic and clear reversal alerts, it serves both momentum traders and contrarian scalpers alike. Whether you’re trading breakouts or anticipating mean reversions, this indicator provides clarity and structure to your decision-making.

Session-Based Sentiment Oscillator [TradeDots]Track, analyze, and monitor market sentiment across global trading sessions with this advanced multi-session sentiment analysis tool. This script provides session-specific sentiment readings for Asian (Tokyo), European (London), and US (New York) markets, combining price action, volume analysis, and volatility factors into a comprehensive sentiment oscillator. It is an original indicator designed to help traders understand regional market psychology and capitalize on cross-session sentiment shifts directly on TradingView.

📝 HOW IT WORKS

1. Multi-Component Sentiment Engine

Price Action Momentum : Calculates normalized price movement relative to recent trading ranges, providing directional sentiment readings.

Volume-Weighted Analysis : When volume data is available, incorporates volume flow direction to validate price-based sentiment signals.

Volatility-Adjusted Factors : Accounts for changing market volatility conditions by comparing current ATR against historical averages.

Weighted Combination : Merges all components using optimized weightings (Price: 1.0, Volume: 0.3, Volatility: 0.2) for balanced sentiment readings.

2. Session-Segregated Tracking

Automatic Session Detection : Precisely identifies active trading sessions based on user-configured time parameters.

Independent Calculations : Maintains separate sentiment accumulation for each major session, updated only during respective active hours.

Historical Preservation : Stores session-specific sentiment values even when sessions are closed, enabling cross-session comparison.

Real-Time Updates : Continuously processes sentiment during active sessions while preserving inactive session data.

3. Cross-Session Transition Analysis

Sentiment Differential Detection : Monitors sentiment changes when transitioning between trading sessions.

Configurable Thresholds : Generates signals only when sentiment shifts exceed user-defined minimum thresholds.

Directional Signals : Provides distinct bullish and bearish transition alerts with visual markers.

Smart Filtering : Applies smoothing algorithms to reduce false signals from minor sentiment variations.

⚙️ KEY FEATURES

1. Session-Specific Dashboard

Real-Time Status Display : Shows current session activity (ACTIVE/CLOSED) for all three major sessions.

Sentiment Percentages : Displays precise sentiment readings as percentages for easy interpretation.

Strength Classification : Automatically categorizes sentiment as HIGH (>50%), MEDIUM (20-50%), or LOW (<20%).

Customizable Positioning : Place dashboard in any corner with adjustable size options.

2. Advanced Signal Generation

Transition Alerts : Triangle markers indicate significant sentiment shifts between sessions.

Extreme Conditions : Diamond markers highlight overbought/oversold threshold breaches.

Configurable Sensitivity : Adjust signal thresholds from 0.05 to 0.50 based on trading style.

Alert Integration : Built-in TradingView alert conditions for automated notifications.

3. Forex Currency Strength Analysis

Base/Quote Decomposition : For forex pairs, separates sentiment into individual currency strength components.

Major Currency Support : Analyzes USD, EUR, GBP, JPY, CHF, CAD, AUD, NZD strength relationships.

Relative Strength Display : Shows which currency is driving pair movement during active sessions.

4. Visual Enhancement System

Session Background Colors : Distinct background shading for each active trading session.

Overbought/Oversold Zones : Configurable extreme sentiment level visualization with colored zones.

Multi-Timeframe Compatibility : Works across all timeframes while maintaining session accuracy.

Customizable Color Schemes : Full color customization for dashboard, signals, and plot elements.

🚀 HOW TO USE IT

1. Add the Script

Search for "Session-Based Sentiment Oscillator " in the Indicators tab or manually add it to your chart. The indicator will appear in a separate pane below your main chart.

2. Configure Session Times

Asian Session : Set Tokyo market hours (default: 00:00-09:00) based on your chart timezone.

European Session : Configure London market hours (default: 07:00-16:00) for European analysis.

US Session : Define New York market hours (default: 13:00-22:00) for American markets.

Timezone Adjustment : Ensure session times match your broker's specifications and account for daylight saving changes.

3. Optimize Analysis Parameters

Sentiment Period : Choose 5-50 bars (default: 14) for sentiment calculation lookback period.

Smoothing Settings : Select 1-10 bars smoothing (default: 3) with SMA, EMA, or RMA options.

Component Selection : Enable/disable volume analysis, price action, and volatility factors based on available data.

Signal Sensitivity : Adjust threshold from 0.05-0.50 (default: 0.15) for transition signal generation.

4. Interpret Readings and Signals

Positive Values : Indicate bullish sentiment for the active session.

Negative Values : Suggest bearish sentiment conditions.

Dashboard Status : Monitor which session is currently active and their respective sentiment strengths.

Transition Signals : Watch for triangle markers indicating significant cross-session sentiment changes.

Extreme Alerts : Note diamond markers when sentiment reaches overbought (>70%) or oversold (<-70%) levels.

5. Set Up Alerts

Configure TradingView alerts for:

- Bullish session transitions

- Bearish session transitions

- Overbought condition alerts

- Oversold condition alerts

❗️LIMITATIONS

1. Data Dependency

Volume Requirements : Volume-based analysis only functions when volume data is provided by your broker. Many forex brokers do not supply reliable volume data.

Price Action Focus : In absence of volume data, sentiment calculations rely primarily on price movement and volatility factors.

2. Session Time Sensitivity

Manual Adjustment Required : Session times must be manually updated for daylight saving time changes.

Broker Variations : Different brokers may have slightly different session definitions requiring time parameter adjustments.

3. Ranging Market Limitations

Trend Bias : Sentiment calculations may be less reliable during extended sideways or low-volatility market conditions.

Lag Consideration : As with all sentiment indicators, readings may lag during rapid market transitions.

4. Regional Market Focus

Major Session Coverage : Designed primarily for major global sessions; may not capture sentiment from smaller regional markets.

Weekend Gaps : Does not account for weekend gap effects on sentiment calculations.

⚠️ RISK DISCLAIMER

Trading and investing carry significant risk and can result in financial loss. The "Session-Based Sentiment Oscillator " is provided for informational and educational purposes only. It does not constitute financial advice.

- Always conduct your own research and analysis

- Use proper risk management and position sizing in all trades

- Past sentiment patterns do not guarantee future market behavior

- Combine this indicator with other technical and fundamental analysis tools

- Consider overall market context and your personal risk tolerance

This script is an original creation by TradeDots, published under the Mozilla Public License 2.0.

Session-based sentiment analysis should be used as part of a comprehensive trading strategy. No single indicator can predict market movements with certainty. Exercise proper risk management and maintain realistic expectations about indicator performance across varying market conditions.

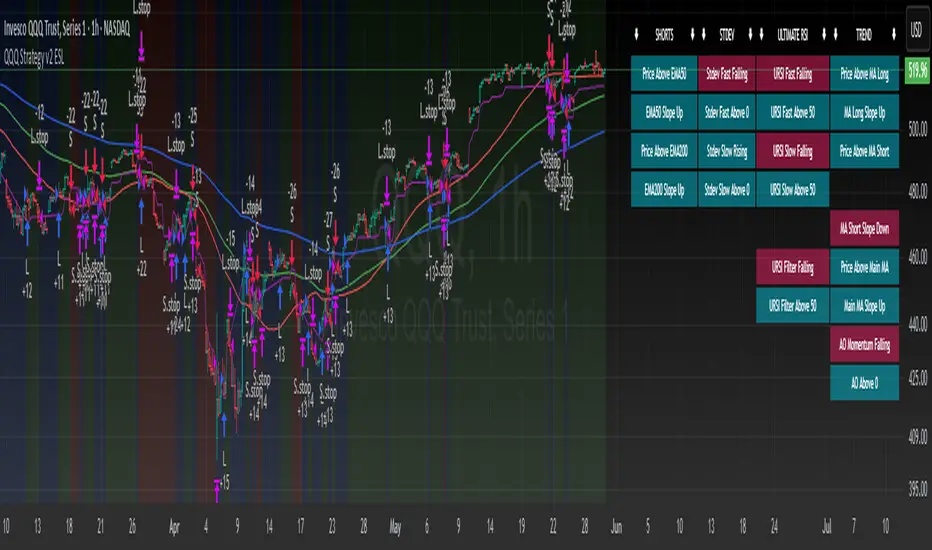

QQQ Strategy v2 ESL | easy-peasy-x This is a strategy optimized for QQQ (and SPY) for the 1H timeframe. It significantly outperforms passive buy-and-hold approach. With settings adjustments, it can be used on various assets like stocks and cryptos and various timeframes, although the default out of the box settings favor QQQ 1H.

The strategy uses various triggers to take both long and short trades. These can be adjusted in settings. If you try a different asset, see what combination of triggers works best for you.

Some of the triggers employ LuxAlgo's Ultimate RSI - shoutout to him for great script, check it out here .

Other triggers are based on custom signed standard deviation - basically the idea is to trade Bollinger Bands expansions (long to the upside, short to the downside) and fade or stay out of contractions.

There are three key moving averages in the strategy - LONG MA, SHORT MA, BASIC MA. Long and Short MAs are guides to eyes on the chart and also act as possible trend filters (adjustable in settings). Basic MA acts as guide to eye and a possible trade trigger (adjustable in settings).

There are a few trend filters the strategy can use - moving average, signed standard deviation, ultimate RSI or none. The filters act as an additional condition on triggers, making the strategy take trades only if both triggers and trend filter allows. That way one can filter out trades with unfavorable risk/reward (for instance, don't long if price is under the MA200). Different trade filters can be used for long and short trades.

The strategy employs various stop loss types, the default of which is a trailing %-based stop loss type. ATR-based stop loss is also available. The default 1.5% trailing stop loss is suitable for leveraged trading.

Lastly, the strategy can trigger take profit orders if certain conditions are met, adjustable in settings. Also, it can hold onto winning trades and exit only after stop out (in which case, consecutive triggers to take other positions will be ignored until stop out).

Let me know if you like it and if you use it, what kind of tweaks would you like to see.

With kind regards,

easy-peasy-x

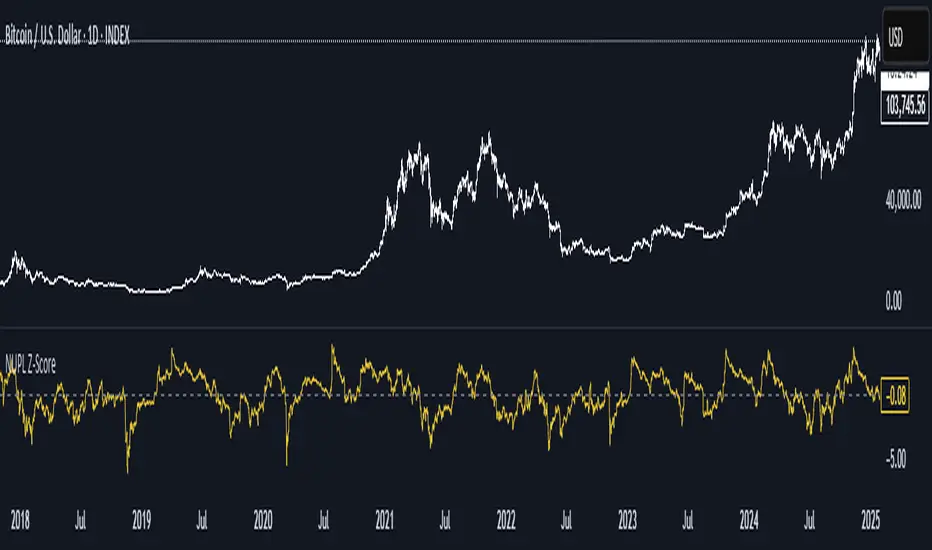

NUPL Z-ScoreThis indicator is derived from Market Value and Realized Value, which can be defined as:

Market Value: The current price of Bitcoin multiplied by the number of coins in circulation. This is like market cap in traditional markets i.e. share price multiplied by number of shares.

Realized Value: Rather than taking the current price of Bitcoin, Realized Value takes the price of each Bitcoin when it was last moved i.e. the last time it was sent from one wallet to another wallet. It then adds up all those individual prices and takes an average of them. It then multiplies that average price by the total number of coins in circulation.

By subtracting Realized Value from Market Value we calculate Unrealized Profit/Loss.

Unrealized Profit/Loss estimates the total paper profits/losses in Bitcoin held by investors. This is interesting to know but of greater value is identifying how this changes relatively over time.

To do this we can divide Unrealized Profit/Loss by Market Cap. This creates Net Unrealized Profit/Loss, sometimes referred to as NUPL, which is very useful to track investor sentiment over time for Bitcoin.

Relative Unrealised Profit/Loss is another name used for this analysis.

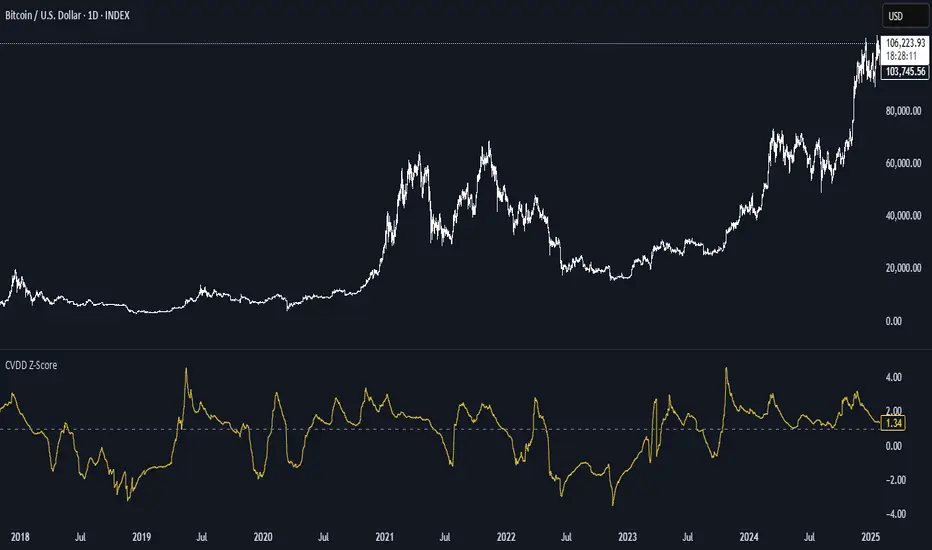

CVDD Z-ScoreCVDD stands for Cumulative Value Coin Days Destroyed.

Coin Days Destroyed is a term used for bitcoin to identify a value of sorts to UTXO’s (unspent transaction outputs). You can learn more about UTXO’s here. They can be thought of as coins moving between wallets.

int this script you have the option to change the Z-Score length.

Supply In Profit Z-ScoreZ-score of BTC Supply in Profit.

Supply in Profit is an On-Chain BTC indicator that shows the percentage of BTC in profit.

In this indicator you can choose to use a Z-Score or not.

BTC Thermocap Z-ScoreBTC Thermocap Indicator Overview

The BTC Thermocap is a specialized on-chain ratio indicator designed to provide deeper insight into Bitcoin's market valuation relative to its cumulative issuance. By comparing the current market price of Bitcoin to the total value of all BTC ever mined (also known as "thermocap"), this indicator helps identify potential overvaluation or undervaluation periods within the Bitcoin market cycle.

Key Features and Customizable Inputs:

Moving Average Length (MA Length)

Moving Average Type (MA Type) - SMA or EMA

Z-Score Calculation Length

Z-Score Toggle (Use Z-Score)

Mitsos4 RSI + BB + Dispersion + Trendlines + VIX Fix Mitsos4 RSI + BB + Dispersion + Trendlines + VIX Fix

This powerful custom indicator combines two analytical tools into one view:

RSI-based Bollinger Bands with Dispersion and the Vix Fix volatility spike detector.

It is designed for traders who want early volatility signals and precision RSI insights, all in a single pane.

🧩 What's Included:

✅ 1. RSI + BB (EMA) + Dispersion

RSI-Based Bollinger Bands: Tracks the RSI with Bollinger Bands using an EMA as the basis.

Dispersion Zone: A buffer zone around the moving average band for more sensitive overbought/oversold detection.

Dynamic RSI Coloring:

🟢 Green: RSI breaks above the dispersion zone.

🔴 Red: RSI breaks below the dispersion zone.

🟡 Yellow: RSI inside the zone (neutral).

Trendlines at RSI levels: 40 (green), 50 (yellow), 60 (red).

Alerts when RSI crosses dispersion zones.

✅ 2. CM_Williams_Vix_Fix

Designed to simulate VIX-like volatility spikes on non-VIX instruments.

Detects potential market bottoms by measuring price deviation from recent highs.

Includes:

Bollinger Band range on WVF.

Percentile high/low zones to detect significant volatility moves.

Histogram plot of WVF for quick visual alerts.

Color-coded spikes (green when above upper thresholds).

⚙️ User Controls:

Adjustable RSI, Bollinger Band, and dispersion settings.

Toggle options for:

Viewing high/low VIX percentiles.

Showing standard deviation bands for WVF.

Custom trendline display levels at RSI key areas.

📌 Best Use Cases:

Detect early market reversals and volatility spikes.

Combine RSI strength with volatility-based bottom signals.

Layer dispersion-based logic on top of classic RSI strategies.

MACD + RSI + EMA + BB + ATR Day Trading StrategyEntry Conditions and Signals

The strategy implements a multi-layered filtering approach to entry conditions, requiring alignment across technical indicators, timeframes, and market conditions .

Long Entry Requirements

Trend Filter: Fast EMA (9) must be above Slow EMA (21), price must be above Fast EMA, and higher timeframe must confirm uptrend

MACD Signal: MACD line crosses above signal line, indicating increasing bullish momentum

RSI Condition: RSI below 70 (not overbought) but above 40 (showing momentum)

Volume & Volatility: Current volume exceeds 1.2x 20-period average and ATR shows sufficient market movement

Time Filter: Trading occurs during optimal hours (9:30-11:30 AM ET) when market volatility is typically highest

Exit Strategies

The strategy employs multiple exit mechanisms to adapt to changing market conditions and protect profits :

Stop Loss Management

Initial Stop: Placed at 2.0x ATR from entry price, adapting to current market volatility

Trailing Stop: 1.5x ATR trailing stop that moves up (for longs) or down (for shorts) as price moves favorably

Time-Based Exits: All positions closed by end of trading day (4:00 PM ET) to avoid overnight risk

Best Practices for Implementation

Settings

Chart Setup: 5-minute timeframe for execution with 15-minute chart for trend confirmation

Session Times: Focus on 9:30-11:30 AM ET trading for highest volatility and opportunity

Average RSI (Daily + Weekly)📈 Average RSI (Relative Strength Index) – Beginner’s Guide

What it is:

The Average RSI is a technical indicator that combines multiple RSI values—such as daily and weekly RSI—into a single, smoothed line. This helps traders get a clearer picture of a stock’s momentum over both short- and medium-term timeframes.

Why it matters:

The RSI tells you whether a stock is potentially overbought (priced too high and due for a pullback) or oversold (priced too low and due for a bounce). Traditional RSI uses a scale from 0 to 100, with key levels at 70 (overbought) and 30 (oversold).

By averaging RSI across different timeframes, you reduce noise and get a better signal for trends and reversals.

How traders use it:

✅ Buy zone: When the average RSI dips below 40, it could signal a good entry point.

⚠️ Neutral zone: Between 40 and 60 means the trend isn’t strong—wait for more confirmation.

🚫 Sell zone: Above 60–70 may indicate the asset is overbought or due for a pullback.

Helpful for:

Spotting better entry/exit points

Filtering out false signals

Staying in trend-following trades longer

My scriptImplied Volatility vs Historical Volatility

**Uncheck Plot box**

IV > HV = Overvalued

IV = HV = Fair Value

IV > HV = Undervalued

1. Pair with IV Rank: Use IV vs HV to confirm the setup, but IV Rank (50+, 70+) tells you how “high” IV is relative to its own history.

2. Timeframe: Use daily charts — IV is not meaningful on intraday timeframes.

3. Avoid noise: Use a smoothed HV (e.g., 20-day) and don’t chase small crossovers — look for clear divergence.

RSI SwingRadar🧠 Strategy Overview

This long-only strategy combines RSI/MA crossovers with ATR-based risk management, designed for cleaner entries during potential bounce phases — especially tuned for assets like XMR/USDT.

🔍 Core Logic:

- RSI Crossover: Entry occurs when the 14-period RSI crosses above its 14-period SMA, signaling a potential shift in momentum.

- Oversold Filter: The RSI must have been below a user-defined oversold threshold (default: 35) on the previous candle, filtering for bounce setups after a pullback.

- ATR-Based Stop/Target: Stop-loss is placed below the low by a user-adjustable ATR multiplier (default: 0.5×). Take-profit is calculated with a Risk:Reward multiplier (default: 4×).

These elements work in tandem — RSI crossovers give momentum confirmation, oversold filtering adds context, and ATR-based exits adapt to volatility, creating a compact yet responsive strategy.

📉 Visuals:

- Dynamic Bands: The chart displays the active stop-loss, entry price, and take-profit as colored bands for easy visual tracking.

- Clean Overlay: Designed with simplicity — only confirmed setups are shown, keeping noise low.

✅ Suggested Use:

- Works best on XMR/USDT or similarly trending assets.

- Best suited for pullback entries during broader uptrends.

- Adjustable for different volatility conditions and asset behaviors.

⚠️ Disclaimer

- This strategy is for educational and research purposes only.

- It does not guarantee profitability in any market.

- Always backtest, forward-test, and understand your own risk tolerance before using any

strategy in a live environment.

- Past performance is not indicative of future results.

- This script is not financial advice.

Sri_Momentum Burst Histogram📝 Description :

🌀 Sri_Momentum Burst Histogram — A Custom Momentum and Volatility Fusion Tool

The Sri_Momentum Burst Histogram is a unique technical analysis tool designed to visualize sudden changes in price momentum in the form of a dynamic, color-coded histogram. This indicator helps traders identify trend accelerations, early momentum shifts, and potential exhaustion in real time.

By combining a MACD-like momentum engine with a volatility-sensitive Bollinger Band range, this script offers an enhanced view of market bursts — moments where momentum "pops" beyond typical ranges. The result is a refined perspective on market sentiment, helping traders to anticipate reversals, follow breakouts, and assess the relative strength of ongoing trends.

🧠 Core Methodology

The indicator calculates the difference between a fast and slow EMA (Exponential Moving Average), similar to a MACD histogram.

This difference is then compared across candles to gauge the rate of change in momentum — referred to here as a “momentum burst.”

A sensitivity multiplier allows you to scale the response based on your preferred timeframe and trading style.

A volatility band, derived from Bollinger Band logic, is used to frame the relative intensity of the momentum change.

The histogram is divided into two parts:

Green/Lime Bars represent increasing and decreasing bullish momentum.

Red/Orange Bars represent increasing and decreasing bearish momentum.

⚙️ Customizable Inputs

Momentum Sensitivity: Adjust the responsiveness of the burst detection mechanism.

Short EMA Period: Sets the lookback period for the fast EMA.

Long EMA Period: Sets the lookback period for the slow EMA.

Volatility Band Length: Controls the length used for Bollinger Band calculations.

Band Std Dev Multiplier: Adjusts how wide the volatility range should be, based on price dispersion.

📈 How to Use It

Use the green/red histogram bars to visually gauge momentum strength and direction.

Watch for transitions in color intensity (e.g., green to lime, red to orange) as early warning signs of trend exhaustion or reversal.

Combine with other indicators like RSI, MACD, ADX, or volume profiles to confirm entry/exit points.

Useful in both trending and ranging markets, especially on lower timeframes for scalping or intraday setups.

✅ Key Features

Easy-to-read histogram with intuitive color coding.

Fully customizable settings for fine-tuned signal control.

Can be used on any asset class — stocks, forex, crypto, commodities.

Optimized for real-time use with minimal lag.

🔐 This script is an original creation, developed independently by adapting publicly known mathematical concepts into a unique visualization tool. All function and variable names have been customized for originality and compliance with TradingView’s publishing and community standards.

💡 Developed by: @venkat_27

🧩 For educational purposes only — not financial advice.

Custom Paul MACD-likePaul MACD is an indicator created by David Paul. It is implemented to effectively represent trend periods and non-trend (sideways/consolidation) periods, and its calculation method is particularly designed to reduce whipsaw.

Unlike the existing MACD which uses the difference between short-term (12) and long-term (26) exponential moving averages (EMA), Paul MACD has a different calculation method. This indicator uses a "center value" or "intermediate value". Calculation occurs when this intermediate value is higher than the High value (specifically, the difference between the center and High is calculated) or lower than the Low value (specifically, the difference between the center and Low is calculated). Otherwise, the value becomes 0. Here, the High and Low values are intended to be smoothly reflected using Smoothed Moving Average (SMMA). The indicator's method itself (using SMMA and ZLMA) is aimed at diluting whipsaws.

Thanks to this calculation method, in sections where whipsaw occurs, meaning when the intermediate value is between High and Low, the indicator value is expressed as 0 and appears as a horizontal line (zero line). This serves to visually clearly show sideways/consolidation periods.

RSI.TrendContext

The Relative Strength Index (RSI) is one of the most widely used classical indicators in technical analysis, typically employed to identify overbought or oversold market conditions. It reflects the degree of upside or downside dominance within a specified period. However, in its standard form, RSI is not particularly effective as a standalone entry trigger.

The RSI.Trend indicator enhances the RSI to provide a more reliable method for distinguishing between bullish and bearish market regimes and offers specific entry triggers. It adds supplementary value to the pure RSI read.________________________________________

Concept

In trending markets, an Exponential Moving Average (EMA) of the price is often smoother and more stable than raw price data. As a result, the RSI calculated on this smoothed price (i.e., the EMA) tends to react earlier and more consistently than the standard RSI. Specifically:

• In uptrends, the RSI of the EMA tends to exceed the RSI of the original price.

• In downtrends, it tends to lag behind.

The difference between these two RSI readings provides a stable and less noisy measure of market bias—positive in uptrends, negative in downtrends. The crossing points can serve as entry triggers. This is, what the RSI.Trend is trying to capture.

________________________________________

The RSI.Trend indicator operates as follows:

• It first computes the 5-period EMA of the price series of the underlying ("EMA5").

• It calculates the 14-period RSI of the original price series ("RSI") as well as the 14-period RSI of EMA5 ("RSIEMA").

• It then determines the 14-period EMA of RSI ("RSI.MA") and RSIEMA ("RSIEMA.MA").

These values are used to define a Baseline and a Trigger Line:

• Baseline: The average of RSI and RSI.MA.

• Trigger Line: The average of RSIEMA and RSIEMA.MA.

Essentially, the baseline represents a smoother version of the RSI of the original price series, while the trigger line is a smoother version of the RSI on the EMA5 of the original price series.

Additionally, the RSI.Trend Background Value is calculated as the difference between the Trigger Line and the Baseline, slightly accelerated by incorporating the current bias of this difference. This acceleration causes the Background Value to react somewhat faster than the pure difference between the two lines.

How to use the RSI.Trend:

• As mentioned in the introductory context, during uptrends, the trigger line remains above the baseline; in downtrends, it stays below the baseline.

• A crossover of the baseline by the trigger line indicates a regime shift from bearish to bullish and can signal avoiding adding short positions, closing short positions, or adding long positions.

• A crossunder of the baseline by the trigger line indicates a regime shift from bullish to bearish and can signal avoiding adding long positions, closing long positions, or adding short positions.

• The level of the Trigger Line can serve as a confidence indicator; for instance, if the trigger line crosses under the baseline coming from very high values, it implies high confidence.

• The Background Value indicates the accelerated difference between the two lines:

o > 0 (Green background): Indicates a Bullish regime.

o < 0 (Red background): Indicates a Bearish regime.

The Background Value reacts slightly faster than line crossings due to its acceleration relative to the difference of the two lines.

Including these lines in the script besides the Background Value, provides insight into their levels and their origins, aiding in formulating confidence in an entry trigger, which the background value alone cannot provide. The change in slope of the trigger Line can also be used as an early and fast position-trigger.

Finally, the Background Value can be utilized in continuous trading scenarios (i.e., no entry points, always engaged) as a multiplier on a predefined max-exposure value, representing the current exposure as a fraction of that max-exposure.

The usage of RSI.Trend is also exemplified in the introductory chart.________________________________________

Final Notes

As with all indicators, the RSI.Trend is most effective when used in conjunction with other technical tools and market context. It does not predict future price movements; rather, it reflects current market dynamics and recent directional tendencies. Use it with discretion and as part of a broader trading strategy.

RSI Crossover Signal Companion - Alerts + Visuals🔷 RSI Crossover Signal Companion — Alerts + Visuals

The Relative Strength Index (RSI) is a momentum oscillator that measures the speed and change of recent price movements. It helps traders identify overbought or oversold conditions, possible trend reversals, and momentum strength.

This utility builds on TradingView’s classic Relative Strength Index (RSI) by adding real-time alerts and triangle markers when the RSI crosses its own moving average — a common technique for early momentum detection.

It is designed as a lightweight, visual companion tool for traders using RSI/MA crossover logic in manual or semi-automated strategies.

🔍 Features

✅ Preserves the full original RSI layout, including:

• Gradient fill and overbought/oversold zones

• Standard RSI input settings (length, source, etc.)

• MA smoothing options with user-defined type and length

🔺 Adds visual triangle markers:

🔼 Up triangle when RSI crosses above its MA

🔽 Down triangle when RSI crosses below its MA

📢 Built-in alerts for RSI/MA crosses:

“RSI Crossed Above MA”

“RSI Crossed Below MA”

📈 How to Use

This script is ideal for:

• Spotting early momentum shifts

• Confirming entries or exits in other systems (price action, trendlines, breakouts)

• Building alert-based automation (webhooks, bots, etc.)

Popular use cases:

• Combine with trend indicators like MA200 or MA12

• Use in confluence with price structure and divergence

• Validate breakout moves with momentum confirmation

⚙️ Customization

RSI length, MA length, MA type, and source are fully adjustable

Triangle marker size, shape, and color can be edited under Style

Alerts are pre-built and ready for use