Well Rounded Moving AverageIntroduction

There are tons of filters, way to many, and some of them are redundant in the sense they produce the same results as others. The task to find an optimal filter is still a big challenge among technical analysis and engineering, a good filter is the Kalman filter who is one of the more precise filters out there. The optimal filter theorem state that : The optimal estimator has the form of a linear observer , this in short mean that an optimal filter must use measurements of the inputs and outputs, and this is what does the Kalman filter. I have tried myself to Kalman filters with more or less success as well as understanding optimality by studying Linear–quadratic–Gaussian control, i failed to get a complete understanding of those subjects but today i present a moving average filter (WRMA) constructed with all the knowledge i have in control theory and who aim to provide a very well response to market price, this mean low lag for fast decision timing and low overshoots for better precision.

Construction

An good filter must use information about its output, this is what exponential smoothing is about, simple exponential smoothing (EMA) is close to a simple moving average and can be defined as :

output = output(1) + α(input - output(1))

where α (alpha) is a smoothing constant, typically equal to 2/(Period+1) for the EMA.

This approach can be further developed by introducing more smoothing constants and output control (See double/triple exponential smoothing - alpha-beta filter) .

The moving average i propose will use only one smoothing constant, and is described as follow :

a = nz(a ) + alpha*nz(A )

b = nz(b ) + alpha*nz(B )

y = ema(a + b,p1)

A = src - y

B = src - ema(y,p2)

The filter is divided into two components a and b (more terms can add more control/effects if chosen well) , a adjust itself to the output error and is responsive while b is independent of the output and is mainly smoother, adding those components together create an output y , A is the output error and B is the error of an exponential moving average.

Comparison

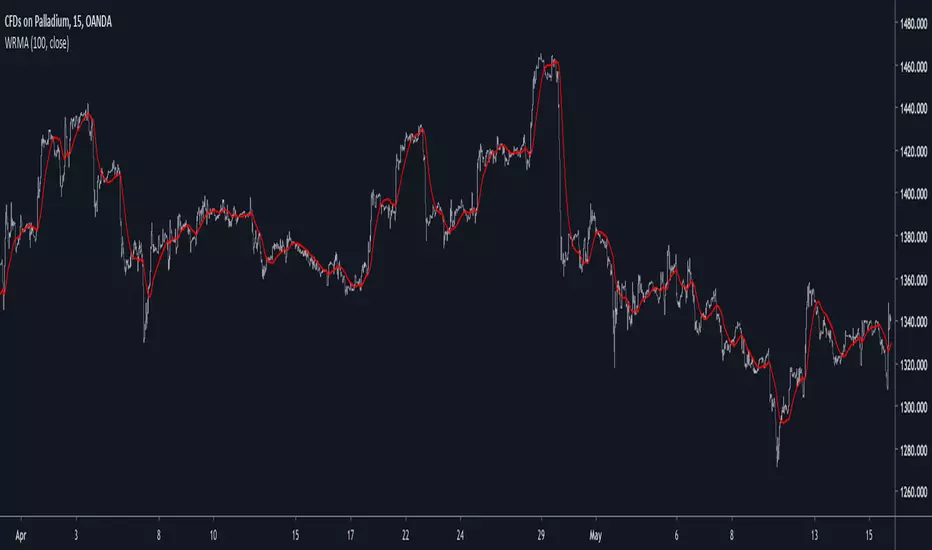

There are a lot of low-lag filters out there, but the overshoots they induce in order to reduce lag is not a great effect. The first comparison is with a least square moving average, a moving average who fit a line in a price window of period length .

Lsma in blue and WRMA in red with both length = 100 . The lsma is a bit smoother but induce terrible overshoots

ZLMA in blue and WRMA in red with both length = 100 . The lag difference between each moving average is really low while VWRMA is way more precise.

Hull MA in blue and WRMA in red with both length = 100 . The Hull MA have similar overshoots than the LSMA.

Reduced overshoots moving average (ROMA) in blue and WRMA in red with both length = 100 . ROMA is an indicator i have made to reduce the overshoots of a LSMA, but at the end WRMA still reduce way more the overshoots while being smoother and having similar lag.

I have added a smoother version, just activate the extra smooth option in the indicator settings window. Here the result with length = 200 :

This result is a little bit similar to a 2 order Butterworth filter. Our filter have more overshoots which in this case could be useful to reduce the error with edges since other low pass filters tend to smooth their amplitude thus reducing edge estimation precision.

Conclusions

I have presented a well rounded filter in term of smoothness/stability and reactivity. Try to add more terms to have different results, you could maybe end up with interesting results, if its the case share them with the community :)

As for control theory i have seen neural networks integrated to Kalman flters which leaded to great accuracy, AI is everywhere and promise to be a game a changer in real time data smoothing. So i asked myself if it was possible for a neural networks to develop pinescript indicators, if yes then i could be replaced by AI ? Brrr how frightening.

Thanks for reading :)

Overshoot

Least Squares Moving Average With Overshoot ReductionIntroduction

The ability to reduce lag while keeping a good level of stability has been a major challenge for smoothing filters in technical analysis. Stability involve many parameters, one of them being overshoots. Overshoots are a common effect induced by low-lagging filters, they are defined as the ability of a signal output to exceed a target input. This effect can lead to major drawbacks such as whipsaw and reduction of precision. I propose a modification of the least squares moving average "Reduced Overshoots Moving Average" (ROMA) to reduce overshoots induced by the lsma by using a scaled recursive dispersion coefficient with the purpose of reducing overshoots.

Overshoots - Causes and Effects

Control theory and electronic engineering use step response to measure overshoots, the target signal is defined as an heaviside step function which will be used as input signal for our filter.

In white an input signal, in blue a least squares moving average with the input signal as source, the circle show the overshoot induced by the lsma, the filter exceed drastically the target input. But why low lag filters often induce overshoots ? This is because in order to reduce lag those filter will increase certain frequencies of the input signal, this reduce lag but induce overshoots because the amplitude of those frequencies have been increased, so its normal for the filter to exceed the input target. The increase of frequencies is not a bad process but when those frequencies are already of large amplitudes (high volatility periods) the overshoots can be seen.

Comparison With ROMA

Our method will use the line rescaling technique to estimate the lsma for efficiency sake. This method involve calculating the z-score of a line and multiplying it by the correlation of the line and the target input (price). Then we rescale this result by adding this z-score multiplied by the dispersion coefficient to a simple moving average. Lets compare the step response of our filer and the lsma.

ROMA (in red) need more data to be computed but reduce the mean absolute error in comparison with the classic lsma, it is seen that instead of following increasing, ROMA decrease thus ending with an undershoot.

ROMA in (red) and an lsma (in blue) with both length = 14, ROMA decrease overshoots with the cost of less smoothing, both filter match when there are no overshoots situations.

Both filters with length = 200, large periods increase the amplitude of overshoots, ROMA stabilize early at the cost of some smoothness.

The running Mean Absolute Error of both filters with length = 100, ROMA (in red) is on average closer to the price than the lsma (in blue)

Conclusion

I presented a modification of the least squares moving average with the goal to provide both stability and rapidity, the statistics show that ROMA do a better job when it comes to reduce the mean absolute error. Alternatives methods can involve decreasing the period it take for the filter to be on a steady state (reducing filter period during high volatility periods) , various filters already exploit this method.

Side Project

I'am not that good when it come to make my post easy to read, this is why i'am currently making an article explaining the basis of digital signal processing. This post will help you to understand signals and things such as lag, frequency transform, cycles, overshoots, ringing, FIR/IIR filters, impulse response, convolution, filter topology and many more. I love to post indicators but also making more educational content as well, so stay tuned :)

Thanks for reading, let me know if you need help with something, i would be happy to assist you.

please be kind to notify me if you find errors about the indicator in order for me to update it as fast as possible.