No Gaps - JizzanyNo Gaps – Jizzany

Fill the blanks. Own the patterns.

Don’t let thin futures feeds or blazing-fast 1 s bars break your flow—this overlay stitches every missing pixel back into your chart so you can:

🔍 Analyze low-liquidity markets (futures, exotic FX, crypto alt-pairs) without awkward jumps

⏱️ Trade ultra-low timeframes (1 s, tick charts) with full confidence in every wick

📈 Spot price patterns seamlessly, even when your broker’s feed skips a beat

How it works: Auto-detects gaps between sessions or feeds, then draws miniature candles from the prior close to the current open—using real intrabar highs/lows—so nothing ever goes unseen.

Perfect for scalpers, day traders, and anyone who demands continuity in every bar. Try it on your next chart and rediscover the story in every candle.

Turn This

Into This

This

Into

Pine utilities

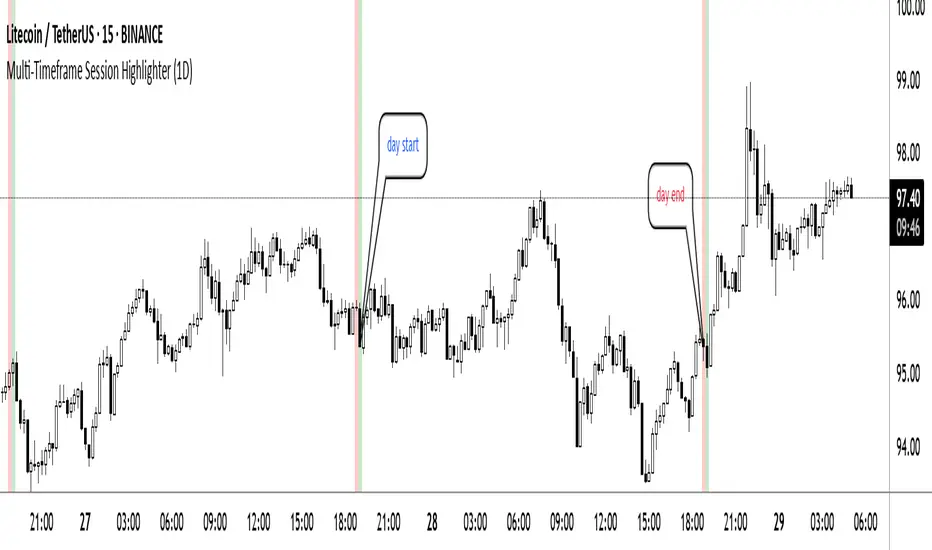

Multi-Timeframe Session HighlighterWhat is the Multi-Timeframe Session Highlighter?

It’s a simple Pine Script indicator that paints two special candles on your chart, no matter what timeframe you’re looking at. Think of it as a highlighter pen for session starts and ends—can be used for session-based strategies or just keeping an eye on key turning points.

How it works:

Green Bar (Session Open): Marks the exact bar when your chosen higher-timeframe session kicks off. If you select “4H,” on the indicator, you’ll see green on every 4-hour open, even if you’re staring at a 15-minute chart.

Red Bar (Session Close): Highlights the very last lower-timeframe candle immediately before that session wraps up. So on a 1H chart with “Daily” selected, you’ll get a red band on the 23:00 hour before the new daily bar at midnight.

Customizable: Pick your own colors and transparency level to match your chart theme.

Getting started:

Add the indicator to your chart.

In the inputs, select the session timeframe (for example, “240” for 4H or “D” for daily).

Choose your favorite green and red shades.

That’s it.

Killzones (UTC+3) by Roy⏰ Time-Based Division – Trading Quarters:

The trading day is divided into four main quarters, each reflecting distinct market behaviours:

Opo Finance Blog

Quarter Time (Israel Time) Description

Q1 16:30–18:30 Wall Street opening; highest volatility.

Q2 18:30–20:30 Continuation or correction of the opening move.

Q3 20:30–22:30 Quieter market; often characterized by consolidation.

Q4 22:30–24:00 Preparation for market close; potential breakouts or sharp movements.

This framework assists traders in anticipating market dynamics within each quarter, enhancing decision-making by aligning strategies with typical intraday patterns.

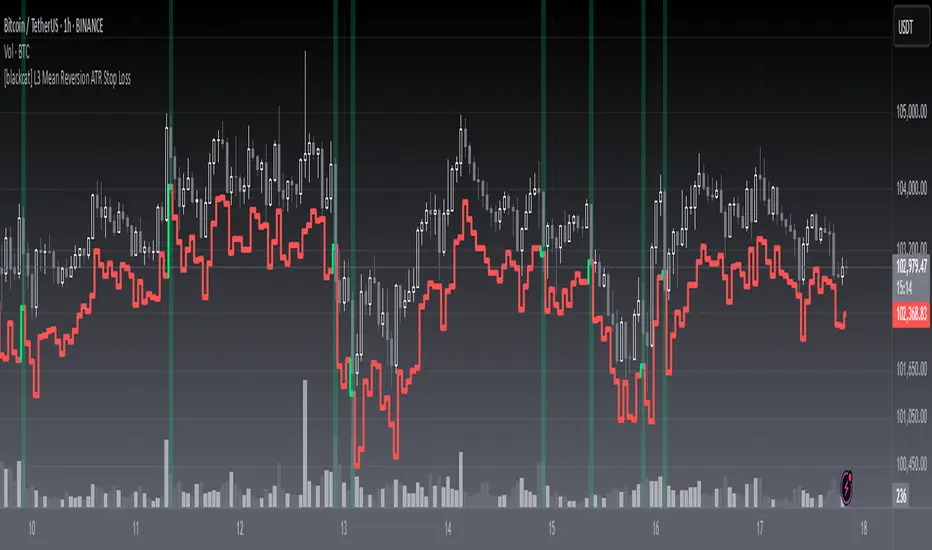

[blackcat] L3 Mean Reversion ATR Stop Loss OVERVIEW

The L3 Mean Reversion ATR Stop Loss indicator is meticulously crafted to empower traders by offering statistically-driven stop-loss levels that adapt seamlessly to evolving market dynamics. By harmoniously blending mean reversion concepts with Advanced True Range (ATR) metrics, it delivers a robust framework for managing risks more effectively. 🌐 The primary objective is to furnish traders with intelligent exit points grounded in both short-term volatility assessments and long-term trend evaluations.

Key highlights encompass:

• Dynamic calculation of Z-scores to evaluate deviations from established means

• Adaptive stop-loss pricing leveraging real-time ATR measurements

• Clear visual cues enabling swift decision-making processes

TECHNICAL ANALYSIS COMPONENTS

📉 Z-SCORE CALCULATION

Measures how many standard deviations an asset's current price lies away from its average

Facilitates identification of extreme conditions indicative of impending reversals

Utilizes simple moving averages and standard deviation computations

📊 STANDARD DEVIATION MEASUREMENT

Quantifies dispersion of closing prices around the mean

Provides insights into underlying price distribution characteristics

Crucial for assessing potential volatility levels accurately

🕵️♂️ ADAPTIVE STOP-LOSS DETECTION

Employs ATR as a proxy for prevailing market volatility

Modulates stop-loss placements dynamically responding to shifting trends

Ensures consistent adherence to predetermined risk management protocols

INDICATOR FUNCTIONALITY

🔢 Core Algorithms

Integrate Smooth Moving Averages (SMAs) alongside standardized deviation formulas

Generate precise Z-scores reflecting true price deviations

Leverage ATR-derived multipliers for fine-grained stop-loss adjustments

🖱️ User Interface Elements

Interactive plots displaying real-time stop-loss markers

Context-sensitive color coding enhancing readability

Background shading indicating proximity to stop-level activations

STRATEGY IMPLEMENTATION

✅ Entry Conditions

Confirm bullish/bearish setups validated through multiple confirmatory signals

Ensure alignment between Z-score readings and broader trend directions

Validate entry decisions considering concurrent market sentiment factors

🚫 Exit Mechanisms

Trigger exits upon hitting predefined ATR-based stop-loss thresholds

Monitor continuous breaches signifying potential trend reversals

Execute partial/total closes contingent upon cumulative loss limits

PARAMETER CONFIGURATIONS

🎯 Optimization Guidelines

Period Length: Governs responsiveness versus smoothing trade-offs

ATR Length: Dictates the temporal scope for volatility analysis

Stop Loss ATR Multiplier: Tunes sensitivity towards stop-trigger activations

💬 Customization Recommendations

Commence with baseline defaults; iteratively refine parameters

Evaluate impacts independently prior to combined adjustments

Prioritize minimizing erroneous trigger occurrences first

Sustain balanced risk-reward profiles irrespective of chosen settings

ADVANCED RISK MANAGEMENT

🛡️ Proactive Risk Mitigation Techniques

Enforce strict compliance with pre-defined maximum leverage constraints

Mandatorily apply trailing stop-loss orders conforming to script outputs

Allocate positions proportionately relative to available capital reserves

Conduct periodic reviews gauging strategy effectiveness rigorously

⚠️ Potential Pitfalls & Solutions

Address frequent violations arising during heightened volatility phases

Manage false alerts warranting manual interventions judiciously

Prepare contingency plans mitigating margin call possibilities

Continuously assess automated system reliability amidst fluctuating conditions

PERFORMANCE AUDITS & REFINEMENTS

🔍 Critical Evaluation Metrics

Assess win percentages consistently across diverse trading instruments

Calculate average profit ratios per successful execution

Measure peak drawdown durations alongside associated magnitudes

Analyze signal generation frequencies revealing hidden patterns

📈 Historical Data Analysis Tools

Maintain comprehensive records capturing every triggered event

Compare realized profits/losses against backtested simulations

Identify recurrent systematic errors demanding corrective actions

Implement iterative refinements bolstering overall efficacy steadily

PROBLEM SOLVING ADVICE

🔧 Frequent Encountered Challenges

Unpredictable behaviors emerging within thinly traded markets

Latency issues manifesting during abrupt price fluctuations

Overfitted models yielding suboptimal results post-extensive tuning

Inaccuracies stemming from incomplete or delayed data inputs

💡 Effective Resolution Pathways

Exclude low-liquidity assets prone to erratic movements

Introduce buffer intervals safeguarding major news/event impacts

Limit ongoing optimization attempts preventing model degradation

Verify seamless connectivity ensuring uninterrupted data flows

USER ENGAGEMENT SEGMENT

🤝 Community Contributions Welcome

Highly encourage active participation sharing experiences & recommendations!

THANKS

A heartfelt acknowledgment extends to all developers contributing invaluable insights about adaptive stop-loss strategies using statistical measures! ✨

PORTFOLIO TABLE Full [Titans_Invest]PORTFOLIO TABLE Full

This is a complete table for monitoring your assets or cryptocurrencies in your SPOT wallet without needing to access your broker’s website or app.

⯁ HOW TO USE THIS TABLE❓

Simply select the asset and enter the amount you hold.

The table will display the value of each asset and the total value of your portfolio.

You can monitor up to 19 assets in real time.

⯁ CONVERT VALUES

You can also enable and select a currency for conversion.

For example, cryptocurrencies are calculated in US dollars by default, but you can choose euros as the conversion currency.

The values originally in dollars will then be displayed in euros.

⯁ TRACK THE DAILY VARIATION OF YOUR PORTFOLIO

You’ll be able to monitor your portfolio’s raw daily variation in real time.

🔶 Track your Portfolio in real time:

🔶 Add your local Currency to Convert Values:

🔶 Follow your Portfolio Live:

___________________________________________________________

📜 SCRIPT : PORTFOLIO TABLE Full

🎴 Art by : @Titans_Invest & @DiFlip

👨💻 Dev by : @Titans_Invest & @DiFlip

🎑 Titans Invest — The Wizards Without Gloves 🧤

✨ Enjoy!

___________________________________________________________

o Mission 🗺

• Inspire Traders to manifest Magic in the Market.

o Vision 𐓏

• To elevate collective Energy 𐓷𐓏

EMA Validation4 EMA with Support/Resistance Validation (EMA-V)

This indicator displays four Exponential Moving Averages (EMAs) with customizable periods (default: 21, 50, 100, 200) and visually validates their roles as support or resistance.

Each EMA changes color based on its behavior: green for respected support , red for respected resistance, or default colors when unvalidated.

Ideal for traders seeking to identify reliable support and resistance levels across multiple timeframes.

ATR Volatility giua64ATR Volatility giua64 – Smart Signal + VIX Filter

📘 Script Explanation (in English)

Title: ATR Volatility giua64 – Smart Signal + VIX Filter

This script analyzes market volatility using the Average True Range (ATR) and compares it to its moving average to determine whether volatility is HIGH, MEDIUM, or LOW.

It includes:

✅ Custom or preset configurations for different asset classes (Forex, Indices, Gold, etc.).

✅ An optional external volatility index input (like the VIX) to refine directional bias.

✅ A directional signal (LONG, SHORT, FLAT) based on ATR strength, direction, and external volatility conditions.

✅ A clean visual table showing key values such as ATR, ATR average, ATR %, VIX level, current range, extended range, and final signal.

This tool is ideal for traders looking to:

Monitor the intensity of price movements

Filter trading strategies based on volatility conditions

Identify momentum acceleration or exhaustion

⚙️ Settings Guide

Here’s a breakdown of the user inputs:

🔹 ATR Settings

Setting Description

ATR Length Number of periods for ATR calculation (default: 14)

ATR Smoothing Type of moving average used (RMA, SMA, EMA, WMA)

ATR Average Length Period for the ATR moving average baseline

🔹 Asset Class Preset

Choose between:

Manual – Define your own point multiplier and thresholds

Forex (Pips) – Auto-set for FX markets (high precision)

Indices (0.1 Points) – For index instruments like DAX or S&P

Gold (USD) – Preset suitable for XAU/USD

If Manual is selected, configure:

Setting Description

Points Multiplier Multiplies raw price ranges into useful units (e.g., 10 for Gold)

Low Volatility Threshold Threshold to define "LOW" volatility

High Volatility Threshold Threshold to define "HIGH" volatility

🔹 Extended Range and VIX

Setting Description

Timeframe for Extended High/Low Used to compare larger price ranges (e.g., Daily or Weekly)

External Volatility Index (VIX) Symbol for a volatility index like "VIX" or "EUVI"

Low VIX Threshold Below this level, VIX is considered "low" (default: 20)

High VIX Threshold Above this level, VIX is considered "high" (default: 30)

🔹 Table Display

Setting Description

Table Position Where the visual table appears on the chart (e.g., bottom_center, top_left)

Show ATR Line on Chart Whether to display the ATR line directly on the chart

✅ Signal Logic Summary

The script determines the final signal based on:

ATR being above or below its average

ATR rising or falling

ATR percentage being significant (>2%)

VIX being high or low

Conditions Signal

ATR rising + high volatility + low VIX LONG

ATR falling + high volatility + high VIX SHORT

ATR flat or low volatility or low %ATR FLAT

Apex Edge - MTF Confluence PanelApex Edge – MTF Confluence Panel

Description:

The Apex Edge – MTF Confluence Panel is a powerful multi-timeframe analysis tool built to streamline trade decision-making by aggregating key confluences across three user-defined timeframes. The panel visually presents the state of five core market signals—Trend, Momentum, Sweep, Structure, and Trap—alongside a unified Score column that summarizes directional bias with clarity.

Traders can customize the number of bullish/bearish conditions required to trigger a score signal, allowing the tool to be tailored for both conservative and aggressive trading styles. This script is designed for those who value a clean, structured, and objective approach to identifying market alignment—whether scalping or swing trading.

How it Works:

Across each of the three selected timeframes, the panel evaluates:

Trend: Based on a user-configurable Hull Moving Average (HMA), the script compares price relative to trend to determine bullish, bearish, or neutral bias.

Momentum: Uses OBV (On-Balance Volume) with volume spike detection to identify bursts of strong buying or selling pressure.

Sweep: Detects potential liquidity grabs by identifying price rejections beyond prior swing highs/lows. A break below a previous low with reversal signals bullish intent (and vice versa for bearish).

Structure: Uses dynamic pivot-based logic to identify market structure breaks (BOS) beyond recent confirmed swing levels.

Trap: Flags potential false moves by measuring RSI overbought/oversold signal clusters combined with minimal price movement—highlighting exhaustion or deceptive breaks.

Score: A weighted consensus of the above components. The number of required confluences to trigger a score (default: 3) can be set by the user via input, offering flexibility in signal sensitivity.

Why It’s Useful for Traders:

Quick Decision-Making: The color-coded panel provides instant visual feedback on whether confluences align across timeframes—ideal for fast-paced environments like scalping or high-volatility news sessions.

Multi-Timeframe Confidence: Helps eliminate guesswork by confirming whether higher and lower timeframe conditions support your trade idea.

Customizability: Adjustable confluence threshold means traders can fine-tune how sensitive the system is—more signals for faster entries, stricter confluence for higher conviction trades.

Built-In Alerts: Automated alerts for score alignment, trap detection, and liquidity sweeps allow traders to stay informed even when away from the screen.

Strategic Edge: Supports directional bias confirmation and trade filtering with logic designed to mimic professional decision-making workflows.

Features:

Clean, real-time confluence table across three user-selected timeframes

Configurable score sensitivity via “Minimum Confluences for Score” input

Cell-based colour coding for at-a-glance trade direction

Built-in alerts for score alignment, traps, and sweep triggers

Note - This Indicator works great in sync with Apex Edge - Session Sweep Pro

Useful levels for TP = previous session high/low boxes or fib levels.

⚠️ Disclaimer:

This script is for informational and educational purposes only and should not be considered financial advice. Always perform your own due diligence and practice proper risk management when trading.

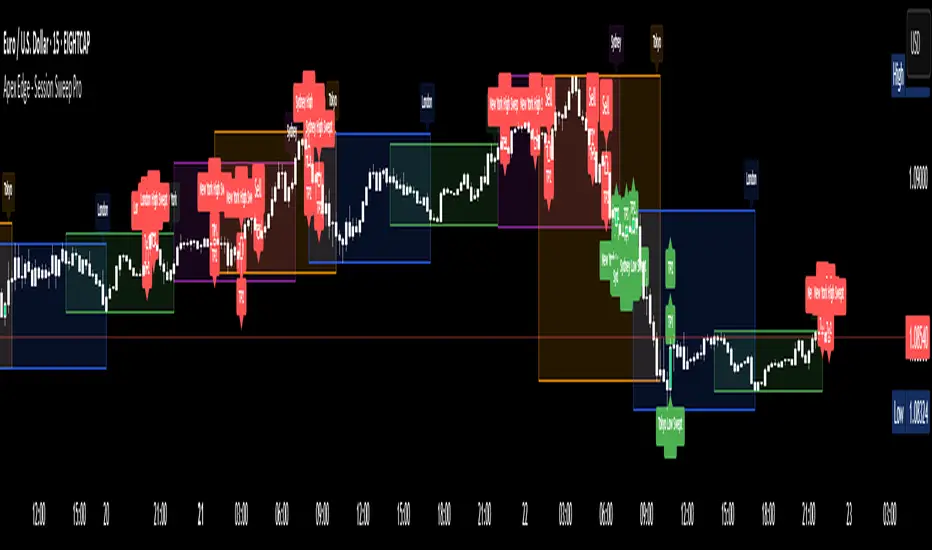

Apex Edge - Session Sweep ProApex Edge Session Sweep Pro

By Apex Edge | 2025 Edition

🔍 What is it?

The Apex Session Sweep Pro is a precision trading tool designed for identifying high-probability liquidity sweep entries during key global market sessions. It combines powerful sweep detection logic with dynamic candle colouring, session visualization, TP projections, and real-time alerts — all within a clean, performance-optimized Pine Script engine.

This is not your average session box indicator. This is Apex-grade.

⚙️ How it Works

The indicator detects session liquidity sweeps by tracking price action relative to previous session highs and lows. When a session high/low is swept (i.e., price breaches it and then closes in the opposite direction), it generates a signal:

Buy Signal → Price sweeps previous low and closes back above it

Sell Signal → Price sweeps previous high and closes back below it

Each session is boxed on the chart (Tokyo, London, New York, Sydney), color-coded, and dynamically labelled.

Upon detecting a valid sweep, the script:

Plots a small entry label (toggleable)

Projects up to 5 customizable TP levels

Coloured candles for visual trade direction

Alerts for Buy or Sell sweep signals (optional)

All elements are memory-managed and customizable to suit your trading style.

🧠 Key Features

✅ Smart Sweep Detection Logic

✅ Global Market Session Boxes (Custom Times)

✅ Toggleable Entry Labels + TP Levels

✅ Candle Colouring by Signal

✅ Manual TP input + TP toggles

✅ Real-time Alerts for Apex entries

🕒 Why Are My Sessions Offset?

Your chart’s time zone may be different from UTC. This script is UTC-based by design, so if your chart is set to UTC+1, for example, the sessions will appear one hour later. Either:

Adjust your chart to UTC or or Exchange for perfect alignment,

Or tweak the session input times manually.

🧰 Who is this for?

This tool is made for:

Intraday traders looking for sweeps into liquidity

SMC (Smart Money Concept) strategists

Forex, crypto, and indices traders

Anyone who uses session-based levels to define entries

Whether you scalp London or ride NY swings, this tool frames each session cleanly — and shows you where the traps are laid.

🚨 Disclaimer

This indicator is a technical tool, not financial advice. Use proper risk management. Past performance ≠ future results.

Apex Edge – Super RSIThe Apex Edge – Super RSI is not your average RSI. This is an institutional-grade signal engine designed for serious traders who want confluence, control, and confidence — all wrapped into one visual powerhouse.

━━━━━━━━━━━━━━━━━━━━

KEY FEATURES

━━━━━━━━━━━━━━━━━━━━

✔ **RSI + Divergence Engine**

• Classic & Hidden Divergences (auto-detected)

• Labelled with shapes:

▲ Green Triangle – Buy Signal (strength-based size)

▼ Red Triangle – Sell Signal

◆ Green Diamond – Classic Bullish Divergence

◆ Red Diamond – Classic Bearish Divergence

● Green Circle – Hidden Bullish Divergence

● Red Circle – Hidden Bearish Divergence

Note - Users can edit symbol colours in settings for better clarity

✔ **Trap Detection System**

• Detects low-move, high-signal clusters (liquidity traps)

• Automatically suppresses signals for X bars after detection

• Trap zones shown with shaded background (optional)

✔ **Signal Scoring Logic**

• Each signal is scored 1–6 based on:

• RSI Threshold Break

• RSI Slope

• Divergence Detected

• Trap Avoidance

• Multi-Timeframe Confluence (optional)

• The plotted shape size reflects the strength of the entry signal

✔ **Multi-Timeframe Confluence (MTF)**

• Optional filter that uses HTF and VHTF RSI alignment

• Prevents countertrend signals

• MTF Bias shown on HUD panel

✔ **Always-On HUD Panel**

• Displays:

• Signal Type

• Signal Score

• Divergence Type

• RSI (LTF & HTF)

• Trap & Cooldown Status

• MTF Bias

• Volatility %

✔ **Alert Ready**

• Buy/Sell alerts

• Trap Detected alert

• Divergence alert with dynamic message

• Perfect for webhook integrations

━━━━━━━━━━━━━━━━━━━━

📘 HOW TO TRADE IT

━━━━━━━━━━━━━━━━━━━━

✅ **Buy Setup**

• Green triangle (▲) appears **below bar**

• RSI is oversold and rising

• HTF RSI agrees (optional)

• Signal score is 3+ for best confidence

• Avoid signals during cooldown zone

✅ **Sell Setup**

• Red triangle (▼) appears **above bar**

• RSI is overbought and falling

• HTF RSI agrees (optional)

• Signal score is 3+ for best confidence

✅ **Divergences**

• Use diamonds/circles to identify momentum shifts

• Strongest when aligned with score 4–6

❗**Trap Zones**

• When background is shaded, wait for cooldown

• Signals during traps are suppressed for safety

━━━━━━━━━━━━━━━━━━━━

📊 BEST USED WITH

━━━━━━━━━━━━━━━━━━━━

🔹 Apex Edge – Session Sweep Pro (to visualize liquidity levels)

🔹 Volume Profile or OBV (volume-based confirmation)

🔹 EMA Ribbon (for trend alignment)

🔹 Fair Value Gap indicator (smart money models)

━━━━━━━━━━━━━━━━━━━━

🧠 PRO TIPS

━━━━━━━━━━━━━━━━━━━━

• Use the HUD for decision confidence — if everything aligns, you’ve got an Apex-grade setup.

• Wait for candle close to confirm divergence-based entries.

• Score 5–6 = sniper entries. Score 1–2 = warning shots.

This indicator can be used alongside Apex Edge Session Sweep Pro for better visual clarity.

━━━━━━━━━━━━━━━━━━━━

© Apex Edge | All rights reserved.

3 days ago

Release Notes

Update - Added a toggle to show/hide HUD when using on smaller mobile devices so as not to clutter the screen.

Kaito Box with RSI Div(Dynamic Adjustment + MA + Long)The script implements a dynamic trading strategy that combines box range detection, RSI divergence signals, and moving average trend analysis. It is designed for use on OKX Signal Bots and includes features for dynamic position scaling and partial position closing. Below is a summary of its key functionalities:

Key Features:

Box Range Detection:

The script identifies price ranges using the highest high and lowest low of a configurable boxLength period.

These levels are plotted on the chart to visualize the price range.

RSI Divergence Detection:

The script calculates RSI using a configurable rsiLength.

Detects bullish divergence when price makes a lower low, but RSI makes a higher low.

Detects bearish divergence when price makes a higher high, but RSI makes a lower high.

Includes separate left and right lookback periods (leftLookback, rightLookback) for precise local extrema detection.

Customizable Moving Averages:

Supports multiple types of Moving Averages (SMA, EMA, SMMA, WMA, VWMA).

Calculates and plots MA20, MA50, MA100, and MA200 on a user-defined timeframe (custom_timeframe).

Identifies uptrends and downtrends based on the alignment of the moving averages and price levels.

Dynamic Position Scaling:

Implements dynamic position sizing for long entries and partial position closing for exits.

The percentage of position size added or closed is based on the difference between the current price and the average position price (avgPrice), with configurable minimum thresholds (minEnterPercent, minExitPercent).

Signal Integration for OKX Bots:

Sends buy/sell signals to OKX Signal Bots using the configured signalToken.

Supports market or limit orders with configurable price offsets and investment types.

Trend-Based Signal Filtering:

Only triggers long signals during downtrends and short signals during uptrends, ensuring trades align with the overall market context.

Visual Annotations:

Plots bullish and bearish divergence signals on the chart.

Displays labels showing dynamic position size adjustments and current average price during trades.

How It Works:

Long Signals:

Triggered when the price breaches the lower box range, and a bullish RSI divergence is detected.

Additional filtering ensures long trades are executed only during downtrend conditions.

Dynamically adjusts the position size based on the price difference from the average entry price.

Short Signals:

Triggered when the price breaches the upper box range, and a bearish RSI divergence is detected.

Additional filtering ensures short trades are executed only during uptrend conditions.

Dynamically closes portions of the position based on price movement relative to the average entry price.

Alerts:

Generates actionable alerts formatted for OKX bots, including order type, signal token, and dynamically calculated position sizes.

Use Case:

This strategy is well-suited for automated trading on platforms like OKX, where it can:

Exploit price ranges and RSI divergences for precise entries and exits.

Dynamically manage position sizes to optimize risk-reward.

Adapt to different market conditions using configurable parameters like moving averages, divergence lookbacks, and trend filters.

This script provides a robust foundation for traders looking to automate their strategies while maintaining flexibility and control over their trading logic.

PORTFOLIO TABLE Simple [Titans_Invest]PORTFOLIO TABLE Simple

This is a simple table for you to monitor your assets or cryptocurrencies in your SPOT wallet without needing to access your broker’s website or wallet app.

⯁ HOW TO USE THIS TABLE❓

You only need to select the asset and enter the amount of each one.

The table will show how much you have of each asset and the total value of your portfolio.

You’ll be able to monitor up to 39 assets in real time.

⯁ CONVERT VALUES

You can also activate and select a currency for conversion.

For example, cryptocurrency assets are calculated in US dollars, but you can select euros as the conversion currency.

The values originally in dollars will then be displayed in euros.

⯁ Track your Portfolio in real time:

⯁ Add your local Currency to Convert Values:

⯁ Follow your Portfolio Live:

___________________________________________________________

📜 SCRIPT : PORTFOLIO TABLE Simple

🎴 Art by : @Titans_Invest & @DiFlip

👨💻 Dev by : @Titans_Invest & @DiFlip

🎑 Titans Invest — The Wizards Without Gloves 🧤

✨ Enjoy!

___________________________________________________________

o Mission 🗺

• Inspire Traders to manifest Magic in the Market.

o Vision 𐓏

• To elevate collective Energy 𐓷𐓏

ETH to RTH Gap DetectorETH to RTH Gap Detector

What It Does

This indicator identifies and tracks custom-defined gaps that form between Extended Trading Hours (ETH) and Regular Trading Hours (RTH). Unlike traditional gap definitions, this indicator uses a specialized approach - defining up gaps as the space between previous session close high to current session initial balance low, and down gaps as the space from previous session close low to current session initial balance high. Each detected gap is monitored until it's touched by price.

Key Features

Detects custom-defined ETH-RTH gaps based on previous session close and current session initial balance

Automatically identifies both up gaps and down gaps

Visualizes gaps with color-coded boxes that extend until touched

Tracks when gaps are filled (when price touches the gap area)

Offers multiple display options for filled gaps (color change, border only, pattern, or delete)

Provides comprehensive statistics including total gaps, up/down ratio, and touched gap percentage

Includes customizable alert system for real-time gap filling notifications

Features toggle options for dashboard visibility and weekend sessions

Uses time-based box coordinates to avoid common TradingView drawing limitations

How To Use It

Configure Session Times : Set your preferred RTH hours and timezone (default 9:30-16:00 America/New York)

Set Initial Balance Period : Adjust the initial balance period (default 30 minutes) for gap detection sensitivity

Monitor Gap Formation : The indicator automatically detects gaps between the previous session close and current session IB

Watch For Gap Fills : Gaps change appearance or disappear when price touches them, based on your selected style

Check Statistics : View the dashboard to see total gaps, directional distribution, and touched percentage

Set Alerts : Enable alerts to receive notifications when gaps are filled

Settings Guide

RTH Settings : Configure the start/end times and timezone for Regular Trading Hours

Initial Balance Period : Controls how many minutes after market open to calculate the initial balance (1-240 minutes)

Display Settings : Toggle gap boxes, extension behavior, and dashboard visibility

Filled Box Style : Choose how filled gaps appear - Filled (color change), Border Only, Pattern, or Delete

Color Settings : Customize colors for up gaps, down gaps, and filled gaps

Alert Settings : Control when and how alerts are triggered for gap fills

Weekend Session Toggle : Option to include or exclude weekend trading sessions

Technical Details

The indicator uses time-based coordinates (xloc.bar_time) to prevent "bar index too far" errors

Gap boxes are intelligently limited to avoid TradingView's 500-bar drawing limitation

Box creation and fill detection use proper range intersection logic for accuracy

Session detection is handled using TradingView's session string format for reliability

Initial balance detection is precisely calculated based on time difference

Statistics calculations exclude zero-division scenarios for stability

This indicator works best on futures markets with extended and regular trading hours, especially indices (ES, NQ, RTY) and commodities. Performs well on timeframes from 1-minute to 1-hour.

What Makes It Different

Most gap indicators focus on traditional open-to-previous-close gaps, but this tool offers a specialized definition more relevant to ETH/RTH transitions. By using the initial balance period to define gap edges, it captures meaningful price discrepancies that often provide trading opportunities. The indicator combines sophisticated gap detection logic with clean visualization and comprehensive tracking statistics. The customizable fill styles and integrated alert system make it practical for both chart analysis and active trading scenarios.

weighted support or resistance linesQ: Why should users choose this script?

A: I found that in all the publicly available scripts about support and resistance lines, there is basically no weight identification for these lines. In other words, users do not know which support or resistance lines are the most important. So I specifically wrote this script.

1. By adjusting the weights, only the most effective support or resistance lines are displayed. (Length threshold of trend price (Bar))

2. By selecting the number of K-lines, only the latest number of support or resistance lines generated will be displayed. (Maximum number of reserved S/R lines)

3. By selecting whether to automatically remove lines, only support or resistance lines that have not been penetrated by the k-line will be displayed. If this function is checked, the weight can be adjusted lower, as high-weight SR may have already been penetrated, and the newly generated SR may have a lower weight. (Automatically remove lines penetrated by closing price confirmation)

4. Notes: The default parameters work well in 15-minute candlestick charts. For candlestick charts with other time periods, the parameters can be adjusted appropriately. It is suitable for sideways trading but not for strong trends.

5. I'm quite satisfied with the performance of the script, as I specifically optimized it, lol

30-70 RSI Strategy with Colored BarThis script colors price bars based on Relative Strength Index (RSI) levels, giving traders a quick and visual way to assess overbought or oversold market conditions directly on the chart.

📈 Key Features:

✅ RSI-Based Bar Coloring:

Green bars when RSI is above the upper threshold (default 70) – suggests bullish momentum.

Red bars when RSI is below the lower threshold (default 30) – indicates bearish pressure.

Bars remain uncolored when RSI is between thresholds – a neutral zone.

🔧 Customizable RSI Settings:

Adjustable RSI length (default: 14 periods)

Adjustable overbought/oversold levels (default: 70/30)

🧠 Helps traders:

Quickly spot potential reversals or trend continuations

Visually align price action with momentum

🛠️ Usage:

Ideal for trend-following, reversal, and momentum strategies.

Works across any timeframe (1m, 5m, 1h, daily, etc.).

nineLivesUtilLibLibrary "nineLivesUtilLib"

isDateInRange(currentTime, useTimeFilter, startDate, endDate)

Checks if the current time is within the specified date range.

Parameters:

currentTime (int) : The current bar's time (time).

useTimeFilter (bool) : Bool 📅: Enable the date range filter.

startDate (int) : Timestamp 📅: The start date for the filter.

endDate (int) : Timestamp 📅: The end date for the filter.

Returns: True if the current time is within the range or filtering is disabled, false otherwise.

@example

inDateRange = nineLivesUtilLib.isDateInRange(time, useTimeFilter, startDate, endDate)

if inDateRange

// Execute trading logic

checkVolumeCondition(currentVolume, useVolumeFilter, volumeThresholdMultiplier, volumeLength)

Checks if the current volume meets the threshold condition.

Parameters:

currentVolume (float) : The current bar's volume (volume).

useVolumeFilter (bool) : Bool 📊: Enable the volume filter.

volumeThresholdMultiplier (float) : Float 📊: Volume threshold relative to average (e.g., 1.5 for 1.5x average).

volumeLength (int) : Int 📊: Lookback length for the volume average.

Returns: True if the volume condition is met or filtering is disabled, false otherwise.

@example

volumeOk = nineLivesUtilLib.checkVolumeCondition(volume, useVolumeFilter, volumeThreshold, volumeLength)

if volumeOk

// Proceed with trading logic

checkMultiTimeframeCondition(currentClose, currentOpen, htfClose, htfOpen, useMultiTimeframe, alignment)

Checks alignment with higher timeframe direction.

Parameters:

currentClose (float) : Float: The current bar's closing price (close).

currentOpen (float) : Float: The current bar's opening price (open).

htfClose (float) : Float: The closing price from the higher timeframe (must be fetched by the calling script using request.security).

htfOpen (float) : Float: The opening price from the higher timeframe (must be fetched by the calling script using request.security).

useMultiTimeframe (bool) : Bool ⏱️: Enable multi-timeframe analysis.

alignment (string) : String ⏱️: Desired alignment ("same", "opposite", "any").

Returns: True if the timeframe alignment condition is met or analysis is disabled, false otherwise.

@example

// In the calling script:

= request.security(syminfo.tickerid, higherTimeframe, )

tfOk = nineLivesUtilLib.checkMultiTimeframeCondition(close, open, htfClose, htfOpen, useMultiTimeframe, tfAlignment)

if tfOk

// Proceed with trading logic

checkMarketRegime(useMarketRegime, regimeIndicator, regimeThreshold, regimeLength, regimeMode)

Detects the market regime (trending or ranging) and checks if trading is allowed.

Parameters:

useMarketRegime (bool) : Bool 🔍: Enable market regime detection.

regimeIndicator (string) : String 🔍: Indicator to use ("ADX" or "Volatility").

regimeThreshold (int) : Int 🔍: Threshold for trend strength/volatility.

regimeLength (simple int) : Int 🔍: Lookback length for the indicator.

regimeMode (string) : String 🔍: Trading mode based on regime ("trend_only", "range_only", "adaptive").

Returns: A tuple containing:

: conditionMet (bool) - True if trading is allowed based on the regime mode and detection, false otherwise.

: inTrendingRegime (bool) - True if the current regime is trending based on the indicator and threshold.

@example

= nineLivesUtilLib.checkMarketRegime(useMarketRegime, regimeIndicator, regimeThreshold, regimeLength, regimeMode)

if regimeOk

// Proceed with trading logic

applyCooldown(buySignal, sellSignal, cooldownBars)

Applies a cooldown period after a signal.

Parameters:

buySignal (bool) : Bool: Buy signal (potentially after primary entry logic).

sellSignal (bool) : Bool: Sell signal (potentially after primary entry logic).

cooldownBars (int) : Int ⏳: The number of bars to wait after a signal before allowing another.

Returns: A tuple containing:

: cooldownFilteredBuy (bool) - Buy signal after cooldown filter.

: cooldownFilteredSell (bool) - Sell signal after cooldown filter.

@example

= nineLivesUtilLib.applyCooldown(rawBuySignal, rawSellSignal, iCool)

applyAllFilters(rawBuy, rawSell, inDateRange, tradeDirection, volumeOk, tfOk, regimeOk, drawdownOk, cooldownOkBuy, cooldownOkSell)

Applies all filtering conditions to the buy and sell signals.

Parameters:

rawBuy (bool) : Bool: The initial buy signal candidate (from primary entry logic, e.g., after cooldown).

rawSell (bool) : Bool: The initial sell signal candidate (from primary entry logic, e.g., after cooldown).

inDateRange (bool) : Bool 📅: Result from isDateInRange.

tradeDirection (string) : String 🔄: Overall trade direction preference ("longs_only", "shorts_only", "both").

volumeOk (bool) : Bool 📊: Result from checkVolumeCondition.

tfOk (bool) : Bool ⏱️: Result from checkMultiTimeframeCondition.

regimeOk (bool) : Bool 🔍: Result from checkMarketRegime.

drawdownOk (bool) : Bool 📉: Result from checkDrawdownExceeded (or equivalent).

cooldownOkBuy (bool) : Bool ⏳: Result from applyCooldown for buy.

cooldownOkSell (bool) : Bool ⏳: Result from applyCooldown for sell.

Returns: A tuple containing:

: finalBuySignal (bool) - The final buy signal after all filters.

: finalSellSignal (bool) - The final sell signal after all filters.

@example

= nineLivesUtilLib.applyAllFilters(cooldownBuy, cooldownSell, inDateRange, tradeDirection, volumeOk, tfOk, regimeOk, !drawdownExceeded, cooldownBuy, cooldownSell)

NOTE: This function filters signals generated by your primary entry logic (e.g., EMA crossover).

checkDrawdownExceeded(currentEquity, useMaxDrawdown, maxDrawdownPercent)

Tracks maximum equity and checks if current drawdown exceeds a threshold.

Parameters:

currentEquity (float) : Float: The strategy's current equity (strategy.equity).

useMaxDrawdown (bool) : Bool 📉: Enable max drawdown protection.

maxDrawdownPercent (float) : Float 📉: The maximum allowed drawdown as a percentage.

Returns: True if drawdown protection is enabled and the current drawdown exceeds the threshold, false otherwise.

@example

drawdownExceeded = nineLivesUtilLib.checkDrawdownExceeded(strategy.equity, useMaxDrawdown, maxDrawdownPercent)

if drawdownExceeded

// Consider stopping entries or exiting positions in the strategy script

calculateExitPrice(positionAvgPrice, percentage, isStop, isLong)

Calculates a stop loss or take profit price based on a percentage from the average entry price.

Parameters:

positionAvgPrice (float) : Float: The average price of the current position (strategy.position_avg_price).

percentage (float) : Float: The stop loss or take profit percentage (e.g., 2.0 for 2%).

isStop (bool) : Bool: True if calculating a stop loss price, false if calculating a take profit price.

isLong (bool) : Bool: True if the position is long, false if short.

Returns: The calculated stop price or take profit price, or na if no position or percentage is invalid.

@example

longSL = nineLivesUtilLib.calculateExitPrice(strategy.position_avg_price, stopLossPercent, true, true)

shortTP = nineLivesUtilLib.calculateExitPrice(strategy.position_avg_price, takeProfitPercent, false, false)

calculateTrailingStopLevel(positionAvgPrice, trailOffsetPercent, trailPercent, currentHigh, currentLow, isLong)

Calculates the current trailing stop level for a position.

Parameters:

positionAvgPrice (float) : Float: The average price of the current position (strategy.position_avg_price).

trailOffsetPercent (float) : Float 🔄: The percentage price movement to activate the trailing stop.

trailPercent (float) : Float 🔄: The percentage distance the stop trails behind the price.

currentHigh (float) : Float: The current bar's high (high).

currentLow (float) : Float: The current bar's low (low).

isLong (bool) : Bool: True if the position is long, false if short.

Returns: The calculated trailing stop price if active, otherwise na.

@example

longTrailStop = nineLivesUtilLib.calculateTrailingStopLevel(strategy.position_avg_price, trailOffset, trailPercent, high, low, true)

shortTrailStop = nineLivesUtilLib.calculateTrailingStopLevel(strategy.position_avg_price, trailOffset, trailPercent, high, low, false)

if not na(longTrailStop)

strategy.exit("Long Trail", from_entry="Long", stop=longTrailStop)

Custom Time Session Background (Amsterdam Time, DST Safe)This indicator highlights two custom intraday time ranges with background colors on your chart. The times are set based on your local Amsterdam time and automatically adjust for Daylight Saving Time (DST).

📌 Features:

- Define two separate time ranges (Start & End) in local Amsterdam time

- Background color highlighting for each range

- Fully DST-aware using the "Europe/Amsterdam" timezone

- Works across all intraday timeframes

🎯 Use Cases:

- Highlight key market sessions (e.g., EU open, NY overlap)

- Visually segment your trading hours

- Eliminate manual DST adjustments

Developed with Pine Script v5.

Made for traders who want clarity during specific time zones, without worrying about time shifts across the year.

Bar Count for XAUThis TradingView indicator labels every other five-minute candle for XAU during the current Beijing session, which runs from 06:00 to 05:00 the next day. It shows the actual bar numbers—1, 3, 5, and so on—only for today’s session; yesterday’s labels are automatically cleared at the new open. The tags appear just below each qualifying candle with no background box, and you can adjust the font size in the settings. In short, it gives you a clean, real-time visual of intraday bar order without clutter

Overnight ES Strategy: CBC + Fractal + RSI + ATR FilterThis script is designed for overnight trading of the E-mini S&P 500 futures (ES) between 6 PM and 11 PM EST.

It combines multiple technical confluences to generate high-probability buy and sell signals, focusing on volatility-rich, low-liquidity evening sessions.

Key Features:

Candle Body Confluence (CBC) Approximation:

Identifies candles with small real bodies compared to total range, simulating consolidation zones where price is likely to reverse.

Williams Fractal Confirmation:

Detects local tops and bottoms based on 5-bar fractal reversal patterns, helping validate breakout or reversal points.

RSI Filter:

Ensures momentum is supportive — buys only when RSI < 35 (oversold) and sells only when RSI > 65 (overbought).

ATR Volatility Filter:

Trades are only allowed if the Average True Range (ATR) exceeds a user-defined threshold, filtering out low-volatility, risky environments.

Time Session Control:

Signals are only generated during the user-defined evening session (default: 6 PM to 11 PM EST) to match market behavior.

Real-Time Alerts Enabled:

Alerts can be set for BUY or SELL conditions, enabling mobile notifications, emails, or pop-ups without constant chart monitoring.

Recommended Settings:

Chart Timeframe: 15-minute or 30-minute candles

Assets: ES Mini (ES1!), NQ Mini, or other CME futures

Session: New York Time (EST)

ATR Threshold: Adjust based on market conditions; 5.0 suggested starting point for ES Mini on 15m.

Important:

This script only plots signals, it does not auto-execute trades.

Always backtest and paper trade before using live capital.

Volatility can vary; consider adjusting RSI and ATR filters based on market environment.

Credits:

Script designed based on confluence of price action, momentum, reversal structure, and volatility filtering principles used by professional traders.

Inspired by Candle Body Confluence (CBC) theory and Williams fractal techniques.

RSI + MACD + Liquidity FinderLiquidity Finder: The liquidity zones are heuristic and based on volume and swing points. You may need to tweak the volumeThreshold and lookback to match the asset's volatility and timeframe.

Timeframe: This script works on any timeframe, but signals may vary in reliability (e.g., higher timeframes like 4H or 1D may reduce noise).

Customization: You can modify signal conditions (e.g., require only RSI or MACD) or add filters like trend direction using moving averages.

Backtesting: Use TradingView's strategy tester to evaluate performance by converting the indicator to a strategy (replace plotshape with strategy.entry/strategy.close).

Sweep Reversal 5M PRO – by [TuNombre]🔹 **Sweep Reversal 5M PRO – by ** 🔹

This indicator is built to detect high-probability *Institutional Sweeps* using Swing Failure Patterns (SFP), fully filtered with Smart Money Concepts (SMC) logic and volume confirmation.

✅ Identifies key liquidity grabs

✅ Confirms with strong impulse candle + increasing volume

✅ Filters out false signals (doji, weak zones, low volume)

✅ Optimized for the 5-minute timeframe (5M)

✅ Compatible with push alerts to your mobile

---

**How to use it:**

1. Wait for a “BUY” or “SELL” signal on the chart

2. Only enter if the next candle confirms with momentum

3. Place a tight stop just beyond the sweep

4. Recommended Take Profit: 1:1 minimum / 2:1 ideal

---

💡 Inspired by institutional trading (SMC, ICT-style setups)

🔒 Developed by – private or team-based use

📲 Activate alerts to get real-time trade opportunities on your phone

---

⚠️ This script does not repaint.

Built for serious traders who want precision, not noise.

The Hebrew CalendarThis indicator displays the current Hebrew (Jewish) calendar date based on the real-time Gregorian calendar. Features included:

Calculates and displays the current Hebrew day, month, and year.

Recognizes leap years and adjusts month counts accordingly.

Aligns with traditional Hebrew month names (Tishrei, Cheshvan, Kislev, etc.).

The calculations align with the Hebrew Calendar Converter from:

👉 www.chabad.org

The results are shown in a table overlay on your chart's top-right corner. This indicator is great for symbolic traders, astro enthusiasts, or anyone interested in ancient timekeeping systems woven into financial timeframes. Enjoy, time travelers! ⌛

The Mayan CalendarThis indicator displays the current date in the Mayan Calendar, based on real-time UTC time. It calculates and presents:

🌀 Long Count (Baktun.Katun.Tun.Uinal.Kin) – A linear count of days since the Mayan epoch (August 11, 3114 BCE).

🔮 Tzolk'in Date – A 260-day sacred cycle combining a number (1–13) and one of 20 day names (e.g., 4 Ajaw).

🌾 Haab' Date – A 365-day civil cycle divided into 18 months of 20 days + 5 "nameless" days (Wayeb').

The calculations follow Smithsonian standards and align with the Maya Calendar Converter from the National Museum of the American Indian:

👉 maya.nmai.si.edu

The results are shown in a table overlay on your chart's top-right corner. This indicator is great for symbolic traders, astro enthusiasts, or anyone interested in ancient timekeeping systems woven into financial timeframes. Enjoy, time travelers! ⌛