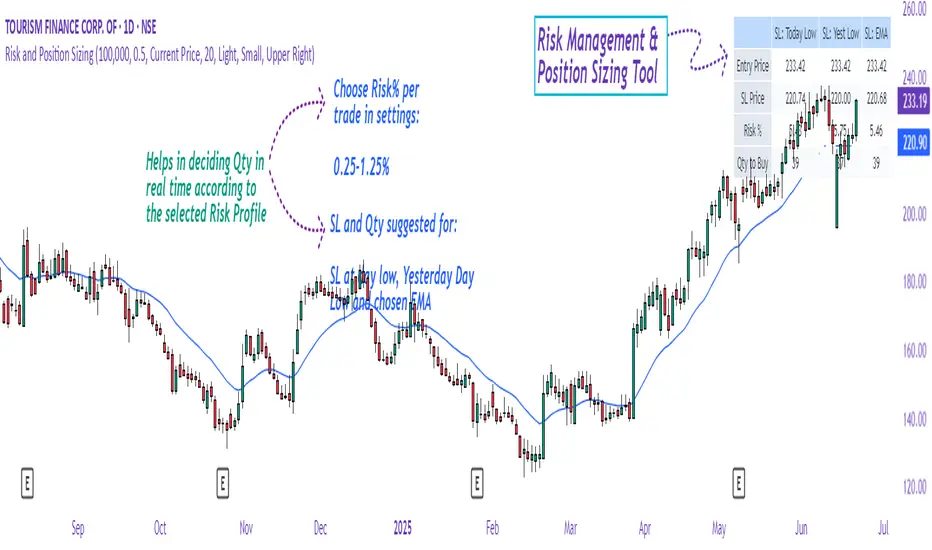

Risk and Position Sizing📏 Why Position Size Should Be Based on Risk?

Let’s say you are ready to lose 1,000 in a trade. Based on your stop loss level, you can calculate how many shares (or quantity) to buy, so that if the stop hits, you only lose that ₹1,000.

This is called risk-based position sizing. It makes your trade size dynamic — small when SL is wide, bigger when SL is tight. No more random position sizes — just systematic.

Portfolio size is multiplied by the selected risk % to get money risk per trade.

This amount is then used to calculate how many shares can be bought for the given stop-loss.

So chose your portfolio size in settings. Default Portfolio size is 1,00,000 .

You can select your risk % per portfolio in the settings — for example:

0.25% for conservative style

0.5% to 1% for balanced traders

1.25% or 1.5% for aggressive ones (not recommended for beginners)

This script will automatically calculate how much quantity you should buy, for each stop-loss scenario.

📈 Progressive & Inverse-Progressive Risk Styles

Some traders follow progressive position sizing — they start with small risk when the trend is just starting, and increase the risk % as the trend confirms.

Others follow inverse-progressive sizing — they take high risk at early stages of a bull market, and reduce risk as the trend matures (when upside becomes limited).

📌 This script allows you to manually control the risk % in settings, so you can adjust it based on your trading phase and style.

📋 Three SL Scenarios – Choose What Matches Your Style

The table shows three different stop-loss conditions, and for each one it calculates:

Today’s Low – tightest stop loss

Yesterday’s Low – slightly safer, ideal for short-term swing trades

EMA Stop (configurable) – gives more breathing room.

You can visually compare all 3 in the table and choose whichever fits your strategy and comfort.

Also, you can customize:

Theme: dark or light

Font size

Table position (upper/lower corners)

🧠 Designed for traders who take risk management seriously.

Let this script handle the math. You focus on execution.

Happy Trading!

– LensOfChartist

Portfolio management

SIP Evaluator and Screener [Trendoscope®]The SIP Evaluator and Screener is a Pine Script indicator designed for TradingView to calculate and visualize Systematic Investment Plan (SIP) returns across multiple investment instruments. It is tailored for use in TradingView's screener, enabling users to evaluate SIP performance for various assets efficiently.

🎲 How SIP Works

A Systematic Investment Plan (SIP) is an investment strategy where a fixed amount is invested at regular intervals (e.g., monthly or weekly) into a financial instrument, such as stocks, mutual funds, or ETFs. The goal is to build wealth over time by leveraging the power of compounding and mitigating the impact of market volatility through disciplined, consistent investing. Here’s a breakdown of how SIPs function:

Regular Investments : In an SIP, an investor commits to investing a fixed sum at predefined intervals, regardless of market conditions. This consistency helps inculcate a habit of saving and investing.

Cost Averaging : By investing a fixed amount regularly, investors purchase more units when prices are low and fewer units when prices are high. This approach, known as dollar-cost averaging, reduces the average cost per unit over time and mitigates the risk of investing a large amount at a peak price.

Compounding Benefits : Returns generated from the invested amount (e.g., capital gains or dividends) are reinvested, leading to exponential growth over the long term. The longer the investment horizon, the greater the potential for compounding to amplify returns.

Dividend Reinvestment : In some SIPs, dividends received from the underlying asset can be reinvested to purchase additional units, further enhancing returns. Taxes on dividends, if applicable, may reduce the reinvested amount.

Flexibility and Accessibility : SIPs allow investors to start with small amounts, making them accessible to a wide range of individuals. They also offer flexibility in terms of investment frequency and the ability to adjust or pause contributions.

In the context of the SIP Evaluator and Screener , the script simulates an SIP by calculating the number of units purchased with each fixed investment, factoring in commissions, dividends, taxes and the chosen price reference (e.g., open, close, or average prices). It tracks the cumulative investment, equity value, and dividends over time, providing a clear picture of how an SIP would perform for a given instrument. This helps users understand the impact of regular investing and make informed decisions when comparing different assets in TradingView’s screener. It offers insights into key metrics such as total invested amount, dividends received, equity value, and the number of installments, making it a valuable resource for investors and traders interested in understanding long-term investment outcomes.

🎲 Key Features

Customizable Investment Parameters: Users can define the recurring investment amount, price reference (e.g., open, close, HL2, HLC3, OHLC4), and whether fractional quantities are allowed.

Commission Handling: Supports both fixed and percentage-based commission types, adjusting calculations accordingly.

Dividend Reinvestment: Optionally reinvests dividends after a user-specified period, with the ability to apply tax on dividends.

Time-Bound Analysis: Allows users to set a start year for the analysis, enabling historical performance evaluation.

Flexible Dividend Periods: Dividends can be evaluated based on bars, days, weeks, or months.

Visual Outputs: Plots key metrics like total invested amount, dividends, equity value, and remainder, with customizable display options for clarity in the data window and chart.

🎲 Using the script as an indicator on Tradingview Supercharts

In order to use the indicator on charts, do the following.

Load the instrument of your choice - Preferably a stable stocks, ETFs.

Chose monthly timeframe as lower timeframes are insignificant in this type of investment strategy

Load the indicator SIP Evaluator and Screener and set the input parameters as per your preference.

Indicator plots, investment value, dividends and equity on the chart.

🎲 Visualizations

Installments : Displays the number of SIP installments (gray line, visible in the data window).

Invested Amount : Shows the cumulative amount invested, excluding reinvested dividends (blue area plot).

Dividends : Tracks total dividends received (green area plot).

Equity : Represents the current market value of the investment based on the closing price (purple area plot).

Remainder : Indicates any uninvested cash after each installment (gray line, visible in the data window).

🎲 Deep dive into the settings

The SIP Evaluator and Screener offers a range of customizable settings to tailor the Systematic Investment Plan (SIP) simulation to your preferences. Below is an explanation of each setting, its purpose, and how it impacts the analysis:

🎯 Duration

Start Year (Default: 2020) : Specifies the year from which the SIP calculations begin. When Start Year is enabled via the timebound option, the script only considers data from the specified year onward. This is useful for analyzing historical SIP performance over a defined period. If disabled, the script uses all available data.

Timebound (Default: False) : A toggle to enable or disable the Start Year restriction. When set to False, the SIP calculation starts from the earliest available data for the instrument.

🎯 Investment

Recurring Investment (Default: 1000.0) : The fixed amount invested in each SIP installment (e.g., $1000 per period). This represents the regular contribution to the SIP and directly influences the total invested amount and quantity purchased.

Allow Fractional Qty (Default: True) : When enabled, the script allows the purchase of fractional units (e.g., 2.35 shares). If disabled, only whole units are purchased (e.g., 2 shares), with any remaining funds carried forward as Remainder. This setting impacts the precision of investment allocation.

Price Reference (Default: OPEN): Determines the price used for purchasing units in each SIP installment. Options include:

OPEN : Uses the opening price of the bar.

CLOSE : Uses the closing price of the bar.

HL2 : Uses the average of the high and low prices.

HLC3 : Uses the average of the high, low, and close prices.

OHLC4 : Uses the average of the open, high, low, and close prices. This setting affects the cost basis of each purchase and, consequently, the total quantity and equity value.

🎯 Commission

Commission (Default: 3) : The commission charged per SIP installment, expressed as either a fixed amount (e.g., $3) or a percentage (e.g., 3% of the investment). This reduces the amount available for purchasing units.

Commission Type (Default: Fixed) : Specifies how the commission is calculated:

Fixed ($) : A flat fee is deducted per installment (e.g., $3).

Percentage (%) : A percentage of the investment amount is deducted as commission (e.g., 3% of $1000 = $30). This setting affects the net amount invested and the overall cost of the SIP.

🎯 Dividends

Apply Tax On Dividends (Default: False) : When enabled, a tax is applied to dividends before they are reinvested or recorded. The tax rate is set via the Dividend Tax setting.

Dividend Tax (Default: 47) : The percentage of tax deducted from dividends if Apply Tax On Dividends is enabled (e.g., 47% tax reduces a $100 dividend to $53). This reduces the amount available for reinvestment or accumulation.

Reinvest Dividends After (Default: True, 2) : When enabled, dividends received are reinvested to purchase additional units after a specified period (e.g., 2 units of time, defined by Dividends Availability). If disabled, dividends are tracked but not reinvested. Reinvestment increases the total quantity and equity over time.

Dividends Availability (Default: Bars) : Defines the time unit for evaluating when dividends are available for reinvestment. Options include:

Bars : Based on the number of chart bars.

Weeks : Based on weeks.

Months : Based on months (approximated as 30.5 days). This setting determines the timing of dividend reinvestment relative to the Reinvest Dividends After period.

🎯 How Settings Interact

These settings work together to simulate a realistic SIP. For example, a $1000 recurring investment with a 3% commission and fractional quantities enabled will calculate the number of units purchased at the chosen price reference after deducting the commission. If dividends are reinvested after 2 months with a 47% tax, the script fetches dividend data, applies the tax, and adds the net dividend to the investment amount for that period. The Start Year and Timebound settings ensure the analysis aligns with the desired timeframe, while the Dividends Availability setting fine-tunes dividend reinvestment timing.

By adjusting these settings, users can model different SIP scenarios, compare performance across instruments in TradingView’s screener, and gain insights into how commissions, dividends, and price references impact long-term returns.

🎲 Using the script with Pine Screener

The main purpose of developing this script is to use it with Tradingview Pine Screener so that multiple ETFs/Funds can be compared.

In order to use this as a screener, the following things needs to be done.

Add SIP Evaluator and Screener to your favourites (Required for it to be added in pine screener)

Create a watch list containing required instruments to compare

Open pine screener from Tradingview main menu Products -> Screeners -> Pine or simply load the URL - www.tradingview.com

Select the watchlist created from Watchlist dropdown.

Chose the SIP Evaluator and Screener from the "Choose Indicator" dropdown

Set timeframe to 1 month and update settings as required.

Press scan to display collected data on the screener.

🎲 Use Case

This indicator is ideal for educational purposes, allowing users to experiment with SIP strategies across different instruments. It can be applied in TradingView’s screener to compare SIP performance for stocks, ETFs, or other assets, helping users understand how factors like commissions, dividends, and price references impact returns over time.

Share SizePurpose: The "Share Size" indicator is a powerful risk management tool designed to help traders quickly determine appropriate share/contract sizes based on their predefined risk per trade and the current market's volatility (measured by ATR). It calculates potential dollar differences from recent highs/lows and translates them into a recommended share/contract size, accounting for a user-defined ATR-based offset. This helps you maintain consistent risk exposure across different instruments and market conditions.

How It Works: At its core, the indicator aims to answer the question: "How many shares/contracts can I trade to keep my dollar risk within limits if my stop loss is placed at a recent high or low, plus an ATR-based buffer?"

Price Difference Calculation: It first calculates the dollar difference between the current close price and the high and low of the current bar (Now) and the previous 5 bars (1 to 5).

Tick Size & Value Conversion: These price differences are then converted into dollar values using the instrument's specific tickSize and tickValue. You can select common futures contracts (MNQ, MES, MGC, MCL), a generic "Stock" setting, or define custom values.

ATR Offset: An Average True Range (ATR) based offset is added to these dollar differences. This offset acts as a buffer, simulating a stop loss placed beyond the immediate high/low, accounting for market noise or volatility.

Risk-Based Share Size: Finally, using your Default Risk ($) input, the indicator calculates how many shares/contracts you can take for each of the 6 high/low scenarios (current bar, 5 previous bars) to ensure your dollar risk per trade remains constant.

Dynamic Table: All these calculations are presented in a clear, real-time table at the bottom-left of your chart. The table dynamically adjusts its "Label" to show the selected symbol preset, making it easy to see which instrument's settings are currently being used. The "Shares" rows indicate the maximum shares/contracts you can trade for a given risk and stop placement. The cells corresponding to the largest dollar difference (and thus smallest share size) for both high and low scenarios are highlighted, drawing your attention to the most conservative entry points.

Key Benefits:

Consistent Risk: Helps maintain a consistent dollar risk per trade, regardless of the instrument or its current price/volatility.

Dynamic Sizing: Automatically adjusts share/contract size based on market volatility and your chosen stop placement.

Quick Reference: Provides a real-time, easy-to-read table directly on your chart, eliminating manual calculations.

Informed Decision Making: Assists in quickly assessing trade opportunities and potential position sizes.

Setup Parameters (Inputs)

When you add the "Share Size" indicator to your chart, you'll see a settings dialog with the following parameters:

1. Symbol Preset:

Purpose: This is the primary setting to define the tick size and value for your chosen trading instrument.

Options:

MNQ (Micro Nasdaq 100 Futures)

MES (Micro E-mini S&P 500 Futures)

MGC (Micro Gold Futures)

MCL (Micro Crude Oil Futures)

Stock (Generic stock setting, with tick size/value of 0.01)

Custom (Allows you to manually input tick size and value)

Default: MNQ

Importance: Crucial for accurate dollar calculations. Ensure this matches the instrument you are trading.

2. Tick Size (Manual Override):

Purpose: Only used if Symbol Preset is set to Custom. This defines the smallest price increment for your instrument.

Type: Float

Default: 0.25

Hidden: This input is hidden (display=display.none) unless "Custom" is selected. You might need to change display=display.none to display=display.inline in the code if you want to see and adjust it directly in the settings for "Custom" mode.

3. Tick Value (Manual Override):

Purpose: Only used if Symbol Preset is set to Custom. This defines the dollar value of one tickSize increment.

Type: Float

Default: 0.50

Hidden: This input is hidden (display=display.none) unless "Custom" is selected. Similar to Tick Size, you might need to adjust its display property if you want it visible.

4. Default Risk ($):

Purpose: This is your maximum desired dollar risk per trade. All share size calculations will be based on this value.

Type: Float

Default: 50.0

Hidden: This input is hidden (display=display.none). It's a critical setting, so consider making it visible by changing display=display.none to display=display.inline in the code if you want users to easily adjust their risk.

ATR Offset Settings (Group): This group of settings allows you to fine-tune the ATR-based buffer added to your potential stop loss.

5. ATR Offset Length:

Purpose: Defines the lookback period for the Average True Range (ATR) calculation used for the offset.

Type: Integer

Default: 7

Hidden: This input is hidden (display=display.none).

6. ATR Offset Timeframe:

Purpose: Specifies the timeframe on which the ATR for the offset will be calculated. This allows you to use ATR from a higher timeframe for your stop buffer, even if your chart is on a lower timeframe.

Type: Timeframe string (e.g., "1" for 1 minute, "60" for 1 hour, "D" for Daily)

Default: "1" (1 Minute)

Hidden: This input is hidden (display=display.none).

7. ATR Offset Multiplier (x ATR):

Purpose: Multiplies the calculated ATR value to determine the final dollar offset added to your high/low price difference. A value of 1.0 means one full ATR is added. A value of 0.5 means half an ATR is added.

Type: Float

Minimum Value: 0 (no offset)

Default: 1.0

Hidden: This input is hidden (display=display.none).

Multi-Session MarkerMulti-Session Marker is a flexible visual tool for traders who want to highlight up to 10 custom trading sessions directly on their chart’s background.

Custom Sessions: Enter up to 10 time ranges (in HHMM-HHMM format) to mark any market session, news window, or personal focus period.

Visual Clarity: For each session, toggle the highlight on or off and select a unique background color and opacity, making it easy to distinguish active trading windows at a glance.

Universal Time Handling: Session times automatically follow your chart’s time zone—no manual adjustment required.

Efficient and Fast: Utilizes TradingView’s bgcolor() for smooth performance, even on fast timeframes like 1-second charts.

Clean Interface: All session controls are grouped for easy editing in the indicator’s settings panel.

How to use:

In the indicator settings, enter your desired session times (e.g., 0930-1130) for each session you want to highlight.

Toggle “Show Session” and pick a color for each session.

The background will automatically highlight those periods on your chart.

This indicator is ideal for day traders, futures traders, or anyone who wants to visually segment their trading day for better focus and analysis.

TradePlanner ProPlan smarter. Trade with precision.

TradePlanner Pro is a professional-grade overlay tool designed to streamline your trading decisions by visually organizing your trade plans directly on the chart. Built for traders who value preparation and clarity, this script enables precise entry planning, risk management, and target visualization—all tailored per symbol.

Core Purpose

TradePlanner Pro helps you map out potential trades using pre-defined symbol-based presets. It dynamically calculates position sizes based on your account size or fixed risk, then visualizes key trade levels (Entry, Take Profits, Stop Loss) with profit/loss metrics in both dollar and percentage terms. It's the perfect companion for traders who prepare their setups in advance and want their plans clearly represented on the chart.

Key Features

🔹 Per-Symbol Presets: Define entries, up to 3 take-profit levels, and stop-losses for each ticker.

🔹 Dynamic Risk Sizing: Choose between percentage-based risk or fixed dollar risk per trade.

🔹 Visual Trade Mapping: Automatically plots Entry, TP1–TP3, and SL lines on your chart.

🔹 Real-Time P&L Labels: Displays profit/loss amounts and percentages, with optional R/R ratios.

🔹 Custom Investment Display: Shows how much capital is allocated per trade.

🔹 Clean, Configurable UI: Adjust label positions, font sizes, opacity, and label visibility to match your style.

Whether you're swing trading or day trading, TradePlanner Pro helps you stay disciplined, organized, and confident in your execution.

How to Use TradePlanner Pro – Step-by-Step Guide

TradePlanner Pro is designed to be easy to set up while giving you full control over how your trades are visualized and calculated. Here’s how to get started:

1. Start with Default Settings

By default, the script assumes:

Account Size: $10,000

Max Money per Trade (%): 1.0%

Max Risk (USD): 0 (disabled; only percentage risk is used)

This means the script will size each trade to risk 1% of your account balance per trade unless you override it with a fixed USD risk amount.

2. Set Up Your Symbol Presets

The "Symbol Presets" input is a flexible text area where you define trade setups for each ticker.

Format (one per line):

SYMBOL:Entry,TP1 ,SL

Example:

AAPL:250,260,270,240

MSFT:100,110,90

TSLA:180,200,170

You can include 1 to 3 take-profit levels.

The script will only activate for the current chart’s symbol, matching what's listed.

3. Customize Risk Parameters

You can use:

Account % Risk – Based on account size and % risk.

Fixed USD Risk – When a dollar amount is entered (>0), it takes priority and calculates share size based on the risk per share.

There's also an option to round share quantities down to whole units, which is useful for stock or crypto trading platforms that only allow whole-number units.

4. Choose What to Display

Toggle on/off these elements as needed:

Show Entry/TP/SL Lines

Show P&L Labels – Profit/loss amounts at each target and SL.

Show Amount Invested – Includes total dollar value in the quantity label.

Show Percentages – Adds % gain/loss to each label.

Show Risk/Reward Ratios – Optionally displayed beside or below TP labels.

You can further adjust:

Font size and label opacity

Label position offset – In percent of price range, so they don’t overlap the actual levels.

5. Read the Visual Outputs

Once the preset matches the current chart symbol:

Lines will appear for Entry, TP1-TP3, and Stop Loss.

Labels will display your:

Trade quantity (and invested amount)

Dollar and % profit at each target

Total loss at stop loss

Optional R/R ratios

Everything updates dynamically and adjusts to your current chart scale and bar availabilit

Position Size Calculator v206/17/2025 - Updated to add MGC to list of instruments

Position Size Calculator for Futures Trading

A professional position sizing tool designed specifically for futures traders who want to maintain disciplined risk management. This indicator calculates the optimal number of contracts based on your predefined risk amount and provides instant visual feedback.

Key Features:

• Interactive price selection - simply click on the chart to set entry, stop loss, and take profit levels

• Supports all major futures contracts: ES, NQ, GC, RTY, YM, MNQ, MES with accurate contract specifications

• Customizable risk amount (defaults to $500 but fully adjustable)

• Real-time position size calculations that never exceed your risk tolerance

• Visual risk validation with color-coded header (green = valid risk, red = excessive risk)

• Automatic 2:1 risk/reward ratio calculations

• Compact, non-intrusive table display in top-right corner

• Clean interface with no chart clutter

How to Use:

Select your futures instrument from the dropdown

Set your maximum risk amount (default $500)

Click on the chart to set your Entry Price

Click on the chart to set your Stop Loss Price

Optionally click to set your Take Profit Price

The calculator instantly shows maximum contracts, actual risk, expected profit, and R/R ratio

Risk Management:

The indicator enforces strict risk management by calculating the maximum number of contracts you can trade while staying within your specified risk limit. The header turns green when your trade is within acceptable risk parameters and red when the risk is too high, providing instant visual feedback.

Perfect for day traders, swing traders, and anyone trading futures who wants to maintain consistent position sizing and risk management discipline.

Luma DCA Simulator (BTC only)Luma DCA Simulator – Guide

What is the Luma DCA Simulator?

The Luma DCA Tracker shows how regular Bitcoin investments (Dollar Cost Averaging) would have developed over a freely selectable period – directly in the chart, transparent and easy to follow.

Settings Overview

1. Investment amount per interval

Specifies how much capital is invested at each purchase (e.g. 100).

2. Start date

Defines the point in time from which the simulation begins – e.g. 01.01.2020.

3. Investment interval

Determines how frequently investments are made:

– Daily

– Weekly

– Every 14 days

– Monthly

4. Language

Switches the info box display between English and German.

5. Show investment data (optional)

If activated, the chart will display additional values such as total invested capital, BTC amount, current value, and profit/loss.

What the Chart Displays

Entry points: Each DCA purchase is marked as a point in the price chart.

Average entry price: An orange line visualizes the evolving DCA average.

Info box (bottom left) with a live summary of:

– Total invested capital

– Total BTC acquired

– Average entry price

– Current portfolio value

– Profit/loss in absolute terms and percentage

Note on Accuracy

This simulation is for illustrative purposes only.

Spreads, slippage, fees, and tax effects are not included.

Actual results may vary.

Technical Note

For daily or weekly intervals, the chart timeframe should be set to 1 day or lower to ensure all purchases are accurately included.

Larger timeframes (e.g. weekly or monthly charts) may result in missed investments.

Currency Handling

All calculations are based on the selected chart symbol (e.g. BTCUSD, BTCEUR, BTCUSDT).

The displayed currency is automatically determined by the chart used.

Luma DCA Tracker (BTC)Luma DCA Tracker (BTC) – User Guide

Function

This indicator simulates a regular Bitcoin investment strategy (Dollar Cost Averaging). It calculates and visualizes:

Accumulated BTC amount

Average entry price

Total amount invested

Current portfolio value

Profit/loss in absolute and percentage terms

Settings

Investment per interval

Fixed amount to be invested at each interval (e.g., 100 USD)

Start date

The date when DCA simulation begins

Investment interval

Choose between:

daily, weekly, every 14 days, or monthly

Show investment data

Displays additional chart lines (total invested, value, profit, etc.)

Chart Elements

Orange line: Average DCA entry price

Grey dots: Entry points based on selected interval

Info box (bottom left): Live summary of all key values

Notes

Purchases are simulated at the closing price of each interval

No fees, slippage, or taxes are included

The indicator is a simulation only and not linked to an actual portfolio

X-Day Capital Efficiency ScoreThis indicator helps identify the Most Profitable Movers for Your fixed Capital (ie, which assets offer the best average intraday profit potential for a fixed capital).

Unlike traditional volatility indicators (like ATR or % change), this script calculates how much real dollar profit you could have made each day over a custom lookback period — assuming you deployed your full capital into that ticker daily.

How it works:

Calculates the daily intraday range (high − low)

Filters for clean candles (where body > 60% of the candle range)

Assumes you invested the full amount of capital ($100K set as default) on each valid day

Computes an average daily profit score based on price action over the selected period (default set to 20 days)

Plots the score in dollars — higher = more efficient use of capital

Why It’s Useful:

Compare tickers based on real dollar return potential — not just % volatility

Spot low-priced, high-volatility stocks that are better suited for intraday or momentum trading

Inputs:

Capital ($): Amount you're hypothetically deploying (e.g., 100,000)

Look Back Period: Number of past days to average over (e.g., 20)

Futures Margin Lookup TableThis script applies a table to your chart, which provides the intraday and overnight margin requirements of the currently selected symbol.

In this indicator the user must provide the broker data in the form of specifically formatted text blocks. The data for which should be found on the broker website under futures margin requirements.

The purpose for it's creation is due to the non-standard way each individual broker may price their margins and lack of information within TradingView when connected to some (maybe all) brokers, including during paper trading, as the flat percentage rule is not accurate.

An example of information could look like this

MES;Micro S&P;$50;$2406

ES;E-Mini S&P;$500;$24,053

GC;Gold;$500;$16500

NQ;E-Mini Nasdaq;$1,000;$34,810

FDAX;Dax Index;€2,000;€44,311

Each symbol begins a new line, and the values on that line are separated by semicolons (;)

Each line consists of the following...

SYMBOL : Search string used to match to the beginning of the current chart symbol.

NAME: Human readable name

INTRA: Intraday trading margin requirement per contract

OVERNIGHT: Overnight trading margin requirement per contract

The script simply finds a matching line within your provided information using the current chart symbol.

So for example the continuous chart for

NQ1!

would match to the user specified line starting with NQ... as would the individual contract dates such as NQM2025, NQK2025, etc.

NOTES:

There is a possibility that symbols with similar starting characters could match. If this is the case put the longer symbol higher in the list.

There is also a line / character limit to the text input fields within pinescript. Ensure the text you enter / paste into them is not truncated. If so there are 3 input fields for just this purpose. Find the last complete line and continue the remaining symbol lines on the subsequent inputs.

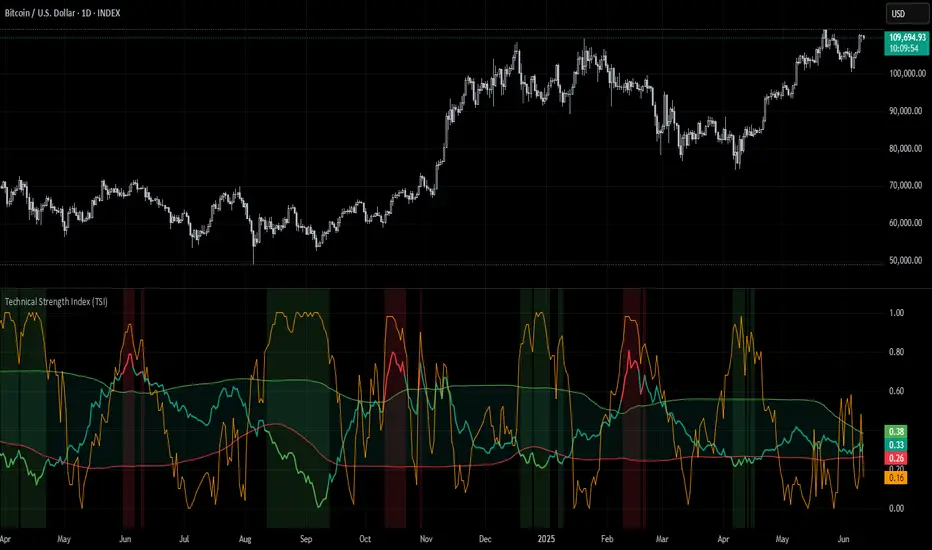

Technical Strength Index (TSI)📘 TSI with Dynamic Bands – Technical Strength Index

The TSI with Dynamic Bands is a multi-factor indicator designed to measure the statistical strength and structure of a trend. It combines several quantitative metrics into a single, normalized score between 0 and 1, allowing traders to assess the technical quality of market moves and detect overbought/oversold conditions with adaptive precision.

🧠 Core Components

This indicator draws from the StatMetrics library, blending:

📈 Trend Persistence: via the Hurst exponent, indicating whether price action is mean-reverting or trending.

📉 Risk-Adjusted Volatility: via the inverted , rewarding smoother, less erratic price movement.

🚀 Momentum Strength: using a combination of directional momentum and Z-score–normalized returns.

These components are normalized and averaged into the TSI line.

🎯 Features

TSI Line: Composite score of trend quality (0 = weak/noise, 1 = strong/structured).

Dynamic Bands: Mean ± 1 standard deviation envelopes provide adaptive context.

Overbought/Oversold Detection: Based on a rolling quantile (e.g. 90th/10th percentile of TSI history).

Signal Strength Bar (optional): Measures how statistically extreme the current TSI value is, helping validate confidence in trade setups.

Dynamic Color Cues: Background and bar gradients help visually identify statistically significant zones.

📈 How to Use

Look for overbought (red background) or oversold (green background) conditions as potential reversal zones.

Confirm trend strength with the optional signal strength bar — stronger values suggest higher signal confidence.

Use the TSI line and context bands to filter out noisy ranges and focus on structured price moves.

⚙️ Inputs

Lookback Period: Controls the smoothing and window size for statistical calculations.

Overbought/Oversold Quantiles: Adjust the thresholds for signal zones.

Plot Signal Strength: Enable or disable the signal confidence bar.

Overlay Signal Strength: Show signal strength in the same panel (compact) or not (cleaner TSI-only view).

🛠 Example Use Cases

Mean reversion traders identifying reversal zones with statistical backing

Momentum/Trend traders confirming structure before entries

Quantitative dashboards or multi-asset screening tools

⚠️ Disclaimer

This script is for educational and informational purposes only. It does not constitute financial advice or a recommendation to buy or sell any financial instrument.

This AI is not a financial advisor; please consult your financial advisor for personalized advice.

SmartPhase Analyzer📝 SmartPhase Analyzer – Composite Market Regime Classifier

SmartPhase Analyzer is an adaptive regime classification tool that scores market conditions using a customizable set of statistical indicators. It blends multiple normalized metrics into a composite score, which is dynamically evaluated against rolling statistical thresholds to determine the current market regime.

✅ Features:

Composite score calculated from 13+ toggleable statistical indicators:

Sharpe, Sortino, Omega, Alpha, Beta, CV, R², Entropy, Drawdown, Z-Score, PLF, SRI, and Momentum Rank

Uses dynamic thresholds (mean ± std deviation) to classify regime states:

🟢 BULL – Strongly bullish

🟩 ACCUM – Mildly bullish

⚪ NEUTRAL – Sideways

🟧 DISTRIB – Mildly bearish

🔴 BEAR – Strongly bearish

Color-coded histogram for composite score clarity

Real-time regime label plotted on chart

Benchmark-aware metrics (Alpha, Beta, etc.)

Modular design using the StatMetrics library by RWCS_LTD

🧠 How to Use:

Enable/disable metrics in the settings panel to customize your composite model

Use the composite histogram and regime background for discretionary or systematic analysis

⚠️ Disclaimer:

This indicator is for educational and informational purposes only. It does not constitute financial advice or a trading recommendation. Always consult your financial advisor before making investment decisions.

Pair TradingPAIR TRADING

Description:

This indicator is a simple and intuitive tool for rotating between two assets based on their relative price ratio. By comparing the prices of Asset A and Asset B, it plots a “ratio line” (gray) with dynamic upper and lower boundaries (red and blue).

When the ratio reaches the red line, Asset A is expensive → rotate out of A and into B.

When the ratio touches the blue line, Asset A is cheap → rotate back into A.

The chart also shows:

🔹 Background highlights for visual cues

🔹 “Rotate to A” or “Rotate to B” markers for easy decisions

🔹 A live summary table with mean ratio, upper/lower boundaries, and current ratio

How to Use:

Select Asset A and Asset B in the settings.

Adjust the Lookback Period and Threshold if needed.

Watch the gray ratio line as it moves:

Above red line? → Consider rotating into B

Below blue line? → Consider rotating into A

Use the background color changes and rotation labels to spot clear rotation opportunities!

Why Pair Trading?

Pair trading is a powerful way to manage a portfolio because it neutralizes market direction risk and focuses on relative value.

By rotating between correlated assets, you can:

Smooth out returns

Avoid holding a weak asset too long

Capture reversion when assets diverge too far

This approach can enhance risk-adjusted returns and help keep your portfolio balanced and nimble!

How to Pick Pairs:

Choose assets with strong correlation or similar drivers.

Look for common trends (sector, macro).

Start with assets you know best (high-conviction ideas).

Make sure both have good liquidity for reliable trading!

TO HELP FIND CORRELATED ASSETS:

Use the Correlation Coefficient indicator in TradingView:

Click Indicators

Search for “Correlation Coefficient”

Add it to your chart

Input the symbol of the second asset (e.g., if you’re on MSTR, input TSLA).

This plots the rolling correlation coefficient — super helpful!

Pair trading can turn big swings into steady rotations and help you stay active even when the market is choppy. It’s a simple, practical approach to keep your portfolio balanced.

Simple Position CalculatorThis indicator provides a real-time position sizing calculator designed for fast momentum trading. It instantly calculates optimal trade size based on your risk parameters, entry/exit prices, and exchange conditions (fees/slippage). Perfect for high-speed entries during candle closes and breakouts.

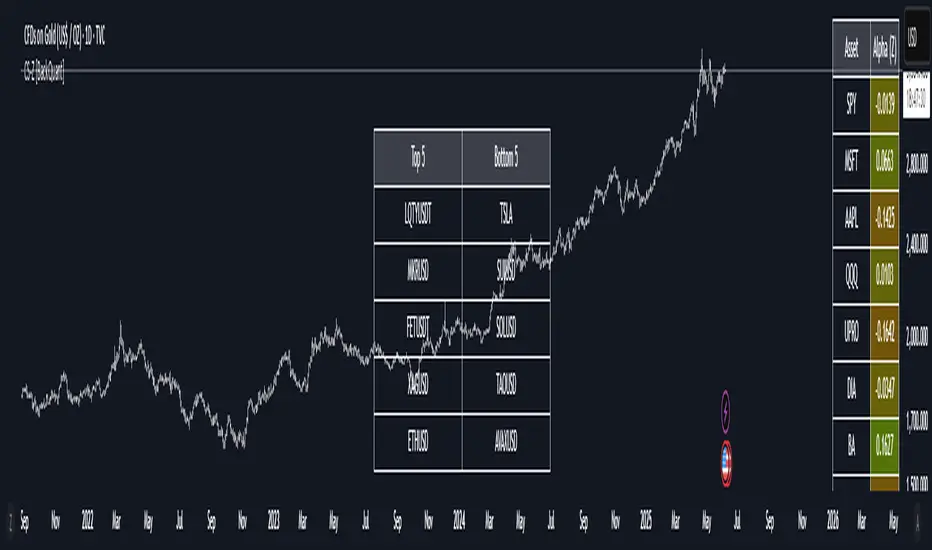

40 Ticker Cross-Sectional Z-Scores [BackQuant]40 Ticker Cross-Sectional Z-Scores

BackQuant’s 40 Ticker Cross-Sectional Z-Scores is a powerful portfolio management strategy that analyzes the relative performance of up to 40 different assets, comparing them on a cross-sectional basis to identify the top and bottom performers. This indicator computes Z-scores for each asset based on their log returns and evaluates them relative to the mean and standard deviation over a rolling window. The Z-scores represent how far an asset's return deviates from the average, and these values are used to rank the assets, allowing for dynamic asset allocation based on performance.

By focusing on the strongest-performing assets and avoiding the weakest, this strategy aims to enhance returns while managing risk. Additionally, by adjusting for standard deviations, the system offers a risk-adjusted method of ranking assets, making it suitable for traders who want to dynamically allocate capital based on performance metrics rather than just price movements.

Key Features

1. Cross-Sectional Z-Score Calculation:

The system calculates Z-scores for 40 different assets, evaluating their log returns against the mean and standard deviation over a rolling window. This enables users to assess the relative performance of each asset dynamically, highlighting which assets are performing better or worse compared to their historical norms. The Z-score is a useful statistical tool for identifying outliers in asset performance.

2. Asset Ranking and Allocation:

The system ranks assets based on their Z-scores and allocates capital to the top performers. It identifies the top and bottom assets, and traders can allocate capital to the top-performing assets, ensuring that their portfolio is aligned with the best performers. Conversely, the bottom assets are removed from the portfolio, reducing exposure to underperforming assets.

3. Rolling Window for Mean and Standard Deviation Calculations:

The Z-scores are calculated based on rolling means and standard deviations, making the system adaptive to changing market conditions. This rolling calculation window allows the strategy to adjust to recent performance trends and minimize the impact of outdated data.

4. Mean and Standard Deviation Visualization:

The script provides real-time visualizations of the mean (x̄) and standard deviation (σ) of asset returns, helping traders quickly identify trends and volatility in their portfolio. These visual indicators are useful for understanding the current market environment and making more informed allocation decisions.

5. Top & Bottom Performer Tables:

The system generates tables that display the top and bottom performers, ranked by their Z-scores. Traders can quickly see which assets are outperforming and underperforming. These tables provide clear and actionable insights, helping traders make informed decisions about which assets to include in their portfolio.

6. Customizable Parameters:

The strategy allows traders to customize several key parameters, including:

Rolling Calculation Window: Set the window size for the rolling mean and standard deviation calculations.

Top & Bottom Tickers: Choose how many of the top and bottom assets to display and allocate capital to.

Table Orientation: Select between vertical or horizontal table formats to suit the user’s preference.

7. Forward Test & Out-of-Sample Testing:

The system includes out-of-sample forward tests, ensuring that the strategy is evaluated based on real-time performance, not just historical data. This forward testing approach helps validate the robustness of the strategy in dynamic market conditions.

8. Visual Feedback and Alerts:

The system provides visual feedback on the current asset rankings and allocations, with dynamic labels and plots on the chart. Additionally, users receive alerts when allocations change, keeping them informed of important adjustments.

9. Risk Management via Z-Scores and Std Dev:

The system’s approach to asset selection is based on Z-scores, which normalize performance relative to the historical mean. By incorporating standard deviation, it accounts for the volatility and risk associated with each asset. This allows for more precise risk management and portfolio construction.

10. Note on Mean Reversion Strategy:

If you take the inverse of the signals provided by this indicator, the strategy can be used for mean-reversion rather than trend-following. This would involve buying the underperforming assets and selling the outperforming ones. However, it's important to note that this approach does not work well with highly correlated assets, as the relationship between the assets could result in the same directional movement, undermining the effectiveness of the mean-reversion strategy.

References

www.uts.edu.au

onlinelibrary.wiley.com

www.cmegroup.com

Final Thoughts

The 40 Ticker Cross-Sectional Z-Scores strategy offers a data-driven approach to portfolio management, dynamically allocating capital based on the relative performance of assets. By using Z-scores and standard deviations, this strategy ensures that capital is directed to the strongest performers while avoiding weaker assets, ultimately improving the risk-adjusted returns of the portfolio. Whether you’re focused on trend-following or looking to explore mean-reversion strategies, this flexible system can be tailored to suit your investment goals.

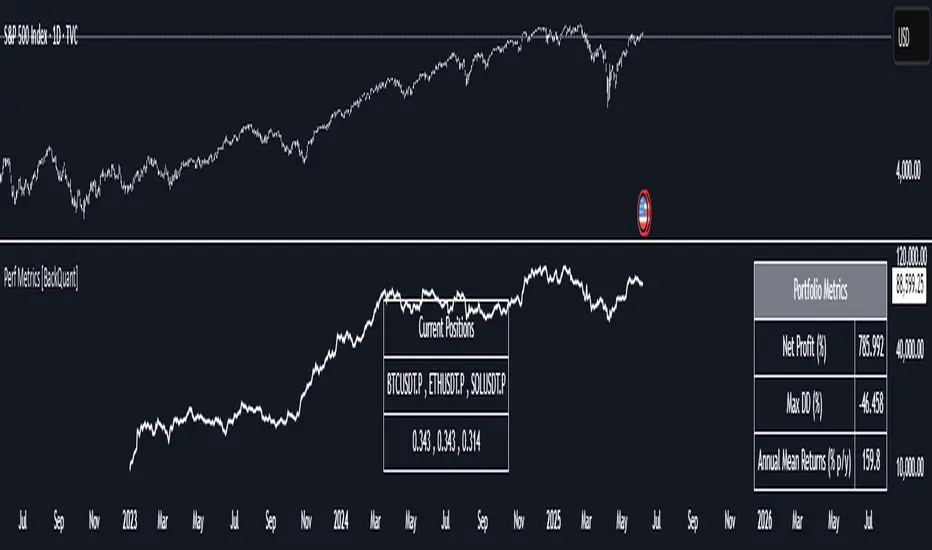

Performance Metrics With Bracketed Rebalacing [BackQuant]Performance Metrics With Bracketed Rebalancing

The Performance Metrics With Bracketed Rebalancing script offers a robust method for assessing portfolio performance, integrating advanced portfolio metrics with different rebalancing strategies. With a focus on adaptability, the script allows traders to monitor and adjust portfolio weights, equity, and other key financial metrics dynamically. This script provides a versatile approach for evaluating different trading strategies, considering factors like risk-adjusted returns, volatility, and the impact of portfolio rebalancing.

Please take the time to read the following:

Key Features and Benefits of Portfolio Methods

Bracketed Rebalancing:

Bracketed Rebalancing is an advanced strategy designed to trigger portfolio adjustments when an asset's weight surpasses a predefined threshold. This approach minimizes overexposure to any single asset while maintaining flexibility in response to market changes. The strategy is particularly beneficial for mitigating risks that arise from significant asset weight fluctuations. The following image illustrates how this method reacts when asset weights cross the threshold:

Daily Rebalancing:

Unlike the bracketed method, Daily Rebalancing adjusts portfolio weights every trading day, ensuring consistent asset allocation. This method aims for a more even distribution of portfolio weights, making it a suitable option for traders who prefer less sensitivity to individual asset volatility. Here's an example of Daily Rebalancing in action:

No Rebalancing:

For traders who prefer a passive approach, the "No Rebalancing" option allows the portfolio to remain static, without any adjustments to asset weights. This method may appeal to long-term investors or those who believe in the inherent stability of their selected assets. Here’s how the portfolio looks when no rebalancing is applied:

Portfolio Weights Visualization:

One of the standout features of this script is the visual representation of portfolio weights. With adjustable settings, users can track the current allocation of assets in real-time, making it easier to analyze shifts and trends. The following image shows the real-time weight distribution across three assets:

Rolling Drawdown Plot:

Managing drawdown risk is a critical aspect of portfolio management. The Rolling Drawdown Plot visually tracks the drawdown over time, helping traders monitor the risk exposure and performance relative to the peak equity levels. This feature is essential for assessing the portfolio's resilience during market downturns:

Daily Portfolio Returns:

Tracking daily returns is crucial for evaluating the short-term performance of the portfolio. The script allows users to plot daily portfolio returns to gain insights into daily profit or loss, helping traders stay updated on their portfolio’s progress:

Performance Metrics

Net Profit (%):

This metric represents the total return on investment as a percentage of the initial capital. A positive net profit indicates that the portfolio has gained value over the evaluation period, while a negative value suggests a loss. It's a fundamental indicator of overall portfolio performance.

Maximum Drawdown (Max DD):

Maximum Drawdown measures the largest peak-to-trough decline in portfolio value during a specified period. It quantifies the most significant loss an investor would have experienced if they had invested at the highest point and sold at the lowest point within the timeframe. A smaller Max DD indicates better risk management and less exposure to significant losses.

Annual Mean Returns (% p/y):

This metric calculates the average annual return of the portfolio over the evaluation period. It provides insight into the portfolio's ability to generate returns on an annual basis, aiding in performance comparison with other investment opportunities.

Annual Standard Deviation of Returns (% p/y):

This measure indicates the volatility of the portfolio's returns on an annual basis. A higher standard deviation signifies greater variability in returns, implying higher risk, while a lower value suggests more stable returns.

Variance:

Variance is the square of the standard deviation and provides a measure of the dispersion of returns. It helps in understanding the degree of risk associated with the portfolio's returns.

Sortino Ratio:

The Sortino Ratio is a variation of the Sharpe Ratio that only considers downside risk, focusing on negative volatility. It is calculated as the difference between the portfolio's return and the minimum acceptable return (MAR), divided by the downside deviation. A higher Sortino Ratio indicates better risk-adjusted performance, emphasizing the importance of avoiding negative returns.

Sharpe Ratio:

The Sharpe Ratio measures the portfolio's excess return per unit of total risk, as represented by standard deviation. It is calculated by subtracting the risk-free rate from the portfolio's return and dividing by the standard deviation of the portfolio's excess return. A higher Sharpe Ratio indicates more favorable risk-adjusted returns.

Omega Ratio:

The Omega Ratio evaluates the probability of achieving returns above a certain threshold relative to the probability of experiencing returns below that threshold. It is calculated by dividing the cumulative probability of positive returns by the cumulative probability of negative returns. An Omega Ratio greater than 1 indicates a higher likelihood of achieving favorable returns.

Gain-to-Pain Ratio:

The Gain-to-Pain Ratio measures the return per unit of risk, focusing on the magnitude of gains relative to the severity of losses. It is calculated by dividing the total gains by the total losses experienced during the evaluation period. A higher ratio suggests a more favorable balance between reward and risk.

www.linkedin.com

Compound Annual Growth Rate (CAGR) (% p/y):

CAGR represents the mean annual growth rate of the portfolio over a specified period, assuming the investment has been compounding over that time. It provides a smoothed annual rate of growth, eliminating the effects of volatility and offering a clearer picture of long-term performance.

Portfolio Alpha (% p/y):

Portfolio Alpha measures the portfolio's performance relative to a benchmark index, adjusting for risk. It is calculated using the Capital Asset Pricing Model (CAPM) and represents the excess return of the portfolio over the expected return based on its beta and the benchmark's performance. A positive alpha indicates outperformance, while a negative alpha suggests underperformance.

Portfolio Beta:

Portfolio Beta assesses the portfolio's sensitivity to market movements, indicating its exposure to systematic risk. A beta greater than 1 suggests the portfolio is more volatile than the market, while a beta less than 1 indicates lower volatility. Beta is used to understand the portfolio's potential for gains or losses in relation to market fluctuations.

Skewness of Returns:

Skewness measures the asymmetry of the return distribution. A positive skew indicates a distribution with a long right tail, suggesting more frequent small losses and fewer large gains. A negative skew indicates a long left tail, implying more frequent small gains and fewer large losses. Understanding skewness helps in assessing the likelihood of extreme outcomes.

Value at Risk (VaR) 95th Percentile:

VaR at the 95th percentile estimates the maximum potential loss over a specified period, given a 95% confidence level. It provides a threshold value such that there is a 95% probability that the portfolio will not experience a loss greater than this amount.

Conditional Value at Risk (CVaR):

CVaR, also known as Expected Shortfall, measures the average loss exceeding the VaR threshold. It provides insight into the tail risk of the portfolio, indicating the expected loss in the worst-case scenarios beyond the VaR level.

These metrics collectively offer a comprehensive view of the portfolio's performance, risk exposure, and efficiency. By analyzing these indicators, investors can make informed decisions, balancing potential returns with acceptable levels of risk.

Conclusion

The Performance Metrics With Bracketed Rebalancing script provides a comprehensive framework for evaluating and optimizing portfolio performance. By integrating advanced metrics, adaptive rebalancing strategies, and visual analytics, it empowers traders to make informed decisions in managing their investment portfolios. However, it's crucial to consider the implications of rebalancing strategies, as academic research indicates that predictable rebalancing can lead to market impact costs. Therefore, adopting flexible and less predictable rebalancing approaches may enhance portfolio performance and reduce associated costs.

Risk-Adjusted Momentum Oscillator# Risk-Adjusted Momentum Oscillator (RAMO): Momentum Analysis with Integrated Risk Assessment

## 1. Introduction

Momentum indicators have been fundamental tools in technical analysis since the pioneering work of Wilder (1978) and continue to play crucial roles in systematic trading strategies (Jegadeesh & Titman, 1993). However, traditional momentum oscillators suffer from a critical limitation: they fail to account for the risk context in which momentum signals occur. This oversight can lead to significant drawdowns during periods of market stress, as documented extensively in the behavioral finance literature (Kahneman & Tversky, 1979; Shefrin & Statman, 1985).

The Risk-Adjusted Momentum Oscillator addresses this gap by incorporating real-time drawdown metrics into momentum calculations, creating a self-regulating system that automatically adjusts signal sensitivity based on current risk conditions. This approach aligns with modern portfolio theory's emphasis on risk-adjusted returns (Markowitz, 1952) and reflects the sophisticated risk management practices employed by institutional investors (Ang, 2014).

## 2. Theoretical Foundation

### 2.1 Momentum Theory and Market Anomalies

The momentum effect, first systematically documented by Jegadeesh & Titman (1993), represents one of the most robust anomalies in financial markets. Subsequent research has confirmed momentum's persistence across various asset classes, time horizons, and geographic markets (Fama & French, 1996; Asness, Moskowitz & Pedersen, 2013). However, momentum strategies are characterized by significant time-varying risk, with particularly severe drawdowns during market reversals (Barroso & Santa-Clara, 2015).

### 2.2 Drawdown Analysis and Risk Management

Maximum drawdown, defined as the peak-to-trough decline in portfolio value, serves as a critical risk metric in professional portfolio management (Calmar, 1991). Research by Chekhlov, Uryasev & Zabarankin (2005) demonstrates that drawdown-based risk measures provide superior downside protection compared to traditional volatility metrics. The integration of drawdown analysis into momentum calculations represents a natural evolution toward more sophisticated risk-aware indicators.

### 2.3 Adaptive Smoothing and Market Regimes

The concept of adaptive smoothing in technical analysis draws from the broader literature on regime-switching models in finance (Hamilton, 1989). Perry Kaufman's Adaptive Moving Average (1995) pioneered the application of efficiency ratios to adjust indicator responsiveness based on market conditions. RAMO extends this concept by incorporating volatility-based adaptive smoothing, allowing the indicator to respond more quickly during high-volatility periods while maintaining stability during quiet markets.

## 3. Methodology

### 3.1 Core Algorithm Design

The RAMO algorithm consists of several interconnected components:

#### 3.1.1 Risk-Adjusted Momentum Calculation

The fundamental innovation of RAMO lies in its risk adjustment mechanism:

Risk_Factor = 1 - (Current_Drawdown / Maximum_Drawdown × Scaling_Factor)

Risk_Adjusted_Momentum = Raw_Momentum × max(Risk_Factor, 0.05)

This formulation ensures that momentum signals are dampened during periods of high drawdown relative to historical maximums, implementing an automatic risk management overlay as advocated by modern portfolio theory (Markowitz, 1952).

#### 3.1.2 Multi-Algorithm Momentum Framework

RAMO supports three distinct momentum calculation methods:

1. Rate of Change: Traditional percentage-based momentum (Pring, 2002)

2. Price Momentum: Absolute price differences

3. Log Returns: Logarithmic returns preferred for volatile assets (Campbell, Lo & MacKinlay, 1997)

This multi-algorithm approach accommodates different asset characteristics and volatility profiles, addressing the heterogeneity documented in cross-sectional momentum studies (Asness et al., 2013).

### 3.2 Leading Indicator Components

#### 3.2.1 Momentum Acceleration Analysis

The momentum acceleration component calculates the second derivative of momentum, providing early signals of trend changes:

Momentum_Acceleration = EMA(Momentum_t - Momentum_{t-n}, n)

This approach draws from the physics concept of acceleration and has been applied successfully in financial time series analysis (Treadway, 1969).

#### 3.2.2 Linear Regression Prediction

RAMO incorporates linear regression-based prediction to project momentum values forward:

Predicted_Momentum = LinReg_Value + (LinReg_Slope × Forward_Offset)

This predictive component aligns with the literature on technical analysis forecasting (Lo, Mamaysky & Wang, 2000) and provides leading signals for trend changes.

#### 3.2.3 Volume-Based Exhaustion Detection

The exhaustion detection algorithm identifies potential reversal points by analyzing the relationship between momentum extremes and volume patterns:

Exhaustion = |Momentum| > Threshold AND Volume < SMA(Volume, 20)

This approach reflects the established principle that sustainable price movements require volume confirmation (Granville, 1963; Arms, 1989).

### 3.3 Statistical Normalization and Robustness

RAMO employs Z-score normalization with outlier protection to ensure statistical robustness:

Z_Score = (Value - Mean) / Standard_Deviation

Normalized_Value = max(-3.5, min(3.5, Z_Score))

This normalization approach follows best practices in quantitative finance for handling extreme observations (Taleb, 2007) and ensures consistent signal interpretation across different market conditions.

### 3.4 Adaptive Threshold Calculation

Dynamic thresholds are calculated using Bollinger Band methodology (Bollinger, 1992):

Upper_Threshold = Mean + (Multiplier × Standard_Deviation)

Lower_Threshold = Mean - (Multiplier × Standard_Deviation)

This adaptive approach ensures that signal thresholds adjust to changing market volatility, addressing the critique of fixed thresholds in technical analysis (Taylor & Allen, 1992).

## 4. Implementation Details

### 4.1 Adaptive Smoothing Algorithm

The adaptive smoothing mechanism adjusts the exponential moving average alpha parameter based on market volatility:

Volatility_Percentile = Percentrank(Volatility, 100)

Adaptive_Alpha = Min_Alpha + ((Max_Alpha - Min_Alpha) × Volatility_Percentile / 100)

This approach ensures faster response during volatile periods while maintaining smoothness during stable conditions, implementing the adaptive efficiency concept pioneered by Kaufman (1995).

### 4.2 Risk Environment Classification

RAMO classifies market conditions into three risk environments:

- Low Risk: Current_DD < 30% × Max_DD

- Medium Risk: 30% × Max_DD ≤ Current_DD < 70% × Max_DD

- High Risk: Current_DD ≥ 70% × Max_DD

This classification system enables conditional signal generation, with long signals filtered during high-risk periods—a approach consistent with institutional risk management practices (Ang, 2014).

## 5. Signal Generation and Interpretation

### 5.1 Entry Signal Logic

RAMO generates enhanced entry signals through multiple confirmation layers:

1. Primary Signal: Crossover between indicator and signal line

2. Risk Filter: Confirmation of favorable risk environment for long positions

3. Leading Component: Early warning signals via acceleration analysis

4. Exhaustion Filter: Volume-based reversal detection

This multi-layered approach addresses the false signal problem common in traditional technical indicators (Brock, Lakonishok & LeBaron, 1992).

### 5.2 Divergence Analysis

RAMO incorporates both traditional and leading divergence detection:

- Traditional Divergence: Price and indicator divergence over 3-5 periods

- Slope Divergence: Momentum slope versus price direction

- Acceleration Divergence: Changes in momentum acceleration

This comprehensive divergence analysis framework draws from Elliott Wave theory (Prechter & Frost, 1978) and momentum divergence literature (Murphy, 1999).

## 6. Empirical Advantages and Applications

### 6.1 Risk-Adjusted Performance

The risk adjustment mechanism addresses the fundamental criticism of momentum strategies: their tendency to experience severe drawdowns during market reversals (Daniel & Moskowitz, 2016). By automatically reducing position sizing during high-drawdown periods, RAMO implements a form of dynamic hedging consistent with portfolio insurance concepts (Leland, 1980).

### 6.2 Regime Awareness

RAMO's adaptive components enable regime-aware signal generation, addressing the regime-switching behavior documented in financial markets (Hamilton, 1989; Guidolin, 2011). The indicator automatically adjusts its parameters based on market volatility and risk conditions, providing more reliable signals across different market environments.

### 6.3 Institutional Applications

The sophisticated risk management overlay makes RAMO particularly suitable for institutional applications where drawdown control is paramount. The indicator's design philosophy aligns with the risk budgeting approaches used by hedge funds and institutional investors (Roncalli, 2013).

## 7. Limitations and Future Research

### 7.1 Parameter Sensitivity

Like all technical indicators, RAMO's performance depends on parameter selection. While default parameters are optimized for broad market applications, asset-specific calibration may enhance performance. Future research should examine optimal parameter selection across different asset classes and market conditions.

### 7.2 Market Microstructure Considerations

RAMO's effectiveness may vary across different market microstructure environments. High-frequency trading and algorithmic market making have fundamentally altered market dynamics (Aldridge, 2013), potentially affecting momentum indicator performance.

### 7.3 Transaction Cost Integration

Future enhancements could incorporate transaction cost analysis to provide net-return-based signals, addressing the implementation shortfall documented in practical momentum strategy applications (Korajczyk & Sadka, 2004).

## References

Aldridge, I. (2013). *High-Frequency Trading: A Practical Guide to Algorithmic Strategies and Trading Systems*. 2nd ed. Hoboken, NJ: John Wiley & Sons.

Ang, A. (2014). *Asset Management: A Systematic Approach to Factor Investing*. New York: Oxford University Press.

Arms, R. W. (1989). *The Arms Index (TRIN): An Introduction to the Volume Analysis of Stock and Bond Markets*. Homewood, IL: Dow Jones-Irwin.

Asness, C. S., Moskowitz, T. J., & Pedersen, L. H. (2013). Value and momentum everywhere. *Journal of Finance*, 68(3), 929-985.

Barroso, P., & Santa-Clara, P. (2015). Momentum has its moments. *Journal of Financial Economics*, 116(1), 111-120.

Bollinger, J. (1992). *Bollinger on Bollinger Bands*. New York: McGraw-Hill.

Brock, W., Lakonishok, J., & LeBaron, B. (1992). Simple technical trading rules and the stochastic properties of stock returns. *Journal of Finance*, 47(5), 1731-1764.

Calmar, T. (1991). The Calmar ratio: A smoother tool. *Futures*, 20(1), 40.

Campbell, J. Y., Lo, A. W., & MacKinlay, A. C. (1997). *The Econometrics of Financial Markets*. Princeton, NJ: Princeton University Press.

Chekhlov, A., Uryasev, S., & Zabarankin, M. (2005). Drawdown measure in portfolio optimization. *International Journal of Theoretical and Applied Finance*, 8(1), 13-58.

Daniel, K., & Moskowitz, T. J. (2016). Momentum crashes. *Journal of Financial Economics*, 122(2), 221-247.

Fama, E. F., & French, K. R. (1996). Multifactor explanations of asset pricing anomalies. *Journal of Finance*, 51(1), 55-84.

Granville, J. E. (1963). *Granville's New Key to Stock Market Profits*. Englewood Cliffs, NJ: Prentice-Hall.

Guidolin, M. (2011). Markov switching models in empirical finance. In D. N. Drukker (Ed.), *Missing Data Methods: Time-Series Methods and Applications* (pp. 1-86). Bingley: Emerald Group Publishing.

Hamilton, J. D. (1989). A new approach to the economic analysis of nonstationary time series and the business cycle. *Econometrica*, 57(2), 357-384.

Jegadeesh, N., & Titman, S. (1993). Returns to buying winners and selling losers: Implications for stock market efficiency. *Journal of Finance*, 48(1), 65-91.

Kahneman, D., & Tversky, A. (1979). Prospect theory: An analysis of decision under risk. *Econometrica*, 47(2), 263-291.

Kaufman, P. J. (1995). *Smarter Trading: Improving Performance in Changing Markets*. New York: McGraw-Hill.

Korajczyk, R. A., & Sadka, R. (2004). Are momentum profits robust to trading costs? *Journal of Finance*, 59(3), 1039-1082.

Leland, H. E. (1980). Who should buy portfolio insurance? *Journal of Finance*, 35(2), 581-594.

Lo, A. W., Mamaysky, H., & Wang, J. (2000). Foundations of technical analysis: Computational algorithms, statistical inference, and empirical implementation. *Journal of Finance*, 55(4), 1705-1765.

Markowitz, H. (1952). Portfolio selection. *Journal of Finance*, 7(1), 77-91.

Murphy, J. J. (1999). *Technical Analysis of the Financial Markets: A Comprehensive Guide to Trading Methods and Applications*. New York: New York Institute of Finance.

Prechter, R. R., & Frost, A. J. (1978). *Elliott Wave Principle: Key to Market Behavior*. Gainesville, GA: New Classics Library.

Pring, M. J. (2002). *Technical Analysis Explained: The Successful Investor's Guide to Spotting Investment Trends and Turning Points*. 4th ed. New York: McGraw-Hill.

Roncalli, T. (2013). *Introduction to Risk Parity and Budgeting*. Boca Raton, FL: CRC Press.

Shefrin, H., & Statman, M. (1985). The disposition to sell winners too early and ride losers too long: Theory and evidence. *Journal of Finance*, 40(3), 777-790.

Taleb, N. N. (2007). *The Black Swan: The Impact of the Highly Improbable*. New York: Random House.

Taylor, M. P., & Allen, H. (1992). The use of technical analysis in the foreign exchange market. *Journal of International Money and Finance*, 11(3), 304-314.

Treadway, A. B. (1969). On rational entrepreneurial behavior and the demand for investment. *Review of Economic Studies*, 36(2), 227-239.

Wilder, J. W. (1978). *New Concepts in Technical Trading Systems*. Greensboro, NC: Trend Research.

Money Risk Management with Trade Tracking

Overview

The Money Risk Management with Trade Tracking indicator is a powerful tool designed for traders on TradingView to simplify trade simulation and risk management. Unlike the TradingView Strategy Tester, which can be complex for beginners, this indicator provides an intuitive, beginner-friendly interface to evaluate trading strategies in a realistic manner, mirroring real-world trading conditions.

Built on the foundation of open-source contributions from LuxAlgo and TCP, this indicator integrates external indicator signals, overlays take-profit (TP) and stop-loss (SL) levels, and provides detailed money management analytics. It empowers traders to visualize potential profits, losses, and risk-reward ratios, making it easier to understand the financial outcomes of their strategies.

Key Features

Signal Integration: Seamlessly integrates with external long and short signals from other indicators, allowing traders to overlay TP/SL levels based on their preferred strategies.

Realistic Trade Simulation: Simulates trades as they would occur in real-world scenarios, accounting for initial capital, risk percentage, leverage, and compounding effects.

Money Management Dashboard: Displays critical metrics such as current capital, unrealized P&L, risk amount, potential profit, risk-reward ratio, and trade status in a customizable, beginner-friendly table.

TP/SL Visualization: Plots TP and SL levels on the chart with customizable styles (solid, dashed, dotted) and colors, along with optional labels for clarity.

Performance Tracking: Tracks total trades, win/loss counts, win rate, and profit factor, providing a clear overview of strategy performance.

Liquidation Risk Alerts: Warns traders if stop-loss levels risk liquidation based on leverage settings, enhancing risk awareness.

Benefits for Traders

Beginner-Friendly: Simplifies the complexities of the TradingView Strategy Tester, offering an intuitive interface for new traders to simulate and evaluate trades without confusion.

Real-World Insights: Helps traders understand the actual profit or loss potential of their strategies by factoring in capital, risk, and leverage, bridging the gap between theoretical backtesting and real-world execution.

Enhanced Decision-Making: Provides clear, real-time analytics on risk-reward ratios, unrealized P&L, and trade performance, enabling informed trading decisions.

Customizable and Flexible: Allows customization of TP/SL settings, table positions, colors, and sizes, catering to individual trader preferences.

Risk Management Focus: Encourages disciplined trading by highlighting risk amounts, potential profits, and liquidation risks, fostering better financial planning.

Why This Indicator Stands Out

Many traders struggle to translate backtested strategy results into real-world outcomes due to the abstract nature of percentage-based profitability metrics. This indicator addresses that challenge by providing a practical, user-friendly tool that simulates trades with real-world parameters like capital, leverage, and compounding. Its open-source nature ensures accessibility, while its integration with other indicators makes it versatile for various trading styles.

How to Use

Add to TradingView: Copy the Pine Script code into TradingView’s Pine Editor and add it to your chart.

Configure Inputs: Set your initial capital, risk percentage, leverage, and TP/SL values in the indicator settings. Select external long/short signal sources if integrating with other indicators.

Monitor Dashboards: Use the Money Management and Target Dashboard tables to track trade performance and risk metrics in real time.

Analyze Results: Review win rates, profit factors, and P&L to refine your trading strategy.

Credits

This indicator builds upon the open-source contributions of LuxAlgo and TCP , whose efforts in sharing their code have made this tool possible. Their dedication to the trading community is deeply appreciated.

The LEAP Contest - Symbol & Max Position Table TrackerDescription:

This indicator tracks the maximum contracts allowed to be traded for TradingView’s *"The Leap"* Contest. It displays a horizontal table at the bottom right of your chart showing up to 20 symbols along with their maximum allowable open contract positions.

Use case:

Designed specifically for traders participating in *The Leap* Contest on TradingView.

Users need to enter the symbol and the maximum contracts allowed for that symbol in the settings menu for each new contest.

It provides a quick reference to ensure compliance with contest rules on maximum position sizes.

How it works:

The table shows two rows: the top row displays the symbol name, and the bottom row shows the max contract limit.

If the currently loaded chart symbol matches any symbol in the list, its text color changes to yellow .

Customization:

Symbols and limits must be updated in the indicator’s settings before each contest to reflect the current rules.

PCA Regime-Adjusted MomentumSummary

The PCA Regime-Adjusted Momentum (PCA-RAM) is an advanced market analysis tool designed to provide nuanced insights into market momentum and structural stability. It moves beyond traditional indicators by using Principal Component Analysis (PCA) to deconstruct market data into its most essential patterns.

The indicator provides two key pieces of information:

A smoothed momentum signal based on the market's dominant underlying trend.

A dynamic regime filter that gauges the stability and clarity of the market's structure, advising you when to trust or fade the momentum signals.

This allows traders to not only identify potential shifts in momentum but also to understand the context and confidence behind those signals.

Core Concepts & Methodology

The strength of this indicator lies in its sound, data-driven methodology.

1. Principal Component Analysis (PCA)

At its core, the indicator analyzes a rolling window (default 50 periods) of standardized market data (Open, High, Low, Close, and Volume). PCA is a powerful statistical technique that distills this complex, 5-dimensional data into its fundamental, uncorrelated components of variance. We focus on the First Principal Component (PC1), which represents the single most dominant pattern or "theme" driving the market's behavior in the lookback window.

2. The Momentum Signal

Instead of just looking at price, we project the current market data onto this dominant underlying pattern (PC1). This gives us a raw "projection score" that measures how strongly the current bar aligns with the historically dominant market structure. This raw score is then smoothed using two an exponential moving averages (a fast and a slow line) to create a clear, actionable momentum signal, similar in concept to a MACD.

3. The Dynamic Regime Filter

This is arguably the indicator's most powerful feature. It answers the question: "How clear is the current market picture?"

It calculates the Market Concentration Ratio, which is the percentage of total market variance explained by PC1 alone.

A high ratio indicates that the market is moving in a simple, one-dimensional way (e.g., a clear, strong trend).

A low ratio indicates the market is complex, multi-dimensional, and choppy, with no single dominant theme.

Crucially, this filter is dynamic. It compares the current concentration ratio to its own recent average, allowing it to adapt to any asset or timeframe. It automatically learns what "normal" and "choppy" look like for the specific chart you are viewing.

How to Interpret the Indicator

The indicator is displayed in a separate pane with two key visual elements:

The Momentum Lines (White & Gold)

White Line: The "Fast Line," representing the current momentum.

Gold Line: The "Slow Line," acting as the trend confirmation.

Bullish Signal: A crossover of the White Line above the Gold Line suggests a shift to positive momentum.

Bearish Signal: A crossover of the White Line below the Gold Line suggests a shift to negative momentum.

The Regime Filter (Purple & Dark Red Background)

This is your confidence gauge.

Navy Blue Background (High Concentration): The market structure is stable, simple, and trending. Momentum signals are more reliable and should be given higher priority.

Dark Red Background (Low Concentration): The market structure is complex, choppy, or directionless. Momentum signals are unreliable and prone to failure or "whipsaws." This is a signal to be cautious, tighten stops, or potentially stay out of the market.

Potential Trading Strategies

This tool is versatile and can be used in several ways:

1. Primary Signal Strategy

Condition: Wait for the background to turn Purple, confirming a stable, high-confidence regime.

Entry: Take the next crossover signal from the momentum lines (White over Gold for long, White under Gold for short).

Exit/Filter: Consider exiting positions or ignoring new signals when the background turns Navy.

2. As a Confirmation or Filter for Your Existing Strategy

Do you have a trend-following system? Only enable its long and short signals when the PCA-RAM background is Purple.

Do you have a range-trading or mean-reversion system? It might be most effective when the PCA-RAM background is Navy, indicating a lack of a clear trend.

3. Advanced Divergence Analysis

Look for classic divergences between price and the momentum lines. For example, if the price is making a new high, but the Gold Line is making a lower high, it may indicate underlying weakness in the trend, even on a Purple background. This divergence signal is more powerful because it shows that the new price high is not being confirmed by the market's dominant underlying pattern.

Correlation MA – 15 Assets + Average (Optional)This indicator calculates the moving average of the correlation coefficient between your charted asset and up to 15 user-selected symbols. It helps identify uncorrelated or inversely correlated assets for diversification, pair trading, or hedging.

Features:

✅ Compare your current chart against up to 15 assets

✅ Toggle assets on/off individually

✅ Custom correlation and MA lengths

✅ Real-time average correlation line across enabled assets

✅ Horizontal lines at +1, 0, and -1 for easy visual reference

Ideal for:

Portfolio diversification analysis

Finding low-correlation stocks

Mean-reversion & pair trading setups

Crypto, equities, ETFs

To use: set the benchmark chart (e.g. TSLA), choose up to 15 assets, and adjust settings as needed. Look for assets with correlation near 0 or negative values for uncorrelated performance.

Dr Avinash Talele momentum indicaterTrend and Volatility Metrics

EMA10, EMA20, EMA50: