AsturRiskPanelIndicator Summary

ATR Engine

Length & Smoothing: Choose how many bars to use (default 14) and the smoothing method (RMA/SMA/EMA/WMA).

Median ATR: Computes a rolling median of ATR over a user-defined look-back (default 14) to derive a “scalp” target.

Scalp Target

Automatically set at ½ × median ATR, snapped to the nearest tick.

Optional rounding to whole points for simplicity.

Stop Calculation

ATR Multiplier: Scales current ATR by a user input (default 1.5) to produce your stop distance in points (and ticks when appropriate).

Distortion Handling: Switches between point-only and point + tick displays based on contract specifications.

Risk & Sizing

Risk % of account per trade (default 2 %).

Calculates dollar risk per contract and optimal contract count.

Displays all metrics (scalp, stop, risk/contract, max contracts, max risk, account size) in a customizable on-chart table.

ATR-Based Stop Placement Guidelines

Trade Context ATR Multiplier Notes

Tight Range Entry 1.0 × ATR High-conviction, precise entries. Expect more shake-outs.

Standard Trend Entry 1.5 × ATR Balanced for H2/L2, MTR, DT/DB entries.

Breakouts/Microchannels 2.0 × ATR Wide stops through chop—Brooks-style breathing room.

How to Use

Select ATR Settings

Pick an ATR length (e.g. 14) and smoothing (RMA for stability).

Adjust the median length if you want a faster/slower scalp line.

Align Multiplier with Your Setup

For tight-range entries, set ATR Multiplier ≈ 1.0.

For standard trend trades, leave at 1.5.

For breakout/pullback setups, increase to 2.0 or more.

Customize Risk Parameters

Enter your account size and desired risk % per trade (e.g. 2 %).

The table auto-calculates how many contracts you can take.

Read the On-Chart Table

Scalp shows your intraday target.

Stop gives Brooks-style stop distance in points (and ticks).

Risk/Contract is the dollar risk per contract.

Max Contracts tells you maximum position size.

Max Risk confirms total dollar exposure.

Visual Confirmation

Place your entry, then eyeball the scalp and stop levels against chart structure (e.g. swing highs/lows).

Adjust the ATR multiplier if market context shifts (e.g. volatility spikes).

By blending this sizing panel with contextual ATR multipliers, you’ll consistently give your trades the right amount of “breathing room” while keeping risk in check.

Portfolio management

Profit Guard ProProfitGuard Pro

ProfitGuard Pro is a risk management and profit calculation tool that helps traders optimize their trades by handling position sizing, risk management, leverage, and take profit calculations. With support for both cumulative and non-cumulative take profit strategies, this versatile indicator provides the insights you need to maximize your trading strategy.

How to Use ProfitGuard Pro:

Load the Indicator: Add ProfitGuard Pro to your chart in TradingView.

Set Your Entry Position: Input your desired entry price.

Define Your Stop Loss: Enter the price at which your trade will exit to minimize losses.

Add Take Profit Levels: Input your TP1, TP2, TP3, and TP4 levels, as needed.

If you want fewer take profit levels, adjust the number of TPs in the settings menu. You can choose between 1 to 4 take profit levels based on your strategy.

Adjust Risk Settings: Specify your account size and risk percentage to calculate position size and leverage.

Choose Cumulative or Non-Cumulative Mode: Toggle cumulative profit mode to either recalculate position sizes as each take profit is hit or keep position sizes static for each TP.

Once set up, ProfitGuard Pro will automatically calculate your position size, leverage, and potential profits for each take profit level, providing a clear visual on your chart to guide your trading decisions.

Key Features:

Risk Management:

Calculate your risk percentage based on account size and stop loss.

Visualize risk in dollar terms and percentage of your account.

Position Size & Leverage:

Automatically calculate the ideal position size and leverage for your trade based on your entry, stop loss, and risk settings.

Ensure you are trading with the appropriate leverage for your account size.

Cumulative vs Non-Cumulative Profit Mode:

Cumulative Mode: Adjusts position size after each take profit is reached, recalculating for remaining contracts.

Non-Cumulative Mode: Treats each take profit as a separate calculation using the full position size.

Take Profit Levels:

Set up to 4 customizable take profit levels.

Adjust percentage values for each TP target, and visualize them on your chart with easy-to-read lines.

Profit Calculation:

Displays potential profits for each take profit level based on whether cumulative or non-cumulative mode is selected.

Calculate your risk-reward ratio dynamically at each TP.

Customizable Visuals:

Easily customize the table's size, position, and color scheme to fit your chart.

Visualize key trade details like leverage, contracts, margin, and profits directly on your chart.

Short and Long Position Support:

Automatically adjusts calculations based on whether you're trading long or short.

Value at Risk (VaR/CVaR) - Stop Loss ToolThis script calculates Value at Risk (VaR) and Conditional Value at Risk (CVaR) over a configurable T-bar forward horizon, based on historical T-bar log returns. It plots projected price thresholds that reflect the worst X% of historical return outcomes, helping set statistically grounded stop-loss levels.

A 95% 5-day VaR of −3% means: “In the worst 5% of all historical 5-day periods, losses were 3% or more.” If you're bullish, and your thesis is correct, price should not behave like one of those worst-case scenarios. So if the market starts trading below that 5-day VaR level, it may indicate that your long bias is invalidated, and a stop-loss near that level can help protect against further downside consistent with tail-risk behavior.

How it's different:

Unlike ATR or standard deviation-based methods, which measure recent volatility magnitude, VaR/CVaR incorporate both the magnitude and **likelihood** (5% chance for example) of adverse moves. This makes it better suited for risk-aware position sizing and exits grounded in actual historical return distributions.

How to use for stop placement:

- Set your holding horizon (T) and confidence level (e.g., 95%) in the inputs.

- The script plots a price level below which only the worst 5% (or chosen %) of T-bar returns have historically occurred (VaR).

- If price approaches or breaches the VaR line, your bullish/bearish thesis may be invalidated.

- CVaR gives a deeper threshold: the average loss **if** things go worse than VaR — useful for a secondary or emergency stop.

FURTHER NOTES FROM SOURCE CODE:

//======================================================================//

// If you're bullish (expecting the price to go up), then under normal circumstances, prices should not behave like they do on the worst-case days.

// If they are — you're probably wrong, or something unexpected is happening. Basically, returns shouldn't be exhibiting downside tail-like behavior if you're bullish.

// VaR(95%, T) gives the threshold below which the price falls only 5% of the time historically, over T days/bars and considering N historical samples.

// CVaR tells you the expected/average price level if that adverse move continues

// Caveats:

// For a variety of reasons, VaR underestimates volatility, despite using historical returns directly rather than making normality assumptions

// as is the case with the standard historicalvol/bollinger band/stdev/ATR approaches)

// Volatility begets volatility (volatility clustering), and VaR is not a conditional probability on recent volatility so it likely underestimates the true volatility of an adverse event

// Regieme shifts occur (bullish phase after prolonged bearish behavior), so upside/short VaR would underestimate the best-case days in the beginning of that move, depending on lookahead horizon/sampling period

// News/events happen, and maybe your sampling period doesn't contain enough event-driven returns to form reliable stats

// In general of course, this tool assumes past return distributions are reflective of forward risk (not the case in non-stationary time series)

// Thus, this tool is not predictive — it shows historical tail risk, not guaranteed outcomes.

// Also, when forming log-returns, overlapping windows of returns are used (to get more samples), but this introduces autocorrelation (if it wasn't there already). This means again, the true VaR is underestimated.

// Description:

// This script calculates and plots both Value at Risk (VaR) and

// Conditional Value at Risk (CVaR) for a given confidence level, using

// historical log returns. It computes both long-side (left tail) and

// short-side (right tail) risk, and converts them into price thresholds (red and green lines respectively).

//

// Key Concepts:

// - VaR: "There is a 95% chance the loss will be less than this value over T days. Represents the 95th-percentile worst empirical returns observed in the sampling period, over T bars.

// - CVaR: "Given that the loss exceeds the VaR, the average of those worst 5% losses is this value. (blue line)" Expected tail loss. If the worst case breached, how bad can it get on average

// - For shorts, the script computes the mirror (right-tail) equivalents.

// - Use T-day log returns if estimating risk over multiple days forward.

// - You can see instances where the VaR for time T, was surpassed historically with the "backtest" boolean

//

// Usage for Stop-Loss:

// - LONG POSITIONS:

// • 95th percentile means, 5% of the time (1 in 20 times) you'd expect to get a VaR level loss (touch the red line), over the next T bars.

// • VaR threshold = minimum price expected with (1 – confidence)% chance.

// • CVaR threshold = expected price if that worst-case zone is breached.

// → Use as potential stop-loss (VaR) or disaster stop (CVaR). If you're bullish (and you're right), price should not be exhibiting returns consistent with the worst 5% of days/T_bars historically.

//======================================================================//

1A Monthly P&L Table - Using Library1A Monthly P&L Table: Track Your Performance Month-by-Month

Overview:

The 1A Monthly P&L Table is a straightforward yet powerful indicator designed to give you an immediate overview of your asset's (or strategy's) percentage performance on a monthly basis. Displayed conveniently in the bottom-right corner of your chart, this tool helps you quickly assess historical gains and losses, making it easier to analyze trends in performance over time.

Key Features:

Monthly Performance at a Glance: Clearly see the percentage change for each past month.

Cumulative P&L: A running total of the displayed monthly P&L is provided, giving you a quick sum of performance over the selected period.

Customizable Display:

Months to Display: Choose how many past months you want to see in the table (from 1 to 60 months).

Text Size: Adjust the text size (Tiny, Small, Normal, Large, Huge) to fit your viewing preferences.

Text Color: Customize the color of the text for better visibility against your chart background.

Intraday & Daily Compatibility: The table is optimized to display on daily and intraday timeframes, ensuring it's relevant for various trading styles. (Note: For very long-term analysis on weekly/monthly charts, you might consider other tools, as this focuses on granular monthly P&L.)

How It Works:

The indicator calculates the percentage change from the close of the previous month to the close of the current month. For the very first month displayed, it calculates the P&L from the opening price of the chart's first bar to the close of that month. This data is then neatly organized into a table, updated on the last bar of the day or session.

Ideal For:

Traders and investors who want a quick, visual summary of monthly performance.

Analyzing seasonal trends or consistent periods of profitability/drawdown.

Supplementing backtesting results with a clear month-by-month breakdown.

Settings:

Text Color: Changes the color of all text within the table.

Text Size: Controls the font size of the table content.

Months to Display: Determines the number of recent months included in the table.

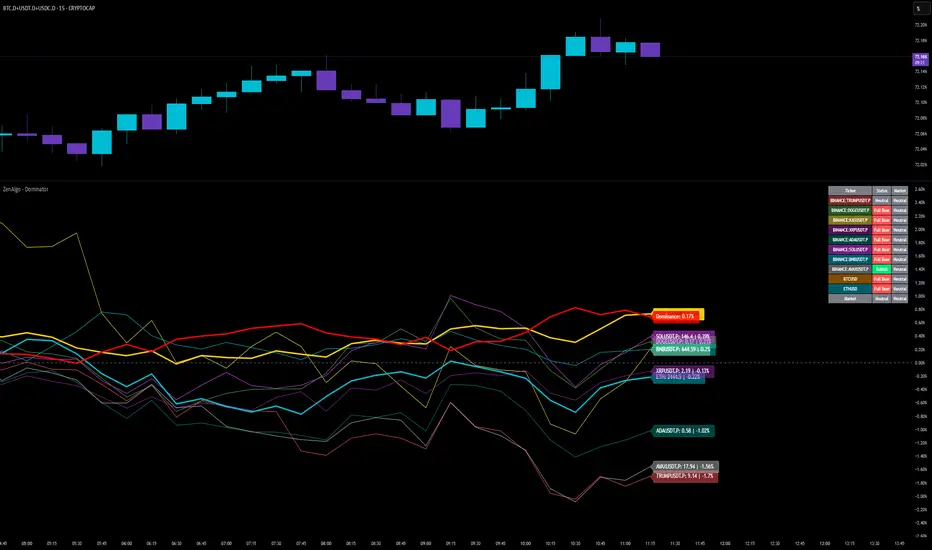

ZenAlgo - DominatorThis indicator provides a structured multi-ticker overview of market momentum and relative strength by analyzing short-term price behavior across selected assets in comparison with broader crypto dominance and Bitcoin/ETH performance.

Ticker and Market Data Handling

The script accepts up to 9 user-defined symbols (tickers) along with BTCUSD and ETHUSD. For each symbol:

It retrieves the current price.

It also requests the daily opening price from the "D" timeframe to compute intraday percentage change.

For BTC, ETH, and dominance (sum of BTC, USDT, and USDC dominance), daily change is calculated using this same method.

This comparison enables tracking relative performance from the daily open, which provides meaningful insight into intraday strength or weakness among different assets.

Dominance Logic

The indicator aggregates dominance data from BTC , USDT , and USDC using TradingView’s CRYPTOCAP indices. This combined dominance is used as a reference in directional and status calculations. ETH dominance is also analyzed independently.

Changes in dominance are used to infer whether market attention is shifting toward Bitcoin/stablecoins (typically indicating risk-off sentiment) or away from them (typically risk-on behavior, benefiting altcoins).

Price Direction Estimation

The script estimates directional bias using an EMA-based deviation technique:

A short EMA (user-defined lookback , default 4 bars) is calculated.

The current close is compared to the EMA to assess directional bias.

Recent candle changes are also inspected to confirm a consistent short-term trend (e.g., 3 consecutive higher closes for "up").

A small threshold is used to avoid classifying flat movements as trends.

This directionality logic is applied separately to:

The selected ticker's price

BTC price

Combined dominance

This allows the script to contextualize the movement of each asset within broader market conditions.

Market Status Evaluation

A custom function analyzes ETH and BTC dominance trends along with their relative strength to define the overall market regime:

Altseason is identified when BTC dominance is declining, ETH dominance rising, and ETH outperforms BTC.

BTC Season occurs when BTC dominance is rising, ETH dominance falling, and BTC outperforms ETH.

If neither condition is met, the state is Neutral .

This classification is shown alongside each ticker's row in the table and helps traders assess whether market conditions favor Bitcoin, Ethereum, or altcoins in general.

Ticker Status Classification

Each ticker is analyzed independently using the earlier directional logic. Its status is then determined as follows:

Full Bull : Ticker is trending up while dominance is declining or BTC is also rising.

Bullish : Ticker is trending up but not supported by broader bullish context.

Bearish : Ticker is trending down but without broader confirmation.

Full Bear : Ticker is trending down while dominance rises or BTC falls.

Neutral : No strong directional bias or conflicting context.

This classification reflects short-term momentum and macro alignment and is color-coded in the results table.

Table Display and Plotting

A configurable table is shown on the chart, which:

Displays the name and status of each selected ticker.

Optionally includes BTC, ETH, and market state.

Uses color-coding for intuitive interpretation.

Additionally, price changes from the daily open are plotted for each selected ticker, BTC, ETH, and combined dominance. These values are also labeled directly on the chart.

Labeling and UX Enhancements

Labels next to the current candle display price and percent change for each active ticker and for BTC, ETH, and combined dominance.

Labels update each bar, and old labels are deleted to avoid clutter.

Ticker names are dynamically shortened by stripping exchange prefixes.

How to Use This Indicator

This tool helps traders:

Spot early rotations between Bitcoin and altcoins.

Identify intraday momentum leaders or laggards.

Monitor which tickers align with or diverge from broader market trends.

Detect possible sentiment shifts based on dominance trends.

It is best used on lower to mid timeframes (15m–4h) to capture intraday to short-term shifts. Users should cross-reference with longer-term trend tools or structural indicators when making directional decisions.

Interpretation of Values

% Change : Measures intraday move from daily open. Strong positive/negative values may indicate breakouts or reversals.

Status : Describes directional strength relative to market conditions.

Market State : Gives a general bias toward BTC dominance, ETH strength, or altcoin momentum.

Limitations & Considerations

The indicator does not analyze liquidity or volume directly.

All logic is based on short-term movements and may produce false signals in ranging or low-volume environments.

Dominance calculations rely on external CRYPTOCAP indices, which may differ from exchange-specific flows.

Added Value Over Other Free Tools

Unlike basic % change tables or price overlays, this indicator:

Integrates dominance-based macro context into ticker evaluation.

Dynamically classifies market regimes (BTC season / Altseason).

Uses multi-factor logic to determine ticker bias, avoiding single-metric interpretation.

Displays consolidated information in a table and chart overlays for rapid assessment.

Crypto Portfolio vs BTC – Custom Blend TrackerThis tool tracks the performance of a custom-weighted crypto portfolio (SUI, BTC, SOL, DEEP, DOGE, LOFI, and Other) against BTC. Simply input your start date to anchor performance and compare your basket’s relative strength over time. Ideal for portfolio benchmarking, alt-season tracking, or macro trend validation.

Supports all timeframes. Based on BTC-relative returns (not USD). Open-source and customizable.

Risk Calculator PRO — manual lot size + auto lot-suggestionWhy risk management?

90 % of traders blow up because they size positions emotionally. This tool forces Risk-First Thinking: choose the amount you’re willing to lose, and the script reverse-engineers everything else.

Key features

1. Manual or Market Entry – click “Use current price” or type a custom entry.

2. Setup-based ₹-Risk – four presets (A/B/C/D). Edit to your workflow.

3. Lot-Size Input + Auto Lot Suggestion – you tell the contract size ⇒ script tells you how many lots.

4. Auto-SL (optional) – tick to push stop-loss to exactly 1-lot risk.

5. Instant Targets – 1 : 2, 1 : 3, 1 : 4, 1 : 5 plotted and alert-ready.

6. P&L Preview – table shows potential profit at each R-multiple plus real ₹ at SL.

7. Margin Column – enter per-lot margin once; script totals it for any size.

8. Clean Table UI – dark/light friendly; updates every 5 bars.

9. Alert Pack – SL, each target, plus copy-paste journal line on the chart.

How to use

1. Add to chart > “Format”.

2. Type the lot size for the symbol (e.g., 1250 for Natural Gas, 1 for cash equity).

3. Pick Side (Buy / Sell) & Setup grade.

4. ✅ If you want the script to place SL for you, tick Auto-SL (risk = 1 lot).

5. Otherwise type your own Stop-loss.

6. Read the table:

• Suggested lots = how many to trade so risk ≤ setup ₹.

• Risk (currency) = real money lost if SL hits.

7. Set TradingView alerts on the built-in conditions (T1_2, SL_hit, etc.) if you’d like push / email.

8. Copy the orange CSV label to Excel / Sheets for journalling.

Best practices

• Never raise risk to “fit” a trade. Lower size instead.

• Review win-rate vs. R multiple monthly; adjust setups A–D accordingly.

• Test Auto-SL in replay before going live.

Disclaimer

This script is educational. Past performance ≠ future results. The author isn’t responsible for trading losses.

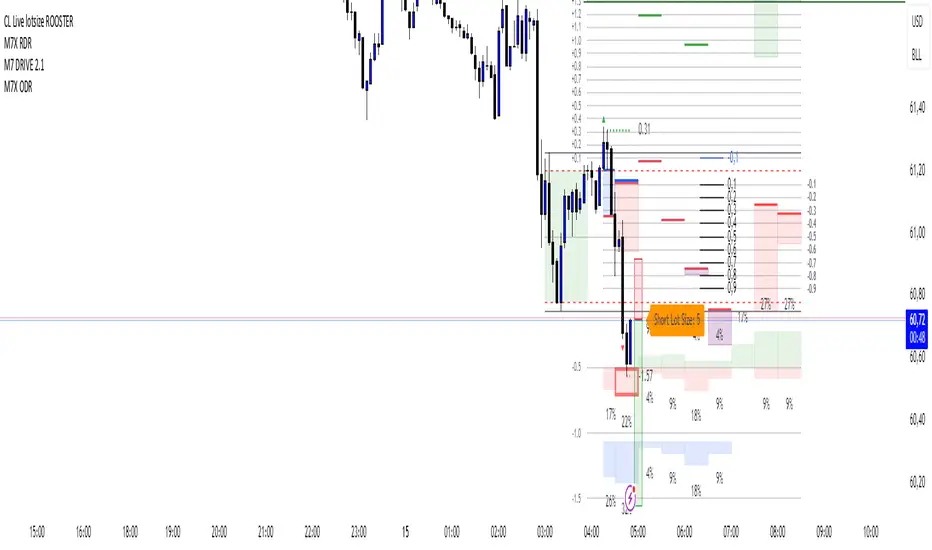

CL Live lotsize ROOSTER📄 Description:

This is a utility script designed for manual futures traders who enter with market orders and want to size their positions precisely based on $ risk.

⚙️ Features:

✅ Calculates live contract size based on:

A fixed dollar risk amount (e.g. $100)

A manually set static stop-loss price

The live market price as your entry

✅ Uses a configurable risk-reward ratio (e.g. 1:3)

✅ Plots entry, stop, and target levels on the chart

✅ Displays calculated contract size as a floating label

🎯 Why this tool?

Built to support fast execution workflows , this tool helps traders who:

Enter trades at candle close or open

Want to pre-calculate their market order size before the signal

Prefer a visual, consistent, real-time R:R validation system

Avoid fumbling with the long/short position tool at the last second

🔧 Settings:

Static Stop-Loss Price: Enter the price level where you'd place your SL

Account Risk ($): How much you’re willing to risk per trade

Risk-Reward Ratio: Set your target multiplier (e.g. 3 for 3R)

PORTFOLIO TABLE Full [Titans_Invest]PORTFOLIO TABLE Full

This is a complete table for monitoring your assets or cryptocurrencies in your SPOT wallet without needing to access your broker’s website or app.

⯁ HOW TO USE THIS TABLE❓

Simply select the asset and enter the amount you hold.

The table will display the value of each asset and the total value of your portfolio.

You can monitor up to 19 assets in real time.

⯁ CONVERT VALUES

You can also enable and select a currency for conversion.

For example, cryptocurrencies are calculated in US dollars by default, but you can choose euros as the conversion currency.

The values originally in dollars will then be displayed in euros.

⯁ TRACK THE DAILY VARIATION OF YOUR PORTFOLIO

You’ll be able to monitor your portfolio’s raw daily variation in real time.

🔶 Track your Portfolio in real time:

🔶 Add your local Currency to Convert Values:

🔶 Follow your Portfolio Live:

___________________________________________________________

📜 SCRIPT : PORTFOLIO TABLE Full

🎴 Art by : @Titans_Invest & @DiFlip

👨💻 Dev by : @Titans_Invest & @DiFlip

🎑 Titans Invest — The Wizards Without Gloves 🧤

✨ Enjoy!

___________________________________________________________

o Mission 🗺

• Inspire Traders to manifest Magic in the Market.

o Vision 𐓏

• To elevate collective Energy 𐓷𐓏

Position Size Calculator (Fixed % or ATR-based Stop Support)Position Size Calculator (Fixed % or ATR-based Stop Support)

Purpose and Background

This indicator allows traders to calculate appropriate position sizes directly on the chart, based on a key rule:

“What percentage of your capital are you willing to risk per trade?”

While many traders focus on entries and indicators, position sizing and risk allocation are often overlooked.

This tool visualizes and simplifies the “1% risk rule” promoted by IBD (Investor’s Business Daily) and William J. O’Neil, helping both beginners and experienced traders maintain disciplined capital management.

Key Features

Automatically calculates and displays:

・ Position Size

The number of units (shares, contracts, coins) you can hold based on your stop-loss range and risk allowance.

・ Stop Price

The price level at which your stop-loss would be triggered.

・ Risk Amount

The maximum loss per trade based on your portfolio size and risk percentage.

Two stop-loss modes available:

・ Fixed % Mode

O’Neil suggests using up to 8% stop-loss in uptrends and keeping it tighter (around 4%) in corrections. This mode allows flexible manual settings.

・ ATR-Based Mode

Uses the asset’s average volatility to dynamically calculate stop-loss width using the Average True Range (ATR).

ATR Usage and Recommended Settings

ATR helps you avoid noise-based stop-outs and align your risk with market volatility.

There are two parameters you can adjust:

・ ATR Length

Defines how many bars are used to calculate the average range.

・Shorter values (5–10) respond faster for day trades

・Longer values (14–21) offer smoother ranges for swing/position trades(Default is 14)

・ATR Multiplier

Sets how wide the stop-loss is by multiplying the ATR value:

・Day trading: 1.0–1.5×

・Swing trading: 1.5–2.5×

・Position trading: 2.0–3.0×

Practical Examples: Risk % × Stop-Loss % → Max Positions

This tool helps estimate how many positions you can hold in a portfolio based on your risk per trade and stop width.

Examples:

・Risk 0.5%, Stop 8% → Max 16 positions

・Risk 0.5%, Stop 4% → Max 8 positions

・Risk 1.0%, Stop 8% → Max 8 positions

・Risk 1.0%, Stop 4% → Max 4 positions

・Risk 2.0%, Stop 8% → Max 4 positions

・Risk 2.0%, Stop 4% → Max 2 positions

These assume worst-case scenarios where all positions are stopped out simultaneously within your overall portfolio risk limit.

Display & Customization Options

・ Currency Display: USD or JPY

No currency conversion is applied. Select based on your trading region (e.g., USD for U.S. stocks, JPY for Japanese stocks).

Support for additional currencies can be added upon request.

・ Show/Hide Decimal Places

Toggle decimals for better visibility. Ideal for fractional assets like crypto and CFDs.

・ Position of Output

Choose from top-right, middle-right, or bottom-right on the chart.

・ Text Display Size: Large / Normal / Small

Choose the table size that best suits your viewing preferences.

・ Explanation of Displayed Labels

・ Position Size : Units to buy/sell based on risk

・ Stop Price : Price where stop-loss is triggered

・ Risk Amount : Max loss allowed for the trade

How to Use

1、Set your Portfolio Size

2、Choose your Currency (USD or JPY)

3、Input Risk per Trade (%) (e.g., 1%)

4、Select Stop Loss Method

・ Fixed % : Enter a manual stop-loss percent (e.g., 8%)

・ ATR : Then also enter:

・ ATR Length : Number of bars used to calculate ATR (e.g., 14)

・ ATR Multiplier : Factor applied to ATR to determine stop-loss (e.g., 2.0)

5、Adjust decimals, label position, or text size as needed

6、The result is displayed in a table directly on your chart

Notes

・ Uses the current close price (close) as the basis

Real-time bid/ask data isn't available in Pine Script, so the close price is used for consistent results.

・ No buy/sell signals are generated

This tool is for position sizing and risk calculation only, not trade entries.

Recommended For

・Traders who want precise, rule-based position sizing

・Users following IBD or O’Neil’s 1% risk principle

・Those incorporating ATR for stop-loss strategies

・Multi-asset traders (stocks, crypto, CFDs, etc.)

・ Anyone who wants to calculate position size and risk without using a calculator or external tool—fully inside TradingView

TCP | Money Management indicator | Crypto Version📌 TCP | Money Management Indicator | Crypto Version

A robust, multi-target risk and capital management indicator tailored for crypto traders. Whether you're trading spot, perpetual futures, or leverage tokens, this tool empowers you with precise control over risk, reward, and position sizing—directly on your chart. Eliminate guesswork and trade with confidence.

🔰 Introduction: Master Your Capital, Master Your Trades

Poor money management is the number one reason traders lose their accounts, even with solid strategies. The TCP Money Management Indicator, built by Trade City Pro (TCP), solves this problem by providing a structured, rule-based approach to capital allocation.

Want to dive deeper into the concept of money management? Check out our comprehensive tutorial on TradingView, " TradeCityPro Academy: Money Management ", to understand the principles that power this indicator and transform your trading mindset.

This indicator equips you to:

• Calculate optimal position sizes based on your capital, risk percentage, and leverage

• Set up to 5 customizable take-profit targets with partial close percentages

• Access real-time metrics like Risk-to-Reward (R/R), USD profit, and margin usage

• Trade with discipline, avoiding emotional or inconsistent decisions

💸 Money Management Formula

The indicator uses a professional capital allocation model:

Position Size = (Capital × Risk %) ÷ (Stop Loss % × Leverage)

From this, it calculates:

• Total risk amount in USD

• Optimal position size for your trade

• Margin required for each take-profit target

• Adjusted R/R for each target, accounting for partial position closures

🛠 How to Use

Enter Trade Parameters: Input your capital, risk %, leverage, entry price, and stop-loss price.

Set Take-Profit Targets: Enable 1 to 5 take-profit levels and specify the percentage of the position to close at each.

Real-Time Calculations: The indicator automatically computes:

• R/R ratio for each target

• Profit in USD for each partial close

• Margin used per target (in % and USD)

Visualize Your Trade:

• Price levels for entry, stop-loss, and take-profits are plotted on the chart.

• A dynamic info panel on the left side displays all key metrics.

🔄 Dynamic Adjustments: As each take-profit target is hit and a portion of the position is closed, the indicator recalculates the remaining position size, expected profit, R/R, and margin for subsequent targets. This ensures accuracy and reflects real-world trade behavior.

📊 Table Overview

The left-side panel provides a clear snapshot:

• Trade Setup: Capital, entry price, stop-loss, risk amount, and position size

• Per Target: Percentage closed, R/R, profit in USD, and margin used

• Summary: Total expected profit across all targets

⚙️ Settings Panel

• Total Capital ($): Your account size for the trade

• Risk per Trade (%): The percentage of capital you’re willing to risk

• Leverage: The leverage applied to the trade

• Entry/Stop-Loss Prices: Define your trade’s risk zone

• Take-Profit Targets (1–5): Set price levels and percentage to close at each

🔍 Use Case Example

Imagine you have $1,000 capital, risking 1%, using 10x leverage:

• Entry: $100 | Stop-Loss: $95

• TP1: $110 (close 50%) | TP2: $115 (close 50%)

The indicator calculates the exact position size, profit at each target, and margin allocation in real time, with all metrics displayed on the chart.

✅ Why Traders Love It

• Precision: No more manual calculations or guesswork

• Versatility: Works on all crypto pairs (BTC, ETH, altcoins, etc.)

• Flexibility: Perfect for scalping, swing trading, or futures strategies

• Universal: Compatible with all timeframes

• Transparency: Fully manual, with clear and reliable outputs

🧩 Built by Trade City Pro (TCP)

Developed by TCP, a trusted name in trading tools, used by over 150,000 traders worldwide. This indicator is coded in Pine Script v5, ensuring compatibility with TradingView’s platform.

🧾 Final Notes

• No Auto-Trading: This is a manual tool for disciplined traders

• No Repainting: All calculations are accurate and non-repainting

• Tested: Rigorously validated across major crypto pairs

• Publish-Ready: Built for seamless use on TradingView

🔗 Resources

• Money Management Tutorial: Learn the fundamentals of capital management with our detailed guide: TradeCityPro Academy: Money Management

• TradingView Profile: Explore more tools by TCP on TradingView

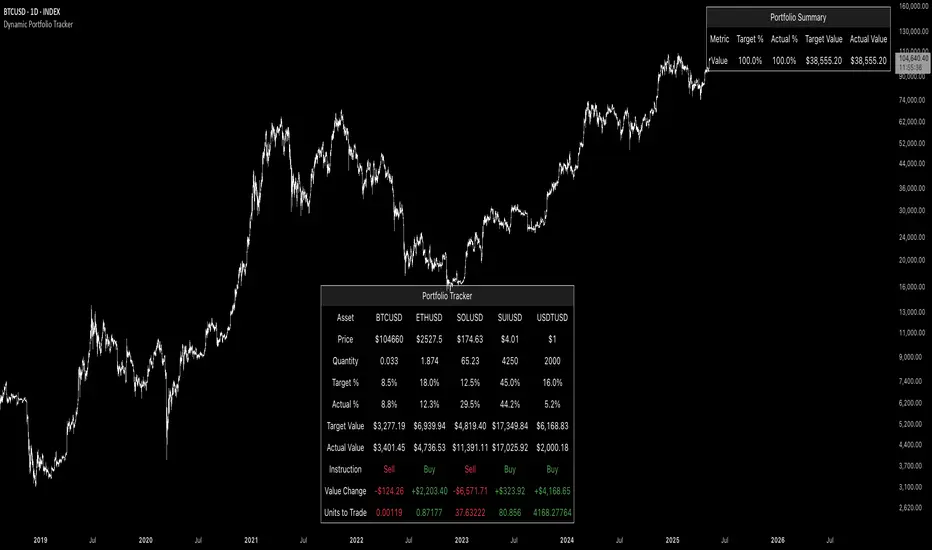

Dynamic Portfolio TrackerDynamic Portfolio Tracker

The Dynamic Portfolio Tracker is a visual tool for actively managing and monitoring a multi-asset portfolio directly on TradingView. It allows users to input up to 15 custom assets (with a default setup for 5), define how much of each asset they hold, and assign a target allocation percentage to each. The script then calculates live market prices, total portfolio value, current vs. target weightings, and provides clear, color-coded instructions on whether to buy, sell, or hold each asset. It displays all this data in an on-chart table, showing both the dollar amount and the quantity to adjust for each asset, helping users keep their portfolio aligned with their strategy in real time.

How to Use the Inputs (What Each Field Means)

1. Portfolio Assets (Tickers)

Fields: Asset 1 Ticker, Asset 2 Ticker, …, Asset 15 Ticker

What it does: Lets you select which assets (crypto, stocks, etc.) you want to track. These are live symbols pulled from TradingView.

2. Asset Quantities

Fields: Asset 1 Amount, Asset 2 Amount, …, Asset 15 Amount

What it means: How much of each asset you currently hold. For example:

• 0.03 BTC

• 2.1 ETH

Why it’s needed: The script multiplies this by the live price to calculate the current dollar value of each asset in your portfolio.

3. Target %

Fields: Asset 1 Implied %, Asset 2 Implied %, …, Asset 15 Implied %

What it means: Your desired allocation for each asset. For example:

• 40% BTC

• 20% ETH

• 10% SOL, etc.

Important: These must total 100% or less across all assets. The script checks this and shows an error if the total exceeds 100%.

The Dynamic Portfolio Tracker displays two powerful on-chart tables:

1. Main Table — Per Asset Breakdown

This table shows detailed, real-time information for each asset in your portfolio. Each row represents a different asset, and each column has a specific meaning:

Column What It Means

Asset = The symbol of the asset (e.g., BTCUSD, ETHUSD), auto-stripped from the exchange name.

Price = The current market price of the asset, pulled live from TradingView.

Quantity = How much of that asset you currently hold, entered manually in the inputs.

Target % = The percentage of your total portfolio you want this asset to represent.

Actual % = What percentage of your portfolio it currently makes up (based on price × quantity).

Target Value = How much (in $) this asset should be worth in your portfolio.

Actual Value = How much (in $) this asset is currently worth.

Instruction = Whether to Buy, Sell, or Hold to match your target allocation.

Value Change = The dollar amount you’d need to buy/sell to rebalance this asset.

Units to Trade = The number of asset units to buy/sell to reach the target value.

2. Portfolio Summary Table — Portfolio Totals

This smaller table appears in the top-right corner and summarizes your entire portfolio at a glance:

Target % = Total of all your assigned target allocations (should equal 100%).

Actual % = Actual portfolio composition (always 100% unless your capital is zero).

Target Value = Total value your portfolio should be based on your target percentages.

Actual Value = Current live total value of your portfolio.

If there’s a discrepancy between Target Value and Actual Value, the difference is shown in each row of the main table, so you can adjust individual assets accordingly.

Privacy First: Hide Sensitive Financial Data

A unique feature of this tool is the ability to hide sensitive financial data, such as:

• Target Value

• Actual Value

• Total Portfolio Value

You can turn these off using toggle settings, and they’ll be replaced with a crossed-out eye icon (👁️🗨️) — just like on modern crypto exchanges. This feature makes the script safe for streaming, screenshots, or sharing publicly while protecting your privacy.

But more importantly:

Feelings are the enemy of good investing.

Seeing the value of your portfolio fluctuate can trigger fear or greed. By hiding your dollar values, you’re not just securing your data — you’re reducing the temptation to react emotionally.

It’s just numbers. Systems over Feelings.

Table Automatically Adapts to Your Asset Count

The Dynamic Portfolio Tracker is designed to scale with your portfolio. Simply choose how many assets you want to track (up to 15), and the table will automatically resize to fit exactly that number — no wasted space or empty rows.

• Select 1 to 15 assets using the “Number of Assets” input

• The table expands or contracts dynamically to show only those rows

• All calculations, summaries, and layout elements adjust accordingly in real time

This keeps the interface clean, focused, and perfectly tailored to your setup — whether you’re tracking 3 coins or managing a full portfolio of 12+ tokens.

Customize Your Table to Match Your Style

The Dynamic Portfolio Tracker offers a full suite of visual customization options, allowing you to tailor the table to your charting style or stream layout. You can:

• Choose text colors for labels, values, and headers

• Set background colors for the full table and header row — or turn them off completely for a clean, transparent look

• Control border and frame settings, including color, thickness, or disabling them entirely

• Pick custom colors for Buy and Sell signals in the rebalance column

• Adjust table font size from tiny to large to match your resolution or preferences

Special Thanks

This tool wouldn’t exist without the knowledge and inspiration gained through The Real World. A sincere thank you to the Investing Master, the Guides, and Professor Adam — your frameworks and lessons brought clarity, discipline, and structure to this build.

And of course, glory to L4 — where real men are made.

Risk ModuleRisk Module

This indicator provides a visual reference to determine position sizing and approximate stop placement. It is designed to support trade planning by calculating equalized risk per trade based on a stop distance derived from volatility. The tool offers supportive reference points that allow for quick evaluation of risk and position size consistency across varying markets.

Equalized Risk Per Trade

The indicator calculates the number of shares that can be traded to maintain consistent monetary risk. The formula is based on the distance between the current price and the visual stop reference, adjusting the position size proportionally.

Position Size = Dollar Risk / (Entry Price – Stop Price)

The risk is calculated as a percentage of account size; both of which can be set in the indicator’s settings tab. This creates a consistent risk exposure across trades regardless of volatility or structural stop distance.

Stop Placement Reference

The visual stop reference is derived from the Average True Range (ATR), providing a volatility-based anchor. The default value is set to 2 × ATR, but this can be customized.

Price Model: Uses the current price ± ATR × multiplier. This model reacts to price movement and is set as the default option.

EMA Model: Uses the 20-period EMA ± ATR × multiplier. This model is less reactive and can be an option when used in combination with an envelope indicator.

Chart Elements

Stop Levels: Plotted above and below either the current price or EMA, depending on the selected model. These serve as visual reference points for stop placement; the lower level a sell stop for long trades, the upper level a buy stop for short trades.

Information Table: Displays the number of shares to trade, stop level and percentage risk. A compact mode is available to reduce the table to essential information (H/L and Shares).

Settings Overview

Stop Model: Choose between “Price” or “EMA” stop calculation logic.

ATR Multiplier: Change the distance between price/EMA and the stop reference.

Account Size / Risk %: These risk parameters are used to calculate dollar risk per trade.

Visible Bars: Number of recent bars to show stop markers on.

Compact Mode: Minimal table view for reduced chart footprint.

Table Position / Size: Controls table placement and scale on the chart.

SBC ProtfoSBC Portfo PNL Indicator

Description

The SBC Portfo PNL Indicator is a user-friendly tool designed for Hebrew-speaking traders to track the Profit and Loss (PNL) of their stock portfolios on TradingView charts. It supports up to 5 distinct portfolios, each capable of holding an unlimited number of stocks with unlimited buy commands, allowing real-time monitoring of portfolio performance.

Key Features

- Multi-Portfolio Support: Track up to 5 separate portfolios for different trading strategies or accounts.

- Unlimited Stock Entries: Add unlimited stocks and buy commands per portfolio.

- Detailed Buy Commands: Input for each stock:

- Stock Ticker (e.g., AAPL, TSLA).

- Buy Price (e.g., 150.25).

- Buy Amount (e.g., 10).

- Hebrew-Friendly Interface: Intuitive settings dialog with clear instructions in Hebrew.

- Customizable PNL Tracking: Visualize PNL on charts with real-time updates based on market data.

How to Use

1. Add the Indicator:

- Go to the Indicators menu in TradingView and add the "SBC Portfo" PNL Indicator.

2. Configure Portfolios:

- Open the indicator’s settings dialog.

- For each portfolio (up to 5), enter data in the provided input fields using this format:

PortfolioName:StockTicker:BuyPricexBuyAmount;StockTicker:BuyPricexBuyAmount

Example:

Portfolio1:AAPL:150.25x10;TSLA:266.72x5

- This represents a portfolio named "Portfolio1" with:

- 10 shares of AAPL bought at $150.25.

- 5 shares of TSLA bought at $266.72.

- Repeat for additional portfolios (e.g., Portfolio2, Portfolio3).

- Add multiple buy commands for the same stock if needed (e.g., AAPL:160.50x20).

3. Apply Settings:

- Save settings to display PNL based on current market prices.

4. Monitor PNL:

- View PNL for each portfolio on the chart via tables, labels, or graphical overlays (based on settings).

Input Format

Enter portfolio data manually in the settings dialog, one input field per portfolio:

PortfolioName:StockTicker:BuyPricexBuyAmount;StockTicker:BuyPricexBuyAmount

- PortfolioName: Unique name (e.g., Portfolio1, Growth).

- StockTicker: Stock symbol (e.g., AAPL).

- BuyPrice: Purchase price per share (e.g., 150.25).

- BuyAmount: Number of shares (e.g., 10).

- Use

: to separate portfolio name, ticker, and buy data

x to separate price and amount

; for multiple stocks in the portfolio

Example:

- Portfolio 1: GrowthPortfolio:AAPL:150.25x10;TSLA:266.72x5

- Portfolio 2: DividendPortfolio:KO:55.20x50;PG:145.30x30

Notes

- Hebrew Support: Settings and labels are optimized for Hebrew users.

- Manual Input: Enter portfolio data manually in the settings dialog using the correct format.

- Compatibility: Works with any stock ticker supported by TradingView.

תיאור אינדיקטור SBC Portfo PNL הוא כלי ידידותי למשתמש שתוכנן במיוחד עבור סוחרים דוברי עברית למעקב אחר רווח והפסד (PNL) של תיקי המניות שלהם ישירות בגרפים של TradingView. הוא תומך בעד 5 תיקים נפרדים, כאשר כל תיק יכול להכיל מספר בלתי מוגבל של מניות עם פקודות קנייה בלתי מוגבלות, ומאפשר מעקב בזמן אמת אחר ביצועי התיק.

תכונות עיקריות

- תמיכה בריבוי תיקים: מעקב אחר עד 5 תיקים נפרדים עבור אסטרטגיות מסחר או חשבונות שונים.

- רישום מניות ללא הגבלה: הוספת מספר בלתי מוגבל של מניות ופקודות קנייה לכל תיק.

- פקודות קנייה מפורטות: הזנת נתונים עבור כל מניה:

- סימול המניה (למשל, AAPL, TSLA).

- מחיר קנייה (למשל, 150.25).

- כמות קנייה (למשל, 10).

- ממשק ידידותי לעברית: חלונית הגדרות אינטואיטיבית עם הוראות ברורות בעברית.

- מעקב PNL הניתן להתאמה: הצגת רווח והפסד בגרפים עם עדכונים בזמן אמת בהתבסס על נתוני השוק.

כיצד להשתמש

1. הוספת האינדיקטור:

- נווט לתפריט האינדיקטורים ב-TradingView והוסף את "SBC Portfo PNL Indicator".

2. הגדרת תיקים:

- פתח את חלונית ההגדרות של האינדיקטור.

- עבור כל תיק (עד 5), הזן נתונים בשדות המסופקים בפורמט הבא:

PortfolioName:StockTicker:BuyPricexBuyAmount;StockTicker:BuyPricexBuyAmount

לדוגמה:

Portfolio1:AAPL:150.25x10;TSLA:266.72x5

שורה זו מייצגת תיק בשם "Portfolio1" עם:

- 10 מניות של AAPL שנקנו ב-$150.25.

- 5 מניות של TSLA שנקנו ב-$266.72.

- חזור על התהליך עבור תיקים נוספים (למשל, Portfolio2, Portfolio3).

- ניתן להוסיף פקודות קנייה מרובות לאותה מניה לפי הצורך (למשל, AAPL:160.50x20).

3. החלת ההגדרות:

- שמור את ההגדרות להצגת ה-PNL בהתבסס על מחירי השוק הנוכחיים.

4. מעקב אחר PNL:

- צפה ב-PNL עבור כל תיק בגרף באמצעות טבלאות, תוויות או שכבות גרפיות (בהתאם להגדרות).

פורמט קלט הזן נתוני תיק ידנית בחלונית ההגדרות, שדה קלט אחד לכל תיק: PortfolioName:StockTicker:BuyPricexBuyAmount;StockTicker:BuyPricexBuyAmount

PortfolioName: שם ייחודי (למשל, Portfolio1, Growth).

StockTicker: סימול המניה (למשל, AAPL).

BuyPrice: מחיר רכישה למניה (למשל, 150.25).

BuyAmount: מספר המניות (למשל, 10).

השתמש ב-

: להפרדה בין שם התיק, סימול ונתוני קנייה

x להפרדה בין מחיר וכמות

; להפרדה בין מניות מרובות

דוגמה:

- תיק 1: GrowthPortfolio:AAPL:150.25x10;TSLA:266.72x5

- תיק 2: DividendPortfolio:KO:55.20x50;PG:145.30x30

Release Notes

Version 1.1 includes:

- Calculations for extended hours (Pre-Market & After-Hours).

- Option to display portfolio summary data for stocks not in the portfolio (enable via settings checkbox).

- Table background for better visibility; click to bring table to the front.

- Updated text strings (names, titles, tooltips).

הערות

תמיכה בעברית: ההגדרות והתוויות מותאמות למשתמשים דוברי עברית.

הזנה ידנית: הזן נתוני תיק ידנית בחלונית ההגדרות תוך שימוש בפורמט הנכון.

תאימות: עובד עם כל סימול מניה הנתמך על ידי TradingView.

גרסה 1.1 מכילה:

1. חישובים כוללים שעות מסחר מורחבות (Pre-Market ו-After-Hours).

2. אפשרות להציג נתוני תיק כוללים עבור מניות שאינן בתיק (הפעל באמצעות תיבת סימון בהגדרות).

3. צבע רקע לטבלה לשיפור הנראות; לחיצה על הטבלה מביאה אותה לחזית.

4. תיקון נוסחים (שמות, כותרות, וטולטיפים).

PORTFOLIO TABLE Simple [Titans_Invest]PORTFOLIO TABLE Simple

This is a simple table for you to monitor your assets or cryptocurrencies in your SPOT wallet without needing to access your broker’s website or wallet app.

⯁ HOW TO USE THIS TABLE❓

You only need to select the asset and enter the amount of each one.

The table will show how much you have of each asset and the total value of your portfolio.

You’ll be able to monitor up to 39 assets in real time.

⯁ CONVERT VALUES

You can also activate and select a currency for conversion.

For example, cryptocurrency assets are calculated in US dollars, but you can select euros as the conversion currency.

The values originally in dollars will then be displayed in euros.

⯁ Track your Portfolio in real time:

⯁ Add your local Currency to Convert Values:

⯁ Follow your Portfolio Live:

___________________________________________________________

📜 SCRIPT : PORTFOLIO TABLE Simple

🎴 Art by : @Titans_Invest & @DiFlip

👨💻 Dev by : @Titans_Invest & @DiFlip

🎑 Titans Invest — The Wizards Without Gloves 🧤

✨ Enjoy!

___________________________________________________________

o Mission 🗺

• Inspire Traders to manifest Magic in the Market.

o Vision 𐓏

• To elevate collective Energy 𐓷𐓏

Credit Spread Monitor: HY & IG vs US10Y📉 Credit Spread Monitor: HY & IG vs US10Y

This indicator provides a dynamic and visual way to monitor credit spreads relative to the US Treasury benchmark. By comparing High Yield (HY) and Investment Grade (IG) corporate bond yields to the 10-Year US Treasury Yield (US10Y), it helps assess market stress, investor risk appetite, and potential macro turning points.

🔍 What It Does

-Calculates credit spreads:

HY Spread = BAMLH0A0HYM2EY − US10Y

IG Spread = BAMLC0A0CMEY − US10Y

-Detects macro risk regimes using statistical thresholds and yield curve signals:

🔴 HY Spread > +2σ → Potential financial stress

🟠 Inverted Yield Curve + HY Spread > 2% → Recession risk

🟢 HY Spread < 1.5% → Risk-on environment

-Visually highlights conditions with intuitive background colors for fast decision-making.

📊 Data Sources Explained

🔴 High Yield (HY): BAMLH0A0HYM2EY → ICE BofA US High Yield Index Effective Yield

🔵 Investment Grade (IG): BAMLC0A0CMEY → ICE BofA US Corporate Index Effective Yield

⚪ Treasury 10Y: US10Y → 10-Year US Treasury Yield

⚪ Treasury 2Y: US02Y → 2-Year US Treasury Yield (used to detect curve inversion)

✅ This Indicator Is Ideal For:

Macro traders looking to anticipate economic inflection points

Portfolio managers monitoring systemic risk or credit cycles

Fixed-income analysts tracking the cost of corporate borrowing

ETF/Asset allocators identifying shifts between risk-on and risk-off environments

🧠 Why It's Useful

This script helps visualize how tight or loose credit conditions are relative to government benchmarks. Since HY spreads typically widen before major downturns, this tool can provide early warning signals. Similarly, compressed spreads may indicate overheating or complacency in risk markets.

🛠️ Practical Use Case:

You’re managing a multi-asset portfolio. The HY spread jumps above +2σ while the yield curve remains inverted. You decide to reduce exposure to equities and high-yield bonds and rotate into cash or Treasuries as recession risk rises.

📎 Additional Notes

Sourced from FRED (Federal Reserve Economic Data) and TradingView’s bond feeds.

Designed to work best on daily resolution, using open prices to ensure consistency across series with different update timings.

This script is original, not based on built-in or public templates, and intended to offer educational, statistical, and visual insights for serious market participants.

Average Daily LiquidityIt is important to have sufficient daily trading value (liquidity) to ensure you can easily enter and, importantly, exit the trade. This indicator allows you to see if the traded value of a stock is adequate. The default average is 10 periods and it is common to average the daily traded value as both price and volume can have spikes causing trading errors. Some investors use a 5 period for a week, 10 period for 2 weeks, 20 or 21 period for 4 weeks/month and 65 periods for a quarter. You need to ascertain your buying amount such as $10000 and then have the average daily trading value be your comfortable moving average more such as average liquidity is more than 10 x MA(close x volume) or $100000 in this example. The value is extremely important for small and micro cap stocks you may wish to purchase.

ETF Builder & Backtest System [TradeDots]Create, analyze, and monitor your own custom “ETF-like” portfolio directly on TradingView. This script merges up to 10 different assets with user-defined weightings into a single composite chart, allowing you to see how your personalized portfolio would have performed historically. It is an original tool designed to help traders and investors quickly gauge risk and return profiles without leaving the TradingView platform.

📝 HOW IT WORKS

1. Custom Portfolio Construction

Multiple Assets : Combine up to 10 different stocks, ETFs, cryptocurrencies, or other symbols.

User-Defined Weights : Allocate each asset a percentage weight (e.g., 15% in AAPL, 10% in MSFT, etc.).

Single Composite Value : The script calculates a weighted “ETF-style” price, effectively simulating a merged portfolio curve on your chart.

2. Performance Tracking & Return Analysis

Automatic History Capture : The indicator records each asset’s starting price when it first appears in your chosen date range.

Rolling Updates : As time progresses, all asset prices are continually evaluated and the portfolio value is updated in real time.

Buy & Hold Returns : See how each asset—and the overall portfolio—performed from the “start” date to the most recent bar.

Annualized Return : Automatically calculates CAGR (Compound Annual Growth Rate) to help visualize performance over varying timescales.

3. Table & Visual Output

Performance Table : A comprehensive table displays individual asset returns, annualized returns, and portfolio totals.

Normalized Chart Plot : The composite ETF value is scaled to 100 at the start date, making it easy to compare relative growth or decline.

Optional Time Filter : You can define a specific date range (Start/End Dates) to focus on a particular period or to limit historical data.

⚙️ KEY FEATURES

1. Flexible Asset Selection

Choose any symbols from multiple asset classes. The script will only run calculations when data is available—no need to worry about missing quotes.

2. Dynamic Table Reporting

Start Price for each asset

Percentage Weight in the portfolio

Total Return (%) and Annualized Return (%)

3. Simple Backtesting Logic

This script takes a straightforward Buy & Hold perspective. Once the start date is reached, the portfolio remains static until the end date, so you can quickly assess hypothetical growth.

4. Plot Customization

Toggle the main “ETF” plot on/off.

Alter the visual style for tables and text.

Adjust the time filter to limit or extend your performance measurement window.

🚀 HOW TO USE IT

1. Add the Script

Search for “ETF Builder & Backtest System ” in the Indicators & Strategies tab or manually add it to your chart after saving it in your Pine Editor.

2. Configure Inputs

Enable Time Filter : Choose whether to restrict the analysis to a particular date range.

Start & End Date : Define the period you want to measure performance over (e.g., from 2019-12-31 to 2025-01-01).

Assets & Weights : Enter each symbol and specify a percentage weight (up to 10 assets).

Display Options : Pick where you want the Table to appear and choose background/text colors.

3. Interpret the Table & Plots

Asset Rows : Each asset’s ticker, weighting, start price, and performance metrics.

ETF Total Row : Summarizes total weighting, composite starting value, and overall returns.

Normalized Plot : Tracks growth/decline of the combined portfolio, starting at 100 on the chart.

4. Refine Your Strategy

Compare how different weights or a new mix of assets would have performed over the same period.

Assess if certain assets contribute disproportionately to your returns or volatility.

Use the results to guide allocations in your real trading or paper trading accounts.

❗️LIMITATIONS

1. Buy & Hold Only

This script does not handle rebalancing or partial divestments. Once the portfolio starts, weights remain fixed throughout the chosen timeframe.

2. No Reinvestment Tracking

Dividends or other distributions are not factored into performance.

3. Data Availability

If historical data for a particular asset is unavailable on TradingView, related results may display as “N/A.”

4. Market Regimes & Volatility

Past performance does not guarantee similar future behavior. Markets can change rapidly, which may render historical backtests less predictive over time.

⚠️ RISK DISCLAIMER

Trading and investing carry significant risk and can result in financial loss. The “ETF Builder & Backtest System ” is provided for informational and educational purposes only. It does not constitute financial advice.

Always conduct your own research.

Use proper risk management and position sizing.

Past performance does not guarantee future results.

This script is an original creation by TradeDots, published under the Mozilla Public License 2.0.

Use this indicator as part of a broader trading or investment approach—consider fundamental and technical factors, overall market context, and personal risk tolerance. No trading tool can assure profits; exercise caution and responsibility in all financial decisions.

Grid Bot Visualizer V1

📊 Grid Bot Visualizer – V1

A dynamic and visual support tool for grid trading strategies.

🔧 Key Features

• Fixed grid levels based on a central entry price

• Customizable spacing, number of levels, and range

• Color-coded lines (🟢 green above, 🔴 red below)

• Expands automatically when price exceeds boundaries (within the defined box)

• Optional price labels shown outside the grid

• Grid visually framed by a blue box

• Vertical line to mark grid origin

• Built-in alert when price hits a grid level

⚙️ Use Case

Ideal for visualizing grid bot logic in volatile markets.

Monitor how price interacts with predefined zones.

✅ Alert Ready

Use alertcondition to get notified when a grid level is touched.

Max RR CalculatorAutomatically calculates the maximum RR reached during trade. Entry is at the candle close. There is an option available that takes another trade after getting stopped out on the next candle that is in same bias as first trade.

(If the first trade is a long and gets stopped out, then the second trade will wait until the next up candle to enter long again)

Price Map Profile [BigBeluga]An advanced volume-based tool designed to map out how trading activity is distributed across price levels. It combines dynamic volume profiling with structural pivot detection to highlight key levels of interest in the market — including hidden support/resistance zones and dominant liquidity areas.

Unlike traditional volume profiles locked to fixed sessions, this indicator continuously processes historical bars to build a real-time "map" of volume distribution. It intelligently reveals where buyers and sellers were most active, helping traders pinpoint high-impact zones with clarity.

🔵 KEY FEATURES

Creates a volume map profile by scanning price action over a defined lookback window (`length`).

Divides price vertically into volume bins (default: 100) and aggregates either total volume or bar count per bin.

Bins are plotted as horizontal zones extending to the right of the chart — wider offset means more volume at that price.

Each zone is color-coded using gradients to represent volume magnitude:

- Below average volume = cool tones (blue/teal)

- Above average volume = warm tones (red/orange)

The highest volume bin is highlighted with a red label showing the exact volume, helping to identify strong price agreement.

Detects pivot highs and lows using a 15-bar swing method, marking them as potential S/R levels.

If a pivot level is located inside a low-volume zone (volume < average), it is emphasized with a dashed line and label .

Pivot line color matches direction:

- High pivots = yellow

- Low pivots = aqua

The volume of the bin containing the pivot is shown alongside the pivot, providing volume context for the structural level.

Filters out nearby duplicate pivots using ATR-based distance checks to ensure clean and non-redundant signals.

🔵 HOW TO USE

Use the wide red zones as liquidity and consolidation areas where price may stall, reverse, or absorb volume.

Pivot-based dashed lines within low-volume zones highlight hidden support/resistance levels where price may react sharply.

Combine this indicator with trend or order flow tools to validate reversal or breakout setups .

Switch between Volume and Frequency modes to adapt to the type of data your asset provides.

🔵 CONCLUSION

The Price Map Profile transforms raw volume into an actionable visual map. By aligning volume depth with key market structure levels, it helps traders identify where market participants are most active — and where hidden inefficiencies lie. Ideal for traders seeking precision entries, dynamic S/R zones, and deeper volume structure insight.

Prop Firm Business SimulatorThe prop firm business simulator is exactly what it sounds like. It's a plug and play tool to test out any tradingview strategy and simulate hypothetical performance on CFD Prop Firms.

Now what is a modern day CFD Prop Firm?

These companies sell simulated trading challenges for a challenge fee. If you complete the challenge you get access to simulated capital and you get a portion of the profits you make on those accounts payed out.

I've included some popular firms in the code as presets so it's easy to simulate them. Take into account that this info will likely be out of date soon as these prices and challenge conditions change.

Also, this tool will never be able to 100% simulate prop firm conditions and all their rules. All I aim to do with this tool is provide estimations.

Now why is this tool helpful?

Most traders on here want to turn their passion into their full-time career, prop firms have lately been the buzz in the trading community and market themselves as a faster way to reach that goal.

While this all sounds great on paper, it is sometimes hard to estimate how much money you will have to burn on challenge fees and set realistic monthly payout expectations for yourself and your trading. This is where this tool comes in.

I've specifically developed this for traders that want to treat prop firms as a business. And as a business you want to know your monthly costs and income depending on the trading strategy and prop firm challenge you are using.

How to use this tool

It's quite simple you remove the top part of the script and replace it with your own strategy. Make sure it's written in same version of pinescript before you do that.

//--$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$--//--------------------------------------------------------------------------------------------------------------------------$$$$$$

//--$$$$$--Strategy-- --$$$$$$--// ******************************************************************************************************************************

//--$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$--//--------------------------------------------------------------------------------------------------------------------------$$$$$$

length = input.int(20, minval=1, group="Keltner Channel Breakout")

mult = input(2.0, "Multiplier", group="Keltner Channel Breakout")

src = input(close, title="Source", group="Keltner Channel Breakout")

exp = input(true, "Use Exponential MA", display = display.data_window, group="Keltner Channel Breakout")

BandsStyle = input.string("Average True Range", options = , title="Bands Style", display = display.data_window, group="Keltner Channel Breakout")

atrlength = input(10, "ATR Length", display = display.data_window, group="Keltner Channel Breakout")

esma(source, length)=>

s = ta.sma(source, length)

e = ta.ema(source, length)

exp ? e : s

ma = esma(src, length)

rangema = BandsStyle == "True Range" ? ta.tr(true) : BandsStyle == "Average True Range" ? ta.atr(atrlength) : ta.rma(high - low, length)

upper = ma + rangema * mult

lower = ma - rangema * mult

//--Graphical Display--// *-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-$$$$$$

u = plot(upper, color=#2962FF, title="Upper", force_overlay=true)

plot(ma, color=#2962FF, title="Basis", force_overlay=true)

l = plot(lower, color=#2962FF, title="Lower", force_overlay=true)

fill(u, l, color=color.rgb(33, 150, 243, 95), title="Background")

//--Risk Management--// *-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-$$$$$$

riskPerTradePerc = input.float(1, title="Risk per trade (%)", group="Keltner Channel Breakout")

le = high>upper ? false : true

se = lowlower

strategy.entry('PivRevLE', strategy.long, comment = 'PivRevLE', stop = upper, qty=riskToLots)

if se and upper>lower

strategy.entry('PivRevSE', strategy.short, comment = 'PivRevSE', stop = lower, qty=riskToLots)

The tool will then use the strategy equity of your own strategy and use this to simulat prop firms. Since these CFD prop firms work with different phases and payouts the indicator will simulate the gains until target or max drawdown / daily drawdown limit gets reached. If it reaches target it will go to the next phase and keep on doing that until it fails a challenge.

If in one of the phases there is a reward for completing, like a payout, refund, extra it will add this to the gains.

If you fail the challenge by reaching max drawdown or daily drawdown limit it will substract the challenge fee from the gains.

These gains are then visualised in the calendar so you can get an idea of yearly / monthly gains of the backtest. Remember, it is just a backtest so no guarantees of future income.

The bottom pane (non-overlay) is visualising the performance of the backtest during the phases. This way u can check if it is realistic. For instance if it only takes 1 bar on chart to reach target you are probably risking more than the firm wants you to risk. Also, it becomes much less clear if daily drawdown got hit in those high risk strategies, the results will be less accurate.

The daily drawdown limit get's reset every time there is a new dayofweek on chart.

If you set your prop firm preset setting to "'custom" the settings below that are applied as your prop firm settings. Otherwise it will use one of the template by default it's FTMO 100K.

The strategy I'm using as an example in this script is a simple Keltner Channel breakout strategy. I'm using a 0.05% commission per trade as that is what I found most common on crypto exchanges and it's close to the commissions+spread you get on a cfd prop firm. I'm targeting a 1% risk per trade in the backtest to try and stay within prop firm boundaries of max 1% risk per trade.

Lastly, the original yearly and monthly performance table was developed by Quantnomad and I've build ontop of that code. Here's a link to the original publication:

That's everything for now, hope this indicator helps people visualise the potential of prop firms better or to understand that they are not a good fit for their current financial situation.

Advanced Momentum Scanner [QuantAlgo]The Advanced Momentum Scanner is a sophisticated technical indicator designed to identify market momentum and trend direction using multiple exponential moving averages (EMAs), momentum metrics, and adaptive visualization techniques. It is particularly valuable for those looking to identify trading and investing opportunities based on trend changes and momentum shifts across any market and timeframe.

🟢 Technical Foundation

The Advanced Momentum Scanner utilizes a multi-layered approach with four different EMA periods to identify market momentum and trend direction:

Ultra-Fast EMA for quick trend changes detection (default: 5)

Fast EMA for short-term trend analysis (default: 10)

Mid EMA for intermediate confirmation (default: 30)

Slow EMA for long-term trend identification (default: 100)

For momentum detection, the indicator implements a Rate of Change (RoC) calculation to measure price momentum over a specified period. It further enhances analysis by incorporating RSI readings for overbought/oversold conditions, volatility measurements through ATR, and optional volume confirmation. When these elements align, the indicator generates trading signals based on the selected sensitivity mode (Conservative, Balanced, or Aggressive).

🟢 Key Features & Signals

1. Multi-Period Trend Identification

The indicator combines multiple EMAs of different lengths to provide comprehensive trend analysis within the same timeframe, displaying the information through color-coded visual elements on the chart.

When an uptrend is detected, chart elements are colored with the bullish theme color (default: green/teal).

Similarly, when a downtrend is detected, chart elements are colored with the bearish theme color (default: red).

During neutral or indecisive periods, chart elements are colored with a neutral gray color, providing clear visual distinction between trending and non-trending market conditions.

This visualization provides immediate insights into underlying trend direction without requiring separate indicators, helping traders and investors quickly identify the market's current state.

2. Trend Strength Information Panel

The trend panel operates in three different sensitivity modes (Conservative, Aggressive, and Balanced), each affecting how the indicator processes and displays market information.

The Conservative mode prioritizes trend sustainability over frequency, showing only strong trend movements with high probability.

The Aggressive mode detects early trend changes, providing more frequent signals but potentially more false positives.

The Balanced mode offers a middle ground with moderate signal frequency and reliability.

Regardless of the selected mode, the panel displays:

Current trend direction (UPTREND, DOWNTREND, or NEUTRAL)

Trend strength percentage (0-100%)

Early detection signals when applicable

The active sensitivity mode

This comprehensive approach helps traders and investors:

→ Assess the strength of current market trends

→ Identify early potential trend changes before full confirmation

→ Make more informed trading and investing decisions based on trend context

3. Customizable Visualization Settings

This indicator offers extensive visual customization options to suit different trading styles and preferences:

Display options:

→ Fully customizable uptrend, downtrend, and neutral colors

→ Color-coded price bars showing trend direction

→ Dynamic gradient bands visualizing potential trend channels

→ Optional background coloring based on trend intensity

→ Adjustable transparency levels for all visual elements

These visualization settings can be fine-tuned through the indicator's interface, allowing traders and investors to create a personalized chart environment that emphasizes the most relevant information for their strategy.

The indicator also features a comprehensive alert system with notifications for:

New trend formations (uptrend, downtrend, neutral)

Early trend change signals

Momentum threshold crossovers

Other significant market conditions

Alerts can be customized and delivered through TradingView's notification system, making it easy to stay informed of important market developments even when you are away from the charts.

🟢 Practical Usage Tips

→ Trend Analysis and Interpretation: The indicator visualizes trend direction and strength directly on the chart through color-coding and the information panel, allowing traders and investors to immediately identify the current market context. This information helps in assessing the potential for continuation or reversal.

→ Signal Generation Strategies: The indicator generates potential trading signals based on trend direction, momentum confirmation, and selected sensitivity mode. Users can choose between Conservative (fewer but more reliable signals), Balanced (moderate approach), or Aggressive (more frequent but potentially less reliable signals).

→ Multi-Period Trend Assessment: Through its layered EMA approach, the indicator enables users to understand trend conditions across different lookback periods within the same timeframe. This helps in identifying the dominant trend and potential turning points.

🟢 Pro Tips

Adjust EMA periods based on your timeframe:

→ Lower values for shorter timeframes and more frequent signals

→ Higher values for higher timeframes and more reliable signals

Fine-tune sensitivity mode based on your trading style:

→ "Conservative" for position trading/long-term investing and fewer false signals

→ "Balanced" for swing trading/medium-term investing with moderate signal frequency

→ "Aggressive" for scalping/day trading and catching early trend changes

Look for confluence between components:

→ Strong trend strength percentage and direction in the information panel

→ Overall market context aligning with the expected direction

Use for multiple trading approaches:

→ Trend following during strong momentum periods

→ Counter-trend trading at band extremes during overextension

→ Early trend change detection with sensitivity adjustments

→ Stop loss placement using dynamic bands

Combine with:

→ Volume indicators for additional confirmation

→ Support/resistance analysis for strategic entry/exit points

→ Multiple timeframe analysis for broader market context