Adaptive Qualitative Quantitative Estimation (QQE) [Loxx]Adaptive QQE is a fixed and cycle adaptive version of the popular Qualitative Quantitative Estimation (QQE) used by forex traders. This indicator includes varoius types of RSI caculations and adaptive cycle measurements to find tune your signal.

Qualitative Quantitative Estimation (QQE):

The Qualitative Quantitative Estimation (QQE) indicator works like a smoother version of the popular Relative Strength Index (RSI) indicator. QQE expands on RSI by adding two volatility based trailing stop lines. These trailing stop lines are composed of a fast and a slow moving Average True Range (ATR).

There are many indicators for many purposes. Some of them are complex and some are comparatively easy to handle. The QQE indicator is a really useful analytical tool and one of the most accurate indicators. It offers numerous strategies for using the buy and sell signals. Essentially, it can help detect trend reversal and enter the trade at the most optimal positions.

Wilders' RSI:

The Relative Strength Index ( RSI ) is a well versed momentum based oscillator which is used to measure the speed (velocity) as well as the change (magnitude) of directional price movements. Essentially RSI , when graphed, provides a visual mean to monitor both the current, as well as historical, strength and weakness of a particular market. The strength or weakness is based on closing prices over the duration of a specified trading period creating a reliable metric of price and momentum changes. Given the popularity of cash settled instruments (stock indexes) and leveraged financial products (the entire field of derivatives); RSI has proven to be a viable indicator of price movements.

RSX RSI:

RSI is a very popular technical indicator, because it takes into consideration market speed, direction and trend uniformity. However, the its widely criticized drawback is its noisy (jittery) appearance. The Jurk RSX retains all the useful features of RSI , but with one important exception: the noise is gone with no added lag.

Rapid RSI:

Rapid RSI Indicator, from Ian Copsey's article in the October 2006 issue of Stocks & Commodities magazine.

RapidRSI resembles Wilder's RSI , but uses a SMA instead of a WilderMA for internal smoothing of price change accumulators.

VHF Adaptive Cycle:

Vertical Horizontal Filter (VHF) was created by Adam White to identify trending and ranging markets. VHF measures the level of trend activity, similar to ADX DI. Vertical Horizontal Filter does not, itself, generate trading signals, but determines whether signals are taken from trend or momentum indicators. Using this trend information, one is then able to derive an average cycle length.

Band-pass Adaptive Cycle:

Even the most casual chart reader will be able to spot times when the market is cycling and other times when longer-term trends are in play. Cycling markets are ideal for swing trading however attempting to “trade the swing” in a trending market can be a recipe for disaster. Similarly, applying trend trading techniques during a cycling market can equally wreak havoc in your account. Cycle or trend modes can readily be identified in hindsight. But it would be useful to have an objective scientific approach to guide you as to the current market mode.

There are a number of tools already available to differentiate between cycle and trend modes. For example, measuring the trend slope over the cycle period to the amplitude of the cyclic swing is one possibility.

We begin by thinking of cycle mode in terms of frequency or its inverse, periodicity. Since the markets are fractal ; daily, weekly, and intraday charts are pretty much indistinguishable when time scales are removed. Thus it is useful to think of the cycle period in terms of its bar count. For example, a 20 bar cycle using daily data corresponds to a cycle period of approximately one month.

When viewed as a waveform, slow-varying price trends constitute the waveform's low frequency components and day-to-day fluctuations (noise) constitute the high frequency components. The objective in cycle mode is to filter out the unwanted components--both low frequency trends and the high frequency noise--and retain only the range of frequencies over the desired swing period. A filter for doing this is called a bandpass filter and the range of frequencies passed is the filter's bandwidth.

Included:

-Toggle on/off bar coloring

-Customize RSI signal using fixed, VHF Adaptive, and Band-pass Adaptive calculations

-Choose from three different RSI types

Visuals:

-Red/Green line is the moving average of RSI

-Thin white line is the fast trend

-Dotted yellow line is the slow trend

Happy trading!

RSX

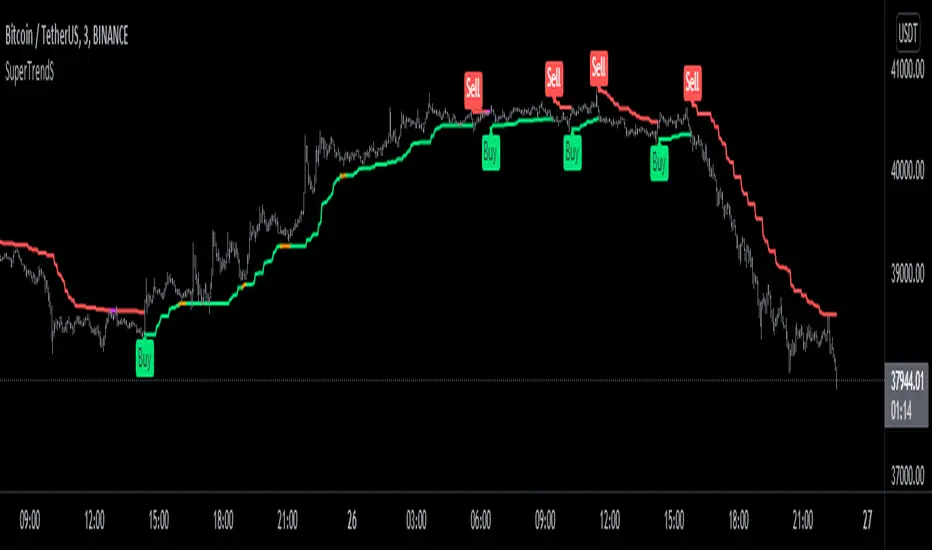

SuperTrendSHey! By using this script you can choose between the Regular SuperTrend and Pivot Point SuperTrend.

Pivot Point SuperTrend differs in calculation from the regular SuperTrend and as the name suggests, Pivot Points are used instead of ATR.

I made this script to make it easier to switch and compare between one another.

Also included Jurik RSX as a Momentum Indicator. SuperTrend changes color to purple when it's a bear trend and RSX is in an overbought state. And orange when it's a bull trend and RSX is in an oversold state. A reversal might be expected when color changes to purple & orange occur.

Special thanks to;

Kivanc Ozbilgic for SuperTrend

LonesomeTheBlue for Pivot Point SuperTrend

& everget for Jurik RSX

Enjoy!

KINSKI RSI/RSX DivergenceThe Relative Strength Index (RSI) is a momentum indicator that measures the magnitude of recent price changes to analyse overbought or oversold conditions. RSI values range from 0 to 100.

The Relative Strength Index (RSI) is calculated using the following formula: RSI = 100 - 100 / (1 + RS) Where RS = average gain of upward phases during the specified time frame / average loss of downward phases during the specified time frame.

An asset price is considered overbought (due for a correction) if the RSI is above 70 and oversold (due for a recovery) if it is below 30. More extreme values (80/20) are also used to avoid false readings.

In a strong uptrend, the RSI often reaches 70 and above for long periods, and downtrends can remain at 30 or below for long periods.

Divergence detection in RSI is one of the important functions of this indicator. The reason is that an RSI divergence is a more reliable signal than the overbought and oversold indicators themselves. You will get overbought and oversold signals all the time. However, the divergence is a rare event.

In general, RSI divergence means that the RSI indicator is moving in the opposite direction compared to the price. So while the price is moving, the RSI is telling us in advance to expect a change in direction.

Positive RSI divergence

A positive RSI divergence is when the price trend has lower lows and lower highs, while the RSI indicator does the opposite - higher highs and higher lows. The price continues to fall while the RSI indicator begins to rise.

Negative RSI divergence

Negative RSI divergence is the opposite of positive divergence. It applies to uptrends where the price reaches higher highs and higher lows. However, the RSI shows lower highs and lower lows - the price goes up but the RSI goes down. The price closes with higher highs and higher lows, while the RSI indicator does the opposite - lower lows and lower highs, confirming a negative divergence. As a result, there is a sharp decline in the price.

RSX Indicator - Base script: SharkCIA by Jaggedsoft (Linked in the source code)

The RSX is the noise-free variant of the more popular RSI oscillator. Typically, any indicator can be smoothed by applying a moving average. However, a major disadvantage of such a method is that there is a time lag between the indicator and the price. RSX Indicator attempts to do this without signal delay.

What distinguishes this indicator from others of this type?

Display of RSI indicator together/alone with RSX and RSI smoothed

display of the RSI indicator (option: "RSI: On/Off")

display of the RSX indicator (option: "RSX: On/Off")

display of the RSI indicator as smoothed version (option: "RSI Smoothed: On/Off")

offers the possibility to choose between different view variants

many settings for additional information, layout and divergence identification

enables completely new comparison possibilities and insights with the additional RSI variants

Williams %R & RSI with Multiple PeriodsDESCRIPTION

1. Calculates %R and RSI with multiple period lengths.

1 period length value is defined by User.

8 period length values follow User's selection of classic number sequences, e.g. Fibonacci, Leonardo, Lucas, Narayana, etc.

2. User selects which indicator and periods to display or hide.

DEFAULTS

%R default custom period: 10.

RSI default custom period: 14.

%R & RSI default number sequence periods: Lucas numbers 11, 18, 29, 47, 76, 123, 199, 322.

CALCULATIONS

%R = (period high - most recent period's close price)/(period high - period low)

RSI = 100 - 1 / (100 + RS), where RS = SMMA(up, period) / SMMA(down, period)

PURPOSE

1. Identify price trends.

CREDITS

1. Williams %R technical analysis momentum oscillator by Larry Williams.

2. Wilder's Relative Strength Index technical analysis momentum oscillator by J. Welles Wilder.

3. "Solarized" color scheme by Ethan Schoonover.

RSX-D [ID: AC-P]The "AC-P" version of Jaggedsoft's RSX Divergence and Everget's RSX script is my personal customized version of RSX with the following additions and modifications:

LSMA-D line that averages in three LSMA components to form a composite, the LSMA-D line. Offset for the LSMA-D line is set to -2 to offset latency from averaging togther the LSMA components to form a composite - recommended to adjust to your timeframe and asset/pair accordingly.

Divergence component from JustUncle, RicardoSantos, and Neobutane divergence scripts

Crossover indication and alerts for Midline, and custom M1 and M2 levels for both RSX and the LSMA-D line from Daveatt's CCI Stochastic Script

EMA21/55 zone cross highlighting option

SMA9/EMA45 MA option from my RSI sma/ema Cu script

Libertus Divergences and Pivot labels from Jaggedsoft's RSX Divergence script are hidden/off by default

Designed for darkmode by default. Minor visual changes from Jaggedsoft's and Everget's script(s) for darkmode and visual aesthetic.

Please Note:

Divergences that use fractal-based detection logic, offset, or a combination of both generally have a 1-2 bar/candle lag. This is an INHERENT limitation of divergence detection with fractals and offsets. Divergences generally will have a higher strikerate on HTF than LTF due to the 1-2 bar lag. While I'm not going to rule out a programming solution or math construct/formula that attempts to alleivates the 1-2 bar lag for divergences, this script is not it - please keep that in mind when using divergence components with a fractal base and offset.

LSMA-D is a composite of three LSMA lines, all with offset options. Different lengths and Offset values can compensate/adjust for the smoothing/latency from RSX, but only up to a certain point. For each LSMA, the least square regression line is calculated for the previous time periods, so the idea is that with finely tuned adjustments, you can get crossover/crossunder signals from the RSX with the LSMA-D line that you simply can't get with the SMA9/EMA45 due to the already smoothed RSX.

The defaults for the RSX and various components for the LSMA-D here will MOSTLY LIKELY NOT WORK OR BE APPLICABLE to every timeframe and asset that you trade - adjust, backtest, and test accordingly. The defaults are here are MEANT to be adjusted to the asset class and timeframe that you are trading.

If you're not familiar with the LSMA, tradingview author Alexgrover has a few great scripts that go into detail how the LSMA works, in addition to different interpretations and implementations of the LSMA.

References/Acknowledgements:

//@version=4

// Copyright (c) 2019-present, Alex Orekhov (everget)

// Jurik RSX script may be freely distributed under the MIT license.

//

//-------------------------------------------------------------------

// Acknowledgements:

//---- Base script:

// RSX Divergence — SharkCIA by Jaggedsoft

//

// Jurik Moving Average by Everget

//

//---- Divergences/Signals:

// Libertus RSI Divergences

//

// Price Divergence Dectector V3 by JustUncle

//

// Price Divergence Detector V2 by RicardoSantos

//

// Stochastic RSI with Divergences by Neobutane

//

// CCI Stochastic by Daveatt

//

//---- Misc. Reference:

// RSI SMA/EMA Cu by Auroagwei

//

// CBCI Cu by Auroagwei

//

// Chop and explode by fhenry0331

//

// T-Step LSMA by RafaelZioni

//

// Scripts by Jaggedsoft for structure and formatting

// Scripts by Everget for structure and formatting

//-------------------------------------------------------------------

// RSX-D v08

// Author: Auroagwei

// www.tradingview.com

//-------------------------------------------------------------------

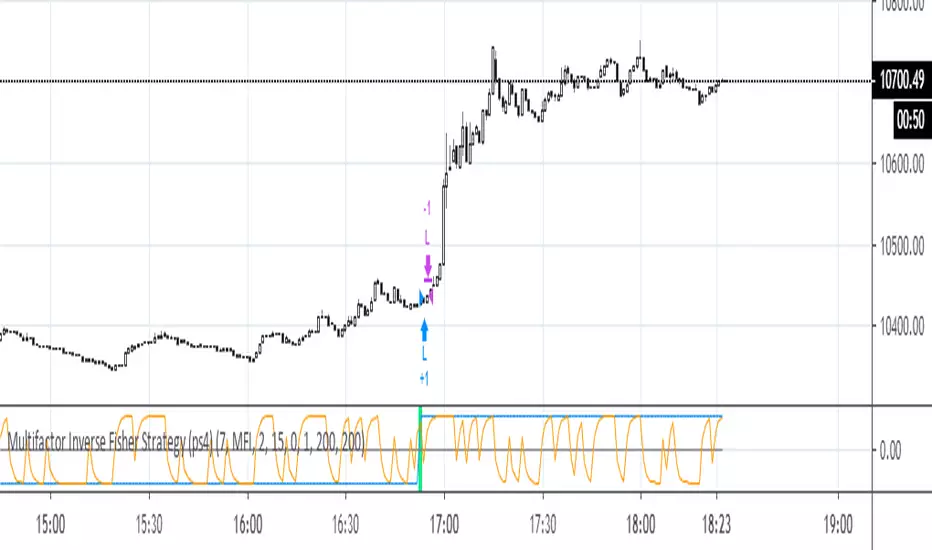

Multifactor Inverse Fisher Strategy (ps4)Best for higher time frames - 30m, 1H, 2H, 3H, 4H, D this strategy uses several factors that are pushed through an Inverse Fisher Transform (IFT). The higher the TF, the better the performance, up to 98%, but the number of deals tends to drop). Middle time frames (5m, 15m) look viable with Scaled Price (Scaled %P) and MFI factors. The factor list can be extended to include cci, stoch, rsi_stoch, emo, macd, cog, dpo, roc, accdist, cctbb, mom, awesome, tva, etc. Some of them need to be rescaled to a 0..100 interval. The IFT produces a value in the -1..1 interval (see: www.mesasoftware.com). This indicator does NOT repaint.

RSX Divergence — SharkCIARSX is a "noise free" version of RSI, with no added lag.

This version takes everget's implementation of RSX and adds divergences.

Credit for the divergences goes to Libertus:

Check out everget's scripts here: www.tradingview.com

Jurik RSXAdopted to Pine from www.prorealcode.com .

I haven't yet understood the details of the algorithm but it matches the original Jurik's RSX one to one.

Jurik's RSX is a "noise free" version of RSI, with no added lag. To learn more about this indicator see www.jurikres.com .

Good luck!

RSX FracticalityA little project I was working on to avoid studying for finals. Using LazyBear's RSX code for a smoother RSI, then taking the RSX of fib number lengths. Take the average of that, then the JMA of that from the same fib numbers. The average of that is then treated as the trend, take the average of the trend values from the main time frames, the script calls pretty far back so adding a W or M TF I think would throw the calculations off. Then I smoothed that value using the jma's to create the overall trend. I got the idea from Ehler's Empirical Mode Decomposition about identifying peaks and valleys and creating an average of that to create a range. The idea is that if the trend is above the Average Peak then it is a bull trend, less than the average valley it's a bear trend, in between it's ranging. It looks like it turned out alright, I'll be working on this idea of fractals a lot this summer to see if I can improve it or build something better off of the idea.

JMA RSX Clone [LazyBear]RSX is a "noise free" version of RSI, with no added lag. This is a port of a clone to Pine.

Use this indicator just like RSI. I have set the default length to 14, feel free to experiment. You can reduce length with out worrying about jaggedness.

Options page has all the configurable parameters. You can use the plot names to setup alerts.

I have couple of more indicators built using this, will post them later. Let me know what you think about this indicator.

RSX Clone compared to normal RSI:

Smoothness helps a lot in identifying the divergences correctly:

More info:

www.jurikres.com

List of my public indicators: bit.ly

List of my app-store indicators: blog.tradingview.com