Advanced Fully Reversed Candles with Reversed IchimokuThe "Advanced Fully Reversed Candles with Reversed Ichimoku" indicator is a sophisticated tool designed for traders who seek a unique perspective on market dynamics. This innovative indicator not only reverses the traditional candlestick chart but also inverts the Ichimoku Cloud components, providing a comprehensive view of the market's inverted behavior.

Key Features:

Reversed Candlestick Chart:

The indicator recalculates the OHLC (Open, High, Low, Close) prices by reversing them along the price axis. This means that what typically would be an upward movement is displayed as a downward movement, and vice versa. This reversal provides an alternative view that can help traders identify hidden patterns and potential reversal points that might not be obvious on a standard chart.

Reversed Ichimoku Cloud:

All components of the Ichimoku Cloud indicator are recalculated based on the reversed price data. This includes:

Tenkan-sen (Conversion Line): Reversed based on the highest and lowest prices over the specified period.

Kijun-sen (Base Line): Reversed in a similar manner to the Tenkan-sen, providing a medium-term perspective on price trends.

Senkou Span A (Leading Span A): Reversed to form one boundary of the Kumo (cloud), offering insight into future support and resistance levels.

Senkou Span B (Leading Span B): Reversed to form the other boundary of the Kumo, complementing Senkou Span A.

Chikou Span (Lagging Span): Reversed and plotted backward for additional confirmation of trend direction and strength.

Dynamic Price Range Calculation:

The indicator dynamically calculates the maximum and minimum prices over the last 500 bars (or the available range if fewer bars are present). This ensures that the reversal is always based on the most relevant data, providing accurate and up-to-date visualizations.

Visual Enhancements:

The reversed candlesticks are color-coded for easy interpretation: green for upward movements and red for downward movements, based on the reversed data.

The Ichimoku Cloud is filled with semi-transparent colors to clearly distinguish between bullish and bearish conditions even in its reversed state.

Debugging Aids:

For transparency and accuracy, the indicator plots the maximum and minimum price lines used for the reversal calculations. This allows users to verify the internal workings of the indicator and ensure the reversal logic is correctly applied.

Usage:

This indicator is ideal for advanced traders and analysts who want to explore market behavior from an unconventional angle. By reversing both the candlestick chart and the Ichimoku Cloud, it provides a unique perspective that can uncover new trading opportunities and enhance market analysis.

Customization:

Users can customize the periods for the Tenkan-sen, Kijun-sen, and Senkou Span B, as well as the displacement for the Ichimoku Cloud. This flexibility allows traders to adapt the indicator to their specific trading strategies and timeframes.

Conclusion:

The "Advanced Fully Reversed Candles with Reversed Ichimoku" indicator is a powerful tool that transforms traditional market analysis. By inverting both price movements and key technical indicators, it opens up a new dimension of trading insights, helping traders to see the market in a completely different light.

Parameters:

Tenkan-sen period (default: 9)

Kijun-sen period (default: 26)

Senkou Span B period (default: 52)

Displacement (default: 26)

How to Apply:

Add the script to your TradingView account via the Pine Editor.

Customize the parameters according to your trading strategy.

Analyze the reversed candlestick chart and Ichimoku Cloud to gain unique insights into market trends and potential reversal points.

Signals

Advanced ADX [CryptoSea]The Advanced ADX Analysis is a sophisticated tool designed to enhance market analysis through detailed ADX calculations. This tool is built for traders who seek to identify market trends, strength, and potential reversals with higher accuracy. By leveraging the Average Directional Index (ADX), Directional Indicator Plus (DI+), and Directional Indicator Minus (DI-), this indicator offers a comprehensive view of market dynamics.

New Overlay Feature: This script uses the new 'force overlay' feature which lets you plot on the chart as well as plotting in an oscillator pane at the same time.

force_overlay=true

Key Features

Comprehensive ADX Tracking: Tracks ADX values along with DI+ and DI- to provide a complete view of market trend strength and direction. The ADX measures the strength of the trend, while DI+ and DI- indicate the trend direction. This combined analysis helps traders identify strong and weak trends with precision.

Trend Duration Monitoring: Monitors the duration of strong and weak trends, offering insights into trend persistence and potential reversals. By keeping track of how long the ADX has been above or below a certain threshold, traders can gauge the sustainability of the current trend.

Customizable Alerts: Features multiple alert options for strong trends, weak trends, and DI crossovers, ensuring traders are notified of significant market events. These alerts can be tailored to notify traders when certain conditions are met, such as when the ADX crosses a threshold or when DI+ crosses DI-.

Adaptive Display Options: Includes customizable background color settings and extended statistics display for in-depth market analysis. Users can choose to highlight strong or weak trends on the chart background, making it easier to visualize market conditions at a glance.

In the example below, we have a bullish scenario play out where the DI+ has been above the DI- for 11 candles and our dashboard shows the average is 10.48 candles. With the ADX above its threshold this would be a bullish signal.

This ended up in a 20%+ move to the upside. The dashboard will help point out things to consider when looking to exit the position, the DI+ getting close to the max DI+ duration would be a sign that momentum is weakening and that price may cool off or even reverse.

How it Works

ADX Calculation: Computes the ADX, DI+, and DI- values using a user-defined period. The ADX is derived from the smoothed average of the absolute difference between DI+ and DI-. This calculation helps determine the strength of a trend without considering its direction.

Trend Duration Analysis: Tracks and calculates the duration of strong and weak trends, as well as DI+ and DI- durations. This analysis provides a detailed view of how long a trend has been in place, helping traders assess the reliability of the trend.

Alert System: Provides a robust alert system that triggers notifications for strong trends, weak trends, and DI crossovers. The alerts are based on specific conditions such as the duration of the trend or the crossover of directional indicators, ensuring traders are informed about critical market movements.

Visual Enhancements: Utilizes color gradients and background settings to visually represent trend strength and duration. This feature enhances the visual analysis of trends, making it easier for traders to identify significant market changes at a glance.

In the example below, we see the ADX weakening after we have just had a move up, if you are looking to get into this position you want to see the ADX growing with either the DI+ or DI- breaking their average durations.

As you can see below, although the ADX manages to move above the threshold, there are no DI+/- breaks which is shown by price moving sideways. Not something most traders would be interested in.

Application

Strategic Decision-Making: Assists traders in making informed decisions by providing detailed analysis of ADX movements and trend durations. By understanding the strength and direction of trends, traders can better time their entries and exits.

Trend Confirmation: Reinforces trading strategies by confirming potential reversals and trend strength through ADX and DI analysis. This confirmation helps traders validate their trading signals, reducing the risk of false signals.

Customized Analysis: Adapts to various trading styles with extensive input settings that control the display and sensitivity of trend data. Traders can customize the indicator to suit their specific needs, making it a versatile tool for different trading strategies.

The Advanced ADX Analysis by is an invaluable addition to a trader's toolkit, offering depth and precision in market trend analysis to navigate complex market conditions effectively. With its comprehensive tracking, alert system, and customizable display options, this indicator provides traders with the tools they need to stay ahead of the market.

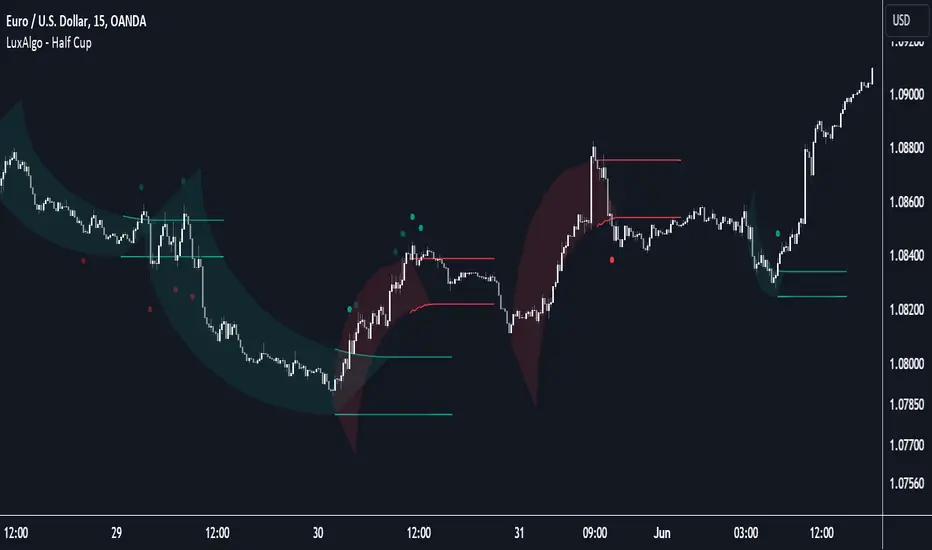

Half Cup [LuxAlgo]The Half Cup indicator detects and displays patterns with the shape of a Half Cup , initiating a channel. From this channel, breakouts are detected and highlighted with dots.

Users can control the shape of the Half Cup and the channel length through various settings.

Do note that the displayed half cups are displayed retrospectively, making them subject to backpainting.

🔶 USAGE

The idea behind the indicator is derived from the Cup & Handle pattern, which requires waiting for the pattern full completion.

Our Half Cup publication aims to find opportunities when the potential cup is only formed halfway.

In this example, a green dot shows the first breakout of the upper channel extremity. A few bars later, the price went under it, after which it returned above, triggering a second green dot. Both triggers were good opportunities in this case, and the price rose afterward.

The Half Cup pattern can be the start of a potential complete Cup & Handle (As in the example above, a complete Cup pattern (without the Handle ) is shown, manually drawn with dashed lines).

Every green/red dot, whether on a bullish or bearish pattern, points to a breakout respectively above/below the channel.

Besides drawing patterns and the corresponding breakouts, the Half Cup indicator can also provide insights into trends and potential opportunities in the long run.

🔶 DETAILS

🔹 Validation

Several criteria must be fulfilled before a visible pattern on the chart is drawn.

Calculations are done beforehand to know where the Half Cup pattern would be positioned.

The pattern's bottom and top edges are checked for the number of bars whose closing price is outside the half-cup area. When the number of breakouts above/below is equal to or lower than the user-defined settings ( Max % Breaks Top/Bottom ), the pattern is drawn together with a brighter-colored channel next to it.

Dots highlighting the channel's breakout can be drawn from that moment until the end of both channel lines.

🔹 Positioning

Users can adjust the following settings to fit their needs:

% Broadness: Moves the Top/Bottom line (bullish or bearish) diagonally upwards/downwards.

Vertical Shift: Shifts the entire pattern up/down.

Channel Length: Sets the line length of the channel.

Note that adjusting the position of the pattern will change the validation; the script will be rerun to check if patterns are still valid or if new patterns can be drawn. Some patterns may disappear, while new ones may appear.

Before adjusting the position, the user can set Max % Breaks Top/Bottom at 100%. When the positioning is set, Max % Breaks Top/Bottom can be set as desired.

🔹 Updated Drawings

The Half Cup pattern is always drawn retrospectively (that is it is subject to backpainting), the channel is drawn from the bar from where the pattern is detected. Every breakout of the channel will remain visible as dots.

When a new swing high/low is found while the previous swing low/high remains the same, the pattern is updated to minimize clutter. The dots of earlier drawings will remain visible (to ensure no repainting occurs), but the color becomes faded, as such bright dots are associated with patterns that are visible on the chart, while faded dots are from removed/updated patterns.

🔶 SETTINGS

Swing Length: Period used for the swing detection, with higher values returning longer-term Swing Levels.

🔹 Validation

Max % Breaks Bottom: Allowed maximum amount of bars where the closing price is below the bottom of the Half Cup pattern against the total width of the pattern (bars).

Max % Breaks Top: Allowed maximum amount of bars where the closing price is above the top of the Half Cup pattern against the total width of the pattern (bars).

🔹 Positioning

% Broadness: Moves the Top/Bottom line (bullish or bearish) diagonally upwards/downwards.

Vertical Shift: Shifts the entire pattern up/down.

Channel Length: Sets the line length of the channel.

Uptrick: Bullish/Bearish Signal DetectorDetailed Explanation of the "Uptrick: Bullish/Bearish Signal Detector" Script

The "Uptrick: Bullish/Bearish Signal Detector" script is a sophisticated tool designed for the TradingView platform, leveraging Pine Script version 5. This script is crafted to enhance traders' ability to identify bullish (buy) and bearish (sell) signals directly on their trading charts. By combining the power of the MACD (Moving Average Convergence Divergence) and RSI (Relative Strength Index) indicators, this script provides a unique and efficient method for detecting potential trading opportunities. Below is an in-depth exploration of its purpose, features, and functionality.

Purpose

The primary purpose of this script is to assist traders in identifying potential entry and exit points in the market by signaling bullish and bearish conditions. This automated detection helps traders make more informed decisions without the need to manually analyze complex indicators. By overlaying signals directly on the price chart, the script allows for quick visual identification of market trends and reversals.

Uniqueness

What sets this script apart is its dual use of MACD and RSI indicators. While many trading strategies might rely on a single indicator, combining MACD and RSI enhances the reliability of the signals by filtering out false positives. The script not only identifies trends but also adds a layer of confirmation through the RSI, which measures the speed and change of price movements.

Inputs and Features

Customizable Label Appearance:

The script allows users to customize the appearance of the labels that indicate bullish and bearish signals. Users can set their preferred colors for the labels and the text, ensuring that the signals are easily distinguishable and aesthetically pleasing on their charts.

MACD Calculation:

The script calculates the MACD line and signal line using user-defined input values for the fast length, slow length, and signal length. The MACD histogram, which is the difference between the MACD line and the signal line, is used to determine the momentum of the market.

RSI Calculation:

The RSI is calculated using a user-defined input length. The RSI helps in identifying overbought or oversold conditions, which are crucial for confirming the strength of the trend detected by the MACD.

Bullish and Bearish Conditions:

The script defines bullish conditions as those where the MACD histogram is positive and the RSI is above 50. Bearish conditions are defined where the MACD histogram is negative and the RSI is below 50. This combination of conditions ensures that signals are generated based on both momentum and relative strength, reducing the likelihood of false signals.

Label Plotting:

The script plots labels on the chart to indicate bullish and bearish signals. When a bullish condition is met, and the previous signal was not bullish, a "LONG" label is plotted. Similarly, when a bearish condition is met, and the previous signal was not bearish, a "SHORT" label is plotted. This feature helps in clearly marking the points of interest for traders, making it easier to spot potential trades.

Tracking Previous Signals:

To avoid repetitive signals, the script keeps track of the last signal. If the last signal was bullish, it avoids plotting another bullish signal immediately. The same logic applies to bearish signals. This tracking ensures that signals are spaced out and only significant changes in market conditions are highlighted.

How It Works

The script operates in a loop, processing each bar (or candlestick) on the chart as new data comes in. It calculates the MACD and RSI values for each bar and checks if the current conditions meet the criteria for a bullish or bearish signal. If a signal is detected and it is different from the last signal, a label is plotted on the chart at the current bar's price level. This real-time processing allows traders to see the signals as they form, providing timely insights into market movements.

Practical Application

For practical use, a trader would add this script to their TradingView chart. They can customize the input parameters for the MACD and RSI calculations to fit their trading strategy or preferred settings. Once added, the script will automatically analyze the price data and start plotting "LONG" and "SHORT" labels based on the detected signals. Traders can then use these labels to make decisions on entering or exiting trades, adjusting their strategy as necessary based on the signals provided.

Conclusion

The "Uptrick: Bullish/Bearish Signal Detector" script is a powerful tool for any trader looking to leverage technical indicators for better trading decisions. By combining MACD and RSI, it offers a robust method for detecting market trends and potential reversals. The customizable features and real-time signal plotting make it a versatile and user-friendly addition to any trading toolkit. This script not only simplifies the process of technical analysis but also enhances the accuracy of trading signals, thereby potentially increasing the trader's success rate in the market.

FVG Instantaneous Mitigation Signals [LuxAlgo]The FVG Instantaneous Mitigation Signals indicator detects and highlights "instantaneously" mitigated fair value gaps (FVG), that is FVGs that get mitigated one bar after their creation, returning signals upon mitigation.

Take profit/stop loss areas, as well as a trailing stop loss are also included to complement the signals.

🔶 USAGE

Instantaneous Fair Value Gap mitigation is a new concept introduced in this script and refers to the event of price mitigating a fair value gap one bar after its creation.

The resulting signal sentiment is opposite to the bias of the mitigated fair value gap. As such an instantaneously mitigated bearish FGV results in a bullish signal, while an instantaneously mitigated bullish FGV results in a bearish signal.

Fair value gap areas subject to instantaneous mitigation are highlighted alongside their average level, this level is extended until reached in a direction opposite to the FVG bias and can be used as a potential support/resistance level.

Users can filter out less volatile fair value gaps using the "FVG Width Filter" setting, with higher values highlighting more volatile fair value gaps subject to instantaneous mitigation.

🔹 TP/SL Areas

Users can enable take-profit/stop-loss areas. These are displayed upon a new signal formation, with an area starting from the mitigated FVG area average to this average plus/minus N ATRs, where N is determined by their respective multiplier settings.

Using a higher multiplier will return more distant areas from the price, requiring longer-term variations to be reached.

🔹 Trailing Stop Loss

A trailing-stop loss is included, increasing when the price makes a new higher high or lower low since the trailing has been set. Using a higher trailing stop multiplier will allow its initial position to be further away from the price, reducing its chances of being hit.

The trailing stop can be reset on "Every Signal", whether they are bullish or bearish, or only on an "Inverse Signal", which will reset the trailing when a signal of opposite bias is detected, this will preserve an existing trailing stop when a new signal of the same bias to the present one is detected.

🔶 DETAILS

Fair Value Gaps are ubiquitous to price action traders. These patterns arise when there exists a disparity between supply and demand. The action of price coming back and filling these imbalance areas is referred to as "mitigation" or "rebalancing".

"Instantaneous mitigation" refers to the event of price quickly mitigating a prior fair value gap, which in the case of this script is one bar after their creation. These events are indicative of a market more attentive to imbalances, and more willing to correct disparities in supply and demand.

If the market is particularly sensitive to imbalances correction then these can be excessively corrected, leading to further imbalances, highlighting a potential feedback process.

🔶 SETTINGS

FVG Width Filter: Filter out FVGs with thinner areas from returning a potential signal.

🔹 TP/SL

TP Area: Enable take-profit areas for new signals.

Multiplier: Control the distance from the take profit and the price, with higher values returning more distant TP's.

SL Area: Enable stop-loss areas for new signals.

Multiplier: Control the distance from the stop loss and the price, with higher values returning more distant SL's.

🔹 Trailing Stop

Reset Trailing Stop: Determines when the trailing stop is reset.

Multiplier: Controls the initial position of the trailing stop, with higher values returning more distant trailing stops.

Inversion Fair Value Gaps [TradingFinder] IFVG ICT Signal| Alert🔵 Introduction

🟣 Inversion Fair Value Gap (IFVG)

An ICT Inversion Fair Value Gap, or reverse FVG, occurs when a fair value gap fails to hold its price, resulting in the price moving beyond and breaking the gap. This situation marks the initial change in price momentum.

Generally, prices respect fair value gaps and continue in their trend direction. However, when a fair value gap is breached, it transforms into an inversion fair value gap, signaling a potential short-term reversal or a subsequent change in direction.

🔵 How to Use

🟣 Identifying an Inversion Fair Value Gap

To spot an IFVG, you must first identify a fair value gap.

Inversion fair value gaps can be categorized into two types :

🟣 Bullish Inversion Fair Value Gap

A bullish IFVG occurs when a bearish fair value gap is invalidated by the price closing above it.

Steps to identify it :

Identify a bearish fair value gap.

When the price closes above this gap, it becomes a bullish inversion fair value gap.

This gap acts as a support level, pushing the price upwards and indicating a shift in momentum from sellers to buyers.

🟣 Bearish Inversion Fair Value Gap

A bearish IFVG happens when a bullish fair value gap fails, with the price closing below it.

Steps to identify it :

Identify a bullish fair value gap.

When the price closes below this gap, it becomes a bearish inversion fair value gap.

This gap acts as a resistance level, pushing the price downwards and indicating a shift in momentum from buyers to sellers.

🔵 Settings

🟣 Global Settings

Show All Inversion FVG: If disabled, only the most recent FVG will be displayed.

IFVG Validity Period (Bar): Determines the maximum duration (in number of candles) that the FVG and IFVG remain valid.Switching Colors Theme Mode: Includes three modes: "Off", "Light", and "Dark". "Light" mode adjusts colors for light mode use, "Dark" mode adjusts colors for dark mode use, and "Off" disables color adjustments.

🟣 Logic Settings

FVG Filter : This refines the number of identified FVG areas based on a specified algorithm to focus on higher quality signals and reduce noise.

Types of FVG filters :

Very Aggressive Filter : Adds a condition where, for an upward FVG, the last candle's highest price must exceed the middle candle's highest price, and for a downward FVG, the last candle's lowest price must be lower than the middle candle's lowest price. This minimally filters out FVGs.

Aggressive Filte r: Builds on the Very Aggressive mode by ensuring the middle candle is not too small, filtering out more FVGs.

Defensive Filter : Adds criteria regarding the size and structure of the middle candle, requiring it to have a substantial body and specific polarity conditions, filtering out a significant number of FVGs.

Very Defensive Filter : Further refines filtering by ensuring the first and third candles are not small-bodied doji candles, retaining only the highest quality signals.

Mitigation Level FVG and IFVG : Options include "Proximal", "Distal", or "50 % OB" modes, which you can choose based on your needs. The "50 % OB" line is the midpoint between distal and proximal.

🟣 Display Settings

Show Bullish IFVG : Toggles the display of demand-related boxes.

Show Bearish IFVG : Toggles the display of supply-related boxes.

🟣 Alert Settings

Alert Inversion FVG Mitigation : Enables alerts for Inversion FVG mitigation.

Message Frequency : Determines the frequency of alerts. Options include 'All' (every function call), 'Once Per Bar' (first call within the bar), and 'Once Per Bar Close' (final script execution of the real-time bar). Default is 'Once per Bar'.

Show Alert Time by Time Zone : Configures the time zone for alert messages. Default is 'UTC'.

Display More Info : Provides additional details in alert messages, including price range, date, hour, and minute. Set to 'Off' to exclude this information.

Candle Body Support/Resistance [LuxAlgo]The Candle Body Support/Resistance indicator is a tool that provides Support/Resistance levels from high-volatility candles, a concept originally described by Steve Nison in "Beyond Candlesticks".

Users can define the candle body percentage used to set the detected support/resistance levels. Occurrences of price testing the returned levels are highlighted using user-customizable dots.

🔶 USAGE

Support/Resistance levels are drawn from volatile candles, that is candles having a body (range between opening and closing price) whose magnitude is larger than the Volatility Threshold , which is determined by the multiplicative factor of an ATR (Average True Range) using a user set length.

The level starts from the opening price +/- a percentage of the open-close range. Users can adjust the percentage of the candle body used as support/resistance levels respectively, with higher percentage values returning levels prone to get reached sooner by the price.

A test is considered valid when a wick passes through the Support/Resistance level while the closing price is not breaking it.

Two modes are included, Trailing and Historical , both affecting the displayed elements of the indicator, these are described in the sub-section below.

🔹 Historical

The Historical Mode will draw a separate line from every Volatile Candle . When this line is tested, a dot will be drawn.

In the above example, the red resistance line was tested once until a bullish volatile candle formed, which closed just below the resistance level. The resistance level was tested again, after which the newly created support level was broken quickly, and the price decreased. These levels proved helpful later, acting as resistance/support levels (illustrated by the extra manually drawn dashed white lines).

To prevent cluttering Support/Resistance , lines will be deleted when the line is mitigated and hasn't been tested.

When a Support/Resistance line reaches its Maximum Line Length , it will also be deleted when it has not been tested.

🔹 Trailing

When a new volatile candle of the same type (bullish/bearish) appears while the Support/Resistance isn't broken, this line will be updated with the values of the new volatile candle. This creates a trailing line and a less cluttered chart.

Unlike the Historical mode , a line will not be deleted after a while or when it is mitigated. Instead, the line won't be updated anymore. A new line will start from the next found volatile candle.

Using the same situation as the Historical Mode example, we can note the future significance of old support/resistance levels (illustrated by the extra manually drawn dashed white lines).

The user can switch between these 2 modes, each offering a unique perspective on the market. This provides a more in-depth examination of the market, enhancing the user's trading analysis.

Using a copy of our indicator while using both modes can also be helpful.

🔶 DETAILS

The Support level is the opening price of a bullish volatile candle plus a user-set percentage of the candle's body, while the Resistance level is the opening price of a bearish volatile candle minus a percentage of the candle's body.

The following example illustrates the ATR with the multiplicative factor (Volatility Threshold) where the body of Volatile candles exceeds the ATR limits. Changing the Volatility Threshold and ATR length gives users extra flexibility to adjust to their needs.

🔹 Max Line Length

When using the Historical Mode and the duration of a displayed level reaches the user-set Max Line Length value, the level will return to the last test or be deleted when it has not been tested.

🔶 SETTINGS

Display Mode: Display mode of the indicator.

Support %: Sets the distance of the Support Line from the opening price relative to the candle body.

Resistance %: Sets the distance of the Resistance Line from the opening price relative to the candle body.

🔹 Filter

Length ATR: Amount of bars for the calculation of the Average True Range.

Volatility Threshold: multiplicative factor of ATR.

Max Line Length: Maximum allowed duration/length (in bars) of a Support/Resistance level.

FVG & IFVG ICT [TradingFinder] Inversion Fair Value Gap Signal🔵 Introduction

🟣 Fair Value Gap (FVG)

To spot a Fair Value Gap (FVG) on a chart, you need to perform a detailed candle-by-candle analysis.

Here’s the process :

Focus on Candles with Large Bodies : Identify a candle with a substantial body and examine it alongside the preceding candle.

Check Surrounding Candles : The candles immediately before and after the central candle should have long shadows.

Ensure No Overlap : The bodies of the candles before and after the central candle should not overlap with the body of the central candle.

Determine the FVG Range : The gap between the shadows of the first and third candles forms the FVG range.

🟣 ICT Inversion Fair Value Gap (IFVG)

An ICT Inversion Fair Value Gap, also known as a reverse FVG, is a failed fair value gap where the price does not respect the gap. An IFVG forms when a fair value gap fails to hold the price and the price moves beyond it, breaking the fair value gap.

This marks the initial shift in price momentum. Typically, when the price moves in one direction, it respects the fair value gaps and continues its trend.

However, if a fair value gap is violated, it acts as an inversion fair value gap, indicating the first change in price momentum, potentially leading to a short-term reversal or a subsequent change in direction.

🟣 Bullish Inversion Fair Value Gap (Bullish IFVG)

🟣 Bearish Inversion Fair Value Gap (Bearish IFVG)

🔵 How to Use

🟣 Identify an Inversion Fair Value Gap

To identify an IFVG, you first need to recognize a fair value gap. Just as fair value gaps come in two types, inversion fair value gaps also fall into two categories:

🟣 Bullish Inversion Fair Value Gap

A bullish IFVG is essentially a bearish fair value gap that is invalidated by the price closing above it.

Here’s how to identify it :

Identify a bearish fair value gap.

When the price closes above this bearish fair value gap, it transforms into a bullish inversion fair value gap.

This gap acts as support for the price and drives it upwards, indicating a reduction in sellers' strength and an initial shift in momentum towards buyers.

🟣 Bearish Inversion Fair Value Gap

A bearish IFVG is primarily a bullish fair value gap that fails to hold the price, with the price closing below it.

Here’s how to identify it :

Identify a bullish fair value gap.

When the price closes below this gap, it becomes a bearish inversion fair value gap.

This gap acts as resistance for the price, pushing it downwards. A bearish inversion fair value gap signifies a decrease in buyers' momentum and an increase in sellers' strength.

🔵 Setting

🟣 Global Setting

Show All FVG : If it is turned off, only the last FVG will be displayed.

S how All Inversion FVG : If it is turned off, only the last FVG will be displayed.

FVG and IFVG Validity Period (Bar) : You can specify the maximum time the FVG and the IFVG remains valid based on the number of candles from the origin.

Switching Colors Theme Mode : Three modes "Off", "Light" and "Dark" are included in this parameter. "Light" mode is for color adjustment for use in "Light Mode".

"Dark" mode is for color adjustment for use in "Dark Mode" and "Off" mode turns off the color adjustment function and the input color to the function is the same as the output color.

🟣 Logic Setting

FVG Filter

When utilizing FVG filtering, the number of identified FVG areas undergoes refinement based on a specified algorithm. This process helps to focus on higher quality signals and eliminate noise.

Here are the types of FVG filters available :

Very Aggressive Filter : Introduces an additional condition to the initial criteria. For an upward FVG, the highest price of the last candle must exceed the highest price of the middle candle. Similarly, for a downward FVG, the lowest price of the last candle should be lower than the lowest price of the middle candle. This mode minimally filters out FVGs.

Aggressive Filter : Builds upon the Very Aggressive mode by considering the size of the middle candle. It ensures the middle candle is not too small, thereby eliminating more FVGs compared to the Very Aggressive mode.

Defensive Filter : In addition to the conditions of the Very Aggressive mode, the Defensive mode incorporates criteria regarding the size and structure of the middle candle. It requires the middle candle to have a substantial body, with specific polarity conditions for the second and third candles relative to the first candle's direction. This mode filters out a significant number of FVGs, focusing on higher-quality signals.

Very Defensive Filter : Further refines filtering by adding conditions that the first and third candles should not be small-bodied doji candles. This stringent mode eliminates the majority of FVGs, retaining only the highest quality signals.

Mitigation Level FVG and IFVG : Its inputs are one of "Proximal", "Distal" or "50 % OB" modes, which you can enter according to your needs. The "50 % OB" line is the middle line between distal and proximal.

🟣 Display Setting

Show Bullish FVG : Enables the display of demand-related boxes, which can be toggled on or off.

Show Bearish FVG : Enables the display of supply-related boxes along the path, which can also be toggled on or off.

Show Bullish IFVG : Enables the display of demand-related boxes, which can be toggled on or off.

Show Bearish IFVG : Enables the display of supply-related boxes along the path, which can also be toggled on or off.

🟣 Alert Setting

Alert FVG Mitigation : If you want to receive the alert about FVG's mitigation after setting the alerts, leave this tick on. Otherwise, turn it off.

Alert Inversion FVG Mitigation : If you want to receive the alert about Inversion FVG's mitigation after setting the alerts, leave this tick on. Otherwise, turn it off.

Message Frequency : This parameter, represented as a string, determines the frequency of announcements. Options include: 'All' (triggers the alert every time the function is called), 'Once Per Bar' (triggers the alert only on the first call within the bar), and 'Once Per Bar Close' (activates the alert only during the final script execution of the real-time bar upon closure). The default setting is 'Once per Bar'.

Show Alert time by Time Zone : The date, hour, and minute displayed in alert messages can be configured to reflect any chosen time zone. For instance, if you prefer London time, you should input 'UTC+1'. By default, this input is configured to the 'UTC' time zone.

Display More Info : The 'Display More Info' option provides details regarding the price range of the order blocks (Zone Price), along with the date, hour, and minute. If you prefer not to include this information in the alert message, you should set it to 'Off'.

ICT Propulsion Block [LuxAlgo]The ICT Propulsion Block indicator is meant to detect and highlight propulsion blocks, which are specific price structures introduced by the Inner Circle Trader (ICT).

Propulsion Blocks are essentially blocks located where prices interact with preceding order blocks. Traders often utilize them when analyzing price movements to identify potential turning points and market behavior or areas of interest in the market.

🔶 USAGE

An order block is a significant area on a price chart where there was a notable accumulation or distribution of orders, often identified by a strong move in price followed by a consolidation or sideways movement. Traders use order blocks to identify potential support or resistance levels.

A Propulsion Block, on the other hand, is a concept taught by the Inner Circle Trader (ICT) and refers to a specific type of order block that interacts with the preceding order block. Traders often analyze propulsion blocks to identify potential turning points and areas of interest in the market.

A mitigated order block refers to an order block that has been invalidated or nullified due to subsequent market movements or developments. It no longer holds the same significance or relevance in the current market context.

Let's explore a bearish order block and propulsion block scenario commonly utilized by ICT traders in their trading strategies.

🔶 SETTINGS

🔹 Order & Propulsion Blocks

Swing Detection Length: Lookback period used to detect swing points for creating order blocks and/or propulsion blocks.

Mitigation Price: Allows users to choose between the closing price or the candle's wick for mitigation.

Highlight Propulsion Block Signals: Highlights the propulsion block and its sentiment for easier identification and analysis.

Remove Unassociated Order Blocks: Eliminate order blocks that are not associated with any propulsion block.

Remove Mitigated Blocks: Eliminates mitigated order blocks and propulsion blocks along with their associated order blocks, streamlining the visualization for clearer analysis.

Most Recent Blocks: Activates processing of the specified number of most recent blocks according to the option. If not enabled, the script defaults to processing the last 125 occurrences.

🔹 Order & Propulsion Blocks Style

Bullish Order & Propulsion Blocks: Toggles the visibility of bullish order and propulsion blocks, along with color customization options.

Bearish Order & Propulsion Blocks: Toggles the visibility of bearish order and propulsion blocks, along with color customization options.

Block Labels: Toggles the visibility of order and propulsion block labels, and label size customization option.

🔶 RELATED SCRIPTS

Order-Blocks-Breaker-Blocks .

ACD Indicator [TradingFinder] M Fisher Pivots Methodology Signal🔵 Introduction

The book "The Logical Trader" begins with a comprehensive review of the ACD Methodology principles, which include identifying specific price points related to the opening range.

This method allows you to set reference points for trading and use points "A" and "C" for trade entry. You will also learn about the "Pivot Range" and how to combine them with the ACD method to maximize position size and minimize risk.

In this indicator, the strategy is implemented to make it easier to use.

🔵 How to Use

The "ACD" strategy can be applied to various markets such as stocks, commodities, or forex, providing buy and sell signals that allow you to set your price targets and stop losses.

This strategy is based on the assumption that the opening range of trades is statistically significant each day, meaning the initial market fluctuations influence the market until the end of the day.

The ACD trading strategy is known as a breakout strategy and performs best in volatile or strongly trending markets, such as crude oil and stocks.

Some of the rules for using the ACD strategy include the following :

Consider points A and C as reference points and continuously pay attention to these points during trades. These points serve as entry and exit points for trades.

Examine daily and multi-day pivot ranges to analyze market trends. If the price is above the pivots, the trend is upward, and if below the pivots, the trend is downward.

Trading with the ACD strategy in forex is possible using the ACD indicator. This indicator is a technical tool used to measure the balance between supply and demand in the market. By analyzing trading volume and price, this indicator helps traders identify trend strength and suitable entry and exit points.

To use the ACD indicator, consider the following :

Identifying strong trends: The ACD indicator can help you identify strong and stable trends in the market.

Determining entry and exit points: ACD provides buy and sell signals to enter or exit trades at the best possible time.

Bullish Setup :

When the "A up" line is broken, it is advisable to wait for some time to ensure that this is not a "Fake Breakout" and that the price stabilizes above this line.

After entering the trade, the best stop loss you can choose is below the "A down" line. However, it is recommended to test this in backtests to achieve the best results. The suitable reward-to-risk ratio for this strategy is 1, which should also be backtested.

Bearish Setup :

When the "A down" line is broken, it is advisable to wait for some time to ensure that this is not a "Fake Breakout" and that the price stabilizes below this line.

After entering the trade, the best stop loss you can choose is above the "A up" line. However, it is recommended to test this in backtests to achieve the best results. The suitable reward-to-risk ratio for this strategy is 1, which should also be backtested.

🔵 Setting

NDay Pivot Range Period : Using this entry you can specify the number of days to calculate NDay Pivot Range.

Show Daily Pivot Range : Set the Daily Pivot color and displayed or not.

Show NDay Pivot Range : Set the NDay Pivot color and displayed or not.

ATR Period Levels : Determining the period of the ATR indicator, which is used to determine the A and C levels.

Show Tokyo ACD Setup : Set the Tokyo ACD Setup color and displayed or not.

Tokyo Opening Range Time : The amount of time taken to determine the opening range. You can set this number between 5 and 60 minutes.

Tokyo Session : Market start and end time.

A Level Multiplier : The coefficient that is multiplied by ATR to determine the distance of line A up and A down.

C Level Multiplier : The coefficient that is multiplied by ATR to determine the distance of line C up and C down.

The same settings exist for the London and New York sessions.

Swing Failure Zones and Signals [AlgoAlpha]Elevate your trading strategy with the Swing Failure Zones and Signals indicator by AlgoAlpha! This powerful tool helps you identify potential swing failure zones, offering clear bullish and bearish signals to guide your trading decisions. 📈💡

🎨 Bullish/Bearish Color Customization : Easily set the colors for bullish and bearish signals to match your chart preferences.

🧹 Mitigated Zone Removal : Option to remove mitigated zones from the chart for a cleaner view.

🔍 Range High/Low Lookback : Adjustable lookback period for determining significant highs and lows.

🖌 Dynamic Zone Creation : Automatically draws zones based on swing failure criteria.

🔔 Alert Conditions : Set alerts for both bullish and bearish swing failure conditions to stay informed without constant monitoring.

Quick Guide to Using the Swing Failure Zones and Signals Indicator

🛠 Add the Indicator : Search for "Swing Failure Zones and Signals " in TradingView's Indicators & Strategies. Customize settings like lookback period, colors, and zone removal options to fit your trading style.

📊 Market Analysis : Watch for the appearance of the zones and the directional arrows for potential reversal signals. Use these signals to identify key market entries and exits.

🔔 Alerts : Enable alerts for bullish and bearish swing failure conditions to capture trading opportunities without constant chart monitoring.

How it works

The indicator calculates the direction and length of each candle to identify swing failure points by comparing current high and low prices with those from the lookback period. A bullish swing failure is detected when the current low is lower than the previous low and the close is higher than the previous high, while a bearish swing failure occurs when the current high is higher than the previous high and the close is lower than the previous low. Upon detection, the script creates zones on the chart to indicate these failure points and manages them by removing invalidated zones based on the user's settings. Visual signals are plotted on the chart as arrows, and alerts are set for these conditions to help traders capture potential entry opportunities efficiently.

Enhance your trading edge with this robust tool designed to spotlight critical swing failure points in the market! 💪📈

Linear Regression Oscillator [ChartPrime]Linear Regression Oscillator Indicator

Overview:

The Linear Regression Oscillator is a custom TradingView indicator designed to provide insights into potential mean reversion and trend conditions. By calculating a linear regression on the closing prices over a user-defined period, this oscillator helps identify overbought and oversold levels and highlights trend changes. The indicator also offers visual cues and color-coded price bars to aid in quick decision-making.

Key Features:

◆ Customizable Look-Back Period:

Input: Length

Default: 20

Description: Determines the period over which the linear regression is calculated. A longer period smooths the oscillator but may lag, while a shorter period is more responsive but may be noisier.

◆ Overbought and Oversold Thresholds:

Inputs: Upper Threshold and Lower Threshold

Default: 1.5 and -1.5 respectively

Description: Define the upper and lower bounds for identifying overbought and oversold conditions. Values outside these thresholds suggest potential reversals.

◆ Candlestick Color Plotting:

Input: Plot Bar Color

Default: false

Description: Option to color the price bars based on the oscillator's value, providing a visual representation of market conditions. Bars turn cyan for positive oscillator values and blue for negative.

◆ Mean Reversion and Trend Signals:

Visual markers and labels indicate when the oscillator suggests mean reversion or trend changes, aiding in identifying key market turning points.

◆ Invalidation Levels:

Tracks the highest and lowest prices over a recent period to set levels where the current trend signal would be considered invalidated.

◆ Gradient Color Coding:

Utilizes gradient color coding to enhance the visualization of oscillator values, making it easier to interpret overbought and oversold conditions.

◆ Usage Notes:

Setting the Look-Back Period:

Adjust the "Length" input based on the timeframe and the type of trading you are conducting. Shorter periods are more suited for intraday trading, while longer periods can be used for swing trading.

Interpreting Thresholds:

Use the upper and lower threshold inputs to fine-tune the sensitivity of the overbought and oversold signals. Higher absolute values reduce the number of signals but increase their reliability.

Candlestick Coloring:

Enabling the "Plot Bar Color" option can help quickly identify the current state of the oscillator in relation to the zero line. This visual aid can be particularly useful in fast-moving markets.

Mean Reversion and Trend Signals:

Pay attention to the symbols and labels on the chart indicating mean reversion and trend changes. These signals are designed to highlight potential entry and exit points.

Invalidation Levels:

Use the plotted invalidation levels as stop-loss or signal invalidation points. If the price moves beyond these levels, the current trend signal is likely invalid.

This indicator helps traders identify overbought and oversold conditions, potential mean reversions, and trend changes based on the linear regression of the closing prices over a specified look-back period.

Advanced Awesome Oscillator [CryptoSea]Advanced AO Analysis Indicator

The Advanced AO Analysis indicator is a sophisticated tool designed to evaluate the Awesome Oscillator (AO) in search of regular and hidden divergences that signal potential price reversals. By tracking the intensity and duration of the AO's movements, this indicator aids traders in pinpointing critical points in price action.

Key Features

Divergence Detection: Identifies both regular and hidden bullish and bearish divergences, providing early signs of potential market reversals.

Customizable Lookback Periods: Allows users to set specific lookback windows to define the strength and relevance of detected divergences.

Adaptive Oscillator Display: Features customizable display options for the AO, enabling users to view data in different modes suited to their analysis needs.

Alert System: Includes configurable alerts to notify users of potential divergence formations, helping traders respond promptly.

How it Works

AO Calculation: Computes the AO as the difference between short-term and long-term moving averages of the midpoints of bars, highlighting momentum shifts.

Pivot Point Analysis: Utilizes advanced algorithms to find low and high pivot points based on the oscillator values, crucial for spotting trend reversals.

Range Validation: Verifies that divergences occur within a predefined range from pivot points, ensuring their validity and strength.

Visualisation: Plots AO values and potential divergences directly on the chart, aiding in quick visual analysis.

Application

Strategic Decision-Making: Assists traders in making informed decisions by providing detailed analysis of AO movements and divergence.

Trend Confirmation: Reinforces trading strategies by confirming potential reversals with pivot point detection and divergence analysis.

Behavioural Insight: Offers insights into market dynamics and sentiment by analyzing the depth and duration of AO cycles above and below zero.

The Advanced AO Analysis indicator equips traders with a powerful analytical tool for studying the Awesome Oscillator in-depth, enhancing their ability to spot and act on divergence-based trading opportunities in the cryptocurrency markets.

Enhanced Reversal DetectionScript Description:

The "Enhanced Reversal Detection" indicator is a powerful tool designed to identify potential market reversals across various financial instruments. It incorporates a sophisticated algorithm that analyzes price action along with key technical indicators such as the Relative Strength Index (RSI), Bollinger Bands, and Moving Average (MA).

How to Use:

Adjustable Parameters: The indicator offers a range of adjustable parameters to cater to different trading preferences and market conditions.

RSI Length: Adjusts the length of the RSI calculation to fine-tune sensitivity.

Overbought Level: Sets the threshold for identifying overbought conditions on the RSI scale.

Oversold Level: Sets the threshold for identifying oversold conditions on the RSI scale.

Bollinger Bands Length: Determines the length of the Bollinger Bands calculation.

Bollinger Bands Multiplier: Adjusts the standard deviation multiplier for the Bollinger Bands, influencing band width.

Moving Average Length: Defines the length of the Moving Average calculation to capture trend direction.

Min Bars Between Signals: Sets the minimum number of bars required between consecutive reversal signals.

ADX Length: Adjusts the length of the Average Directional Index (ADX) calculation.

ADX Threshold: Defines the threshold value for ADX, serving as a filter for reversal signals.

Signal Generation: The indicator generates signals for both bullish and bearish reversals based on predefined criteria. A bullish reversal signal is triggered when the closing price exceeds the lower Bollinger Band and RSI falls below the oversold threshold. Conversely, a bearish reversal signal occurs when the closing price falls below the upper Bollinger Band and RSI surpasses the overbought threshold.

Alerts: Traders can opt to receive alerts for bullish and bearish reversal signals, enabling them to stay informed of potential trading opportunities even when away from the platform.

Publication Readiness:

To ensure readiness for publication in the TradingView public library, the script has been meticulously crafted and documented:

The code is extensively commented to provide clear explanations of parameters, calculations, and signal generation logic.

Best coding practices have been followed to enhance readability and maintainability.

Rigorous testing has been conducted to validate the accuracy and reliability of signal generation across various market conditions.

The script adheres to TradingView's guidelines and policies for script publication, ensuring compliance with platform standards and user expectations.

With its comprehensive features and user-friendly design, the "Enhanced Reversal Detection" indicator is poised to become a valuable asset for traders seeking to identify high-probability reversal opportunities in the financial markets.

Bayesian Trend Indicator [ChartPrime]Bayesian Trend Indicator

Overview:

In probability theory and statistics, Bayes' theorem (alternatively Bayes' law or Bayes' rule), named after Thomas Bayes, describes the probability of an event, based on prior knowledge of conditions that might be related to the event.

The "Bayesian Trend Indicator" is a sophisticated technical analysis tool designed to assess the direction of price trends in financial markets. It combines the principles of Bayesian probability theory with moving average analysis to provide traders with a comprehensive understanding of market sentiment and potential trend reversals.

At its core, the indicator utilizes multiple moving averages, including the Exponential Moving Average (EMA), Simple Moving Average (SMA), Double Exponential Moving Average (DEMA), and Volume Weighted Moving Average (VWMA) . These moving averages are calculated based on user-defined parameters such as length and gap length, allowing traders to customize the indicator to suit their trading strategies and preferences.

The indicator begins by calculating the trend for both fast and slow moving averages using a Smoothed Gradient Signal Function. This function assigns a numerical value to each data point based on its relationship with historical data, indicating the strength and direction of the trend.

// Smoothed Gradient Signal Function

sig(float src, gap)=>

ta.ema(source >= src ? 1 :

source >= src ? 0.9 :

source >= src ? 0.8 :

source >= src ? 0.7 :

source >= src ? 0.6 :

source >= src ? 0.5 :

source >= src ? 0.4 :

source >= src ? 0.3 :

source >= src ? 0.2 :

source >= src ? 0.1 :

0, 4)

Next, the indicator calculates prior probabilities using the trend information from the slow moving averages and likelihood probabilities using the trend information from the fast moving averages . These probabilities represent the likelihood of an uptrend or downtrend based on historical data.

// Define prior probabilities using moving averages

prior_up = (ema_trend + sma_trend + dema_trend + vwma_trend) / 4

prior_down = 1 - prior_up

// Define likelihoods using faster moving averages

likelihood_up = (ema_trend_fast + sma_trend_fast + dema_trend_fast + vwma_trend_fast) / 4

likelihood_down = 1 - likelihood_up

Using Bayes' theorem , the indicator then combines the prior and likelihood probabilities to calculate posterior probabilities, which reflect the updated probability of an uptrend or downtrend given the current market conditions. These posterior probabilities serve as a key signal for traders, informing them about the prevailing market sentiment and potential trend reversals.

// Calculate posterior probabilities using Bayes' theorem

posterior_up = prior_up * likelihood_up

/

(prior_up * likelihood_up + prior_down * likelihood_down)

Key Features:

◆ The trend direction:

To visually represent the trend direction , the indicator colors the bars on the chart based on the posterior probabilities. Bars are colored green to indicate an uptrend when the posterior probability is greater than 0.5 (>50%), while bars are colored red to indicate a downtrend when the posterior probability is less than 0.5 (<50%).

◆ Dashboard on the chart

Additionally, the indicator displays a dashboard on the chart , providing traders with detailed information about the probability of an uptrend , as well as the trends for each type of moving average. This dashboard serves as a valuable reference for traders to monitor trend strength and make informed trading decisions.

◆ Probability labels and signals:

Furthermore, the indicator includes probability labels and signals , which are displayed near the corresponding bars on the chart. These labels indicate the posterior probability of a trend, while small diamonds above or below bars indicate crossover or crossunder events when the posterior probability crosses the 0.5 threshold (50%).

The posterior probability of a trend

Crossover or Crossunder events

◆ User Inputs

Source:

Description: Defines the price source for the indicator's calculations. Users can select between different price values like close, open, high, low, etc.

MA's Length:

Description: Sets the length for the moving averages used in the trend calculations. A larger length will smooth out the moving averages, making the indicator less sensitive to short-term fluctuations.

Gap Length Between Fast and Slow MA's:

Description: Determines the difference in lengths between the slow and fast moving averages. A higher gap length will increase the difference, potentially identifying stronger trend signals.

Gap Signals:

Description: Defines the gap used for the smoothed gradient signal function. This parameter affects the sensitivity of the trend signals by setting the number of bars used in the signal calculations.

In summary, the "Bayesian Trend Indicator" is a powerful tool that leverages Bayesian probability theory and moving average analysis to help traders identify trend direction, assess market sentiment, and make informed trading decisions in various financial markets.

FiboSequFiboSequ: Fibonacci Sequence Marking

Leonardo Fibonacci was an Italian mathematician who lived in the 12th century. His real name was Leonardo of Pisa, but he is commonly known as "Fibonacci." Fibonacci is famous for introducing the Hindu-Arabic numeral system to the Western world. This system is the basis of the modern decimal number system we use today.

Fibonacci Sequence

The Fibonacci sequence is a series of numbers that frequently appears in mathematics and nature. The first two numbers in the sequence are 0 and 1, and each subsequent number is the sum of the two preceding numbers.

The sequence is as follows:

0, 1, 1, 2, 3, 5, 8, 13, 21, 34, 55, 89, 144, 233, 377, 610, 987, 1597, 2584, ...

Fibonacci Time Zones:

Fibonacci time zones are used to identify potential turning points in the market at specific time intervals. These time zones correspond to the Fibonacci sequence in terms of consecutive days or weeks.

The Fibonacci sequence has a wide range of applications in both mathematics and nature. Leonardo Fibonacci's work has had a significant impact on the development of modern mathematics and numeral systems. In financial markets, the Fibonacci sequence and ratios are frequently used by technical analysts to predict and analyze market movements.

Description:

Overview:

The FiboSequ indicator marks significant days on a price chart based on the Fibonacci sequence. This can help traders identify potential turning points or areas of interest in the market. The Fibonacci sequence is a series of numbers where each number is the sum of the two preceding ones, often found in nature and financial markets.

Fibonacci Sequence:

The sequence used in this indicator includes: 1, 3, 5, 8, 13, 21, 34, 55, 89, 144, 233, 377, 610, 987, 1597, and 2584.

These numbers represent the days to be marked on the chart, highlighting possible significant market movements.

How It Works:

User Input:

Users can input the starting date (Year, Month, and Day) from which the Fibonacci sequence will begin to be calculated.

This allows flexibility and customization based on the trader's analysis needs.

Calculation:

The starting date is converted into a timestamp in seconds.

For each bar on the chart, the number of days since the starting date is calculated.

The indicator checks if the current day matches any of the Fibonacci sequence days, the previous day, or the next day.

In this indicator, Fibonacci numbers can be displayed on the chart as plus and minus 2 days. For example, for the 145th day, signals start to appear as 143,144 and 145. This is due to dates that sometimes coincide with weekends and public holidays.

Marking the Chart:

When a match is found, a label is placed above the bar indicating the day number from the Fibonacci sequence.

These labels are colored blue with white text for easy visibility.

Usage:

This indicator can be used on any timeframe and market to help identify potential areas where price might react.

It is especially useful for those who employ Fibonacci analysis in their trading strategy.

Example:

If the starting date is January 1, 2020, the indicator will mark significant Fibonacci days (e.g., 1, 3, 5, 8 days, etc.) on the chart from this date onward.

Community Guidelines Compliance:

This indicator adheres to TradingView's Pine Script community guidelines.

It provides customizable user inputs and does not violate any terms of use.

By using the FiboSequ indicator, traders can enhance their technical analysis by incorporating time-based Fibonacci levels, potentially leading to better market timing and decision-making.

Frequently Asked Questions (FAQ)

Q: What is the FiboSequ indicator?

A: The FiboSequ indicator is a technical analysis tool that marks significant days on a price chart based on the Fibonacci sequence. This indicator helps traders identify potential turning points or areas of interest in the market.

Q: What is the Fibonacci sequence and why is it important?

A: The Fibonacci sequence is a series of numbers where each number is the sum of the two preceding ones. The first two numbers are 0 and 1. This sequence frequently appears in nature and financial markets and is used in technical analysis to identify important support and resistance levels.

Q: How do the Fibonacci time zones in the indicator work?

A: Fibonacci time zones are used to identify potential market turning points at specific time intervals. The indicator calculates days based on the Fibonacci sequence (e.g., 1, 3, 5, 8 days, etc.) from the starting date and marks them on the chart.

Q: How can users set the starting date?

A: Users can input the starting date by specifying the year, month, and day. This sets the date from which the indicator begins its calculations, providing flexibility for user analysis.

Q: What do the labels in the indicator represent?

A: The labels mark specific days in the Fibonacci sequence. For example, 1st day, 3rd day, 5th day, etc. These labels are displayed in blue with white text for easy visibility.

Q: Which timeframes can I use the FiboSequ indicator on?

A: The FiboSequ indicator can be used on any timeframe. This includes daily, weekly, or monthly charts, as well as shorter timeframes.

Q: Which markets can the FiboSequ indicator be used in?

A: The FiboSequ indicator can be used in various financial markets, including stocks, forex, cryptocurrencies, commodities, and more.

Q: How can I achieve better market timing with the FiboSequ indicator?

A: The FiboSequ indicator helps identify potential market turning points using time-based Fibonacci levels. This can lead to better market timing and more informed trading decisions for traders.

-Please feel free to write your valuable comments and opinions. I attach importance to your valuable opinions so that I can improve myself.

Breakouts with Tests & Retests [LuxAlgo]The Breakouts Tests & Retests indicator highlights tests and retests of levels constructed from detected swing points. A swing area of interest switches colors when a breakout occurs.

Users can control the sensitivity of the swing point detection and the width of the swing areas.

🔶 USAGE

When a Swing point is detected, an area of interest is drawn, colored green for a bullish swing and red when bearish.

A test is confirmed when the opening price is situated in the area of interest, and the closing price is above or below the area, depending on whether it is a bullish or bearish swing. Tests are highlighted with a solid-colored triangle.

A breakout is confirmed when the price closes in the opposite position, below or above the area, in which case the area will switch colors.

If the opening price is located within the area and the closing price closes outside the area, in the same direction as the breakout, this is considered a retest . Retests are highlighted with a hollow-colored triangle.

Note that tests/retests do not act on wicks. The main factor is that the opening price is in the area of interest, while the closing price is outside.

🔹 Area Of Interest Width

The user can adjust the width of the swing areas. Changing the " Width " is a fast and easy way to find different areas of interest.

A higher "Multiple" setting would return a wider area, allowing price to develop within it for a longer period of time and potentially provide later test signals.

When a swing area is broken, a higher "Width" setting can make it more complicated for the price to break it again, allowing a swing area to remain valid for a longer period of time thus potentially providing more retest signals.

🔶 DETAILS

Generally, only one bullish/bearish pattern can be active at a time. This means that no more than 1 bullish or bearish area will be active.

The " Display " settings, however, can help control how areas of different types are displayed.

Bullish AND Bearish: Both, bullish and bearish patterns can be drawn at the same time

Bullish OR Bearish: Only 1 bullish or 1 bearish pattern is drawn at a time

Bullish: Only bullish patterns

Bearish: Only bearish patterns

🔹 Test/Retest Labels

The user can adjust the settings so only the latest test/retest label is shown or set a minimum number of bars until the next test/retest can be drawn.

🔹 Maximum Bars

Users can set a limit of bars for when there is no test/retest in that period; the area of interest won't be updated anymore and will be available and ready for the next Swing.

An option for pulling the area back to the last retest is included.

🔶 SETTINGS

Display: Determines which swing areas are displayed by the indicator. See the "DETAILS" section for more information

Multiple: Adjusts the width of the areas of interest

Maximum Bars: Limit of bars for when there is no test/retest

Display Test/Retest Labels: Show all labels or just the last test/retest label associated with a swing area

Minimum Bars: Minimum bars required for a subsequent test/retest label are allowed to be displayed

Set Back To Last Retest: When after "Maximum Bars" no test/retest is found, place the right side of the area at the last test/retest

🔹 Swings

Left: x amount of wicks on the left of a potential Swing need to be higher/lower for a Swing to be confirmed.

Right: The number of wicks on the right of a potential swing needs to be higher/lower for a Swing to be confirmed.

🔹 Style

Bullish: color for test period (before a breakout) / retest period (after a breakout)

Bearish: color for test period (before a breakout) / retest period (after a breakout)

Label Size

Entry Fragger - Strategy

For basic instructions please visit my other script "Entry Fragger".

The Signal Logic is explained there.

v1.4:

- Added advanced backtesting with fully customizable entries.

- Fully automated Buy Signals (profitable).

- Adjustable timeframes for signal logic. (requested)

Every setting affects the accuracy and profitability greatly now, based on settings applied.

The strategy performs best on high timeframes with larger capital and no leverage.

Useless for Forex, but absolutely smashes stocks and crypto on mid to high timeframes.

Please read through my other scripts description.

Set values as preferred and try your assets.

It does NOT work on low timeframes and forex!

Hint: BTC 4H, Custom Timeframe 1h, Moon Mode and Show Sell Signals enabled, R2R: 2.

Higher Timeframe High & Low [ChartPrime]The Higher Timeframe High & Low Indicator plots key levels (high, low, and average price) from a higher timeframe onto the current chart, aiding traders in identifying significant support and resistance zones.

The indicator also detects and labels breakout points and can display trend directions based on these higher timeframe levels breakout points.

Key Features:

◆ Higher Timeframe Levels:

Plots the high, low, and average price from a selected higher timeframe onto the current chart.

Extends these levels into the future for better visualization.

◆ Breakout Detection:

Identifies and labels breakouts above the higher timeframe high or below the higher timeframe low.

Breakout points are clearly marked with labels indicating "High Break" or "Low Break" with timeframe mark.

If the following break out type is the same that previous, it does not marked by labels, but still marked by bar color.

◆ Trend Visualization:

Optionally displays trend direction by changing bar colors and line styles based on breakout conditions.

Trend indication helps in identifying bullish or bearish market conditions.

◆ Support and Resistance Indication:

Marks support and resistance points with '◆' symbols when the current timeframe's high or low interacts with the higher timeframe's levels.

◆ Period separation:

Background color changes to indicate period separation if enabled.

◆ Inputs:

Extension to the right of High and Low: Sets the number of bars to extend the high and low lines into the future.

Timeframe: Selects the higher timeframe (e.g., Daily) to use for plotting high and low levels.

Period Separator: Toggles the visual separator for periods.

Show Trend?: Toggles the trend visualization, changing bar colors and plot styles based on breakouts.

Show Breakout Labels?: Toggles the Breakout Labels visualization.

Indicator Logic:

Historical vs. Real-Time Bars: Adjusts values based on whether the bar is historical or real-time to ensure accurate plotting.

High and Low Prices: Retrieves the high and low prices from the selected higher timeframe.

Breakout Conditions: Determines if the current price has crossed above the higher timeframe high (high break) or below the higher timeframe low (low break).

Color and Trend Logic: Adjusts colors and checks for breakouts to avoid multiple labels and indicate trend direction.

Usage Notes:

This indicator is ideal for traders looking to integrate multi-timeframe analysis into their strategy.

The higher timeframe levels act as significant support and resistance zones, helping traders identify potential reversal or continuation points.

The breakout labels and trend visualization provide additional context for trading decisions, indicating when the price has breached key levels and is likely to continue in that direction.

This indicator enhances chart analysis by providing clear, visual cues from higher timeframe data, helping traders make more informed decisions based on a broader market perspective.

Advanced Stochastic [CryptoSea]The Advanced Stochastic Indicator is a sophisticated tool designed to enhance market analysis through detailed stochastic calculations. This tool is built for traders who seek to identify market divergences and pivot points with higher accuracy.

Key Features

Multi-Layer Stochastic Analysis: Tracks both standard and smoothed stochastic values to provide a granular view of market momentum.

Divergence Detection: Automatically detects both regular and hidden bullish and bearish divergences, offering critical insights into potential market reversals.

Adaptive Oscillator Display: Features customizable display options for the stochastic oscillator, allowing traders to view data in Default, Histogram, or Both modes.

Customizable Lookback Periods: Users can set specific lookback periods for divergence analysis and stochastic calculations, tailoring the tool to fit various trading strategies.

In the example below, there is a bearish divergence above 0. You would first want the stoch to break below the 0 level as a show of strength, this would be an aggressive entry, a higher probability option would be to wait for the stoch to retest and reject from 0 which is what we have a few candles later.

How it Works

Stochastic Calculation: Computes the stochastic oscillator by smoothing the %K line over a user-defined period, then applying a second smoothing for the %D line.

Pivot Point Analysis: Utilizes advanced algorithms to find low and high pivot points based on the oscillator values, crucial for spotting trend reversals.

Colour-Coded Divergence Alerts: Utilizes color codes to highlight divergence signals directly on the chart, aiding in quick visual analysis.

Responsive Threshold Settings: Includes options to adjust the sensitivity of divergence detection, ensuring that only significant divergences are highlighted.

In the example below, we have 2 divergence signals. The first a bullish one which fails to break above 0. The second signal is given above 0 so you would want a retest and a show of strength when the stoch returns to 0 but it fails to hold. Both of these divergence signals are invalidated.

Application

Strategic Decision-Making: Assists traders in making informed decisions by providing detailed analysis of stochastic movements and divergence.

Trend Confirmation: Reinforces trading strategies by confirming potential reversals with pivot point detection and divergence analysis.

Customized Analysis: Adapts to various trading styles with extensive input settings that control the display and sensitivity of oscillator data.

The Advanced Stochastic Indicator by is an invaluable addition to a trader's toolkit, offering depth and precision in market trend analysis to navigate complex market conditions effectively.

MTF Williams Vix Market Bottoms [CryptoSea]MTF Williams Vix Fix Indicator is a dynamic tool tailored for traders looking to capture market extremes with high precision. This multi-timeframe indicator leverages the concept of the Williams Vix Fix to spot potential reversals before they occur.

Key Features

Multi-Timeframe Analysis: Provides simultaneous visibility across multiple timeframes, enabling traders to assess market conditions comprehensively from a single chart.

Advanced Volatility Detection: Utilizes a modified Vix Fix formula to highlight extreme price deviations, which often precede significant market reversals.

Customizable Settings: Offers extensive input options to tweak the lookback periods, percentile thresholds, and visibility settings, aligning with various trading strategies.

Visual Band Indicators: Features upper bands and range highs that signal potential overbought and oversold conditions, enhancing trading decision-making.

Below, you can see how the indicator performs across different timeframes, providing valuable insights into market behavior.

How it Works

Vix Fix Calculation: Determines the worst-case 'panic' sell-offs in price as a percentage of the high, capturing the emotional extremes of the market.

Statistical Bands: Employs Bollinger bands over the Vix Fix values to define normal and extreme volatility conditions.

Color-Coded Indicators: Uses color differentiation to instantly highlight when readings surpass critical upper band or range high thresholds, signaling key trading opportunities.

For instance, in the analysis provided below, notice how the indicator flags significant market moves, allowing traders to anticipate potential entry or exit points.

Application

Risk Management: Aids in identifying extreme market conditions where prices may revert, helping in effective position sizing and risk management.