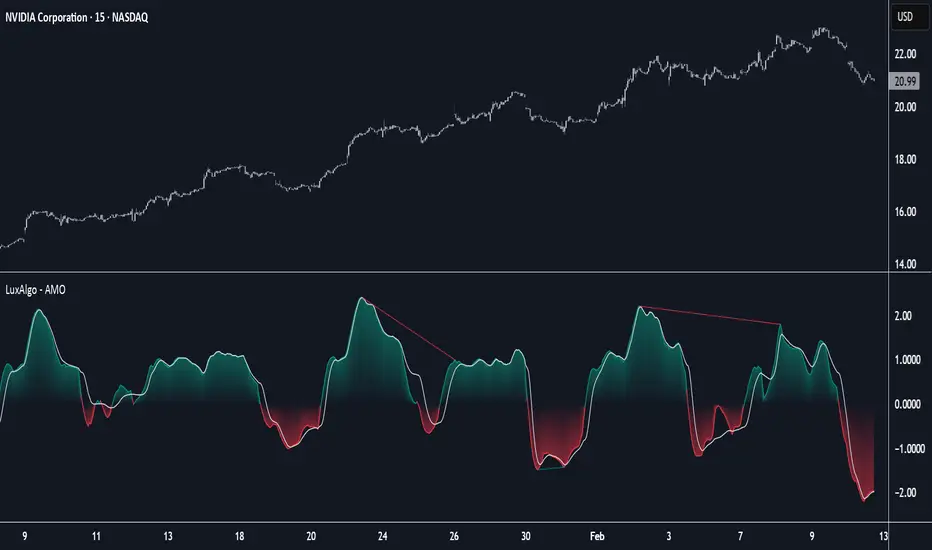

Adaptive Momentum Oscillator [LuxAlgo]The Adaptive Momentum Oscillator tool allows traders to measure the current relative momentum over a given period using the maximum delta in price.

It features a histogram with gradient color, divergences, and an adaptive moving average that allows traders to clearly see the smoothed trend direction.

🔶 USAGE

This unbounded oscillator has positive momentum when values are above 0 and negative momentum when values are below 0. The adaptive moving average is used as a minimum lag smoothing tool over the momentum histogram.

🔹 Signal Line

There are two main uses for the signal line drawn on the chart above.

Momentum crosses above or below the signal line: acceleration in momentum.

Signal line crosses the 0 value: positive or negative momentum.

🔹 Data Length

On the chart above, we can compare different length sizes and how the tool values change, allowing traders to get a shorter or longer-term view of current market strength.

🔹 Smoothing Length

In the previous figure, we can compare how different Smoothing Length values affect the oscillator output.

🔹 Divergences

The divergence detector is disabled by default. Traders can enable it and adjust the divergence length from the settings panel.

As we can see in the chart above, by changing the length of the divergences, traders can fine-tune their detection, a small number will detect smaller divergences, and use a larger number for larger divergences.

🔶 SETTINGS

Data: Select data source, close price by default

Data Length: Select the length for data gathering

Smoothing Length: Select the length for data smoothing

Divergences: Enable/Disable divergences detection and length

Smooth

Forward-Backward Exponential Oscillator [LuxAlgo]The Forward-Backward Exponential Oscillator is a normalized oscillator able to estimate directional shifts by making use of a unique "Forward-Backward Filtering" calculation method for Exponential Moving Averages (EMAs).

This unique method provides a smooth normalized representation of the price with reduced lag.

🔶 USAGE

The oscillator consists of 2 series of values derived from normalizing the sum of each EMA's change across the selected user lookback window (length), one less reactive computed forward (in grey), and the other re-calculated backward for each bar (in blue).

Given this "Forward-Backwards" calculation method, we are able to produce a more reactive oscillator compared to the same operation done on a simple double-smoothed EMA.

The interaction between these 2 values (Forward Value and Backward Value) can highlight shifts in market momentum over time.

When the Forward Value is above the Backward Value, the price is seen moving up, and likewise, when the Forward EMA is below, the Backward EMA price is seen moving down.

The indicator specifically displays the difference between values through a histogram located at the 50 mark on the oscillator.

🔹 Projection

We project the approximated future values of the forward value in front of the current line. This helps show the data that is being used for the creation of the Forward Value.

🔹 Length & Smoothing

The Smoothing Input controls the length of the EMAs which are analyzed.

The Length Input controls the lookback for the sum of changes from the EMAs.

Displayed below is a comparison of varying input sizes and their results.

As seen above:

A larger length input will result in slower, gradual movement by the oscillator since the summed values are from a larger lookback.

A higher smoothing setting will result in smoother EMAs, leading to a smoother oscillator output that is less contaminated by noisy variations.

Note: The length of the projection is tied to the "length" input, to get a longer projection, a larger length is required.

🔶 DETAILS

Forward-backward filtering is a method applied to LTI (linear time-invariant) filters to provide a filter response with zero-phase shift, this has the visible effect of shifting a regular causal filter response to the right, making it appear has have effectively 0 lag.

The name of this operation indicates that the filter is first calculated forward over a series of values (like regular moving averages), then calculated backward, using the previous output as input for the filter, effectively applying the filter twice.

While this operation effectively allows us to obtain a zero-lag response when applied to an EMA, it is subject to repainting, as this indicator only returns the normalized sum of changes of the forward-backward EMA, which does not introduce any repainting behaviors in the final output of the oscillator.

🔶 SETTINGS

Length: Change the calculation lookback length for the oscillator.

Smoothing: Alter the smoothness of the back-end EMA calculations.

Source: Change the source input used for the indicator.

Adaptive Fisherized Z-scoreHello Fellas,

It's time for a new adaptive fisherized indicator of me, where I apply adaptive length and more on a classic indicator.

Today, I chose the Z-score, also called standard score, as indicator of interest.

Special Features

Advanced Smoothing: JMA, T3, Hann Window and Super Smoother

Adaptive Length Algorithms: In-Phase Quadrature, Homodyne Discriminator, Median and Hilbert Transform

Inverse Fisher Transform (IFT)

Signals: Enter Long, Enter Short, Exit Long and Exit Short

Bar Coloring: Presents the trade state as bar colors

Band Levels: Changes the band levels

Decision Making

When you create such a mod you need to think about which concepts are the best to conclude. I decided to take Inverse Fisher Transform instead of normalization to make a version which fits to a fixed scale to avoid the usual distortion created by normalization.

Moreover, I chose JMA, T3, Hann Window and Super Smoother, because JMA and T3 are the bleeding-edge MA's at the moment with the best balance of lag and responsiveness. Additionally, I chose Hann Window and Super Smoother because of their extraordinary smoothing capabilities and because Ehlers favours them.

Furthermore, I decided to choose the half length of the dominant cycle instead of the full dominant cycle to make the indicator more responsive which is very important for a signal emitter like Z-score. Signal emitters always need to be faster or have the same speed as the filters they are combined with.

Usage

The Z-score is a low timeframe scalper which works best during choppy/ranging phases. The direction you should trade is determined by the last trend change. E.g. when the last trend change was from bearish market to bullish market and you are now in a choppy/ranging phase confirmed by e.g. Chop Zone or KAMA slope you want to do long trades.

Interpretation

The Z-score indicator is a momentum indicator which shows the number of standard deviations by which the value of a raw score (price/source) is above or below the mean value of what is being observed or measured. Easily explained, it is almost the same as Bollinger Bands with another visual representation form.

Signals

B -> Buy -> Z-score crosses above lower band

S -> Short -> Z-score crosses below upper band

BE -> Buy Exit -> Z-score crosses above 0

SE -> Sell Exit -> Z-score crosses below 0

If you were reading till here, thank you already. Now, follows a bunch of knowledge for people who don't know the concepts I talk about.

T3

The T3 moving average, short for "Tim Tillson's Triple Exponential Moving Average," is a technical indicator used in financial markets and technical analysis to smooth out price data over a specific period. It was developed by Tim Tillson, a software project manager at Hewlett-Packard, with expertise in Mathematics and Computer Science.

The T3 moving average is an enhancement of the traditional Exponential Moving Average (EMA) and aims to overcome some of its limitations. The primary goal of the T3 moving average is to provide a smoother representation of price trends while minimizing lag compared to other moving averages like Simple Moving Average (SMA), Weighted Moving Average (WMA), or EMA.

To compute the T3 moving average, it involves a triple smoothing process using exponential moving averages. Here's how it works:

Calculate the first exponential moving average (EMA1) of the price data over a specific period 'n.'

Calculate the second exponential moving average (EMA2) of EMA1 using the same period 'n.'

Calculate the third exponential moving average (EMA3) of EMA2 using the same period 'n.'

The formula for the T3 moving average is as follows:

T3 = 3 * (EMA1) - 3 * (EMA2) + (EMA3)

By applying this triple smoothing process, the T3 moving average is intended to offer reduced noise and improved responsiveness to price trends. It achieves this by incorporating multiple time frames of the exponential moving averages, resulting in a more accurate representation of the underlying price action.

JMA

The Jurik Moving Average (JMA) is a technical indicator used in trading to predict price direction. Developed by Mark Jurik, it’s a type of weighted moving average that gives more weight to recent market data rather than past historical data.

JMA is known for its superior noise elimination. It’s a causal, nonlinear, and adaptive filter, meaning it responds to changes in price action without introducing unnecessary lag. This makes JMA a world-class moving average that tracks and smooths price charts or any market-related time series with surprising agility.

In comparison to other moving averages, such as the Exponential Moving Average (EMA), JMA is known to track fast price movement more accurately. This allows traders to apply their strategies to a more accurate picture of price action.

Inverse Fisher Transform

The Inverse Fisher Transform is a transform used in DSP to alter the Probability Distribution Function (PDF) of a signal or in our case of indicators.

The result of using the Inverse Fisher Transform is that the output has a very high probability of being either +1 or –1. This bipolar probability distribution makes the Inverse Fisher Transform ideal for generating an indicator that provides clear buy and sell signals.

Hann Window

The Hann function (aka Hann Window) is named after the Austrian meteorologist Julius von Hann. It is a window function used to perform Hann smoothing.

Super Smoother

The Super Smoother uses a special mathematical process for the smoothing of data points.

The Super Smoother is a technical analysis indicator designed to be smoother and with less lag than a traditional moving average.

Adaptive Length

Length based on the dominant cycle length measured by a "dominant cycle measurement" algorithm.

Happy Trading!

Best regards,

simwai

---

Credits to

@cheatcountry

@everget

@loxx

@DasanC

@blackcat1402

Machine Learning: Anchored Gaussian Process Regression [LuxAlgo]Machine Learning: Anchored Gaussian Process Regression is an anchored version of Machine Learning: Gaussian Process Regression .

It implements Gaussian Process Regression (GPR), a popular machine-learning method capable of estimating underlying trends in prices as well as forecasting them. Users can set a Training Window by choosing 2 points. GPR will be calculated for the data between these 2 points.

Do remember that forecasting trends in the market is challenging, do not use this tool as a standalone for your trading decisions.

🔶 USAGE

When adding the indicator to the chart, users will be prompted to select a starting and ending point for the calculations, click on your chart to select those points.

Start & end point are named 'Anchor 1' & 'Anchor 2', the Training Window is located between these 2 points. Once both points are positioned, the Training Window is set, whereafter the Gaussian Process Regression (GPR) is calculated using data between both Anchors .

The blue line is the GPR fit, the red line is the GPR prediction, derived from data between the Training Window .

Two user settings controlling the trend estimate are available, Smooth and Sigma.

Smooth determines the smoothness of our estimate, with higher values returning smoother results suitable for longer-term trend estimates.

Sigma controls the amplitude of the forecast, with values closer to 0 returning results with a higher amplitude.

One of the advantages of the anchoring process is the ability for the user to evaluate the accuracy of forecasts and further understand how settings affect their accuracy.

The publication also shows the mean average (faint silver line), which indicates the average of the prices within the calculation window (between the anchors). This can be used as a reference point for the forecast, seeing how it deviates from the training window average.

🔶 DETAILS

🔹 Limited Training Window

The Training Window is limited due to matrix.new() limitations in size.

When the 2 points are too far from each other (as in the latter example), the line will end at the maximum limit, without giving a size error.

The red forecasted line is always given priority.

🔹 Positioning Anchors

Typically Anchor 1 is located further in history than Anchor 2 , however, placing Anchor 2 before Anchor 1 is perfectly possibly, and won't give issues.

🔶 SETTINGS

Anchor 1 / Anchor 2: both points will form the Training Window .

Forecasting Length: Forecasting horizon, determines how many bars in the 'future' are forecasted.

Smooth: Controls the degree of smoothness of the model fit.

Sigma: Noise variance. Controls the amplitude of the forecast, lower values will make it more sensitive to outliers.

Machine Learning: Gaussian Process Regression [LuxAlgo]We provide an implementation of the Gaussian Process Regression (GPR), a popular machine-learning method capable of estimating underlying trends in prices as well as forecasting them.

While this implementation is adapted to real-time usage, do remember that forecasting trends in the market is challenging, do not use this tool as a standalone for your trading decisions.

🔶 USAGE

The main goal of our implementation of GPR is to forecast trends. The method is applied to a subset of the most recent prices, with the Training Window determining the size of this subset.

Two user settings controlling the trend estimate are available, Smooth and Sigma . Smooth determines the smoothness of our estimate, with higher values returning smoother results suitable for longer-term trend estimates.

Sigma controls the amplitude of the forecast, with values closer to 0 returning results with a higher amplitude. Do note that due to the calculation of the method, lower values of sigma can return errors with higher values of the training window.

🔹 Updating Mechanisms

The script includes three methods to update a forecast. By default a forecast will not update for new bars (Lock Forecast).

The forecast can be re-estimated once the price reaches the end of the forecasting window when using the "Update Once Reached" method.

Finally "Continuously Update" will update the whole forecast on any new bar.

🔹 Estimating Trends

Gaussian Process Regression can be used to estimate past underlying local trends in the price, allowing for a noise-free interpretation of trends.

This can be useful for performing descriptive analysis, such as highlighting patterns more easily.

🔶 SETTINGS

Training Window: Number of most recent price observations used to fit the model

Forecasting Length: Forecasting horizon, determines how many bars in the future are forecasted.

Smooth: Controls the degree of smoothness of the model fit.

Sigma: Noise variance. Controls the amplitude of the forecast, lower values will make it more sensitive to outliers.

Update: Determines when the forecast is updated, by default the forecast is not updated for new bars.

Savitzky-Golay Filtered Chande Momentum OscillatorThe Savitzky-Golay Filtered Chande Momentum Oscillator (SGCMO) is a modified version of the Chande Momentum Oscillator that functions as a powerful analytical tool, capable of detecting trends and mean reversals. By applying a Savitzky-Golay filter to the price data, the oscillator provides enhanced visualization and smoother readings. (credit to © anieri for the Savitzky-Golay filter code: www.tradingview.com)

Chande Momentum Oscillator

The Chande Momentum Oscillator (CMO) is a technical indicator developed by Tushar Chande. It measures the momentum of an asset's price movement and provides insights into the overbought or oversold conditions of the market. The CMO calculates the difference between the sum of positive price changes and the sum of negative price changes over a specified period, and then normalizes it to a scale between -100 and +100. Traders and investors use the CMO to identify potential trend reversals, confirm the strength of a current trend, and generate buy or sell signals.

Smoothing

The Savitzky-Golay filter is a digital filter commonly employed for smoothing and noise reduction in time-series data. In the context of the SGCMO, the aim is to effectively smooth the CMO values, reducing the impact of short-term fluctuations and providing clearer insights into underlying trends. Additionally, an exponential moving average (EMA) filter is applied to further reduce noise and enhance trend visibility. This filtered CMO indicator may provide traders and investors with a clearer and more refined representation of momentum changes in the underlying asset, helping them make more informed trading decisions.

Application

The SGCMO serves as both a trend-following and mean-reversion tool. Traders can track the current trend using bullish white lines or bearish orange lines in trending markets. Alternatively, they can utilize green and red vertical lines, which indicate price retracement and help capture pullbacks and reversals. Green vertical lines appear when the trend reverses upwards in an oversold zone (-50 to -80), while red vertical lines indicate negative trend reversals in an overbought zone (50 to 80). Opening long positions when green and white lines appear, or short positions when red and orange lines are visible, can be considered. However, it is advisable to combine this indicator with other complementary technical analysis tools and incorporate it into a comprehensive trading strategy to maximize its effectiveness.

Kalman Filtered ROC & Stochastic with MA SmoothingThe "Smooth ROC & Stochastic with Kalman Filter" indicator is a trend following tool designed to identify trends in the price movement. It combines the Rate of Change (ROC) and Stochastic indicators into a single oscillator, the combination of ROC and Stochastic indicators aims to offer complementary information: ROC measures the speed of price change, while Stochastic identifies overbought and oversold conditions, allowing for a more robust assessment of market trends and potential reversals. The indicator plots green "B" labels to indicate buy signals and blue "S" labels to represent sell signals. Additionally, it displays a white line that reflects the overall trend for buy signals and a blue line for sell signals. The aim of the indicator is to incorporate Kalman and Moving Average (MA) smoothing techniques to reduce noise and enhance the clarity of the signals.

Rationale for using Kalman Filter:

The Kalman Filter is chosen as a smoothing tool in the indicator because it effectively reduces noise and fluctuations. The Kalman Filter is a mathematical algorithm used for estimating and predicting the state of a system based on noisy and incomplete measurements. It combines information from previous states and current measurements to generate an optimal estimate of the true state, while simultaneously minimizing the effects of noise and uncertainty. In the context of the indicator, the Kalman Filter is applied to smooth the input data, which is the source for the Rate of Change (ROC) calculation. By considering the previous smoothed state and the difference between the current measurement and the predicted value, the Kalman Filter dynamically adjusts its estimation to reduce the impact of outliers.

Calculation:

The indicator utilizes a combination of the ROC and the Stochastic indicator. The ROC is smoothed using a Kalman Filter (credit to © Loxx: ), which helps eliminate unwanted fluctuations and improve the signal quality. The Stochastic indicator is calculated with customizable parameters for %K length, %K smoothing, and %D smoothing. The smoothed ROC and Stochastic values are then averaged using the formula ((roc + d) / 2) to create the blended oscillator. MA smoothing is applied to the combined oscillator aiming to further reduce fluctuations and enhance trend visibility. Traders are free to choose their own preferred MA type from 'EMA', 'DEMA', 'TEMA', 'WMA', 'VWMA', 'SMA', 'SMMA', 'HMA', 'LSMA', and 'PEMA' (credit to: © traderharikrishna for this code: ).

Application:

The indicator's buy signals (represented by green "B" labels) indicate potential entry points for buying assets, suggesting a bullish trend. The white line visually represents the trend, helping traders identify and follow the upward momentum. Conversely, the sell signals (blue "S" labels) highlight possible exit points or opportunities for short selling, indicating a bearish trend. The blue line illustrates the bearish movement, aiding in the identification of downward momentum.

The "Smoothed ROC & Stochastic" indicator offers traders a comprehensive view of market trends by combining two powerful oscillators. By incorporating the ROC and Stochastic indicators into a single oscillator, it provides a more holistic perspective on the market's momentum. The use of a Kalman Filter for smoothing helps reduce noise and enhance the accuracy of the signals. Additionally, the indicator allows customization of the smoothing technique through various moving average types. Traders can also utilize the overbought and oversold zones for additional analysis, providing insights into potential market reversals or extreme price conditions. Please note that future performance of any trading strategy is fundamentally unknowable, and past results do not guarantee future performance.

ALMA Smoothed Gaussian Moving AverageThis indicator is an altered version of the Gaussian Moving Average (GMA) (Credit to author: © LeafAlgo ). The GMA applies weights to the prices, giving more importance to the values closer to the current period and gradually diminishing the significance of older prices. The ALMA Smoothed Gaussian Moving Average (ASGMA) applies an ALMA smoothing to its price data to minimize lag and provide a more accurate representation of the underlying trend by dynamically adapting to changing market conditions. The Arnaud Legoux Moving Average (ALMA) is a specialized smoothing technique that adjusts the weights of the moving average based on market volatility. Its calculation uses Wavelet Transform techniques which enables this type of smoothing to capture both high-frequency and low-frequency components of a signal or data. The rationale for this mashup between ALMA and Gaussian filtering is to smooth the moving average line over the smoothed price data and produce stronger trend signals.

ASGMA serves as a trend-following indicator, identifying both bullish and bearish trends. It provides buy and sell signals indicated by "B" and "S" labels plotted alongside the price data. Additionally, the ASGMA's Exponential Moving Average (EMA) line alternates between green and red, indicating bullish and bearish momentum, respectively.

The ASGMA also incorporates two popular momentum indicators, the Relative Strength Index (RSI) and the Chande Momentum Oscillator (CMO). The inclusion of these indicators aims to enhance trend identification and reversal signals. For a strong buy signal, all three indicators (RSI, CMO, and ASGMA) must indicate bullish conditions, resulting in a vertical green line. Conversely, a vertical red line is plotted when all indicators indicate bearish conditions, representing a strong sell signal.

The ASGMA, with its unique combination of smoothing techniques and indicator amalgamation, provides traders and investors with powerful analytical tools. It can be applied in trend-following strategies using the regular buy and sell signals generated by labels and the EMA line. Alternatively, the vertical lines offer stronger buy and sell signals. These features aid in identifying potential entry and exit points, thereby enhancing trading decisions and market analysis. However, it is important to remember that the future performance of any trading strategy is fundamentally unknowable, and past results do not guarantee future performance.

MTF Evolving Weighted Composite Value Area🧾 Description:

This indicator calculates evolving value areas across 3 different timeframes/periods and combines them into one composite, multi-timeframe evolving value area - with each of the underlying timeframes' VAs assigned their own weighting/importance in the final calculation. Layered with extra smoothing options, this creates an informative and useful 'rolling value area' effect that can give you a better perspective on the value area across multiple periods at once as it develops - without total calculation resets at the onset of every new period.

Let's start with a simplified primer on value areas and then jump in to the new ideas this indicator introduces.

🤔 What is a value area?

Value areas are a tool used in market profile analysis to determine the range of prices that represents where most trading activity occurred during a specific time period, typically within a single 'bar' of a certain higher timeframe, such as the 4-hour, daily, or weekly. It helps traders understand the levels where the market finds value.

To calculate the value area, we look at the distribution of prices and trading volume. We determine a percentage, usually 70% or 80%, that represents the significant portion of trading volume. Then, we identify the price range that contains this percentage of trading volume, which becomes the value area.

Value areas are useful because they provide insights into market dynamics and potential support and resistance levels. They show where traders have been most active and where they find value, and traders can use this information to make better-informed decisions.

For example, if price is trading within the value area, it suggests that it's within a range where traders see value and are actively participating, which could indicate a balanced market. If the price moves above or below the value area, it may signal a potential shift in market sentiment or a breakout/breakdown from the established range.

By understanding the value area, traders can identify potential areas of supply and demand, determine levels of interest for buyers and sellers, and make decisions based on the market's perception of value.

📑 Limitations of traditional value areas

Static representation: Value areas are usually represented as static zones calculated after the fact. For example, after a daily period is completed, a typical 1D VA indicator will display the value area for the past period with static horizontal lines. This approach doesn't give you the power to see how the value area evolved, or developed, during the time period, as it is only displayed retroactively. It also doesn't give you the ability to view it as it evolves in real-time. This is why we chose to use an evolving value area representation, specifically borrowed from @sourcey's Value Area POC/VAH/VAL script function for calculating evolving VAs.

Rollover resets - no memory of past periods!: The traditional value area is calculated over a static period - it is calculated from the beginning of the period, for example a 1 day period, to the end, and that's the end of it. When the next daily period begins, the calculation resets, and has no memory of the preceding period. This limits the usefulness of the value area visual when viewed near the beginning of a new period before price and volume have been given ample time to define an area.

Hard to absorb all of that information: Value areas aren't generally meant to be a hardline representation of something extremely exact - they're based on a percentage of the area where traders appeared to find value over a certain time period. Most traders use them as a guide for support and resistance levels or finding an expected range. Traders typically overlay multiple VAs - sometimes requiring several instances of the same indicator to be applied - to represent the VA across multiple timeframes such as the 4H, 1D, or 1W. The chart quickly gets cluttered and it's not necessarily easy to understand the relationship between these multiple periods' VAs at a glance.

🧪 New concepts introduced in this indicator

With the evolving weighted composite value area we tried to address these limitations, and we think the result can be useful and intuitive for traders who want more dynamic and practical VAs for their everyday technical analysis.

⚖️ 1. A composite, weighted multi-timeframe VA

This indicator's value areas represent a combination or composite of the value areas calculated across multiple timeframes. The VAs calculated across each timeframe are then given a weighting percentage, which determines their contribution to the final 'weighted composite value area'.

Pictured below: a 4H/1D/1W MTF evolving weighted composite VA on the BTCUSDT Perpetual Futures (Binance) 5 minute chart:

Traditionally, when traders wanted to get a view of where the majority of trading activity occurred over the past four hours, day, and week, they would need to apply three value area indicators (or sometimes one if it allows multiple custom timeframes), each set to a different period (4H, 1D, 1W). The chart gets cluttered quickly and the information is hard to absorb in one shot. Addressing this problem was the main impetus for creating this weighted composite process.

〰️ 2. Rolling and smoothed evolving VAs

Because the composite VA is calculated based on multiple period VAs, there is no one single point where the area calculation resets (unless all 3 selected timeframes happen to rollover on the same bar). This creates a 'rolling' effect that gives a sense of the progression of the VA as price transitions through the different underlying time periods, without the traditional 'jump' in calculations between periods.

Pictured below: a 1D/1W/1M MTF evolving weighted composite VA on the NQ futures 1H chart:

To help give even more of a sense of perspective and 'progression' of the VA, there are also smoothing options to even out the 'jumps' at period-rollover points.

✔️ What's it good for?

Smoothed, rolling, and evolving multi-timeframe VAs that give you a better real-time perspective of where traders are finding value across multiple time periods at once.

📎 References

1. @sourcey's Value Area POC/VAH/VAL script by adapting its f_poc(tf) function.

💠 Features:

A MTF evolving weighted composite value area based on 3 underlying VAs calculated across customizable timeframes

Aesthetic and flexible coloring and color theme styling options

Period-roller labels and options for ease-of-use and legibility

⚙️ Settings:

Calculation Decimal Resolution: This setting essentially determines how 'granular' the value area calculating process is. This value should be set to some multiple of the tick size/smallest decimal of the symbol's price chart. Eg. On BTCUSDT, the tick size/decimal is usually 0.1. So, you might use 0.5. On TSLA, the tick size is 0.01. You might use 0.05 or 0.25. Beware: if the resolution is too small, calculation will take too long and the script may timeout.

Show Me Suggested Resolutions: If enabled, a label will display in the bottom right of the chart with some suggested resolutions for the current chart.

Area Percentage: Set the displayed percentage of the calculated composite value area. Igor method = 70%; Daniel method: 68%.

Use a Color Theme: When this setting is enabled, all manual 'Bullish and Bearish Colors' are overridden. All plots will use the colors from your selected Color Theme - excepting those plots set to use the 'Single Color' coloring method.

Color Theme: When 'Use a Color Theme' is enabled, this setting allows you to select the color theme you wish to use.

Resistance Color: When 'Use a Color Theme' is disabled, this will set the 'resistance color' for the composite VA.

Support Color: When 'Use a Color Theme' is disabled, this will set the 'support color' for the composite VA.

Show Period Rollover Labels: When enabled, a label will show above or below the composite VA marking any underlying period rollovers with the label 'New __' (eg. 'New 4H', 'New 1D', 'New 1W').

Size: Sets the font size of the period rollover labels.

Show Period Rollover Lines: When enabled, a translucent vertical dashed line will be drawn across the composite VA when one of the underlying periods rolls over.

Fill Composite Value Area: When enabled, the composite VA will be filled with a gradient coloring from the support line to the resistance line using their respective colors.

Smooth: When enabled, a smoothing moving average will be applied to the composite value area.

Smoothing Period: Set the lookback period for the smoothing average.

Smoothing Type: Set the calculation type for the smoothing average. Options include: Exponential, Simple, Weighted, Volume-Weighted, and Hull.

Enable: Include/exclude a timeframe's VA in the composite VA calculation.

Timeframe: Set the timeframe for this specific underlying VA.

Weighting %: Set the weighting percentage or 'importance' of this timeframe's value area in calculating the composite VA. Beware! The sum of the weighting percentages across all enabled timeframes must ALWAYS add up to 100 in order for this indicator to work as designed.

T3 JMA KAMA VWMAEnhancing Trading Performance with T3 JMA KAMA VWMA Indicator

Introduction

In the dynamic world of trading, staying ahead of market trends and capitalizing on volume-driven opportunities can greatly influence trading performance. To address this, we have developed the T3 JMA KAMA VWMA Indicator, an innovative tool that modifies the traditional Volume Weighted Moving Average (VWMA) formula to increase responsiveness and exploit high-volume market conditions for optimal position entry. This article delves into the idea behind this modification and how it can benefit traders seeking to gain an edge in the market.

The Idea Behind the Modification

The core concept behind modifying the VWMA formula is to leverage more responsive moving averages (MAs) that align with high-volume market activity. Traditional VWMA utilizes the Simple Moving Average (SMA) as the basis for calculating the weighted average. While the SMA is effective in providing a smoothed perspective of price movements, it may lack the desired responsiveness to capitalize on short-term volume-driven opportunities.

To address this limitation, our T3 JMA KAMA VWMA Indicator incorporates three advanced moving averages: T3, JMA, and KAMA. These MAs offer enhanced responsiveness, allowing traders to react swiftly to changing market conditions influenced by volume.

T3 (T3 New and T3 Normal):

The T3 moving average, one of the components of our indicator, applies a proprietary algorithm that provides smoother and more responsive trend signals. By utilizing T3, we ensure that the VWMA calculation aligns with the dynamic nature of high-volume markets, enabling traders to capture price movements accurately.

JMA (Jurik Moving Average):

The JMA component further enhances the indicator's responsiveness by incorporating phase shifting and power adjustment. This adaptive approach ensures that the moving average remains sensitive to changes in volume and price dynamics. As a result, traders can identify turning points and anticipate potential trend reversals, precisely timing their position entries.

KAMA (Kaufman's Adaptive Moving Average):

KAMA is an adaptive moving average designed to dynamically adjust its sensitivity based on market conditions. By incorporating KAMA into our VWMA modification, we ensure that the moving average adapts to varying volume levels and captures the essence of volume-driven price movements. Traders can confidently enter positions during periods of high trading volume, aligning their strategies with market activity.

Benefits and Usage

The modified T3 JMA KAMA VWMA Indicator offers several advantages to traders looking to exploit high-volume market conditions for position entry:

Increased Responsiveness: By incorporating more responsive moving averages, the indicator enables traders to react quickly to changes in volume and capture short-term opportunities more effectively.

Enhanced Entry Timing: The modified VWMA aligns with high-volume periods, allowing traders to enter positions precisely during price movements influenced by significant trading activity.

Improved Accuracy: The combination of T3, JMA, and KAMA within the VWMA formula enhances the accuracy of trend identification, reversals, and overall market analysis.

Comprehensive Market Insights: The T3 JMA KAMA VWMA Indicator provides a holistic view of market conditions by considering both price and volume dynamics. This comprehensive perspective helps traders make informed decisions.

Analysis and Interpretation

The modified VWMA formula with T3, JMA, and KAMA offers traders a valuable tool for analyzing volume-driven market conditions. By incorporating these advanced moving averages into the VWMA calculation, the indicator becomes more responsive to changes in volume, potentially providing deeper insights into price movements.

When analyzing the modified VWMA, it is essential to consider the following points:

Identifying High-Volume Periods:

The modified VWMA is designed to capture price movements during high-volume periods. Traders can use this indicator to identify potential market trends and determine whether significant trading activity is driving price action. By focusing on these periods, traders may gain a better understanding of the market sentiment and adjust their strategies accordingly.

Confirmation of Trend Strength:

The modified VWMA can serve as a confirmation tool for assessing the strength of a trend. When the VWMA line aligns with the overall trend direction, it suggests that the current price movement is supported by volume. This confirmation can provide traders with additional confidence in their analysis and help them make more informed trading decisions.

Potential Entry and Exit Points:

One of the primary purposes of the modified VWMA is to assist traders in identifying potential entry and exit points. By capturing volume-driven price movements, the indicator can highlight areas where market participants are actively participating, indicating potential opportunities for opening or closing positions. Traders can use this information in conjunction with other technical analysis tools to develop comprehensive trading strategies.

Interpretation of Angle and Gradient:

The modified VWMA incorporates an angle calculation and color gradient to further enhance interpretation. The angle of the VWMA line represents the slope of the indicator, providing insights into the momentum of price movements. A steep angle indicates strong momentum, while a shallow angle suggests a slowdown. The color gradient helps visualize this angle, with green indicating bullish momentum and purple indicating bearish momentum.

Conclusion

By modifying the VWMA formula to incorporate the T3, JMA, and KAMA moving averages, the T3 JMA KAMA VWMA Indicator offers traders an innovative tool to exploit high-volume market conditions for optimal position entry. This modification enhances responsiveness, improves timing, and provides comprehensive market insights.

Enjoy checking it out!

---

Credits to:

◾ @cheatcountry – Hann Window Smoothing

◾ @loxx – T3

◾ @everget – JMA

MathEasingFunctionsLibrary "MathEasingFunctions"

A collection of Easing functions.

Easing functions are commonly used for smoothing actions over time, They are used to smooth out the sharp edges

of a function and make it more pleasing to the eye, like for example the motion of a object through time.

Easing functions can be used in a variety of applications, including animation, video games, and scientific

simulations. They are a powerful tool for creating realistic visual effects and can help to make your work more

engaging and enjoyable to the eye.

---

Includes functions for ease in, ease out, and, ease in and out, for the following constructs:

sine, quadratic, cubic, quartic, quintic, exponential, elastic, circle, back, bounce.

---

Reference:

easings.net

learn.microsoft.com

ease_in_sine_unbound(v)

Sinusoidal function, the position over elapsed time (unbound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_in_sine(v)

Sinusoidal function, the position over elapsed time (bound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_out_sine_unbound(v)

Sinusoidal function, the position over elapsed time (unbound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_out_sine(v)

Sinusoidal function, the position over elapsed time (bound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_in_out_sine_unbound(v)

Sinusoidal function, the position over elapsed time (unbound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_in_out_sine(v)

Sinusoidal function, the position over elapsed time (bound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_in_quad_unbound(v)

Quadratic function, the position equals the square of elapsed time (unbound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_in_quad(v)

Quadratic function, the position equals the square of elapsed time (bound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_out_quad_unbound(v)

Quadratic function, the position equals the square of elapsed time (unbound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_out_quad(v)

Quadratic function, the position equals the square of elapsed time (bound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_in_out_quad_unbound(v)

Quadratic function, the position equals the square of elapsed time (unbound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_in_out_quad(v)

Quadratic function, the position equals the square of elapsed time (bound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_in_cubic_unbound(v)

Cubic function, the position equals the cube of elapsed time (unbound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_in_cubic(v)

Cubic function, the position equals the cube of elapsed time (bound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_out_cubic_unbound(v)

Cubic function, the position equals the cube of elapsed time (unbound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_out_cubic(v)

Cubic function, the position equals the cube of elapsed time (bound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_in_out_cubic_unbound(v)

Cubic function, the position equals the cube of elapsed time (unbound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_in_out_cubic(v)

Cubic function, the position equals the cube of elapsed time (bound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_in_quart_unbound(v)

Quartic function, the position equals the formula `f(t)=t^4` of elapsed time (unbound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_in_quart(v)

Quartic function, the position equals the formula `f(t)=t^4` of elapsed time (bound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_out_quart_unbound(v)

Quartic function, the position equals the formula `f(t)=t^4` of elapsed time (unbound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_out_quart(v)

Quartic function, the position equals the formula `f(t)=t^4` of elapsed time (bound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_in_out_quart_unbound(v)

Quartic function, the position equals the formula `f(t)=t^4` of elapsed time (unbound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_in_out_quart(v)

Quartic function, the position equals the formula `f(t)=t^4` of elapsed time (bound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_in_quint_unbound(v)

Quintic function, the position equals the formula `f(t)=t^5` of elapsed time (unbound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_in_quint(v)

Quintic function, the position equals the formula `f(t)=t^5` of elapsed time (bound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_out_quint_unbound(v)

Quintic function, the position equals the formula `f(t)=t^5` of elapsed time (unbound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_out_quint(v)

Quintic function, the position equals the formula `f(t)=t^5` of elapsed time (bound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_in_out_quint_unbound(v)

Quintic function, the position equals the formula `f(t)=t^5` of elapsed time (unbound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_in_out_quint(v)

Quintic function, the position equals the formula `f(t)=t^5` of elapsed time (bound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_in_expo_unbound(v)

Exponential function, the position equals the exponential formula of elapsed time (unbound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_in_expo(v)

Exponential function, the position equals the exponential formula of elapsed time (bound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_out_expo_unbound(v)

Exponential function, the position equals the exponential formula of elapsed time (unbound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_out_expo(v)

Exponential function, the position equals the exponential formula of elapsed time (bound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_in_out_expo_unbound(v)

Exponential function, the position equals the exponential formula of elapsed time (unbound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_in_out_expo(v)

Exponential function, the position equals the exponential formula of elapsed time (bound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_in_circ_unbound(v)

Circular function, the position equals the circular formula of elapsed time (unbound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_in_circ(v)

Circular function, the position equals the circular formula of elapsed time (bound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_out_circ_unbound(v)

Circular function, the position equals the circular formula of elapsed time (unbound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_out_circ(v)

Circular function, the position equals the circular formula of elapsed time (bound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_in_out_circ_unbound(v)

Circular function, the position equals the circular formula of elapsed time (unbound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_in_out_circ(v)

Circular function, the position equals the circular formula of elapsed time (bound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_in_back_unbound(v)

Back function, the position retreats a bit before resuming (unbound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_in_back(v)

Back function, the position retreats a bit before resuming (bound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_out_back_unbound(v)

Back function, the position retreats a bit before resuming (unbound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_out_back(v)

Back function, the position retreats a bit before resuming (bound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_in_out_back_unbound(v)

Back function, the position retreats a bit before resuming (unbound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_in_out_back(v)

Back function, the position retreats a bit before resuming (bound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_in_elastic_unbound(v)

Elastic function, the position oscilates back and forth like a spring (unbound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_in_elastic(v)

Elastic function, the position oscilates back and forth like a spring (bound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_out_elastic_unbound(v)

Elastic function, the position oscilates back and forth like a spring (unbound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_out_elastic(v)

Elastic function, the position oscilates back and forth like a spring (bound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_in_out_elastic_unbound(v)

Elastic function, the position oscilates back and forth like a spring (unbound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_in_out_elastic(v)

Elastic function, the position oscilates back and forth like a spring (bound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_in_bounce_unbound(v)

Bounce function, the position bonces from the boundery (unbound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_in_bounce(v)

Bounce function, the position bonces from the boundery (bound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_out_bounce_unbound(v)

Bounce function, the position bonces from the boundery (unbound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_out_bounce(v)

Bounce function, the position bonces from the boundery (bound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_in_out_bounce_unbound(v)

Bounce function, the position bonces from the boundery (unbound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

ease_in_out_bounce(v)

Bounce function, the position bonces from the boundery (bound).

Parameters:

v (float) : `float` Elapsed time.

Returns: Ratio of change.

select(v, formula, effect, bounded)

Parameters:

v (float)

formula (string)

effect (string)

bounded (bool)

Adaptive Fusion ADX VortexIntroduction

The Adaptive Fusion ADX DI Vortex Indicator is a powerful tool designed to help traders identify trend strength and potential trend reversals in the market. This indicator uses a combination of technical analysis (TA) and mathematical concepts to provide accurate and reliable signals.

Features

The Adaptive Fusion ADX DI Vortex Indicator has several features that make it a powerful tool for traders. The Fusion Mode combines the Vortex Indicator and the ADX DI indicator to provide a more accurate picture of the market. The Hurst Exponent Filter helps to filter out choppy markets (inspired by balipour). Additionally, the indicator can be customized with various inputs and settings to suit individual trading strategies.

Signals

The enterLong signal is generated when the algorithm detects that it's a good time to buy a stock or other asset. This signal is based on certain conditions such as the values of technical indicators like ADX, Vortex, and Fusion. For example, if the ADX value is above a certain threshold and there is a crossover between the plus and minus lines of the ADX indicator, then the algorithm will generate an enterLong signal.

Similarly, the enterShort signal is generated when the algorithm detects that it's a good time to sell a stock or other asset. This signal is also based on certain conditions such as the values of technical indicators like ADX, Vortex, and Fusion. For example, if the ADX value is above a certain threshold and there is a crossunder between the plus and minus lines of the ADX indicator, then the algorithm will generate an enterShort signal.

The exitLong and exitShort signals are generated when the algorithm detects that it's a good time to close a long or short position, respectively. These signals are also based on certain conditions such as the values of technical indicators like ADX, Vortex, and Fusion. For example, if the ADX value crosses above a certain threshold or there is a crossover between the minus and plus lines of the ADX indicator, then the algorithm will generate an exitLong signal.

Usage

Traders can use this indicator in a variety of ways, depending on their trading strategy and style. Short-term traders may use it to identify short-term trends and potential trade opportunities, while long-term traders may use it to identify long-term trends and potential investment opportunities. The indicator can also be used to confirm other technical indicators or trading signals. Personally, I prefer to use it for short-term trades.

Strengths

One of the strengths of the Adaptive Fusion ADX DI Vortex Indicator is its accuracy and reliability. The indicator uses a combination of TA and mathematical concepts to provide accurate and reliable signals, helping traders make informed trading decisions. It is also versatile and can be used in a variety of trading strategies.

Weaknesses

While this indicator has many strengths, it also has some weaknesses. One of the weaknesses is that it can generate false signals in choppy or sideways markets. Additionally, the indicator may lag behind the market, making it less effective in fast-moving markets. That's a reason why I included the Hurst Exponent Filter and special smoothing.

Concepts

The Adaptive ADX DI Vortex Indicator with Fusion Mode and Hurst Filter is based on several key concepts. The Average Directional Index (ADX) is used to measure trend strength, while the Vortex Indicator is used to identify trend reversals. The Hurst Exponent is used to filter out noise and provide a more accurate picture of the market.

In conclusion, the Adaptive Fusion ADX DI Vortex Indicator is a versatile and powerful tool for traders. By combining technical analysis and mathematical concepts, this indicator provides accurate and reliable signals for identifying trend strength and potential trend reversals. While it has some weaknesses, its many strengths and features make it a valuable addition to any trader's toolbox.

---

Credits to:

▪️@cheatcountry – Hann Window Smoohing

▪️@loxx – VHF and T3

▪️@balipour – Hurst Exponent Filter

Ehlers Data Sampling Relative Strength Indicator [CC]The Data Sampling Indicator was created by John Ehlers (Stocks and Commodities Mar 2023) and this is a genius method to reduce noise in the market data but also doesn't introduce any lag while doing so. The way this works is because traditionally, people have always relied on the close price as the default input for many indicators such as the RSI or MACD as examples. Since the open is usually virtually identical to the previous close, it has been ignored by most people but Ehlers discovered that if you do a simple average of open and close for the input on any indicator, you can remove much of the noise without any added lag. I have used the RSI as he did in his example and plotted both to show the difference between the traditional RSI and using Ehlers' process as the new Data Sampling RSI. You can clearly see that this new RSI follows the price fluctuations much closer and is much smoother than the traditional RSI. As usual, I have included different colors to show the strength of the buy or sell signals so darker colors mean it is a very strong signal and lighter colors means it is a normal signal. Buy when the line turns green and sell when it turns red.

Feel free to try out this method to replace the input for any indicator and let me know how this works for you! And of course let me know if you would like me to publish any indicator script.

VHF Adaptive Linear Regression KAMAIntroduction

Heyo, in this indicator I decided to add VHF adaptivness, linear regression and smoothing to a KAMA in order to squeeze all out of it.

KAMA:

Developed by Perry Kaufman, Kaufman's Adaptive Moving Average (KAMA) is a moving average designed to account for market noise or volatility. KAMA will closely follow prices when the price swings are relatively small and the noise is low. KAMA will adjust when the price swings widen and follow prices from a greater distance. This trend-following indicator can be used to identify the overall trend, time turning points and filter price movements.

VHF:

Vertical Horizontal Filter (VHF) was created by Adam White to identify trending and ranging markets. VHF measures the level of trend activity, similar to ADX DI. Vertical Horizontal Filter does not, itself, generate trading signals, but determines whether signals are taken from trend or momentum indicators. Using this trend information, one is then able to derive an average cycle length.

Linear Regression Curve:

A line that best fits the prices specified over a user-defined time period.

This is very good to eliminate bad crosses of KAMA and the pric.

Usage

You can use this indicator on every timeframe I think. I mostly tested it on 1 min, 5 min and 15 min.

Signals

Enter Long -> crossover(close, kama) and crossover(kama, kama )

Enter Short -> crossunder(close, kama) and crossunder(kama, kama )

Thanks for checking this out!

--

Credits to

▪️@cheatcountry – Hann Window Smoohing

▪️@loxx – VHF and T3

▪️@LucF – Gradient

Multi SMI Ergodic OscillatorThe Multi SMI Ergodic Oscillator (Multi SMIEO) indicator can be used to identify potential buy and sell signals based on the relationship between the TSI and EMA lines.

The script is creating an indicator that plots multiple (3) sets of Time Series Indicator (TSI-Indicator) and Exponential Moving Average (EMA-Signal) lines as a single indicator.

The TSI is a momentum oscillator that helps identify overbought and oversold conditions. It is calculated using the close prices of an asset, a short-term moving average, and a long-term moving average. The script uses three different pairs of input values for the short-term and long-term periods, which can be adjusted by the user.

The EMA is a type of moving average that gives more weight to recent prices. It is calculated by applying a weighting factor to the most recent price, and then adding that weighted value to the previous EMA value. The script uses three different input values for the length of the EMA, which can also be adjusted by the user.

After calculating the TSI and EMA for each set, the script plots them on the same graph, with different colors and widths to differentiate them. The three sets of TSI and EMA lines are plotted to allow the user to compare the results of different periods. The script also plots a horizontal line at zero, which is used as a reference point for the oscillations of the indicator lines.

One way to use this indicator is to look for crossovers between the TSI and the EMA lines. A bullish crossover occurs when the TSI crosses above the EMA. This suggests that the buying pressure is increasing and a potential buy signal is generated. A bearish crossover occurs when the TSI crosses below the EMA. This suggests that the selling pressure is increasing and a potential sell signal is generated.

Some other ways that the indicator can be used include:

1. Identifying trends: The TSI and EMA lines can be used to identify the direction of the trend. An uptrend is present when the TSI and EMA lines are both trending upwards, while a downtrend is present when the TSI and EMA lines are both trending downwards.

2. Overbought and oversold conditions: The TSI can be used to identify overbought and oversold conditions. When the TSI is above the upper limit of the range, the asset is considered overbought and may be due for a price correction. Conversely, when the TSI is below the lower limit of the range, the asset is considered oversold and may be due for a price rebound.

3. Confirming price action: The Multi SMIEO indicator can be used to confirm price action. If a bullish divergence is present, it confirms a potential bullish reversal. If a bearish divergence is present, it confirms a potential bearish reversal.

4. Multiple time frame analysis: By using different periods for the TSI and EMA lines, the indicator can be used to analyze the asset on multiple time frames. It can be useful to compare the results of different periods to get a better understanding of the asset's price movements.

5. Risk management: This indicator can be used as an element of risk management strategy, it can help traders to identify overbought and oversold conditions to set stop loss or take profit levels.

The Multi SMI Ergodic Oscillator (Multi SMIEO) is a versatile indicator that can be used in a number of ways to analyze the price movements of an asset. It can be used to identify potential buy and sell signals, trends, overbought and oversold conditions, and to confirm price action. By using different periods for the TSI and EMA lines, the indicator can also be used to analyze the asset on multiple time frames. However, it is important to remember that indicators are based on historical data, and past performance does not guarantee future results.

It is important to use the indicator as part of a comprehensive trading strategy that includes risk management and other analysis techniques, such as fundamental and technical analysis. It is also important to keep in mind that indicators are not a standalone solution for trading, they should be used in conjunction with other market analysis and research techniques to generate better results.

Lastly, it is important to keep in mind that trading in financial markets comes with a certain level of risk and it is crucial to always have a proper risk management plan in place. Never invest more than you can afford to lose.

Recent Distance Dynamic AverageThis experimental moving average references the highest percent distance from source to historical output

The length is adapted by

- tightening as the source and output distance grow

- loosening when the output has caught up.

Can be used "indicator on indicator" as a smoother or stabilizer.

Smooth EMA/DEMA/TEMA/EHMA (SEMA)This is my attempt at smoothing the exponential moving average any its cousins. I literally just smoothed the source and alpha and this is what we got. I really like this because you get a nice smooth yet fast acting moving average that works better than a traditional simple moving average. This script also included directional alerts.

Smooth EMA

Smooth DEMA

Smooth TEMA

Smooth EHMA

Adaptive VWAP Stdev BandsIntroduction

Heyo, here are some adaptive VWAP Standard Deviation Bands with nice colors.

I used Ehlers dominant cycle theories and ZLSMA smoothing to create this indicator.

You can choose between different algorithms to determine the dominant cycle and this will be used as reset period.

Everytime bar_index can be divided through the dominant cycle length and the result is zero VWAP resets if have chosen an adaptive mode in the settings.

The other reset event you can use is just a simple time-based event, e.g. reset every day.

Usage

I think people buy/sell when it reaches extreme zones.

Enjoy!

---

Credits to:

@SandroTurriate - VWAP Stdev Bands

@blackcat1402 - Dominant Cycle Analysis

@DasanC - Dominant Cycle Analysis

@veryfid - ZLSMA

(Sry, too lazy for linking)

I took parts of their code. Ty guys for your work! Just awesome.

Many Moving AveragesA smooth looking indicator created from a mix of ALMA and LRC curves. Includes alternative calculation for both which I came up with through trial and error so a variety of combinations work to varying degrees. Just something I was playing around with that looked pretty nice in the end.

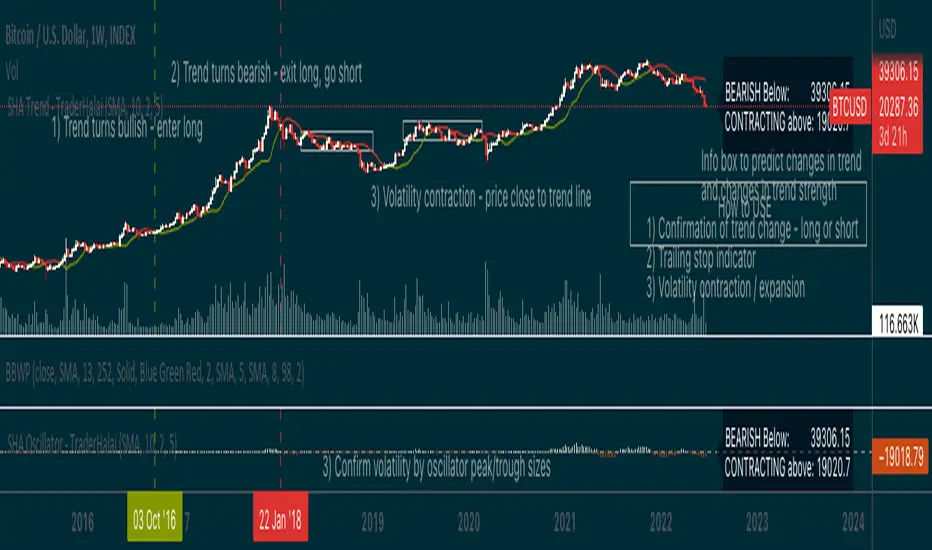

Smoothed Heikin Ashi Trend on Chart - TraderHalai BACKTESTSmoothed Heikin Ashi Trend on chart - Backtest

This is a backtest of the Smoothed Heikin Ashi Trend indicator, which computes the reverse candle close price required to flip a Heikin Ashi trend from red to green and vice versa. The original indicator can be found in the scripts section of my profile.

This particular back test uses this indicator with a Trend following paradigm with a percentage-based stop loss.

Note, that backtesting performance is not always indicative of future performance, but it does provide some basis for further development and walk-forward / live testing.

Testing was performed on Bitcoin , as this is a primary target market for me to use this kind of strategy.

Sample Backtesting results as of 10th June 2022:

Backtesting parameters:

Position size: 10% of equity

Long stop: 1% below entry

Short stop: 1% above entry

Repainting: Off

Smoothing: SMA

Period: 10

8 Hour:

Number of Trades: 1046

Gross Return: 249.27 %

CAGR Return: 14.04 %

Max Drawdown: 7.9 %

Win percentage: 28.01 %

Profit Factor (Expectancy): 2.019

Average Loss: 0.33 %

Average Win: 1.69 %

Average Time for Loss: 1 day

Average Time for Win: 5.33 days

1 Day:

Number of Trades: 429

Gross Return: 458.4 %

CAGR Return: 15.76 %

Max Drawdown: 6.37 %

Profit Factor (Expectancy): 2.804

Average Loss: 0.8 %

Average Win: 7.2 %

Average Time for Loss: 3 days

Average Time for Win: 16 days

5 Day:

Number of Trades: 69

Gross Return: 1614.9 %

CAGR Return: 26.7 %

Max Drawdown: 5.7 %

Profit Factor (Expectancy): 10.451

Average Loss: 3.64 %

Average Win: 81.17 %

Average Time for Loss: 15 days

Average Time for Win: 85 days

Analysis:

The strategy is typical amongst trend following strategies with a less regular win rate, but where profits are more significant than losses. Most of the losses are in sideways, low volatility markets. This strategy performs better on higher timeframes, where it shows a positive expectancy of the strategy.

The average win was positively impacted by Bitcoin’s earlier smaller market cap, as the percentage wins earlier were higher.

Overall the strategy shows potential for further development and may be suitable for walk-forward testing and out of sample analysis to be considered for a demo trading account.

Note in an actual trading setup, you may wish to use this with volatility filters, combined with support resistance zones for a better setup.

As always, this post/indicator/strategy is not financial advice, and please do your due diligence before trading this live.

Original indicator links:

On chart version -

Oscillator version -

Update - 27/06/2022

Unfortunately, It appears that the original script had been taken down due to auto-moderation because of concerns with no slippage / commission. I have since adjusted the backtest, and re-uploaded to include the following to address these concerns, and show that I am genuinely trying to give back to the community and not mislead anyone:

1) Include commission of 0.1% - to match Binance's maker fees prior to moving to a fee-less model.

2) Include slippage of 10 ticks (This is a realistic slippage figure from searching online for most crypto exchanges)

3) Adjust account balance to 10,000 - since most of us are not millionaires.

The rest of the backtesting parameters are comparable to previous results:

Backtesting parameters:

Initial capital: 10000 dollars

Position size: 10% of equity

Long stop: 2% below entry

Short stop: 2% above entry

Repainting: Off

Smoothing: SMA

Period: 10

Slippage: 10 ticks

Commission: 0.1%

This script still remains to shows viability / profitablity on higher term timeframes (with slightly higher drawdown), and I have included the backtest report below to document my findings:

8 Hour:

Number of Trades: 1082

Gross Return: 233.02%

CAGR Return: 14.04 %

Max Drawdown: 7.9 %

Win percentage: 25.6%

Profit Factor (Expectancy): 1.627

Average Loss: 0.46 %

Average Win: 2.18 %

Average Time for Loss: 1.33 day

Average Time for Win: 7.33 days

Once again, please do your own research and due dillegence before trading this live. This post is for education and information purposes only, and should not be taken as financial advice.

EchoMorphicAverageLibrary "EchoMorphicAverage"

Original Self Referencing Moving Average which references

it's own output agsainst itself and the incoming source to dynamically

alter smoothness and length internally per calculation cycle.

@kaigouthro

Inputs are float length series.

Contact Me for More Dynamic Float Length Indicators.

wema(src, mod, len)

Waited Echo-Morphic Average

Parameters:

src : (float) input value

mod : (float) modifier(0-1) mix of current value

len : (float) length

Returns: output processed smoothed value

wemaStack(src, mod, len)

Stacked Multipass Waited Echo-Morphic Average

Parameters:

src : (float) input value

mod : (float) modifier(0-1) mix of current value

len : (float) length

Returns: output processed smoothed value

Heikin Ashi Volatility Percentile - TraderHalaiThe Heikin Ashi Volatility Percentile (HAVP) Oscillator was inspired by the legendary Bollinger Band Width Percentile indicator(known as BBWP), written by Caretaker, and made famous by Eric Krown, a famous influencer.

This script borrows aspects of the BBWP indicator which enables the HAVP oscillator to visually match the look and feel of BBWP and allows similar configuration functions (such as colouring function, smoothing MAs and alerts)

The fundamentals of this script are however different to BBWP. Instead of Bollinger band width, this script uses a reverse function of Heikin Ashi close (implemented in my Smoothed Heikin Ashi Trend

indicator, linked below).

The reverse Heikin Ashi close is smoothed using Ehler's SuperSmoother function, providing smooth oscillation and earlier signals of volatility tops and bottoms.

From an automated backtest that I have conducted on the BTCUSD index pair, I have observed comparable performance to BBWP across multiple timeframes when combining with stochastic direction to give a bias on overall direction. Using parameters I have tested, it performs better on mid-term timeframes such as 3h,4h and 6h. BBWP outperforms on 1h and 1d, with lower timeframes being comparable.

From the results, using HAVP over BBWP tends to result in reduced holding time and more frequent trades, which may or may not be desirable, although the behaviour can be adjusted using the parameters provided.

For instance, the smoother oscillation provided by HAVP provides a great predictability factor and earlier confirmation signals, which is something that Ehler emphasised in his trading style, and something which I agree with personally. I would encourage you to try out both HAVP and BBWP and see which fits your trading style.

Releasing this as open source allows for the betterment of the community and further development, criticism and discussion.

Thanks and enjoy! :)

Smoothed Heikin Ashi Trend on Chart - TraderHalaiThis indicator is a predictive tool using Heikinashi to calculate shifts in trade direction.

It works by reverse-engineering the regular candle stick closing price required, to flip the Heiken Ashi candle from Red to Green and vice-versa.

Below, is an earlier indicator that I released and created. This plots this price as an oscillator, which allows traders to get a predictive indicator of a trend change.

This indicator extends upon this functionality by adding a smoothing function to the reverse-engineered regular candle stick closing price, to reduce the choppiness of signals. It also plots the indicator on the chart to allow for easier visual confirmation.

How to use

1) As a directional bias - Bullish or bearish

2) Volatility expansion/contraction - further distance from line means volatility expansion - am planning to release an oscillator version also

3) Trailing stop loss - once you are in a trade

Other Features

Select a moving average period and smoothing calculation method (e.g. SMA / EMA)

Non-repaint mode for backtesting and use/integration with higher timeframes

Final note - Open Source

I am releasing this as open-source for the benefit of the community and to allow further development, scrutiny and criticism. Please feel free to use this indicator as you see fit. If you do use this indicator to create another script, feel free to drop me a note, as I would be highly interested in your idea.

Thanks, and Enjoy!