Crypto Options Greeks & Volatility Analyzer [BackQuant]Crypto Options Greeks & Volatility Analyzer

Overview

The Crypto Options Greeks & Volatility Analyzer is a comprehensive analytical tool that calculates Black-Scholes option Greeks up to the third order for Bitcoin and Ethereum options. It integrates implied volatility data from VOLMEX indices and provides multiple visualization layers for options risk analysis.

Quick Introduction to Options Trading

Options are financial derivatives that give the holder the right, but not the obligation, to buy or sell an underlying asset at a predetermined price (strike price) within a specific time period (expiration date). Understanding options requires grasping two fundamental concepts:

Call Options : Give the right to buy the underlying asset at the strike price. Calls increase in value when the underlying price rises above the strike price.

Put Options : Give the right to sell the underlying asset at the strike price. Puts increase in value when the underlying price falls below the strike price.

The Language of Options: Greeks

Options traders use "Greeks" - mathematical measures that describe how an option's price changes in response to various factors:

Delta : How much the option price moves for each $1 change in the underlying

Gamma : How fast delta changes as the underlying moves

Theta : Daily time decay - how much value erodes each day

Vega : Sensitivity to implied volatility changes

Rho : Sensitivity to interest rate changes

These Greeks are essential for understanding risk. Just as a pilot needs instruments to fly safely, options traders need Greeks to navigate market conditions and manage positions effectively.

Why Volatility Matters

Implied volatility (IV) represents the market's expectation of future price movement. High IV means:

Options are more expensive (higher premiums)

Market expects larger price swings

Better for option sellers

Low IV means:

Options are cheaper

Market expects smaller moves

Better for option buyers

This indicator helps you visualize and quantify these critical concepts in real-time.

Back to the Indicator

Key Features & Components

1. Complete Greeks Calculations

The indicator computes all standard Greeks using the Black-Scholes-Merton model adapted for cryptocurrency markets:

First Order Greeks:

Delta (Δ) : Measures the rate of change of option price with respect to underlying price movement. Ranges from 0 to 1 for calls and -1 to 0 for puts.

Vega (ν) : Sensitivity to implied volatility changes, expressed as price change per 1% change in IV.

Theta (Θ) : Time decay measured in dollars per day, showing how much value erodes with each passing day.

Rho (ρ) : Interest rate sensitivity, measuring price change per 1% change in risk-free rate.

Second Order Greeks:

Gamma (Γ) : Rate of change of delta with respect to underlying price, indicating how quickly delta will change.

Vanna : Cross-derivative measuring delta's sensitivity to volatility changes and vega's sensitivity to price changes.

Charm : Delta decay over time, showing how delta changes as expiration approaches.

Vomma (Volga) : Vega's sensitivity to volatility changes, important for volatility trading strategies.

Third Order Greeks:

Speed : Rate of change of gamma with respect to underlying price (∂Γ/∂S).

Zomma : Gamma's sensitivity to volatility changes (∂Γ/∂σ).

Color : Gamma decay over time (∂Γ/∂T).

Ultima : Third-order volatility sensitivity (∂²ν/∂σ²).

2. Implied Volatility Analysis

The indicator includes a sophisticated IV ranking system that analyzes current implied volatility relative to its recent history:

IV Rank : Percentile ranking of current IV within its 30-day range (0-100%)

IV Percentile : Percentage of days in the lookback period where IV was lower than current

IV Regime Classification : Very Low, Low, High, or Very High

Color-Coded Headers : Visual indication of volatility regime in the Greeks table

Trading regime suggestions based on IV rank:

IV Rank > 75%: "Favor selling options" (high premium environment)

IV Rank 50-75%: "Neutral / Sell spreads"

IV Rank 25-50%: "Neutral / Buy spreads"

IV Rank < 25%: "Favor buying options" (low premium environment)

3. Gamma Zones Visualization

Gamma zones display horizontal price levels where gamma exposure is highest:

Purple horizontal lines indicate gamma concentration areas

Opacity scaling : Darker shading represents higher gamma values

Percentage labels : Shows gamma intensity relative to ATM gamma

Customizable zones : 3-10 price levels can be analyzed

These zones are critical for understanding:

Pin risk around expiration

Potential for explosive price movements

Optimal strike selection for gamma trading

Market maker hedging flows

4. Probability Cones (Expected Move)

The probability cones project expected price ranges based on current implied volatility:

1 Standard Deviation (68% probability) : Shown with dashed green/red lines

2 Standard Deviations (95% probability) : Shown with dotted green/red lines

Time-scaled projection : Cones widen as expiration approaches

Lognormal distribution : Accounts for positive skew in asset prices

Applications:

Strike selection for credit spreads

Identifying high-probability profit zones

Setting realistic price targets

Risk management for undefined risk strategies

5. Breakeven Analysis

The indicator plots key price levels for options positions:

White line : Strike price

Green line : Call breakeven (Strike + Premium)

Red line : Put breakeven (Strike - Premium)

These levels update dynamically as option premiums change with market conditions.

6. Payoff Structure Visualization

Optional P&L labels display profit/loss at expiration for various price levels:

Shows P&L at -2 sigma, -1 sigma, ATM, +1 sigma, and +2 sigma price levels

Separate calculations for calls and puts

Helps visualize option payoff diagrams directly on the chart

Updates based on current option premiums

Configuration Options

Calculation Parameters

Asset Selection : BTC or ETH (limited by VOLMEX IV data availability)

Expiry Options : 1D, 7D, 14D, 30D, 60D, 90D, 180D

Strike Mode : ATM (uses current spot) or Custom (manual strike input)

Risk-Free Rate : Adjustable annual rate for discounting calculations

Display Settings

Greeks Display : Toggle first, second, and third-order Greeks independently

Visual Elements : Enable/disable probability cones, gamma zones, P&L labels

Table Customization : Position (6 options) and text size (4 sizes)

Price Levels : Show/hide strike and breakeven lines

Technical Implementation

Data Sources

Spot Prices : INDEX:BTCUSD and INDEX:ETHUSD for underlying prices

Implied Volatility : VOLMEX:BVIV (Bitcoin) and VOLMEX:EVIV (Ethereum) indices

Real-Time Updates : All calculations update with each price tick

Mathematical Framework

The indicator implements the full Black-Scholes-Merton model:

Standard normal distribution approximations using Abramowitz and Stegun method

Proper annualization factors (365-day year)

Continuous compounding for interest rate calculations

Lognormal price distribution assumptions

Alert Conditions

Four categories of automated alerts:

Price-Based : Underlying crossing strike price

Gamma-Based : 50% surge detection for explosive moves

Moneyness : Deep ITM alerts when |delta| > 0.9

Time/Volatility : Near expiration and vega spike warnings

Practical Applications

For Options Traders

Monitor all Greeks in real-time for active positions

Identify optimal entry/exit points using IV rank

Visualize risk through probability cones and gamma zones

Track time decay and plan rolls

For Volatility Traders

Compare IV across different expiries

Identify mean reversion opportunities

Monitor vega exposure across strikes

Track higher-order volatility sensitivities

Conclusion

The Crypto Options Greeks & Volatility Analyzer transforms complex mathematical models into actionable visual insights. By combining institutional-grade Greeks calculations with intuitive overlays like probability cones and gamma zones, it bridges the gap between theoretical options knowledge and practical trading application.

Whether you're:

A directional trader using options for leverage

A volatility trader capturing IV mean reversion

A hedger managing portfolio risk

Or simply learning about options mechanics

This tool provides the quantitative foundation needed for informed decision-making in cryptocurrency options markets.

Remember that options trading involves substantial risk and complexity. The Greeks and visualizations provided by this indicator are tools for analysis - they should be combined with proper risk management, position sizing, and a thorough understanding of options strategies.

As crypto options markets continue to mature and grow, having professional-grade analytics becomes increasingly important. This indicator ensures you're equipped with the same analytical capabilities used by institutional traders, adapted specifically for the unique characteristics of 24/7 cryptocurrency markets.

Statistics

Sat Stacking Strategies Simulation (SSSS)Sat Stacking Strategies Simulation (SSSS)

This indicator simulates and compares different Bitcoin stacking strategies over time, allowing you to visualize performance, cost basis, and stacking behavior directly on your chart.

Core Features:

Three Stacking Strategies

• Trend-Based – Stack only when price is above/below a long-term SMA.

• Stack the Dip – Buy during sharp pullbacks or oversold conditions.

• Price Zone – Stack only in “cheap”, “fair”, or “expensive” zones based on a simulated Short-Term Holder (STH) cost basis.

Always Stack Benchmark

Compare your chosen strategy against a simple “Always Stack” approach for a real-world DCA reference.

Performance Metrics Table

Track:

• Total Fiat Added

• Total BTC Accumulated

• Current Value

• Average Cost per BTC

• PnL %

• CAGR

• Sharpe Ratio & Stdev

• Stack Events & Time Underwater

Advanced Options

• Simulate cash-secured puts on unused fiat.

• Simulate covered calls on BTC holdings.

• Roll over unused stacking amounts for future buys.

This tool is designed for Bitcoiners, stackers, and DCA enthusiasts who want to backtest and visualize their stacking plan—whether you keep it simple or go full quant.

Sometimes the best alpha is just showing up every week with your wallet open… and occasionally wearing a helmet. 🪖💰

Hann Window FIR Filter Ribbon [BigBeluga]🔵 OVERVIEW

The Hann Window FIR Filter Ribbon is a trend-following visualization tool based on a family of FIR filters using the Hann window function. It plots a smooth and dynamic ribbon formed by six Hann filters of progressively increasing length. Gradient coloring and filled bands reveal trend direction and compression/expansion behavior. When short-term trend shifts occur (via filter crossover), it automatically anchors visual support/resistance zones at the nearest swing highs or lows.

🔵 CONCEPTS

Hann FIR Filter: A finite impulse response filter that uses a Hann (cosine-based) window for weighting past price values, resulting in a non-lag, ultra-smooth output.

hannFilter(length)=>

var float hann = na // Final filter output

float filt = 0

float coef = 0

for i = 1 to length

weight = 1 - math.cos(2 * math.pi * i / (length + 1))

filt += price * weight

coef += weight

hann := coef != 0 ? filt / coef : na

Ribbon Stack: The indicator plots 6 Hann FIR filters with increasing lengths, creating a smooth "ribbon" that adapts to price shifts and visually encodes volatility.

Gradient Coloring: Line colors and fill opacity between layers are dynamically adjusted based on the distance between the filters, showing momentum expansion or contraction.

Dynamic Swing Zones: When the shortest filter crosses its nearest neighbor, a swing high/low is located, and a triangle-style level is anchored and projected to the right.

Self-Extending Levels: These dynamic levels persist and extend until invalidated or replaced by a new opposite trend break.

🔵 FEATURES

Plots 6 Hann FIR filters with increasing lengths (controlled by Ribbon Size input).

Automatically colors each filter and the fill between them with smooth gradient transitions.

Detects trend shifts via filter crossover and anchors visual resistance (red) or support (green) zones.

Support/resistance zones are triangle-style bands built around recent swing highs/lows.

Levels auto-extend right and adapt in real time until invalidated by price action.

Ribbon responds smoothly to price and shows contraction or expansion behavior clearly.

No lag in crossover detection thanks to FIR architecture.

Adjustable sensitivity via Length and Ribbon Size inputs.

🔵 HOW TO USE

Use the ribbon gradient as a visual trend strength and smooth direction cue.

Watch for crossover of shortest filters as early trend change signals.

Monitor support/resistance zones as potential high-probability reaction points.

Combine with other tools like momentum or volume to confirm trend breaks.

Adjust ribbon thickness and length to suit your trading timeframe and volatility preference.

🔵 CONCLUSION

Hann Window FIR Filter Ribbon blends digital signal processing with trading logic to deliver a visually refined, non-lagging trend tool. The adaptive ribbon offers insight into momentum compression and release, while swing-based levels give structure to potential reversals. Ideal for traders who seek smooth trend detection with intelligent, auto-adaptive zone plotting.

Price Label with Custom SymbolsThis Indicator plots a label with RSI, Current price of the selected chart symbol, Net change and percent change, VIX at previous day close, Current VIX and some Market helpers like ES, DXY, CL, TICK, ADD and VOLD. You can replace the symbols for your favorites.

TRI - Quick Analysis"TRI - Quick Analysis" is a multi-indicator dashboard designed to give traders an immediate overview of market momentum, trend strength, volume flow, and volatility.

It visually summarizes key technical indicators in a compact table, including:

RSI (momentum)

MACD Histogram (trend momentum)

ADX + SuperTrend (trend strength & direction)

StochRSI (oversold/overbought)

CCI (price deviation)

CMF (volume flow)

MFI (volume-weighted momentum)

OBV (cumulative volume pressure)

ATR (volatility)

%B Bollinger (position within Bollinger Bands)

Each value is color-coded (green, red, blue) based on whether it's favorable, unfavorable, or neutral for a potential long position.

At the bottom of the table, a summary score dynamically aggregates signals from all indicators and provides a simple trading score.

This tool is designed for discretionary traders looking for a quick, color-coded insight into current market conditions without relying on a single signal.

Multi-Ticker TableMulti-Ticker Table

A customizable TradingView indicator that displays a clean, organized table of up to 10 user-defined ticker symbols with their current daily price, daily dollar change, and daily percentage change.

Key features include:

Enable/disable individual tickers with custom symbols

Customizable font sizes and colors for header and body rows

Customizable table background colors for header and data rows

Flexible table positioning anywhere on the chart (top/middle/bottom × left/center/right)

Highlights positive changes in green and negative changes in red for quick visual analysis

Hides chart candles to display the table as a standalone dashboard

Ideal for traders who want a quick, at-a-glance summary of multiple markets or instruments without cluttering the chart.

Futures Risk Contract TableFutures risk table for NQ MNQ YM MYM ES and MES

changeable capital and risk percentage along with points.

Daily Manipulation Probability Dashboard📜 Summary

Tired of getting stopped out on a "Judas Swing" just before the price moves in your intended direction? This indicator is designed to give you a statistical edge by quantifying the daily manipulation move.

The Daily Manipulation Probability Dashboard analyzes thousands of historical trading days to reveal the probability of the initial "stop-hunt" or "fakeout" move reaching certain percentage levels. It presents this data in a clean, intuitive dashboard right on your chart, helping you make more data-driven decisions about stop-loss placement and entry timing.

🧠 The Core Concept

The logic is simple but powerful. For every trading day, we measure two things:

Amplitude Above Open (AAO): The distance price travels up from the daily open (High - Open).

Amplitude Below Open (ABO): The distance price travels down from the daily open (Open - Low).

The indicator defines the "Manipulation" as the smaller of these two moves. The idea is that this smaller move often acts as a liquidity grab to trap traders before the day's primary, larger move ("Distribution") begins.

This tool focuses exclusively on providing deep statistical insight into this crucial manipulation phase.

🛠️ How to Use This Tool

This dashboard is designed to be a practical part of your daily analysis and trade planning.

1. Smarter Stop-Loss Placement

This is the primary use case. The "Prob. (%)" column tells you the historical chance of the manipulation move being at least a certain size.

Example: If the table shows that for EURUSD, the ≥ 0.25% level has a probability of 30%, you can flip this information: there is a 70% probability that the daily manipulation move will be less than 0.25%.

Action: Placing your stop-loss just beyond a level with a low probability gives you a statistically sound buffer against typical stop-hunts.

2. Entry Timing and Patience

The live arrow (→) shows you where the current day's manipulation falls.

Example: If the arrow is pointing at ≥ 0.10% and you know there is a high probability (e.g., 60%) of the manipulation reaching ≥ 0.20%, you might wait for a deeper pullback before entering, anticipating that the "Judas Swing" hasn't completed yet.

3. Assessing Daily Character

Quickly see if the current day's action is unusual. If the manipulation move is already in a very low probability zone (e.g., > 1.00%), it might indicate that your Bias is wrong, or signal a high-volatility day or a potential trend reversal.

📊 Understanding the Dashboard

Ticker: The top-right shows the current symbol you are analyzing.

→ (Arrow): Points to the row that corresponds to the current, live day's manipulation amplitude.

Manip. Level: The percentage threshold being analyzed (e.g., ≥ 0.20%).

Days Analyzed: The raw count of historical days where the manipulation move met or exceeded this level.

Prob. (%): The key statistic. The cumulative probability of the manipulation move being at least the size of the level.

⚙️ Settings

Position: Choose where you want the dashboard to appear on your chart.

Text Size: Adjust the font size for readability.

Max Historical Days to Analyze: Set the number of past daily candles to include in the statistical analysis. A larger number provides a more robust sample size.

I believe this tool provides a unique, data-driven edge for intraday traders across all markets (Forex, Crypto, Stocks, Indices). Your feedback and suggestions are highly welcome!

- @traderprimez

Filtro Antirumore – Breakout + Volume by G.I.N.e TradingWhat this indicator does:

- Calculates the range of the last N candles (default: 10)

- Generates a signal only if the price breaks above or below that range

- Confirms the signal only if the volume is above its moving average

- Displays a green square in the lower panel if the breakout is valid

- The color can be customized by the user

Confidence Score – Antirumore DAX H1How it works

Calculates 5 signal validity conditions

Assigns 1 point for each condition met

Displays a colored bar in the lower panel:

🟥 Red (0–1): noise, avoid

🟧 Orange (2–3): to be evaluated

🟩 Green (4–5): strong signal

ES Gap Trading LevelsImproved closing time handling so that the gap is based on the last bar to capture the 3:59:59 closing price.

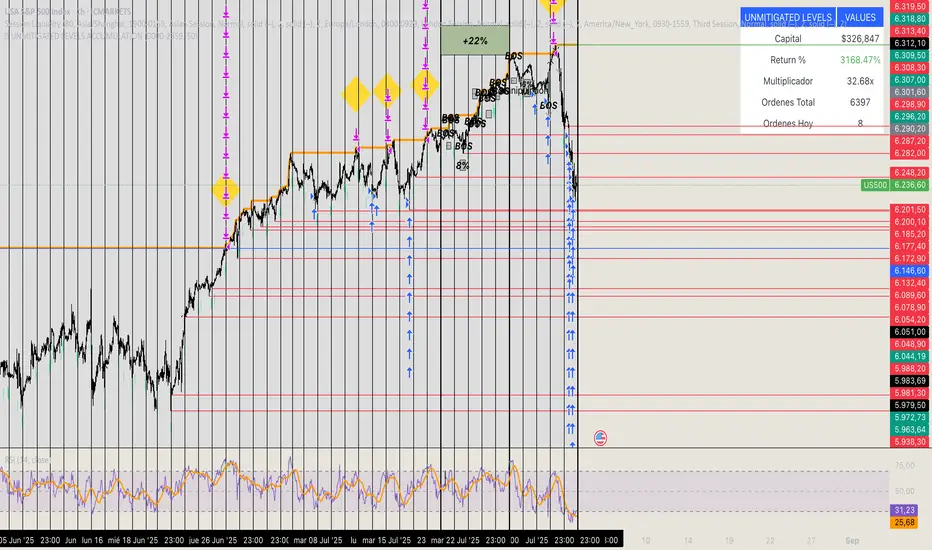

🏆 UNMITIGATED LEVELS ACCUMULATIONPDH TO ATH RISK FREE

All the PDL have a buy limit which starts at 0.1 lots which will duplicate at the same time the capital incresases. All of the buy limits have TP in ATH for max reward.

CCI Turbo Pro [CongTrader]📄 Full Description for Publishing — CCI Turbo Pro

⚡️ CCI Turbo Pro — Advanced CCI with Reversal Zones & Alerts

This advanced CCI (Commodity Channel Index) indicator is built for traders who want enhanced reversal signals, customizable extreme zones, and dynamic alerts. It improves the classic CCI with better visual cues and momentum filtering to help you avoid false signals.

🛠️ How to Use:

CCI Length (default = 20): Adjust based on your trading timeframe.

Overbought/Oversold Zones:

Overbought = 200

Oversold = -200

Extreme OB = 300 (red zone)

Extreme OS = -300 (green zone)

When the CCI crosses from below −200 → BUY signal

When the CCI crosses from above +200 → SELL signal

Background turns green/red in extreme zones

Optional labels show entry signals clearly

This indicator is useful for:

Reversal Trading

Momentum Shifts

Scalping, Swing, or Intraday strategies

Overbought/Oversold Confirmation

Works on:

Any asset (Crypto, Forex, Stocks, Indices)

Any timeframe

🔔 Alerts Included:

📈 CCI Buy Alert → CCI crossed up from oversold

📉 CCI Sell Alert → CCI crossed down from overbought

🚨 Extreme OB/OS Alert → CCI enters extreme reversal zone

Alerts help you stay informed even when away from the screen.

🔎 Keywords (for search discovery):

CCI, CCI Reversal, CCI Alert, Turbo CCI, Advanced CCI, CCI Zones, CCI Overbought, CCI Oversold, Momentum Reversal, CCI Scalping, CongTrader, CCI Buy Sell, Technical Indicator

🙏 Thank You

If this indicator adds value to your trading, please give it a 👍, leave a comment, or follow for more free tools from CongTrader. Your support helps independent creators grow the community.

⚠️ Disclaimer

This indicator is for educational purposes only and does not constitute financial advice. Use this tool with your own judgment and risk management. Past performance does not guarantee future results.

✍️ Created by CongTrader — Free, Open-Source Tools for Smarter Traders...

Z-Score Mean ReversionThe "Mean Reversion Z-Score" indicator is a statistical tool that helps traders identify potential price reversals by measuring how far the current price has deviated from its mean (average) in terms of standard deviations. Here's what it does:

Calculates the Z-score by comparing the current price to its moving average, then dividing by the standard deviation of prices over a specified period (default 14 periods).

Identifies when the price has moved too far from its mean, suggesting a potential reversion opportunity:

Values above +2 indicate overbought conditions (potential sell)

Values below -2 indicate oversold conditions (potential buy)

Generates clear visual signals:

Green triangle (▲) for buy signals when crossing above -2

Red triangle (▼) for sell signals when crossing below +2

Color-coded background for quick visual reference

Plots reference lines at ±1.5 and ±2.0 standard deviations to help gauge the strength of the current trend.

This indicator is particularly useful for range-bound markets and mean reversion trading strategies, helping traders spot potential entry and exit points based on statistical extremes.

Square-root Decay Volume ProfileThis indicator displays a custom price profile that mimics a volume profile using occurrence-based weighting rather than actual volume. It counts how often the selected price source (e.g., close) falls within each price bin over a lookback period. What makes it unique is the use of square-root time decay: more recent price occurrences are given greater importance, while older data is discounted proportionally to the inverse square root of its age.

Each bin's relative weight is visualized as a horizontal bar aligned to the right edge of the chart, showing where price has "spent time" more recently. This allows traders to identify areas of interest, balance zones, and potential support/resistance levels based on decayed price density.

Key Features:

Square-root decay weighting favors recent price action

Adjustable lookback period, bin count, and histogram width

Works with any price source (close, hl2, etc.)

Plots boxes directly on the chart for clear visualization

This tool is especially useful for discretionary traders seeking a price-centric alternative to traditional volume profiles, with an added emphasis on recency.

safa bot alertGood trading for everying and stuff that very gfood and stuff please let me puibisjertpa 9uihthsi fuckitgn code

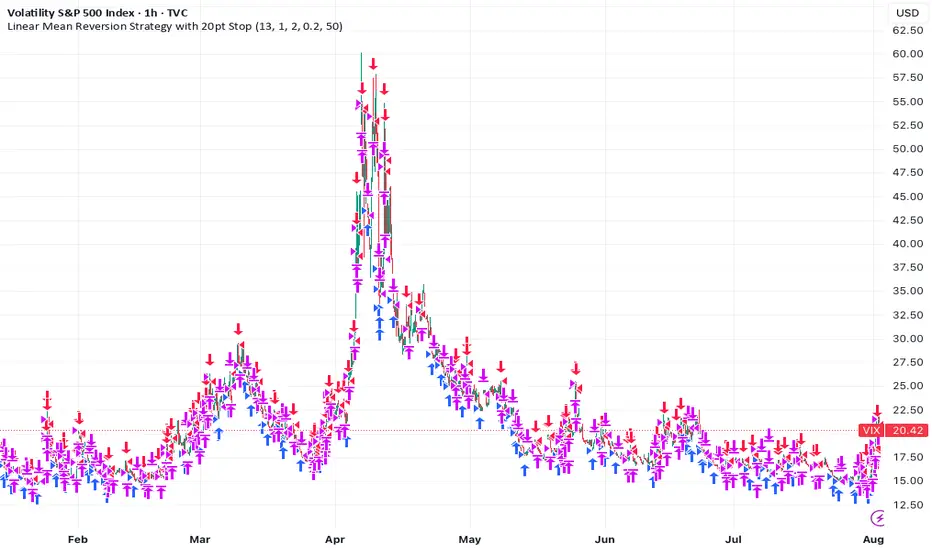

Linear Mean Reversion Strategy📘 Strategy Introduction: Linear Mean Reversion with Fixed Stop

This strategy implements a simple yet powerful mean reversion model that assumes price tends to oscillate around a dynamic average over time. It identifies statistically significant deviations from the moving average using a z-score, and enters trades expecting a return to the mean.

🧠 Core Logic:

A z-score is calculated by comparing the current price to its moving average, normalized by standard deviation, over a user-defined half-life window.

Trades are entered when the z-score crosses a threshold (e.g., ±1), signaling overbought or oversold conditions.

The strategy exits positions either when price reverts back near the mean (z-score close to 0), or if a fixed stop loss of 100 points is hit, whichever comes first.

⚙️ Key Features:

Dynamic mean and volatility estimation using moving average and standard deviation

Configurable z-score thresholds for entry and exit

Position size scaling based on z-score magnitude

Fixed stop loss to control risk and avoid prolonged drawdowns

🧪 Use Case:

Ideal for range-bound markets or assets that exhibit stationary behavior around a mean, this strategy is especially useful on assets with mean-reverting characteristics like currency pairs, ETFs, or large-cap stocks. It is best suited for traders looking for short-term reversions rather than long-term trends.

Mara JPY Strength (USDJPY+EURJPY+GBPJPY)/3 + DXYJPY, USDJPY, EURJPY, GBPJPY, smart money, bias, index, forex indicator, DXY, strength meter, professional, trading tool, price action

7* Previous Bar OHLC + 5m 20 EMAincreased label height for 7* Previous Bar OHLC + 5m 20 EMA. hope it helps :)

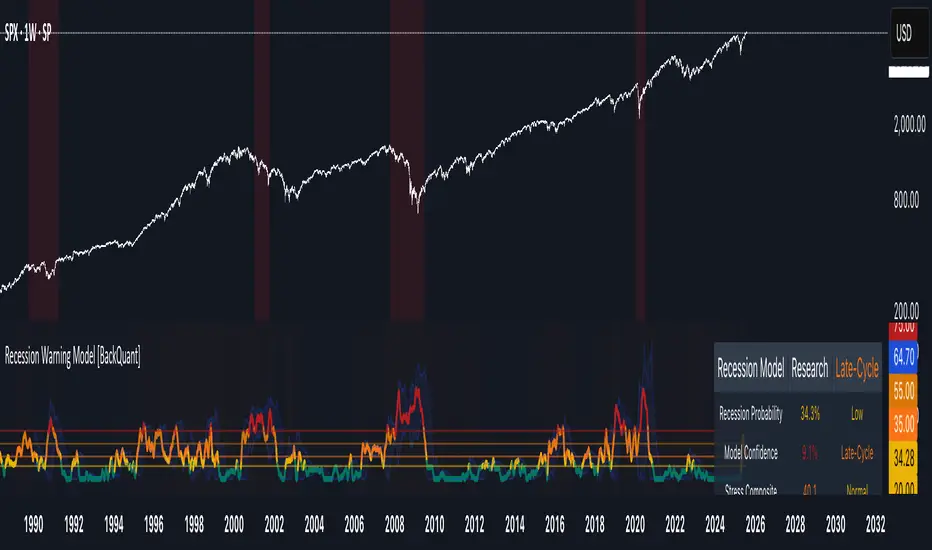

Recession Warning Model [BackQuant]Recession Warning Model

Overview

The Recession Warning Model (RWM) is a Pine Script® indicator designed to estimate the probability of an economic recession by integrating multiple macroeconomic, market sentiment, and labor market indicators. It combines over a dozen data series into a transparent, adaptive, and actionable tool for traders, portfolio managers, and researchers. The model provides customizable complexity levels, display modes, and data processing options to accommodate various analytical requirements while ensuring robustness through dynamic weighting and regime-aware adjustments.

Purpose

The RWM fulfills the need for a concise yet comprehensive tool to monitor recession risk. Unlike approaches relying on a single metric, such as yield-curve inversion, or extensive economic reports, it consolidates multiple data sources into a single probability output. The model identifies active indicators, their confidence levels, and the current economic regime, enabling users to anticipate downturns and adjust strategies accordingly.

Core Features

- Indicator Families : Incorporates 13 indicators across five categories: Yield, Labor, Sentiment, Production, and Financial Stress.

- Dynamic Weighting : Adjusts indicator weights based on recent predictive accuracy, constrained within user-defined boundaries.

- Leading and Coincident Split : Separates early-warning (leading) and confirmatory (coincident) signals, with adjustable weighting (default 60/40 mix).

- Economic Regime Sensitivity : Modulates output sensitivity based on market conditions (Expansion, Late-Cycle, Stress, Crisis), using a composite of VIX, yield-curve, financial conditions, and credit spreads.

- Display Options : Supports four modes—Probability (0-100%), Binary (four risk bins), Lead/Coincident, and Ensemble (blended probability).

- Confidence Intervals : Reflects model stability, widening during high volatility or conflicting signals.

- Alerts : Configurable thresholds (Watch, Caution, Warning, Alert) with persistence filters to minimize false signals.

- Data Export : Enables CSV output for probabilities, signals, and regimes, facilitating external analysis in Python or R.

Model Complexity Levels

Users can select from four tiers to balance simplicity and depth:

1. Essential : Focuses on three core indicators—yield-curve spread, jobless claims, and unemployment change—for minimalistic monitoring.

2. Standard : Expands to nine indicators, adding consumer confidence, PMI, VIX, S&P 500 trend, money supply vs. GDP, and the Sahm Rule.

3. Professional : Includes all 13 indicators, incorporating financial conditions, credit spreads, JOLTS vacancies, and wage growth.

4. Research : Unlocks all indicators plus experimental settings for advanced users.

Key Indicators

Below is a summary of the 13 indicators, their data sources, and economic significance:

- Yield-Curve Spread : Difference between 10-year and 3-month Treasury yields. Negative spreads signal banking sector stress.

- Jobless Claims : Four-week moving average of unemployment claims. Sustained increases indicate rising layoffs.

- Unemployment Change : Three-month change in unemployment rate. Sharp rises often precede recessions.

- Sahm Rule : Triggers when unemployment rises 0.5% above its 12-month low, a reliable recession indicator.

- Consumer Confidence : University of Michigan survey. Declines reflect household pessimism, impacting spending.

- PMI : Purchasing Managers’ Index. Values below 50 indicate manufacturing contraction.

- VIX : CBOE Volatility Index. Elevated levels suggest market anticipation of economic distress.

- S&P 500 Growth : Weekly moving average trend. Declines reduce wealth effects, curbing consumption.

- M2 + GDP Trend : Monitors money supply and real GDP. Simultaneous declines signal credit contraction.

- NFCI : Chicago Fed’s National Financial Conditions Index. Positive values indicate tighter conditions.

- Credit Spreads : Proxy for corporate bond spreads using 10-year vs. 2-year Treasury yields. Widening spreads reflect stress.

- JOLTS Vacancies : Job openings data. Significant drops precede hiring slowdowns.

- Wage Growth : Year-over-year change in average hourly earnings. Late-cycle spikes often signal economic overheating.

Data Processing

- Rate of Change (ROC) : Optionally applied to capture momentum in data series (default: 21-bar period).

- Z-Score Normalization : Standardizes indicators to a common scale (default: 252-bar lookback).

- Smoothing : Applies a short moving average to final signals (default: 5-bar period) to reduce noise.

- Binary Signals : Generated for each indicator (e.g., yield-curve inverted or PMI below 50) based on thresholds or Z-score deviations.

Probability Calculation

1. Each indicator’s binary signal is weighted according to user settings or dynamic performance.

2. Weights are normalized to sum to 100% across active indicators.

3. Leading and coincident signals are aggregated separately (if split mode is enabled) and combined using the specified mix.

4. The probability is adjusted by a regime multiplier, amplifying risk during Stress or Crisis regimes.

5. Optional smoothing ensures stable outputs.

Display and Visualization

- Probability Mode : Plots a continuous 0-100% recession probability with color gradients and confidence bands.

- Binary Mode : Categorizes risk into four levels (Minimal, Watch, Caution, Alert) for simplified dashboards.

- Lead/Coincident Mode : Displays leading and coincident probabilities separately to track signal divergence.

- Ensemble Mode : Averages traditional and split probabilities for a balanced view.

- Regime Background : Color-coded overlays (green for Expansion, orange for Late-Cycle, amber for Stress, red for Crisis).

- Analytics Table : Optional dashboard showing probability, confidence, regime, and top indicator statuses.

Practical Applications

- Asset Allocation : Adjust equity or bond exposures based on sustained probability increases.

- Risk Management : Hedge portfolios with VIX futures or options during regime shifts to Stress or Crisis.

- Sector Rotation : Shift toward defensive sectors when coincident signals rise above 50%.

- Trading Filters : Disable short-term strategies during high-risk regimes.

- Event Timing : Scale positions ahead of high-impact data releases when probability and VIX are elevated.

Configuration Guidelines

- Enable ROC and Z-score for consistent indicator comparison unless raw data is preferred.

- Use dynamic weighting with at least one economic cycle of data for optimal performance.

- Monitor stress composite scores above 80 alongside probabilities above 70 for critical risk signals.

- Adjust adaptation speed (default: 0.1) to 0.2 during Crisis regimes for faster indicator prioritization.

- Combine RWM with complementary tools (e.g., liquidity metrics) for intraday or short-term trading.

Limitations

- Macro indicators lag intraday market moves, making RWM better suited for strategic rather than tactical trading.

- Historical data availability may constrain dynamic weighting on shorter timeframes.

- Model accuracy depends on the quality and timeliness of economic data feeds.

Final Note

The Recession Warning Model provides a disciplined framework for monitoring economic downturn risks. By integrating diverse indicators with transparent weighting and regime-aware adjustments, it empowers users to make informed decisions in portfolio management, risk hedging, or macroeconomic research. Regular review of model outputs alongside market-specific tools ensures its effective application across varying market conditions.