HarmonicMapLibLibrary "HarmonicMapLib"

Harmonic Pattern Library implementation utilising maps

method tostring(this)

convert Range value to string

Namespace types: Range

Parameters:

this (Range) : Range value

Returns: converted string representation

method tostring(this)

convert array of Range value to string

Namespace types: array

Parameters:

this (array) : array object

Returns: converted string representation

method tostring(this)

convert map of string to Range value to string

Namespace types: map

Parameters:

this (map) : map object

Returns: converted string representation

method tostring(this)

convert RatioMap to string

Namespace types: RatioMap

Parameters:

this (RatioMap) : RatioMap object

Returns: converted string representation

method tostring(this)

convert array of RatioMap to string

Namespace types: array

Parameters:

this (array) : array object

Returns: converted string representation

method tostring(this)

convert map of string to RatioMap to string

Namespace types: map

Parameters:

this (map) : map object

Returns: converted string representation

method tostring(this)

convert map of string to bool to string

Namespace types: map

Parameters:

this (map) : map object

Returns: converted string representation

method tostring(this)

convert PrzRange to string

Namespace types: PrzRange

Parameters:

this (PrzRange) : PrzRange object

Returns: converted string representation

method tostring(this)

convert array of PrzRange to string

Namespace types: array

Parameters:

this (array) : array object

Returns: converted string representation

getHarmonicMap()

Creates the RatioMap for harmonic patterns

Returns: map haronic ratio rules for all patterns

method evaluate(patternsMap, pattern, ratioRange, properties, ratioValue)

evaluates harmonic ratio range

Namespace types: map

Parameters:

patternsMap (map) : parameter containing valid pattern names

pattern (string) : Pattern type to be evaluated

ratioRange (Range) : ratio range to be checked

properties (ScanProperties) : Scan Properties

ratioValue (float)

Returns: void

method evaluate(przRange, pattern, ratioRange, priceRange, properties)

Evaluate PRZ ranges

Namespace types: map

Parameters:

przRange (map)

pattern (string) : Pattern name

ratioRange (Range) : Range of ratio for the pattern

priceRange (Range) : Price range based on ratio

properties (ScanProperties) : ScanProperties object

Returns: void

method scanRatio(currentPatterns, rules, properties, ratioName, ratioValue)

Scan for particular named ratio of harmonic pattern to filter valid patterns

Namespace types: map

Parameters:

currentPatterns (map) : Current valid patterns map

rules (map) : map Harmonic ratio rules

properties (ScanProperties) : ScanProperties object

ratioName (string) : Specific ratio name

ratioValue (float) : ratio value to be checked

Returns: updated currentPatterns object

method scanPatterns(patterns, x, a, b, c, d, properties)

Scan for patterns based on X, A, B, C, D values

Namespace types: map

Parameters:

patterns (map) : List of allowed patterns

x (float) : X coordinate

a (float) : A coordinate

b (float) : B coordinate

c (float) : C coordinate

d (float) : D coordinate

properties (ScanProperties) : ScanProperties object. If na, default values are initialised

Returns: updated valid patterns map

method scanProjections(patterns, x, a, b, c, properties)

Scan for projections based on X, A, B, C values

Namespace types: map

Parameters:

patterns (map) : List of allowed patterns

x (float) : X coordinate

a (float) : A coordinate

b (float) : B coordinate

c (float) : C coordinate

properties (ScanProperties) : ScanProperties object. If na, default values are initialised

Returns: updated valid projections map

method merge(this, other)

merge two ranges into one

Namespace types: Range

Parameters:

this (Range) : first range

other (Range) : second range

Returns: combined range

method union(this, other)

union of two ranges into one

Namespace types: Range

Parameters:

this (Range) : first range

other (Range) : second range

Returns: union range

method overlaps(this, other)

checks if two ranges intersect

Namespace types: Range

Parameters:

this (Range) : first range

other (Range) : second range

Returns: true if intersects, false otherwise

method consolidate(this)

Consolidate ranges into PRZ

Namespace types: map

Parameters:

this (map) : map of Ranges

Returns: consolidated PRZ

method consolidateMany(this)

Consolidate ranges into multiple PRZ ranges

Namespace types: map

Parameters:

this (map) : map of Ranges

Returns: consolidated array of PRZ ranges

method getRange(currentPatterns, x, a, b, c, properties)

Get D range based on X, A, B, C coordinates for the current patterns

Namespace types: map

Parameters:

currentPatterns (map) : List of valid patterns

x (float) : X coordinate

a (float) : A coordinate

b (float) : B coordinate

c (float) : C coordinate

properties (ScanProperties) : ScanProperties object. If na, default values are initialised

Returns: map of D ranges

method getPrzRange(currentPatterns, x, a, b, c, properties)

Get PRZ range based on X, A, B, C coordinates for the current patterns

Namespace types: map

Parameters:

currentPatterns (map) : List of valid patterns

x (float) : X coordinate

a (float) : A coordinate

b (float) : B coordinate

c (float) : C coordinate

properties (ScanProperties) : ScanProperties object. If na, default values are initialised

Returns: PRZRange for the pattern

method getProjectionRanges(currentPatterns, x, a, b, c, properties)

Get projection range based on X, A, B, C coordinates for the current patterns

Namespace types: map

Parameters:

currentPatterns (map) : List of valid patterns

x (float) : X coordinate

a (float) : A coordinate

b (float) : B coordinate

c (float) : C coordinate

properties (ScanProperties) : ScanProperties object. If na, default values are initialised

Returns: array of projection ranges

Range

Collection of range values

Fields:

values (array) : array of float values

RatioMap

ratio map for pattern

Fields:

ratioMap (map) : map of string to Range (array of float)

ScanProperties

Pattern Scanning properties

Fields:

strictMode (series bool) : strict scanning mode will check for overflows

logScale (series bool) : scan ratios in log scale

errorMin (series float) : min error threshold

errorMax (series float)

mintick (series float) : minimum tick value of price

PrzRange

Potential reversal zone range

Fields:

patterns (array) : array of pattern names for the given XABCD combination

prz (Range) : PRZ range

Statistics

Intrinsic Event (Multi DC OS)Overview

This indicator implements an event-based approach to analyze price movements in the foreign exchange market, inspired by the intrinsic time framework introduced in Fractals and Intrinsic Time - A Challenge to Econometricians by U. A. Müller et al. (1995). It identifies significant price events using an intrinsic time perspective and supports multi-agent analysis to reflect the heterogeneous nature of financial markets. The script plots these events as lines and labels on the chart, offering a visual tool for traders to understand market dynamics at different scales.

Key Features

Intrinsic Events : The indicator detects directional change (DC) and overshoot (OS) events based on user-defined thresholds (delta), aligning with the paper’s concept of intrinsic time (Section 6). Intrinsic time redefines time based on market activity, expanding during volatile periods and contracting during inactive ones, rather than relying on a physical clock.

Multi-Agent Analysis : Supports up to five agents, each with its own threshold and color settings, reflecting the heterogeneous market hypothesis (Section 5). This allows the indicator to capture the perspectives of market participants with different time horizons, such as short-term FX dealers and long-term central banks.

How It Works

Intrinsic Events Detection : The script identifies two types of events using intrinsic time principles:

Directional Change (DC) : Triggered when the price reverses by the threshold (delta) against the current trend (e.g., a drop by delta in an uptrend signals a "Down DC").

Overshoot (OS) : Occurs when the price continues in the trend direction by the threshold (e.g., a rise by delta in an uptrend signals an "Up OS").

DC events are plotted as solid lines, and OS events as dashed lines, with labels like "Up DC" or "OS Down" for clarity. The label style adjusts based on the trend to ensure visibility.

Multi-Agent Setup : Each agent operates independently with its own threshold, mimicking market participants with varying time horizons (Section 5). Smaller thresholds detect frequent, short-term events, while larger thresholds capture broader, long-term movements.

Settings

Each agent can be configured with:

Enable Agent : Toggle the agent on or off.

Threshold (%) : The percentage threshold (delta) for detecting DC and OS events (default values: 0.1%, 0.2%, 0.5%, 1%, 2% for agents 1–5).

Up Mode Color : Color for lines and labels in up mode (DC events).

Down Mode Color : Color for lines and labels in down mode (OS events).

Usage Notes

This indicator is designed for the foreign exchange market, leveraging its high liquidity, as noted in the paper (Section 1). Adjust the threshold values based on the instrument’s volatility—higher volatility leads to more intrinsic events (Section 4). It can be adapted to other markets where event-based analysis applies.

Reference

The methodology is based on:

Fractals and Intrinsic Time - A Challenge to Econometricians by U. A. Müller, M. M. Dacorogna, R. D. Davé, O. V. Pictet, R. B. Olsen, and J. R. Ward (June 28, 1995). Olsen & Associates Preprint.

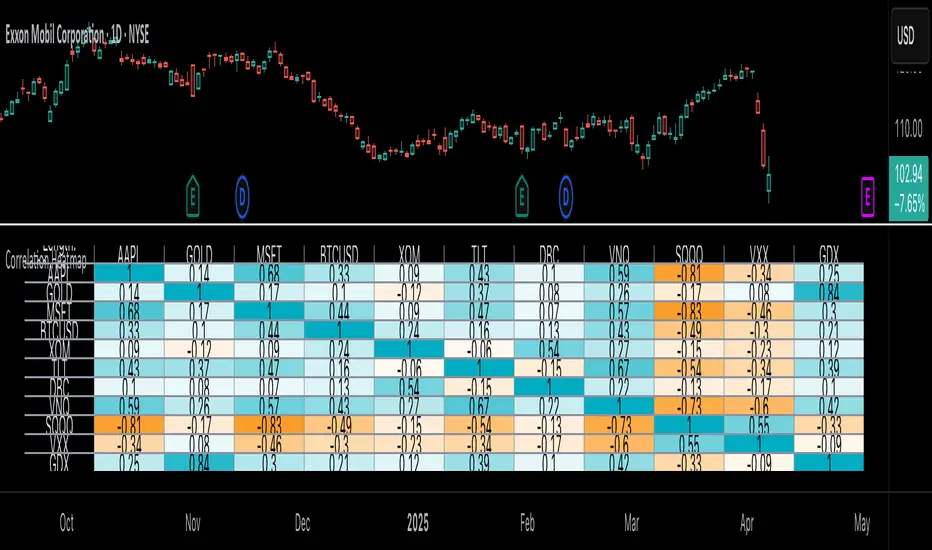

Correlation Heatmap█ OVERVIEW

This indicator creates a correlation matrix for a user-specified list of symbols based on their time-aligned weekly or monthly price returns. It calculates the Pearson correlation coefficient for each possible symbol pair, and it displays the results in a symmetric table with heatmap-colored cells. This format provides an intuitive view of the linear relationships between various symbols' price movements over a specific time range.

█ CONCEPTS

Correlation

Correlation typically refers to an observable statistical relationship between two datasets. In a financial time series context, it usually represents the extent to which sampled values from a pair of datasets, such as two series of price returns, vary jointly over time. More specifically, in this context, correlation describes the strength and direction of the relationship between the samples from both series.

If two separate time series tend to rise and fall together proportionally, they might be highly correlated. Likewise, if the series often vary in opposite directions, they might have a strong anticorrelation . If the two series do not exhibit a clear relationship, they might be uncorrelated .

Traders frequently analyze asset correlations to help optimize portfolios, assess market behaviors, identify potential risks, and support trading decisions. For instance, correlation often plays a key role in diversification . When two instruments exhibit a strong correlation in their returns, it might indicate that buying or selling both carries elevated unsystematic risk . Therefore, traders often aim to create balanced portfolios of relatively uncorrelated or anticorrelated assets to help promote investment diversity and potentially offset some of the risks.

When using correlation analysis to support investment decisions, it is crucial to understand the following caveats:

• Correlation does not imply causation . Two assets might vary jointly over an analyzed range, resulting in high correlation or anticorrelation in their returns, but that does not indicate that either instrument directly influences the other. Joint variability between assets might occur because of shared sensitivities to external factors, such as interest rates or global sentiment, or it might be entirely coincidental. In other words, correlation does not provide sufficient information to identify cause-and-effect relationships.

• Correlation does not predict the future relationship between two assets. It only reflects the estimated strength and direction of the relationship between the current analyzed samples. Financial time series are ever-changing. A strong trend between two assets can weaken or reverse in the future.

Correlation coefficient

A correlation coefficient is a numeric measure of correlation. Several coefficients exist, each quantifying different types of relationships between two datasets. The most common and widely known measure is the Pearson product-moment correlation coefficient , also known as the Pearson correlation coefficient or Pearson's r . Usually, when the term "correlation coefficient" is used without context, it refers to this correlation measure.

The Pearson correlation coefficient quantifies the strength and direction of the linear relationship between two variables. In other words, it indicates how consistently variables' values move together or in opposite directions in a proportional, linear manner. Its formula is as follows:

𝑟(𝑥, 𝑦) = cov(𝑥, 𝑦) / (𝜎𝑥 * 𝜎𝑦)

Where:

• 𝑥 is the first variable, and 𝑦 is the second variable.

• cov(𝑥, 𝑦) is the covariance between 𝑥 and 𝑦.

• 𝜎𝑥 is the standard deviation of 𝑥.

• 𝜎𝑦 is the standard deviation of 𝑦.

In essence, the correlation coefficient measures the covariance between two variables, normalized by the product of their standard deviations. The coefficient's value ranges from -1 to 1, allowing a more straightforward interpretation of the relationship between two datasets than what covariance alone provides:

• A value of 1 indicates a perfect positive correlation over the analyzed sample. As one variable's value changes, the other variable's value changes proportionally in the same direction .

• A value of -1 indicates a perfect negative correlation (anticorrelation). As one variable's value increases, the other variable's value decreases proportionally.

• A value of 0 indicates no linear relationship between the variables over the analyzed sample.

Aligning returns across instruments

In a financial time series, each data point (i.e., bar) in a sample represents information collected in periodic intervals. For instance, on a "1D" chart, bars form at specific times as successive days elapse.

However, the times of the data points for a symbol's standard dataset depend on its active sessions , and sessions vary across instrument types. For example, the daily session for NYSE stocks is 09:30 - 16:00 UTC-4/-5 on weekdays, Forex instruments have 24-hour sessions that span from 17:00 UTC-4/-5 on one weekday to 17:00 on the next, and new daily sessions for cryptocurrencies start at 00:00 UTC every day because crypto markets are consistently open.

Therefore, comparing the standard datasets for different asset types to identify correlations presents a challenge. If two symbols' datasets have bars that form at unaligned times, their correlation coefficient does not accurately describe their relationship. When calculating correlations between the returns for two assets, both datasets must maintain consistent time alignment in their values and cover identical ranges for meaningful results.

To address the issue of time alignment across instruments, this indicator requests confirmed weekly or monthly data from spread tickers constructed from the chart's ticker and another specified ticker. The datasets for spreads are derived from lower-timeframe data to ensure the values from all symbols come from aligned points in time, allowing a fair comparison between different instrument types. Additionally, each spread ticker ID includes necessary modifiers, such as extended hours and adjustments.

In this indicator, we use the following process to retrieve time-aligned returns for correlation calculations:

1. Request the current and previous prices from a spread representing the sum of the chart symbol and another symbol ( "chartSymbol + anotherSymbol" ).

2. Request the prices from another spread representing the difference between the two symbols ( "chartSymbol - anotherSymbol" ).

3. Calculate half of the difference between the values from both spreads ( 0.5 * (requestedSum - requestedDifference) ). The results represent the symbol's prices at times aligned with the sample points on the current chart.

4. Calculate the arithmetic return of the retrieved prices: (currentPrice - previousPrice) / previousPrice

5. Repeat steps 1-4 for each symbol requiring analysis.

It's crucial to note that because this process retrieves prices for a symbol at times consistent with periodic points on the current chart, the values can represent prices from before or after the closing time of the symbol's usual session.

Additionally, note that the maximum number of weeks or months in the correlation calculations depends on the chart's range and the largest time range common to all the requested symbols. To maximize the amount of data available for the calculations, we recommend setting the chart to use a daily or higher timeframe and specifying a chart symbol that covers a sufficient time range for your needs.

█ FEATURES

This indicator analyzes the correlations between several pairs of user-specified symbols to provide a structured, intuitive view of the relationships in their returns. Below are the indicator's key features:

Requesting a list of securities

The "Symbol list" text box in the indicator's "Settings/Inputs" tab accepts a comma-separated list of symbols or ticker identifiers with optional spaces (e.g., "XOM, MSFT, BITSTAMP:BTCUSD"). The indicator dynamically requests returns for each symbol in the list, then calculates the correlation between each pair of return series for its heatmap display.

Each item in the list must represent a valid symbol or ticker ID. If the list includes an invalid symbol, the script raises a runtime error.

To specify a broker/exchange for a symbol, include its name as a prefix with a colon in the "EXCHANGE:SYMBOL" format. If a symbol in the list does not specify an exchange prefix, the indicator selects the most commonly used exchange when requesting the data.

Note that the number of symbols allowed in the list depends on the user's plan. Users with non-professional plans can compare up to 20 symbols with this indicator, and users with professional plans can compare up to 32 symbols.

Timeframe and data length selection

The "Returns timeframe" input specifies whether the indicator uses weekly or monthly returns in its calculations. By default, its value is "1M", meaning the indicator analyzes monthly returns. Note that this script requires a chart timeframe lower than or equal to "1M". If the chart uses a higher timeframe, it causes a runtime error.

To customize the length of the data used in the correlation calculations, use the "Max periods" input. When enabled, the indicator limits the calculation window to the number of periods specified in the input field. Otherwise, it uses the chart's time range as the limit. The top-left corner of the table shows the number of confirmed weeks or months used in the calculations.

It's important to note that the number of confirmed periods in the correlation calculations is limited to the largest time range common to all the requested datasets, because a meaningful correlation matrix requires analyzing each symbol's returns under the same market conditions. Therefore, the correlation matrix can show different results for the same symbol pair if another listed symbol restricts the aligned data to a shorter time range.

Heatmap display

This indicator displays the correlations for each symbol pair in a heatmap-styled table representing a symmetric correlation matrix. Each row and column corresponds to a specific symbol, and the cells at their intersections correspond to symbol pairs . For example, the cell at the "AAPL" row and "MSFT" column shows the weekly or monthly correlation between those two symbols' returns. Likewise, the cell at the "MSFT" row and "AAPL" column shows the same value.

Note that the main diagonal cells in the display, where the row and column refer to the same symbol, all show a value of 1 because any series of non-na data is always perfectly correlated with itself.

The background of each correlation cell uses a gradient color based on the correlation value. By default, the gradient uses blue hues for positive correlation, orange hues for negative correlation, and white for no correlation. The intensity of each blue or orange hue corresponds to the strength of the measured correlation or anticorrelation. Users can customize the gradient's base colors using the inputs in the "Color gradient" section of the "Settings/Inputs" tab.

█ FOR Pine Script® CODERS

• This script uses the `getArrayFromString()` function from our ValueAtTime library to process the input list of symbols. The function splits the "string" value by its commas, then constructs an array of non-empty strings without leading or trailing whitespaces. Additionally, it uses the str.upper() function to convert each symbol's characters to uppercase.

• The script's `getAlignedReturns()` function requests time-aligned prices with two request.security() calls that use spread tickers based on the chart's symbol and another symbol. Then, it calculates the arithmetic return using the `changePercent()` function from the ta library. The `collectReturns()` function uses `getAlignedReturns()` within a loop and stores the data from each call within a matrix . The script calls the `arrayCorrelation()` function on pairs of rows from the returned matrix to calculate the correlation values.

• For consistency, the `getAlignedReturns()` function includes extended hours and dividend adjustment modifiers in its data requests. Additionally, it includes other settings inherited from the chart's context, such as "settlement-as-close" preferences.

• A Pine script can execute up to 40 or 64 unique `request.*()` function calls, depending on the user's plan. The maximum number of symbols this script compares is half the plan's limit, because `getAlignedReturns()` uses two request.security() calls.

• This script can use the request.security() function within a loop because all scripts in Pine v6 enable dynamic requests by default. Refer to the Dynamic requests section of the Other timeframes and data page to learn more about this feature, and see our v6 migration guide to learn what's new in Pine v6.

• The script's table uses two distinct color.from_gradient() calls in a switch structure to determine the cell colors for positive and negative correlation values. One call calculates the color for values from -1 to 0 based on the first and second input colors, and the other calculates the colors for values from 0 to 1 based on the second and third input colors.

Look first. Then leap.

Timed Reversion Markers (Custom Session Alerts)This script plots vertical histogram markers at specific intraday time points defined by the user. It is designed for traders who follow time-based reversion or breakout setups tied to predictable market behavior at key clock times, such as institutional opening moves, midday reversals, or end-of-day volatility.

Unlike traditional price-action indicators, this tool focuses purely on time-based triggers, a technique often used in time cycle analysis, market internals, and volume-timing strategies.

The indicator includes eight fully customizable time inputs, allowing users to mark any intraday minute with precision using a decimal hour format (for example, 9.55 for 9:55 AM). Each input is automatically converted into hour and minute format, and a visual histogram marker is plotted once per day at that exact time.

Example use cases:

Mark institutional session opens (e.g., 9:30, 10:00, 15:30)

Time-based mean reversion or volatility windows

Backtest recurring time-based reactions

Highlight algorithmic spike zones

The vertical plots serve as non-intrusive, high-contrast visual markers for scalping setups, session analysis, and decision-making checkpoints. All markers are displayed at the top of the chart without interfering with price candles.

Statistical OHLC Projections [neo|]█ OVERVIEW

Statistical OHLC Projections is an indicator designed to offer users a customizable deep-dive on measuring historical price levels for any timeframe. The indicator separates price into two distinct levels, "Manipulation" and "Distribution", where the idea is that for higher timeframe candles, e.g. an up-close candle, the distance from the open to the bottom of the wick would constitute the Manipulation, and the rest would be considered the Distribution. By measuring out these levels, we can gain insight on how far the market may move from higher timeframe opens to their manipulations and distributions, and apply this knowledge to our analysis.

IMPORTANT: Since levels are based on the lookback available on your chart, if the levels aren't being displayed this likely means you don't have enough lookback for your selected timeframe. To check this, enable the stat table to see how many values are available for your timeframe, and either reduce the lookback or increase your chart timeframe.

█ CONCEPTS

The core concept revolves around understanding market behavior through the lens of historical candle structure. The indicator dissects OHLC data to provide statistical boundaries of expected price movement.

- Manipulation Levels: These represent the areas typically seen as liquidity grabs or false moves where price extends in one direction before reversing.

- Distribution Levels: These highlight where the bulk of directional movement tends to occur, often following the manipulation move.

The tool aggregates this data across your selected timeframe to inform you of potential levels associated with it.

█ FEATURES

Multiple Display Types: Display statistical data through two sleek styles, areas or lines. Where areas represent the area between two customizable lookback values, and lines represent one average value.

Adjustable Timeframe Selection: Whether you want to see data based on the 1D chart, or the 1W chart, anything is possible. Simply change the timeframe on the dropdown menu and if there is sufficient lookback the indicator will adjust to your requested timeframe.

Customizable Historical Lookback: By default, the indicator will measure the average 60 values of your requested timeframe, however this may be adjusted to be higher or lower based on your preference. If you want to measure recent moves, 10-20 lookback may be better for you, or if you want more data for less volatile instruments, a value of 100 may be better.

Historical Display: Prevent historical levels from being removed by unchecking the "Remove Previous Drawings" option, this will allow you to examine how the levels previously interacted with price.

NY Midnight Anchoring: By checking the "Use NY Midnight" option, you may see the projection anchored to the New York midnight open time, which is often a significant level on indices.

Alerts: You may enable alerts for any of the indicator's provided levels to stay informed, even when off the charts.

█ How to use

To use the indicator, simply apply it to your chart and modify any of your desired inputs.

By default, the indicator will provide levels for the "1D" timeframe, with a desired lookback of 60, on most instruments and plans this can be gotten when you are on the 30 minute timeframe or above.

When price reaches or extends beyond a manipulation level, observe how it reacts and whether it rejects from that level, if it does this may be an indication that the candle for the timeframe you selected may be reversing.

█ SETTINGS AND OPTIONS

Customize the indicator’s behavior, timeframe sources, and visual appearance to fit your analysis style. Each setting has been designed with flexibility in mind, whether you're working on lower or higher timeframes.

Display Mode: Switch between different display styles for levels: - Default: Shows all statistical levels as individual lines.

- Areas: Plots filled zones between two customizable lookbacks to represent the range between them.

This is ideal for visually mapping high-probability zones of price activity.

Timeframe Settings:

- Show First/Second Timeframe: Choose to show one or both timeframe projections simultaneously.

- First Timeframe / Second Timeframe: Define the higher timeframe candle you want to base calculations on (e.g., 1D, 1W).

- Use NY Midnight: When enabled and using the daily timeframe, the levels will be anchored to the New York Midnight Open (00:00 EST), a key institutional timing reference, especially useful for indices and forex.

Calculation Settings:

- Main Lookback Period: The number of historical candles used in the statistical calculations. A lower number focuses on recent price action, while a higher number smooths results across broader history.

- First Lookback / Second Lookback: Used when “Areas” mode is selected to define the range of the shaded zone. For example, an area from 20 to 60 candles creates a band between short- and long-term price behavior averages.

Visual Settings:

- Line Style: Set your preferred visual style: Solid, Dashed, or Dotted.

- Remove Previous Drawings: When enabled, only the most recent projection is shown on the chart. Disable to retain previous levels and visually backtest their reactions over time.

Color Settings:

Customize each level independently to match your chart theme:

- Manipulation High/Low

- Distribution High/Low

- Open Level

- Label Text Color

Premium/Discount Zones:

- Enable Premium/Discount Zones: Overlay price zones above and below equilibrium to visualize potential overbought (premium) and oversold (discount) areas.

- Premium/Discount Colors: Fully customizable zone colors for clarity and emphasis.

Table Settings:

- Show Statistics Table: Adds an on-chart table summarizing key levels from your active timeframe(s).

- Table Cell Color: Set the background color of the table cells for visibility.

- Table Position: Choose from preset chart locations to position the table where it works best for your layout.

Alerts:

Stay on top of price interactions with key levels even when you're away from the charts.

- Manipulation Hits (High)

- Manipulation Hits (Low)

- Distribution Hits (High)

- Distribution Hits (Low)

TrendLibrary "Trend"

calculateSlopeTrend(source, length, thresholdMultiplier)

Parameters:

source (float)

length (int)

thresholdMultiplier (float)

Purpose:

The primary goal of this function is to determine the short-term trend direction of a given data series (like closing prices). It does this by calculating the slope of the data over a specified period and then comparing that slope against a dynamic threshold based on the data's recent volatility. It classifies the trend into one of three states: Upward, Downward, or Flat.

Parameters:

`source` (Type: `series float`): This is the input data series you want to analyze. It expects a series of floating-point numbers, typically price data like `close`, `open`, `hl2` (high+low)/2, etc.

`length` (Type: `int`): This integer defines the lookback period. The function will analyze the `source` data over the last `length` bars to calculate the slope and standard deviation.

`thresholdMultiplier` (Type: `float`, Default: `0.1`): This is a sensitivity factor. It's multiplied by the standard deviation to determine how steep the slope needs to be before it's considered a true upward or downward trend. A smaller value makes it more sensitive (detects trends earlier, potentially more false signals), while a larger value makes it less sensitive (requires a stronger move to confirm a trend).

Calculation Steps:

Linear Regression: It first calculates the value of a linear regression line fitted to the `source` data over the specified `length` (`ta.linreg(source, length, 0)`). Linear regression finds the "best fit" straight line through the data points.

Slope Calculation: It then determines the slope of this linear regression line. Since `ta.linreg` gives the *value* of the line on the current bar, the slope is calculated as the difference between the current bar's linear regression value (`linRegValue`) and the previous bar's value (`linRegValue `). A positive difference means an upward slope, negative means downward.

Volatility Measurement: It calculates the standard deviation (`ta.stdev(source, length)`) of the `source` data over the same `length`. Standard deviation is a measure of how spread out the data is, essentially quantifying its recent volatility.

Adaptive Threshold: An adaptive threshold (`threshold`) is calculated by multiplying the standard deviation (`stdDev`) by the `thresholdMultiplier`. This is crucial because it means the definition of a "flat" trend adapts to the market's volatility. In volatile times, the threshold will be wider, requiring a larger slope to signal a trend. In quiet times, the threshold will be narrower.

Trend Determination: Finally, it compares the calculated `slope` to the adaptive `threshold`:

If the `slope` is greater than the positive `threshold`, the trend is considered **Upward**, and the function returns `1`.

If the `slope` is less than the negative `threshold` (`-threshold`), the trend is considered **Downward**, and the function returns `-1`.

If the `slope` falls between `-threshold` and `+threshold` (inclusive of 0), the trend is considered **Flat**, and the function returns `0`.

Return Value:

The function returns an integer representing the determined trend direction:

`1`: Upward trend

`-1`: Downward trend

`0`: Flat trend

In essence, this library function provides a way to gauge trend direction using linear regression, but with a smart filter (the adaptive threshold) to avoid classifying minor noise or low-volatility periods as significant trends.

Chonky ATR Levels 2.0Show ATR based high/low projections.

Choose a custom ATR calculation in the indicator's settings.

The default is a 20day RMA based ATR.

----------How projections are calculated----------

To project the ATR High, the ATR value is added to the low of the current candle that matches the ATR's timeframe.

To project the ATR Low, the ATR value is subtracted from the high of the current candle that matches the ATR's timeframe.

Example:

If a 20day RMA ATR is used:

- the ATR High will be the current day's low + the ATR value.

- the ATR Low will be the current day's high - the ATR value.

*However*, if the price action exceeds either ATR projection, the opposite ATR level will be fixed to the extreme of the period.

See the AUDUSD screenshot above for an example.

The ATR Low was exceeded, so the ATR High projection is capped at the high of day.

If the ATR High is exceeded, the ATR Low would be capped at the low of day.

Metatrader CalculatorThe “ Metatrader Calculator ” indicator calculates the position size, risk, and potential gain of a trade, taking into account the account balance, risk percentage, entry price, stop loss price, and risk/reward ratio. It supports the XAUUSD, XAGUSD, and BTCUSD pairs, automatically calculating the position size (in lots) based on these parameters. The calculation is displayed in a table on the chart, showing the lot size, loss in dollars, and potential gain based on the defined risk.

CME Price LimitCalculates the CME Price Limit

The reference price is obtained from the previous day's closing settlement price

(data pulled from the asset's daily chart with settlement enabled)

Percentage limit can be modified in settings

Buffer can be enabled (for example, 2% buffer on a 7% limit, so a line gets drawn at 5% too)

Alert can be enabled for price crossing a certain percentage from reference on the day

You can choose to plot the historical lines on every day, or the current day only

The reference price output can be found in the data window, or in the indicator status line if enabled in the settings.

Before placing real trades with this, you should compare the indicator's reference price to what's shown on CME's website, to double check that TradingView's data matches for your contract.

www.cmegroup.com

VNIndex Over 6.5% Downside Drop Indicator with TableOverview: The VNIndex 6.5% Downside Drop Indicator is a powerful tool designed to help traders and investors identify significant market drops on the VNIndex (or any other asset) based on a 6.5% downside threshold. This Pine Script® indicator automatically detects when the price of an asset drops by more than 6.5% within a single day, and visually marks those events on the chart.

Key Features:

6.5% Downside Drop Detection: Automatically calculates the daily percentage drop and identifies when the price falls by more than 6.5%.

Table Display: Displays the dates and corresponding percentage drops of all identified instances in a convenient table at the bottom right of the chart.

Markers: Red down-pointing markers are plotted above bars where the price drop exceeds the 6.5% threshold, making it easy to spot critical drop events at a glance.

Easy-to-Read Table: The table lists the date and drop percentage, updating dynamically as new drops are detected. This allows for easy tracking of significant downside moves over time.

How to Use:

Install the Script: Add this indicator to your TradingView chart.

Monitor Price Drops: The indicator will automatically detect when the price drops by over 6.5% from the previous close and display a marker on the chart and the table in the bottom right corner.

View the Table: The table displays the date and the percentage drop of each detected event, making it easy to track past significant moves.

Alerts: You can set an alert for 6.5% drops to receive notifications in real-time.

Customization Options:

The drop percentage threshold (6.5%) can be adjusted in the script to fit other market conditions or assets.

The table can be resized or styled based on user preference for better visibility.

Why Use This Indicator? This indicator is perfect for traders looking to spot large, significant price movements quickly. Large downside drops can signal potential market reversals or trading opportunities, and this tool helps you track such events effortlessly. Whether you're monitoring the VNIndex or any other asset, this indicator provides crucial insights into volatile price action, helping you make more informed decisions.

Open Source License: This indicator is open source and free to use under the Mozilla Public License 2.0. You are welcome to modify, distribute, and contribute to the project.

Contributions: Feel free to contribute improvements, fixes, or new features by creating a pull request. Let’s collaborate to make this indicator even better for the community!

Manual Trade Ledger# Manual Options Trade Journal – Pine Script

This project is a Pine Script implementation for TradingView that allows users to manually log options trades into a live table overlay on a chart.

## ✨ Features

- 📥 Manual entry of ticker, premium, contracts, strike, expiry, notes

- 📈 Auto-filled live data: timestamp, price, and % change since first log

- 🧾 Tabular logging for trade journaling and exporting to Google Sheets

- 🔧 Fully customizable and designed to support product experimentation

## 🎯 Use Case

This project was built to support a real-world trading workflow for options traders who:

- Prefer to manually log trades while watching charts

- Want a visual, copyable ledger that evolves in real-time

- Want to later analyze entries/exits in spreadsheets or dashboards

## 🛠 How It Works

1. Toggle the `Log Trade` switch inside TradingView’s indicator settings

2. Fill in your trade metadata (ticker, premium, etc.)

3. The script captures timestamp, price, and calculates % change

4. Each new trade adds a row to the table (up to 50 max)

Zig Zag Trend Metrics“ Zig Zag Trend Metrics ” is a highly versatile indicator, built on the classic Zig Zag concept and thoughtfully designed for technical traders seeking a deeper, more structured view of market dynamics. This tool identifies significant swing highs and lows, classifies them, and annotates each with key metrics, offering a precise snapshot of each movement. It enhances visual analysis by drawing connecting lines that outline the flow of market structure, making trend progression and reversals instantly recognizable. Beyond visual mapping, it features a compact, real-time statistics table that calculates the average price and time deltas for both bullish and bearish swings, giving traders deep insights into trend momentum and rhythm. With extensive customization options, this indicator adapts seamlessly to vast trading styles or chart setups, empowering traders to spot patterns, evaluate trend strength, and make more confident, data-backed decisions.

❖ FEATURES

✦ Automatic Swing Detection

At its core, this indicator automatically identifies swing highs and lows based on a customizable lookback period (default: 10 bars).

✦ Labeling Swing Points

Each swing is visualized with a label that includes:

Swing Classification : “HH” (Higher High), “LH” (Lower High), “LL” (Lower Low), or “HL” (Higher Low).

Price Difference : Displayed in percentage or absolute value from the previous opposite swing.

Time Difference : The number of bars since the previous swing of the opposite type.

These labels offer traders clear, immediate insight into price movements and structural changes.

✦ Visual Lines

The indicator draws three types of lines:

Bullish Lines: Connect recent swing lows to new swing highs, indicating uptrends.

Bearish Lines: Connect recent swing highs to new swing lows, indicating downtrends.

Range Lines: Connect consecutive highs or lows to outline price channels.

Each line type can be color-coded and customized for visibility.

✦ Statistics Table

An on-screen metrics table provides a live summary of trends. Script uses Relative Averaging to smooth price and time changes. This prevents outliers from distorting the data and provides a more reliable sense of typical swing behavior.

Uptrend Metrics: Shows average price and time differences from recent bullish swings.

Downtrend Metrics: Shows the same for bearish swings.

🛠️ Customization Options

Ability to tailor the indicator to suit their strategy and aesthetic preferences:

Swing Period: Adjust sensitivity to short- or long-term swings.

Color Settings: Customize line and label colors.

Label Display: Choose between absolute or percentage price differences.

Table Settings: Modify size, location, or visibility.

This makes the indicator highly flexible and useful across various timeframes and assets.

Gioteen-NormThe "Gioteen-Norm" indicator is a versatile and powerful technical analysis tool designed to help traders identify key market conditions such as divergences, overbought/oversold levels, and trend strength. By normalizing price data relative to a moving average and standard deviation, this indicator provides a unique perspective on price behavior, making it easier to spot potential reversals or continuations in the market.

The indicator calculates a normalized value based on the difference between the selected price and its moving average, scaled by the standard deviation over a user-defined period. Additionally, an optional moving average of this normalized value (Green line) can be plotted to smooth the output and enhance signal clarity. This dual-line approach makes it an excellent tool for both short-term and long-term traders.

***Key Features

Divergence Detection: The Gioteen-Norm excels at identifying divergences between price action and the normalized indicator value. For example, if the price makes a higher high while Red line forms a lower high, it may signal a bearish divergence, hinting at a potential reversal.

Overbought/Oversold Conditions: Extreme values of Red line (e.g., significantly above or below zero) can indicate overbought or oversold conditions, helping traders anticipate pullbacks or bounces.

Trend Strength Insight: The normalized output reflects how far the price deviates from its average, providing a measure of momentum and trend strength.

**Customizable Parameters

Traders can adjust the period, moving average type, applied price, and shift to suit their trading style and timeframe.

**How It Works

Label1 (Red Line): Represents the normalized price deviation from a user-selected moving average (SMA, EMA, SMMA, or LWMA) divided by the standard deviation over the specified period. This line highlights the relative position of the price compared to its historical range.

Label2 (Green Line, Optional): A moving average of Label1, which smooths the normalized data to reduce noise and provide clearer signals. This can be toggled on or off via the "Draw MA" option.

**Inputs

Period: Length of the lookback period for normalization (default: 100).

MA Method: Type of moving average for normalization (SMA, EMA, SMMA, LWMA; default: EMA).

Applied Price: Price type used for calculation (Close, Open, High, Low, HL2, HLC3, HLCC4; default: Close).

Shift: Shifts the indicator forward or backward (default: 0).

Draw MA: Toggle the display of the Label2 moving average (default: true).

MA Period: Length of the moving average for Label2 (default: 50).

MA Method (Label2): Type of moving average for Label2 (SMA, EMA, SMMA, LWMA; default: SMA).

**How to Use

Divergence Trading: Look for discrepancies between price action and Label1. A bullish divergence (higher low in Label1 vs. lower low in price) may suggest a buying opportunity, while a bearish divergence could indicate a selling opportunity.

Overbought/Oversold Levels: Monitor extreme Label1 values. For instance, values significantly above +2 or below -2 could indicate overextension, though traders should define thresholds based on the asset and timeframe.

Trend Confirmation: Use Label2 to confirm trend direction. A rising Label2 suggests increasing bullish momentum, while a declining Label2 may indicate bearish pressure.

Combine with Other Tools: Pair Gioteen-Norm with support/resistance levels, RSI, or volume indicators for a more robust trading strategy.

**Notes

The indicator is non-overlay, meaning it plots below the price chart in a separate panel.

Avoid using a Period value of 1, as it may lead to unstable results due to insufficient data for standard deviation calculation.

This tool is best used as part of a broader trading system rather than in isolation.

**Why Use Gioteen-Norm?

The Gioteen-Norm indicator offers a fresh take on price normalization, blending statistical analysis with moving average techniques. Its flexibility and clarity make it suitable for traders of all levels—whether you're scalping on short timeframes or analyzing long-term trends. By publishing this for free, I hope to contribute to the TradingView community and help traders uncover hidden opportunities in the markets.

**Disclaimer

This indicator is provided for educational and informational purposes only. It does not constitute financial advice. Always backtest and validate any strategy before trading with real capital, and use proper risk management.

Uptrick: Z-Score FlowOverview

Uptrick: Z-Score Flow is a technical indicator that integrates trend-sensitive momentum analysi s with mean-reversion logic derived from Z-Score calculations. Its primary objective is to identify market conditions where price has either stretched too far from its mean (overbought or oversold) or sits at a statistically “normal” range, and then cross-reference this observation with trend direction and RSI-based momentum signals. The result is a more contextual approach to trade entry and exit, emphasizing precision, clarity, and adaptability across varying market regimes.

Introduction

Financial instruments frequently transition between trending modes, where price extends strongly in one direction, and ranging modes, where price oscillates around a central value. A simple statistical measure like Z-Score can highlight price extremes by comparing the current price against its historical mean and standard deviation. However, such extremes alone can be misleading if the broader market structure is trending forcefully. Uptrick: Z-Score Flow aims to solve this gap by combining Z-Score with an exponential moving average (EMA) trend filter and a smoothed RSI momentum check, thus filtering out signals that contradict the prevailing market environment.

Purpose

The purpose of this script is to help traders pinpoint both mean-reversion opportunities and trend-based pullbacks in a way that is statistically grounded yet still mindful of overarching price action. By pairing Z-Score thresholds with supportive conditions, the script reduces the likelihood of acting on random price spikes or dips and instead focuses on movements that are significant within both historical and current contextual frameworks.

Originality and Uniquness

Layered Signal Verification: Signals require the fulfillment of multiple layers (Z-Score extreme, EMA trend bias, and RSI momentum posture) rather than merely breaching a statistical threshold.

RSI Zone Lockout: Once RSI enters an overbought/oversold zone and triggers a signal, the script locks out subsequent signals until RSI recovers above or below those zones, limiting back-to-back triggers.

Controlled Cooldown: A dedicated cooldown mechanic ensures that the script waits a specified number of bars before issuing a new signal in the opposite direction.

Gradient-Based Visualization: Distinct gradient fills between price and the Z-Mean line enhance readability, showing at a glance whether price is trading above or below its statistical average.

Comprehensive Metrics Panel: An optional on-chart table summarizes the Z-Score’s key metrics, streamlining the process of verifying current statistical extremes, mean levels, and momentum directions.

Why these indicators were merged

Z-Score measurements excel at identifying when price deviates from its mean, but they do not intrinsically reveal whether the market’s trajectory supports a reversion or if price might continue along its trend. The EMA, commonly used for spotting trend directions, offers valuable insight into whether price is predominantly ascending or descending. However, relying solely on a trend filter overlooks the intensity of price moves. RSI then adds a dedicated measure of momentum, helping confirm if the market’s energy aligns with a potential reversal (for example, price is statistically low but RSI suggests looming upward momentum). By uniting these three lenses—Z-Score for statistical context, EMA for trend direction, and RSI for momentum force—the script offers a more comprehensive and adaptable system, aiming to avoid false positives caused by focusing on just one aspect of price behavior.

Calculations

The core calculation begins with a simple moving average (SMA) of price over zLen bars, referred to as the basis. Next, the script computes the standard deviation of price over the same window. Dividing the difference between the current price and the basis by this standard deviation produces the Z-Score, indicating how many standard deviations the price is from its mean. A positive Z-Score reveals price is above its average; a negative reading indicates the opposite.

To detect overall market direction, the script calculates an exponential moving average (emaTrend) over emaTrendLen bars. If price is above this EMA, the script deems the market bullish; if below, it’s considered bearish. For momentum confirmation, the script computes a standard RSI over rsiLen bars, then applies a smoothing EMA over rsiEmaLen bars. This smoothed RSI (rsiEma) is monitored for both its absolute level (oversold or overbought) and its slope (the difference between the current and previous value). Finally, slopeIndex determines how many bars back the script compares the basis to check whether the Z-Mean line is generally rising, falling, or flat, which then informs the coloring scheme on the chart.

Calculations and Rational

Simple Moving Average for Baseline: An SMA is used for the core mean because it places equal weight on each bar in the lookback period. This helps maintain a straightforward interpretation of overbought or oversold conditions in the context of a uniform historical average.

Standard Deviation for Volatility: Standard deviation measures the variability of the data around the mean. By dividing price’s difference from the mean by this value, the Z-Score can highlight whether price is unusually stretched given typical volatility.

Exponential Moving Average for Trend: Unlike an SMA, an EMA places more emphasis on recent data, reacting quicker to new price developments. This quicker response helps the script promptly identify trend shifts, which can be crucial for filtering out signals that go against a strong directional move.

RSI for Momentum Confirmation: RSI is an oscillator that gauges price movement strength by comparing average gains to average losses over a set period. By further smoothing this RSI with another EMA, short-lived oscillations become less influential, making signals more robust.

SlopeIndex for Slope-Based Coloring: To clarify whether the market’s central tendency is rising or falling, the script compares the basis now to its level slopeIndex bars ago. A higher current reading indicates an upward slope; a lower reading, a downward slope; and similar readings, a flat slope. This is visually represented on the chart, providing an immediate sense of the directionality.

Inputs

zLen (Z-Score Period)

Specifies how many bars to include for computing the SMA and standard deviation that form the basis of the Z-Score calculation. Larger values produce smoother but slower signals; smaller values catch quick changes but may generate noise.

emaTrendLen (EMA Trend Filter)

Sets the length of the EMA used to detect the market’s primary direction. This is pivotal for distinguishing whether signals should be considered (price aligning with an uptrend or downtrend) or filtered out.

rsiLen (RSI Length)

Defines the window for the initial RSI calculation. This RSI, when combined with the subsequent smoothing EMA, forms the foundation for momentum-based signal confirmations.

rsiEmaLen (EMA of RSI Period)

Applies an exponential moving average over the RSI readings for additional smoothing. This step helps mitigate rapid RSI fluctuations that might otherwise produce whipsaw signals.

zBuyLevel (Z-Score Buy Threshold)

Determines how negative the Z-Score must be for the script to consider a potential oversold signal. If the Z-Score dives below this threshold (and other criteria are met), a buy signal is generated.

zSellLevel (Z-Score Sell Threshold)

Determines how positive the Z-Score must be for a potential overbought signal. If the Z-Score surpasses this threshold (and other checks are satisfied), a sell signal is generated.

cooldownBars (Cooldown (Bars))

Enforces a bar-based delay between opposite signals. Once a buy signal has fired, the script must wait the specified number of bars before registering a new sell signal, and vice versa.

slopeIndex (Slope Sensitivity (Bars))

Specifies how many bars back the script compares the current basis for slope coloration. A bigger slopeIndex highlights larger directional trends, while a smaller number emphasizes shorter-term shifts.

showMeanLine (Show Z-Score Mean Line)

Enables or disables the plotting of the Z-Mean and its slope-based coloring. Traders who prefer minimal chart clutter may turn this off while still retaining signals.

Features

Statistical Core (Z-Score Detection):

This feature computes the Z-Score by taking the difference between the current price and the basis (SMA) and dividing by the standard deviation. In effect, it translates price fluctuations into a standardized measure that reveals how significant a move is relative to the typical variation seen over the lookback. When the Z-Score crosses predefined thresholds (zBuyLevel for oversold and zSellLevel for overbought), it signals that price could be at an extreme.

How It Works: On each bar, the script updates the SMA and standard deviation. The Z-Score is then refreshed accordingly. Traders can interpret particularly large negative or positive Z-Score values as scenarios where price is abnormally low or high.

EMA Trend Filter:

An EMA over emaTrendLen bars is used to classify the market as bullish if the price is above it and bearish if the price is below it. This classification is applied to the Z-Score signals, accepting them only when they align with the broader price direction.

How It Works: If the script detects a Z-Score below zBuyLevel, it further checks if price is actually in a downtrend (below EMA) before issuing a buy signal. This might seem counterintuitive, but a “downtrend” environment plus an oversold reading often signals a potential bounce or a mean-reversion play. Conversely, for sell signals, the script checks if the market is in an uptrend first. If it is, an overbought reading aligns with potential profit-taking.

RSI Momentum Confirmation with Oversold/Overbought Lockout:

RSI is calculated over rsiLen, then smoothed by an EMA over rsiEmaLen. If this smoothed RSI dips below a certain threshold (for example, 30) and then begins to slope upward, the indicator treats it as a potential sign of recovering momentum. Similarly, if RSI climbs above a certain threshold (for instance, 70) and starts to slope downward, that suggests dwindling momentum. Additionally, once RSI is in these zones, the indicator locks out repetitive signals until RSI fully exits and re-enters those extreme territories.

How It Works: Each bar, the script measures whether RSI has dropped below the oversold threshold (like 30) and has a positive slope. If it does, the buy side is considered “unlocked.” For sell signals, RSI must exceed an overbought threshold (70) and slope downward. The combination of threshold and slope helps confirm that a reversal is genuinely in progress instead of issuing signals while momentum remains weak or stuck in extremes.

Cooldown Mechanism:

The script features a custom bar-based cooldown that prevents issuing new signals in the opposite direction immediately after one is triggered. This helps avoid whipsaw situations where the market quickly flips from oversold to overbought or vice versa.

How It Works: When a buy signal fires, the indicator notes the bar index. If the Z-Score and RSI conditions later suggest a sell, the script compares the current bar index to the last buy signal’s bar index. If the difference is within cooldownBars, the signal is disallowed. This ensures a predefined “quiet period” before switching signals.

Slope-Based Coloring (Z-Mean Line and Shadow):

The script compares the current basis value to its value slopeIndex bars ago. A higher reading now indicates a generally upward slope, while a lower reading indicates a downward slope. The script then shades the Z-Mean line in a corresponding bullish or bearish color, or remains neutral if little change is detected.

How It Works: This slope calculation is refreshingly straightforward: basis – basis . If the result is positive, the line is colored bullish; if negative, it is colored bearish; if approximately zero, it remains neutral. This provides a quick visual cue of the medium-term directional bias.

Gradient Overlays:

With gradient fills, the script highlights where price stands in relation to the Z-Mean. When price is above the basis, a purple-shaded region is painted, visually indicating a “bearish zone” for potential overbought conditions. When price is below, a teal-like overlay is used, suggesting a “bullish zone” for potential oversold conditions.

How It Works: Each bar, the script checks if price is above or below the basis. It then applies a fill between close and basis, using distinct colors to show whether the market is trading above or below its mean. This creates an immediate sense of how extended the market might be.

Buy and Sell Labels (with Alerts):

When a legitimate buy or sell condition passes every check (Z-Score threshold, EMA trend alignment, RSI gating, and cooldown clearance), the script plots a corresponding label directly on the chart. It also fires an alert (if alerts are set up), making it convenient for traders who want timely notifications.

How It Works: If rawBuy or rawSell conditions are met (refined by RSI, EMA trend, and cooldown constraints), the script calls the respective plot function to paint an arrow label on the chart. Alerts are triggered simultaneously, carrying easily recognizable messages.

Metrics Table:

The optional on-chart table (activated by showMetrics) presents real-time Z-Score data, including the current Z-Score, its rolling mean, the maximum and minimum Z-Score values observed over the last zLen bars, a percentile position, and a short-term directional note (rising, falling, or flat).

Current – The present Z-Score reading

Mean – Average Z-Score over the zLen period

Min/Max – Lowest and highest Z-Score values within zLen

Position – Where the current Z-Score sits between the min and max (as a percentile)

Trend – Whether the Z-Score is increasing, decreasing, or flat

Conclusion

Uptrick: Z-Score Flow offers a versatile solution for traders who need a statistically informed perspective on price extremes combined with practical checks for overall trend and momentum. By leveraging a well-defined combination of Z-Score, EMA trend classification, RSI-based momentum gating, slope-based visualization, and a cooldown mechanic, the script reduces the occurrence of false or premature signals. Its gradient fills and optional metrics table contribute further clarity, ensuring that users can quickly assess market posture and make more confident trading decisions in real time.

Disclaimer

This script is intended solely for informational and educational purposes. Trading in any financial market comes with substantial risk, and there is no guarantee of success or the avoidance of loss. Historical performance does not ensure future results. Always conduct thorough research and consider professional guidance prior to making any investment or trading decisions.

15% Below Daily LowESPP discount pricing (15%) - Line chart that follows the daily low of the chart to show what price you could buy a company stock with the typical discount of 15%.

Candle Height & Trend Probability DashboardDescription and Guide

Description:

This Pine Script for TradingView displays a dashboard that calculates the probability of price increases or decreases based on past price movements. It analyzes the last 30 candles (by default) and shows the probabilities for different timeframes (from 1 minute to 1 week). Additionally, it checks volatility using the ATR indicator.

Script Features:

Calculates probabilities of an upward (Up %) or downward (Down %) price move based on past candles.

Displays a dashboard showing probabilities for multiple timeframes.

Color-coded probability display:

Green if the upward probability exceeds a set threshold.

Red if the downward probability exceeds the threshold.

Yellow if neither threshold is exceeded.

Considers volatility using the ATR indicator.

Triggers alerts when probabilities exceed specific values.

How to Use:

Insert the script into TradingView: Copy and paste the script into the Pine Script editor.

Adjust parameters:

lookback: Number of past candles used for calculation (default: 30).

alertThresholdUp & alertThresholdDown: Thresholds for probabilities (default: 51%).

volatilityLength & volatilityThreshold: ATR volatility settings.

dashboardPosition: Choose where the dashboard appears on the chart.

Enable visualization: The dashboard will be displayed over the chart.

Set alerts: The script triggers notifications when probabilities exceed set thresholds.

Strategy Stats [presentTrading]Hello! it's another weekend. This tool is a strategy performance analysis tool. Looking at the TradingView community, it seems few creators focus on this aspect. I've intentionally created a shared version. Welcome to share your idea or question on this.

█ Introduction and How it is Different

Strategy Stats is a comprehensive performance analytics framework designed specifically for trading strategies. Unlike standard strategy backtesting tools that simply show cumulative profits, this analytics suite provides real-time, multi-timeframe statistical analysis of your trading performance.

Multi-timeframe analysis: Automatically tracks performance metrics across the most recent time periods (last 7 days, 30 days, 90 days, 1 year, and 4 years)

Advanced statistical measures: Goes beyond basic metrics to include Information Coefficient (IC) and Sortino Ratio

Real-time feedback: Updates performance statistics with each new trade

Visual analytics: Color-coded performance table provides instant visual feedback on strategy health

Integrated risk management: Implements sophisticated take profit mechanisms with 3-step ATR and percentage-based exits

BTCUSD Performance

The table in the upper right corner is a comprehensive performance dashboard showing trading strategy statistics.

Note: While this presentation uses Vegas SuperTrend as the underlying strategy, this is merely an example. The Stats framework can be applied to any trading strategy. The Vegas SuperTrend implementation is included solely to demonstrate how the analytics module integrates with a trading strategy.

⚠️ Timeframe Limitations

Important: TradingView's backtesting engine has a maximum storage limit of 10,000 bars. When using this strategy stats framework on smaller timeframes such as 1-hour or 2-hour charts, you may encounter errors if your backtesting period is too long.

Recommended Timeframe Usage:

Ideal for: 4H, 6H, 8H, Daily charts and above

May cause errors on: 1H, 2H charts spanning multiple years

Not recommended for: Timeframes below 1H with long history

█ Strategy, How it Works: Detailed Explanation

The Strategy Stats framework consists of three primary components: statistical data collection, performance analysis, and visualization.

🔶 Statistical Data Collection

The system maintains several critical data arrays:

equityHistory: Tracks equity curve over time

tradeHistory: Records profit/loss of each trade

predictionSignals: Stores trade direction signals (1 for long, -1 for short)

actualReturns: Records corresponding actual returns from each trade

For each closed trade, the system captures:

float tradePnL = strategy.closedtrades.profit(tradeIndex)

float tradeReturn = strategy.closedtrades.profit_percent(tradeIndex)

int tradeType = entryPrice < exitPrice ? 1 : -1 // Direction

🔶 Performance Metrics Calculation

The framework calculates several key performance metrics:

Information Coefficient (IC):

The correlation between prediction signals and actual returns, measuring forecast skill.

IC = Correlation(predictionSignals, actualReturns)

Where Correlation is the Pearson correlation coefficient:

Correlation(X,Y) = (nΣXY - ΣXY) / √

Sortino Ratio:

Measures risk-adjusted return focusing only on downside risk:

Sortino = (Avg_Return - Risk_Free_Rate) / Downside_Deviation

Where Downside Deviation is:

Downside_Deviation = √

R_i represents individual returns, T is the target return (typically the risk-free rate), and n is the number of observations.

Maximum Drawdown:

Tracks the largest percentage drop from peak to trough:

DD = (Peak_Equity - Trough_Equity) / Peak_Equity * 100

🔶 Time Period Calculation

The system automatically determines the appropriate number of bars to analyze for each timeframe based on the current chart timeframe:

bars_7d = math.max(1, math.round(7 * barsPerDay))

bars_30d = math.max(1, math.round(30 * barsPerDay))

bars_90d = math.max(1, math.round(90 * barsPerDay))

bars_365d = math.max(1, math.round(365 * barsPerDay))

bars_4y = math.max(1, math.round(365 * 4 * barsPerDay))

Where barsPerDay is calculated based on the chart timeframe:

barsPerDay = timeframe.isintraday ?

24 * 60 / math.max(1, (timeframe.in_seconds() / 60)) :

timeframe.isdaily ? 1 :

timeframe.isweekly ? 1/7 :

timeframe.ismonthly ? 1/30 : 0.01

🔶 Visual Representation

The system presents performance data in a color-coded table with intuitive visual indicators:

Green: Excellent performance

Lime: Good performance

Gray: Neutral performance

Orange: Mediocre performance

Red: Poor performance

█ Trade Direction

The Strategy Stats framework supports three trading directions:

Long Only: Only takes long positions when entry conditions are met

Short Only: Only takes short positions when entry conditions are met

Both: Takes both long and short positions depending on market conditions

█ Usage

To effectively use the Strategy Stats framework:

Apply to existing strategies: Add the performance tracking code to any strategy to gain advanced analytics

Monitor multiple timeframes: Use the multi-timeframe analysis to identify performance trends

Evaluate strategy health: Review IC and Sortino ratios to assess predictive power and risk-adjusted returns

Optimize parameters: Use performance data to refine strategy parameters

Compare strategies: Apply the framework to multiple strategies to identify the most effective approach

For best results, allow the strategy to generate sufficient trade history for meaningful statistical analysis (at least 20-30 trades).

█ Default Settings

The default settings have been carefully calibrated for cryptocurrency markets:

Performance Tracking:

Time periods: 7D, 30D, 90D, 1Y, 4Y

Statistical measures: Return, Win%, MaxDD, IC, Sortino Ratio

IC color thresholds: >0.3 (green), >0.1 (lime), <-0.1 (orange), <-0.3 (red)

Sortino color thresholds: >1.0 (green), >0.5 (lime), <0 (red)

Multi-Step Take Profit:

ATR multipliers: 2.618, 5.0, 10.0

Percentage levels: 3%, 8%, 17%

Short multiplier: 1.5x (makes short take profits more aggressive)

Stop loss: 20%

Spent Output Profit Ratio (SOPR) Z-Score | [DeV]SOPR Z-Score

The Spent Output Profit Ratio (SOPR) is an advanced on-chain metric designed to provide deep insights into Bitcoin market dynamics by measuring the ratio between the combined USD value of all Bitcoin outputs spent on a given day and their combined USD value at the time of creation (typically, their purchase price). As a member of the Realized Profit/Loss family of metrics, SOPR offers a window into aggregate seller behavior, effectively representing the USD amount received by sellers divided by the USD amount they originally paid. This indicator enhances this metric by normalizing it into a Z-Score, enabling a statistically robust analysis of market sentiment relative to historical trends, augmented by a suite of customizable features for precision and visualization.

SOPR Settings -

Lookback Length (Default: 150 days): Determines the historical window for calculating the Z-Score’s mean and standard deviation. A longer lookback captures broader market cycles, providing a stable baseline for identifying extreme deviations, which is particularly valuable for long-term strategic analysis.

Smoothing Period (Default: 100 days): Applies an EMA to the raw SOPR, balancing responsiveness to recent changes with noise reduction. This extended smoothing period ensures the indicator focuses on sustained shifts in seller behavior, ideal for institutional-grade trend analysis.

Moving Average Settings -

MA Lookback Length (Default: 90 days): Sets the period for the Z-Score’s moving average, offering a shorter-term trend signal relative to the 150-day Z-Score lookback. This contrast enhances the ability to detect momentum shifts within the broader context.

MA Type (Default: EMA): Provides six moving average types, from the simple SMA to the volume-weighted VWMA. The default EMA strikes an optimal balance between smoothness and responsiveness, while alternatives like HMA (Hull) or VWMA (volume-weighted) allow for specialized applications, such as emphasizing recent price action or incorporating volume dynamics.

Display Settings -

Show Moving Average (Default: True): Toggles the visibility of the Z-Score MA plot, enabling users to focus solely on the raw Z-Score when preferred.

Show Background Colors (Default: True): Activates dynamic background shading, enhancing visual interpretation of market regimes.

Background Color Source (Default: SOPR): Allows users to tie the background color to either the SOPR Z-Score’s midline (reflecting adjustedZScore > 0) or the MA’s trend direction (zScoreMA > zScoreMA ). This dual-source option provides flexibility to align the visual context with the primary analytical focus.

Analytical Applications -

Bear Market Resistance: When the Z-Score approaches or exceeds zero (raw SOPR near 1), it often signals resistance as sellers rush to exit at break-even, a pattern historically observed during downtrends. A rising Z-Score MA crossing zero can confirm this pressure.

Bull Market Support: Conversely, a Z-Score dropping below zero in uptrends indicates reluctance to sell at a loss, forming support as sell pressure diminishes. The MA’s bullish coloring reinforces confirmation of renewed buying interest.

Extreme Deviations: Values significantly above or below zero highlight overbought or oversold conditions, respectively, offering opportunities for contrarian positioning when paired with other on-chain or price-based metrics.

Econometrica by [SS]This is Econometrica, an indicator that aims to bridge a big gap between the resources available for analysis of fundamental data and its impact on tickers and price action.

I have noticed a general dearth of available indicators that offer insight into how fundamentals impact a ticker and provide guidance on how they these economic factors influence ticker behaviour.

Enter Econometrica. Econometrica is a math based indicator that aims to co-integrate and model indicator price action in relation to critical economic metrics.

Econometrica supports the following US based economic data:

CPI

Non-Farm Payroll

Core Inflation

US Money Supply

US Central Bank Balance Sheet

GDP

PCE

Let's go over the functions of Econometrica.

Creating a Regression Cointegrated Model

The first thing Econometrica does is creates a co-integrated regression, as you see in the main chart, predicting ticker value ranges from fundamental economic data.

You can visualize this in the main chart above, but here are some other examples:

SPY vs Core Inflation:

BA vs PCE:

QQQ vs US Balance Sheet:

The band represents the anticipated range the ticker should theoretically fall in based on the underlying economic value. The indicator will breakdown the relationship between the economic indicator and the ticker more precisely. In the images above, you can see how there are some metrics provided, including Stationairty, lagged correlation, Integrated Correlation and R2. Let's discuss these very briefly:

Stationarity: checks to ensure that the relationship between the economic indicator and ticker is stationary. Stationary data is important for making unbiased inferences and projections, so having data that is stationary is valuable.

Lagged Correlation: This is a very interesting metric. Lagged correlation means whether there is a delay in the economic indicator and the response of the ticker. Typically, you will observed a lagged correlation between an economic indicator and price of a ticker, as it can take some time for economic changes to reach the market. This lagged correlation will provide you with how long it takes for the economic indicator to catch up with the ticker in months.

Integrated Correlation: This metric tells you how good of a fit the regression bands are in relation to the ticker price. A higher correlation, means the model is better at consistent and accurate information about the anticipated range for the ticker in relation to the economic indicator.