Buy on 5% dip strategy with time adjustment

This script is a strategy called "Buy on 5% Dip Strategy with Time Adjustment 📉💡," which detects a 5% drop in price and triggers a buy signal 🔔. It also automatically closes the position once the set profit target is reached 💰, and it has additional logic to close the position if the loss exceeds 14% after holding for 230 days ⏳.

Strategy Explanation

Buy Condition: A buy signal is triggered when the price drops 5% from the highest price reached 🔻.

Take Profit: The position is closed when the price hits a 1.22x target from the average entry price 📈.

Forced Sell Condition: If the position is held for more than 230 days and the loss exceeds 14%, the position is automatically closed 🚫.

Leverage & Capital Allocation: Leverage is adjustable ⚖️, and you can set the percentage of capital allocated to each trade 💸.

Time Limits: The strategy allows you to set a start and end time ⏰ for trading, making the strategy active only within that specific period.

Code Credits and References

Credits: This script utilizes ideas and code from @QuantNomad and jangdokang for the profit table and algorithm concepts 🔧.

Sources:

Monthly Performance Table Script by QuantNomad:

ZenAndTheArtOfTrading's Script:

Strategy Performance

This strategy provides risk management through take profit and forced sell conditions and includes a performance table 📊 to track monthly and yearly results. You can compare backtest results with real-time performance to evaluate the strategy's effectiveness.

The performance numbers shown in the backtest reflect what would have happened if you had used this strategy since the launch date of the SOXL (the Direxion Daily Semiconductor Bull 3x Shares ETF) 📅. These results are not hypothetical but based on actual performance from the day of the ETF’s launch 📈.

Caution ⚠️

No Guarantee of Future Results: The results are based on historical performance from the launch of the SOXL ETF, but past performance does not guarantee future results. It’s important to approach with caution when applying it to live trading 🔍.

Risk Management: Leverage and capital allocation settings are crucial for managing risk ⚠️. Make sure to adjust these according to your risk tolerance ⚖️.

Statistics

ADX BoxDescription:

The ADX Box indicator provides traders with a quick and intuitive way to monitor the current trend strength based on the Average Directional Index (ADX), calculated with a customisable period (default: 7 periods).

This compact indicator neatly displays the current ADX value rounded to one decimal place, along with a clear directional arrow:

Green upward triangle (▲): Indicates that ADX is rising above its moving average, signaling increasing trend strength.

Red downward triangle (▼): Indicates that ADX is declining below its moving average, signaling weakening trend strength.

Key Features:

Small and clean visual representation.

Dynamically updates in real-time directly on the chart.

Ideal for quick trend strength assessment without cluttering your workspace.

Recommended Usage:

Quickly identifying whether market trends are strengthening or weakening.

Enhancing decision-making for trend-following or breakout trading strategies.

Complementing other indicators such as ATR boxes for volatility measurement.

Feel free to use, share, and incorporate this indicator into your trading setups for clearer insights and more confident trading decisions!

Correlation TableThis indicator displays a vertical table that shows the correlation between the asset currently loaded on the chart and up to 32 selected trading pairs. It offers the following features:

Chart-Based Correlation: Correlations are calculated based on the asset you have loaded in your chart, providing relevant insights for your current market focus.

Configurable Pairs: Choose from a list of 32 symbols (e.g., AUDUSD, EURUSD, GBPUSD, etc.) with individual checkboxes to include or exclude each pair in the correlation analysis.

Custom Correlation Length: Adjust the lookback period for the correlation calculation to suit your analysis needs.

Optional EMA Smoothing: Enable an Exponential Moving Average (EMA) on the price data, with a configurable EMA length, to smooth the series before calculating correlations.

Color-Coded Output: The table cells change color based on the correlation strength and direction—neutral, bullish (green), or bearish (red)—making it easy to interpret at a glance.

Clear Table Layout: The indicator outputs a neatly organized vertical table with headers for "Pair" and "Correlation," ensuring the information is displayed cleanly and is easy to understand.

Ideal for traders who want a quick visual overview of how different instruments correlate with their current asset, this tool supports informed multi-asset analysis

ITALIANO:

Questo indicatore visualizza una tabella verticale che mostra la correlazione tra l'asset attualmente caricato sul grafico e fino a 32 coppie di trading selezionate. Offre le seguenti funzionalità:

Correlazione basata sul grafico: le correlazioni vengono calcolate in base all'asset caricato nel grafico, fornendo informazioni pertinenti per il tuo attuale focus di mercato.

Coppie configurabili: scegli da un elenco di 32 simboli (ad esempio, AUDUSD, EURUSD, GBPUSD, ecc.) con caselle di controllo individuali per includere o escludere ciascuna coppia nell'analisi della correlazione.

Lunghezza di correlazione personalizzata: regola il periodo di lookback per il calcolo della correlazione in base alle tue esigenze di analisi.

Smoothing EMA opzionale: abilita una media mobile esponenziale (EMA) sui dati dei prezzi, con una lunghezza EMA configurabile, per smussare la serie prima di calcolare le correlazioni.

Output codificato a colori: le celle della tabella cambiano colore in base alla forza e alla direzione della correlazione, neutra, rialzista (verde) o ribassista (rosso), rendendola facile da interpretare a colpo d'occhio.

Clear Table Layout: l'indicatore genera una tabella verticale ordinatamente organizzata con intestazioni per "Coppia" e "Correlazione", assicurando che le informazioni siano visualizzate in modo chiaro e siano facili da comprendere.

Ideale per i trader che desiderano una rapida panoramica visiva di come diversi strumenti siano correlati con il loro asset corrente, questo strumento supporta un'analisi multi-asset informata

Standard Deviation (fadi)The Standard Deviation indicator uses standard deviation to map out price movements. Standard deviation measures how much prices stray from their average—small values mean steady trends, large ones mean wild swings. Drawing from up to 20 years of data, it plots key levels using customizable Fibonacci lines tied to that standard deviation, giving traders a snapshot of typical price behavior.

These levels align with a bell curve: about 68% of price moves stay within 1 standard deviation, 95% within roughly 2, and 99.7% within roughly 3. When prices break past the 1 StDev line, they’re outliers—only 32% of moves go that far. Prices often snap back to these lines or the average, though the reversal might not happen the same day.

How Traders Use It

If prices surge past the 1 StDev line, traders might wait for momentum to fade, then trade the pullback to that line or the average, setting a target and stop.

If prices dip below, they might buy, anticipating a bounce—sometimes a day or two later. It’s a tool to spot overstretched prices likely to revert and/or measure the odds of continuation.

Settings

Higher Timeframe: Sets the Higher Timeframe to calculate the Standard Deviation for

Show Levels for the Last X Days: Displays levels for the specified number of days.

Based on X Period: Number of days to calculate standard deviation (e.g., 20 years ≈ 5,040 days). Larger periods smooth out daily level changes.

Mirror Levels on the Other Side: Plots symmetric positive and negative levels around the average.

Fibonacci Levels Settings: Defines which levels and line styles to show. With mirroring, negative values aren’t needed.

Background Transparency: Turn on Background color derived from the level colors with the specified transparency

Overrides: Lets advanced users input custom standard deviations for specific tickers (e.g., NQ1! at 0.01296).

StatPivot- Dynamic Range Analyzer - indicator [PresentTrading]Hello everyone! In the following few open scripts, I would like to share various statistical tools that benefit trading. For this time, it is a powerful indicator called StatPivot- Dynamic Range Analyzer that brings a whole new dimension to your technical analysis toolkit.

This tool goes beyond traditional pivot point analysis by providing comprehensive statistical insights about price movements, helping you identify high-probability trading opportunities based on historical data patterns rather than subjective interpretations. Whether you're a day trader, swing trader, or position trader, StatPivot's real-time percentile rankings give you a statistical edge in understanding exactly where current price action stands within historical contexts.

Welcome to share your opinions! Looking forward to sharing the next tool soon!

█ Introduction and How it is Different

StatPivot is an advanced technical analysis tool that revolutionizes retracement analysis. Unlike traditional pivot indicators that only show static support/resistance levels, StatPivot delivers dynamic statistical insights based on historical pivot patterns.

Its key innovation is real-time percentile calculation - while conventional tools require new pivot formations before updating (often too late for trading decisions), StatPivot continuously analyzes where current price stands within historical retracement distributions.

Furthermore, StatPivot provides comprehensive statistical metrics including mean, median, standard deviation, and percentile distributions of price movements, giving traders a probabilistic edge by revealing which price levels represent statistically significant zones for potential reversals or continuations. By transforming raw price data into statistical insights, StatPivot helps traders move beyond subjective price analysis to evidence-based decision making.

█ Strategy, How it Works: Detailed Explanation

🔶 Pivot Point Detection and Analysis

The core of StatPivot's functionality begins with identifying significant pivot points in the price structure. Using the parameters left and right, the indicator locates pivot highs and lows by examining a specified number of bars to the left and right of each potential pivot point:

Copyp_low = ta.pivotlow(low, left, right)

p_high = ta.pivothigh(high, left, right)

For a point to qualify as a pivot low, it must have left higher lows to its left and right higher lows to its right. Similarly, a pivot high must have left lower highs to its left and right lower highs to its right. This approach ensures that only significant turning points are recognized.

🔶 Percentage Change Calculation

Once pivot points are identified, StatPivot calculates the percentage changes between consecutive pivot points:

For drops (when a pivot low is lower than the previous pivot low):

CopydropPercent = (previous_pivot_low - current_pivot_low) / previous_pivot_low * 100

For rises (when a pivot high is higher than the previous pivot high):

CopyrisePercent = (current_pivot_high - previous_pivot_high) / previous_pivot_high * 100

These calculations quantify the magnitude of each market swing, allowing for statistical analysis of historical price movements.

🔶 Statistical Distribution Analysis

StatPivot computes comprehensive statistics on the historical distribution of drops and rises:

Average (Mean): The arithmetic mean of all recorded percentage changes

CopyavgDrop = array.avg(dropValues)

Median: The middle value when all percentage changes are arranged in order

CopymedianDrop = array.median(dropValues)

Standard Deviation: Measures the dispersion of percentage changes from the average

CopystdDevDrop = array.stdev(dropValues)

Percentiles (25th, 75th): Values below which 25% and 75% of observations fall

Copyq1 = array.get(sorted, math.floor(cnt * 0.25))

q3 = array.get(sorted, math.floor(cnt * 0.75))

VaR95: The maximum expected percentage drop with 95% confidence

Copyvar95D = array.get(sortedD, math.floor(nD * 0.95))

Coefficient of Variation (CV): Measures relative variability

CopycvD = stdDevDrop / avgDrop

These statistics provide a comprehensive view of market behavior, enabling traders to understand the typical ranges and extreme moves.

🔶 Real-time Percentile Ranking

StatPivot's most innovative feature is its real-time percentile calculation. For each current price, it calculates:

The percentage drop from the latest pivot high:

CopycurrentDropPct = (latestPivotHigh - close) / latestPivotHigh * 100

The percentage rise from the latest pivot low:

CopycurrentRisePct = (close - latestPivotLow) / latestPivotLow * 100

The percentile ranks of these values within the historical distribution:

CopyrealtimeDropRank = (count of historical drops <= currentDropPct) / total drops * 100

This calculation reveals exactly where the current price movement stands in relation to all historical movements, providing crucial context for decision-making.

🔶 Cluster Analysis

To identify the most common retracement zones, StatPivot performs a cluster analysis by dividing the range of historical drops into five equal intervals:

CopyrangeSize = maxVal - minVal

For each interval boundary:

Copyboundaries = minVal + rangeSize * i / 5

By counting the number of observations in each interval, the indicator identifies the most frequently occurring retracement zones, which often serve as significant support or resistance areas.

🔶 Expected Price Targets

Using the statistical data, StatPivot calculates expected price targets:

CopytargetBuyPrice = close * (1 - avgDrop / 100)

targetSellPrice = close * (1 + avgRise / 100)

These targets represent statistically probable price levels for potential entries and exits based on the average historical behavior of the market.

█ Trade Direction

StatPivot functions as an analytical tool rather than a direct trading signal generator, providing statistical insights that can be applied to various trading strategies. However, the data it generates can be interpreted for different trade directions:

For Long Trades:

Entry considerations: Look for price drops that reach the 70-80th percentile range in the historical distribution, suggesting a statistically significant retracement

Target setting: Use the Expected Sell price or consider the average rise percentage as a reasonable target

Risk management: Set stop losses below recent pivot lows or at a distance related to the statistical volatility (standard deviation)

For Short Trades:

Entry considerations: Look for price rises that reach the 70-80th percentile range, indicating an unusual extension

Target setting: Use the Expected Buy price or average drop percentage as a target

Risk management: Set stop losses above recent pivot highs or based on statistical measures of volatility

For Range Trading:

Use the most common drop and rise clusters to identify probable reversal zones

Trade bounces between these statistically significant levels

For Trend Following:

Confirm trend strength by analyzing consecutive higher pivot lows (uptrend) or lower pivot highs (downtrend)

Use lower percentile retracements (20-30th percentile) as entry opportunities in established trends

█ Usage

StatPivot offers multiple ways to integrate its statistical insights into your trading workflow:

Statistical Table Analysis: Review the comprehensive statistics displayed in the data table to understand the market's behavior. Pay particular attention to:

Average drop and rise percentages to set reasonable expectations

Standard deviation to gauge volatility

VaR95 for risk assessment

Real-time Percentile Monitoring: Watch the real-time percentile display to see where the current price movement stands within the historical distribution. This can help identify:

Extreme movements (90th+ percentile) that might indicate reversal opportunities

Typical retracements (40-60th percentile) that might continue further

Shallow pullbacks (10-30th percentile) that might represent continuation opportunities in trends

Support and Resistance Identification: Utilize the plotted pivot points as key support and resistance levels, especially when they align with statistically significant percentile ranges.

Target Price Setting: Use the expected buy and sell prices calculated from historical averages as initial targets for your trades.

Risk Management: Apply the statistical measurements like standard deviation and VaR95 to set appropriate stop loss levels that account for the market's historical volatility.

Pattern Recognition: Over time, learn to recognize when certain percentile levels consistently lead to reversals or continuations in your specific market, and develop personalized strategies based on these observations.

█ Default Settings

The default settings of StatPivot have been carefully calibrated to provide reliable statistical analysis across a variety of markets and timeframes, but understanding their effects allows for optimal customization:

Left Bars (30) and Right Bars (30): These parameters determine how pivot points are identified. With both set to 30 by default:

A pivot low must be the lowest point among 30 bars to its left and 30 bars to its right

A pivot high must be the highest point among 30 bars to its left and 30 bars to its right

Effect on performance: Larger values create fewer but more significant pivot points, reducing noise but potentially missing important market structures. Smaller values generate more pivot points, capturing more nuanced movements but potentially including noise.

Table Position (Top Right): Determines where the statistical data table appears on the chart.

Effect on performance: No impact on analytical performance, purely a visual preference.

Show Distribution Histogram (False): Controls whether the distribution histogram of drop percentages is displayed.

Effect on performance: Enabling this provides visual insight into the distribution of retracements but can clutter the chart.

Show Real-time Percentile (True): Toggles the display of real-time percentile rankings.

Effect on performance: A critical setting that enables the dynamic analysis of current price movements. Disabling this removes one of the key advantages of the indicator.

Real-time Percentile Display Mode (Label): Chooses between label display or indicator line for percentile rankings.

Effect on performance: Labels provide precise information at the current price point, while indicator lines show the evolution of percentile rankings over time.

Advanced Considerations for Settings Optimization:

Timeframe Adjustment: Higher timeframes generally benefit from larger Left/Right values to identify truly significant pivots, while lower timeframes may require smaller values to capture shorter-term swings.

Volatility-Based Tuning: In highly volatile markets, consider increasing the Left/Right values to filter out noise. In less volatile conditions, lower values can help identify more potential entry and exit points.

Market-Specific Optimization: Different markets (forex, stocks, commodities) display different retracement patterns. Monitor the statistics table to see if your market typically shows larger or smaller retracements than the current settings are optimized for.

Trading Style Alignment: Adjust the settings to match your trading timeframe. Day traders might prefer settings that identify shorter-term pivots (smaller Left/Right values), while swing traders benefit from more significant pivots (larger Left/Right values).

By understanding how these settings affect the analysis and customizing them to your specific market and trading style, you can maximize the effectiveness of StatPivot as a powerful statistical tool for identifying high-probability trading opportunities.

Time Marker Pro: Vertical Line at Key Times)Smart Vertical Line at Specific Time (with Timezone, Color, and Width Controls)

This script draws a vertical line on your chart at a user-defined time once per day, based on the selected timezone.

🕒 Key Features:

Set your target hour and minute

Choose from a list of common timezones (Tehran, UTC, New York, etc.)

Customize the line color and thickness

Works across all intraday timeframes (1min, 5min, 15min, etc.)

Adjusts automatically to bar intervals — no need for exact time matching

This is perfect for traders who want to:

Highlight the start of a session

Mark specific news times, breakouts, or routine entries

Visualize key time-based levels on the chart

Correlation X macroeconomicsFind the correlation between financial assets and the main Brazilian macroeconomic variables:

SELIC rate (Red)

PIB (Green)

Inflation (Blue)

Employment and income (Yellow)

Unlike other indicators that measure the correlation between two assets, the indicator "Correlation X macroeconomics" measures, for example, the correlation that the VALE3 asset has with the SELIC rate.

The correlation is obtained by calculating the variation suffered by a given asset on the day a given Brazilian macroeconomic variable is released.

This indicator can be used on any financial asset.

Use time frame chart = 1 day.

To calculate the correlation, data published by IBGE and the Central Bank of Brazil over a period of time are used. This time period is different depending on the selected macroeconomic variable. Namely:

16 PIB disclosures (4 years)

24 SELIC rate disclosures (3 years)

24 disclosures of IPCA and employment and income data (2 years)

You can select one or more macroeconomic variables to check the effect of correlation separately on each of them.

This indicator "Correlation X macroeconomics" will be updated monthly, as detailed below:

At the end of the day on which the PIB is released

At the end of the day on which employment and income data are released

At the end of the day following the day on which the SELIC rate is published

On the last business day of the month if none of the aforementioned disclosures occur

BTC Dominance PercentageThis BTC Dominance Percentage indicator calculates Bitcoin's dominance relative to altcoins, excluding stablecoins.

🔹 Unlike the standard BTC.D metric, which includes all cryptocurrencies (including stablecoins like USDT, USDC, and DAI), this version focuses only on Bitcoin’s market share compared to altcoins.

🔹 It calculates BTC dominance relative to major altcoins (ETH, BNB, ADA, XRP, SOL) and the OTHERS.D index, which represents smaller-cap altcoins.

🔹 Stablecoins are excluded, providing a clearer view of Bitcoin’s actual strength against the altcoin market, without distortion from fiat-pegged assets.

🚀 This is a true BTC dominance metric for tracking Bitcoin’s market position against altcoins!

Multi-Faceted Analysis ToolHere’s a detailed description for the **Multi-Faceted Analysis Tool** TradingView indicator:

---

## Multi-Faceted Analysis Tool

### Overview

The **Multi-Faceted Analysis Tool** is a powerful TradingView indicator designed to enhance your technical analysis by combining several popular indicators: Simple Moving Average (SMA), Relative Strength Index (RSI), and Moving Average Convergence Divergence (MACD). This indicator provides traders with insightful market signals that can be tailored to fit various trading strategies and timeframes.

### Key Features

1. **Simple Moving Average (SMA)**:

- Plots a customizable SMA on the price chart. The length of the SMA can be adjusted to suit your analysis needs (default is set to 50). The SMA helps identify the overall trend direction.

2. **Relative Strength Index (RSI)**:

- Calculates and plots RSI values, providing insights into potential overbought or oversold market conditions. The user can customize the length of the RSI calculation (default is 14).

- Overbought (70) and oversold (30) levels are visually marked, helping traders identify potential reversal points.

3. **MACD**:

- Computes MACD values with customizable parameters for fast length, slow length, and signal length (defaults are 12, 26, and 9 respectively).

- The MACD histogram is displayed, highlighting the difference between the MACD line and the signal line, which can help traders visualize momentum shifts.

4. **Buy and Sell Signals**:

- Generates clear buy and sell signals based on RSI crossover with established thresholds (buy when RSI crosses above 30, sell when RSI crosses below 70). These signals are visually represented on the chart for easy decision-making.

5. **User-Friendly Customization**:

- All parameters are adjustable, allowing traders to set their preferred values based on individual strategies or market conditions. This flexibility ensures that the tool can cater to a wide range of trading styles.

CHG FROM OPEN %As an intraday trader, I'm more interested in seeing the CHG FROM OPEN % than the CHG % measured from yesterday's close. I overlay this script on a separate Volume pane so it doesn't hide my price chart, and I hide the line since the line isn't particularly useful to me.

This script shows the current real-time CHG FROM OPEN % when you hover outside of the chart during regular trading hours (all times NYC/EST). Hovering over the chart will show you the historical CHG FROM OPEN % and, if extended hours, the CHG FROM OPEN % at the previous close.

You can also find CHG FROM OPEN % in the stock screener, but having it in the chart is more convenient for me.

Share Value Indicator**Share Value Indicator**

This TradingView indicator allows traders to track the real-time total value of their stock holdings. Users can input the number of shares they own, and the script calculates the total value based on the current stock price. A horizontal ray is drawn at the last price level, and a label displays the total value of the shares. The indicator updates dynamically, ensuring only one ray and label are visible at a time. Ideal for traders who want to visualize their investment's real-time worth directly on the chart.

rate_of_changeLibrary "rate_of_change"

// @description: Applies ROC algorithm to any pair of values.

// This library function is used to scale change of value (price, volume) to a percentage value, just as the ROC indicator would do. It is good practice to scale arbitrary ranges to set boundaries when you try to train statistical model.

rateOfChange(value, base, hardlimit)

This function is a helper to scale a value change to its percentage value.

Parameters:

value (float)

base (float)

hardlimit (int)

Returns: per: A float comprised between 0 and 100

TradingView Financial Data ViewerTrading view provides request.security function to view the financial information of a script. The available sets of data is documented on below link

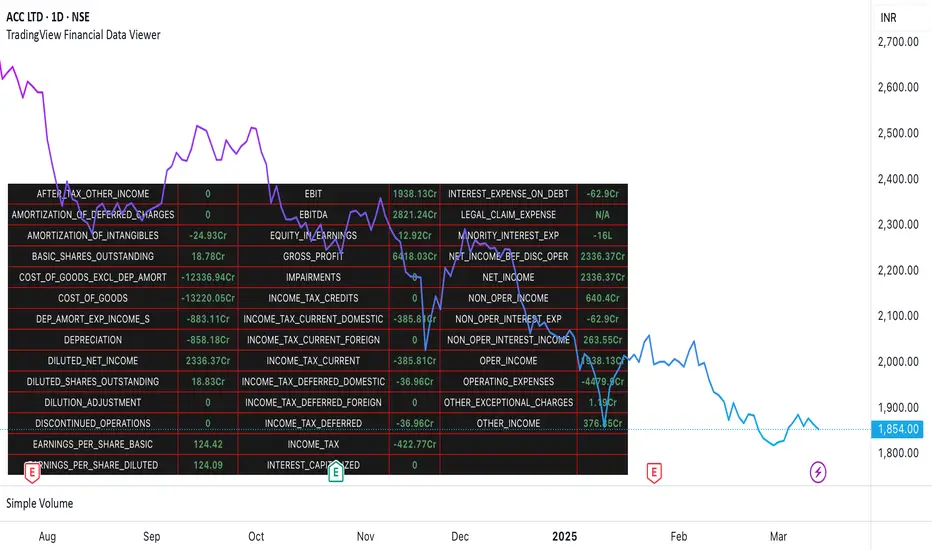

www.tradingview.com

The problem is there is no easy way to view this data as there are limitations to the # of unique requests that can be made. The limit is 40 for general paid accounts. So its makes it impossible to view the data in case you are looking to build a plugin related to some financial analysis.

So I came up with this trading view plugin which based on the documentation bifurcates the values available in the FQ, TTM and FY periods. Then you can select which period you would like to see. How many values you want to see at a time. And then next set of data can be viewed by increasing the Set # from 1 to which ever number keeps giving you the data.

Notes:

This is a data view only indicator and it will only display the latest data available for which quarter was there.

In case you want to view past data then you should go to replay mode and cut to the relative earning tags where you want to view the data

This is again for educational or study purpose only and is majorly helpful for those who want to create indicators based on Trading view supported financials and want to view what values are given for specific financial ids

The documentation reference and source of the plugin can be checked

Avg.ROC TableThis indicator calculates the average Rate of Change (ROC) for up to 30 user-selected assets over a specified number of candles. It then ranks the assets—assigning rank 1 to the asset with the highest average ROC (strongest momentum) and rank 30 to the asset with the lowest. The results are displayed in a clean, easy-to-read table split into two stacks of 15 assets each, allowing you to quickly see which assets are performing best.

MonthlyReturnTableLibrary "MonthlyReturnTable"

TODO: The table displays monthly returns, profits, MDD, and number of trades.

get_table(mode, tablePosition, precision, textSize, marginTop, marginBottom, marginLeft, marginRight, colorHead, colorBull, colorBear, colorZero)

: get_table

Parameters:

mode (string)

tablePosition (string)

precision (int)

textSize (int)

marginTop (int)

marginBottom (int)

marginLeft (int)

marginRight (int)

colorHead (color)

colorBull (color)

colorBear (color)

colorZero (color)

Returns: : null, plot perfTable

Normalized VolumeOVERVIEW

The Normalized Volume (NV) is an attempt at visualizing volume in a format that is more understandable by placing the values on a scale of 0 to 100. 0 in this case is the lowest volume candle available on the chart, and 100 being the highest. Calling a candle “high volume” can be misleading without having something to compare to. For example, in scaling the volume this way we can clearly see that a given candle had 80% of the peak volume or 20%, and gauge the validity of price moves more accurately.

FEATURES

NV by session

Allows user to filter the volume values across 4 different sessions. This can add context to the volume output, because what it high volume during London session may not be high volume relative to New York session.

Overlay plotting

When volume boxes are turned on, this will allow you to toggle how they are plotted.

Color theme

A standard color theme will color the NV based on if the respective candle closed green or red. Selecting variables will color the NV plot based on which range the value falls within.

Session inputs

Activated with the “By session?” Input. Allows user to break the day up into 4 sessions to more accurately gauge volume relative to time of day.

Show Box (X)

Toggles on chart boxes on and off.

Show historical boxes

Will plot prior occurrences of selected volume boxes, deleting them when price fully moves through them in the opposite direction of the initial candle.

Color inputs

Allows for intensive customization in how this tool appears visually.

INTERPRETATION

There are 6 pre-defined ranges that NV can fall within.

NV <= 10

Volume is insignificant

In this range, volume should not be a confirmation in your trading strategy.

NV > 10 and <= 20

Volume is low

In this range, volume should not be a confirmation in your trading strategy.

NV > 20 and <= 40

Volume is fair

In this range, volume should not be the primary confirmation in your trading strategy.

NV > 40 and <= 60

Volume is high

In this range, volume can be the primary confirmation in your trading strategy.

NV > 60 and <= 80

Volume is very high

In this range, volume can be the primary confirmation in your trading strategy.

NV > 80

Volume is extreme

In this range, volume is likely news driven and caution should be taken. High price volatility possible.

To utilize this tool in conjunction with your current strategy, follow the range explanations above section in this section. The higher the NV value, the stronger you can feel about your directional confirmation.

If NV = 100, this means that the highest volume candle occurred up to that point on your selected timeframe. All future data points will be weighed off of this value.

LIMITATIONS

This tool will not load on tickers that do not have volume data, such as VIX.

STRATEGY

The Normalized Volume plot can be used in exactly the same way as you would normally utilize volume in your trading strategy. All we are doing is weighing the volume relative to itself.

Volume boxes can be used as targets to be filled in a similar way to commonly used “fair value gap” strategies. To utilize this strategy, I recommend selecting “Plot to Wicks” in Overlay Plotting and toggling on Show Historical Boxes.

Volume boxes can be used as areas for entry in a similar way to commonly used “order block” strategies. To utilize this strategy, I recommend selecting “Open To Close” in Overlay Plotting.

NOTES

You are able to plot an info label on right side of NV plot using the "Toggle box label" input. When a box is toggled on this label will tell you when the most recent box of that intensity occurred.

This tool is deeply visually customizable, with the ability to adjust line width for plotted boxes, all colors on both box overlays, and all colors on NV panel. Customize it to your liking!

I have a handful of additional features that I plan on adding to this tool in future updates. If there is anything you would like to see added, any bugs you identify, or any strategies you encounter with this tool, I would love to hear from you!

Huge shoutout to @joebaus for assisting in bringing this tool to life, please check out his work here on TradingView!

Volume +OBV + ADXVolume + OBV + ADX Table

Optimized Buyer & Seller Volume with Trend Indications

Overview:

This indicator provides a comprehensive view of market participation and trend strength by integrating Volume, On Balance Volume (OBV) trends, and ADX (Average Directional Index) signals into a visually structured table. Designed for quick decision-making, it highlights buyer and seller dominance while comparing the selected stock with another custom symbol.

Features:

✅ Buyer & Seller Volume Analysis:

Computes buyer and seller volume percentages based on market movements.

Displays daily cumulative volume statistics to assess ongoing market participation.

✅ On Balance Volume (OBV) Trends:

Identifies positive, negative, or neutral OBV trends using an advanced smoothing mechanism.

Highlights accumulation or distribution phases with colored visual cues.

✅ ADX-Based Trend Confirmation:

Evaluates Directional Indicators (DI+ and DI-) to determine the trend direction.

Uses customizable ADX settings to filter out weak trends.

Provides uptrend, downtrend, or neutral signals based on strength conditions.

✅ Custom Symbol Comparison:

Allows users to compare two different assets (e.g., a stock vs. an index or ETF).

Displays a side-by-side comparison of volume dynamics and trend strength.

✅ User-Friendly Table Display:

Presents real-time calculations in a compact and structured table format.

Uses color-coded trend signals for easier interpretation.

Recommended Usage for Best Results:

📌 Pairing this indicator with Sri_Momentum and Sri(+) Pivot will enhance accuracy and provide better trade confirmations.

📌 Adding other major indicators like RSI, CCI, etc., will further increase the probability of winning trades.

How to Use:

Select a custom symbol for comparison.

Adjust ADX settings based on market conditions.

Analyze the table to identify buyer/seller dominance, OBV trends, and ADX trend strength.

Use the combined signals to confirm trade decisions and market direction.

Best Use Cases:

🔹 Trend Confirmation – Validate breakout or reversal signals.

🔹 Volume Strength Analysis – Assess buyer/seller participation before entering trades.

🔹 Multi-Asset Comparison – Compare the behavior of two related instruments.

This indicator is ideal for traders looking to combine volume dynamics with trend-following strategies. 🚀📈

Time of Day Background with Bar Count & TableDescription:

This indicator provides a comprehensive overview of market activity by dynamically displaying the time-of-day background and tracking bullish and bearish bar counts across different sessions. It also features a table summarizing the market performance for the last 7 days, segmented into four time-based sessions: Morning, Afternoon, Evening, and Night.

Key Features:

Time of Day Background:

The chart's background color changes based on the time of day:

Evening (12 AM - 6 AM) is shaded blue.

Morning (6 AM - 12 PM) is shaded aqua.

Afternoon (12 PM - 6 PM) is shaded yellow.

Night (6 PM - 12 AM) is shaded silver.

Bullish and Bearish Bar Counting:

It tracks the number of bullish (closing higher than opening) and bearish (closing lower than opening) candles.

The sum of the price differences (bullish minus bearish) for each session is displayed as a dynamic label, indicating overall market direction for each session.

Session Breakdown:

The chart is divided into four sessions, each lasting 6 hours (Morning, Afternoon, Evening, Night).

A new label is generated at the start of each session, indicating the bullish/bearish performance and the net difference in price movements for that session.

Historical Session Performance:

The indicator tracks and stores the performance for each session over the past 7 days.

A table is generated in the top-right corner of the chart, summarizing the performance for each session (Morning, Afternoon, Evening, Night) and the price changes for each of the past 7 days.

The values are color-coded to indicate positive (green) or negative (red) results.

Dynamic Table:

The table presents performance data for each time session over the past week with color-coded cells:

Green cells indicate positive performance.

Red cells indicate negative performance.

Empty cells represent no data for that session.

Use Case:

This indicator is useful for traders who want to track market activity and performance across different times of day and monitor how each session contributes to the overall market trend. It provides both visual insights (through background color) and numerical data (via the table) for better decision-making.

Settings:

The background color and session labels update automatically based on the time of day.

The table updates every day, tracking the performance of each session over the past week.

Vortex Candle MarkerVortex Candle Marker

The Vortex Candle Marker is a specialized TradingView indicator designed to identify and highlight **Vortex Candles**—candles that momentarily form without wicks on either the high or low. This unique price behavior can signal potential price retracements or reversals, aligning with the **Power of Three (PO3)** concept in price action theory.

Indicator Logic:

A candle is classified as a **Vortex Candle** if either of these conditions is met during its formation:

1. **Vortex Top:** The **high** equals either the **open** or **close**, indicating no upper wick.

2. **Vortex Bottom:** The **low** equals either the **open** or **close**, indicating no lower wick.

When a Vortex Candle is detected, the indicator changes the **candle border color** to **aqua**, making it easy to identify these significant price moments.

Market Insight & PO3 Interpretation:

In typical price behavior, most candles exhibit both upper and lower wicks, representing price exploration before settling at a closing value. A candle forming without a wick suggests **strong directional intent** at that moment. However, by the **Power of Three (PO3)** concept—Accumulation, Manipulation, and Distribution—such wickless formations often imply:

- **Price Reversion Likelihood:** When a candle temporarily forms without a wick, it suggests the market may **revisit the opening price** to establish a wick before the candle closes.

- **Liquidity Manipulation:** The absence of a wick may indicate a **stop-hunt** or liquidity grab, where the price manipulates one side before reversing.

- **Entry Triggers:** Identifying these moments can help traders anticipate potential **retracements** or **continuations** within the PO3 framework.

Practical Application

- **Early Reversal Detection:** Spot potential price reversals by observing wickless candles forming at key levels.

- **Breakout Validation:** Use Vortex Candles to confirm **true breakouts** or **false moves** before the price returns.

- **Liquidity Zones:** Identify areas where the market is likely to revisit to create a wick, signaling entry/exit points.

This indicator is a powerful tool for traders applying **Po3** methodologies and seeking to capture price manipulation patterns.

CAPM Alpha & BetaThe CAPM Alpha & Beta indicator is a crucial tool in finance and investment analysis derived from the Capital Asset Pricing Model (CAPM) . It provides insights into an asset's risk-adjusted performance (Alpha) and its relationship to broader market movements (Beta). Here’s a breakdown:

1. How Does It Work?

Alpha:

Definition: Alpha measures the portion of an investment's return that is not explained by market movements, i.e., the excess return over and above what the market is expected to deliver.

Purpose: It represents the value a fund manager or strategy adds (or subtracts) from an investment’s performance, adjusting for market risk.

Calculation:

Alpha is derived from comparing actual returns to expected returns predicted by CAPM:

Alpha = Actual Return − (Risk-Free Rate + β × (Market Return − Risk-Free Rate))

Alpha = Actual Return − (Risk-Free Rate + β × (Market Return − Risk-Free Rate))

Interpretation:

Positive Alpha: The investment outperformed its CAPM prediction (good performance for additional value/risk).

Negative Alpha: The investment underperformed its CAPM prediction.

Beta:

Definition: Beta measures the sensitivity of an asset's returns relative to the overall market's returns. It quantifies systematic risk.

Purpose: Indicates how volatile or correlated an investment is relative to the market benchmark (e.g., S&P 500).

Calculation:

Beta is computed as the ratio of the covariance of the asset and market returns to the variance of the market returns:

β = Covariance (Asset Return, Market Return) / Variance (Market Return)

β = Variance (Market Return) Covariance (Asset Return, Market Return)

Interpretation:

Beta = 1: The asset’s price moves in line with the market.

Beta > 1: The asset is more volatile than the market (higher risk/higher potential reward).

Beta < 1: The asset is less volatile than the market (lower risk/lower reward).

Beta < 0: The asset moves inversely to the market.

2. How to Use It?

Using Alpha:

Portfolio Evaluation: Investors use Alpha to gauge whether a portfolio manager or a strategy has successfully outperformed the market on a risk-adjusted basis.

If Alpha is consistently positive, the portfolio may deliver higher-than-expected returns for the given level of risk.

Stock/Asset Selection: Compare Alpha across multiple securities. Positive Alpha signals that the asset may be a good addition to your portfolio for excess returns.

Adjusting Investment Strategy: If Alpha is negative, reassess the asset's role in the portfolio and refine strategies.

Using Beta:

Risk Management:

A high Beta (e.g., 1.5) indicates higher sensitivity to market movements. Use such assets if you want to take on more risk during bullish market phases or expect higher returns.

A low Beta (e.g., 0.7) indicates stability and is useful in diversifying risk in volatile or bearish markets.

Portfolio Diversification: Combine assets with varying Betas to achieve the desired level of market responsiveness and smooth out portfolio volatility.

Monitoring Systematic Risk: Beta helps identify whether an investment aligns with your risk tolerance. For example, high-Beta stocks may not be suitable for conservative investors.

Practical Application:

Use both Alpha and Beta together:

Assess performance with Alpha (excess returns).

Assess risk exposure with Beta (market sensitivity).

Example: A stock with a Beta of 1.2 and a highly positive Alpha might suggest a solid performer that is slightly more volatile than the market, making it a suitable pick for risk-tolerant, return-maximizing investors.

In conclusion, the CAPM Alpha & Beta indicator gives a comprehensive view of an asset's performance and risk. Alpha enables performance evaluation on a risk-adjusted basis, while Beta reveals the level of market risk. Together, they help investors make informed decisions, build optimal portfolios, and align investments with their risk-return preferences.

ATR Percentages BoxThis custom indicator provides a quick visual reference for volatility-based price ranges, directly on your TradingView charts. It calculates and displays three ranges derived from the Daily Average True Range (ATR) with a standard 14-period setting:

5 Min (3% ATR): Ideal for very short-term scalping and quick intraday moves.

1 Hour (5% ATR): Useful for hourly setups, short-term trades, and intraday volatility assessment.

Day (10% ATR): Perfect for daily volatility context, swing trades, or placing stops and targets.

The ranges are clearly shown in a compact box at the top-right corner, providing traders immediate insights into realistic price movements, helping to optimise entries, stops, and profit targets efficiently.

Simple APF Strategy Backtesting [The Quant Science]Simple backtesting strategy for the quantitative indicator Autocorrelation Price Forecasting. This is a Buy & Sell strategy that operates exclusively with long orders. It opens long positions and generates profit based on the future price forecast provided by the indicator. It's particularly suitable for trend-following trading strategies or directional markets with an established trend.

Main functions

1. Cycle Detection: Utilize autocorrelation to identify repetitive market behaviors and cycles.

2. Forecasting for Backtesting: Simulate trades and assess the profitability of various strategies based on future price predictions.

Logic

The strategy works as follow:

Entry Condition: Go long if the hypothetical gain exceeds the threshold gain (configurable by user interface).

Position Management: Sets a take-profit level based on the future price.

Position Sizing: Automatically calculates the order size as a percentage of the equity.

No Stop-Loss: this strategy doesn't includes any stop loss.

Example Use Case

A trader analyzes a dayli period using 7 historical bars for autocorrelation.

Sets a threshold gain of 20 points using a 5% of the equity for each trade.

Evaluates the effectiveness of a long-only strategy in this period to assess its profitability and risk-adjusted performance.

User Interface

Length: Set the length of the data used in the autocorrelation price forecasting model.

Thresold Gain: Minimum value to be considered for opening trades based on future price forecast.

Order Size: percentage size of the equity used for each single trade.

Strategy Limit

This strategy does not use a stop loss. If the price continues to drop and the future price forecast is incorrect, the trader may incur a loss or have their capital locked in the losing trade.

Disclaimer!

This is a simple template. Use the code as a starting point rather than a finished solution. The script does not include important parameters, so use it solely for educational purposes or as a boilerplate.

*Auto Backtest & Optimize EngineFull-featured Engine for Automatic Backtesting and parameter optimization. Allows you to test millions of different combinations of stop-loss and take profit parameters, including on any connected indicators.

⭕️ Key Futures

Quickly identify the optimal parameters for your strategy.

Automatically generate and test thousands of parameter combinations.

A simple Genetic Algorithm for result selection.

Saves time on manual testing of multiple parameters.

Detailed analysis, sorting, filtering and statistics of results.

Detailed control panel with many tooltips.

Display of key metrics: Profit, Win Rate, etc..

Comprehensive Strategy Score calculation.

In-depth analysis of the performance of different types of stop-losses.

Possibility to use to calculate the best Stop-Take parameters for your position.

Ability to test your own functions and signals.

Customizable visualization of results.

Flexible Stop-Loss Settings:

• Auto ━ Allows you to test all types of Stop Losses at once(listed below).

• S.VOLATY ━ Static stop based on volatility (Fixed, ATR, STDEV).

• Trailing ━ Classic trailing stop following the price.

• Fast Trail ━ Accelerated trailing stop that reacts faster to price movements.

• Volatility ━ Dynamic stop based on volatility indicators.

• Chandelier ━ Stop based on price extremes.

• Activator ━ Dynamic stop based on SAR.

• MA ━ Stop based on moving averages (9 different types).

• SAR ━ Parabolic SAR (Stop and Reverse).

Advanced Take-Profit Options:

• R:R: Risk/Reward ━ sets TP based on SL size.

• T.VOLATY ━ Calculation based on volatility indicators (Fixed, ATR, STDEV).

Testing Modes:

• Stops ━ Cyclical stop-loss testing

• Pivot Point Example ━ Example of using pivot points

• External Example ━ Built-in example how test functions with different parameters

• External Signal ━ Using external signals

⭕️ Usage

━ First Steps:

When opening, select any point on the chart. It will not affect anything until you turn on Manual Start mode (more on this below).

The chart will immediately show the best results of the default Auto mode. You can switch Part's to try to find even better results in the table.

Now you can display any result from the table on the chart by entering its ID in the settings.

Repeat steps 3-4 until you determine which type of Stop Loss you like best. Then set it in the settings instead of Auto mode.

* Example: I flipped through 14 parts before I liked the first result and entered its ID so I could visually evaluate it on the chart.

Then select the stop loss type, choose it in place of Auto mode and repeat steps 3-4 or immediately follow the recommendations of the algorithm.

Now the Genetic Algorithm at the bottom right will prompt you to enter the Parameters you need to search for and select even better results.

Parameters must be entered All at once before they are updated. Enter recommendations strictly in fields with the same names.

Repeat steps 5-6 until there are approximately 10 Part's left or as you like. And after that, easily pour through the remaining Parts and select the best parameters.

━ Example of the finished result.

━ Example of use with Takes

You can also test at the same time along with Take Profit. In this example, I simply enabled Risk/Reward mode and immediately specified in the TP field Maximum RR, Minimum RR and Step. So in this example I can test (3-1) / 0.1 = 20 Takes of different sizes. There are additional tips in the settings.

━

* Soon you will start to understand how the system works and things will become much easier.

* If something doesn't work, just reset the engine settings and start over again.

* Use the tips I have left in the settings and on the Panel.

━ Details:

Sort ━ Sorting results by Score, Profit, Trades, etc..

Filter ━ Filtring results by Score, Profit, Trades, etc..

Trade Type ━ Ability to disable Long\Short but only from statistics.

BackWin ━ Backtest Window Number of Candle the script can test.

Manual Start ━ Enabling it will allow you to call a Stop from a selected point. which you selected when you started the engine.

* If you have a real open position then this mode can help to save good Stop\Take for it.

1 - 9 Сheckboxs ━ Allow you to disable any stop from Auto mode.

Ex Source - Allow you to test Stops/Takes from connected indicators.

Connection guide:

//@version=6

indicator("My script")

rsi = ta.rsi(close, 14)

buy = not na(rsi) and ta.crossover (rsi, 40) // OS = 40

sell = not na(rsi) and ta.crossunder(rsi, 60) // OB = 60

Signal = buy ? +1 : sell ? -1 : 0

plot(Signal, "🔌Connector🔌", display = display.none)

* Format the signal for your indicator in a similar style and then select it in Ex Source.

⭕️ How it Works

Hypothesis of Uniform Distribution of Rare Elements After Mixing.

'This hypothesis states that if an array of N elements contains K valid elements, then after mixing, these valid elements will be approximately uniformly distributed.'

'This means that in a random sample of k elements, the proportion of valid elements should closely match their proportion in the original array, with some random variation.'

'According to the central limit theorem, repeated sampling will result in an average count of valid elements following a normal distribution.'

'This supports the assumption that the valid elements are evenly spread across the array.'

'To test this hypothesis, we can conduct an experiment:'

'Create an array of 1,000,000 elements.'

'Select 1,000 random elements (1%) for validation.'

'Shuffle the array and divide it into groups of 1,000 elements.'

'If the hypothesis holds, each group should contain, on average, 1~ valid element, with minor variations.'

* I'd like to attach more details to My hypothesis but it won't be very relevant here. Since this is a whole separate topic, I will leave the minimum part for understanding the engine.

Practical Application

To apply this hypothesis, I needed a way to generate and thoroughly mix numerous possible combinations. Within Pine, generating over 100,000 combinations presents significant challenges, and storing millions of combinations requires excessive resources.

I developed an efficient mechanism that generates combinations in random order to address these limitations. While conventional methods often produce duplicates or require generating a complete list first, my approach guarantees that the first 10% of possible combinations are both unique and well-distributed. Based on my hypothesis, this sampling is sufficient to determine optimal testing parameters.

Most generators and randomizers fail to accommodate both my hypothesis and Pine's constraints. My solution utilizes a simple Linear Congruential Generator (LCG) for pseudo-randomization, enhanced with prime numbers to increase entropy during generation. I pre-generate the entire parameter range and then apply systematic mixing. This approach, combined with a hybrid combinatorial array-filling technique with linear distribution, delivers excellent generation quality.

My engine can efficiently generate and verify 300 unique combinations per batch. Based on the above, to determine optimal values, only 10-20 Parts need to be manually scrolled through to find the appropriate value or range, eliminating the need for exhaustive testing of millions of parameter combinations.

For the Score statistic I applied all the same, generated a range of Weights, distributed them randomly for each type of statistic to avoid manual distribution.

Score ━ based on Trade, Profit, WinRate, Profit Factor, Drawdown, Sharpe & Sortino & Omega & Calmar Ratio.

⭕️ Notes

For attentive users, a little tricks :)

To save time, switch parts every 3 seconds without waiting for it to load. After 10-20 parts, stop and wait for loading. If the pause is correct, you can switch between the rest of the parts without loading, as they will be cached. This used to work without having to wait for a pause, but now it does slower. This will save a lot of time if you are going to do a deeper backtest.

Sometimes you'll get the error “The scripts take too long to execute.”

For a quick fix you just need to switch the TF or Ticker back and forth and most likely everything will load.

The error appears because of problems on the side of the site because the engine is very heavy. It can also appear if you set too long a period for testing in BackWin or use a heavy indicator for testing.

Manual Start - Allow you to Start you Result from any point. Which in turn can help you choose a good stop-stick for your real position.

* It took me half a year from idea to current realization. This seems to be one of the few ways to build something automatic in backtest format and in this particular Pine environment. There are already better projects in other languages, and they are created much easier and faster because there are no limitations except for personal PC. If you see solutions to improve this system I would be glad if you share the code. At the moment I am tired and will continue him not soon.

Also You can use my previosly big Backtest project with more manual settings(updated soon)