Iron Bot Statistical Trend Filter📌 Iron Bot Statistical Trend Filter

📌 Overview

Iron Bot Statistical Trend Filter is an advanced trend filtering strategy that combines statistical methods with technical analysis.

By leveraging Z-score and Fibonacci levels, this strategy quantitatively analyzes market trends to provide high-precision entry signals.

Additionally, it includes an optional EMA filter to enhance trend reliability.

Risk management is reinforced with Stop Loss (SL) and four Take Profit (TP) levels, ensuring a balanced approach to risk and reward.

📌 Key Features

🔹 1. Statistical Trend Filtering with Z-Score

This strategy calculates the Z-score to measure how much the price deviates from its historical mean.

Positive Z-score: Indicates a statistically high price, suggesting a strong uptrend.

Negative Z-score: Indicates a statistically low price, signaling a potential downtrend.

Z-score near zero: Suggests a ranging market with no strong trend.

By using the Z-score as a filter, market noise is reduced, leading to more reliable entry signals.

🔹 2. Fibonacci Levels for Trend Reversal Detection

The strategy integrates Fibonacci retracement levels to identify potential reversal points in the market.

High Trend Level (Fibo 23.6%): When the price surpasses this level, an uptrend is likely.

Low Trend Level (Fibo 78.6%): When the price falls below this level, a downtrend is expected.

Trend Line (Fibo 50%): Acts as a midpoint, helping to assess market balance.

This allows traders to visually confirm trend strength and turning points, improving entry accuracy.

🔹 3. EMA Filter for Trend Confirmation (Optional)

The strategy includes an optional 200 EMA (Exponential Moving Average) filter for trend validation.

Price above 200 EMA: Indicates a bullish trend (long entries preferred).

Price below 200 EMA: Indicates a bearish trend (short entries preferred).

Enabling this filter reduces false signals and improves trend-following accuracy.

🔹 4. Multi-Level Take Profit (TP) and Stop Loss (SL) Management

To ensure effective risk management, the strategy includes four Take Profit levels and a Stop Loss:

Stop Loss (SL): Automatically closes trades when the price moves against the position by a certain percentage.

TP1 (+0.75%): First profit-taking level.

TP2 (+1.1%): A higher probability profit target.

TP3 (+1.5%): Aiming for a stronger trend move.

TP4 (+2.0%): Maximum profit target.

This system secures profits at different stages and optimizes risk-reward balance.

🔹 5. Automated Long & Short Trading Logic

The strategy is built using Pine Script®’s strategy.entry() and strategy.exit(), allowing fully automated trading.

Long Entry:

Price is above the trend line & high trend level.

Z-score is positive (indicating an uptrend).

(Optional) Price is also above the EMA for stronger confirmation.

Short Entry:

Price is below the trend line & low trend level.

Z-score is negative (indicating a downtrend).

(Optional) Price is also below the EMA for stronger confirmation.

This logic helps filter out unnecessary trades and focus only on high-probability entries.

📌 Trading Parameters

This strategy is designed for flexible capital management and risk control.

💰 Account Size: $5000

📉 Commissions and Slippage: Assumes 94 pips commission per trade and 1 pip slippage.

⚖️ Risk per Trade: Adjustable, with a default setting of 1% of equity.

These parameters help preserve capital while optimizing the risk-reward balance.

📌 Visual Aids for Clarity

To enhance usability, the strategy includes clear visual elements for easy market analysis.

✅ Trend Line (Blue): Indicates market midpoint and helps with entry decisions.

✅ Fibonacci Levels (Yellow): Highlights high and low trend levels.

✅ EMA Line (Green, Optional): Confirms long-term trend direction.

✅ Entry Signals (Green for Long, Red for Short): Clearly marked buy and sell signals.

These features allow traders to quickly interpret market conditions, even without advanced technical analysis skills.

📌 Originality & Enhancements

This strategy is developed based on the IronXtreme and BigBeluga indicators,

combining a unique Z-score statistical method with Fibonacci trend analysis.

Compared to conventional trend-following strategies, it leverages statistical techniques

to provide higher-precision entry signals, reducing false trades and improving overall reliability.

📌 Summary

Iron Bot Statistical Trend Filter is a statistically-driven trend strategy that utilizes Z-score and Fibonacci levels.

High-precision trend analysis

Enhanced accuracy with an optional EMA filter

Optimized risk management with multiple TP & SL levels

Visually intuitive chart design

Fully customizable parameters & leverage support

This strategy reduces false signals and helps traders ride the trend with confidence.

Try it out and take your trading to the next level! 🚀

Statistics

Broad Market MOEX non normalazeBroad Market MOEX - Relative Strength Indicator for MOEX Stocks

This indicator allows you to compare the price dynamics of major Moscow Exchange stocks relative to the selected asset during the trading session.

Features:

• Tracks 10 key MOEX stocks: Sberbank, Rosneft, Lukoil, Gazprom Neft, NOVATEK, Nornickel, Polyus, Tatneft, Surgutneftegas, Severstal

• Shows the percentage price change of each stock relative to the base price at the start of trading (default 9:00 MSK)

• Allows you to customize the base time for reference

• Clearly displays the strength and weakness of individual stocks relative to each other

• Helps identify leaders and laggards during the trading session

How to use:

1. Add the indicator to any MOEX stock chart

2. Adjust the base time if needed (default 9:00)

3. Monitor the relative dynamics of stocks

4. Use for:

- Finding strong/weak stocks

- Identifying sector rotation

- Intraday trading

- Correlation analysis

Color coding of lines helps easily identify each stock on the chart.

The indicator is useful for intraday traders and anyone monitoring the relative strength of stocks on the Moscow Exchange.

US vs EU Interest Rate SpreadThis script plots the difference (Spread) between the US-Interest Rate (Symbol USINTR) and the EU Interest Rate (Symbol: EUINTR) and plots it in a seperate pane. Areas where the background is green are times were the spread was positive (US interest rate higher than EU interest rate), a red background indicates a higher EU interest rate than US interest rate.

Crypto Candle Low Leverage TrackerCrypto Candle Low Leverage Tracker

The Candle Low Leverage Indicator is a powerful tool for long position traders seeking to manage risk effectively when using leverage. By evaluating the current candle's low price, this indicator helps traders make more informed decisions about potential entry points, stop losses, and leverage levels. The indicator matches the low of the candle to the leverage needed for liquidation, giving you a clear view of how leverage impacts your position.

This indicator provides two critical insights:

% from Candle Low: Tracks how much the price has moved from the low of the current candle. For long position traders, this percentage is crucial for understanding how far the price has come off the low and deciding whether it’s safe to enter a position or if further price action is needed.

Leverage Needed: Estimates the leverage required to reach the candle's low as the liquidation price. Long traders can use this information to adjust leverage to a safer level, ensuring they don’t overexpose themselves to liquidation risks by matching leverage to the candle’s low.

Key Features:

Customizable table positioning (top, middle, bottom).

Toggle options to show/hide % from Candle Low and Leverage Needed.

Visual indicators with color changes: green for positive change, red for negative change, and blue for leverage requirements.

Ideal for long traders, this tool helps evaluate market conditions, manage risks, and calculate the best leverage to use in long trades, ensuring that leverage aligns with the candle’s low to prevent unnecessary liquidations.

Gap Detection Indicator V.1This indicator is designed to detect gaps between candles on the chart. It detects all gaps that are higher than the specified percentage setting, draws a line passing through only the starting and ending points of the last gap, and paints between these lines.

If any candle closes above the gap starting level, the lines between the lines are colored green; If any candle closes below the gap starting level, the lines between the lines are colored red.

UPDATE1:

In addition, two more gap levels were added. A date range was added to enable control within the specified date range.

Triad Trade MatrixOverview

Triad Trade Matrix is an advanced multi-strategy indicator built using Pine Script v5. It is designed to simultaneously track and display key trading metrics for three distinct trading styles on a single chart:

Swing Trading (Swing Supreme):

This mode captures longer-term trends and is designed for trades that typically span several days. It uses customizable depth and deviation parameters to determine swing signals.

Day Trading (Day Blaze):

This mode focuses on intraday price movements. It generates signals that are intended to be executed within a single trading session. The parameters for depth and deviation are tuned to capture more frequent, shorter-term moves.

Scalping (Scalp Surge):

This mode is designed for very short-term trades where quick entries and exits are key. It uses more sensitive parameters to detect rapid price movements suitable for scalping strategies.

Each trading style is represented by its own merged table that displays real-time metrics. The tables update automatically as new trading signals are generated.

Key Features

Multi-Style Tracking:

Swing Supreme (Large): For swing trading; uses a purple theme.

Day Blaze (Medium): For day trading; uses an orange theme.

Scalp Surge (Small): For scalping; uses a green theme.

Real-Time Metrics:

Each table displays key trade metrics including:

Entry Price: The price at which the trade was entered.

Exit Price: The price at which the previous trade was exited.

Position Size: Calculated as the account size divided by the entry price.

Direction: Indicates whether the trade is “Up” (long) or “Down” (short).

Time: The time when the trade was executed (formatted to hours and minutes).

Wins/Losses: The cumulative number of winning and losing trades.

Current Price & PnL: The current price on the chart and the profit/loss computed relative to the entry price.

Duration: The number of bars that the trade has been open.

History Column: A merged summary column that shows the most recent trade’s details (entry, exit, and result).

Customizability:

Column Visibility: Users can toggle individual columns (Ticker, Timeframe, Entry, Exit, etc.) on or off according to their preference.

Appearance Settings: You can customize the table border width, frame color, header background, and text colors.

History Toggle: The merged history column can be enabled or disabled.

Chart Markers: There is an option to show or hide chart markers (labels and lines) that indicate trade entries and exits on the chart.

Trade History Management:

The indicator maintains a rolling history (up to three recent trades per trading style) and displays the latest summary in the merged table.

This history column provides a quick reference to recent performance.

How It Works

Signal Generation & Trade Metrics

Trade Entry/Exit Calculation:

For each trading style, the indicator uses built-in functions (such as ta.lowestbars and ta.highestbars) to analyze price movements. Based on a customizable "depth" and "deviation" parameter, it determines the point of entry for a trade.

Swing Supreme: Uses larger depth/deviation values to capture swing trends.

Day Blaze: Uses intermediate values for intraday moves.

Scalp Surge: Uses tighter parameters to pick up rapid price changes.

Metrics Update:

When a new trade signal is generated (i.e., when the trade entry price is updated), the indicator calculates:

The current PnL as the difference between the current price and the entry price (or vice versa, depending on the trade direction).

The duration as the number of bars since the trade was opened.

The position size using the formula: accountSize / entryPrice.

History Recording:

Each time a new trade is triggered (i.e., when the entry price is updated), a summary string is created (showing entry, exit, and win/loss status) and appended to the corresponding trade history array. The merged table then displays the latest summary from this history.

Table Display

Merged Table Structure:

Each trading style (Swing Supreme, Day Blaze, and Scalp Surge) is represented by a table that has 15 columns. The columns are:

Trade Type (e.g., Swing Supreme)

Ticker

Timeframe

Entry Price

Exit Price

Position Size

Direction

Time of Entry

Account Size

Wins

Losses

Current Price

Current PnL

Duration (in bars)

History (the latest trade summary)

User Customization:

Through the settings panel, users can choose which columns to display.

If a column is toggled off, its cells will remain blank, allowing traders to focus on the metrics that matter most to them.

Appearance & Themes:

The table headers and cell backgrounds are customizable via color inputs. The trading style names are color-coded:

Swing Supreme (Large): Uses a purple theme.

Day Blaze (Medium): Uses an orange theme.

Scalp Surge (Small): Uses a green theme.

How to Use the Indicator

Add the Indicator to Your Chart:

Once published, add "Triad Trade Matrix" to your TradingView chart.

Configure the Settings:

Adjust the Account Size to match your trading capital.

Use the Depth and Deviation inputs for each trading style to fine-tune the signal sensitivity.

Toggle the Chart Markers on if you want visual entry/exit markers on the chart.

Customize which columns are visible via the column visibility toggles.

Enable or disable the History Column to show the merged trade history in the table.

Adjust the appearance settings (colors, border width, etc.) to suit your chart background and preferences.

Interpret the Tables:

Swing Supreme:

This table shows metrics for swing trades.

Look for changes in entry price, PnL, and trade duration to monitor longer-term moves.

Day Blaze:

This table tracks day trading activity.It will update more frequently, reflecting intraday trends.

Scalp Surge:

This table is dedicated to scalping signals.Use it to see quick entry/exit data and rapid profit/loss changes.

The History column (if enabled) gives you a snapshot of the most recent trade (e.g., "E:123.45 X:124.00 Up Win").

Use allerts:

The indicator includes alert condition for new trade entries(both long and short)for each trading style.

Summary:

Triad Trade Matrix provides an robust,multi-dimensional view of your trading performance across swing trading, day trading, and scalping.

Best to be used whith my other indicators

True low high

Vma Ext_Adv_CustomTbl

This indicator is ideal for traders who wish to monitor multiple trading styles simultaneously, with a clear, technical, and real-time display of performance metrics.

Happy Trading!

Ultimate Volatility Scanner by NHBprod - Requested by Client!Hey Everyone!

I created another script to add to my growing library of strategies and indicators that I use for automated crypto and stock trading! This strategy is for BITCOIN but can be used on any stock or crypto. This was requested by a client so I thought I should create it and hopefully build off of it and build variants!

This script gets and compares the 14-day volatility using the ATR percentage for a list of cryptocurrencies and stocks. Cryptocurrencies are preloaded into the script, and the script will show you the TOP 5 coins in terms of volatility, and then compares it to the Bitcoin volatility as a reference. It updates these values once per day using daily timeframe data from TradingView. The coins are then sorted in descending order by their volatility.

If you don't want to use the preloaded set of coins, you have the option of inputting your own coins AND/OR stocks!

Let me know your thoughts.

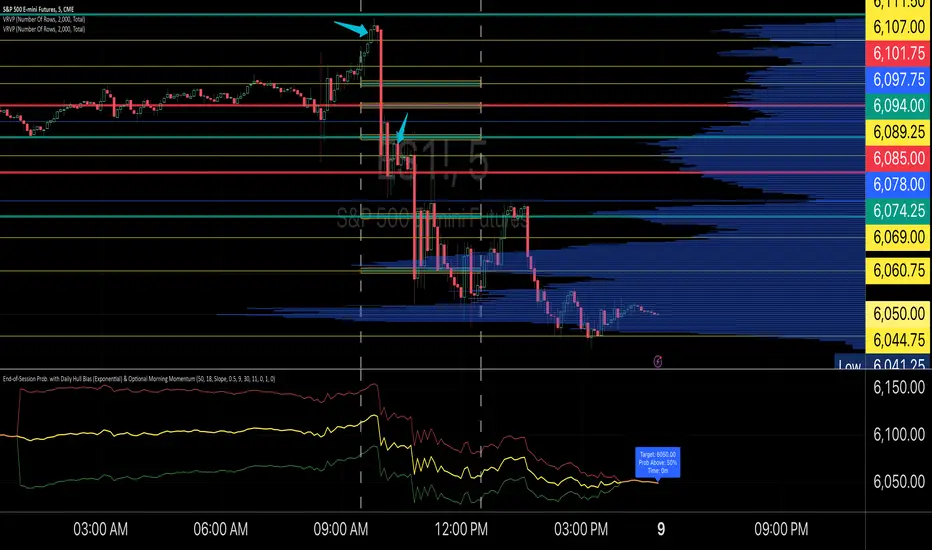

End-of-Session ProbabilityThis indicator estimates the probability that the market will finish the session above a specified target price. It blends a statistical probability model with directional bias and optional morning momentum weighting to help traders gauge end-of-day market expectations.

Key Features:

• Statistical Probability Model:

Uses a normal distribution (with a custom normal CDF approximation) scaled by the square-root-of-time rule. The indicator dynamically adjusts the standard deviation for the remaining session time to compute a z‑score and ultimately the probability that the session close exceeds the target.

• Directional Bias via Daily HullMA (Exponential):

A daily Hull Moving Average (calculated using an exponential method) is used as a big-picture trend indicator. The model allows you to select your bias method—either by comparing the current price to the daily HullMA (Price method) or by using the HullMA’s slope (Slope method). A drift multiplier scales this bias, which then shifts the mean used in the probability calculations.

• Optional Morning Momentum Weight:

For traders who believe that early session moves provide useful clues about the day’s momentum, you can enable an optional weighting. The indicator captures the percentage change from the morning open (within a user-defined time window) and adjusts the expected move accordingly. A multiplier lets you control the strength of this adjustment.

• Visual Outputs:

The indicator plots quantile lines (approximately the 25%, 50%, and 75% levels) for the expected price distribution at session end. An abbreviated on-chart label displays key information:

• Target: The target price (current price plus a user-defined offset)

• Prob Above: The probability (in percentage) that the session close will exceed the target price

• Time: The time remaining in the session (in minutes)

How to Use:

1. Set Your Parameters:

• Expected Session Move: Input your estimated standard deviation for the full-session move in price units.

• Daily Hull MA Settings: Adjust the period for the daily HullMA and choose the bias method (Price or Slope). Modify the drift multiplier to tune the strength of the directional bias.

• Target Offset: Specify an offset from the current price to set your target level.

• Morning Momentum (Optional): Enable the morning momentum weight if you want the indicator to adjust the expected move based on early session price changes. Define the morning session window and set the momentum multiplier.

2. Interpret the Output:

• Quantile Lines: These represent the range of possible end-of-session prices based on your model.

• Abbreviated Label: Provides a quick snapshot of the target price, probability of finishing above that target, and time remaining in the session.

3. Trading Application:

Use the probability output as a guide to assess if the market is likely to continue in the current direction or reverse by session close. The indicator can help you decide on trade entries, exits, or adjustments based on your overall strategy and risk management approach.

This tool is designed to offer a dynamic, statistically driven snapshot of the market’s expected end-of-day behavior, combining both longer-term trend bias and short-term momentum cues.

Buyable Gap Ups (BGU) ScreenerBuyable Gap Ups (BGU) Screener

This custom indicator detects Buyable Gap Ups (BGU), designed to identify stocks with significant price movements driven by gap-ups, often signaling strong bullish momentum. It helps traders spot potential opportunities where a stock has gapped up above the previous day's high with increased volume, suggesting the possibility of continued price strength.

Key Features:

Gap Percentage Threshold: Set a minimum gap percentage required for a valid buyable gap-up.

Volume Change Threshold: Identifies gap-ups accompanied by a significant increase in volume compared to the 50-day average.

ATR-Based Gap Detection (Optional): Use Average True Range (ATR) to determine whether the gap is large enough, factoring in recent volatility.

Customizable Lookback Period: Adjust the number of recent bars to track the frequency of BGU occurrences.

Volume Confirmation: Only signals buyable gaps when volume surpasses a defined threshold above the 50-day average.

Input Parameters:

Gap Percentage Threshold: Adjusts the minimum percentage gap for a valid signal.

Volume Change Threshold: Determines the minimum percentage increase in volume compared to the 50-day moving average.

Use ATR Gap: Option to use ATR to determine the minimum gap size instead of the percentage gap.

ATR Multiplier for Gap: Customizes the gap size based on the ATR.

ATR Length: Adjusts the lookback period for calculating ATR.

Lookback Period for BGU: Set the number of bars over which to calculate the BGU count.

Alerts & Signals:

The script will plot signals below bars where a valid BGU condition is met.

Alerts can be set for when a BGU is detected, giving real-time notifications for potential trading opportunities.

This indicator is designed to help traders find stocks showing strong bullish momentum, especially after earnings or other market-moving events, with the potential for continued uptrend. It is ideal for those looking to incorporate gap-based strategies in their trading.

Precious Metals & GSR (Zeiierman)█ Overview

The Precious Metals & GSR (Zeiierman) is designed to provide traders and investors with a comprehensive view of the Gold-Silver Ratio (GSR) and other precious metal relationships. This tool helps evaluate the relative strength between different metals by analyzing their price ratios over historical periods, using quantile-based analysis and trend interpretation tables to highlight key insights.

The Gold-Silver Ratio (GSR) is a widely utilized metric in precious metals trading, representing the number of silver ounces required to purchase one ounce of gold. Historically, this ratio has fluctuated, providing traders with insights into the relative value of these two metals. By analyzing the GSR, traders can identify potential trading opportunities based on historical patterns and market dynamics.

By integrating customizable percentile bands, gradient coloring for performance visualization, and dynamic ratio analysis, this indicator assists in understanding how one metal is performing relative to another, making it useful for trend tracking, risk management, and portfolio allocation.

█ How It Works

The Precious Metals & GSR Indicator operates by fetching the latest prices of the selected precious metals in the user's chosen currency. It then calculates the ratio between two selected metals (Metal 1 and Metal 2) and analyzes this ratio over a specified period. By computing quantile bands and high/low bands, the indicator provides insights into the historical performance and current standing of the ratio.

⚪ Ratio Calculation

The core of this indicator is the metal ratio, calculated by dividing the price of Metal 1 by Metal 2.

A rising ratio means Metal 1 is outperforming Metal 2.

A falling ratio means Metal 2 is outperforming Metal 1.

The indicator automatically retrieves live market prices of Gold, Silver, Platinum, and Palladium to compute the ratio.

⚪ Quantile Ratio Bands

The indicator calculates the highest (max) and lowest (min) ratio levels over a user-defined period.

It also plots quantile bands at the 10th, 25th, 50th (median), 75th, and 90th percentiles, providing deeper statistical insights into how extreme or average the current ratio is.

The median (Q50) acts as a reference level, showing whether the ratio is above or below its historical midpoint.

⚪ Interpretation Table

The Ratio Interpretation Table provides a text-based summary of the ratio’s strength.

It detects whether Metal 1 is at a historical high, low, or within common ranges.

This helps traders and investors make informed decisions on whether the ratio is overextended, mean-reverting, or trending.

⚪ Precious Metals Table

Displays live market prices for Gold, Silver, Platinum, and Palladium.

Prices are shown in different units (oz, kg, grams, and troy ounces) based on user preferences.

A color-coded system highlights price changes, making it easier to track market movements.

⚪ Physical Holding Calculator

Users can enter their precious metal holdings to estimate their current value.

The system adjusts calculations based on weight, purity (24K, 22K, etc.), and unit of measurement.

The holding value is displayed in the selected currency (USD, EUR, GBP, etc.).

█ How to Use

⚪ Trend Identification

If the ratio is increasing, Metal 1 is gaining strength relative to Metal 2 → Possible Long Position on Metal 1 / Short on Metal 2

If the ratio is decreasing, Metal 2 is gaining strength relative to Metal 1 → Possible Short Position on Metal 1 / Long on Metal 2

⚪ Mean Reversion Strategy

When the ratio reaches the 90th percentile, Metal 1 is historically overextended (expensive) compared to Metal 2.

Traders may look to sell Metal 1 and buy Metal 2, expecting the ratio to decline back toward its historical average.

Example (Gold/Silver Ratio): If the GSR is above the 90th percentile, gold is very expensive relative to silver, suggesting a potential buying opportunity in silver and/or a selling opportunity in gold.

When the ratio reaches the 10th percentile, Metal 1 is historically undervalued (cheap) compared to Metal 2.

Traders may look to buy Metal 1 and sell Metal 2, expecting the ratio to rise back toward its historical average.

Example (Gold/Silver Ratio): If the GSR is below the 10th percentile, gold is very cheap relative to silver, suggesting a potential buying opportunity in gold and/or a selling opportunity in silver.

⚪ Common Strategy Based on GSR Insights

A common approach involves monitoring the ratio for extreme values based on historical data. When the ratio reaches historically high levels, it suggests that gold is expensive relative to silver, potentially indicating a buying opportunity for silver and/or a selling opportunity for gold. Conversely, when the ratio is at historically low levels, silver is expensive relative to gold, suggesting a potential buying opportunity for gold and/or selling opportunity for silver. This mean-reversion strategy relies on the tendency of the GSR to return to its historical average over time.

⚪ Hedging & Portfolio Diversification

If Gold is strongly outperforming Silver, investors may shift allocations to balance risk.

If Silver is rapidly gaining on Gold, it may indicate increased industrial demand or speculative interest.

⚪ Inflation & Economic Cycles

A rising Gold-Silver ratio often correlates with economic downturns and increased risk aversion.

A falling Gold-Silver ratio may signal stronger economic growth and higher inflation expectations.

█ Settings

Precious Metals Table

Select which metals to display (Gold, Silver, Platinum, Palladium)

Choose measurement units (oz, kg, grams, troy ounces)

Ratio Analysis

Select Metal 1 & Metal 2 for ratio calculation

Set historical length for quantile calculations

Interpretation Table

Enable automated insights based on ratio levels

Physical Holdings Calculator

Enter metal weight, purity, and unit

Select calculation currency

-----------------

Disclaimer

The content provided in my scripts, indicators, ideas, algorithms, and systems is for educational and informational purposes only. It does not constitute financial advice, investment recommendations, or a solicitation to buy or sell any financial instruments. I will not accept liability for any loss or damage, including without limitation any loss of profit, which may arise directly or indirectly from the use of or reliance on such information.

All investments involve risk, and the past performance of a security, industry, sector, market, financial product, trading strategy, backtest, or individual's trading does not guarantee future results or returns. Investors are fully responsible for any investment decisions they make. Such decisions should be based solely on an evaluation of their financial circumstances, investment objectives, risk tolerance, and liquidity needs.

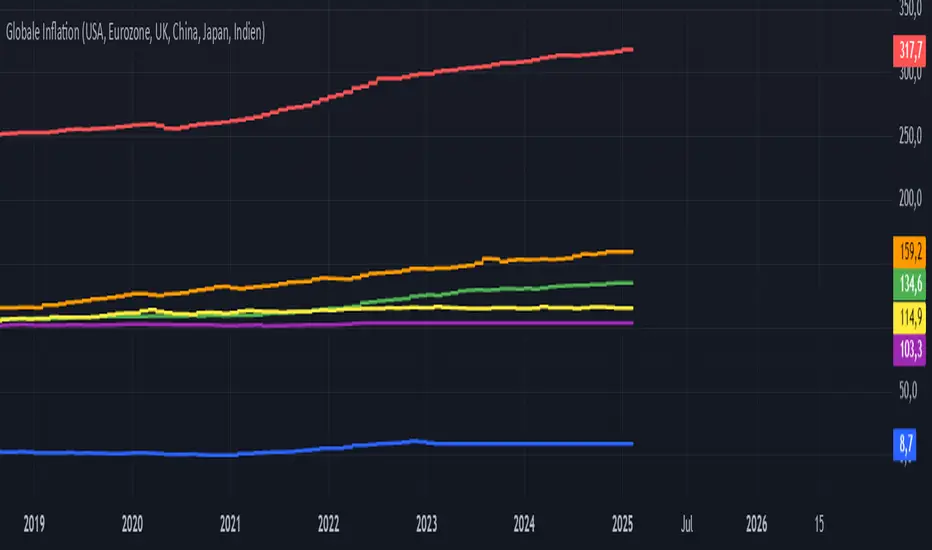

Global Inflation Indicator🔹 Overview:

The Global Inflation Indicator is a macro-analysis tool designed to track and compare inflation trends across major economies. It pulls Consumer Price Index (CPI) data from multiple regions, helping traders and investors analyze how inflation impacts global markets, particularly gold, forex, and commodities.

📊 Key Features:

✅ Tracks inflation in six major economies:

🇺🇸 USA (CPIAUCSL) – Key driver for USD and gold prices

🇪🇺 Eurozone (CPHPTT01EZM659N) – Euro inflation impact

🇬🇧 United Kingdom (GBRCPIALLMINMEI) – GBP & economic trends

🇨🇳 China (CHNCPIALLMINMEI) – Emerging market impact

🇯🇵 Japan (JPNCPIALLMINMEI) – Yen & inflation control policies

🇮🇳 India (INDCPIALLMINMEI) – Key gold-consuming economy

✅ Real-time Inflation Trends:

Provides a visual comparison of inflation levels in different regions.

Helps traders identify inflationary cycles & their effect on global assets.

✅ Macro-Driven Trading Decisions:

Gold & Forex Correlation: High inflation may increase demand for gold.

Interest Rate Expectations: Central banks respond to inflation shifts.

Currency Strength: Inflation impacts USD, EUR, GBP, JPY, CNY, INR.

📉 How to Use It:

Gold traders can assess inflation trends to predict potential price movements.

Forex traders can compare inflation effects on major currency pairs (EUR/USD, USD/JPY, GBP/USD, etc.).

Stock investors can evaluate how inflation affects central bank policies and interest rates.

📌 Conclusion:

The Global Inflation Indicator is a powerful tool for macroeconomic analysis, providing real-time insights into global inflation trends. By integrating this indicator into your gold, forex, and commodity trading strategies, you can make more informed investment decisions in response to economic changes.

Share SizeA helpful tool that estimates the amount of times you can trade at your current share size in a small account.

You can adjust the numbers in the settings page!

EMA Crossover Backtest [BarScripts]This indicator lets you backtest an EMA crossover strategy with built-in risk management and trade tracking. It simulates long and short trades based on EMA crossovers, allowing you to fine-tune entry conditions, stop-loss placement, and reward/risk settings.

🔹 How It Works:

Long Entry: Fast EMA crosses above Slow EMA, and price closes above Fast EMA.

Short Entry: Fast EMA crosses below Slow EMA, and price closes below Fast EMA.

Stop Loss: Set based on previous bars or a fixed amount.

Take Profit: Adjustable reward/risk ratio.

Higher Timeframe Confluence: Confirms trades based on a larger timeframe.

Trade Hours Filter: Limits trades to specific time windows.

🔹 Key Features:

✅ Shows Entry & Exit Points with visual trade lines.

✅ Customizable EMA Lengths to fit any strategy.

✅ P&L Tracking & Statistics to measure performance.

✅ Position Sizing Options: Fixed position, fixed risk, or percentage of balance.

✅ Commissions Tracking (based on total trades, not contracts).

Use this tool to fine-tune your EMA crossover strategy and see how it performs over time! 🚀

💬 Let me know your feedback—suggest improvements, report issues, or request new features!

Naive Bayes Candlestick Pattern Classifier v1.1 BETAAn intermezzo on why i made this script publication..

A : Candlestick Pattern took hours to backtest, why not using Machine Learning techniques?

B : Machine Learning, no that's gonna be really heavy bro!

A : Not really, because we use Naive Bayes.

B : The simplest, yet powerful machine learning algorithm to separate (a.k.a classify) multivariate data.

----------------------------------------------------------------------------------------------------------------------

Hello, everyone!

After deep research in extracting meaningful information from the market, I ended up building this powerful machine learning indicator based on the evolution of Bayesian Statistics. This indicator not only leverages the simplicity of Naive Bayes but also extends its application to candlestick pattern analysis, making it an invaluable tool for traders who are looking to enhance their technical analysis without spending countless hours manually backtesting each pattern on each market!.

What most interesting part is actually after learning all of likely useless methods like fibonacci, supply and demand, volume profile, etc. We always ended up back to basic like support and resistance and candlestick patterns, but with a slight twist on strategy algorithm design and statistical approach. Thus, the only reason why i made this, because i exactly know that you guys will ended up in this position as time goes by.

The essence of this indicator lies in its ability to automate the recognition and statistical evaluation of various candlestick patterns. Traditionally, traders have relied on visual inspection and manual backtesting to determine the effectiveness of patterns like Bullish Engulfing, Bearish Engulfing, Harami variations, Hammer formations, and even more complex multi-candle patterns such as Three White Soldiers, Three Black Crows, Dark Cloud Cover, and Piercing Pattern. However, these conventional methods are both time-consuming and prone to subjective bias.

To address these challenges, I employed Naive Bayes—a probabilistic classifier that, despite its simplicity, offers robust performance in various domains. Naive Bayes assumes that each feature is independent of the others given the class label, which, although a strong assumption, works remarkably well in practice, especially when the dataset is large like market data and the feature space is high-dimensional. In our case, each candlestick pattern acts as a feature that can be statistically evaluated based on its historical performance. The indicator calculates a probability that a given pattern will lead to a price reversal, by comparing the pattern’s close price to the highest or lowest price achieved in a lookahead window.

One of the standout features of this script is its flexibility. Each candlestick pattern is not only coded into the system but also comes with individual toggles to enable or disable them based on your trading strategy. This means you can choose to focus on single-candle patterns like Bullish Engulfing or more complex multi-candle formations such as Three White Soldiers, without modifying the core code. The built-in customization options allow you to adjust colors and labels for each pattern, giving you the freedom to tailor the visual output to your preference. This level of customization ensures that the indicator integrates seamlessly into your existing TradingView setup.

Moreover, the indicator isn’t just about pattern recognition—it also incorporates outcome-based learning. Every time a pattern is detected, it looks ahead a predefined number of bars to evaluate if the expected reversal actually materialized. This outcome is then stored in arrays, and over time, the script dynamically calculates the probability of success for each pattern. These probabilities are presented in a real-time updating table on your chart, which shows not only the percentage probability but also the count of historical occurrences. With this information at your fingertips, you can quickly gauge the reliability of each pattern in your chosen market and timeframe.

Another significant advantage of this approach is its speed and efficiency. While more complex machine learning models like neural networks might require heavy computational resources and longer training times, the Naive Bayes classifier in this script is lightweight, instantaneous and can be updated on the fly with each new bar. This real-time capability is essential for modern traders who need to make quick decisions in fast-paced markets.

Furthermore, by automating the process of backtesting, the indicator frees up your time to focus on other aspects of trading strategy development. Instead of manually analyzing hundreds or even thousands of candles, you can rely on the statistical power of Naive Bayes to provide you with insights on which patterns are most likely to result in profitable moves. This not only enhances your efficiency but also helps to eliminate the cognitive biases that often plague manual analysis.

In summary, this indicator represents a fusion of traditional candlestick analysis with modern machine learning techniques. It harnesses the simplicity and effectiveness of Naive Bayes to deliver a dynamic, real-time evaluation of various candlestick patterns. Whether you are a seasoned trader looking to refine your technical analysis or a beginner eager to understand market dynamics, this tool offers a powerful, customizable, and efficient solution. Welcome to a new era where advanced statistical methods meet practical trading insights—happy trading and may your patterns always be in your favor!

Note : On this current released beta version, you must manually adjust reversal percentage move based on each market. Further updates may include automated best range detection and probability.

[AcerX] Leverage, TP & Optimal TP CalculatorHow It Works

Inputs:

Portfolio Allocation (%): The percentage of your portfolio you're willing to risk on the trade.

Stop Loss (%): The stop loss distance below the entry price.

Taker Fee (%) and Maker Fee (%): The fees applied on entry and exit.

Calculations:

The script calculates the required "raw" leverage to risk 1% of your portfolio.

It floors the computed leverage to an integer ("effectiveLeverage").

If the computed leverage is less than 1, it shows an error message (and suggests the maximum allocation for at least 1× leverage).

Otherwise, it calculates the TP levels for target profits of 1.2%, 1.5%, and 2%, and an "Optimal TP" that nets a 1% profit after fees.

Display:

A table is drawn on the top right corner of your chart displaying the effective leverage, the TP levels, and an error message if applicable.

Simply add this script as a new indicator in TradingView, and adjust the inputs as needed.

Happy trading!

Adaptive Resonance Oscillator [AlgoAlpha]Introducing the Adaptive Resonance Oscillator , an advanced momentum-based oscillator designed to dynamically adjust to changing market conditions. This innovative indicator detects market frequency through a Hilbert Transform approach, adapting in real-time to identify overbought and oversold conditions with improved accuracy. With built-in divergence detection, trend analysis, and customizable smoothing, this tool is perfect for traders looking to refine their entries and exits based on adaptive oscillation mechanics.

🚀 Key Features :

🔹 Adaptive Frequency Detection – Uses Hilbert Transform principles to dynamically determine market cycle length for precise oscillator calculation.

⚙️ Customizable Smoothing – Option to apply a Hull Moving Average (HMA) for enhanced signal clarity.

📈 Divergence Detection – Identifies bullish and bearish divergences with visual markers, helping traders spot early trend reversals.

🟢 Overbought & Oversold Signals – Highlights extreme momentum conditions with adjustable thresholds.

🔔 Real-Time Alerts – Get notified for crossovers, divergences, and strong trend shifts directly on your TradingView chart.

🎨 Fully Customizable Appearance – Modify colors, divergence sensitivity, and smoothing options to fit your trading style.

🛠 How to Use :

Add the Adaptive Resonance Oscillator to your TradingView chart by clicking the ★ to favorite it.

Monitor the Charts , switch between smoothed and I smoothed modes to identify trend and price swings, use divergences and reversal signals for potential entry/exits.

Set alerts for bullish/bearish crossovers and divergence signals to stay ahead of market moves.

⚙ How It Works :

The indicator begins by applying a Hilbert Transform frequency estimation to the price series, identifying the dominant market cycle length. This is used to calculate a period for the RSI that matches its resonant frequency with the dominant market frequency, dynamically adjusting the Oscillator. The oscillator then applies an optional Hull Moving Average (HMA) smoothing for signal refinement. Additionally, the indicator scans for bullish and bearish divergences by comparing oscillator movements against price action, plotting signals accordingly. When overbought/oversold conditions or divergence events occur, alerts are triggered to notify the trader in real time.

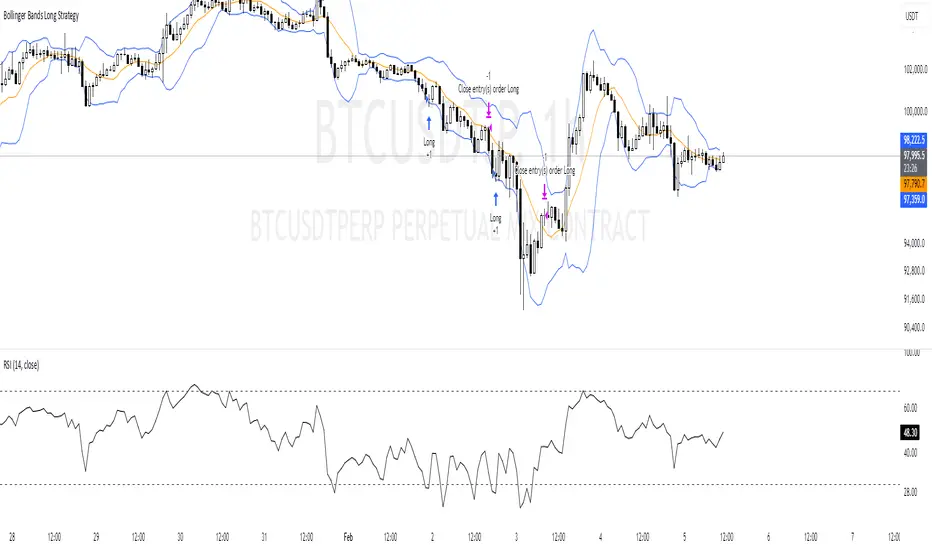

Bollinger Bands Long Strategy

This strategy is designed for identifying and executing long trades based on Bollinger Bands and RSI. It aims to capitalize on potential oversold conditions and subsequent price recovery.

Key Features:

- Bollinger Bands (10,2): The strategy uses Bollinger Bands with a 10-period moving average and a multiplier of 2 to define price volatility.

- RSI Filter: A trade is only triggered when the RSI (14-period) is below 30, ensuring entry during oversold conditions.

- Entry Condition: A long trade is entered immediately when the price crosses below the lower Bollinger Band and the RSI is under 30.

- Exit Condition: The position is exited when the price reaches or crosses above the Bollinger Band basis (20-period moving average).

Best Used For:

- Identifying oversold conditions with a strong potential for a rebound.

- Markets or assets with clear oscillations and volatility e.g., BTC.

**Disclaimer:** This strategy is for educational purposes and should be used with caution. Backtesting and risk management are essential before live trading.

smolka Bayesian Volatile ChannelDescription in English and Russian.

Bayesian Volatile Channel

The script is a loose interpretation of Bayes' theorem, which allows calculating the probability of events given that another event related to it has occurred, the script analyzes volatility and detects anomalies in price charts using a Bayesian approach, updating the model parameters to accurately estimate market fluctuations and detect changes in trends.

How does it work?

1. The script sets the initial parameters (mean price and standard deviation), creating a "hypothesis" about the market behavior.

2. When a new price appears, the script calculates the probability of its compliance with previous expectations. If the new price differs from the forecast, the model parameters (mean and standard deviation) are updated.

3. After updating the model, the probability that the current price and volatility correspond to a normal distribution is calculated.

4. Based on the updated model, volatility channels are built (mean price ± two standard deviations). If the price goes beyond these limits, this signals a possible anomaly indicating changes in the market.

5. The moving averages in the script act as data smoothing and trend analysis, helping to identify the market direction and minimize the impact of random fluctuations. The script uses moving averages to identify uptrends and downtrends, and calculates the average between them to display the overall market balance. These moving averages make market analysis clearer and more resistant to short-term fluctuations.

******************************************************************

Описание на английском и русском языках.

Байесовский волатильный канал

Скрипт является вольной интерпретацией теоремы Байеса, которая позволяет расчитать вероятность событий при условии, что произошло связанное с ним другое событие, скрипт анализирует волатильность и обнаруживает аномалии в графиках цен, используя байесовский подход, обновляя параметры модели для точной оценки рыночных колебаний и обнаружения изменений в тенденциях.

Как это работает?

1. Скрипт устанавливает начальные параметры (среднюю цену и стандартное отклонение), создавая "гипотезу" о поведении рынка.

2. При появлении новой цены скрипт вычисляет вероятность её соответствия предыдущим ожиданиям. Если новая цена отличается от прогноза, параметры модели (среднее и стандартное отклонение) обновляются.

3. После обновления модели рассчитывается вероятность того, что текущая цена и волатильность соответствуют нормальному распределению.

4. На основе обновлённой модели строятся каналы волатильности (средняя цена ± два стандартных отклонения). Если цена выходит за эти пределы, это сигнализирует о возможной аномалии, указывающей на изменения на рынке.

5. Средние скользящие в скрипте выполняют роль сглаживания данных и анализа трендов, помогая выявить направление рынка и минимизировать влияние случайных колебаний. Скрипт использует скользящие средние для определения восходящего и нисходящего трендов, а также рассчитывает среднее значение между ними для отображения общего баланса рынка. Эти скользящие средние делают анализ рынка более чётким и устойчивым к краткосрочным флуктуациям.

Dynamic Deviation Levels [BigBeluga]Dynamic Deviation Levels is an innovative indicator designed to analyze price deviations relative to a smoothed midline. It provides traders with visual cues for overbought/oversold zones, price momentum, levels through labeled deviations and gradient candle coloring.

🔵Key Features:

Smoothed Midline:

A central line calculated as a smoothed median of the price source, serving as the baseline for price deviation analysis.

Dynamic Deviation Levels:

- Three deviation levels are plotted above and below the midline, with labels (1, 2, 3, -1, -2, -3) marking significant price movements.

- Helps traders identify overbought and oversold market conditions.

Heat-Colored Candles:

- Candle colors shift in intensity based on the deviation level, with four gradient shades for both upward and downward movements.

- Quickly highlights market extremes or stable zones.

Interactive Color Scale:

- A gradient scale at the bottom right of the chart visually represents deviation values.

- A triangle marker indicates the current price deviation in real time.

Optional Deviation Levels Display:

- Traders can enable all dynamic levels on the chart to visualize support and resistance areas dynamically.

🔵Usage and Benefits:

Identify Overbought/Oversold Zones: Use labeled deviation levels and heat-colored candles to spot stretched market conditions.

Track Trend Reversals and Momentum: Monitor price interactions with deviation levels for potential trend continuation or reversal signals.

Real-Time Deviation Insights: Leverage the color scale and triangle marker for live deviation tracking and actionable insights.

Map Dynamic Support and Resistance: Enable dynamic levels to highlight key areas where price reactions are likely to occur.

Dynamic Deviation Levels is an indispensable tool for traders aiming to combine price dynamics, momentum analysis, and visual clarity in their trading strategies.

Swing Profile Analyzer [ChartPrime]Swing Profile Analyzer

The Swing Profile Analyzer is a comprehensive tool designed to provide traders with valuable insights into swing frequency profiles, enabling them to identify key price levels and areas of market interest.

⯁ KEY FEATURES

Swing Frequency Profiles

Automatically plots frequency profiles for each swing, highlighting price distribution and key levels of significance.

Point of Control (POC) Line

Marks the price level with the highest number of closes within a swing, acting as a key area for potential price reactions.

Customizable Trend Display

Allows users to toggle between displaying profiles for bullish swings, bearish swings, or both, offering tailored analysis.

Integrated ZigZag Lines

Visualizes swing highs and lows, providing a clear picture of market trends and reversals.

Dynamic Profile Visualization

Profiles are color-coded to indicate the frequency of closes, with the highest value bins distinctly marked for easy recognition.

Max Frequency Highlight

Displays numerical values for the most active price level within each profile, showing how many closes occurred at the peak bin.

Updates only after swing formed

Profiles and POC lines automatically appear after swing is done

⯁ HOW TO USE

Identify Critical Price Levels

Use the POC line and frequency distribution to locate levels where price is likely to react or consolidate.

Analyze Swing Characteristics

Observe swing profiles to understand the strength, duration, and behavior of market trends.

Plan Entries and Exits

Leverage significant price levels and high-frequency bins to make more informed trading decisions.

Focus on Specific Trends

Filter profiles to analyze bullish or bearish swings based on your trading strategy.

⯁ CONCLUSION

The Swing Profile Analyzer is an essential tool for traders seeking to understand price dynamics within market swings. By combining frequency profiles, POC levels, and trend visualization, it enhances your ability to interpret and act on market movements effectively.

Pearson Correlation CoefficientDescription: The Pearson Correlation Coefficient measures the strength and direction of the linear relationship between two data series. Its value ranges from -1 to +1, where:

+1 indicates a perfect positive linear correlation: as one asset increases, the other asset increases proportionally.

0 indicates no linear correlation: variations in one asset have no relation to variations in the other asset.

-1 indicates a perfect negative linear correlation: as one asset increases, the other asset decreases proportionally.

This measure is widely used in technical analysis to assess the degree of correlation between two financial assets. The "Pearson Correlation (Manual Compare)" indicator allows users to manually select two assets and visually display their correlation relationship on a chart.

Features:

Correlation Period: The time period used for calculating the correlation can be adjusted (default: 50).

Comparison Asset: Users can select a secondary asset for comparison.

Visual Plots: The chart includes reference lines for perfect correlations (+1 and -1) and strong correlations (+0.7 and -0.7).

Alerts: Set alerts for when the correlation exceeds certain threshold values (e.g., +0.7 for strong positive correlation).

How to Select the Second Asset:

Primary Asset Selection: The primary asset is the one you select for viewing on the chart. This can be done by simply opening the chart for the desired asset.

Secondary Asset Selection: To select the secondary asset for comparison, use the input field labeled "Comparison Asset" in the script settings. You can manually enter the ticker symbol of the secondary asset you want to compare with the primary asset.

This indicator is ideal for traders looking to identify relationships and correlations between different financial assets to make informed trading decisions.

ELHAI Futures Trend Checker (ES, NQ, YM)The ELHAI Futures Trend Checker is a powerful TradingView indicator designed for futures traders who want to monitor the trend synchronization of the three major U.S. futures indices:

✅ E-mini S&P 500 (ES1!)

✅ E-mini Nasdaq 100 (NQ1!)

✅ E-mini Dow Jones (YM1!)

This indicator checks whether all three futures indices are bullish or bearish during each candle formation. If one of them is out of sync (e.g., two indices are bullish while one is bearish), the indicator triggers an alert and highlights the background in red, helping traders identify potential market indecision or divergence.

Key Features

📌 Designed for Futures Traders – Focuses on ES, NQ, and YM futures contracts.

📌 Live Market Monitoring – Works in real-time and updates dynamically with each tick.

📌 Bullish/Bearish Trend Confirmation – Detects when all three indices are in sync.

📌 Mismatch Detection – Alerts you when at least one index is out of trend.

📌 Custom Alerts – Set up TradingView alerts to be notified instantly when a trend mismatch occurs.

📌 Visual Background Highlight – A red background warns of a market divergence.

How It Works

The script retrieves open and close prices for ES, NQ, and YM.

Determines whether each futures index is bullish (close > open) or bearish (close < open).

If all three indices are bullish or all are bearish, it remains neutral.

If one index is different, an alert is triggered and the background turns red.

How to Use

Apply the indicator to your TradingView chart.

Choose any timeframe – Works well on intraday, daily, or higher timeframes.

Enable alerts: Go to Alerts → Create Alert, select "Futures Trend Mismatch", and set your preferred alert frequency.

Use alongside other indicators like moving averages, RSI, or MACD for better trade confirmation.

Best Use Cases

✔ Day traders & scalpers – Quickly spot market divergence in live trading.

✔ Swing traders – Identify when futures markets lose synchronization.

✔ Trend followers – Confirm if all major futures markets are aligned before making a move.

Final Notes

This indicator was built for Elhai to provide real-time trend analysis across major U.S. futures indices. Use it as a confirmation tool to improve market timing and decision-making.

ICT Killzones + Macros [TakingProphets]The ICT Killzones indicator is a powerful tool designed to visualize key trading sessions and market timing elements used in ICT (Inner Circle Trader) methodology. It includes:

• Session Markers:

- Asia Session

- London Session

- NY AM Session

- NY Lunch Session

- NY PM Session

• Key Price Levels:

- Session high/low levels that extend until violated

- Midnight Open price level (dotted line)

- True Day Open price level (6 PM EST, dotted line)

• ICT Macro Timing:

- First Macro: 9:45 AM - 10:15 AM EST

- Second Macro: 10:45 AM - 11:15 AM EST

- Distinctive L-shaped brackets marking start and end times

Features:

• Fully customizable colors and styles for all elements

• Adjustable label positions and sizes

• Toggle options for each component

• Smart timeframe filtering

• Clean, uncluttered visual design

This indicator helps traders identify key market structure points, session transitions, and optimal trading windows based on ICT concepts.