Anchored Geometric Brownian Motion Projections w/EVAnchored GBM (Geometric Brownian Motion) Projections + EV & Confidence Bands

Version: Pine Script v6

Overlay: Yes

Author:

Published On:

Overview

The Anchored GBM Projections + EV & Confidence Bands indicator leverages the Geometric Brownian Motion (GBM) model to project future price movements based on historical data. By simulating multiple potential future price paths, it provides traders with insights into possible price trajectories, their expected values, and confidence intervals. Additionally, it offers a "Mean of EV" (EV of EV) line, representing the running average of expected values across the projection period.

Key Features

Anchor Time Setup:

Define a specific point in time from which the projections commence.

By default, it uses the current bar's timestamp but can be customized.

Projection Parameters:

Projection Candles (Bars): Determines the number of future bars (time periods) to project.

Number of Simulations: Specifies how many GBM paths to simulate, ensuring statistical relevance via the Central Limit Theorem (CLT).

Display Toggles:

Simulation Lines: Visual representation of individual GBM simulation paths.

Expected Value (EV) Line: The average price across all simulations at each projection bar.

Upper & Lower Confidence Bands: 95% confidence intervals indicating potential price boundaries.

EV of EV Line: Running average of EV values, providing a smoothed central tendency across the projection period. Additionally, this line often acts as an indicator of trend direction.

Visualization:

Clear and distinguishable lines with customizable colors and styles.

Overlayed on the price chart for direct comparison with actual price movements.

Mathematical Foundation

Geometric Brownian Motion (GBM):

Definition: GBM is a continuous-time stochastic process used to model stock prices. It assumes that the logarithm of the stock price follows a Brownian motion with drift.

Equation:

S(t)=S0⋅e(μ−12σ2)t+σW(t)

S(t)=S0⋅e(μ−21σ2)t+σW(t) Where:

S(t)S(t) = Stock price at time tt

S0S0 = Initial stock price

μμ = Drift coefficient (average return)

σσ = Volatility coefficient (standard deviation of returns)

W(t)W(t) = Wiener process (standard Brownian motion)

Drift (μμ) and Volatility (σσ):

Drift (μμ) represents the expected return of the stock.

Volatility (σσ) measures the stock's price fluctuation intensity.

Central Limit Theorem (CLT):

Principle: With a sufficiently large number of independent simulations, the distribution of the sample mean (EV) approaches a normal distribution, regardless of the underlying distribution.

Application: Ensures that the EV and confidence bands are statistically reliable.

Expected Value (EV) and Confidence Bands:

EV: The mean price across all simulations at each projection bar.

Confidence Bands: Range within which the actual price is expected to lie with a specified probability (e.g., 95%).

EV of EV (Mean of Sample Means):

Definition: Represents the running average of EV values across the projection period, offering a smoothed central tendency.

Methodology

Anchor Time Setup:

The indicator starts projecting from a user-defined Anchor Time. If not customized, it defaults to the current bar's timestamp.

Purpose: Allows users to analyze projections from a specific historical point or the latest market data.

Calculating Drift and Volatility:

Returns Calculation: Computes the logarithmic returns from the Anchor Time to the current bar.

returns=ln(StSt−1)

returns=ln(St−1St)

Drift (μμ): Calculated as the simple moving average (SMA) of returns over the period since the Anchor Time.

Volatility (σσ): Determined using the standard deviation (stdev) of returns over the same period.

Simulation Generation:

Number of Simulations: The user defines how many GBM paths to simulate (e.g., 30).

Projection Candles: Determines the number of future bars to project (e.g., 12).

Process:

For each simulation:

Start from the current close price.

For each projection bar:

Generate a random number zz from a standard normal distribution.

Calculate the next price using the GBM formula:

St+1=St⋅e(μ−12σ2)+σz

St+1=St⋅e(μ−21σ2)+σz

Store the projected price in an array.

Expected Value (EV) and Confidence Bands Calculation:

EV Path: At each projection bar, compute the mean of all simulated prices.

Variance and Standard Deviation: Calculate the variance and standard deviation of simulated prices to determine the confidence intervals.

Confidence Bands: Using the standard normal z-score (1.96 for 95% confidence), establish upper and lower bounds:

Upper Band=EV+z⋅σEV

Upper Band=EV+z⋅σEV

Lower Band=EV−z⋅σEV

Lower Band=EV−z⋅σEV

EV of EV (Running Average of EV Values):

Calculation: For each projection bar, compute the average of all EV values up to that bar.

EV of EV =1j+1∑k=0jEV

EV of EV =j+11k=0∑jEV

Visualization: Plotted as a dynamic line reflecting the evolving average EV across the projection period.

Visualization Elements

Simulation Lines:

Appearance: Semi-transparent blue lines representing individual GBM simulation paths.

Purpose: Illustrate a range of possible future price trajectories based on current drift and volatility.

Expected Value (EV) Line:

Appearance: Solid orange line.

Purpose: Shows the average projected price at each future bar across all simulations.

Confidence Bands:

Upper Band: Dashed green line indicating the upper 95% confidence boundary.

Lower Band: Dashed red line indicating the lower 95% confidence boundary.

Purpose: Highlight the range within which the price is statistically expected to remain with 95% confidence.

EV of EV Line:

Appearance: Dashed purple line.

Purpose: Displays the running average of EV values, providing a smoothed trend of the central tendency across the projection period. As the mean of sample means it approximates the population mean (i.e. the trend since the anchor point.)

Current Price:

Appearance: Semi-transparent white line.

Purpose: Serves as a reference point for comparing actual price movements against projected paths.

Usage Instructions

Configuring User Inputs:

Anchor Time:

Set to a specific timestamp to start projections from a historical point or leave it as default to use the current bar's time.

Projection Candles (Bars):

Define the number of future bars to project (e.g., 12). Adjust based on your trading timeframe and analysis needs.

Number of Simulations:

Specify the number of GBM paths to simulate (e.g., 30). Higher numbers yield more accurate EV and confidence bands but may impact performance.

Display Toggles:

Show Simulation Lines: Toggle to display or hide individual GBM simulation paths.

Show Expected Value Line: Toggle to display or hide the EV path.

Show Upper Confidence Band: Toggle to display or hide the upper confidence boundary.

Show Lower Confidence Band: Toggle to display or hide the lower confidence boundary.

Show EV of EV Line: Toggle to display or hide the running average of EV values.

Managing TradingView's Object Limits:

Understanding Limits:

TradingView imposes a limit on the number of graphical objects (e.g., lines) that can be rendered. High values for projection candles and simulations can quickly consume these limits. TradingView appears to only allow a total of 55 candles to be projected, so if you want to see two complete lines, you would have to set the projection length to 27: since 27 * 2 = 54 and 54 < 55.

Optimizing Performance:

Use Toggles: Enable only the necessary visual elements. For instance, disable simulation lines and confidence bands when focusing on the EV and EV of EV lines. You can also use the maximum projection length of 55 with the lower limit confidence band as the only line, visualizing a long horizon for your risk.

Adjust Parameters: Lower the number of projection candles or simulations to stay within object limits without compromising essential insights.

Interpreting the Indicator:

Simulation Lines (Blue):

Represent individual potential future price paths based on GBM. A wider spread indicates higher volatility.

Expected Value (EV) Line (Goldenrod):

Shows the mean projected price at each future bar, providing a central trend.

Confidence Bands (Green & Red):

Indicate the statistical range (95% confidence) within which the price is expected to remain.

EV of EV Line (Dotted Line - Goldenrod):

Reflects the running average of EV values, offering a smoothed perspective of expected price trends over the projection period.

Current Price (White):

Serves as a benchmark for assessing how actual prices compare to projected paths.

Practical Applications

Risk Management:

Confidence Bands: Help in identifying potential support and resistance levels based on statistical confidence intervals.

EV Path: Assists in setting realistic target prices and stop-loss levels aligned with projected expectations.

Trend Analysis:

EV of EV Line: Offers a smoothed trendline, aiding in identifying overarching market directions amidst price volatility. Indicative of the population mean/overall trend of the data since your anchor point.

Scenario Planning:

Simulation Lines: Enable traders to visualize multiple potential outcomes, fostering better decision-making under uncertainty.

Performance Evaluation:

Comparing Actual vs. Projected Prices: Assess how actual price movements align with projected scenarios, refining trading strategies over time.

Mathematical and Statistical Insights

Simulation Integrity:

Independence: Each simulation path is generated independently, ensuring unbiased and diverse projections.

Randomness: Utilizes a Gaussian random number generator to introduce variability in diffusion terms, mimicking real market randomness.

Statistical Reliability:

Central Limit Theorem (CLT): By simulating a sufficient number of paths (e.g., 30), the sample mean (EV) converges to the population mean, ensuring reliable EV and confidence band calculations.

Variance Calculation: Accurate computation of variance from simulation data ensures precise confidence intervals.

Dynamic Projections:

Running Average (EV of EV): Provides a cumulative perspective, allowing traders to observe how the average expectation evolves as the projection progresses.

Customization and Enhancements

Adjustable Parameters:

Tailor the projection length and simulation count to match your trading style and analysis depth.

Visual Customization:

Modify line colors, styles, and transparency to enhance clarity and fit chart aesthetics.

Extended Statistical Metrics:

Future iterations can incorporate additional metrics like median projections, skewness, or alternative confidence intervals.

Dynamic Recalculation:

Implement logic to automatically update projections as new data becomes available, ensuring real-time relevance.

Performance Considerations

Object Count Management:

High simulation counts and extended projection periods can lead to a significant number of graphical objects, potentially slowing down chart performance.

Solution: Utilize display toggles effectively and optimize projection parameters to balance detail with performance.

Computational Efficiency:

The script employs efficient array handling and conditional plotting to minimize unnecessary computations and object creation.

Conclusion

The Anchored GBM Projections + EV & Confidence Bands indicator is a robust tool for traders seeking to forecast potential future price movements using statistical models. By integrating Geometric Brownian Motion simulations with expected value calculations and confidence intervals, it offers a comprehensive view of possible market scenarios. The addition of the "EV of EV" line further enhances analytical depth by providing a running average of expected values, aiding in trend identification and strategic decision-making.

Hope it helps!

Statistics

Engulfing Candlestick StrategyEver wondered whether the Bullish or Bearish Engulfing pattern works or has statistical significance? This script is for you. It works across all markets and timeframes.

The Engulfing Candlestick Pattern is a widely used technical analysis pattern that traders use to predict potential price reversals. It consists of two candles: a small candle followed by a larger one that "engulfs" the previous candle. This pattern is considered bullish when it occurs in a downtrend (bullish engulfing) and bearish when it occurs in an uptrend (bearish engulfing).

Statistical Significance of the Engulfing Pattern:

While many traders rely on candlestick patterns for making decisions, research on the statistical significance of these patterns has produced mixed results. A study by Dimitrios K. Koutoupis and K. M. Koutoupis (2014), titled "Testing the Effectiveness of Candlestick Chart Patterns in Forex Markets," indicates that candlestick patterns, including the engulfing pattern, can provide some predictive power, but their success largely depends on the market conditions and timeframe used. The researchers concluded that while some candlestick patterns can be useful, traders must combine them with other indicators or market knowledge to improve their predictive accuracy.

Another study by Brock, Lakonishok, and LeBaron (1992), "Simple Technical Trading Rules and the Stochastic Properties of Stock Returns," explores the profitability of technical indicators, including candlestick patterns, and finds that simple trading rules, such as those based on moving averages or candlestick patterns, can occasionally outperform a random walk in certain market conditions.

However, Jorion (1997), in his work "The Risk of Speculation: The Case of Technical Analysis," warns that the reliability of candlestick patterns, including the engulfing patterns, can vary significantly across different markets and periods. Therefore, it's important to use these patterns as part of a broader trading strategy that includes other risk management techniques and technical indicators.

Application Across Markets:

This script applies to all markets (e.g., stocks, commodities, forex) and timeframes, making it a versatile tool for traders seeking to explore the statistical effectiveness of the bullish and bearish engulfing patterns in their own trading.

Conclusion:

This script allows you to backtest and visualize the effectiveness of the Bullish and Bearish Engulfing patterns across any market and timeframe. While the statistical significance of these patterns may vary, the script provides a clear framework for evaluating their performance in real-time trading conditions. Always remember to combine such patterns with other risk management strategies and indicators to enhance their predictive power.

Daytrading ES Wick Length StrategyThis Pine Script strategy calculates the combined length of upper and lower wicks of candlesticks and uses a customizable moving average (MA) to identify potential long entry points. The strategy compares the total wick length to the MA with an added offset. If the wick length exceeds the offset-adjusted MA, the strategy enters a long position. The position is automatically closed after a user-defined holding period.

Key Features:

1. Calculates the sum of upper and lower wicks for each candlestick.

2. Offers four types of moving averages (SMA, EMA, WMA, VWMA) for analysis.

3. Allows the user to set a customizable MA length and an offset to shift the MA.

4. Automatically exits positions after a specified number of bars.

5. Visualizes the wick length as a histogram and the offset-adjusted MA as a line.

References:

• Candlestick wick analysis: Nison, S. (1991). Japanese Candlestick Charting Techniques.

• Moving averages: Brock, W., Lakonishok, J., & LeBaron, B. (1992). “Simple Technical Trading Rules and the Stochastic Properties of Stock Returns”. Journal of Finance.

This strategy is suitable for identifying candlesticks with significant volatility and long wicks, which can indicate potential trend reversals or continuations.

Up Gap Strategy with DelayThis strategy, titled “Up Gap Strategy with Delay,” is based on identifying up gaps in the price action of an asset. A gap is defined as the percentage difference between the current bar’s open price and the previous bar’s close price. The strategy triggers a long position if the gap exceeds a user-defined threshold and includes a delay period before entering the position. After entering, the position is held for a set number of periods before being closed.

Key Features:

1. Gap Threshold: The strategy defines an up gap when the gap size exceeds a specified threshold (in percentage terms). The gap threshold is an input parameter that allows customization based on the user’s preference.

2. Delay Period: After the gap occurs, the strategy waits for a delay period before initiating a long position. This delay can help mitigate any short-term volatility that might occur immediately after the gap.

3. Holding Period: Once the position is entered, it is held for a user-defined number of periods (holdingPeriods). This is to capture the potential post-gap trend continuation, as gaps often indicate strong directional momentum.

4. Gap Plotting: The strategy visually plots up gaps on the chart by placing a green label beneath the bar where the gap condition is met. Additionally, the background color turns green to highlight up-gap occurrences.

5. Exit Condition: The position is exited after the defined holding period. The strategy ensures that the position is closed after this time, regardless of whether the price is in profit or loss.

Scientific Background:

The gap theory has been widely studied in financial literature and is based on the premise that gaps in price often represent areas of significant support or resistance. According to research by Kaufman (2002), gaps in price action can be indicators of future price direction, particularly when they occur after a period of consolidation or a trend reversal. Moreover, Gaps and their Implications in Technical Analysis (Murphy, 1999) highlights that gaps can reflect imbalances between supply and demand, leading to high momentum and potential price continuation or reversal.

In trading strategies, utilizing gaps with specific conditions, such as delay and holding periods, can enhance the ability to capture significant price moves. The strategy’s delay period helps avoid potential market noise immediately after the gap, while the holding period seeks to capitalize on the price continuation that often follows gap formation.

This methodology aligns with momentum-based strategies, which rely on the persistence of trends in financial markets. Several studies, including Jegadeesh & Titman (1993), have documented the existence of momentum effects in stock prices, where past price movements can be predictive of future returns.

Conclusion:

This strategy incorporates gap detection and momentum principles, supported by empirical research in technical analysis, to attempt to capitalize on price movements following significant gaps. By waiting for a delay period and holding the position for a specified time, it aims to mitigate the risk associated with early volatility while maximizing the potential for sustained price moves.

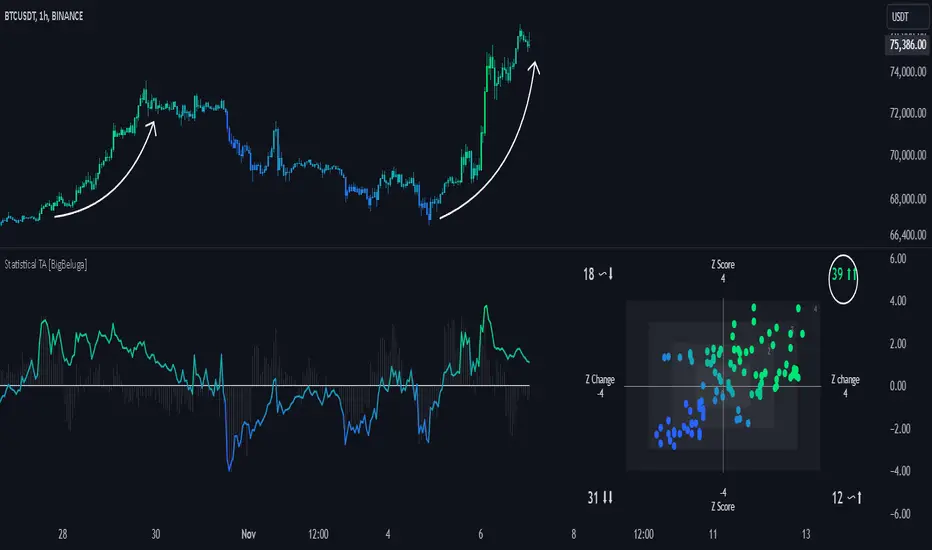

Statistical Trend Analysis (Scatterplot) [BigBeluga]Statistical Trend Analysis (Scatterplot) provides a unique perspective on market dynamics by combining the statistical concept of z-scores with scatterplot visualization to assess price momentum and potential trend shifts.

🧿 What is Z-Score?

Definition: A z-score is a statistical measure that quantifies how far a data point is from the mean, expressed in terms of standard deviations.

In this Indicator:

A high positive z-score indicates the price is significantly above the average.

A low negative z-score indicates the price is significantly below the average.

The indicator also calculates the rate of change of the z-score, helping identify momentum shifts in the market.

🧿 Key Features:

Scatterplot Visualization:

Displays data points of z-score and its change across four quadrants.

Quadrants help interpret market conditions:

Upper Right (Strong Bullish Momentum): Most data points here signal an ongoing uptrend.

Upper Left (Weakening Momentum): Data points here may indicate a potential market shift or ranging market.

Lower Left (Strong Bearish Momentum): Indicates a dominant downtrend.

Lower Right (Trend Shift to Bullish/Ranging): Suggests weakening bearish momentum or an emerging uptrend.

Color-Coded Candles:

Candles are dynamically colored based on the z-score, providing a visual cue about the price's deviation from the mean.

Z-Score Time Series:

A line plot of z-scores over time shows price deviation trends.

A gray histogram displays the rate of change of the z-score, highlighting momentum shifts.

🧿 Usage:

Use the scatterplot and quadrant gauges to understand the current market momentum and potential shifts.

Monitor the z-score line plot to identify overbought/oversold conditions.

Utilize the gray histogram to detect momentum reversals and trend strength.

This tool is ideal for traders who rely on statistical insights to confirm trends, detect potential reversals, and assess market momentum visually and quantitatively.

ROE BandROE Band shows the return on net profit from shareholders' equity and the formula for decomposition

ROE = ROA x CSL x CEL

ROE Band consists of 5 parts:

1. ROE (TTM) is the 12-month ROE calculation in "green"

2. Return on Equity (ROE) is the current quarterly net profit / the average of the beginning and ending periods of shareholders' equity in "yellow"

3. Return on Assets (ROA) is the current quarterly NOPAT (net profit before tax) / the average of the beginning and ending periods of total assets in "blue"

4. Capital structure leverage (CSL) is a financial measure that compares a company's debt to its total capital. It is calculated by taking the average of the beginning and ending periods of total assets / the average of the beginning and ending periods of shareholders' equity. The higher the CSL, the more deb, in. "red"

5. Common earnings leverage (CEL) is the proportion of net profit and NOPAT (net profit before tax), where a lower CEL means more tax, in "orange"

The "😱" emoji represents the value if it increases by more than or decreases by less than 20%, e.g.

- ROE(TTM), ROE, ROA, CEL is decreasing

- CSL is increasing

The "🔥" emoji represents the value if it increases by more than or decreases, e.g.

- ROE(TTM), ROE, ROA, CEL is increasing

- CSL is decreasing

RSI Trend [MacroGlide]The RSI Trend indicator is a versatile and intuitive tool designed for traders who want to enhance their market analysis with visual clarity. By combining Stochastic RSI with moving averages, this indicator offers a dynamic view of market momentum and trends. Whether you're a beginner or an experienced trader, this tool simplifies identifying key market conditions and trading opportunities.

Key Features:

• Stochastic RSI-Based Calculations: Incorporates Stochastic RSI to provide a nuanced view of overbought and oversold conditions, enhancing standard RSI analysis.

• Dynamic Moving Averages: Includes two customizable moving averages (MA1 and MA2) based on smoothed Stochastic RSI, offering flexibility to align with your trading strategy.

• Candle Color Coding: Automatically colors candles on the chart:

• Blue: When the faster moving average (MA2) is above the slower one (MA1), signaling bullish momentum.

• Orange: When the faster moving average is below the slower one, indicating bearish momentum.

• Integrated Scaling: The indicator dynamically adjusts with the chart's scale, ensuring seamless visualization regardless of zoom level.

How to Use:

• Add the Indicator: Apply the indicator to your chart from the TradingView library.

• Interpret Candle Colors: Use the color-coded candles to quickly identify bullish (blue) and bearish (orange) phases.

• Customize to Suit Your Needs: Adjust the lengths of the moving averages and the Stochastic RSI parameters to better fit your trading style and timeframe.

• Combine with Other Tools: Pair this indicator with trendlines, volume analysis, or support and resistance levels for a comprehensive trading approach.

Methodology:

The indicator utilizes Stochastic RSI, a derivative of the standard RSI, to measure momentum more precisely. By applying smoothing and calculating moving averages, the tool identifies shifts in market trends. These trends are visually represented through candle color changes, making it easy to spot transitions between bullish and bearish phases at a glance.

Originality and Usefulness:

What sets this indicator apart is its seamless integration of Stochastic RSI and moving averages with real-time candle coloring. The result is a visually intuitive tool that adapts dynamically to chart scaling, offering clarity without clutter.

Charts:

When applied, the indicator plots two moving averages alongside color-coded candles. The combination of visual cues and trend logic helps traders easily interpret market momentum and make informed decisions.

Enjoy the game!

Smooth RSI [MarktQuant]This indicator combines elements of the Relative Strength Index (RSI) and Rate of Change (RoC) to provide a smoother and potentially more insightful view of market momentum and price movement. The Smooth RSI calculates RSI values across four price points (high, open, low, close) to average them, offering a less volatile RSI signal. Additionally, it incorporates a Rate of Change for trend confirmation, enhancing the decision-making process for trade entries and exits.

Features:

Multi-RSI Calculation: RSI is computed for high, open, low, and close prices, then averaged to reduce noise.

Trend Confirmation with RoC: Uses the Rate of Change to validate the RSI signals, coloring bars based on the trend direction.

Visual Signals:

Bar colors change based on combined RSI and RoC signals.

Green for bullish signals (RSI above 50 and positive RoC).

Red for bearish signals (RSI below 50 and negative RoC).

Horizontal lines at 30, 50, and 70 to denote overbought, neutral, and oversold conditions.

Customizable Display:

Option to show/hide RSI plot or RoC plot for cleaner charts.

Candle plot overlay option to visualize current price action alongside the indicator.

Inputs:

RSI Length: Default 28. Adjusts the lookback period for RSI calculation.

RoC Length: Default 28. Sets the period for the Rate of Change calculation.

Plot Settings:

Show RSI - Toggle RSI plot visibility.

Show RoC - Toggle RoC plot visibility.

Usage:

Long signals are indicated when the average RSI is above 50 and the RoC is positive.

Short signals are suggested when the average RSI falls below 50 with a negative RoC.

The color coding helps visually confirm trends at a glance.

Notes:

This indicator is best used in conjunction with other analysis methods to confirm signals.

Adjust the length parameters based on your trading timeframe for optimal results.

Disclaimer:

This indicator does not guarantee trading success; use it as part of a comprehensive trading strategy. Always conduct your own analysis before making trading decisions.

Market Correlation AnalysisMarket Correlation Analysis is an indicator that measures the correlation of any two instruments.

To express price changes in a way that is comparable, this indicator uses a percentage of the ATR as a unit.

User Inputs:

Other Symbol - the symbol which we want to compare with the symbol of the main chart.

ATR for Price Movement Normalisation - I recommend high values to get the ATR more stable across time - if the ATR drastically changes, the indicator will register that as a price movement, because the unit in which price movements are measured itself changed by a lot. However, with higher values the ATR is stable and, in my opinion, more reliable than simply a percentage change of the current price.

Correlation Length - this is the number of bars for which the correlation coefficient will be calculated.

About The Indicator:

Market Correlation Analysis expresses the price changes of both instruments in question on the same histogram.

By default, the price changes that represent the instrument of the main chart are expressed with thinner bars of stronger colour, while the price changes that represent the other instrument are expressed with much thicker bars, which are of more pale colour.

The correlation coefficient is not expressed on the histogram, as it has a different scale. Therefore, it is only showed as a number.

I hope this indicator can make it easier to understand just how much two instruments have been similar to one another over a certain period of time. The possibility to see the correlation for any given time frame can give information that very specific to any trading style.

Enhanced Price Z-Score OscillatorThe Enhanced Price Z-Score Oscillator by tkarolak is a powerful tool that transforms raw price data into an easy-to-understand statistical visualization using Z-Score-derived candlesticks. Simply put, it shows how far prices stray from their average in terms of standard deviations (Z-Scores), helping traders identify when prices are unusually high (overbought) or unusually low (oversold).

The indicator’s default feature displays Z-Score Candlesticks, where each candle reflects the statistical “distance” of the open, high, low, and close prices from their average. This creates a visual map of market extremes and potential reversal points. For added flexibility, you can also switch to Z-Score line plots based on either Close prices or OHLC4 averages.

With clear threshold lines (±2σ and ±3σ) marking moderate and extreme price deviations, and color-coded zones to highlight overbought and oversold areas, the oscillator simplifies complex statistical concepts into actionable trading insights.

Temporary Help Services Jobs - Trend Allocation StrategyThis strategy is designed to capitalize on the economic trends represented by the Temporary Help Services (TEMPHELPS) index, which is published by the Federal Reserve Economic Data (FRED). Temporary Help Services Jobs are often regarded as a leading indicator of labor market conditions, as changes in temporary employment levels frequently precede broader employment trends.

Methodology:

Data Source: The strategy uses the FRED dataset TEMPHELPS for monthly data on temporary help services.

Trend Definition:

Uptrend: When the current month's value is greater than the previous month's value.

Downtrend: When the current month's value is less than the previous month's value.

Entry Condition: A long position is opened when an uptrend is detected, provided no position is currently held.

Exit Condition: The long position is closed when a downtrend is detected.

Scientific Basis:

The TEMPHELPS index serves as a leading economic indicator, as noted in studies analyzing labor market cyclicality (e.g., Katz & Krueger, 1999). Temporary employment is often considered a proxy for broader economic conditions, particularly in predicting recessions or recoveries. Incorporating this index into trading strategies allows for aligning trades with potential macroeconomic shifts, as suggested by research on employment trends and market performance (Autor, 2001; Valetta & Bengali, 2013).

Usage:

This strategy is best suited for long-term investors or macroeconomic trend followers who wish to leverage labor market signals for equity or futures trading. It operates exclusively on end-of-month data, ensuring minimal transaction costs and noise.

Option Time ValueThis TradingView script calculates and visualizes the time value of an option (Call or Put) based on its market price and intrinsic value. The time value represents the premium paid for the option above its intrinsic value, and it is a key metric for analyzing the cost of holding an option.

This script is suitable for traders analyzing options on indices or stocks, such as the NIFTY 50, and supports both Call and Put options. By dynamically extracting the strike price and option type from the input symbol, it adapts seamlessly to the selected instrument.

Key Features:

Dynamic Instrument Selection:

Users can input the underlying asset (e.g., NSE:NIFTY) and the specific option instrument (e.g., NSE:NIFTY250327C24000 for a Call or NSE:NIFTY250327P24000 for a Put).

Automatic Option Type Detection:

The script detects whether the option is a Call or a Put by parsing the input symbol for the characters "C" (Call) or "P" (Put).

Dynamic Strike Price Extraction:

The strike price is dynamically extracted from the input option symbol, eliminating the need for hardcoding and reducing user errors.

Key Metrics Plotted:

Time Value: The premium paid above the intrinsic value, plotted in blue.

Intrinsic Value: The calculated intrinsic value of the option, plotted in green.

Seamless Integration:

Designed for ease of use and integration into existing TradingView setups.

Automatically adjusts to the timeframe and pricing data of the selected instruments.

McClellan A-D Volume Integration ModelThe strategy integrates the McClellan A-D Oscillator with an adjustment based on the Advance/Decline (A-D) volume data. The McClellan Oscillator is calculated by taking the difference between the short-term and long-term exponential moving averages (EMAs) of the A-D line. This strategy introduces an enhancement where the A-D volume (the difference between the advancing and declining volume) is factored in to adjust the oscillator value.

Inputs:

• ema_short_length: The length for the short-term EMA of the A-D line.

• ema_long_length: The length for the long-term EMA of the A-D line.

• osc_threshold_long: The threshold below which the oscillator must drop for an entry signal to trigger.

• exit_periods: The number of periods after which the position is closed.

• Data Sources:

• ad_advance and ad_decline are the data sources for advancing and declining issues, respectively.

• vol_advance and vol_decline are the volume data for the advancing and declining issues. If volume data is unavailable, it defaults to na (Not Available), and the fallback logic ensures that the strategy continues to function.

McClellan Oscillator with Volume Adjustment:

• The A-D line is calculated by subtracting the declining issues from the advancing issues. Then, the volume difference is applied to this line, creating a “weighted” A-D line.

• The short and long EMAs are calculated for the weighted A-D line to generate the McClellan Oscillator.

Entry Condition:

• The strategy looks for a reversal signal, where the oscillator falls below the threshold and then rises above it again. The condition is designed to trigger a long position when this reversal happens.

Exit Condition:

• The position is closed after a set number of periods (exit_periods) have passed since the entry.

Plotting:

• The McClellan Oscillator and the threshold are plotted on the chart for visual reference.

• Entry and exit signals are highlighted with background colors to make the signals more visible.

Scientific Background:

The McClellan A-D Oscillator is a popular market breadth indicator developed by Sherman and Marian McClellan. It is used to gauge the underlying strength of a market by analyzing the difference between the number of advancing and declining stocks. The oscillator is typically calculated using exponential moving averages (EMAs) of the A-D line, with the idea being that crossovers of these EMAs indicate potential changes in the market’s direction.

The integration of A-D volume into this model adds another layer of analysis, as volume is often considered a leading indicator of price movement. By factoring in volume, the strategy becomes more sensitive to not just the number of advancing or declining stocks but also how significant those movements are based on trading volume, as discussed in Schwager, J. D. (1999). Technical Analysis of the Financial Markets. This enhanced version aims to capture stronger and more sustainable trends in the market, helping to filter out false signals.

Additionally, volume analysis is often used to confirm price movements, as described in Wyckoff, R. (1931). The Day Trading System. Therefore, incorporating the volume of advancing and declining stocks in the McClellan Oscillator offers a more robust signal for trading decisions.

Z-Strike RecoveryThis strategy utilizes the Z-Score of daily changes in the VIX (Volatility Index) to identify moments of extreme market panic and initiate long entries. Scientific research highlights that extreme volatility levels often signal oversold markets, providing opportunities for mean-reversion strategies.

How the Strategy Works

Calculation of Daily VIX Changes:

The difference between today’s and yesterday’s VIX closing prices is calculated.

Z-Score Calculation:

The Z-Score quantifies how far the current change deviates from the mean (average), expressed in standard deviations:

Z-Score=(Daily VIX Change)−MeanStandard Deviation

Z-Score=Standard Deviation(Daily VIX Change)−Mean

The mean and standard deviation are computed over a rolling period of 16 days (default).

Entry Condition:

A long entry is triggered when the Z-Score exceeds a threshold of 1.3 (adjustable).

A high positive Z-Score indicates a strong overreaction in the market (panic).

Exit Condition:

The position is closed after 10 periods (days), regardless of market behavior.

Visualizations:

The Z-Score is plotted to make extreme values visible.

Horizontal threshold lines mark entry signals.

Bars with entry signals are highlighted with a blue background.

This strategy is particularly suitable for mean-reverting markets, such as the S&P 500.

Scientific Background

Volatility and Market Behavior:

Studies like Whaley (2000) demonstrate that the VIX, known as the "fear gauge," is highly correlated with market panic phases. A spike in the VIX is often interpreted as an oversold signal due to excessive hedging by investors.

Source: Whaley, R. E. (2000). The investor fear gauge. Journal of Portfolio Management, 26(3), 12-17.

Z-Score in Financial Strategies:

The Z-Score is a proven method for detecting statistical outliers and is widely used in mean-reversion strategies.

Source: Chan, E. (2009). Quantitative Trading. Wiley Finance.

Mean-Reversion Approach:

The strategy builds on the mean-reversion principle, which assumes that extreme market movements tend to revert to the mean over time.

Source: Jegadeesh, N., & Titman, S. (1993). Returns to Buying Winners and Selling Losers: Implications for Stock Market Efficiency. Journal of Finance, 48(1), 65-91.

MA Deviation Suite [InvestorUnknown]This indicator combines advanced moving average techniques with multiple deviation metrics to offer traders a versatile tool for analyzing market trends and volatility.

Moving Average Types :

SMA, EMA, HMA, DEMA, FRAMA, VWMA: Standard moving averages with different characteristics for smoothing price data.

Corrective MA: This method corrects the MA by considering the variance, providing a more responsive average to price changes.

f_cma(float src, simple int length) =>

ma = ta.sma(src, length)

v1 = ta.variance(src, length)

v2 = math.pow(nz(ma , ma) - ma, 2)

v3 = v1 == 0 or v2 == 0 ? 1 : v2 / (v1 + v2)

var tolerance = math.pow(10, -5)

float err = 1

// Gain Factor

float kPrev = 1

float k = 1

for i = 0 to 5000 by 1

if err > tolerance

k := v3 * kPrev * (2 - kPrev)

err := kPrev - k

kPrev := k

kPrev

ma := nz(ma , src) + k * (ma - nz(ma , src))

Fisher Least Squares MA: Aims to reduce lag by using a Fisher Transform on residuals.

f_flsma(float src, simple int len) =>

ma = src

e = ta.sma(math.abs(src - nz(ma )), len)

z = ta.sma(src - nz(ma , src), len) / e

r = (math.exp(2 * z) - 1) / (math.exp(2 * z) + 1)

a = (bar_index - ta.sma(bar_index, len)) / ta.stdev(bar_index, len) * r

ma := ta.sma(src, len) + a * ta.stdev(src, len)

Sine-Weighted MA & Cosine-Weighted MA: These give more weight to middle bars, creating a smoother curve; Cosine weights are shifted for a different focus.

Deviation Metrics :

Average Absolute Deviation (AAD) and Median Absolute Deviation (MAD): AAD calculates the average of absolute deviations from the MA, offering a measure of volatility. MAD uses the median, which can be less sensitive to outliers.

Standard Deviation (StDev): Measures the dispersion of prices from the mean.

Average True Range (ATR): Reflects market volatility by considering the day's range.

Average Deviation (adev): The average of previous deviations.

// Calculate deviations

float aad = f_aad(src, dev_len, ma) * dev_mul

float mad = f_mad(src, dev_len, ma) * dev_mul

float stdev = ta.stdev(src, dev_len) * dev_mul

float atr = ta.atr(dev_len) * dev_mul

float avg_dev = math.avg(aad, mad, stdev, atr)

// Calculated Median with +dev and -dev

float aad_p = ma + aad

float aad_m = ma - aad

float mad_p = ma + mad

float mad_m = ma - mad

float stdev_p = ma + stdev

float stdev_m = ma - stdev

float atr_p = ma + atr

float atr_m = ma - atr

float adev_p = ma + avg_dev

float adev_m = ma - avg_dev

// upper and lower

float upper = f_max4(aad_p, mad_p, stdev_p, atr_p)

float upper2 = f_min4(aad_p, mad_p, stdev_p, atr_p)

float lower = f_min4(aad_m, mad_m, stdev_m, atr_m)

float lower2 = f_max4(aad_m, mad_m, stdev_m, atr_m)

Determining Trend

The indicator generates trend signals by assessing where price stands relative to these deviation-based lines. It assigns a trend score by summing individual signals from each deviation measure. For instance, if price crosses above the MAD-based upper line, it contributes a bullish point; crossing below an ATR-based lower line contributes a bearish point.

When the aggregated trend score crosses above zero, it suggests a shift towards a bullish environment; crossing below zero indicates a bearish bias.

// Define Trend scores

var int aad_t = 0

if ta.crossover(src, aad_p)

aad_t := 1

if ta.crossunder(src, aad_m)

aad_t := -1

var int mad_t = 0

if ta.crossover(src, mad_p)

mad_t := 1

if ta.crossunder(src, mad_m)

mad_t := -1

var int stdev_t = 0

if ta.crossover(src, stdev_p)

stdev_t := 1

if ta.crossunder(src, stdev_m)

stdev_t := -1

var int atr_t = 0

if ta.crossover(src, atr_p)

atr_t := 1

if ta.crossunder(src, atr_m)

atr_t := -1

var int adev_t = 0

if ta.crossover(src, adev_p)

adev_t := 1

if ta.crossunder(src, adev_m)

adev_t := -1

int upper_t = src > upper ? 3 : 0

int lower_t = src < lower ? 0 : -3

int upper2_t = src > upper2 ? 1 : 0

int lower2_t = src < lower2 ? 0 : -1

float trend = aad_t + mad_t + stdev_t + atr_t + adev_t + upper_t + lower_t + upper2_t + lower2_t

var float sig = 0

if ta.crossover(trend, 0)

sig := 1

else if ta.crossunder(trend, 0)

sig := -1

Backtesting and Performance Metrics

The code integrates with a backtesting library that allows traders to:

Evaluate the strategy historically

Compare the indicator’s signals with a simple buy-and-hold approach

Generate performance metrics (e.g., mean returns, Sharpe Ratio, Sortino Ratio) to assess historical effectiveness.

Practical Usage and Calibration

Default settings are not optimized: The given parameters serve as a starting point for demonstration. Users should adjust:

len: Affects how smooth and lagging the moving average is.

dev_len and dev_mul: Influence the sensitivity of the deviation measures. Larger multipliers widen the bands, potentially reducing false signals but introducing more lag. Smaller multipliers tighten the bands, producing quicker signals but potentially more whipsaws.

This flexibility allows the trader to tailor the indicator for various markets (stocks, forex, crypto) and time frames.

Disclaimer

No guaranteed results: Historical performance does not guarantee future outcomes. Market conditions can vary widely.

User responsibility: Traders should combine this indicator with other forms of analysis, appropriate risk management, and careful calibration of parameters.

Ultra Trade JournalThe Ultra Trade Journal is a powerful TradingView indicator designed to help traders meticulously document and analyze their trades. Whether you're a novice or an experienced trader, this tool offers a clear and organized way to visualize your trading strategy, monitor performance, and make informed decisions based on detailed trade metrics.

Detailed Description

The Ultra Trade Journal indicator allows users to input and visualize critical trade information directly on their TradingView charts.

.........

User Inputs

Traders can specify entry and exit prices , stop loss levels, and up to four take profit targets.

.....

Dynamic Plotting

Once the input values are set, the indicator automatically plots horizontal lines for entry, exit, stop loss, and each take profit level on the chart. These lines are visually distinct, using different colors and styles (solid, dashed, dotted) to represent each element clearly.

.....

Live Position Tracking

If enabled, the indicator can adjust the exit price in real-time based on the current market price, allowing traders to monitor live positions effectively.

.....

Tick Calculations

The script calculates the number of ticks between the entry price and each exit point (stop loss and take profits). This helps in understanding the movement required for each target and assessing the potential risk and reward.

.....

Risk-Reward Ratios

For each take profit level, the indicator computes the risk-reward (RR) ratio by comparing the ticks at each target against the stop loss ticks. This provides a quick view of the potential profitability versus the risk taken.

.....

Comprehensive Table Display

A customizable table is displayed on the chart, summarizing all key trade details. This includes the entry and exit prices, stop loss and take profit levels, tick counts, and their respective RR ratios.

Users can adjust the table's Position and text color to suit their preferences.

.....

Visual Enhancements

The indicator uses adjustable background shading between entry and stop loss/take profit lines to visually represent potential trade outcomes. This shading adjusts based on whether the trade is long or short, providing an intuitive understanding of trade performance.

.........

Overall, the Ultra Trade Journal combines visual clarity with detailed analytics, enabling traders to keep a well-organized record of their trades and enhance their trading strategies through insightful data.

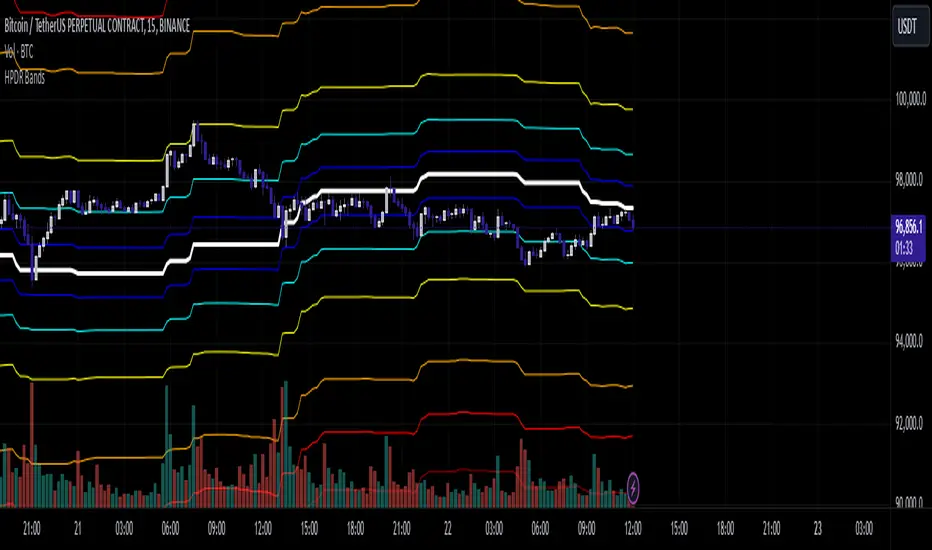

HPDR Bands IndicatorThe HPDR Bands indicator is a customizable tool designed to help traders visualize dynamic price action zones. By combining historical price ranges with adaptive bands, this script provides clear insights into potential support, resistance, and midline levels. The indicator is well-suited for all trading styles, including trend-following and range-bound strategies.

Features:

Dynamic Price Bands: Calculates price zones based on historical highs and lows, blending long-term and short-term price data for responsive adaptation to current market conditions.

Probability Enhancements: Includes a probability plot derived from the relative position of the closing price within the range, adjusted for volatility to highlight potential price movement scenarios.

Fibonacci-Like Levels: Highlights key levels (100%, 95%, 88%, 78%, 61%, 50%, and 38%) for intuitive visualization of price zones, aiding in identifying high-probability trading opportunities.

Midline Visualization: Displays a midline that serves as a reference for price mean reversion or breakout analysis.

How to Use:

Trending Markets: Use the adaptive upper and lower bands to gauge potential breakout or retracement zones.

Range-Bound Markets: Identify support and resistance levels within the defined price range.

Volatility Analysis: Observe the probability plot and its sensitivity to volatility for informed decision-making.

Important Notes:

This script is not intended as investment advice. It is a tool to assist with market analysis and should be used alongside proper risk management and other trading tools.

The script is provided as-is and without warranty. Users are encouraged to backtest and validate its suitability for their specific trading needs.

Happy Trading!

If you find this script helpful, consider sharing your feedback or suggestions for improvement. Collaboration strengthens the TradingView community, and your input is always appreciated!

Bitcoin Premium [SAKANE]Overview

"Bitcoin Premium " is an indicator designed to analyze the price differences (premiums) of Bitcoin between major exchanges. By using this tool, you can visualize these differences and trends across exchanges, helping you make more informed trading decisions.

Features

1. Premium Calculation and Display

- Calculates and visualizes the price differences between major exchanges like Coinbase, Bitfinex, Upbit, and Binance.

- Premiums are displayed in a histogram format for intuitive analysis.

2. Forex Rate Adjustment

- Prices quoted in KRW (e.g., from Upbit) are converted to USD using real-time KRW/USD forex rates.

3. Moving Average Option

- Displays moving averages (SMA or EMA) of premiums for a clearer view of long-term trends.

4. Customizable Settings

- Toggle the premium display for each exchange on or off.

- Includes label displays to support visual analysis.

What Can It Do for You?

1. Identify Arbitrage Opportunities

By observing price differences (premiums) between exchanges, you can identify arbitrage opportunities.

Example: If Bitcoin is cheaper on Binance and more expensive on Coinbase, you could buy on Binance and sell on Coinbase to capture the price difference.

2. Understand Regional Supply and Demand Trends

Each exchange's premium reflects the supply and demand dynamics of its respective region.

Example: A high premium on Upbit may indicate excess demand or regulatory impacts in the South Korean market.

3. Analyze Liquidity

Price differences often highlight liquidity disparities between exchanges. Markets with lower trading volumes tend to have larger premiums due to price distortions.

4. Evaluate Macroeconomic Impacts

Premium movements may reflect changes in macroeconomic factors, such as exchange rates, regulations, or financial conditions specific to each region.

5. Analyze Trends and Market Sentiment

By tracking premium trends, you can gauge market sentiment and understand regional or exchange-specific behaviors to inform your investment decisions.

6. Support Strategic Trading

This tool is useful for short-term arbitrage strategies as well as long-term evaluations of market health.

Exchange Characteristics and Premium Implications

The meaning of premiums varies by exchange.

- Coinbase (US Market)

Primarily used by investors buying directly with fiat currency (USD). A higher premium often signals bullish sentiment among institutional and retail investors.

- Bitfinex (Global Market)

A trader-focused exchange with active large-scale and leveraged trading. Premiums may reflect liquidity and risk appetite.

- Upbit (South Korean Market)

Priced in KRW, making it subject to forex rates and local market dynamics. High premiums may indicate strong demand or regulatory influences in South Korea.

- Binance (Global Market)

The largest exchange by trading volume. Premiums here are often a reflection of the overall market balance.

Notes

- This indicator is for reference only and does not guarantee trading decisions.

- Please consider the characteristics and conditions of each exchange when using this tool.

VIX Spike StrategyThis script implements a trading strategy based on the Volatility Index (VIX) and its standard deviation. It aims to enter a long position when the VIX exceeds a certain number of standard deviations above its moving average, which is a signal of a volatility spike. The position is then exited after a set number of periods.

VIX Symbol (vix_symbol): The input allows the user to specify the symbol for the VIX index (typically "CBOE:VIX").

Standard Deviation Length (stddev_length): The number of periods used to calculate the standard deviation of the VIX. This can be adjusted by the user.

Standard Deviation Multiplier (stddev_multiple): This multiplier is used to determine how many standard deviations above the moving average the VIX must exceed to trigger a long entry.

Exit Periods (exit_periods): The user specifies how many periods after entering the position the strategy will exit the trade.

Strategy Logic:

Data Loading: The script loads the VIX data, both for the current timeframe and as a rescaled version for calculation purposes.

Standard Deviation Calculation: It calculates both the moving average (SMA) and the standard deviation of the VIX over the specified period (stddev_length).

Entry Condition: A long position is entered when the VIX exceeds the moving average by a specified multiple of its standard deviation (calculated as vix_mean + stddev_multiple * vix_stddev).

Exit Condition: After the position is entered, it will be closed after the user-defined number of periods (exit_periods).

Visualization:

The VIX is plotted in blue.

The moving average of the VIX is plotted in orange.

The threshold for the VIX, which is the moving average plus the standard deviation multiplier, is plotted in red.

The background turns green when the entry condition is met, providing a visual cue.

Sources:

The VIX is often used as a measure of market volatility, with high values indicating increased uncertainty in the market.

Standard deviation is a statistical measure of the variability or dispersion of a set of data points. In financial markets, it is used to measure the volatility of asset prices.

References:

Bollerslev, T. (1986). "Generalized Autoregressive Conditional Heteroskedasticity." Journal of Econometrics.

Black, F., & Scholes, M. (1973). "The Pricing of Options and Corporate Liabilities." Journal of Political Economy.

Enhanced Effort vs Result Analysis V.2How to Use in Trading

A. Confirm Breakouts

Check if the Effort-Result Ratio or Z-Score spikes above the Upper Band or Z > +2:

Suggests a strong, efficient price move.

Supports breakout continuation.

B. Identify Reversal or Exhaustion

Look for Effort-Result Ratio or Z-Score dropping below the Lower Band or Z < -2:

Indicates high effort but low price movement (inefficiency).

Often signals potential trend reversal or consolidation.

C. Assess Efficiency of Trends

Use Relative Efficiency Index (REI):

REI near 1 during a trend → Confirms strength (efficient movement).

REI near 0 → Weak or inefficient movement, likely signaling exhaustion.

D. Evaluate Volume-Price Relationship

Monitor the Volume-Price Correlation:

Positive correlation (+1): Confirms price is driven by volume.

Negative correlation (-1): Indicates divergence; price moves independently of volume (potential warning signal).

3. Example Scenarios

Scenario 1: Breakout Confirmation

Effort-Result Ratio spikes above the Upper Band.

Z-Score exceeds +2.

REI approaches 1.

Volume-Price Correlation is positive (near +1).

Action: Strong breakout confirmation → Trend continuation likely.

Scenario 2: Reversal or Exhaustion

Effort-Result Ratio drops below the Lower Band.

Z-Score is below -2.

REI approaches 0.

Volume-Price Correlation weakens or turns negative.

Action: Signals trend exhaustion → Watch for reversal or consolidation.

Scenario 3: Range-Bound Market

Effort-Result Ratio stays within the Bollinger Bands.

Z-Score remains between -1 and +1.

REI fluctuates around 0.5 (neutral efficiency).

Volume-Price Correlation hovers near 0.

Action: Normal conditions → Look for breakout signals before acting.

*IMPORTANT*

There is a problem with the overlay ... How to fix some of it

The Standard Deviation bands dont work while the other variable activated so Id suggest deselecting them. The fix for this is to make sure you have the background selected and by doing this it will highlight on the chart ( you may need to increase the opacity ) when the bands ( Second standard deviation) are touched.

- Also you can use them all at once if you can but you do not need to

Market Flow Volatility Oscillator (AiBitcoinTrend)The Market Flow Volatility Oscillator (AiBitcoinTrend) is a cutting-edge technical analysis tool designed to evaluate and classify market volatility regimes. By leveraging Gaussian filtering and clustering techniques, this indicator provides traders with clear insights into periods of high and low volatility, helping them adapt their strategies to evolving market conditions. Built for precision and clarity, it combines advanced mathematical models with intuitive visual feedback to identify trends and volatility shifts effectively.

👽 How the Indicator Works

👾 Volatility Classification with Gaussian Filtering

The indicator detects volatility levels by applying Gaussian filters to the price series. Gaussian filters smooth out noise while preserving significant price movements. Traders can adjust the smoothing levels using sigma parameters, enabling greater flexibility:

Low Sigma: Emphasizes short-term volatility.

High Sigma: Captures broader trends with reduced sensitivity to small fluctuations.

👾 Clustering Algorithm for Regime Detection

The core of this indicator is its clustering model, which classifies market conditions into two distinct regimes:

Low Volatility Regime: Calm periods with reduced market activity.

High Volatility Regime: Intense periods with heightened price movements.

The clustering process works as follows:

A rolling window of data is analyzed to calculate the standard deviation of price returns.

Two cluster centers are initialized using the 25th and 75th percentiles of the data distribution.

Each price volatility value is assigned to the nearest cluster based on its distance to the centers.

The cluster centers are refined iteratively, providing an accurate and adaptive classification.

👾 Oscillator Generation with Slope R-Values

The indicator computes Gaussian filter slopes to generate oscillators that visualize trends:

Oscillator Low: Captures low-frequency market behavior.

Oscillator High: Tracks high-frequency, faster-changing trends.

The slope is measured using the R-value of the linear regression fit, scaled and adjusted for easier interpretation.

👽 Applications

👾 Trend Trading

When the oscillator rises above 0.5, it signals potential bullish momentum, while dips below 0.5 suggest bearish sentiment.

👾 Pullback Detection

When the oscillator peaks, especially in overbought or oversold zones, provide early warnings of potential reversals.

👽 Indicator Settings

👾 Oscillator Settings

Sigma Low/High: Controls the smoothness of the oscillators.

Smaller Values: React faster to price changes but introduce more noise.

Larger Values: Provide smoother signals with longer-term insights.

👾 Window Size and Refit Interval

Window Size: Defines the rolling period for cluster and volatility calculations.

Shorter windows: adapt faster to market changes.

Longer windows: produce stable, reliable classifications.

Disclaimer: This information is for entertainment purposes only and does not constitute financial advice. Please consult with a qualified financial advisor before making any investment decisions.

Intrabar DistributionThe Intrabar Distribution publication is an extension of the Intrabar BoxPlot publication. Besides a boxplot, it showcases price and volume distribution using intrabar Lower Timeframe (LTF) values (close) which can be displayed on the chart or in a separate pane.

🔶 USAGE

Intrabar Distribution has several features, users can display:

Recent candle for comparison against the other features

Boxplot of recent candle

Price distribution (optionally displayed as a curve)

Volume distribution

🔹 Recent candle / Boxplot

The middle 50% intrabar close values (Interquartile range, or IQR) are shown as a box, where the upper limit is percentile 75 (p75), and the lower limit is percentile 25 (p25). The dashed lines show the addition/subtraction of 1.5*IQR. All values out of range are considered outliers. They are displayed as white dots within the IQR*1.5 range or white X's when beyond the IQR*3 range (extreme outliers).

By showing the middle 50% intrabar values through a box, we can more easily see where the intrabar activity is mainly situated.

Note in the example above an upward-directed candle with a negative volume delta, displayed as a red box and dot (see further).

As seen in the following example, compared against the recent candle (grey candle at the left), most of the intrabar activity lies just beneath the opening price.

Note that results will be more accurate when more data is available, which can be done by making the difference between the current timeframe and the intrabar timeframe large enough.

🔹 Price / Volume distribution

The price and volume distribution can be helpful for highlighting areas of interest.

Here, we can see two areas where intrabar closing prices are mainly positioned.

The following example shows three successive bars. The recent bar is displayed on the left side, together with the volume distribution. The boxplot and price distribution are displayed on the right.

You can see the difference between volume and price distribution.

At the first bar, most price activity is at the top, while most of the volume was generated at the bottom; in other words, the price got briefly in the bottom region, with high volume before it returned.

At the second bar, price and volume are relatively equally distributed, which fits for indecisiveness.

The third bar shows more volume at a higher region; most intrabar closing prices are above the closing price.

Following example shows the same with 'Curve shaped' enabled (Settings: 'Price Distribution')

When 'Curve shaped' is enabled, lines/labels are shown with the standard deviation distance.

A blue 'guide line' can be enabled for easier interpretation.

🔹 Volume Delta

When there is a discrepancy between the delta volume and direction of the candle, this will be displayed as follows:

Red candle: when the sum of the volume of green intrabars is higher than the sum of the volume of red intrabars, the 'mean dot' will be coloured green.

Green candle: when the sum of the volume of red intrabars is higher than the sum of the volume of green intrabars, the 'mean dot' will be coloured red.

🔶 DETAILS

The intrabar values are sorted and split in parts/sections. The number of values in each section is displayed as a white line

The same principle applies to volume distribution, where the sum of volume per section is displayed as an orange area.

The boxplot displays several price values

Last close price

Highest / lowest intrabar close price

Median

p25 / p75

🔹 LTF settings

When 'Auto' is enabled (Settings, LTF), the LTF will be the nearest possible x times smaller TF than the current TF. When 'Premium' is disabled, the minimum TF will always be 1 minute to ensure TradingView plans lower than Premium don't get an error.

Examples with current Daily TF (when Premium is enabled):

500 : 3 minute LTF

1500 (default): 1 minute LTF

5000: 30 seconds LTF (1 minute if Premium is disabled)

🔶 SETTINGS

Location: Chart / Pane (when pane is opted, move the indicator to a separate pane as well)

Parts: divides the intrabar close values into parts/sections

Offset: offsets every drawing at once

Width: width of drawings, only applicable on "location: chart"

Label size: size of price labels

🔹 LTF

LTF: LTF setting

Auto + multiple: Adjusts the initial set LTF

Premium: Enable when your TradingView plan is Premium or higher

🔹 Current Bar

Display toggle + color setting

Offset: offsets only the 'Current Bar' drawing

🔹 Intrabar Boxplot

Display toggle + Colors, dependable on different circumstances.

Up: Price goes up, with more bullish than bearish intrabar volume.

Up-: Price goes up, with more bearish than bullish intrabar volume.

Down: Price goes down, with more bearish than bullish intrabar volume.

Down+: Price goes down, with more bullish than bearish intrabar volume.

Offset: offsets only the 'Boxplot' drawing

🔹 Price distribution

Display toggle + Color.

Curve Shaped

Guide Lines: Display 2 blue lines

Display Price: Show price of 'x' standard deviation

Offset: offsets only the 'Price distribution' drawing

Label size: size of price labels (standard deviation)

🔹 Volume distribution

Display toggle + Color.

Offset: offsets only the 'Volume distribution' drawing

🔹 Table

Show TF: Show intrabar Timeframe.

Textcolor

Size Table: Text Size

Intrabar BoxPlotThe Intrabar BoxPlot publication highlights an uncommon technique by displaying statistical intrabar Lower Timeframe (LTF) values on the chart.

🔶 USAGE

🔹 Middle 50% Boxes

By showing the middle 50% intrabar values through a box, we can more easily see where the intrabar activity is mainly situated.

The middle 50% intrabar values are referred to from here on as Interquartile range (IQR).

In this example, the successive IQRs form a channel where the price eventually breaks out.

Disproportionately distributed values can give insights which can be used to find potential support/resistance areas.

IQR gaps can give valuable information as well. Potentially, the price can return to these gaps.

Seeing the IQR areas against regular candles gives an alternative image of the underlying price movements.

🔹 Highest volume Price level

The script displays the price level with the highest volume situated, dependable on the user's source setting. Setting the source at 'close' will only display intrabar close values; the same goes for high, low, ...

As seen in the above example, the volume levels can aid in finding support/resistance.

🔹 Median

The location of the median off all intrabar values is displayed as a coloured dot: green when the close price is higher than the opening price and red if otherwise. The median can give valuable insights into price movements.

🔹 Outliers

Medium (white dots) and extreme (white X) outliers, in combination with the IQR box, can help identify potential areas of interest.

🔹 Volume Delta

When there is a discrepancy between the delta volume and direction of the candle, this will be displayed as follows:

Green candle: when the sum of the volume of red intrabars is higher than the sum of the volume of green intrabars, the candle will be coloured orange.

Red candle: when the sum of the volume of green intrabars is higher than the sum of the volume of red intrabars, the candle will be coloured blue.

🔹 Highlight Boxplot only

Probably the easiest way to display boxplot only is by changing the Bar's style to Bars .

🔶 DETAILS

All intrabar values (Lower TimeFrame - LTF) are sorted and evaluated. Values can be close , high , low , ... by selecting this in Settings ( source ).

The middle 50% of all values are displayed as a box; this contains the values between percentile 25 (p25) and percentile 75 (p75). The value of percentile rank 75 means 75% of all values are lower. The value of percentile rank 25 means 25% of all values are lower, or 75% is higher.

The difference between p75 and p25 is also known as Interquartile range (IQR)

IQR is used to check for outliers.

Wiki: Boxplot , Interquartile range

Extreme high: maximum value, higher than p75 + IQR*3

Max outlier high: maximum value, higher than p75 + IQR*1.5 but lower than p75 + IQR*3

Max: maximum value, lower than p75 + IQR*1.5

Min: minimum value, higher than p25 - IQR*1.5

Min outlier low: minimum value, lower than p25 - IQR*1.5 but higher than p25 - IQR*3

Extreme low: minimum value, lower than p25 - IQR*3

Max and min must not be interpreted with the current candle high/low.

🔹 Example: Length of chart-puppets

The following example can make it easier to digest. Forty "chart-puppets" are sorted by their length.

The p25 value is 97

The p50 value is 120

The p75 value is 149

75% of all "chart-puppets" are smaller than p75, and 25% is larger than p75.

50% of all "chart-puppets" are smaller than p50, and 50% is larger than p50 (= median).

25% of all "chart-puppets" are smaller than p25, and 75% is larger than p25.

IQR = 149 - 97 = 52

Extreme outlier limit max: p75 + IQR*3 = 149 + 52*3 = 305

Mild outlier limit max: p75 + IQR*1.5 = 149 + 52*1.5 = 227

Mild outlier limit min: p25 - IQR*1.5 = 97 - 52*1.5 = 19

Extreme outlier limit min: p25 - IQR*3 = 97 - 52*3 = -59

In this example there are no outliers to be found, all values are located between p25 - IQR*1.5 (19) and p75 + IQR*1.5. (227)

🔹 Source settings

Note that results are dependable on the chosen source (settings). When, for example, close is chosen as the source, only intrabar close prices are included. This means a low or high can stretch further then the min or max.

Here we can see different results with different source settings

🔹 LTF settings

When 'Auto' is enabled (Settings, LTF), the LTF will be the nearest possible x times smaller TF than the current TF. When 'Premium' is disabled, the minimum TF will always be 1 minute to ensure TradingView plans lower than Premium don't get an error.

Examples with current Daily TF (when Premium is enabled):

500 : 3 minute LTF

1500 (default): 1 minute LTF

5000: 30 seconds LTF (1 minute if Premium is disabled)

🔶 SETTINGS

Source: Set source at close, high, low,...

🔹 LTF

LTF: LTF setting

Auto + multiple: Adjusts the initial set LTF

Premium: Enable when your TradingView plan is Premium or higher

🔹 Intrabar Delta : Colors, dependable on different circumstances.

Up: Price goes up, with more bullish than bearish intrabar volume.

Up-: Price goes up, with more bearish than bullish intrabar volume.

Down: Price goes down, with more bearish than bullish intrabar volume.

Down+: Price goes down, with more bullish than bearish intrabar volume.

🔹 Table

Show table: Show details at the top right corner

Show TF: Show LTF at the bottom right corner

Text color/table size

See DETAILS for more information