Groupings [SS]Hey everyone,

Releasing this indicator called groupings.

If you watch/read my analyses on Tradingview, you will have heard me talk about groups. Groups is something I invented. What it is, is just taking the Euclidean Distance (ED) of the previous 5 candles in a specified period (i.e. daily timeframe, weekly, 1 minute, 5 minute, etc.) and rounding the ED up to a whole number.

I have had great success in this approach because the information provided is broad enough to give leniency in interpretation but narrow enough to hone in on potential moves and target prices.

This indicator is a simplified version of how I do groupings in other software, however it is no less powerful!

What do groups tell us?

A "group" takes into account the previous 5 candles, using the ED. This gives Pinescript a general idea of what the short term trend looks like mathematically. From there, Pinescript can look for other groups that looked similar to how this current trend looks. From there, it can offer us insights into what tends to happen in candles subsequent to this group. For example, the ATR range, the close range and whether it is bearish or bullish.

And that is precisely how this indicator operates, Pinescript will calculate the group of the previous 5 canndles in the timeframe period you are looking at. It will then lookback over the designated "train" length and identify previous groups, and what happened in those groups. It looks specifically at:

- What is that average High ATR associated with that group,

- What is the average Low ATR associated with that group,

- What is the average close range associated with that group,

- What is the sentiment associated with that group.

How to use the indicator?

In terms of use, the indicator is relatively simple to use. It will plot three lines, a red for the anticipated low range, a green for the anticipated high range and purple for the opening range (where the current candle opened at).

In addition, it will plot a dot for the anticipated close area. When the dot is green, it expects a bullish close. When the dot is red, it expects a bearish close.

The indicator is going to give you a heads up as to whether we are in a bullish group, what you can anticipate the high and low range to be and where you can anticipate the close.

Of course, its not always exact, as in the image above you can see it underestimated the high range and over-estimated the low range; however, we did close within the anticipate range.

The indicator is meant to help you with your bias. I will reference this indicator on the daily timeframe at open to see what the expectations are for the day.

However, you can use it on any timeframe you wish.

Other functions:

The indicator can plot the EMA 9, 21 and 5. These are the 3 indicators I like and I find them helpful for both intraday and swing trading. However, they can be toggled off if you do not wish to view them.

In addition, the EMAs will be green if the ticker is trending above the EMA 21 (which is a critical EMA for me to determine the immediate sentiment). If the ticker is below, they will turn red.

There is also the ability to adjust the train time. The default is 1,000 candles back, but I usually have it on 1500. If you have a lot of indicators and a lot going on, on your chart, you may find that 1500 is too much and it will lag/error. That’s okay, 500 candles is sufficient and will not put a lot of stress on Pinescript.

Concluding remarks

Its overall a fairly simple concept and indicator, but it has been a neat and helpful / insightful invention. I originally developed this using R and happy to have now brought it into Pinescript.

I hope you enjoy!

Safe trades everyone!

Statistics

Frequency and Volume ProfileFREQUENCY & VOLUME PROFILE

⚪ OVERVIEW

The Frequency and Volume Profile indicator plots a frequency or volume profile based on the visible bars on the chart, providing insights into price levels with significant trading activity.

⚪ USAGE

● Market Structure Analysis:

Identify key price levels where significant trading activity occurred, which can act as support and resistance zones.

● Volume Analysis:

Use the volume mode to understand where the highest trading volumes have occurred, helping to confirm strong price levels.

● Trend Confirmation:

Analyze the distribution of trading activity to confirm or refute trends, mark important levels as support and resistance, aiding in making more informed trading decisions.

● Frequency Distribution:

In statistics, a frequency distribution is a list of the values that a variable takes in a sample. It is usually a list. Displayed as a histogram.

⚪ SETTINGS

Source: Select the price data to use for the profile calculation (default: hl2).

Move Profile: Set the number of bars to offset the profile from the current bar (default: 100).

Mode: Choose between "Frequency" and "Volume" for the profile calculation.

Profile Color: Customize the color of the profile lines.

Lookback Period: Uses 5000 bars for daily and higher timeframes, otherwise 10000 bars.

The Frequency Profile indicator is a powerful tool for visualizing price levels with significant trading activity, whether in terms of frequency or volume. Its dynamic calculation and customizable settings make it a versatile addition to any trading strategy.

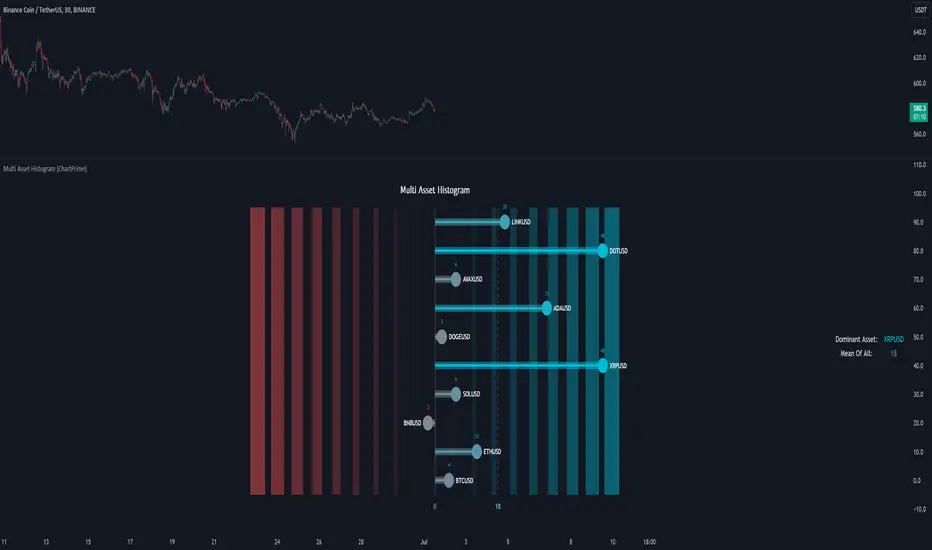

Multi Asset Histogram [ChartPrime]Multi Asset Histogram Indicator

Overview:

The "Multi Asset Histogram" indicator provides a comprehensive visualization of the performance of multiple assets relative to each other. By calculating a score for each asset and displaying it in a histogram format, this indicator helps traders quickly identify the trends, dominant asset and the average performance of the assets in the selected group.

Key Features:

◆ Multi-Asset Score Calculation:

The indicator calculates a trend score for each selected asset based on the price source (e.g., hl2).

The trend score is determined by comparing the current price to the prices over the past bars back defined by user, adding or subtracting points based on whether the current price is higher or lower than previous prices.

// Score Function

trscore(src) =>

total = 0.0

for i = 1 to 50

total += (src >= nz(src ) ? 1 : -1)

total

◆ Flexible Symbol Input:

Traders can input up to 10 different symbols (e.g., BTCUSD, ETHUSD, etc.) to be included in the histogram analysis.

◆ Dynamic Visualization:

A histogram is plotted for each asset, with bars colored based on the score, providing a clear visual representation of the relative performance.

Color gradients from red to aqua indicate the performance, with red representing negative scores and aqua representing positive scores.

◆ Adaptive Histogram Lines:

The width and placement of histogram lines adapt based on the calculated scores, ensuring clear visualization regardless of the values.

Dashed lines represent the mean score of all assets, helping traders identify the overall market trend.

◆Detailed Labels and Values:

Labels are placed on the histogram to display the exact score for each asset.

Mean value and zero line labels provide additional context for the overall performance.

◆ Visual Scaling Lines:

Zero line and mean line are clearly marked, helping traders understand the distribution and scale of scores.

Scales on the left and right of the histogram indicate the performance range.

◆ Informative Table:

A table is displayed on the chart, showing the dominant asset (the one with the highest score) and the mean score of all assets.

The table updates dynamically to reflect real-time changes in asset performance.

◆ Settings:

Length: The value of number bars back is greater or less than the current value of the source

Source: The price source to be used for score calculation (e.g., hl2).

Symbols: Up to 10 different asset symbols can be input for analysis.

Usage Notes:

This indicator is useful for traders who monitor multiple assets simultaneously and need a quick visual reference to identify the strongest and weakest performers.

The color coding and dynamic labels make it easy to interpret the relative performance and make informed trading decisions.

This indicator is designed to enhance multi-asset analysis by providing a clear, visual representation of each asset's performance relative to the others, making it easier to identify trends and dominant assets in the market.

Asset Drawdown & Drawdown HeatMap [InvestorUnknown]Overview

The "Asset Drawdown & Drawdown HeatMap" indicator is designed for educational purposes to help users visualize and analyze the drawdowns of various assets. It highlights both recent and historical drawdowns, offering valuable insights into the performance and risk of different investments. Additionally, it can serve as a complementary analysis tool for trading and investing decisions.

Features

Drawdown Calculation:

Computes the drawdown from the highest value (ATH) to the current value, showing the percentage decline.

Displays both the current drawdown and the maximum historical drawdown for the selected assets.

HeatMap Visualization:

Uses a gradient color scheme to represent the magnitude of drawdowns over a specified lookback period.

Helps identify periods of significant decline and recovery visually.

Multiple Assets:

Supports up to 10 different assets (adding more would make it harder to see the drawdowns of different assets), allowing users to compare drawdowns across various symbols.

Each asset can be individually plotted and color-coded for clarity.

Customizable Settings:

User inputs for high and low value calculations, color preferences, and lookback periods.

Option to color bars based on the drawdown heatmap.

Detailed Functionality

Drawdown Calculation:

The DD() function calculates the current drawdown and the maximum historical drawdown based on the high and low values.

The drawdown is calculated as 100 - (lowvalue / ATH * 100), where ATH is the highest value observed so far.

// - - - - - Custom Function - - - - - //{

DD() =>

ATH = highvalue

ATH := na(ATH ) ? highvalue : math.max(highvalue, ATH )

Drawdown = 100 - lowvalue / ATH * 100

MaxDrawdown = Drawdown

MaxDrawdown := na(MaxDrawdown ) ? Drawdown : math.max(Drawdown, MaxDrawdown )

//}

Security Request:

Uses the request.security() function to fetch drawdown data for each specified asset on a daily timeframe.

Computes both current drawdown (TnDD) and maximum drawdown (TnMDD) for each asset.

// - - - - - Create Variables - - - - - //{

= request.security("", "1D", DD()) // Chart

= request.security(t1, "1D", DD())

= request.security(t2, "1D", DD())

= request.security(t3, "1D", DD())

= request.security(t4, "1D", DD())

= request.security(t5, "1D", DD())

= request.security(t6, "1D", DD())

= request.security(t7, "1D", DD())

= request.security(t8, "1D", DD())

= request.security(t9, "1D", DD())

= request.security(t10, "1D", DD())

//}

Plotting:

Plots the drawdown values for each asset on the chart, with the option to enable or disable plotting for individual assets.

Colors the plotted lines and labels based on user-specified preferences.

HeatMap:

Creates a heatmap color gradient based on the drawdown values over the lookback period.

Colors the bars on the chart according to the heatmap to visualize drawdown severity over time.

// - - - - - HeatMap - - - - - //{

heatcol = color.from_gradient(T0DD, ta.lowest(T0DD,lookback), ta.highest(T0DD,lookback), topcol, botcol)

barcolor(colbars ? heatcol : na)

//}

Labels:

Displays labels for each asset's drawdown value at the end of the chart for quick reference.

This indicator is an excellent tool for educational purposes, helping users understand drawdown dynamics and their implications on asset performance. It also provides a visual aid for monitoring and comparing drawdowns across multiple assets, which can be beneficial for making informed trading and investment decisions.

Moving Average Cross Probability [AlgoAlpha]Moving Average Cross Probability 📈✨

The Moving Average Cross Probability by AlgoAlpha calculates the probability of a cross-over or cross-under between the fast and slow values of a user defined Moving Average type before it happens, allowing users to benefit by front running the market.

✨ Key Features:

📊 Probability Histogram: Displays the Probability of MA cross in the form of a histogram.

🔄 Data Table: Displays forecast information for quick analysis.

🎨 Customizable MAs: Choose from various moving averages and customize their length.

🚀 How to Use:

🛠 Add Indicator: Add the indicator to favorites, and customize the settings to suite your trading style.

📊 Analyze Market: Watch the indicator to look for trend shifts early or for trend continuations.

🔔 Set Alerts: Get notified of bullish/bearish points.

✨ How It Works:

The Moving Average Cross Probability Indicator by AlgoAlpha determines the probability by looking at a probable range of values that the price can take in the next bar and finds out what percentage of those possibilities result in the user defined moving average crossing each other. This is done by first using the HMA to predict what the next price value will be, a standard deviation based range is then calculated. The range is divided by the user defined resolution and is split into multiple levels, each of these levels represent a possible value for price in the next bar. These possible predicted values are used to calculate the possible MA values for both the fast and slow MAs that may occur in the next bar and are then compared to see how many of those possible MA results end up crossing each other.

Stay ahead of the market with the Moving Average Cross Probability Indicator AlgoAlpha! 📈💡

Exponential Grid [Phi, Pi, Euler]If you disagree with one of the EMH principles that price is too random, then by definition you must agree that historic price has deterministic function to a scenario ahead.

I personally believe that constants like phi, pi and e can mimic exponential growth of the price.

In this script, first grid is based on the Lowest price multiplied with self fraction of the constant.

For example:

If you are familiar with fib ratio 1.272, then you must know that it is 1.618 to the power of 0.5.

With default settings of exponent step 0.25

First grid = Lowest price x phi^0.25

Second grid = Lowest price x phi^0.25x2

Third grid = Lowest price x phi^0.25x3 and so on

The script will automatically find the lowest price and update the grid values.

Or you can set up your custom Lowest price manually if you feel like the All Time Low level loses its relevance value after long period.

There are 64 grids including Lowest price level. And it wasn't by a chance. Pine Script has a limitation of max 64 plots. Number of grids shown in the chart depends on the highest price. Once price breaks above ATH a couple of next grids will be plotted automatically. In most cases if everything is plotted, the chart appears squeezed and you'll need to zoom in to see it. Therefore, I adjusted it relatively to the scale of the chart for the comfort.

In some cases 64 plots aren't enough to cover the whole chart. For example, let's take a look at NVIDIA chart:

Since the price has started with 0.0333, it is way too small to cover all with default settings.

We are left with 2 choices:

Either Enable "Round"

OR increase Exponent Step (from 0.25 to 0.5 in the particular example below)

If you set constant to pi or e which is a bigger number than phi, expect the gaps to be bigger. To reduce it to a more gradual way of expansion you can decrease Exponent Step.

Volume, Volatility, and Momentum Metrics IndicatorVolume, Volatility, and Momentum Metrics Indicator

Welcome to our comprehensive TradingView indicator designed to provide traders with essential volume, volatility, and momentum metrics. This powerful tool is ideal for traders looking to enhance their market analysis by visualizing key indicators in a concise and easy-to-read format.

Key Features

1. Volume Metrics:

• Daily Dollar Volume: Understand the monetary value of the traded volume each day.

• Relative Volume (RVOL) Day: Compare the current volume to the previous day’s volume to gauge trading activity.

• Relative Volume (RVOL) 30D: Assess the average trading volume over the past 30 days.

• Relative Volume (RVOL) 90D: Evaluate the average trading volume over the past 90 days.

2. Volatility and Momentum Metrics:

• Average Daily Range (ADR) %: Measure the average daily price range as a percentage of the current price.

• Average True Range (ATR): Track the volatility by calculating the average true range over a specified period.

• Relative Strength Index (RSI): Determine the momentum by analyzing the speed and change of price movements.

3. Customizable Table Positions:

• Place the volume metrics table and the volatility/momentum metrics table in the bottom-left or bottom-right corners of your chart for optimal visibility and convenience.

Why Use This Indicator?

• Enhanced Market Analysis: Quickly assess volume trends, volatility, and momentum to make informed trading decisions.

• User-Friendly Interface: The clear and concise tables provide at-a-glance information without cluttering your chart.

• Customization Options: Choose where to display the tables to suit your trading style and preferences.

How It Works

This indicator uses advanced calculations to provide real-time data on trading volume, price range, and momentum. By displaying this information in separate, neatly organized tables, traders can easily monitor these critical metrics without diverting their focus from the main chart.

Who Can Benefit?

• Day Traders: Quickly gauge intraday trading activity and volatility.

• Swing Traders: Analyze longer-term volume trends and momentum to identify potential trade setups.

• Technical Analysts: Utilize comprehensive metrics to enhance technical analysis and trading strategies.

Get Started

To add this powerful indicator to your TradingView chart, simply search for “Volume, Volatility, and Momentum Metrics” in the TradingView public library, or use the provided link to add it directly to your chart. Enhance your trading analysis and make more informed decisions with our comprehensive TradingView indicator.

Price & Moving Average + Financial IndicatorThis indicator displays:

Moving Average that can be set into SMA or EMA: Default setting is SMA 50

Label price for today's MA

Basic Financial Data:

Type of Sector

Type of Industry

P/E Ratio

Price to Book Ratio

ROE

Revenue (FQ)

Earnings (FQ)

Once again, I let the script open for you guys to custom it based on your own preferences. Hope you guys enjoy it!

Hourly Opening PriceThe Inner Circle Trader has noted that the Opening Price of every Hourly candle can be used in a Power Of 3 (PO3) context.

If Bullish, buy BELOW the hourly open.

If Bearish, sell ABOVE the hourly open.

The Power of 3 ICT model also know as "AMD" is a transformative trading strategy, ingeniously designed to streamline your time analyzing charts by focusing on three pivotal phases in market behavior: accumulation, manipulation, and distribution.

The ICT Power of Three Model dissects the market maker’s algorithm for price delivery into three pivotal actions: Accumulation, Manipulation, and Distribution. Accumulation involves smart money gathering positions before a price surge, while manipulation sees the market creating deceptive movements to trigger stops. Finally, distribution occurs as smart money offloads positions, often catching less informed traders off-guard. This strategy is a critical tool for traders to understand market makers’ maneuvers and to strategically position themselves in the market.

This indicator plots a line at the opening price of each hour and extends it on the chart for the duration of the hour. Each hour starts a new line.

You also have the option of extending the midnight opening price line across the entire trading day.

Bitcoin Fundamentals - Bitcoin Block RewardThe Bitcoin Block Reward is the batch of new Bitcoins generated by the miners after solving each block.

The Block Reward is set as a basic rule and cannot be changed without agreement between the entire Bitcoin network. It started at 50 BTC during the first period. Afterwards the Block Reward gets adjusted to half of it value (Halving Event) on each cycle of 210000 blocks mined.

This is the only way that new bitcoins are created. It creates an incentive for miners to secure the network.

Over time the Block Reward will decreases to a value that might not cover the mining costs. At that point, the use of the Bitcoin Network might have increased sufficiently as to generate enough transaction fees to cover the mining costs.

MOTIVATION

Even though this is a very simple indicator, I'm currently missing a data source to compute the Block Reward value within Tradingview. Therefore, I created this indicator and its associated library function to enable its visualization and (eventually) for coders to make use of the source function to power more elaborate scripts related to the Halving Events.

Hope that helps!

CryptoLibrary "Crypto"

This Library includes functions related to crytocurrencies and their blockchain

btcBlockReward(t)

Delivers the BTC block reward for a specific date/time

Parameters:

t (int) : Time of the current candle

Returns: blockRewardBtc

Bearish vs Bullish ArgumentsThe Bearish vs Bullish Arguments Indicator is a tool designed to help traders visually assess and compare the number of bullish and bearish arguments based on their custom inputs. This script enables users to input up to five bullish and five bearish arguments, dynamically displaying the bias on a clean and customizable table on the chart. This provides traders with a clear, visual representation of the market sentiment they have identified.

Key Features:

Customizable Inputs: Users can input up to five bullish and five bearish arguments, which are displayed in a table on the chart.

Bias Calculation: The script calculates the bias (Bullish, Bearish, or Neutral) based on the number of bullish and bearish arguments provided.

Color Customization: Users can customize the colors for the table background, text, and headers, ensuring the table fits seamlessly into their charting environment.

Reset Functionality: A reset switch allows users to clear all input arguments with a single click, making it easy to start fresh.

How It Works:

Input Fields: The script provides input fields for up to five bullish and five bearish arguments. Each input is a simple text field where users can describe their arguments.

Bias Calculation: The script counts the number of non-empty bullish and bearish arguments and determines the overall bias. The bias is displayed in the table with a dynamically changing color to indicate whether the market sentiment is bullish, bearish, or neutral.

Customizable Table: The table is positioned on the chart according to the user's preference (top-left, top-right, bottom-left, bottom-right) and can be customized in terms of background color and text color.

How to Use:

Add the Indicator: Add the Bearish vs Bullish Arguments Indicator to your chart.

Input Arguments: Enter up to five bullish and five bearish arguments in the provided input fields in the script settings.

Customize Appearance: Adjust the table's background color, text color, and position on the chart to fit your preferences.

Example Use Case:

A trader might use this indicator to visually balance their arguments for and against a particular trade setup. By entering their reasons for a bullish outlook in the bullish argument fields and their reasons for a bearish outlook in the bearish argument fields, they can quickly see which side has more supporting points and make a more informed trading decision.

This script was inspired by Arjoio's concepts

Depth of Market (DOM) [LuxAlgo]The Depth Of Market (DOM) tool allows traders to look under the hood of any market, taking price and volume analysis to the next level. The following features are included: DOM, Time & Sales, Volume Profile, Depth of Market, Imbalances, Buying Pressure, and up to 24 key intraday levels (it really packs a punch).

As a disclaimer, this tool does not use tick data, it is a DOM reconstruction from the provided real-time time series data (price and volume). So the volume you see is from filled orders only, this tool does not show unfilled limit orders.

Traders can enable or disable any of the features at will to avoid being overwhelmed with too much information and to make the tool perform faster.

The features that have the biggest impact on performance are Historical Data Collection, Key Levels (POC & VWAP), Time & Sales, Profile, and Imbalances. Disable these features to improve the indicator computational performance.

🔶 DOM

This is the simplest form of the tool, a simple DOM or ladder that displays the following columns:

PRICE: Price level

BID: Total number of market sell orders filled or limit buy orders filled.

SELL: Sell market orders

BUY: Buy market orders

ASK: Total number of market buy orders filled or limit sell orders filled.

The DOM only collects historical data from the last 24 hours and real-time data.

Traders can select a reset period for the DOM with two options:

DAILY: Resets at the beginning of each trading day

SESSIONS: Resets twice, as DAILY and 15.5 hours later, to coincide with the start of the RTH session for US tickers.

The DOM has two main modes, it can display price levels as ticks or points. The default is automatic based on the current daily volatility, but traders can manually force one mode or the other if they wish.

For convenience, traders have the option to set the number of lines (price levels), and the size of the text and to display only real-time data.

By default, the top price is set to 0 so that the DOM automatically adjusts the price levels to be displayed, but traders can set the top price manually so that the tool displays only the desired price levels in a fixed manner.

🔹 Volume Profile

As additional features to the basic DOM, traders have access to the volume profile histogram and the total volume per price level.

This helps traders identify at a glance key price areas where volume is accumulating (high volume nodes) or areas where volume is lacking (low volume nodes) - these areas are important to some traders who base their decision-making process on them.

🔹 Imbalances

Other added features are imbalances and buying pressure:

Interlevel Imbalance: volume delta between two different price levels

Intralevel Imbalance: delta between buy and sell volume at the same price level

Buying Pressure Percent: percentage of buy volume compared to total volume

Imbalances can help traders identify areas of interest in the price for possible support or resistance.

🔹 Depth

Depth allows traders to see at a glance how much supply is above the current price level or how much demand is below the current price level.

Above the current price level shows the cumulative ask volume (filled sell limit orders) and below the current price level shows the cumulative bid volume (filled buy limit orders).

🔶 KEY LEVELS

The tool includes up to 24 different key intraday levels of particular relevance:

Previous Week Levels

PWH: Previous week high

PWL: Previous week low

PWM: Previous week middle

PWS: Previous week settlement (close)

Previous Day Levels

PDH: Previous day high

PDL: Previous day low

PDM: Previous day middle

PDS: Previous day settlement (close)

Current Day Levels

OPEN: Open of day (or session)

HOD: High of day (or session)

LOD: Low of day (or session)

MOD: Middle of day (or session)

Opening Range

ORH: Open range high

ORL: Open range low

Initial Balance

IBH: Initial balance high

IBL: Initial balance low

VWAP

+3SD: Volume weighted average price plus 3 standard deviations

+2SD: Volume weighted average price plus 2 standard deviations

+1SD: Volume weighted average price plus 1 standard deviation

VWAP: Volume weighted average price

-1SD: Volume weighted average price minus 1 standard deviation

-2SD: Volume weighted average price minus 2 standard deviations

-3SD: Volume weighted average price minus 3 standard deviations

POC: Point of control

Different traders look at different levels, the key levels shown here are objective and specific areas of interest that traders can act on, providing us with potential areas of support or resistance in the price.

🔶 TIME & SALES

The tool also features a full-time and sales panel with time, price, and size columns, a size filter, and the ability to set the timezone to display time in the trader's local time.

The information shown here is what feeds the DOM and it can be useful in several ways, for example in detecting absorption. If a large number of orders are coming into the market but the price is barely moving, this indicates that there is enough liquidity at these levels to absorb all these orders, so if these orders stop coming into the market, the price may turn around.

🔶 SETTINGS

Period: Select the anchoring period to start data collection, DAILY will anchor at the start of the trading day, and SESSIONS will start as DAILY and 15.5 hours later (RTH for US tickers).

Mode: Select between AUTO and MANUAL modes for displaying TICKS or POINTS, in AUTO mode the tool will automatically select TICKS for tickers with a daily average volatility below 5000 ticks and POINTS for the rest of the tickers.

Rows: Select the number of price levels to display

Text Size: Select the text size

🔹 DOM

DOM: Enable/Disable DOM display

Realtime only: Enable/Disable real-time data only, historical data will be collected if disabled

Top Price: Specify the price to be displayed on the top row, set to 0 to enable dynamic DOM

Max updates: Specify how many times the values on the SELL and BUY columns are accumulated until reset.

Profile/Depth size: Maximum size of the histograms on the PROFILE and DEPTH columns.

Profile: Enable/Disable Profile column. High impact on performance.

Volume: Enable/Disable Volume column. Total volume traded at price level.

Interlevel Imbalance: Enable/Disable Interlevel Imbalance column. Total volume delta between the current price level and the price level above. High impact on performance.

Depth: Enable/Disable Depth, showing the cumulative supply above the current price and the cumulative demand below. Impact on performance.

Intralevel Imbalance: Enable/Disable Intralevel Imbalance column. Delta between total buy volume and total sell volume. High impact on performance.

Buying Pressure Percent: Enable/Disable Buy Percent column. Percentage of total buy volume compared to total volume.

Imbalance Threshold %: Threshold for highlighting imbalances. Set to 90 to highlight the top 10% of interlevel imbalances and the top and bottom 10% of intra-level imbalances.

Crypto volume precision: Specify the number of decimals to display on the volume of crypto assets

🔹 Key Levels

Key Levels: Enable/Disable KEY column. Very high performance impact.

Previous Week: Enable/Disable High, Low, Middle, and Close of the previous trading week.

Previous Day: Enable/Disable High, Low, Middle, and Settlement of the previous trading day.

Current Day/Session: Enable/Disable Open, High, Low and Middle of the current period.

Open Range: Enable/Disable High and Low of the first candle of the period.

Initial Balance: Enable/Disable High and Low of the first hour of the period.

VWAP: Enable/Disable Volume-weighted average price of the period with 1, 2, and 3 standard deviations.

POC: Enable/Disable Point of Control (price level with the highest volume traded) of the period.

🔹 Time & Sales

Time & Sales: Enable/Disable time and sales panel.

Timezone offset (hours): Enter your time zone\'s offset (+ or −), including a decimal fraction if needed.

Order Size: Set order size filter. Orders smaller than the value are not displayed.

🔶 THANKS

Hi, I'm makit0 coder of this tool and proud member of the LuxAlgo Opensource team, it's an honor to be part of the LuxAlgo family doing something I love as it's writing opensource code and sharing it with the world. I'd like to thank all of you who use, comment on, and vote for all of our open-source tools, and all of you who give us your support.

And of course thanks to the PineCoders family for all the work in front of and behind the scenes that makes the PineScript community what it is, simply the best.

Peace, Love & PineScript!

PFCF Price BandPFCF Price Band shows price calculated using the previous period's high and low P/TTM FCFPS (TTM's price to free cash flow per share over the last 12 months) multiplied by TTM's current FCFPS ( Similar to price theory = P/E x expected earnings per share)

If the current P/FCFPS is lower than the minimum P/FCFPS, it is considered cheap. In other words, above the maximum P/FCFPS is considered expensive.

PFCF Price Band consists of 2 parts.

- Firstly, the historical P/FCFPS value in "Green" (if TTM FCFPS is positive) or "Red" (if TTM FCFPS is negative) status changes based on the latest high or low price of TTM FCFPS.

- Second, the blue line is the closing price divided by TTM FCFPS, which shows the current P/FCF.

P.S. It is recommended to use it together with the PE Band indicator because just net profit does not mean that a company has good cash flow.

ΔYoY(Economics)Year over year indicator which will benchmark the most recent data vs 1 year lookback; Will automate the lookback for quarterly and monthly data based on timeframe selected (3M for quarterly, 1M for monthly). Tradingview will aggregate weekly data into a monthly data point. SMA applied to get the average over some x period.

Ln(close)Natural log indicator for normalizing data. SMA applied so you can take the average of that normalization factor. Personally use it for US economic data where the value is very large (GDI, Fed Balance Sheet, USM2 etc.) and the year over year delta is not pertinent (USM2) or not available (GDI.. although I did make an indicator to get YoY :D). Any additional ideas leave a comment and I'll take a look.

Uptrick: Complex WMA Indicator with Trend Transitions

The "Complex WMA Indicator with Trend Transitions" is a technical analysis tool designed to help traders identify and visualize market trends using three Weighted Moving Averages (WMAs) of varying lengths. The primary purpose of this indicator is to provide a clearer and more nuanced view of market trends by highlighting bullish and bearish phases and filtering out noise, thereby enabling more informed trading decisions.

Detailed Explanation

This indicator allows users to set the lengths of three WMAs through input parameters. The default lengths are set to 10, 20, and 50, but users can customize these values according to their trading strategy. The WMAs are calculated using the closing prices of the specified periods, and the results are plotted on the chart in red, green, and blue, corresponding to the first, second, and third WMAs, respectively.

The indicator defines two primary conditions for trend analysis: bullish and bearish trends. A bullish trend is identified when both the shorter WMAs (first and second) are above the longest WMA (third), indicating upward momentum. Conversely, a bearish trend is identified when both the shorter WMAs are below the longest WMA, signaling downward momentum.

Crossover Signals and Trend Transitions

The script also identifies crossover signals between the first and second WMAs. A bullish crossover occurs when the first WMA crosses above the second WMA, generating a buy signal. This event is marked on the chart with a green upward label. A bearish crossover, marked with a red downward label, occurs when the first WMA crosses below the second WMA, indicating a sell signal.

To track the trend transitions effectively, the indicator employs a state machine. It maintains two variables, currentTrend and prevTrend, to store the current and previous trend states. The trend state is updated based on the defined trend conditions. When the trend changes from one state to another (e.g., from a bullish trend to a bearish trend), the indicator creates a label at the beginning of the new trend to mark this transition. This helps traders quickly recognize significant changes in market direction.

Visual Enhancements

The indicator enhances visual clarity by coloring the background of the chart based on the identified trend. When a bullish trend is detected, the background turns green, and when a bearish trend is identified, it turns red. The script ensures that only clear bullish and bearish trends are highlighted by excluding the "No Clear Trend" state, which reduces noise and prevents false signals.

Alerts

To further aid traders, the indicator includes alert conditions for both bullish and bearish crossovers. These alerts notify traders when a crossover occurs, enabling them to take timely action based on the identified signals.

Purpose and Unique Features

The primary purpose of the "Complex WMA Indicator with Trend Transitions" is to provide traders with a more precise and actionable analysis of market trends. Unlike simple moving average indicators, this tool uses multiple WMAs and incorporates a state machine to track and highlight trend transitions more effectively. By focusing on clear trend signals and filtering out noise, it helps traders make more informed decisions.

This indicator differs from other moving average-based tools in several ways:

Multi-WMA Analysis: It uses three WMAs of different lengths, providing a more comprehensive view of the market trend.

State Machine for Trends: The use of a state machine to track trend transitions ensures that only significant trends are highlighted, reducing noise.

Visual Clarity: The combination of colored backgrounds and labeled transitions makes it easier for traders to identify and act on trends.

Customization: Users can adjust the lengths of the WMAs to suit their trading strategies, making the indicator versatile.

In summary, the "Complex WMA Indicator with Trend Transitions" offers a sophisticated and customizable approach to trend analysis, providing clear visual cues and alerts for significant market movements, which sets it apart from simpler moving average indicators.

MathTransformLibrary "MathTransform"

Auxiliary functions for transforming data using mathematical and statistical methods

scaler_zscore(x, lookback_window)

Calculates Z-Score normalization of a series.

Parameters:

x (float) : : floating point series to normalize

lookback_window (int) : : lookback period for calculating mean and standard deviation

Returns: Z-Score normalized series

scaler_min_max(x, lookback_window, min_val, max_val, empiric_min, empiric_max, empiric_mid)

Performs Min-Max scaling of a series within a given window, user-defined bounds, and optional midpoint

Parameters:

x (float) : : floating point series to transform

lookback_window (int) : : int : optional lookback window size to consider for scaling.

min_val (float) : : float : minimum value of the scaled range. Default is 0.0.

max_val (float) : : float : maximum value of the scaled range. Default is 1.0.

empiric_min (float) : : float : user-defined minimum value of the input data. This means that the output could exceed the `min_val` bound if there is data in `x` lesser than `empiric_min`. If na, it's calculated from `x` and `lookback_window`.

empiric_max (float) : : float : user-defined maximum value of the input data. This means that the output could exceed the `max_val` bound if there is data in `x` greater than `empiric_max`. If na, it's calculated from `x` and `lookback_window`.

empiric_mid (float) : : float : user-defined midpoint value of the input data. If na, it's calculated from `empiric_min` and `empiric_max`.

Returns: rescaled series

log(x, base)

Applies logarithmic transformation to a value, base can be user-defined.

Parameters:

x (float) : : floating point value to transform

base (float) : : logarithmic base, must be greater than 0

Returns: logarithm of the value to the given base, if x <= 0, returns logarithm of 1 to the given base

exp(x, base)

Applies exponential transformation to a value, base can be user-defined.

Parameters:

x (float) : : floating point value to transform

base (float) : : base of the exponentiation, must be greater than 0

Returns: the result of raising the base to the power of the value

power(x, exponent)

Applies power transformation to a value, exponent can be user-defined.

Parameters:

x (float) : : floating point value to transform

exponent (float) : : exponent for the transformation

Returns: the value raised to the given exponent, preserving the sign of the original value

tanh(x, scale)

The hyperbolic tangent is the ratio of the hyperbolic sine and hyperbolic cosine. It limits an output to a range of −1 to 1.

Parameters:

x (float) : : floating point series

scale (float)

sigmoid(x, scale, offset)

Applies the sigmoid function to a series.

Parameters:

x (float) : : floating point series to transform

scale (float) : : scaling factor for the sigmoid function

offset (float) : : offset for the sigmoid function

Returns: transformed series using the sigmoid function

sigmoid_double(x, scale, offset)

Applies a double sigmoid function to a series, handling positive and negative values differently.

Parameters:

x (float) : : floating point series to transform

scale (float) : : scaling factor for the sigmoid function

offset (float) : : offset for the sigmoid function

Returns: transformed series using the double sigmoid function

logistic_decay(a, b, c, t)

Calculates logistic decay based on given parameters.

Parameters:

a (float) : : parameter affecting the steepness of the curve

b (float) : : parameter affecting the direction of the decay

c (float) : : the upper bound of the function's output

t (float) : : time variable

Returns: value of the logistic decay function at time t

Sharpe and Sortino Ratios█ OVERVIEW

This indicator calculates the Sharpe and Sortino ratios using a chart symbol's periodic price returns, offering insights into the symbol's risk-adjusted performance. It features the option to calculate these ratios by comparing the periodic returns to a fixed annual rate of return or the returns from another selected symbol's context.

█ CONCEPTS

Returns, risk, and volatility

The return on an investment is the relative gain or loss over a period, often expressed as a percentage. Investment returns can originate from several sources, including capital gains, dividends, and interest income. Many investors seek the highest returns possible in the quest for profit. However, prudent investing and trading entails evaluating such returns against the associated risks (i.e., the uncertainty of returns and the potential for financial losses) for a clearer perspective on overall performance and sustainability.

The profitability of an investment typically comes at the cost of enduring market swings, noise, and general uncertainty. To navigate these turbulent waters, investors and portfolio managers often utilize volatility , a measure of the statistical dispersion of historical returns, as a foundational element in their risk assessments because it provides a tangible way to gauge the uncertainty in returns. High volatility suggests increased uncertainty and, consequently, higher risk, whereas low volatility suggests more stable returns with minimal fluctuations, implying lower risk. These concepts are integral components in several risk-adjusted performance metrics, including the Sharpe and Sortino ratios calculated by this indicator.

Risk-free rate

The risk-free rate represents the rate of return on a hypothetical investment carrying no risk of financial loss. This theoretical rate provides a benchmark for comparing the returns on a risky investment and evaluating whether its excess returns justify the risks. If an investment's returns are at or below the theoretical risk-free rate or the risk premium is below a desired amount, it may suggest that the returns do not compensate for the extra risk, which might be a call to reassess the investment.

Since the risk-free rate is a theoretical concept, investors often utilize proxies for the rate in practice, such as Treasury bills and other government bonds. Conventionally, analysts consider such instruments "risk-free" for a domestic holder, as they are a form of government obligation with a low perceived likelihood of default.

The average yield on short-term Treasury bills, influenced by economic conditions, monetary policies, and inflation expectations, has historically hovered around 2-3% over the long term. This range also aligns with central banks' inflation targets. As such, one may interpret a value within this range as a minimum proxy for the risk-free rate, as it may correspond to the minimum rate required to maintain purchasing power over time. This indicator uses a default value of 2% as the risk-free rate in its Sharpe and Sortino ratio calculations. Users can adjust this value from the "Risk-free rate of return" input in the "Settings/Inputs" tab.

Sharpe and Sortino ratios

The Sharpe and Sortino ratios are two of the most widely used metrics that offer insight into an investment's risk-adjusted performance . They provide a standardized framework to compare the effectiveness of investments relative to their perceived risks. These metrics can help investors determine whether the returns justify the risks taken to achieve them, promoting more informed investment decisions.

Both metrics measure risk-adjusted performance similarly. However, they have some differences in their formulas and their interpretation:

1. Sharpe ratio

The Sharpe ratio , developed by Nobel laureate William F. Sharpe, measures the performance of an investment compared to a theoretically risk-free asset, adjusted for the investment risk. The ratio uses the following formula:

Sharpe Ratio = (𝑅𝑎 − 𝑅𝑓) / 𝜎𝑎

Where:

• 𝑅𝑎 = Average return of the investment

• 𝑅𝑓 = Theoretical risk-free rate of return

• 𝜎𝑎 = Standard deviation of the investment's returns (volatility)

A higher Sharpe ratio indicates a more favorable risk-adjusted return, as it signifies that the investment produced higher excess returns per unit of increase in total perceived risk.

2. Sortino ratio

The Sortino ratio is a modified form of the Sharpe ratio that only considers downside volatility , i.e., the volatility of returns below the theoretical risk-free benchmark. Although it shares close similarities with the Sharpe ratio, it can produce very different values, especially when the returns do not have a symmetrical distribution, since it does not penalize upside and downside volatility equally. The ratio uses the following formula:

Sortino Ratio = (𝑅𝑎 − 𝑅𝑓) / 𝜎𝑑

Where:

• 𝑅𝑎 = Average return of the investment

• 𝑅𝑓 = Theoretical risk-free rate of return

• 𝜎𝑑 = Downside deviation (standard deviation of negative excess returns, or downside volatility)

The Sortino ratio offers an alternative perspective on an investment's return-generating efficiency since it does not consider upside volatility in its calculation. A higher Sortino ratio signifies that the investment produced higher excess returns per unit of increase in perceived downside risk.

The risk-free rate (𝑅𝑓) in the numerator of both ratio formulas acts as a baseline for comparing an investment's performance to a theoretical risk-free alternative. By subtracting the risk-free rate from the expected return (𝑅𝑎−𝑅𝑓), the numerator essentially represents the risk premium of the investment.

Comparison with another symbol

In addition to the conventional Sharpe and Sortino ratios, which compare an instrument's returns to a risk-free rate, this indicator can also compare returns to a user-specified benchmark symbol , allowing the calculation of Information ratios .

An Information ratio is a generalized form of the Sharpe ratio that compares an investment's returns to a risky benchmark , such as SPY, rather than a risk-free rate. It measures the investment's active return (the difference between its returns and the benchmark returns) relative to its tracking error (i.e., the volatility of the active return) using the following formula:

𝐼𝑅 = (𝑅𝑝 − 𝑅𝑏) / 𝑇𝐸

Where:

• 𝑅𝑝 = Average return on the portfolio or investment

• 𝑅𝑏 = Average return from the benchmark instrument

• 𝑇𝐸 = Tracking error (volatility of 𝑅𝑝 − 𝑅𝑏)

Comparing returns to a benchmark instrument rather than a theoretical risk-free rate offers unique insights into risk-adjusted performance. Higher Information ratios signify that the investment produced higher active returns per unit of increase in risk relative to the benchmark. Conventional choices for non-risk-free benchmarks include major composite indices like the S&P 500 and DJIA, as the resulting ratios can provide insight into the effectiveness of an investment relative to the broader market.

Users can enable this generalized calculation for both the Sharpe and Sortino ratios by selecting the "Benchmark symbol returns" option from the "Benchmark type" dropdown in the "Settings/Inputs" tab.

It's crucial to note that this indicator compares the charts symbol's rate of change (return) to the rate of change in the benchmark symbol. Consequently, not all symbols available on TradingView are suitable for use with these ratios due to the nature of what their values represent. For instance, using a bond as a benchmark will produce distorted results since each bar's values represent yields rather than prices, meaning it compares the rate of change in the yield. To maintain consistency and relevance in the calculated ratios, ensure the values from the compared symbols strictly represent price information.

█ FEATURES

This indicator provides traders with two widely used metrics for assessing risk-adjusted performance, generalized to allow users to compare the chart symbol's price returns to a fixed risk-free rate or the returns from another risky symbol. Below are the key features of this indicator:

Timeframe selection

The "Returns timeframe" input determines the timeframe of the calculated price returns. Users can select any value greater than or equal to the chart's timeframe. The default timeframe is "1M".

Periodic returns tracking

This indicator compounds and collects requested price returns from the selected timeframe over monthly or daily periods, similar to how the Broker Emulator works when calculating strategy performance metrics on trade data. It employs the following logic:

• Track returns over monthly periods if the chart's data spans at least two months.

• Track returns over daily periods if the chart's data spans at least two days but not two months.

• Do not track or collect returns if the data spans less than two days, as the amount of data is insufficient for meaningful ratio calculations.

The indicator uses the returns collected from up to a specified number of periods to calculate the Sharpe and Sortino ratios, depending on the available historical data. It also uses these periodic returns to calculate the average returns it displays in the Data Window.

Users can control the maximum number of periods the indicator analyzes with the "Max no. of periods used" input in the "Settings/Inputs" tab. The default value is 60 periods.

Benchmark specification

The "Benchmark return type" input specifies the benchmark type the indicator compares to the chart symbol's returns in the ratio calculations. It features the following two options:

• "Risk-free rate of return (%)": Compares the price returns to a user-specified annual rate of return representing a theoretical risk-free rate (e.g., 2%).

• "Benchmark symbol return": Compares the price returns to a selected benchmark symbol (e.g., "AMEX:SPY) to calculate Information ratios.

When comparing a chart symbol's returns to a specified benchmark symbol, this indicator aligns the times of data points from the benchmark with the times of data points from the chart's symbol to facilitate a fair comparison between symbols with different active sessions.

Visualization and display

• The indicator displays the periodic returns requested from the specified "Returns timeframe" in a separate pane. The plot includes dynamic colors to signify positive and negative returns.

• When the "Returns timeframe" value represents a higher timeframe, the indicator displays background highlights on the main chart pane to signify when a new value is available and whether the return is positive or negative.

• When the specified benchmark return type is a benchmark symbol, the indicator displays the requested symbol's returns in the separate pane as a gray line for visual comparison.

• Within the separate pane, the indicator displays a single-cell table that shows the base period it uses for periodic returns, the number of periods it uses in the calculation, the timeframe of the requested data, and the calculated Sharpe and Sortino ratios.

• The Data Window displays the chart symbol and benchmark returns, their periodic averages, and the Sharpe and Sortino ratios.

█ FOR Pine Script™ CODERS

• This script utilizes the functions from our RiskMetrics library to determine the size of the periods, calculate and collect periodic returns, and compute the Sharpe and Sortino ratios.

• The `getAlignedPrices()` function in this script requests price data for the chart's symbol and a benchmark symbol with consistent time alignment by utilizing spread symbols , which helps facilitate a fair comparison between different symbol types. Retrieving prices from spreads avoids potential information loss and data misalignment that can otherwise occur when using separate requests from each symbol's context when those symbols have different sessions or data times.

• For consistency, the `getAlignedPrices()` function includes extended hours and dividend adjustment modifiers in its data requests. Additionally, it includes other settings inherited from the chart's context, such as "settlement-as-close" preferences for fair comparison between futures instruments.

• This script uses the `changePercent()` function from our ta library to calculate the percentage changes of the requested data.

• The newly released `force_overlay` parameter in display-related functions allows indicators to display visuals on the main chart and a separate pane simultaneously. We use the parameter in this script's bgcolor() call to display background highlights on the main chart.

Look first. Then leap.

RiskMetrics█ OVERVIEW

This library is a tool for Pine programmers that provides functions for calculating risk-adjusted performance metrics on periodic price returns. The calculations used by this library's functions closely mirror those the Broker Emulator uses to calculate strategy performance metrics (e.g., Sharpe and Sortino ratios) without depending on strategy-specific functionality.

█ CONCEPTS

Returns, risk, and volatility

The return on an investment is the relative gain or loss over a period, often expressed as a percentage. Investment returns can originate from several sources, including capital gains, dividends, and interest income. Many investors seek the highest returns possible in the quest for profit. However, prudent investing and trading entails evaluating such returns against the associated risks (i.e., the uncertainty of returns and the potential for financial losses) for a clearer perspective on overall performance and sustainability.

One way investors and analysts assess the risk of an investment is by analyzing its volatility , i.e., the statistical dispersion of historical returns. Investors often use volatility in risk estimation because it provides a quantifiable way to gauge the expected extent of fluctuation in returns. Elevated volatility implies heightened uncertainty in the market, which suggests higher expected risk. Conversely, low volatility implies relatively stable returns with relatively minimal fluctuations, thus suggesting lower expected risk. Several risk-adjusted performance metrics utilize volatility in their calculations for this reason.

Risk-free rate

The risk-free rate represents the rate of return on a hypothetical investment carrying no risk of financial loss. This theoretical rate provides a benchmark for comparing the returns on a risky investment and evaluating whether its excess returns justify the risks. If an investment's returns are at or below the theoretical risk-free rate or the risk premium is below a desired amount, it may suggest that the returns do not compensate for the extra risk, which might be a call to reassess the investment.

Since the risk-free rate is a theoretical concept, investors often utilize proxies for the rate in practice, such as Treasury bills and other government bonds. Conventionally, analysts consider such instruments "risk-free" for a domestic holder, as they are a form of government obligation with a low perceived likelihood of default.

The average yield on short-term Treasury bills, influenced by economic conditions, monetary policies, and inflation expectations, has historically hovered around 2-3% over the long term. This range also aligns with central banks' inflation targets. As such, one may interpret a value within this range as a minimum proxy for the risk-free rate, as it may correspond to the minimum rate required to maintain purchasing power over time.

The built-in Sharpe and Sortino ratios that strategies calculate and display in the Performance Summary tab use a default risk-free rate of 2%, and the metrics in this library's example code use the same default rate. Users can adjust this value to fit their analysis needs.

Risk-adjusted performance

Risk-adjusted performance metrics gauge the effectiveness of an investment by considering its returns relative to the perceived risk. They aim to provide a more well-rounded picture of performance by factoring in the level of risk taken to achieve returns. Investors can utilize such metrics to help determine whether the returns from an investment justify the risks and make informed decisions.

The two most commonly used risk-adjusted performance metrics are the Sharpe ratio and the Sortino ratio.

1. Sharpe ratio

The Sharpe ratio , developed by Nobel laureate William F. Sharpe, measures the performance of an investment compared to a theoretically risk-free asset, adjusted for the investment risk. The ratio uses the following formula:

Sharpe Ratio = (𝑅𝑎 − 𝑅𝑓) / 𝜎𝑎

Where:

• 𝑅𝑎 = Average return of the investment

• 𝑅𝑓 = Theoretical risk-free rate of return

• 𝜎𝑎 = Standard deviation of the investment's returns (volatility)

A higher Sharpe ratio indicates a more favorable risk-adjusted return, as it signifies that the investment produced higher excess returns per unit of increase in total perceived risk.

2. Sortino ratio

The Sortino ratio is a modified form of the Sharpe ratio that only considers downside volatility , i.e., the volatility of returns below the theoretical risk-free benchmark. Although it shares close similarities with the Sharpe ratio, it can produce very different values, especially when the returns do not have a symmetrical distribution, since it does not penalize upside and downside volatility equally. The ratio uses the following formula:

Sortino Ratio = (𝑅𝑎 − 𝑅𝑓) / 𝜎𝑑

Where:

• 𝑅𝑎 = Average return of the investment

• 𝑅𝑓 = Theoretical risk-free rate of return

• 𝜎𝑑 = Downside deviation (standard deviation of negative excess returns, or downside volatility)

The Sortino ratio offers an alternative perspective on an investment's return-generating efficiency since it does not consider upside volatility in its calculation. A higher Sortino ratio signifies that the investment produced higher excess returns per unit of increase in perceived downside risk.

█ CALCULATIONS

Return period detection

Calculating risk-adjusted performance metrics requires collecting returns across several periods of a given size. Analysts may use different period sizes based on the context and their preferences. However, two widely used standards are monthly or daily periods, depending on the available data and the investment's duration. The built-in ratios displayed in the Strategy Tester utilize returns from either monthly or daily periods in their calculations based on the following logic:

• Use monthly returns if the history of closed trades spans at least two months.

• Use daily returns if the trades span at least two days but less than two months.

• Do not calculate the ratios if the trade data spans fewer than two days.

This library's `detectPeriod()` function applies related logic to available chart data rather than trade data to determine which period is appropriate:

• It returns true if the chart's data spans at least two months, indicating that it's sufficient to use monthly periods.

• It returns false if the chart's data spans at least two days but not two months, suggesting the use of daily periods.

• It returns na if the length of the chart's data covers less than two days, signifying that the data is insufficient for meaningful ratio calculations.

It's important to note that programmers should only call `detectPeriod()` from a script's global scope or within the outermost scope of a function called from the global scope, as it requires the time value from the first bar to accurately measure the amount of time covered by the chart's data.

Collecting periodic returns

This library's `getPeriodicReturns()` function tracks price return data within monthly or daily periods and stores the periodic values in an array . It uses a `detectPeriod()` call as the condition to determine whether each element in the array represents the return over a monthly or daily period.

The `getPeriodicReturns()` function has two overloads. The first overload requires two arguments and outputs an array of monthly or daily returns for use in the `sharpe()` and `sortino()` methods. To calculate these returns:

1. The `percentChange` argument should be a series that represents percentage gains or losses. The values can be bar-to-bar return percentages on the chart timeframe or percentages requested from a higher timeframe.

2. The function compounds all non-na `percentChange` values within each monthly or daily period to calculate the period's total return percentage. When the `percentChange` represents returns from a higher timeframe, ensure the requested data includes gaps to avoid compounding redundant values.

3. After a period ends, the function queues the compounded return into the array , removing the oldest element from the array when its size exceeds the `maxPeriods` argument.

The resulting array represents the sequence of closed returns over up to `maxPeriods` months or days, depending on the available data.

The second overload of the function includes an additional `benchmark` parameter. Unlike the first overload, this version tracks and collects differences between the `percentChange` and the specified `benchmark` values. The resulting array represents the sequence of excess returns over up to `maxPeriods` months or days. Passing this array to the `sharpe()` and `sortino()` methods calculates generalized Information ratios , which represent the risk-adjustment performance of a sequence of returns compared to a risky benchmark instead of a risk-free rate. For consistency, ensure the non-na times of the `benchmark` values align with the times of the `percentChange` values.

Ratio methods

This library's `sharpe()` and `sortino()` methods respectively calculate the Sharpe and Sortino ratios based on an array of returns compared to a specified annual benchmark. Both methods adjust the annual benchmark based on the number of periods per year to suit the frequency of the returns:

• If the method call does not include a `periodsPerYear` argument, it uses `detectPeriod()` to determine whether the returns represent monthly or daily values based on the chart's history. If monthly, the method divides the `annualBenchmark` value by 12. If daily, it divides the value by 365.

• If the method call does specify a `periodsPerYear` argument, the argument's value supersedes the automatic calculation, facilitating custom benchmark adjustments, such as dividing by 252 when analyzing collected daily stock returns.

When the array passed to these methods represents a sequence of excess returns , such as the result from the second overload of `getPeriodicReturns()`, use an `annualBenchmark` value of 0 to avoid comparing those excess returns to a separate rate.

By default, these methods only calculate the ratios on the last available bar to minimize their resource usage. Users can override this behavior with the `forceCalc` parameter. When the value is true , the method calculates the ratio on each call if sufficient data is available, regardless of the bar index.

Look first. Then leap.

█ FUNCTIONS & METHODS

This library contains the following functions:

detectPeriod()

Determines whether the chart data has sufficient coverage to use monthly or daily returns

for risk metric calculations.

Returns: (bool) `true` if the period spans more than two months, `false` if it otherwise spans more

than two days, and `na` if the data is insufficient.

getPeriodicReturns(percentChange, maxPeriods)

(Overload 1 of 2) Tracks periodic return percentages and queues them into an array for ratio

calculations. The span of the chart's historical data determines whether the function uses

daily or monthly periods in its calculations. If the chart spans more than two months,

it uses "1M" periods. Otherwise, if the chart spans more than two days, it uses "1D"

periods. If the chart covers less than two days, it does not store changes.

Parameters:

percentChange (float) : (series float) The change percentage. The function compounds non-na values from each

chart bar within monthly or daily periods to calculate the periodic changes.

maxPeriods (simple int) : (simple int) The maximum number of periodic returns to store in the returned array.

Returns: (array) An array containing the overall percentage changes for each period, limited

to the maximum specified by `maxPeriods`.

getPeriodicReturns(percentChange, benchmark, maxPeriods)

(Overload 2 of 2) Tracks periodic excess return percentages and queues the values into an

array. The span of the chart's historical data determines whether the function uses

daily or monthly periods in its calculations. If the chart spans more than two months,

it uses "1M" periods. Otherwise, if the chart spans more than two days, it uses "1D"

periods. If the chart covers less than two days, it does not store changes.

Parameters:

percentChange (float) : (series float) The change percentage. The function compounds non-na values from each

chart bar within monthly or daily periods to calculate the periodic changes.

benchmark (float) : (series float) The benchmark percentage to compare against `percentChange` values.

The function compounds non-na values from each bar within monthly or

daily periods and subtracts the results from the compounded `percentChange` values to

calculate the excess returns. For consistency, ensure this series has a similar history

length to the `percentChange` with aligned non-na value times.

maxPeriods (simple int) : (simple int) The maximum number of periodic excess returns to store in the returned array.

Returns: (array) An array containing monthly or daily excess returns, limited

to the maximum specified by `maxPeriods`.

method sharpeRatio(returnsArray, annualBenchmark, forceCalc, periodsPerYear)

Calculates the Sharpe ratio for an array of periodic returns.

Callable as a method or a function.

Namespace types: array

Parameters:

returnsArray (array) : (array) An array of periodic return percentages, e.g., returns over monthly or

daily periods.

annualBenchmark (float) : (series float) The annual rate of return to compare against `returnsArray` values. When

`periodsPerYear` is `na`, the function divides this value by 12 to calculate a

monthly benchmark if the chart's data spans at least two months or 365 for a daily

benchmark if the data otherwise spans at least two days. If `periodsPerYear`

has a specified value, the function divides the rate by that value instead.

forceCalc (bool) : (series bool) If `true`, calculates the ratio on every call. Otherwise, ratio calculation

only occurs on the last available bar. Optional. The default is `false`.

periodsPerYear (simple int) : (simple int) If specified, divides the annual rate by this value instead of the value

determined by the time span of the chart's data.

Returns: (float) The Sharpe ratio, which estimates the excess return per unit of total volatility.

method sortinoRatio(returnsArray, annualBenchmark, forceCalc, periodsPerYear)

Calculates the Sortino ratio for an array of periodic returns.

Callable as a method or a function.

Namespace types: array

Parameters:

returnsArray (array) : (array) An array of periodic return percentages, e.g., returns over monthly or

daily periods.

annualBenchmark (float) : (series float) The annual rate of return to compare against `returnsArray` values. When

`periodsPerYear` is `na`, the function divides this value by 12 to calculate a

monthly benchmark if the chart's data spans at least two months or 365 for a daily

benchmark if the data otherwise spans at least two days. If `periodsPerYear`

has a specified value, the function divides the rate by that value instead.

forceCalc (bool) : (series bool) If `true`, calculates the ratio on every call. Otherwise, ratio calculation

only occurs on the last available bar. Optional. The default is `false`.

periodsPerYear (simple int) : (simple int) If specified, divides the annual rate by this value instead of the value

determined by the time span of the chart's data.

Returns: (float) The Sortino ratio, which estimates the excess return per unit of downside

volatility.

TASC 2024.07 Gaps and Extreme Closes█ OVERVIEW

This script, inspired by Perry Kaufman's article "Trading Opening Gaps and Extreme Closes in Stocks" from the TASC's July 2024 edition of Traders' Tips , provides analytical insights into stock price behaviors following significant price moves. The information about the frequency, pullbacks, and closing patterns of these extreme price movements can aid in developing more effective trading strategies by understanding what to expect during volatile market conditions.

█ CONCEPTS

Perry Kaufman's article investigates the behavior of stock prices following substantial opening gaps and extreme closing moves to identify patterns and expectations that traders can utilize to make informed decisions. The motivation behind the article is to offer traders a more scientific approach to understanding price movements during volatile market conditions, particularly during earnings season or significant economic events. Kaufman's analysis reveals that stock prices have a history of exhibiting certain behaviors after substantial price gaps and extreme closes. This script follows Perry Kaufman's study and helps provide insight into how prices often behave after significant price changes. This analysis can help traders establish price movement expectations and potential strategies for trading such occurrences.

█ CALCULATIONS

Input Parameters:

This script offers users the choice to analyze "Opening Gaps" or "Extreme Closes" for price movements of different predefined magnitudes in a specified direction ("Upward" or "Downward").

Outputs:

Based on the specified inputs, the script performs the following calculations for the active ticker displayed on the chart:

Frequency of Extreme Price Movements : Quantifies the occurrences of directional price movements within predefined percentage ranges.

Average Pullbacks : Computes the average retracement (pullback) from analyzed price movements within each percentage range.

Average Closes : Analyzes the typical closing behavior relative to the directional price movements within each range.

The script organizes the results from these calculations within the table on a separate chart pane, providing users with helpful insights into how a stock historically behaved following significant price movements.

Dickey-Fuller Test for Mean Reversion and Stationarity **IF YOU NEED EXTRA SPECIAL HELP UNDERSTANDING THIS INDICATOR, GO TO THE BOTTOM OF THE DESCRIPTION FOR AN EVEN SIMPLER DESCRIPTION**

Dickey Fuller Test:

The Dickey-Fuller test is a statistical test used to determine whether a time series is stationary or has a unit root (a characteristic of a time series that makes it non-stationary), indicating that it is non-stationary. Stationarity means that the statistical properties of a time series, such as mean and variance, are constant over time. The test checks to see if the time series is mean-reverting or not. Many traders falsely assume that raw stock prices are mean-reverting when they are not, as evidenced by many different types of statistical models that show how stock prices are almost always positively autocorrelated or statistical tests like this one, which show that stock prices are not stationary.

Note: This indicator uses past results, and the results will always be changing as new data comes in. Just because it's stationary during a rare occurrence doesn't mean it will always be stationary. Especially in price, where this would be a rare occurrence on this test. (The Test Statistic is below the critical value.)

The indicator also shows the option to either choose Raw Price, Simple Returns, or Log Returns for the test.

Raw Prices:

Stock prices are usually non-stationary because they follow some type of random walk, exhibiting positive autocorrelation and trends in the long term.

The Dickey-Fuller test on raw prices will indicate non-stationary most of the time since prices are expected to have a unit root. (If the test statistic is higher than the critical value, it suggests the presence of a unit root, confirming non-stationarity.)

Simple Returns and Log Returns:

Simple and log returns are more stationary than prices, if not completely stationary, because they measure relative changes rather than absolute levels.

This test on simple and log returns may indicate stationary behavior, especially over longer periods. (The test statistic being below the critical value suggests the absence of a unit root, indicating stationarity.)

Null Hypothesis (H0): The time series has a unit root (it is non-stationary).

Alternative Hypothesis (H1): The time series does not have a unit root (it is stationary)

Interpretation: If the test statistic is less than the critical value, we reject the null hypothesis and conclude that the time series is stationary.

Types of Dickey-Fuller Tests:

1. (What this indicator uses) Standard Dickey-Fuller Test:

Tests the null hypothesis that a unit root is present in a simple autoregressive model.

This test is used for simple cases where we just want to check if the series has a consistent statistical property over time without considering any trends or additional complexities.

It examines the relationship between the current value of the series and its previous value to see if the series tends to drift over time or revert to the mean.

2. Augmented Dickey-Fuller (ADF) Test:

Tests for a unit root while accounting for more complex structures like trends and higher-order correlations in the data.

This test is more robust and is used when the time series has trends or other patterns that need to be considered.

It extends the regular test by including additional terms to account for the complexities, and this test may be more reliable than the regular Dickey-Fuller Test.

For things like stock prices, the ADF would be more appropriate because stock prices are almost always trending and positively autocorrelated, while the Dickey-Fuller Test is more appropriate for more simple time series.

Critical Values

This indicator uses the following critical values that are essential for interpreting the Dickey-Fuller test results. The critical values depend on the chosen significance levels:

1% Significance Level: Critical value of -3.43.

5% Significance Level: Critical value of -2.86.

10% Significance Level: Critical value of -2.57.